Management Accounting Report: Financial Analysis for Unicorn Groceries

VerifiedAdded on 2021/02/20

|23

|5819

|172

Report

AI Summary

This report provides a detailed analysis of management accounting systems and their application within Unicorn Groceries, a business that offers a wide range of groceries to its customers. The report begins by explaining the essential requirements of management accounting systems, including job costing, expenditure accounting, inventory systems, and price optimization. It then presents various methods for management accounting reporting, such as budget reports, job cost reports, accounts receivable aging, and inventory reports. Furthermore, the report delves into the calculation of costs using both absorption and marginal costing systems, providing detailed profit and loss statements and a reconciliation of profit figures. The report also explores the advantages and disadvantages of different planning tools used for budgetary control. Finally, it examines how Unicorn Groceries utilizes management accounting systems to address financial challenges, making it a comprehensive resource for understanding and applying management accounting principles in a real-world business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

P 1 Explaining and evaluating management accounting systems and its essential requirements

within business............................................................................................................................3

P 2 Presenting different methods which can be used for management accounting reporting ....5

P 3 Calculating cost using absorption and marginal costing system ..........................................6

P 4 Explaining advantages and disadvantages of different types of planning tools which can

be used for budgetary control....................................................................................................10

P 5 Comparing ways in which organization is using management accounting system for

dealing with financial problems................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

P 1 Explaining and evaluating management accounting systems and its essential requirements

within business............................................................................................................................3

P 2 Presenting different methods which can be used for management accounting reporting ....5

P 3 Calculating cost using absorption and marginal costing system ..........................................6

P 4 Explaining advantages and disadvantages of different types of planning tools which can

be used for budgetary control....................................................................................................10

P 5 Comparing ways in which organization is using management accounting system for

dealing with financial problems................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting may be served as a process which in turn plays emphasis on

preparing managerial reports that aid in short term decision making. In the recent times, fore

taking profitable business decisions companies make focus on the adoption of management

accounting tools and techniques. The present report is based on Unicorn which provides

customers with wide range of choices in groceries. In this, the present report will provide deeper

insight about the requirements of management accounting tools in the context of business

organization. Along with this, it also depicts how managerial report helps in developing

competent and strategic policy framework for the near future. This report will also shed light on

the appropriateness of costing system which can be used for cost and profit assessment. In

addition to this, planning tools which can be used by Unicorn for better financial decisions will

also be discussed. Further, report also entails MA techniques which assist in responding

monetary problems effectually.

P 1 Explaining and evaluating management accounting systems and its essential requirements

within business

Management accounting is the process of identification, measurement, analysis,

interpretation and communication pertaining to information which manager undertakes for the

pursuit of an organizational goals (Management Accounting, 2019). With regards to Unicorn,

management accounting is highly significant which helps manager in making profitable

decisions. By using management accounting system business unit can manage its operations

more effectually and thereby enhances profitability aspect.

Job costing

In Unicorn, Operation costing means collecting all the cost such as material, labour and

specific overheads related to the one operation.

Advantages Disadvantages

Assists in determining profitability

aspect of each task

Offers basis for estimating cost of

similar jobs

Provides with detailed assessment

regarding material, labour and overhead

Needs more clerical work

Lack of operation standardization

under this costing system

Highly expensive over others

Management accounting may be served as a process which in turn plays emphasis on

preparing managerial reports that aid in short term decision making. In the recent times, fore

taking profitable business decisions companies make focus on the adoption of management

accounting tools and techniques. The present report is based on Unicorn which provides

customers with wide range of choices in groceries. In this, the present report will provide deeper

insight about the requirements of management accounting tools in the context of business

organization. Along with this, it also depicts how managerial report helps in developing

competent and strategic policy framework for the near future. This report will also shed light on

the appropriateness of costing system which can be used for cost and profit assessment. In

addition to this, planning tools which can be used by Unicorn for better financial decisions will

also be discussed. Further, report also entails MA techniques which assist in responding

monetary problems effectually.

P 1 Explaining and evaluating management accounting systems and its essential requirements

within business

Management accounting is the process of identification, measurement, analysis,

interpretation and communication pertaining to information which manager undertakes for the

pursuit of an organizational goals (Management Accounting, 2019). With regards to Unicorn,

management accounting is highly significant which helps manager in making profitable

decisions. By using management accounting system business unit can manage its operations

more effectually and thereby enhances profitability aspect.

Job costing

In Unicorn, Operation costing means collecting all the cost such as material, labour and

specific overheads related to the one operation.

Advantages Disadvantages

Assists in determining profitability

aspect of each task

Offers basis for estimating cost of

similar jobs

Provides with detailed assessment

regarding material, labour and overhead

Needs more clerical work

Lack of operation standardization

under this costing system

Highly expensive over others

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost

Expenditure accounting

Each business unit produces and sells product with the motive to generate high profit

margin. In this, it is required for the company to make assessment of per unit expenditure.

Hence, by assessing direct and indirect expenses associated with product Unicorn can determine

per unit cost. By dividing total cost from number of units produced cost per unit can be

calculated (Chenhall and Moers, 2015). Hence, by adding profit margin into per unit

consumption price can be calculated by Unicorn.

Advantages Disadvantages

Helps in controlling financial

performance as it gives input for

standard costing

Facilitates ascertainment of unit

production cost

Helps in setting prices of the products

or services

Complex in nature

Expensive and time intensive in nature

Inventory system

Inventory system is the ongoing process of moving goods into and out of a company's

location. With regards to Unicorn effective management of inventory is highly required because

it place direct impact on cost aspect. Hence, for managing both cost and profit firm should focus

on undertaking LIFO, FIFO, EOQ etc method. Moreover, economic order quantity method

clearly presents units which need to be maintained within an organization (Elliot and et.al.,

2018). This in turn exerts control on both holding as well as ordering and thereby increases profit

margin.

Advantages Disadvantages

Tracking of inventory level becomes

easier

Control cost and maximizes profit

Time consuming profit

Need highly skilled personnel

Expenditure accounting

Each business unit produces and sells product with the motive to generate high profit

margin. In this, it is required for the company to make assessment of per unit expenditure.

Hence, by assessing direct and indirect expenses associated with product Unicorn can determine

per unit cost. By dividing total cost from number of units produced cost per unit can be

calculated (Chenhall and Moers, 2015). Hence, by adding profit margin into per unit

consumption price can be calculated by Unicorn.

Advantages Disadvantages

Helps in controlling financial

performance as it gives input for

standard costing

Facilitates ascertainment of unit

production cost

Helps in setting prices of the products

or services

Complex in nature

Expensive and time intensive in nature

Inventory system

Inventory system is the ongoing process of moving goods into and out of a company's

location. With regards to Unicorn effective management of inventory is highly required because

it place direct impact on cost aspect. Hence, for managing both cost and profit firm should focus

on undertaking LIFO, FIFO, EOQ etc method. Moreover, economic order quantity method

clearly presents units which need to be maintained within an organization (Elliot and et.al.,

2018). This in turn exerts control on both holding as well as ordering and thereby increases profit

margin.

Advantages Disadvantages

Tracking of inventory level becomes

easier

Control cost and maximizes profit

Time consuming profit

Need highly skilled personnel

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimization system

In the competitive business arena, Unicorn can attain success only when it offers products

or services at suitable cost. Moreover, now customers are looking for the retailer which offers

products or services to the customers at affordable prices. Thus, by undertaking price

optimization system business unit can assess price on which product needs to offered for

influencing customer decision making and gaining competitive edge (Kaplan and Atkinson,

2015).

Advantages Disadvantages

Helps in setting pricing policies

Assists in building strong customer

base

Employees need training for operating

such software

Expensive

P 2 Presenting different methods which can be used for management accounting reporting

Management Reports means the reports needed by different departments in order to take

the decisions for the company. As per MA, several methods are available which can be

undertaken by the firm for reporting and decision making purpose. Hence, by taking into account

below mentioned reports Unicorn can assess departmental performance and thereby would

become able to appropriate business decisions.

Budget report

This report enables manager to analyse business performance, in the context of all

departments and thereby control cost. Budget report clearly presents variances take place in the

income and expense level of firm over standards. Hence, considering the causes of variance firm

can set suitable monetary budget for upcoming time period (Kylili, Fokaides and Jimenez, 2016).

In addition to this, budget report also enables firm to measure as well as evaluate employee’s

performance and provide them with incentives.

Job cost report

It presents expenditure which associated with different project within business unit. Job

cost report is used by the firm to evaluate the figure of revenue in against to estimation with the

motive to determine profitability aspect. Job cost report provides assistance in high performing

areas so that better efforts can be made.

Accounts receivable ageing

In the competitive business arena, Unicorn can attain success only when it offers products

or services at suitable cost. Moreover, now customers are looking for the retailer which offers

products or services to the customers at affordable prices. Thus, by undertaking price

optimization system business unit can assess price on which product needs to offered for

influencing customer decision making and gaining competitive edge (Kaplan and Atkinson,

2015).

Advantages Disadvantages

Helps in setting pricing policies

Assists in building strong customer

base

Employees need training for operating

such software

Expensive

P 2 Presenting different methods which can be used for management accounting reporting

Management Reports means the reports needed by different departments in order to take

the decisions for the company. As per MA, several methods are available which can be

undertaken by the firm for reporting and decision making purpose. Hence, by taking into account

below mentioned reports Unicorn can assess departmental performance and thereby would

become able to appropriate business decisions.

Budget report

This report enables manager to analyse business performance, in the context of all

departments and thereby control cost. Budget report clearly presents variances take place in the

income and expense level of firm over standards. Hence, considering the causes of variance firm

can set suitable monetary budget for upcoming time period (Kylili, Fokaides and Jimenez, 2016).

In addition to this, budget report also enables firm to measure as well as evaluate employee’s

performance and provide them with incentives.

Job cost report

It presents expenditure which associated with different project within business unit. Job

cost report is used by the firm to evaluate the figure of revenue in against to estimation with the

motive to determine profitability aspect. Job cost report provides assistance in high performing

areas so that better efforts can be made.

Accounts receivable ageing

In the context of business unit, accounts receivable ageing report is highly significant

which helps in managing cash flow to a great extent. As, it clearly exhibits time period for which

credit is taken by the customers. For instance: By undertaking this report, manager of Unicorn

would become able to assess customers or creditors who making payments within the period of

30, 60 and 90 days. Hence, using this report manager can assess problems which take place in

collection process of firm. In this way, such report helps in identifying customers who unable to

pay their balances. Considering all such aspects Unicorn can tighten its credit policies and

thereby reduce the level of defaults.

Inventory and manufacturing report

Unicorn can make manufacturing process more effective and efficient by using stock

report. Moreover, stock report contains information about physical inventory or products,

wastage level, hourly labour or per unit overhead cost. Thus, different assembly lines within

business unit can be compared easily through the means of inventory report (Van der Stede,

2015). This in turn gives clear indication about best performing departments and areas which still

require improvement.

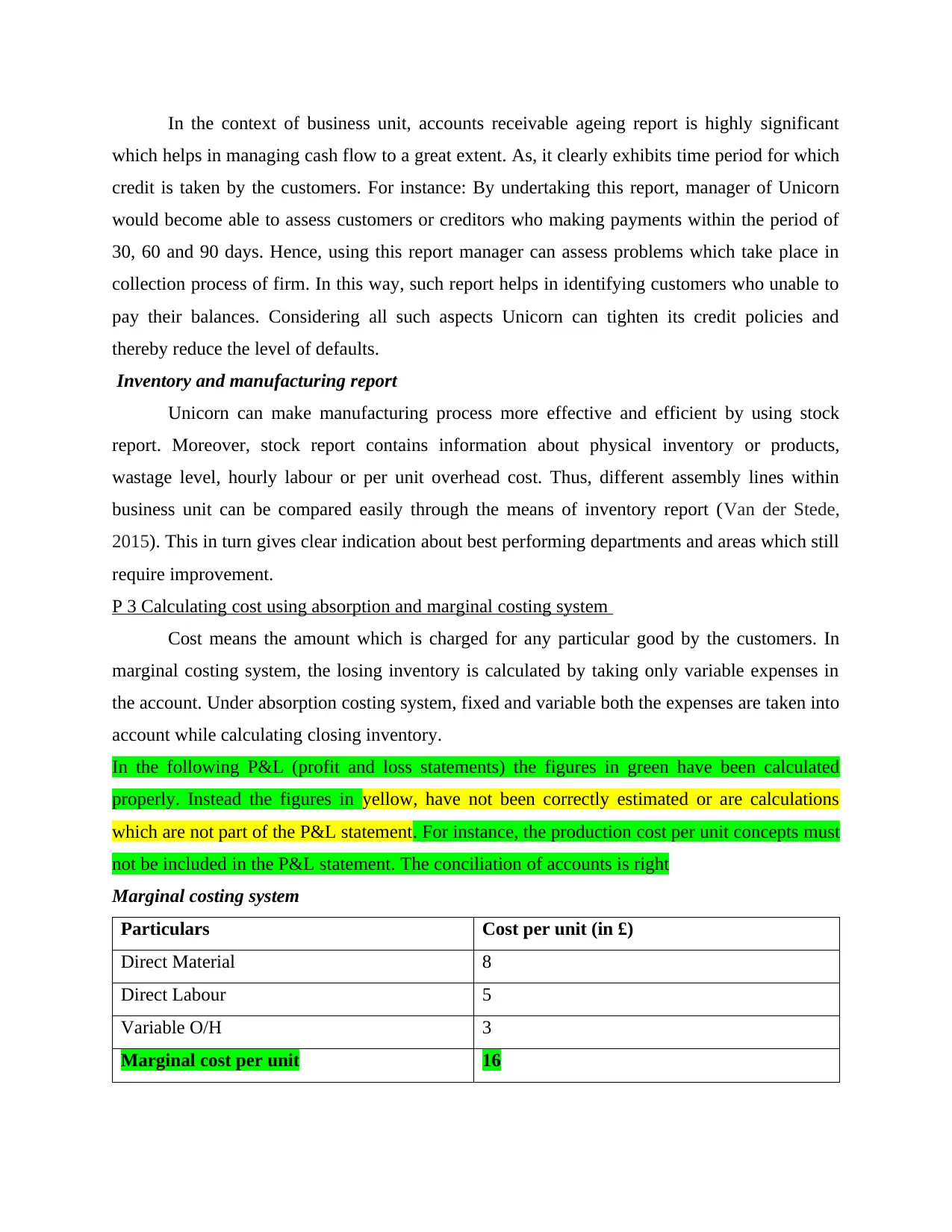

P 3 Calculating cost using absorption and marginal costing system

Cost means the amount which is charged for any particular good by the customers. In

marginal costing system, the losing inventory is calculated by taking only variable expenses in

the account. Under absorption costing system, fixed and variable both the expenses are taken into

account while calculating closing inventory.

In the following P&L (profit and loss statements) the figures in green have been calculated

properly. Instead the figures in yellow, have not been correctly estimated or are calculations

which are not part of the P&L statement. For instance, the production cost per unit concepts must

not be included in the P&L statement. The conciliation of accounts is right

Marginal costing system

Particulars Cost per unit (in £)

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

which helps in managing cash flow to a great extent. As, it clearly exhibits time period for which

credit is taken by the customers. For instance: By undertaking this report, manager of Unicorn

would become able to assess customers or creditors who making payments within the period of

30, 60 and 90 days. Hence, using this report manager can assess problems which take place in

collection process of firm. In this way, such report helps in identifying customers who unable to

pay their balances. Considering all such aspects Unicorn can tighten its credit policies and

thereby reduce the level of defaults.

Inventory and manufacturing report

Unicorn can make manufacturing process more effective and efficient by using stock

report. Moreover, stock report contains information about physical inventory or products,

wastage level, hourly labour or per unit overhead cost. Thus, different assembly lines within

business unit can be compared easily through the means of inventory report (Van der Stede,

2015). This in turn gives clear indication about best performing departments and areas which still

require improvement.

P 3 Calculating cost using absorption and marginal costing system

Cost means the amount which is charged for any particular good by the customers. In

marginal costing system, the losing inventory is calculated by taking only variable expenses in

the account. Under absorption costing system, fixed and variable both the expenses are taken into

account while calculating closing inventory.

In the following P&L (profit and loss statements) the figures in green have been calculated

properly. Instead the figures in yellow, have not been correctly estimated or are calculations

which are not part of the P&L statement. For instance, the production cost per unit concepts must

not be included in the P&L statement. The conciliation of accounts is right

Marginal costing system

Particulars Cost per unit (in £)

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Cost per unit (in £)

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

Particulars Figures (in £) Figures (in £)

May: Figures

(in £)

Sales 16000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

Particulars Figures (in £) Figures (in £)

June: Figures

(in £)

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

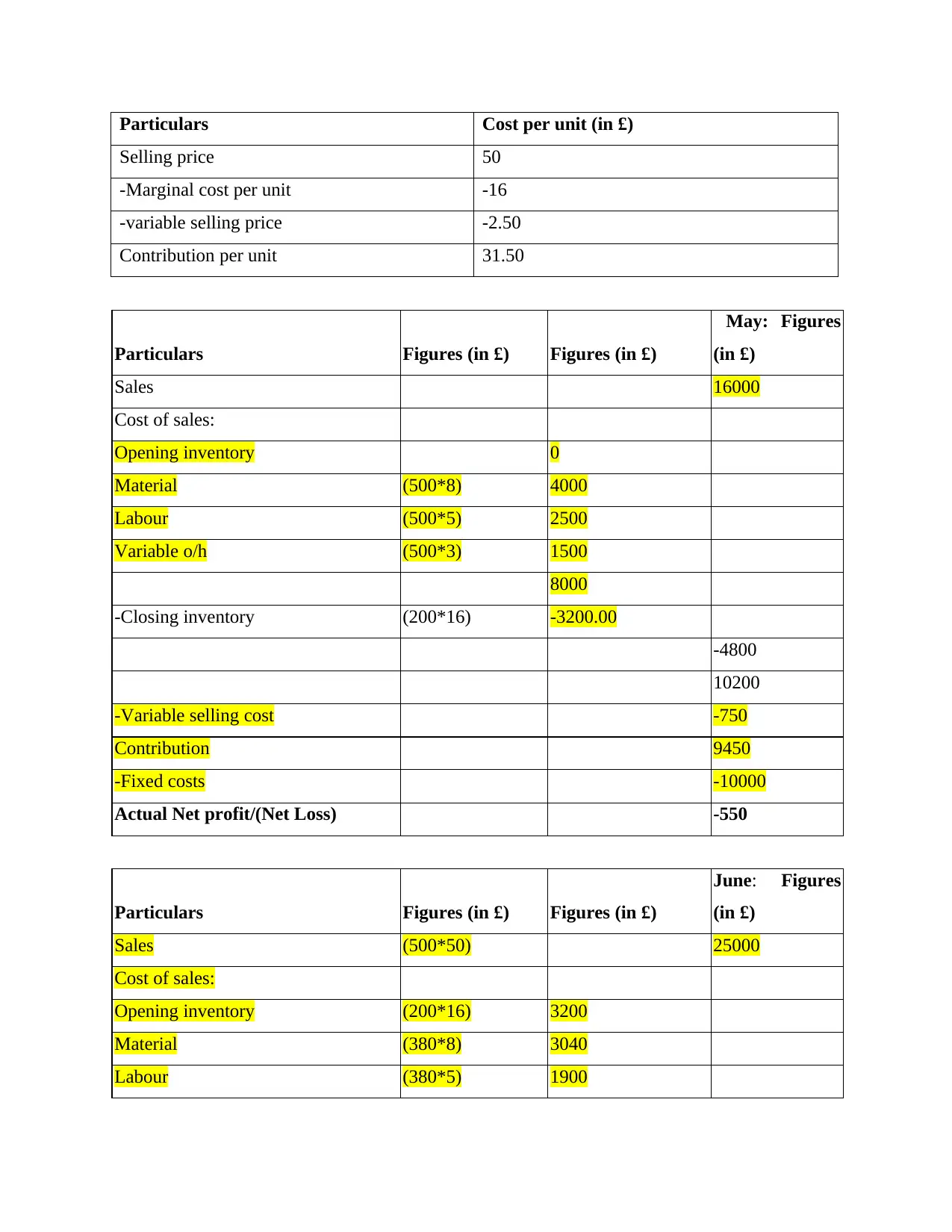

Labour (380*5) 1900

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

Particulars Figures (in £) Figures (in £)

May: Figures

(in £)

Sales 16000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

Particulars Figures (in £) Figures (in £)

June: Figures

(in £)

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Absorption costing system

Computation of cost per unit

Particulars Figures (in £)

Direct Material 8

Direct Labour 5

Variable O/H 3

Absorption cost per unit 26

Particulars Figures (in £) Figures (in £)

May: Figures

(in £)

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Production cost (500*26) 13000

-Closing inventory (200*26) -5200

-7800

(Under)/ Over absorbed Fixed

production o/ h 1000

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Absorption costing system

Computation of cost per unit

Particulars Figures (in £)

Direct Material 8

Direct Labour 5

Variable O/H 3

Absorption cost per unit 26

Particulars Figures (in £) Figures (in £)

May: Figures

(in £)

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Production cost (500*26) 13000

-Closing inventory (200*26) -5200

-7800

(Under)/ Over absorbed Fixed

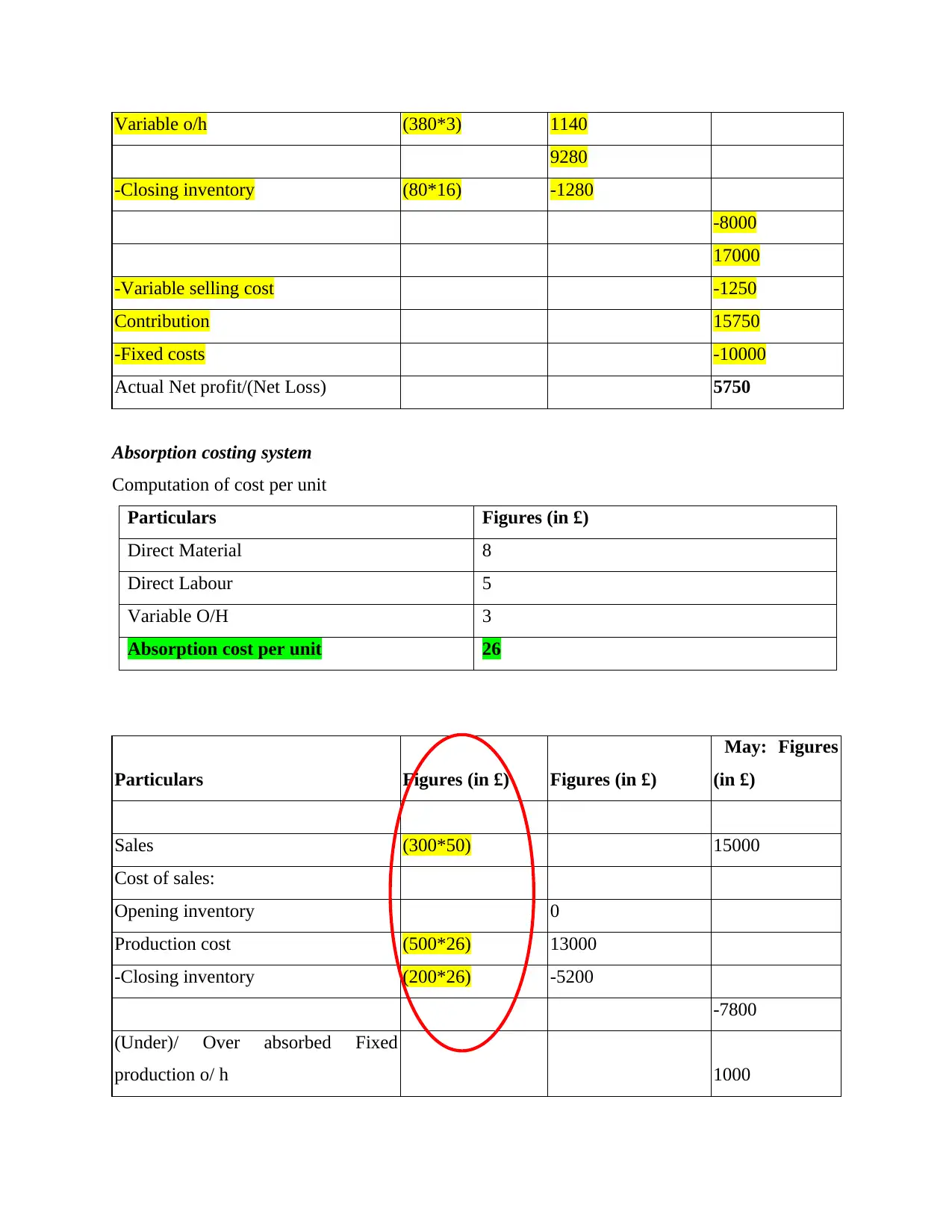

production o/ h 1000

Gross Profit/Loss 8200

-Variable selling cost -750

-Fixed administration -2000

-Fixed selling -4000

Actual Net profit/(Net Loss) 1450

Particulars

Figures (in £) Figures (in £)

June: Figures

(in £)

Sales (500*50) 25000

Cost of sales:

Opening inventory 5200

Production cost (380*26) 9880

-Closing inventory (80*26) -2080

-13000

(Under)/ Over absorbed Fixed

production o/ h -200

Gross Profit/Loss 11800

-Variable selling cost -1250

-Fixed administration -2000

-Fixed selling -4000

Actual Net profit/(Net Loss) 4550

The accounts in the red circles are not part of any profit and loss statement.

Reconciliation of profit figures

Particulars May June

Profit under absorption 1450 4550

Difference in units of inventory

Fixed production overhead (200 units *£10) (120 units* £10)

2000 1200

-Variable selling cost -750

-Fixed administration -2000

-Fixed selling -4000

Actual Net profit/(Net Loss) 1450

Particulars

Figures (in £) Figures (in £)

June: Figures

(in £)

Sales (500*50) 25000

Cost of sales:

Opening inventory 5200

Production cost (380*26) 9880

-Closing inventory (80*26) -2080

-13000

(Under)/ Over absorbed Fixed

production o/ h -200

Gross Profit/Loss 11800

-Variable selling cost -1250

-Fixed administration -2000

-Fixed selling -4000

Actual Net profit/(Net Loss) 4550

The accounts in the red circles are not part of any profit and loss statement.

Reconciliation of profit figures

Particulars May June

Profit under absorption 1450 4550

Difference in units of inventory

Fixed production overhead (200 units *£10) (120 units* £10)

2000 1200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

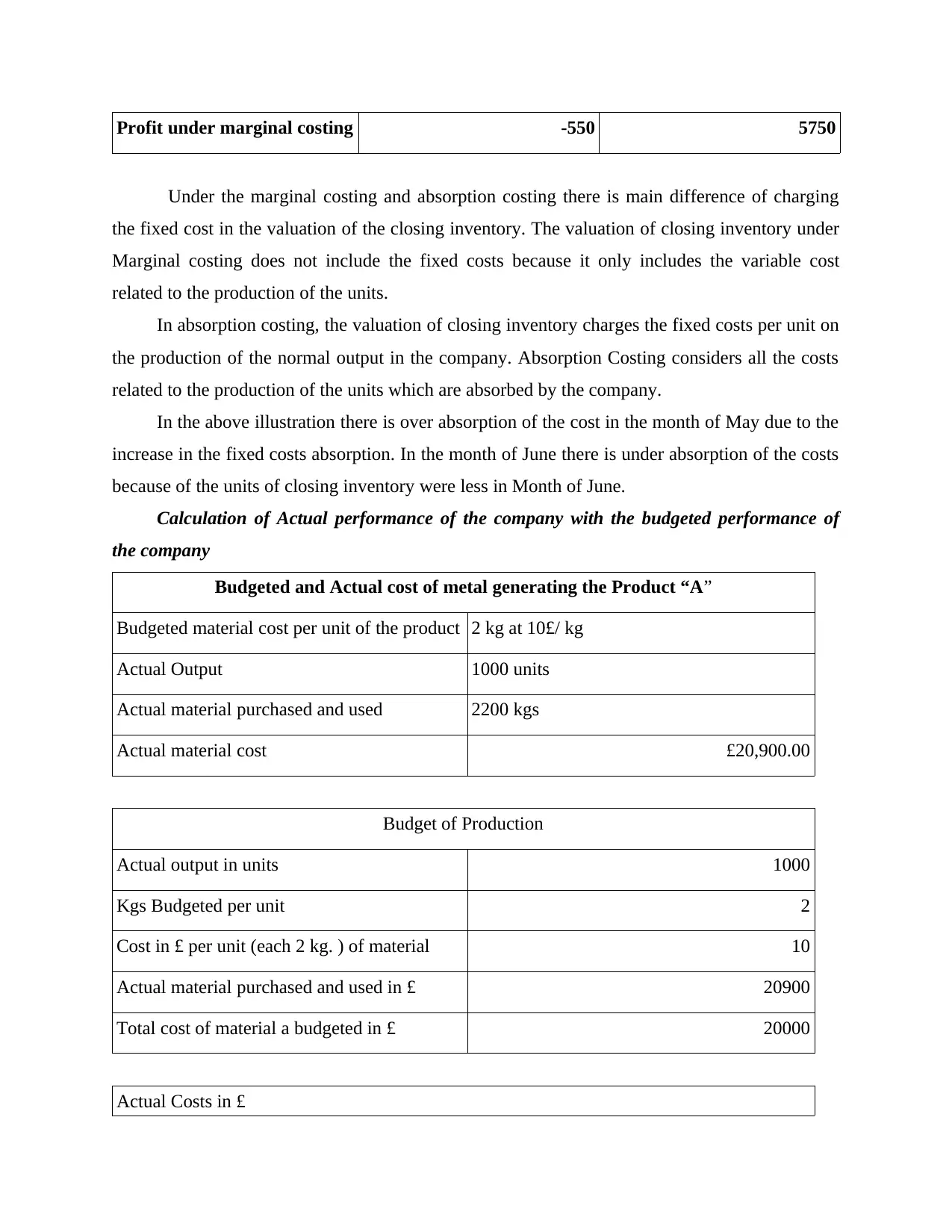

Profit under marginal costing -550 5750

Under the marginal costing and absorption costing there is main difference of charging

the fixed cost in the valuation of the closing inventory. The valuation of closing inventory under

Marginal costing does not include the fixed costs because it only includes the variable cost

related to the production of the units.

In absorption costing, the valuation of closing inventory charges the fixed costs per unit on

the production of the normal output in the company. Absorption Costing considers all the costs

related to the production of the units which are absorbed by the company.

In the above illustration there is over absorption of the cost in the month of May due to the

increase in the fixed costs absorption. In the month of June there is under absorption of the costs

because of the units of closing inventory were less in Month of June.

Calculation of Actual performance of the company with the budgeted performance of

the company

Budgeted and Actual cost of metal generating the Product “A”

Budgeted material cost per unit of the product 2 kg at 10£/ kg

Actual Output 1000 units

Actual material purchased and used 2200 kgs

Actual material cost £20,900.00

Budget of Production

Actual output in units 1000

Kgs Budgeted per unit 2

Cost in £ per unit (each 2 kg. ) of material 10

Actual material purchased and used in £ 20900

Total cost of material a budgeted in £ 20000

Actual Costs in £

Under the marginal costing and absorption costing there is main difference of charging

the fixed cost in the valuation of the closing inventory. The valuation of closing inventory under

Marginal costing does not include the fixed costs because it only includes the variable cost

related to the production of the units.

In absorption costing, the valuation of closing inventory charges the fixed costs per unit on

the production of the normal output in the company. Absorption Costing considers all the costs

related to the production of the units which are absorbed by the company.

In the above illustration there is over absorption of the cost in the month of May due to the

increase in the fixed costs absorption. In the month of June there is under absorption of the costs

because of the units of closing inventory were less in Month of June.

Calculation of Actual performance of the company with the budgeted performance of

the company

Budgeted and Actual cost of metal generating the Product “A”

Budgeted material cost per unit of the product 2 kg at 10£/ kg

Actual Output 1000 units

Actual material purchased and used 2200 kgs

Actual material cost £20,900.00

Budget of Production

Actual output in units 1000

Kgs Budgeted per unit 2

Cost in £ per unit (each 2 kg. ) of material 10

Actual material purchased and used in £ 20900

Total cost of material a budgeted in £ 20000

Actual Costs in £

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

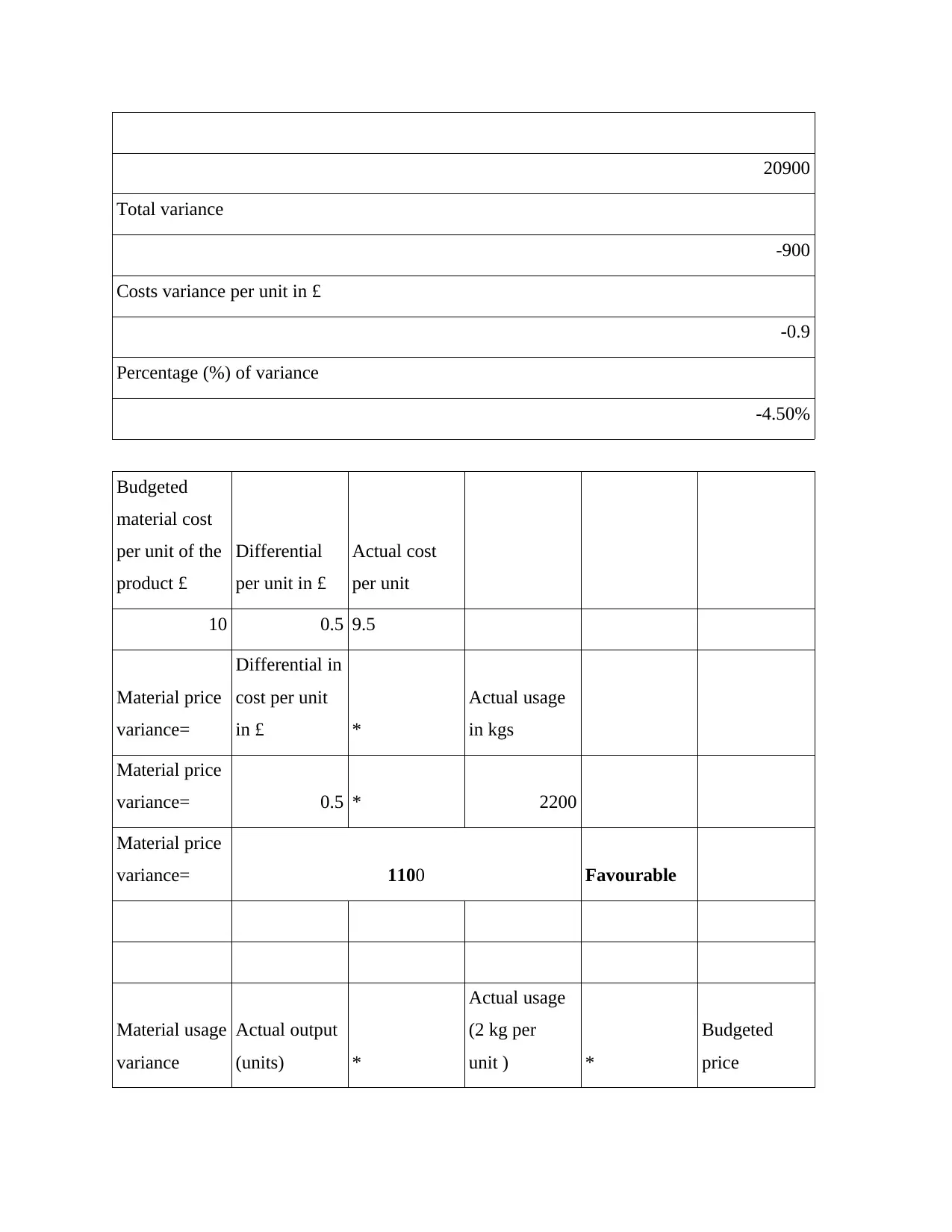

20900

Total variance

-900

Costs variance per unit in £

-0.9

Percentage (%) of variance

-4.50%

Budgeted

material cost

per unit of the

product £

Differential

per unit in £

Actual cost

per unit

10 0.5 9.5

Material price

variance=

Differential in

cost per unit

in £ *

Actual usage

in kgs

Material price

variance= 0.5 * 2200

Material price

variance= 1100 Favourable

Material usage

variance

Actual output

(units) *

Actual usage

(2 kg per

unit ) *

Budgeted

price

Total variance

-900

Costs variance per unit in £

-0.9

Percentage (%) of variance

-4.50%

Budgeted

material cost

per unit of the

product £

Differential

per unit in £

Actual cost

per unit

10 0.5 9.5

Material price

variance=

Differential in

cost per unit

in £ *

Actual usage

in kgs

Material price

variance= 0.5 * 2200

Material price

variance= 1100 Favourable

Material usage

variance

Actual output

(units) *

Actual usage

(2 kg per

unit ) *

Budgeted

price

Material usage

variance 1000 * 2 10

Budgeted use kgs. 2000

Actual use in kgs. 2200

Differential -200

Differential in £ -2000

Unfavourable

Galway Plc material cost is been increased due to the increase in the raw material of the

company. Company has absorbed more units of raw material than the budgeted units of raw

material (Song and et.al 2017). Company’s per unit cost has been decreased but overall cost is

increased due to the over absorption of raw material.

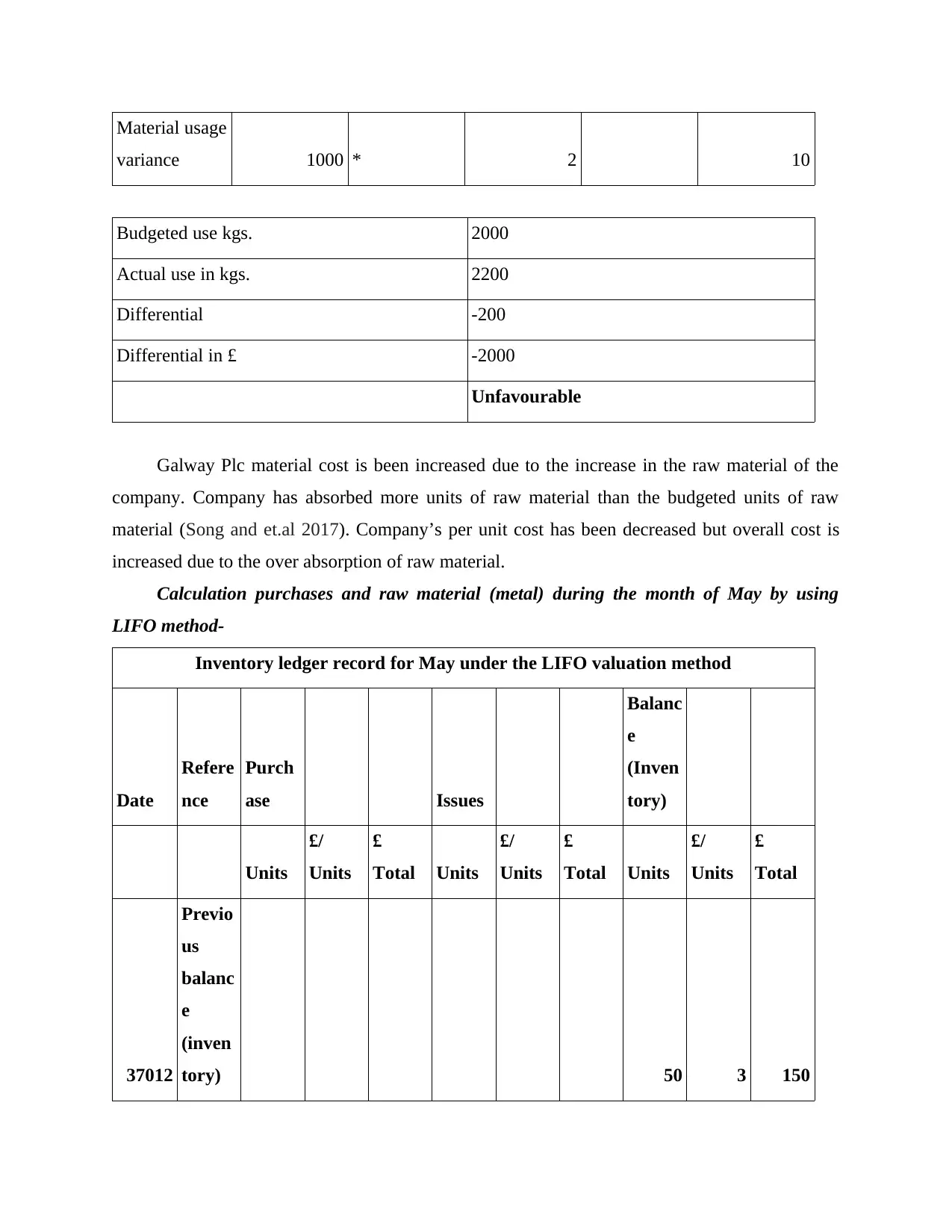

Calculation purchases and raw material (metal) during the month of May by using

LIFO method-

Inventory ledger record for May under the LIFO valuation method

Date

Refere

nce

Purch

ase Issues

Balanc

e

(Inven

tory)

Units

£/

Units

£

Total Units

£/

Units

£

Total Units

£/

Units

£

Total

37012

Previo

us

balanc

e

(inven

tory) 50 3 150

variance 1000 * 2 10

Budgeted use kgs. 2000

Actual use in kgs. 2200

Differential -200

Differential in £ -2000

Unfavourable

Galway Plc material cost is been increased due to the increase in the raw material of the

company. Company has absorbed more units of raw material than the budgeted units of raw

material (Song and et.al 2017). Company’s per unit cost has been decreased but overall cost is

increased due to the over absorption of raw material.

Calculation purchases and raw material (metal) during the month of May by using

LIFO method-

Inventory ledger record for May under the LIFO valuation method

Date

Refere

nce

Purch

ase Issues

Balanc

e

(Inven

tory)

Units

£/

Units

£

Total Units

£/

Units

£

Total Units

£/

Units

£

Total

37012

Previo

us

balanc

e

(inven

tory) 50 3 150

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.