Analysis of Management Accounting Systems at Unicorn Ltd (2017)

VerifiedAdded on 2020/06/06

|19

|4875

|83

Report

AI Summary

This report analyzes the application of management accounting principles within Unicorn Ltd, a retail business. It begins by presenting a management accounting (MA) system, including cost accounting, price optimization, job costing, and inventory management, emphasizing their significance in enhancing profitability and decision-making. The report then explores various reporting methods, such as job costing reports, accounts receivable aging reports, and budget/performance reports, highlighting their benefits for financial planning and resource allocation. Furthermore, it delves into cost calculation using absorption and marginal costing, comparing their advantages. Finally, it examines budgetary control techniques and how Unicorn Ltd can adapt MA systems to address financial challenges, offering a comprehensive overview of financial management strategies for the company.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

P1 Presenting MA system that Unicorn can use for effective financial management.................1

P2 Explaining different methods which can be used for reporting purpose as per managerial

accounting....................................................................................................................................4

P4 Calculation of cost using absorption and marginal costing....................................................6

P4 Explaining advantages and drawbacks of different budgetary control techniques...............10

P5 Comparing how business unit adapt management accounting system for responding

financial problems......................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................................16

INTRODUCTION...........................................................................................................................1

P1 Presenting MA system that Unicorn can use for effective financial management.................1

P2 Explaining different methods which can be used for reporting purpose as per managerial

accounting....................................................................................................................................4

P4 Calculation of cost using absorption and marginal costing....................................................6

P4 Explaining advantages and drawbacks of different budgetary control techniques...............10

P5 Comparing how business unit adapt management accounting system for responding

financial problems......................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................................16

INTRODUCTION

Managerial accounting becomes vital for business units which in turn facilitates optimum use of

financial resources. In recent times, cost control is one of the main motives of firm because it is highly

associated with the enhancement of customer base and profit margin. In this regard, managerial

accounting tools as well as concepts are highly significant that assists in identifying areas of cost control

and thereby helps in improving profit margin. Thus, by considering the tools of management accounting

business unit can develop suitable and strategic framework for the near future. For this project report,

Unicorn has been selected which offers retail products or services to the customers. In this, report will

highlight the requirements as well as manner in which MA system aid in the growth and profitability

aspect of firm. Besides this, it also provides deeper insight about the reporting and planning tools on the

basis of management accounting. Further, it also shed light on the manner in which MA tools help in

responding monetary problems.

P1 Presenting MA system that Unicorn can use for effective financial management

To

Management Team

Unicorn Ltd

Date: 28th December 2017

Subject: Management accounting system

INTRODUCTION: In this, MA tools have discussed along with the reasons due to which they are

essential. Along with this, benefits and drawbacks of each system have also discussed which retail

unit needs to keep in mind while carry out business activities.

Main body

Management accounting and its significance

Management accounting (MA) is highly concerned with taking daily or short term decisions that

contributes in the firm’s profitability. It lays high level of emphasis on analyzing and communicating

internal monetary information that contributes in goal attainment (Fullerton, Kennedy and Widener,

2013). System and aspects of MA are highly significant in the following manner:

MA tools help in monitoring the performance of departments and assists in taking

action.

Further, MA makes improvement in cash flows by reducing the level of expenses.

Facilitates effective business decisions and enhances financial returns.

1 | P a g e

Managerial accounting becomes vital for business units which in turn facilitates optimum use of

financial resources. In recent times, cost control is one of the main motives of firm because it is highly

associated with the enhancement of customer base and profit margin. In this regard, managerial

accounting tools as well as concepts are highly significant that assists in identifying areas of cost control

and thereby helps in improving profit margin. Thus, by considering the tools of management accounting

business unit can develop suitable and strategic framework for the near future. For this project report,

Unicorn has been selected which offers retail products or services to the customers. In this, report will

highlight the requirements as well as manner in which MA system aid in the growth and profitability

aspect of firm. Besides this, it also provides deeper insight about the reporting and planning tools on the

basis of management accounting. Further, it also shed light on the manner in which MA tools help in

responding monetary problems.

P1 Presenting MA system that Unicorn can use for effective financial management

To

Management Team

Unicorn Ltd

Date: 28th December 2017

Subject: Management accounting system

INTRODUCTION: In this, MA tools have discussed along with the reasons due to which they are

essential. Along with this, benefits and drawbacks of each system have also discussed which retail

unit needs to keep in mind while carry out business activities.

Main body

Management accounting and its significance

Management accounting (MA) is highly concerned with taking daily or short term decisions that

contributes in the firm’s profitability. It lays high level of emphasis on analyzing and communicating

internal monetary information that contributes in goal attainment (Fullerton, Kennedy and Widener,

2013). System and aspects of MA are highly significant in the following manner:

MA tools help in monitoring the performance of departments and assists in taking

action.

Further, MA makes improvement in cash flows by reducing the level of expenses.

Facilitates effective business decisions and enhances financial returns.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

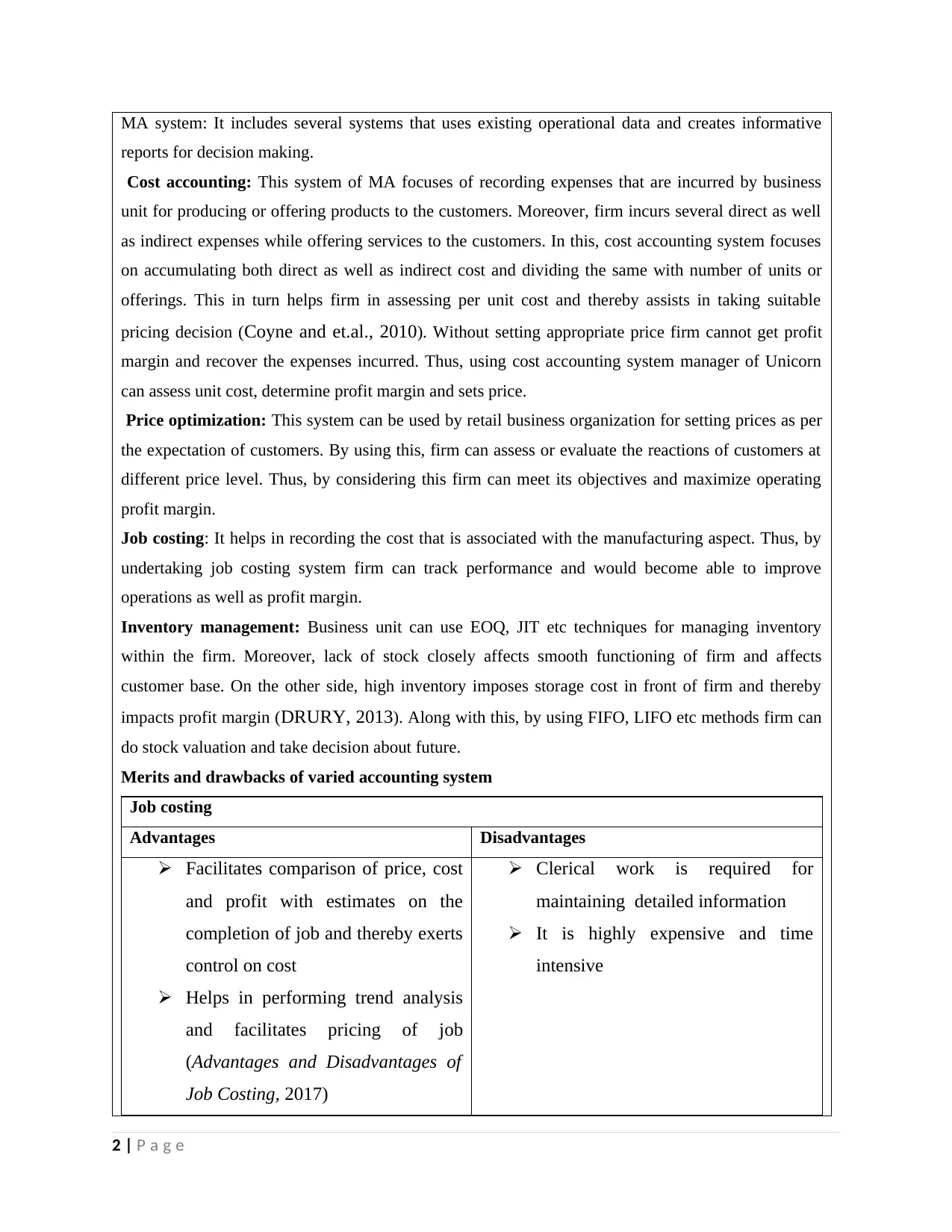

MA system: It includes several systems that uses existing operational data and creates informative

reports for decision making.

Cost accounting: This system of MA focuses of recording expenses that are incurred by business

unit for producing or offering products to the customers. Moreover, firm incurs several direct as well

as indirect expenses while offering services to the customers. In this, cost accounting system focuses

on accumulating both direct as well as indirect cost and dividing the same with number of units or

offerings. This in turn helps firm in assessing per unit cost and thereby assists in taking suitable

pricing decision (Coyne and et.al., 2010). Without setting appropriate price firm cannot get profit

margin and recover the expenses incurred. Thus, using cost accounting system manager of Unicorn

can assess unit cost, determine profit margin and sets price.

Price optimization: This system can be used by retail business organization for setting prices as per

the expectation of customers. By using this, firm can assess or evaluate the reactions of customers at

different price level. Thus, by considering this firm can meet its objectives and maximize operating

profit margin.

Job costing: It helps in recording the cost that is associated with the manufacturing aspect. Thus, by

undertaking job costing system firm can track performance and would become able to improve

operations as well as profit margin.

Inventory management: Business unit can use EOQ, JIT etc techniques for managing inventory

within the firm. Moreover, lack of stock closely affects smooth functioning of firm and affects

customer base. On the other side, high inventory imposes storage cost in front of firm and thereby

impacts profit margin (DRURY, 2013). Along with this, by using FIFO, LIFO etc methods firm can

do stock valuation and take decision about future.

Merits and drawbacks of varied accounting system

Job costing

Advantages Disadvantages

Facilitates comparison of price, cost

and profit with estimates on the

completion of job and thereby exerts

control on cost

Helps in performing trend analysis

and facilitates pricing of job

(Advantages and Disadvantages of

Job Costing, 2017)

Clerical work is required for

maintaining detailed information

It is highly expensive and time

intensive

2 | P a g e

reports for decision making.

Cost accounting: This system of MA focuses of recording expenses that are incurred by business

unit for producing or offering products to the customers. Moreover, firm incurs several direct as well

as indirect expenses while offering services to the customers. In this, cost accounting system focuses

on accumulating both direct as well as indirect cost and dividing the same with number of units or

offerings. This in turn helps firm in assessing per unit cost and thereby assists in taking suitable

pricing decision (Coyne and et.al., 2010). Without setting appropriate price firm cannot get profit

margin and recover the expenses incurred. Thus, using cost accounting system manager of Unicorn

can assess unit cost, determine profit margin and sets price.

Price optimization: This system can be used by retail business organization for setting prices as per

the expectation of customers. By using this, firm can assess or evaluate the reactions of customers at

different price level. Thus, by considering this firm can meet its objectives and maximize operating

profit margin.

Job costing: It helps in recording the cost that is associated with the manufacturing aspect. Thus, by

undertaking job costing system firm can track performance and would become able to improve

operations as well as profit margin.

Inventory management: Business unit can use EOQ, JIT etc techniques for managing inventory

within the firm. Moreover, lack of stock closely affects smooth functioning of firm and affects

customer base. On the other side, high inventory imposes storage cost in front of firm and thereby

impacts profit margin (DRURY, 2013). Along with this, by using FIFO, LIFO etc methods firm can

do stock valuation and take decision about future.

Merits and drawbacks of varied accounting system

Job costing

Advantages Disadvantages

Facilitates comparison of price, cost

and profit with estimates on the

completion of job and thereby exerts

control on cost

Helps in performing trend analysis

and facilitates pricing of job

(Advantages and Disadvantages of

Job Costing, 2017)

Clerical work is required for

maintaining detailed information

It is highly expensive and time

intensive

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

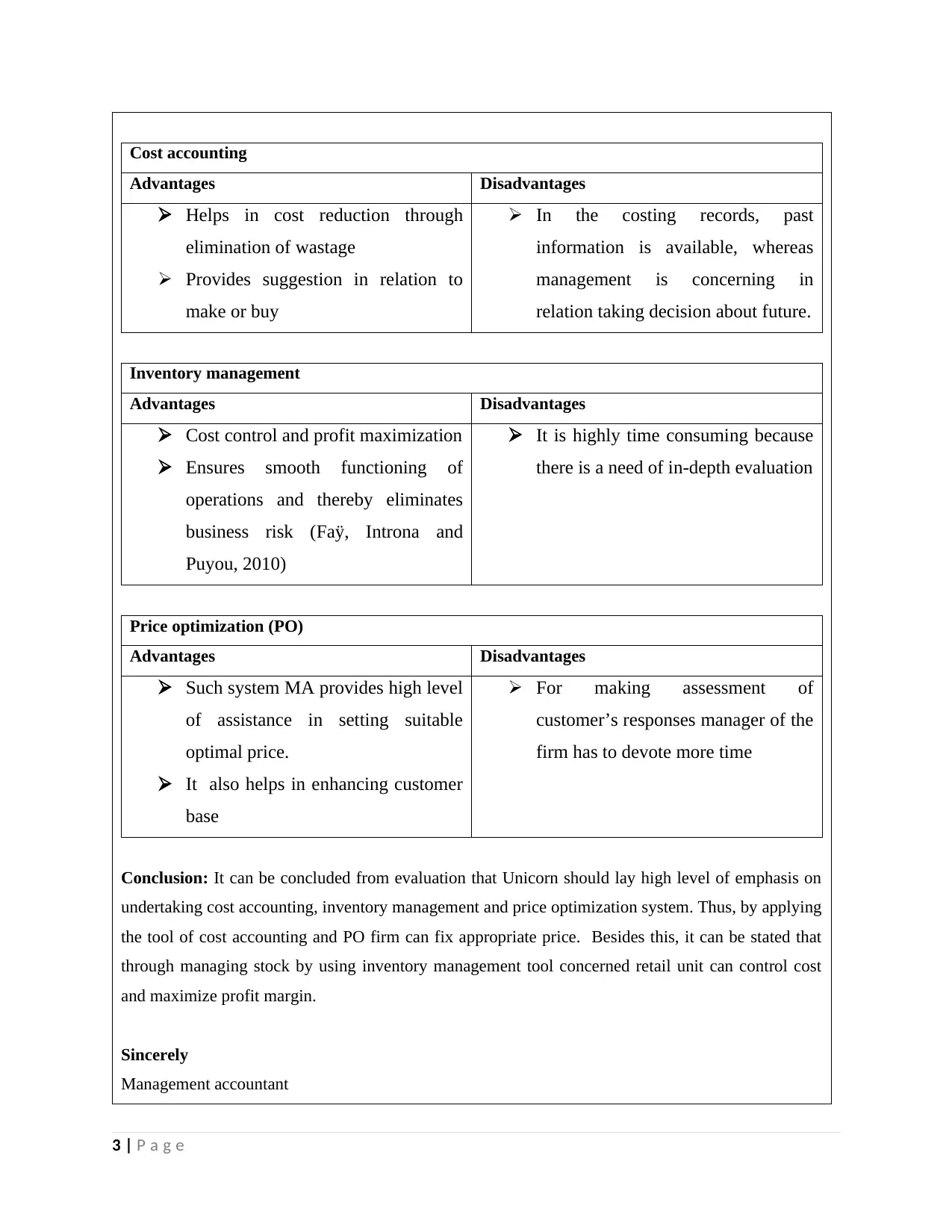

Cost accounting

Advantages Disadvantages

Helps in cost reduction through

elimination of wastage

Provides suggestion in relation to

make or buy

In the costing records, past

information is available, whereas

management is concerning in

relation taking decision about future.

Inventory management

Advantages Disadvantages

Cost control and profit maximization

Ensures smooth functioning of

operations and thereby eliminates

business risk (Faÿ, Introna and

Puyou, 2010)

It is highly time consuming because

there is a need of in-depth evaluation

Price optimization (PO)

Advantages Disadvantages

Such system MA provides high level

of assistance in setting suitable

optimal price.

It also helps in enhancing customer

base

For making assessment of

customer’s responses manager of the

firm has to devote more time

Conclusion: It can be concluded from evaluation that Unicorn should lay high level of emphasis on

undertaking cost accounting, inventory management and price optimization system. Thus, by applying

the tool of cost accounting and PO firm can fix appropriate price. Besides this, it can be stated that

through managing stock by using inventory management tool concerned retail unit can control cost

and maximize profit margin.

Sincerely

Management accountant

3 | P a g e

Advantages Disadvantages

Helps in cost reduction through

elimination of wastage

Provides suggestion in relation to

make or buy

In the costing records, past

information is available, whereas

management is concerning in

relation taking decision about future.

Inventory management

Advantages Disadvantages

Cost control and profit maximization

Ensures smooth functioning of

operations and thereby eliminates

business risk (Faÿ, Introna and

Puyou, 2010)

It is highly time consuming because

there is a need of in-depth evaluation

Price optimization (PO)

Advantages Disadvantages

Such system MA provides high level

of assistance in setting suitable

optimal price.

It also helps in enhancing customer

base

For making assessment of

customer’s responses manager of the

firm has to devote more time

Conclusion: It can be concluded from evaluation that Unicorn should lay high level of emphasis on

undertaking cost accounting, inventory management and price optimization system. Thus, by applying

the tool of cost accounting and PO firm can fix appropriate price. Besides this, it can be stated that

through managing stock by using inventory management tool concerned retail unit can control cost

and maximize profit margin.

Sincerely

Management accountant

3 | P a g e

P2 Explaining different methods which can be used for reporting purpose as per managerial

accounting

To

Management of Unicorn Ltd

Date: 28th December 2017

Subject: Managerial accounting reports

Introduction: The present report is based on various managerial reports that business unit can use to

meet informative and decision making requirements. Further, in this, application and merits of

managerial reports are also presented in the context of Unicorn retail store.

Task

Different types of managerial reports: By preparing below mentioned reports manager of Unicorn

can assess business performance more effectively. All such reports give input to the management

team of the firm and thereby aid in appropriate decisions. Thus, main reports that can be prepared by

Unicorn for developing competent framework are enumerated below:

Job costing report: It clearly depicts expenses that are associated with specific

project. In addition to this, revenue is also matched or compared with estimated

revenue with the motive to evaluate job’s profitability. This in turn helps firm in

assessing high earning areas instead of wasting time on low performing projects

(Fullerton, Kennedy and Widener, 2013). Thus, considering such aspect it can be

stated that job cost report helps firm in making efforts and allocating resources to

highly profitable projects. Besides this, projects which are in progress, manager of the

retail unit can take suitable decision before cost or expenditure level exceeds budget.

Accounts receivable aging report: Effective cash flow management is highly required

within the firm for carry out business activities in the best possible way. In this,

accounts receivable aging report assists management team of retail unit in taking

pertaining to credit extension to its customers. In other words, it can be depicted that

such report helps in assessing the debtors who are making payment within 30, 60 and

90 days in a separate columns. Thus, such separate invoice column helps business

organization in identifying the problems take place in the collection process. On the

4 | P a g e

accounting

To

Management of Unicorn Ltd

Date: 28th December 2017

Subject: Managerial accounting reports

Introduction: The present report is based on various managerial reports that business unit can use to

meet informative and decision making requirements. Further, in this, application and merits of

managerial reports are also presented in the context of Unicorn retail store.

Task

Different types of managerial reports: By preparing below mentioned reports manager of Unicorn

can assess business performance more effectively. All such reports give input to the management

team of the firm and thereby aid in appropriate decisions. Thus, main reports that can be prepared by

Unicorn for developing competent framework are enumerated below:

Job costing report: It clearly depicts expenses that are associated with specific

project. In addition to this, revenue is also matched or compared with estimated

revenue with the motive to evaluate job’s profitability. This in turn helps firm in

assessing high earning areas instead of wasting time on low performing projects

(Fullerton, Kennedy and Widener, 2013). Thus, considering such aspect it can be

stated that job cost report helps firm in making efforts and allocating resources to

highly profitable projects. Besides this, projects which are in progress, manager of the

retail unit can take suitable decision before cost or expenditure level exceeds budget.

Accounts receivable aging report: Effective cash flow management is highly required

within the firm for carry out business activities in the best possible way. In this,

accounts receivable aging report assists management team of retail unit in taking

pertaining to credit extension to its customers. In other words, it can be depicted that

such report helps in assessing the debtors who are making payment within 30, 60 and

90 days in a separate columns. Thus, such separate invoice column helps business

organization in identifying the problems take place in the collection process. On the

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

basis of such aspect, corporation can tighten its credit policies pertaining to the

customers who are unable to make payment. Thus, by doing analysis and evaluation

of accounts receivable aging on periodical basis company can reduce or avoid the

level of debt to a great extent.

Budget or performance report: In the current time frames, managers prepare and use

budget in relation to comparing actual expenditure with predetermined standards.

Thus, performance report contains information about the differences which take place

between actual and budgeted expenses. It also furnishes information about the reasons

due to which deviations are occurred. In this, by considering the causes business unit

can take appropriate action within the suitable time frame (Types of Managerial

Accounting Reports, 2017). Along with this, through using such report and

considering deviations owner of retail unit can develop competent financial plan or

budgeting framework.

Inventory and manufacturing report: Prominent stock management is needed, in the

context of retail unit, because it has direct influence on cost level. Ordering and

holding are the main cost which are highly associated with stock and have an impact

on profit margin. In this regard, by using inventory and manufacturing report firm can

make its manufacturing process more efficient (Ionescu, 2016). Thus, through

undertaking such report manager of the firm can assess wastage level, labour and

overhead cost. In this way, by assessing deviations firm would become able to take

strategic measure for improvements.

Merit and importance of management accounting reports: By using managerial reports retail firm

can get most valuable information and thereby become able to take appropriate decision that make

contribution in the attainment of organizational goals. Thus, main benefits which managerial

accounting reports offer are enumerated below:

Facilitates optimum allocation of resources in different projects

Helps in doing make or buy analysis

Assists in performing relevant cost analysis and profit planning

Provides input for developing suitable budget for upcoming period and helps in

framing competent strategies as well as policy for performance improvement.

Application: From assessment, it has found that budget, accounts receivable aging and inventory &

manufacturing reports are highly suitable or appropriate in the context of Unicorn. Moreover, for

5 | P a g e

customers who are unable to make payment. Thus, by doing analysis and evaluation

of accounts receivable aging on periodical basis company can reduce or avoid the

level of debt to a great extent.

Budget or performance report: In the current time frames, managers prepare and use

budget in relation to comparing actual expenditure with predetermined standards.

Thus, performance report contains information about the differences which take place

between actual and budgeted expenses. It also furnishes information about the reasons

due to which deviations are occurred. In this, by considering the causes business unit

can take appropriate action within the suitable time frame (Types of Managerial

Accounting Reports, 2017). Along with this, through using such report and

considering deviations owner of retail unit can develop competent financial plan or

budgeting framework.

Inventory and manufacturing report: Prominent stock management is needed, in the

context of retail unit, because it has direct influence on cost level. Ordering and

holding are the main cost which are highly associated with stock and have an impact

on profit margin. In this regard, by using inventory and manufacturing report firm can

make its manufacturing process more efficient (Ionescu, 2016). Thus, through

undertaking such report manager of the firm can assess wastage level, labour and

overhead cost. In this way, by assessing deviations firm would become able to take

strategic measure for improvements.

Merit and importance of management accounting reports: By using managerial reports retail firm

can get most valuable information and thereby become able to take appropriate decision that make

contribution in the attainment of organizational goals. Thus, main benefits which managerial

accounting reports offer are enumerated below:

Facilitates optimum allocation of resources in different projects

Helps in doing make or buy analysis

Assists in performing relevant cost analysis and profit planning

Provides input for developing suitable budget for upcoming period and helps in

framing competent strategies as well as policy for performance improvement.

Application: From assessment, it has found that budget, accounts receivable aging and inventory &

manufacturing reports are highly suitable or appropriate in the context of Unicorn. Moreover, for

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making effective use of financial resources retail unit lays emphasis on the preparation of budget. In

this, by doing comparison of actual income and expenses with budgeted figures business organization

can identify the need for improvements. In addition to this, accounts receivable report also helps firm

in assessing whether there is need to tighten the credit policies or not. In addition to this, through

preparing and using stock report company can assess the extent to wastage of both raw and finished

products take place within the firm. Thus, by making evaluation of all such aspects firm can take

action for improvements and thereby enhance profit margin.

Conclusion: It can be summarized from overall assessment that managerial reports serve suitable

information for decision making. Thus, by framing and undertaking all the above depicted reports

firm can make suitable plan for the near time period.

Sincerely

Management accountant

P4 Calculation of cost using absorption and marginal costing

Cost accounting is a specific branch of accounting that key target is to capture company’s

production cost by adding together the cost of input. It includes cost determination and its

thorough analysis helps managerial team in assessing cost behavior, variance analysis and

analyzing cost-volume-profit relationship (Quattrone, 2016). Such analysis aids in better

planning and controlling decisions for Unicorn Ltd. There are two methods used for the purpose

of cost measurement; marginal and absorption which are enumerated underneath:

Marginal costing: Marginal production cost of an item can be found just by adding

together all the variable overheads. With the increase in production and sales volume variable

costs also reflect proportionate changes. In contrast, fixed cost that remain constant or unchanged

is regardless of both output and sales volume. It is a principal techniques used in cost accounting

and aids in successful decisions because it enable Unicorn’s managers to focus on the changing

cost elements like material, labor and other variable costs i.e. manufacturing overheads, sales

cost and others (Hoare, 2015). According to the method, contribution can be compute through

subtracting variable cost from the sales. It is extremely useful for the managers because it gives

an idea to them about how much capital is available in order to pay fixed overheads.

6 | P a g e

this, by doing comparison of actual income and expenses with budgeted figures business organization

can identify the need for improvements. In addition to this, accounts receivable report also helps firm

in assessing whether there is need to tighten the credit policies or not. In addition to this, through

preparing and using stock report company can assess the extent to wastage of both raw and finished

products take place within the firm. Thus, by making evaluation of all such aspects firm can take

action for improvements and thereby enhance profit margin.

Conclusion: It can be summarized from overall assessment that managerial reports serve suitable

information for decision making. Thus, by framing and undertaking all the above depicted reports

firm can make suitable plan for the near time period.

Sincerely

Management accountant

P4 Calculation of cost using absorption and marginal costing

Cost accounting is a specific branch of accounting that key target is to capture company’s

production cost by adding together the cost of input. It includes cost determination and its

thorough analysis helps managerial team in assessing cost behavior, variance analysis and

analyzing cost-volume-profit relationship (Quattrone, 2016). Such analysis aids in better

planning and controlling decisions for Unicorn Ltd. There are two methods used for the purpose

of cost measurement; marginal and absorption which are enumerated underneath:

Marginal costing: Marginal production cost of an item can be found just by adding

together all the variable overheads. With the increase in production and sales volume variable

costs also reflect proportionate changes. In contrast, fixed cost that remain constant or unchanged

is regardless of both output and sales volume. It is a principal techniques used in cost accounting

and aids in successful decisions because it enable Unicorn’s managers to focus on the changing

cost elements like material, labor and other variable costs i.e. manufacturing overheads, sales

cost and others (Hoare, 2015). According to the method, contribution can be compute through

subtracting variable cost from the sales. It is extremely useful for the managers because it gives

an idea to them about how much capital is available in order to pay fixed overheads.

6 | P a g e

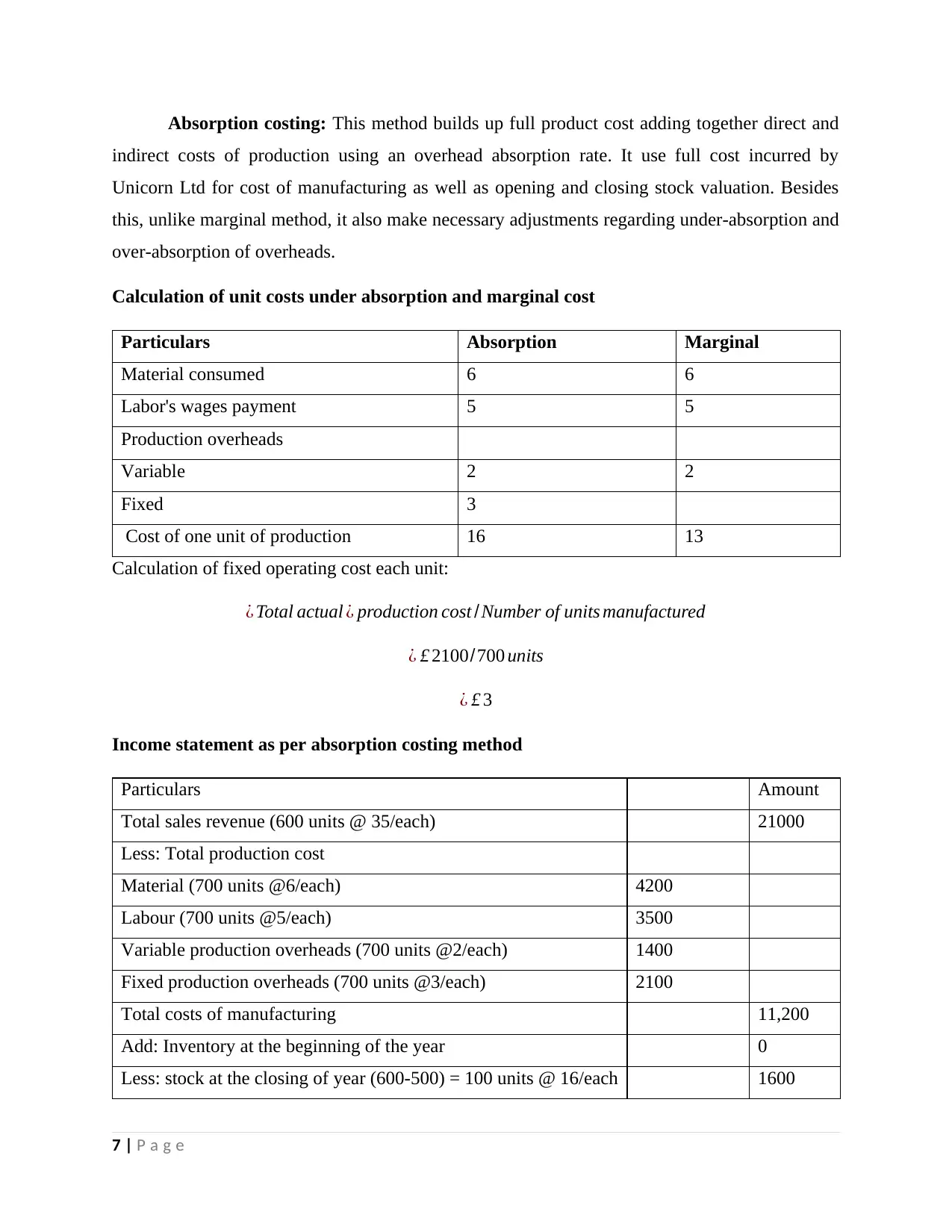

Absorption costing: This method builds up full product cost adding together direct and

indirect costs of production using an overhead absorption rate. It use full cost incurred by

Unicorn Ltd for cost of manufacturing as well as opening and closing stock valuation. Besides

this, unlike marginal method, it also make necessary adjustments regarding under-absorption and

over-absorption of overheads.

Calculation of unit costs under absorption and marginal cost

Particulars Absorption Marginal

Material consumed 6 6

Labor's wages payment 5 5

Production overheads

Variable 2 2

Fixed 3

Cost of one unit of production 16 13

Calculation of fixed operating cost each unit:

¿ Total actual ¿ production cost /Number of units manufactured

¿ £ 2100/700 units

¿ £ 3

Income statement as per absorption costing method

Particulars Amount

Total sales revenue (600 units @ 35/each) 21000

Less: Total production cost

Material (700 units @6/each) 4200

Labour (700 units @5/each) 3500

Variable production overheads (700 units @2/each) 1400

Fixed production overheads (700 units @3/each) 2100

Total costs of manufacturing 11,200

Add: Inventory at the beginning of the year 0

Less: stock at the closing of year (600-500) = 100 units @ 16/each 1600

7 | P a g e

indirect costs of production using an overhead absorption rate. It use full cost incurred by

Unicorn Ltd for cost of manufacturing as well as opening and closing stock valuation. Besides

this, unlike marginal method, it also make necessary adjustments regarding under-absorption and

over-absorption of overheads.

Calculation of unit costs under absorption and marginal cost

Particulars Absorption Marginal

Material consumed 6 6

Labor's wages payment 5 5

Production overheads

Variable 2 2

Fixed 3

Cost of one unit of production 16 13

Calculation of fixed operating cost each unit:

¿ Total actual ¿ production cost /Number of units manufactured

¿ £ 2100/700 units

¿ £ 3

Income statement as per absorption costing method

Particulars Amount

Total sales revenue (600 units @ 35/each) 21000

Less: Total production cost

Material (700 units @6/each) 4200

Labour (700 units @5/each) 3500

Variable production overheads (700 units @2/each) 1400

Fixed production overheads (700 units @3/each) 2100

Total costs of manufacturing 11,200

Add: Inventory at the beginning of the year 0

Less: stock at the closing of year (600-500) = 100 units @ 16/each 1600

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

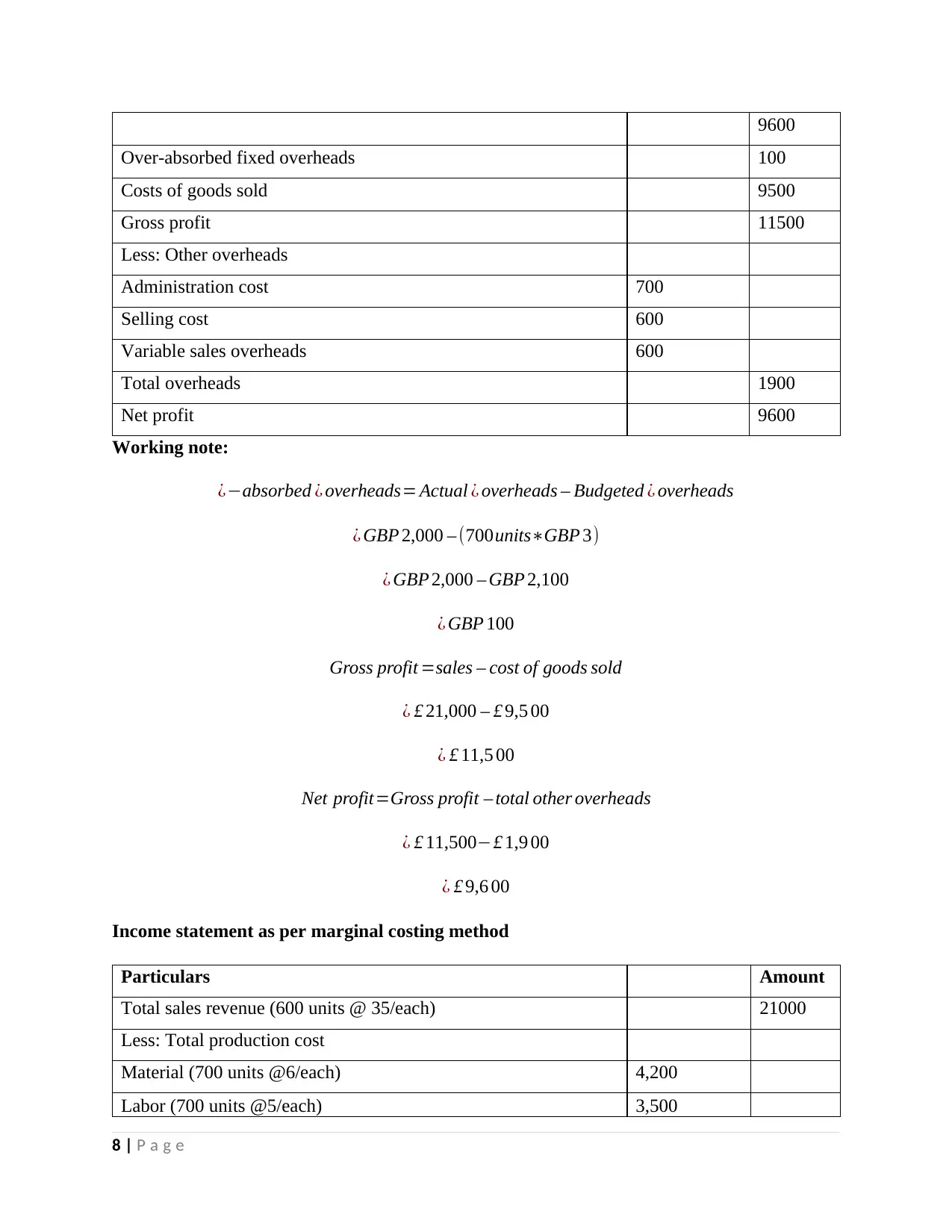

9600

Over-absorbed fixed overheads 100

Costs of goods sold 9500

Gross profit 11500

Less: Other overheads

Administration cost 700

Selling cost 600

Variable sales overheads 600

Total overheads 1900

Net profit 9600

Working note:

¿−absorbed ¿ overheads= Actual ¿ overheads – Budgeted ¿ overheads

¿ GBP 2,000 – (700units∗GBP 3)

¿ GBP 2,000 – GBP 2,100

¿ GBP 100

Gross profit =sales – cost of goods sold

¿ £ 21,000 – £ 9,5 00

¿ £ 11,5 00

Net profit=Gross profit – total other overheads

¿ £ 11,500−£ 1,9 00

¿ £ 9,6 00

Income statement as per marginal costing method

Particulars Amount

Total sales revenue (600 units @ 35/each) 21000

Less: Total production cost

Material (700 units @6/each) 4,200

Labor (700 units @5/each) 3,500

8 | P a g e

Over-absorbed fixed overheads 100

Costs of goods sold 9500

Gross profit 11500

Less: Other overheads

Administration cost 700

Selling cost 600

Variable sales overheads 600

Total overheads 1900

Net profit 9600

Working note:

¿−absorbed ¿ overheads= Actual ¿ overheads – Budgeted ¿ overheads

¿ GBP 2,000 – (700units∗GBP 3)

¿ GBP 2,000 – GBP 2,100

¿ GBP 100

Gross profit =sales – cost of goods sold

¿ £ 21,000 – £ 9,5 00

¿ £ 11,5 00

Net profit=Gross profit – total other overheads

¿ £ 11,500−£ 1,9 00

¿ £ 9,6 00

Income statement as per marginal costing method

Particulars Amount

Total sales revenue (600 units @ 35/each) 21000

Less: Total production cost

Material (700 units @6/each) 4,200

Labor (700 units @5/each) 3,500

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

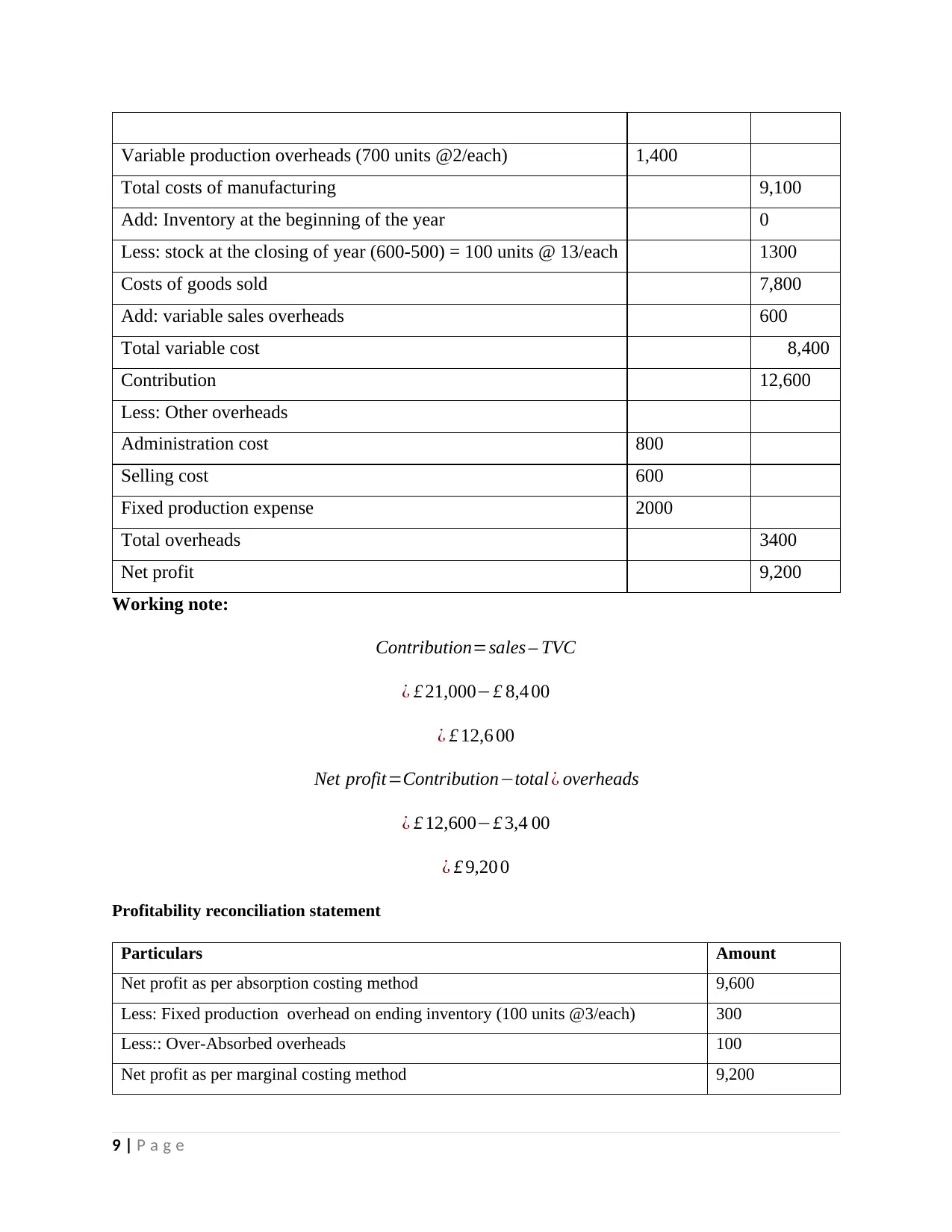

Variable production overheads (700 units @2/each) 1,400

Total costs of manufacturing 9,100

Add: Inventory at the beginning of the year 0

Less: stock at the closing of year (600-500) = 100 units @ 13/each 1300

Costs of goods sold 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution 12,600

Less: Other overheads

Administration cost 800

Selling cost 600

Fixed production expense 2000

Total overheads 3400

Net profit 9,200

Working note:

Contribution=sales – TVC

¿ £ 21,000−£ 8,4 00

¿ £ 12,6 00

Net profit=Contribution−total ¿ overheads

¿ £ 12,600−£ 3,4 00

¿ £ 9,20 0

Profitability reconciliation statement

Particulars Amount

Net profit as per absorption costing method 9,600

Less: Fixed production overhead on ending inventory (100 units @3/each) 300

Less:: Over-Absorbed overheads 100

Net profit as per marginal costing method 9,200

9 | P a g e

Total costs of manufacturing 9,100

Add: Inventory at the beginning of the year 0

Less: stock at the closing of year (600-500) = 100 units @ 13/each 1300

Costs of goods sold 7,800

Add: variable sales overheads 600

Total variable cost 8,400

Contribution 12,600

Less: Other overheads

Administration cost 800

Selling cost 600

Fixed production expense 2000

Total overheads 3400

Net profit 9,200

Working note:

Contribution=sales – TVC

¿ £ 21,000−£ 8,4 00

¿ £ 12,6 00

Net profit=Contribution−total ¿ overheads

¿ £ 12,600−£ 3,4 00

¿ £ 9,20 0

Profitability reconciliation statement

Particulars Amount

Net profit as per absorption costing method 9,600

Less: Fixed production overhead on ending inventory (100 units @3/each) 300

Less:: Over-Absorbed overheads 100

Net profit as per marginal costing method 9,200

9 | P a g e

Interpretation: The findings determined that per unit cost under marginal and absorption costing

method is found to £13 and £16 each unit due to exclusion of fixed manufacturing overheads incurred @

£3/unit in first method. As a result, production cost significantly reported different results to £9,100 and

£11,200 in variable and full method of costing. This is the reason, why later method valued stock at

higher cost of £1,600. Gross profit is derived to £11,500 whilst contribution is comparatively higher to

£12,600 due to excluded fixed manufacturing cost while variable sales overheads has been included to

derive TVC. Net profit under absorption cost found to £9,600 and as per reconciliation statement, if it is

subtracted by fixed cost on closing stock worth £300 and over-absorbed fixed overheads of £400, then net

profit under full costing can be derived to £9,200.

P4 Explaining advantages and drawbacks of different budgetary control techniques

Budgetary control is a system of comparing budgeted figures with the actual results to

find out discrepancies with the view to take remedial actions at a right time. The process of

budgetary control includes budget formulation, maintaining coordination, assigning

responsibilities, comparing actual and expected results and corrective action to achieve desired

profit targets (Zimmerman and Yahya-Zadeh, 2011).

Incremental budgeting: As name suggests, it is a method wherein budget is prepared

using either the actual performance or budget of preceding period with some incremental

charges. It assigns resources considering previous allocation and believes in encouraging

spending up (Quattrone, 2016).

Advantages:

Stable and gradual changes only

Consistency in departmental operations

Simple to operate and preparation is easy

Avoid conflicts among Unicorn’s all the departments

Useful to maintain strong coordination

Drawbacks:

It believes in similar working method over the period not found appropriate, however, in

modern era, it does not look appropriate.

No incentive and reward is available to bring new and interesting thoughts for cost-

cutting.

Always boost spending

10 | P a g e

method is found to £13 and £16 each unit due to exclusion of fixed manufacturing overheads incurred @

£3/unit in first method. As a result, production cost significantly reported different results to £9,100 and

£11,200 in variable and full method of costing. This is the reason, why later method valued stock at

higher cost of £1,600. Gross profit is derived to £11,500 whilst contribution is comparatively higher to

£12,600 due to excluded fixed manufacturing cost while variable sales overheads has been included to

derive TVC. Net profit under absorption cost found to £9,600 and as per reconciliation statement, if it is

subtracted by fixed cost on closing stock worth £300 and over-absorbed fixed overheads of £400, then net

profit under full costing can be derived to £9,200.

P4 Explaining advantages and drawbacks of different budgetary control techniques

Budgetary control is a system of comparing budgeted figures with the actual results to

find out discrepancies with the view to take remedial actions at a right time. The process of

budgetary control includes budget formulation, maintaining coordination, assigning

responsibilities, comparing actual and expected results and corrective action to achieve desired

profit targets (Zimmerman and Yahya-Zadeh, 2011).

Incremental budgeting: As name suggests, it is a method wherein budget is prepared

using either the actual performance or budget of preceding period with some incremental

charges. It assigns resources considering previous allocation and believes in encouraging

spending up (Quattrone, 2016).

Advantages:

Stable and gradual changes only

Consistency in departmental operations

Simple to operate and preparation is easy

Avoid conflicts among Unicorn’s all the departments

Useful to maintain strong coordination

Drawbacks:

It believes in similar working method over the period not found appropriate, however, in

modern era, it does not look appropriate.

No incentive and reward is available to bring new and interesting thoughts for cost-

cutting.

Always boost spending

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.