Analysis of Melmotte Ltd's Financial Performance and Position

VerifiedAdded on 2023/01/11

|10

|1945

|54

Report

AI Summary

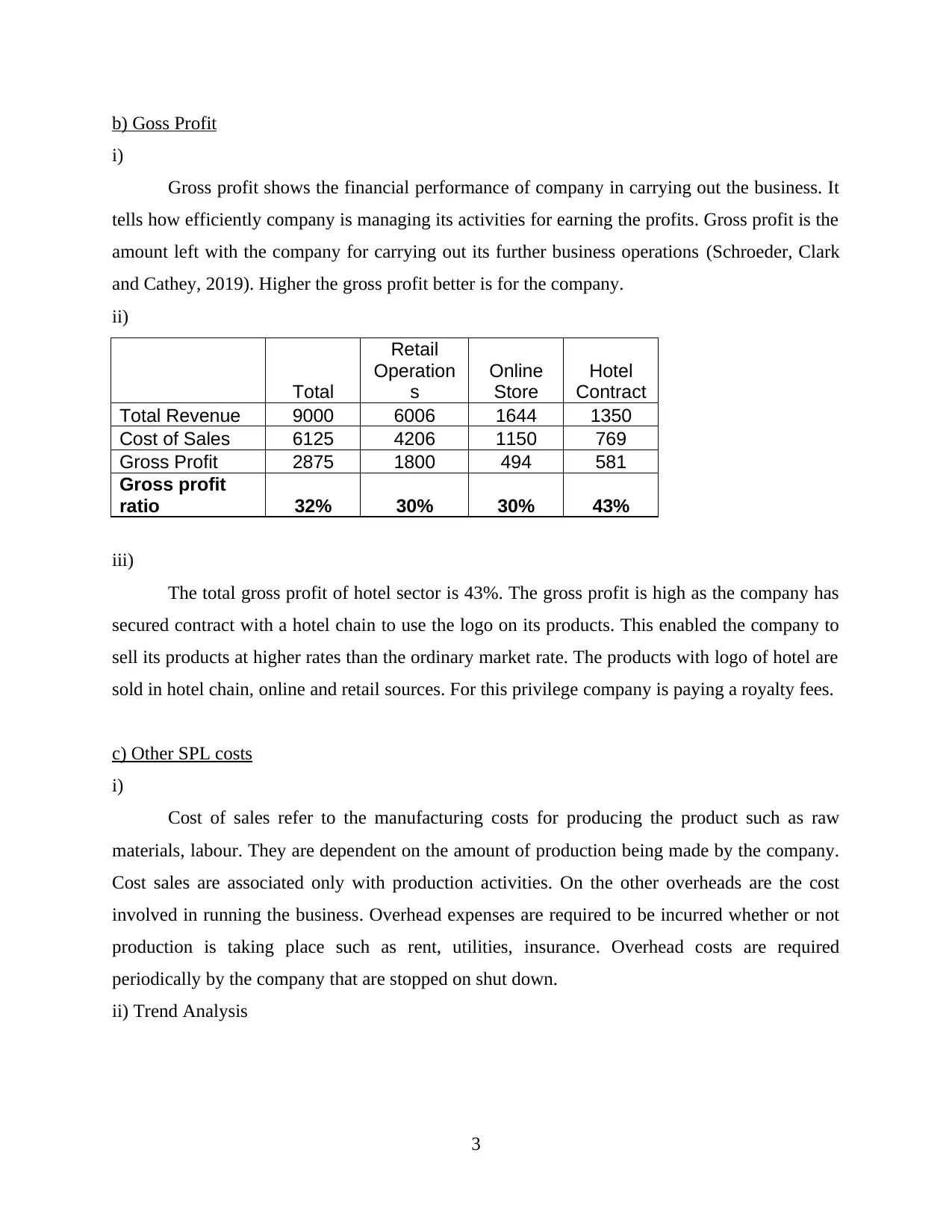

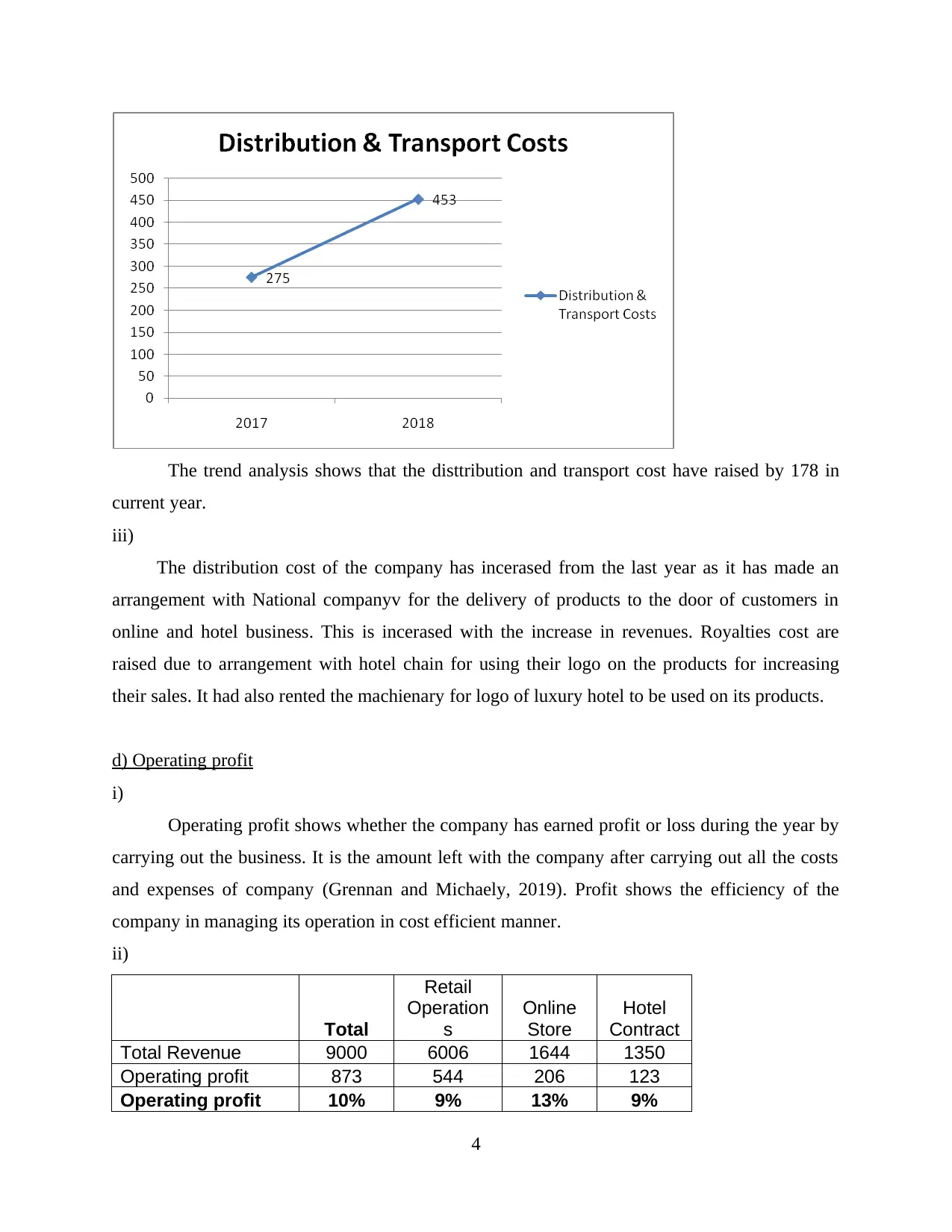

This report provides a comprehensive financial analysis of Melmotte Ltd, examining its financial performance and position. The analysis includes a review of the company's revenue, gross profit, operating profit, and cash flow statements. The report details the company's growth in revenue, highlighting the contributions of retail operations, online stores, and hotel contracts. It assesses the company's efficiency in managing costs and generating profits, examining cost of sales, overhead expenses, and operating profit margins. The report also delves into the company's assets, liabilities, and equity, including non-current assets, depreciation, and development costs. Furthermore, the report evaluates Grosvenor's proposed investment, including the impact of equity capital and the gearing ratio. The analysis identifies the reasons for net cash outflows and assesses their necessity for maintaining the company's financial health. Finally, the report provides insights into the company's financial risks and overall investment viability.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.