Detailed Analysis of Contingent Liabilities in Financial Reporting

VerifiedAdded on 2019/09/24

|9

|2669

|173

Report

AI Summary

This report provides a comprehensive overview of contingent liabilities, which are potential obligations dependent on future events. It defines contingent liabilities, distinguishes them from provisions, and explores their accounting treatment. The report examines various types of contingent liabilities, including probable, possible, and remote liabilities, and provides real-world examples to illustrate each category. It also delves into the risks associated with contingent liabilities and discusses strategies for risk mitigation, such as shifting risks to private enterprises and implementing robust regulations. Furthermore, the report analyzes the optimal timing for initiating contingent liabilities, particularly during market breakdowns, and identifies the causes of market failures that necessitate government intervention. The analysis includes an examination of both explicit and implicit contingent liabilities, with a focus on government guarantees, export guarantees, and other financial guarantees. The report emphasizes the importance of accurate information, well-organized underwriting, and effective risk management to handle contingent liabilities effectively. Overall, this report offers a valuable resource for understanding the complexities of contingent liabilities and their impact on financial reporting and risk management.

What are contingent liabilities?

The initial concept of the contingent liability can be considered as the possibility of

comprising uncertain or certain risk linked with the annual record of the company. Apart

from this, it cannot be assumed from early but it is depended on future or past events.

Contingent liability is defined as the legal contract that occurs either on the non-occurrence of

the probable prospect event or based on the episode of a prospect event. It may be possible

that an organisation that do not have any further kind of controlling measures to such events

occurring in future.

Contingent liability is defined as a suitable concept that may rely on the past event. On the

other hand, it is not mandatory that the funds are prepared to be unrestricted the liabilities at

urgent situation. Apart from this, it may be probable that an appropriate budget is arranged

before the indecisive obligation.

Authentication of the Contingent liabilities

Contingent liabilities do not have any such initial scope of keeping it in record into a

monetary report for organisations. On the other words, these types of compulsion can be

occurring in the far or near in future that no effective options to focus about. Relied on certain

conditions, some of the contingent advantage will be further disclosed at the end by an

organisation. In this relation, some of the contingent advantage will be explored and will

further look like the following:

There need to be some promising commitments from the past events

The possibility of leakage of resources is not easy to achieve in nature

There should an accurate amount of necessity which is further assumed well

The initial concept of the contingent liability can be considered as the possibility of

comprising uncertain or certain risk linked with the annual record of the company. Apart

from this, it cannot be assumed from early but it is depended on future or past events.

Contingent liability is defined as the legal contract that occurs either on the non-occurrence of

the probable prospect event or based on the episode of a prospect event. It may be possible

that an organisation that do not have any further kind of controlling measures to such events

occurring in future.

Contingent liability is defined as a suitable concept that may rely on the past event. On the

other hand, it is not mandatory that the funds are prepared to be unrestricted the liabilities at

urgent situation. Apart from this, it may be probable that an appropriate budget is arranged

before the indecisive obligation.

Authentication of the Contingent liabilities

Contingent liabilities do not have any such initial scope of keeping it in record into a

monetary report for organisations. On the other words, these types of compulsion can be

occurring in the far or near in future that no effective options to focus about. Relied on certain

conditions, some of the contingent advantage will be further disclosed at the end by an

organisation. In this relation, some of the contingent advantage will be explored and will

further look like the following:

There need to be some promising commitments from the past events

The possibility of leakage of resources is not easy to achieve in nature

There should an accurate amount of necessity which is further assumed well

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Determining these above analysed certain approaches, the senior team of management of the

company should be sharing their thoughts about the decisions that whether it may be

considered as contingent liabilities or if it is defined as a major liability as its vital concern.

Taking an illustration

If an organisation serves the bank a assurance period of three major years of period, an initial

subsidiary then for the mentioned period, it is accepted as major contingent liabilities.

Furthermore in the current date, the organisation undergoes annual adversity and along with

this there is no other opportunities let for the organisation to stay, as a contingent liability. in

this relation, the organisation needs to be determining it as a major provision as well as

transfer all the further details for the recognition.

Contingent Provisions and Liability

Provision is defined as strategic responsibilities that can be assumed with the help of

applicable amounts of budget. The contingent provision tries to evaluate that there will be a

major compulsion but no individual or specific amount that can identified. Lastly, these types

of cases are further assumed as a initial provision for the liability.

Apart from this, the provision can be also kept protected in a record book which is further

reduced under an individual account of loss or profit. For instance, provision for negative

amount unpaid or the assessment is being one such incident.

Under few circumstances it is quite difficult for the organisations to capture or keep in record

the transactions related to the business due to nature of uncertainty of the transaction. These

kinds of transactions are known as contingent liability that are necessary to record but the

nature of record is not like how the provisional transactions are recorded in the books of

account. There have been few differences between provision and contingent liability.

company should be sharing their thoughts about the decisions that whether it may be

considered as contingent liabilities or if it is defined as a major liability as its vital concern.

Taking an illustration

If an organisation serves the bank a assurance period of three major years of period, an initial

subsidiary then for the mentioned period, it is accepted as major contingent liabilities.

Furthermore in the current date, the organisation undergoes annual adversity and along with

this there is no other opportunities let for the organisation to stay, as a contingent liability. in

this relation, the organisation needs to be determining it as a major provision as well as

transfer all the further details for the recognition.

Contingent Provisions and Liability

Provision is defined as strategic responsibilities that can be assumed with the help of

applicable amounts of budget. The contingent provision tries to evaluate that there will be a

major compulsion but no individual or specific amount that can identified. Lastly, these types

of cases are further assumed as a initial provision for the liability.

Apart from this, the provision can be also kept protected in a record book which is further

reduced under an individual account of loss or profit. For instance, provision for negative

amount unpaid or the assessment is being one such incident.

Under few circumstances it is quite difficult for the organisations to capture or keep in record

the transactions related to the business due to nature of uncertainty of the transaction. These

kinds of transactions are known as contingent liability that are necessary to record but the

nature of record is not like how the provisional transactions are recorded in the books of

account. There have been few differences between provision and contingent liability.

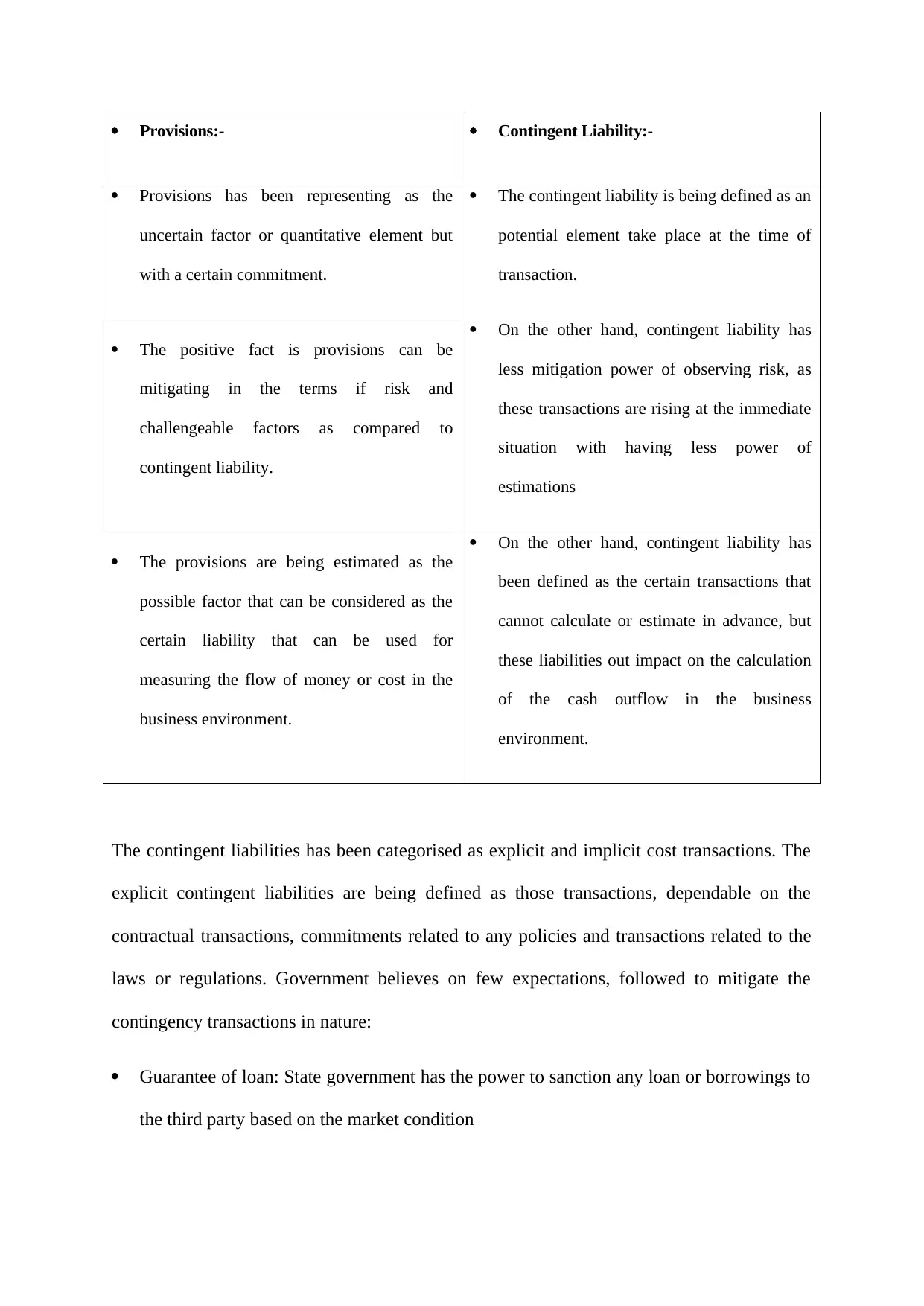

Provisions:- Contingent Liability:-

Provisions has been representing as the

uncertain factor or quantitative element but

with a certain commitment.

The contingent liability is being defined as an

potential element take place at the time of

transaction.

The positive fact is provisions can be

mitigating in the terms if risk and

challengeable factors as compared to

contingent liability.

On the other hand, contingent liability has

less mitigation power of observing risk, as

these transactions are rising at the immediate

situation with having less power of

estimations

The provisions are being estimated as the

possible factor that can be considered as the

certain liability that can be used for

measuring the flow of money or cost in the

business environment.

On the other hand, contingent liability has

been defined as the certain transactions that

cannot calculate or estimate in advance, but

these liabilities out impact on the calculation

of the cash outflow in the business

environment.

The contingent liabilities has been categorised as explicit and implicit cost transactions. The

explicit contingent liabilities are being defined as those transactions, dependable on the

contractual transactions, commitments related to any policies and transactions related to the

laws or regulations. Government believes on few expectations, followed to mitigate the

contingency transactions in nature:

Guarantee of loan: State government has the power to sanction any loan or borrowings to

the third party based on the market condition

Provisions has been representing as the

uncertain factor or quantitative element but

with a certain commitment.

The contingent liability is being defined as an

potential element take place at the time of

transaction.

The positive fact is provisions can be

mitigating in the terms if risk and

challengeable factors as compared to

contingent liability.

On the other hand, contingent liability has

less mitigation power of observing risk, as

these transactions are rising at the immediate

situation with having less power of

estimations

The provisions are being estimated as the

possible factor that can be considered as the

certain liability that can be used for

measuring the flow of money or cost in the

business environment.

On the other hand, contingent liability has

been defined as the certain transactions that

cannot calculate or estimate in advance, but

these liabilities out impact on the calculation

of the cash outflow in the business

environment.

The contingent liabilities has been categorised as explicit and implicit cost transactions. The

explicit contingent liabilities are being defined as those transactions, dependable on the

contractual transactions, commitments related to any policies and transactions related to the

laws or regulations. Government believes on few expectations, followed to mitigate the

contingency transactions in nature:

Guarantee of loan: State government has the power to sanction any loan or borrowings to

the third party based on the market condition

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Guarantee of Export: Guarantees provided to the exporter based on the agreement and the

certainty of the agreement done with the importer in the business market but the

government focused on the certainty of the two parties for final approval of the guarantee

Other financial guarantee: All kinds of financial guarantees are related to the exchange of

money in the international market. Under this factor, government also focused on the PPP

concept

Insurance: the government provides insurance facilities to the required parties under

explicit contingent liability but after analysing the situation of insurer

Apart from this, the implicit contingent liability is directly concerned to the moral obligations

related to the public interest-group. The implicit contingency liabilities are focusing on the

schemes related to the social security that are being obliged by legislative body of a nation.

The implicit contingency liability is even focused on the costs related to the future recurrent

that is reliable to calculate future cash flow in the selective market.

Category of Conditional Liabilities

A business or an organization is supported by contingent liabilities for dealing with process

of lawful matters in future with its three categories. Possibility of becoming responsible to

somebody to have the authority of anything is estimated by the probable liability. Such as, a

probable would, in fact, be conditional liability on the basis of a company who could be

waiting in order to move with the cost of finance before the estimation of the results.

There is an important feature of probable liability which is to ensure regarding the

accountability and its approximation rationally. Rebates, corporate taxes and prizes are the

examples of liability which may be computed within the budget of low cost. Additionally,

any types of products and goods have the liabilities of warranty. In such type of liability, few

certainty of the agreement done with the importer in the business market but the

government focused on the certainty of the two parties for final approval of the guarantee

Other financial guarantee: All kinds of financial guarantees are related to the exchange of

money in the international market. Under this factor, government also focused on the PPP

concept

Insurance: the government provides insurance facilities to the required parties under

explicit contingent liability but after analysing the situation of insurer

Apart from this, the implicit contingent liability is directly concerned to the moral obligations

related to the public interest-group. The implicit contingency liabilities are focusing on the

schemes related to the social security that are being obliged by legislative body of a nation.

The implicit contingency liability is even focused on the costs related to the future recurrent

that is reliable to calculate future cash flow in the selective market.

Category of Conditional Liabilities

A business or an organization is supported by contingent liabilities for dealing with process

of lawful matters in future with its three categories. Possibility of becoming responsible to

somebody to have the authority of anything is estimated by the probable liability. Such as, a

probable would, in fact, be conditional liability on the basis of a company who could be

waiting in order to move with the cost of finance before the estimation of the results.

There is an important feature of probable liability which is to ensure regarding the

accountability and its approximation rationally. Rebates, corporate taxes and prizes are the

examples of liability which may be computed within the budget of low cost. Additionally,

any types of products and goods have the liabilities of warranty. In such type of liability, few

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses arise that is induced later. So, to record the progress in future a document of

supplementary financial is observed and kept.

Taking the example of jay Company, household products have been produced by it and five

years of warranty of the quality of the goods has been given.

The next category that is the possible liability which is not needed for keeping in track the

records or registered in the format of balance sheet. It can also be said that it is very easy to

note down the possible liability in the formation of the memorandum that is readable as

testimonial of monetary.

On the basis of an example, a customer is buying a washing machine by a company and

guarantee of large scale facilities has been given, but after a year if it found that the machine

is not functioning properly and complaint is filed against the name of the brand and threats

are given legally in order to claim the total price of the product to be refund or replacement of

the machine, then there is no estimation regarding the period of time as well as the price of

the penalty that has to be paid to the consumers by the company. In accordance with the

decision that the court takes, it cannot be assured but imagined regarding the compensation of

the money or the process of the court that be initiated lawfully in further events. Rather, any

type of problems associated with possible liabilities can be planned and thought before with

assurance. Due to this, there are possibilities of possible liability of revealing in the file form

to the economic report.

The remote liability is the third liability that is without any probability or possibility. In Jay

Company case, the Company is likely to have low possibilities of losing legally if it has no

clue regarding evidence or has no value. In accordance with the generally accepted

accounting principles (GAAP), no extra entry should be placed on the balance sheet also

without any other communication verification in the declaration of monetary.

supplementary financial is observed and kept.

Taking the example of jay Company, household products have been produced by it and five

years of warranty of the quality of the goods has been given.

The next category that is the possible liability which is not needed for keeping in track the

records or registered in the format of balance sheet. It can also be said that it is very easy to

note down the possible liability in the formation of the memorandum that is readable as

testimonial of monetary.

On the basis of an example, a customer is buying a washing machine by a company and

guarantee of large scale facilities has been given, but after a year if it found that the machine

is not functioning properly and complaint is filed against the name of the brand and threats

are given legally in order to claim the total price of the product to be refund or replacement of

the machine, then there is no estimation regarding the period of time as well as the price of

the penalty that has to be paid to the consumers by the company. In accordance with the

decision that the court takes, it cannot be assured but imagined regarding the compensation of

the money or the process of the court that be initiated lawfully in further events. Rather, any

type of problems associated with possible liabilities can be planned and thought before with

assurance. Due to this, there are possibilities of possible liability of revealing in the file form

to the economic report.

The remote liability is the third liability that is without any probability or possibility. In Jay

Company case, the Company is likely to have low possibilities of losing legally if it has no

clue regarding evidence or has no value. In accordance with the generally accepted

accounting principles (GAAP), no extra entry should be placed on the balance sheet also

without any other communication verification in the declaration of monetary.

Extenuating Threats Related to Contingent Liabilities:-

The risks related to contingent liabilities are not able to consider as an acceptable choice for

the government. It can be considered that there is unanimous involvement of contingent

liabilities with different countries and its associated hazards as well. In such case, it is

essential to relate the group of conditional liability with accuracy and the purpose of selecting

that option. To safeguard the number of risks related to contingent liabilities, some activities

like shifting the risks to strong private enterprise like process of early parliamentary could be

advantageous. Besides, there would be requirements for them who strategizes and makes

decisions to identify the features of threat and to supply ample regulations to absorb it into

exercise. Apart, the requirement of support that is supposed that expects to be discovered

back in sequence after taking a satisfactory decision regarding contingent liabilities for

functioning duties and responsibilities.

In order to reduce the amount of risk, the initiative has been taken by many countries with

many schemes. Such as, development of few directions of strategies has been legally

proposed by Australia before going to an issuance where guarantees have the control and

duties depending on it as well. As to say, before entering into any type of agreement the

condition of the government is that there should any specific risk which would be seen or

well-recognized. Additionally, identification of the number of risks and also the recovery of

amount of loses has to be considered by the private agencies. Furthermore, the high security

of nation and the price threats, as well as growing money value with planning of risk

management properly bearded by the government, could be investigated.

Which is the right time to take Contingent Liabilities?

According to the opinion of the Government, when the market breaks down then it is the

perfect time to initiate contingent liabilities as per the discussion mentioned above. Regarding

The risks related to contingent liabilities are not able to consider as an acceptable choice for

the government. It can be considered that there is unanimous involvement of contingent

liabilities with different countries and its associated hazards as well. In such case, it is

essential to relate the group of conditional liability with accuracy and the purpose of selecting

that option. To safeguard the number of risks related to contingent liabilities, some activities

like shifting the risks to strong private enterprise like process of early parliamentary could be

advantageous. Besides, there would be requirements for them who strategizes and makes

decisions to identify the features of threat and to supply ample regulations to absorb it into

exercise. Apart, the requirement of support that is supposed that expects to be discovered

back in sequence after taking a satisfactory decision regarding contingent liabilities for

functioning duties and responsibilities.

In order to reduce the amount of risk, the initiative has been taken by many countries with

many schemes. Such as, development of few directions of strategies has been legally

proposed by Australia before going to an issuance where guarantees have the control and

duties depending on it as well. As to say, before entering into any type of agreement the

condition of the government is that there should any specific risk which would be seen or

well-recognized. Additionally, identification of the number of risks and also the recovery of

amount of loses has to be considered by the private agencies. Furthermore, the high security

of nation and the price threats, as well as growing money value with planning of risk

management properly bearded by the government, could be investigated.

Which is the right time to take Contingent Liabilities?

According to the opinion of the Government, when the market breaks down then it is the

perfect time to initiate contingent liabilities as per the discussion mentioned above. Regarding

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this, scarcity of ample resources for allocating that an individual achieves is the indication of

failure of the market. The reasons for generating some failure are mentioned below:-

Unsatisfactory guidelines and information:

It usually occurs at the time of high-cost work based on information in which the attraction of

the agents is to supply information that is neither complete nor accurate which creates

problems with resources distributing very unprofessionally. This means responsible

borrowers under which the market is running won’t get the admission in the credit market.

Simultaneously, few advantageous projects can also be not funded.

With the support and help of the government, the value of market can be well-developed and

grown at comparatively lower price from private markets. Also, loan could be got from the

department of payment collection and private sectors which is effective option. But, loan

provider may not supply any guarantee after obtaining the amount of loan also. So, the focus

of the government should be on becoming planned about the risk of underwriting or

accumulation of loan. Other than this, in order to deal with the information that is defective

different technical tools could also be used by the Government. This means that there is

necessity of more well-organized underwriters than loan providers for gaining information

properly regarding market.

Irregularity in providing information:

There are some that supplies irregular information while the contract is being signed, thus

this kind of symmetric information occurs. Moreover, maximum agents are not skilled in

gaining the right number of information at the time of contract. This usually occurs in the

market of insurance that deals with transacting money or in any type of material insurance.

Such as, because of flood insurance in a region lacked, during flood the crop production were

failure of the market. The reasons for generating some failure are mentioned below:-

Unsatisfactory guidelines and information:

It usually occurs at the time of high-cost work based on information in which the attraction of

the agents is to supply information that is neither complete nor accurate which creates

problems with resources distributing very unprofessionally. This means responsible

borrowers under which the market is running won’t get the admission in the credit market.

Simultaneously, few advantageous projects can also be not funded.

With the support and help of the government, the value of market can be well-developed and

grown at comparatively lower price from private markets. Also, loan could be got from the

department of payment collection and private sectors which is effective option. But, loan

provider may not supply any guarantee after obtaining the amount of loan also. So, the focus

of the government should be on becoming planned about the risk of underwriting or

accumulation of loan. Other than this, in order to deal with the information that is defective

different technical tools could also be used by the Government. This means that there is

necessity of more well-organized underwriters than loan providers for gaining information

properly regarding market.

Irregularity in providing information:

There are some that supplies irregular information while the contract is being signed, thus

this kind of symmetric information occurs. Moreover, maximum agents are not skilled in

gaining the right number of information at the time of contract. This usually occurs in the

market of insurance that deals with transacting money or in any type of material insurance.

Such as, because of flood insurance in a region lacked, during flood the crop production were

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

unable to claim any insurance from the companies. In the same way, flood badly affected the

insurance for the farming land of the farmers which the insurance company could not

recover.

The failed trial for securing the amount of insurance which has been harmed from the attack

of the terrorists on 11 September 2001 is one of the great examples of this. On the basis of

this severe event, the Government of US requested for adopting a planned resolution for

sharing large amount of economic losses associating with the industry of insurance in huge

assault cases. Therefore, two main programs are established in the industry, first is loan

guarantee for temporary airline and secondly, extensive guarantee program for SMEs during

downturn of economic that occurred in Japan. So, for reducing the risk that the Government

takes these programs could be used.

Existence of Externalities:

Externalities attempt to be dependent on some of the costs of reimbursement and social

expenditure. They are in the involvement state as they aren’t placed with the market prices.

On the basis of this concept, there is a need of applying few serious actions by the

Government that enable to challenge and sponsor such events. The guarantees of these

supports can justify it. It could be seen that maximum events are present which supplies good

promotion of progress and growth of economic. Supportive rules of EU state put such events.

It can be said that few progressive activities laid under the rules are such as, to enhance the

backward areas and encourage the SMEs. More than that, in order to employ and also save

the environment there could be sessions for training, as well as practices for developing and

research. This type of practices and events are taken that possibly gives a positive result and

damages are recovered further.

insurance for the farming land of the farmers which the insurance company could not

recover.

The failed trial for securing the amount of insurance which has been harmed from the attack

of the terrorists on 11 September 2001 is one of the great examples of this. On the basis of

this severe event, the Government of US requested for adopting a planned resolution for

sharing large amount of economic losses associating with the industry of insurance in huge

assault cases. Therefore, two main programs are established in the industry, first is loan

guarantee for temporary airline and secondly, extensive guarantee program for SMEs during

downturn of economic that occurred in Japan. So, for reducing the risk that the Government

takes these programs could be used.

Existence of Externalities:

Externalities attempt to be dependent on some of the costs of reimbursement and social

expenditure. They are in the involvement state as they aren’t placed with the market prices.

On the basis of this concept, there is a need of applying few serious actions by the

Government that enable to challenge and sponsor such events. The guarantees of these

supports can justify it. It could be seen that maximum events are present which supplies good

promotion of progress and growth of economic. Supportive rules of EU state put such events.

It can be said that few progressive activities laid under the rules are such as, to enhance the

backward areas and encourage the SMEs. More than that, in order to employ and also save

the environment there could be sessions for training, as well as practices for developing and

research. This type of practices and events are taken that possibly gives a positive result and

damages are recovered further.

It can also be observed that there could be consideration of few negative externalities like

failure in the case of the bank as well as social and lawful procedure such as guarantees of

deposits or bailouts. Moreover, there is availability of few factors affecting externally such as

disruptions of bank because of the deprivation in funds or growing debts ratio in the bank

where consumers are needed to be observed again. It is important for consumers to progress

and develop economically. Hence, the ratio of the insolvency of the bank could be reduced by

this type of guarding instrument properly.

failure in the case of the bank as well as social and lawful procedure such as guarantees of

deposits or bailouts. Moreover, there is availability of few factors affecting externally such as

disruptions of bank because of the deprivation in funds or growing debts ratio in the bank

where consumers are needed to be observed again. It is important for consumers to progress

and develop economically. Hence, the ratio of the insolvency of the bank could be reduced by

this type of guarding instrument properly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.