Management Accounting System Report: Unilever Case Study Analysis

VerifiedAdded on 2023/01/18

|13

|3533

|57

Report

AI Summary

This comprehensive report delves into the management accounting system employed by Unilever, a transnational business. It begins with an introduction to management accounting (MA) and the role of management accountants within an enterprise, specifically focusing on Unilever. The report then explores the scope of MA, its relationship with various business functions like marketing and HRM, and contrasts it with financial accounting, highlighting overlaps and differences. Subsequent sections analyze different cost reporting methods such as job costing, batch costing, inventory costing, and activity-based costing. The report further examines income statements using marginal and absorption costing techniques, providing detailed calculations. Finally, it explains break-even analysis and its significance, followed by a discussion of net profit calculations and their importance in achieving organizational objectives. The report provides a thorough overview of MA principles and their application within Unilever's context, drawing on financial data and analysis to support its findings.

MANAGEMENT

ACCOUNTING SYSTEM

ACCOUNTING SYSTEM

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Explaining MA and the role of the management accountant in an enterprise ...........................1

Question 2........................................................................................................................................2

Management accounting scope and its role with respect to different business function............2

Question 3........................................................................................................................................3

Areas where financial accountant and management accountant overlap and their differences..3

Question 4........................................................................................................................................4

Cost reports and there types in MA and difference these type of cost reporting have with

evaluation of there advantages....................................................................................................4

Question 5........................................................................................................................................5

Income statement using marginal and absorption costing techniques........................................5

Question 6........................................................................................................................................6

The way Break even analysis works and its importance for the enterprise................................6

Question 7........................................................................................................................................7

Net profit calculation and explanations of its importance for the management accountant and

its use in driving organisational objectives.................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Explaining MA and the role of the management accountant in an enterprise ...........................1

Question 2........................................................................................................................................2

Management accounting scope and its role with respect to different business function............2

Question 3........................................................................................................................................3

Areas where financial accountant and management accountant overlap and their differences..3

Question 4........................................................................................................................................4

Cost reports and there types in MA and difference these type of cost reporting have with

evaluation of there advantages....................................................................................................4

Question 5........................................................................................................................................5

Income statement using marginal and absorption costing techniques........................................5

Question 6........................................................................................................................................6

The way Break even analysis works and its importance for the enterprise................................6

Question 7........................................................................................................................................7

Net profit calculation and explanations of its importance for the management accountant and

its use in driving organisational objectives.................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION

Management accounting system usually mean the system that helps the business in

measuring and evaluating different management process of the organisation(Armitage, Webb

and Glynn, 2016). Report is based on the company Unilever and it is transnational business

having its headquarter at London, UK. Report will include Understanding of management

accounting systems and application of different management accounting techniques.

Question 1

Explaining MA and the role of the management accountant in an enterprise

MA defined as the practice of facilitating the financial information and the

resources to the managers in the process of making decision. It is used by an internal

management of the company where different activities within the business are analysed. The

main objective of MA is to use the statistical data and in taking accurate and better decision in

controlling an enterprise, development and the business activities. In other words, management

accounting is representation of the financial data and the business activities for internal

management of company(Ball, Grubnic and Birchall, 2014)

MA is the profession which includes partnering in the decision making of management,

devising performance systems of management on providing an expertise in the financial

reporting and controlling for enabling the management in framing and executing strategy of an

organization.

Role of management accountant

Managerial accountant analyses and records financial information through collection

interpretation and preparation of financial data for the company and management team of an

organisation. The MA data is used for forming practical decision that will the benefit the growth

of the firm. MA is required to be critical thinker and strong mathematical background so that it

can make correct calculation of the financial data. Accountant has to keep record of all the

transaction that are incurred by the company. They have to forecast about the future by making

appropriate budgets and estimated cash flows. They plays very critical role in the present times

as organisations take their decisions based on financial information that is prepared by the

organisation. The routine reports and the reports for the long run purposes are been forwarded to

the managerial personnel at different levels in order to take appropriate action at right time. He

also make use of such reports for the purpose of taking an important decisions in an effective

1

Management accounting system usually mean the system that helps the business in

measuring and evaluating different management process of the organisation(Armitage, Webb

and Glynn, 2016). Report is based on the company Unilever and it is transnational business

having its headquarter at London, UK. Report will include Understanding of management

accounting systems and application of different management accounting techniques.

Question 1

Explaining MA and the role of the management accountant in an enterprise

MA defined as the practice of facilitating the financial information and the

resources to the managers in the process of making decision. It is used by an internal

management of the company where different activities within the business are analysed. The

main objective of MA is to use the statistical data and in taking accurate and better decision in

controlling an enterprise, development and the business activities. In other words, management

accounting is representation of the financial data and the business activities for internal

management of company(Ball, Grubnic and Birchall, 2014)

MA is the profession which includes partnering in the decision making of management,

devising performance systems of management on providing an expertise in the financial

reporting and controlling for enabling the management in framing and executing strategy of an

organization.

Role of management accountant

Managerial accountant analyses and records financial information through collection

interpretation and preparation of financial data for the company and management team of an

organisation. The MA data is used for forming practical decision that will the benefit the growth

of the firm. MA is required to be critical thinker and strong mathematical background so that it

can make correct calculation of the financial data. Accountant has to keep record of all the

transaction that are incurred by the company. They have to forecast about the future by making

appropriate budgets and estimated cash flows. They plays very critical role in the present times

as organisations take their decisions based on financial information that is prepared by the

organisation. The routine reports and the reports for the long run purposes are been forwarded to

the managerial personnel at different levels in order to take appropriate action at right time. He

also make use of such reports for the purpose of taking an important decisions in an effective

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manner. He plays an important role in raising and application of funds for making decisions

about maintaining leverage position. Therefore, management accountant seeks for maintaining

optimum level of capital structure and giving appropriate considerations to the several costs of

the capital theories, possibility of trading and leverage. He occupies the pivotal position within

an enterprise by performing all the staff functions and also contains a line authority over an

accountant & the other employees in their respective office. He facilitates significant information

to internal stakeholders for decision making in short period. He plays a critical role in framing

reports in relation to standard cost, variance analysis, cash flow assessment, budgets,

performance evaluation, liquidity management that in turn ensures proper controlling. His role is

to guide and educate executives in respect to need for controlling information & ways in using it.

He shifts the important information from the report in a clear format for the external

parties(Barbu and et. al., 2014).

Question 2

Management accounting scope and its role with respect to different business function

Management accounting is having a wider scope, as it contain important information

which is used by the accountants for financial analysis of the business. The scope for different

role of management accounting in Unilever is as following:- Financial accounting:- Without the efficient use of financial accounting, the management

accounting can not operate effectively as financial accounting provides the historical

information of the Unilever that is used by business managers for making decision that

can benefits the organisation.

Cost accounting:- By using cost accounting, different techniques are used to determine

cost of manufacturing and financial data is been used in order to find the cost associated

with product and processes. It is generally considered as backbone of management

accounting as it provides different analytical that business can use in order to discharge

its respective responsibilities(Bromwich and Scapens, 2016).

Financial management:- It is generally the planning and controlling of different financial

resources and it usually deals with raising funds and their effective utilization in

Unilever.

Management accounting is playing an important role for different function of business

and these roles are as following:-

2

about maintaining leverage position. Therefore, management accountant seeks for maintaining

optimum level of capital structure and giving appropriate considerations to the several costs of

the capital theories, possibility of trading and leverage. He occupies the pivotal position within

an enterprise by performing all the staff functions and also contains a line authority over an

accountant & the other employees in their respective office. He facilitates significant information

to internal stakeholders for decision making in short period. He plays a critical role in framing

reports in relation to standard cost, variance analysis, cash flow assessment, budgets,

performance evaluation, liquidity management that in turn ensures proper controlling. His role is

to guide and educate executives in respect to need for controlling information & ways in using it.

He shifts the important information from the report in a clear format for the external

parties(Barbu and et. al., 2014).

Question 2

Management accounting scope and its role with respect to different business function

Management accounting is having a wider scope, as it contain important information

which is used by the accountants for financial analysis of the business. The scope for different

role of management accounting in Unilever is as following:- Financial accounting:- Without the efficient use of financial accounting, the management

accounting can not operate effectively as financial accounting provides the historical

information of the Unilever that is used by business managers for making decision that

can benefits the organisation.

Cost accounting:- By using cost accounting, different techniques are used to determine

cost of manufacturing and financial data is been used in order to find the cost associated

with product and processes. It is generally considered as backbone of management

accounting as it provides different analytical that business can use in order to discharge

its respective responsibilities(Bromwich and Scapens, 2016).

Financial management:- It is generally the planning and controlling of different financial

resources and it usually deals with raising funds and their effective utilization in

Unilever.

Management accounting is playing an important role for different function of business

and these roles are as following:-

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting with Marketing:- Management accounting plays a key role for

marketing as it closely work with marketing department at Unilever in order to manage

and develop sales of the business by monitoring the recent trends in the business.

Marketing works to conduct different campaigns, while management accounting

determines the cost that will be associated with campaign and the way it can be managed. Management accounting with HRM:- Role of HRM is to develop and control budgets of

the departments and management accounting prepare them to have budgeted items like

recruitment, incentives etc.(Chenhall and Moers, 2015).

MA with Manufacturing:- MA helps Unilever to determine the respective product that

can used in habit of manufacturing and the respective cost that will be associated during

the manufacturing process will be determine by Management accountants.

Question 3

Areas where financial accountant and management accountant overlap and their differences

MA and financial accountant are having different roles and responsibilities for the

business and these differences are as following:-

MANAGEMENT ACCOUNTANT FINANCIAL ACCOUNTANT

For the internal purpose of the

organisation they prepare this report

and the data they collect is confidential.

They do not set any pattern for the

reporting and the data is as per the

targeted audience(Endenich, 2014).

They work with both financial and non-

financial data in reports.

There focus is on present and forecasts

for future.

They prepare reports for public view

and the respective data is disclosed in

front of the public.

They follow IFRS or US GAAP as they

are universal reporting standards and

any individual can understand the same.

They work on the financial data of the

enterprise.

There focus is on history and reports on

the prior quarter or year.

There are different areas where the financial accountant and management accountant

work together and overlap each other. These areas are as following:-

3

marketing as it closely work with marketing department at Unilever in order to manage

and develop sales of the business by monitoring the recent trends in the business.

Marketing works to conduct different campaigns, while management accounting

determines the cost that will be associated with campaign and the way it can be managed. Management accounting with HRM:- Role of HRM is to develop and control budgets of

the departments and management accounting prepare them to have budgeted items like

recruitment, incentives etc.(Chenhall and Moers, 2015).

MA with Manufacturing:- MA helps Unilever to determine the respective product that

can used in habit of manufacturing and the respective cost that will be associated during

the manufacturing process will be determine by Management accountants.

Question 3

Areas where financial accountant and management accountant overlap and their differences

MA and financial accountant are having different roles and responsibilities for the

business and these differences are as following:-

MANAGEMENT ACCOUNTANT FINANCIAL ACCOUNTANT

For the internal purpose of the

organisation they prepare this report

and the data they collect is confidential.

They do not set any pattern for the

reporting and the data is as per the

targeted audience(Endenich, 2014).

They work with both financial and non-

financial data in reports.

There focus is on present and forecasts

for future.

They prepare reports for public view

and the respective data is disclosed in

front of the public.

They follow IFRS or US GAAP as they

are universal reporting standards and

any individual can understand the same.

They work on the financial data of the

enterprise.

There focus is on history and reports on

the prior quarter or year.

There are different areas where the financial accountant and management accountant

work together and overlap each other. These areas are as following:-

3

Both Financial and management accountant follows same rules and principles of

accounting.

Financial and management accountant provides useful financial information for the users

and have concern for the financial statements, revenue, expenses, assets etc(Hyndman,

2016).

Same type of accounting principles and concepts are used by both the accountants and

measure the costs for different accounting periods.

Both Financial and management accountants are having knowledge in accounting

expertise and both have focus on performance management and decision analysis.

Question 4

Cost reports and there types in MA and difference these type of cost reporting have with

evaluation of there advantges

Different types of cost reports in management accounting and there benefits are as

following:-

Job costing:- It is a method of making record with respect to cost of manufacturing job of the

business. Here, the accountant track the associated cost with respect to each job and maintain the

respective data that is relevant to Unilever's operations. It is a specific accounting methodology

that is used in the business to track the respective expenses that will be required in order to have

unique product in hand. The different benefits with respect to job costing are as following:-

This is a detailed analysis of costs of materials, labour and overheads.

It helps Unilever to understand which job is profitable and which is not.

This cost reporting helps Unilever to know separately the profit earned by each job.

With the completion of job, the element of cost, its selling price and the earned profit can

be compared in order to control the cost(Hyndman and et. al., 2014).

Batch costing:- Here, the homogeneous products are taken as cost unit and this cost reporting is

used in order to understand the associated cost per unit. This type of cost reporting benefits the

business in following ways:-

The work of accountants get reduce with the help of batch costing as the costing is done

for a batch of product that are having homogeneous jobs.

It helps in reducing the cost of production that arises and supervision become easy for the

accountants(Lavia López and Hiebl, 2014)(Lavia López and Hiebl, 2014).

4

accounting.

Financial and management accountant provides useful financial information for the users

and have concern for the financial statements, revenue, expenses, assets etc(Hyndman,

2016).

Same type of accounting principles and concepts are used by both the accountants and

measure the costs for different accounting periods.

Both Financial and management accountants are having knowledge in accounting

expertise and both have focus on performance management and decision analysis.

Question 4

Cost reports and there types in MA and difference these type of cost reporting have with

evaluation of there advantges

Different types of cost reports in management accounting and there benefits are as

following:-

Job costing:- It is a method of making record with respect to cost of manufacturing job of the

business. Here, the accountant track the associated cost with respect to each job and maintain the

respective data that is relevant to Unilever's operations. It is a specific accounting methodology

that is used in the business to track the respective expenses that will be required in order to have

unique product in hand. The different benefits with respect to job costing are as following:-

This is a detailed analysis of costs of materials, labour and overheads.

It helps Unilever to understand which job is profitable and which is not.

This cost reporting helps Unilever to know separately the profit earned by each job.

With the completion of job, the element of cost, its selling price and the earned profit can

be compared in order to control the cost(Hyndman and et. al., 2014).

Batch costing:- Here, the homogeneous products are taken as cost unit and this cost reporting is

used in order to understand the associated cost per unit. This type of cost reporting benefits the

business in following ways:-

The work of accountants get reduce with the help of batch costing as the costing is done

for a batch of product that are having homogeneous jobs.

It helps in reducing the cost of production that arises and supervision become easy for the

accountants(Lavia López and Hiebl, 2014)(Lavia López and Hiebl, 2014).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory costing:- This method is used for determining the cost associated with the inventory

and it helps the company in determining associated stock cost before the sale of the products and

service is made. The cost of stock can be reduced in Unilever by Avoiding minimum order

quantities and have clear idea about the reorder point. Unilever is required to have an improved

forecast accuracy in the business and reduce manufacturing lot sizes for reducing the associated

cost of stock. The benefits of this costing is as following:-

This method is easy to apply and normal physical flow of goods in there.

No manipulation of income is there as it determine which unit to ship(Lukka and Vinnari,

2014).

Activity based costing:- This costing method is used by the business in order to identify

different activities and assign the cost with respect to these activities by understanding there

actual consumption. The benefits of activity based costing are as following:-

It brings accuracy in the cost associated with the product and have focus on the cause and

effects the cost incurrence relationship.

It identifies cost behaviour and also reduce the cost. It traces the cost and helps in making

better decision by fixing selling prices of products.

Question 5

Income statement using marginal and absorption costing techniques

Marginal costing techniques:-

It is a costing technique in which variable cost is charged to units of cost and the fixed

cost for the period is written off against the contribution. The basic advantage of using this

method is that it is constant in nature irrespective of the volume of production. It having an

effective cost control and is having uniform and realistic valuation(Melnyk, and et. al., 2014).

Absorption costing techniques:-

This method accumulates the associated cost with respect to production process. It

creates an inventory valuation and that is usually stated in balance sheet of Unilever. It tracks the

profits more accurately and accounts for the production costs that is, it evaluate the profitability

and prices also includes the fixed cost. This further helps out the management of Unilever in

order to evaluate the profitability and prices also includes the fixed cost for the products(Otley,

2016).

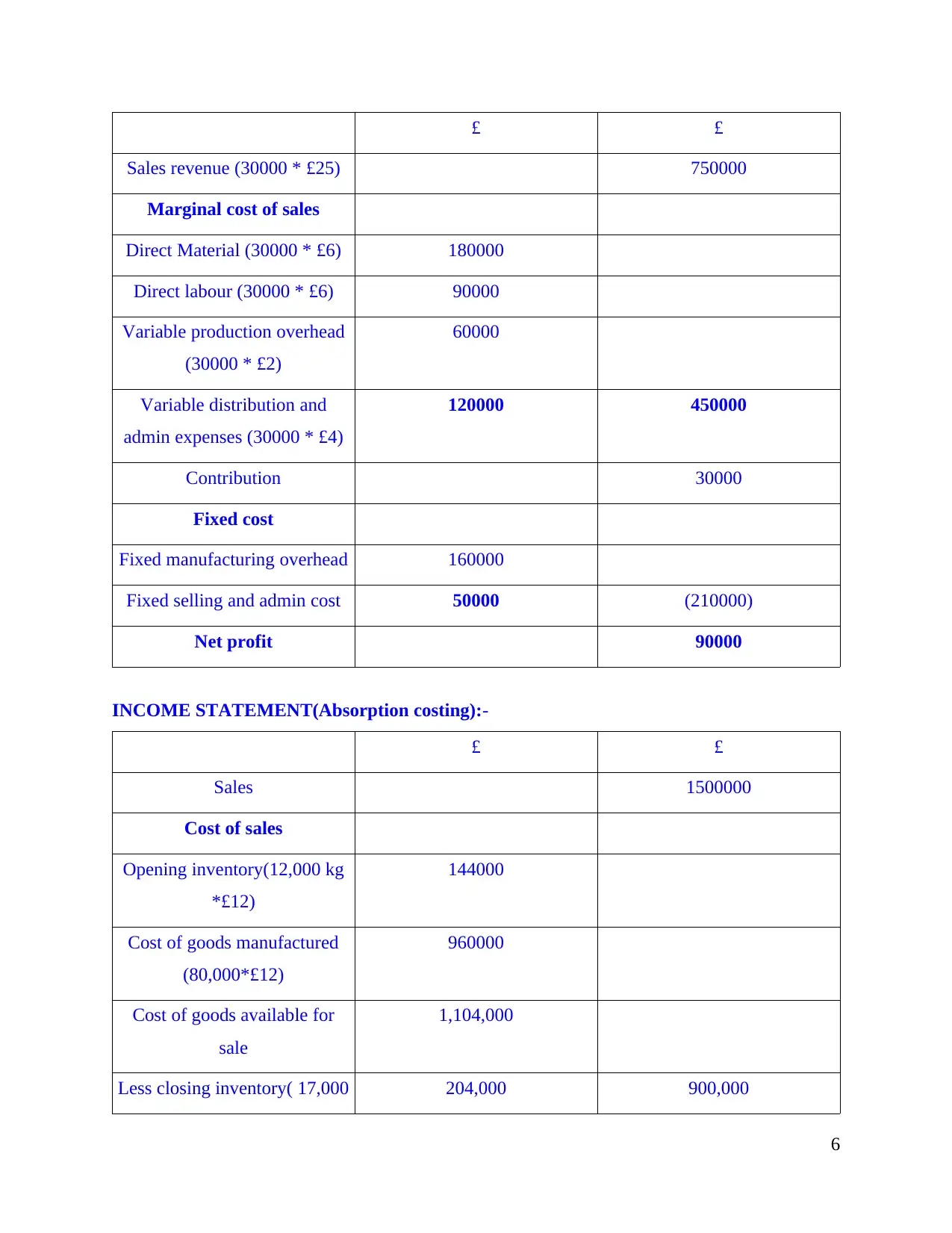

INCOME STATEMENT(Marginal costing):-

5

and it helps the company in determining associated stock cost before the sale of the products and

service is made. The cost of stock can be reduced in Unilever by Avoiding minimum order

quantities and have clear idea about the reorder point. Unilever is required to have an improved

forecast accuracy in the business and reduce manufacturing lot sizes for reducing the associated

cost of stock. The benefits of this costing is as following:-

This method is easy to apply and normal physical flow of goods in there.

No manipulation of income is there as it determine which unit to ship(Lukka and Vinnari,

2014).

Activity based costing:- This costing method is used by the business in order to identify

different activities and assign the cost with respect to these activities by understanding there

actual consumption. The benefits of activity based costing are as following:-

It brings accuracy in the cost associated with the product and have focus on the cause and

effects the cost incurrence relationship.

It identifies cost behaviour and also reduce the cost. It traces the cost and helps in making

better decision by fixing selling prices of products.

Question 5

Income statement using marginal and absorption costing techniques

Marginal costing techniques:-

It is a costing technique in which variable cost is charged to units of cost and the fixed

cost for the period is written off against the contribution. The basic advantage of using this

method is that it is constant in nature irrespective of the volume of production. It having an

effective cost control and is having uniform and realistic valuation(Melnyk, and et. al., 2014).

Absorption costing techniques:-

This method accumulates the associated cost with respect to production process. It

creates an inventory valuation and that is usually stated in balance sheet of Unilever. It tracks the

profits more accurately and accounts for the production costs that is, it evaluate the profitability

and prices also includes the fixed cost. This further helps out the management of Unilever in

order to evaluate the profitability and prices also includes the fixed cost for the products(Otley,

2016).

INCOME STATEMENT(Marginal costing):-

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

£ £

Sales revenue (30000 * £25) 750000

Marginal cost of sales

Direct Material (30000 * £6) 180000

Direct labour (30000 * £6) 90000

Variable production overhead

(30000 * £2)

60000

Variable distribution and

admin expenses (30000 * £4)

120000 450000

Contribution 30000

Fixed cost

Fixed manufacturing overhead 160000

Fixed selling and admin cost 50000 (210000)

Net profit 90000

INCOME STATEMENT(Absorption costing):-

£ £

Sales 1500000

Cost of sales

Opening inventory(12,000 kg

*£12)

144000

Cost of goods manufactured

(80,000*£12)

960000

Cost of goods available for

sale

1,104,000

Less closing inventory( 17,000 204,000 900,000

6

Sales revenue (30000 * £25) 750000

Marginal cost of sales

Direct Material (30000 * £6) 180000

Direct labour (30000 * £6) 90000

Variable production overhead

(30000 * £2)

60000

Variable distribution and

admin expenses (30000 * £4)

120000 450000

Contribution 30000

Fixed cost

Fixed manufacturing overhead 160000

Fixed selling and admin cost 50000 (210000)

Net profit 90000

INCOME STATEMENT(Absorption costing):-

£ £

Sales 1500000

Cost of sales

Opening inventory(12,000 kg

*£12)

144000

Cost of goods manufactured

(80,000*£12)

960000

Cost of goods available for

sale

1,104,000

Less closing inventory( 17,000 204,000 900,000

6

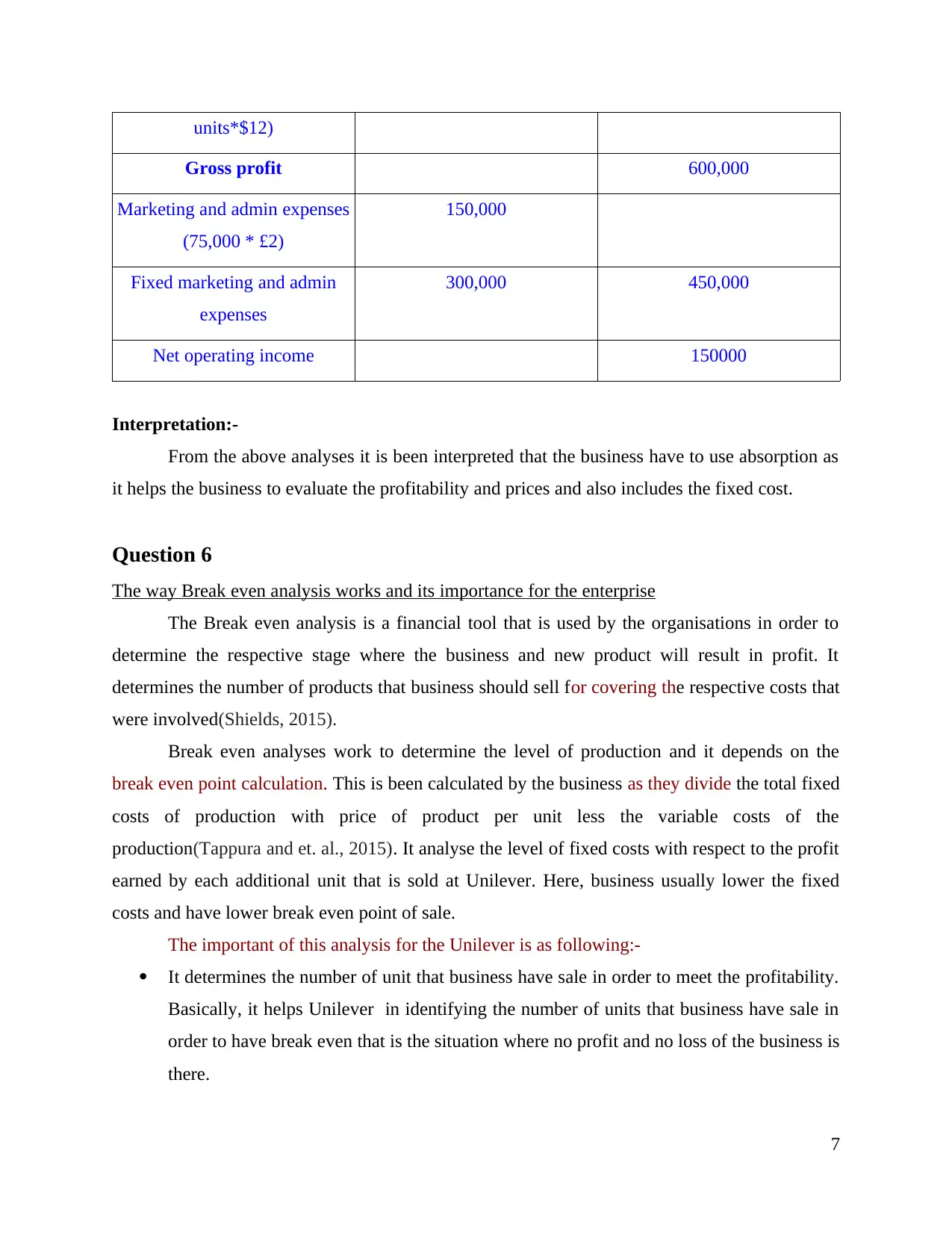

units*$12)

Gross profit 600,000

Marketing and admin expenses

(75,000 * £2)

150,000

Fixed marketing and admin

expenses

300,000 450,000

Net operating income 150000

Interpretation:-

From the above analyses it is been interpreted that the business have to use absorption as

it helps the business to evaluate the profitability and prices and also includes the fixed cost.

Question 6

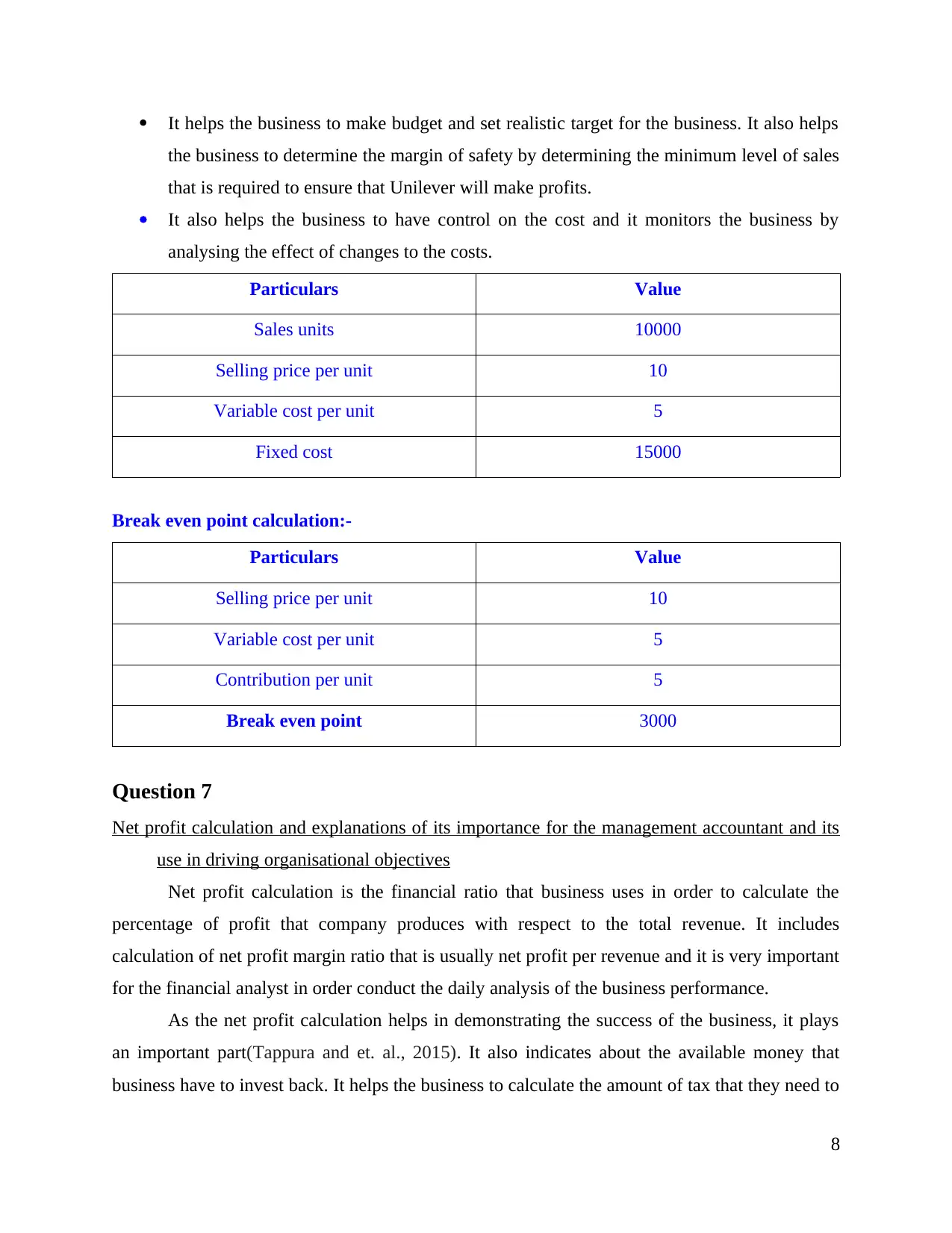

The way Break even analysis works and its importance for the enterprise

The Break even analysis is a financial tool that is used by the organisations in order to

determine the respective stage where the business and new product will result in profit. It

determines the number of products that business should sell for covering the respective costs that

were involved(Shields, 2015).

Break even analyses work to determine the level of production and it depends on the

break even point calculation. This is been calculated by the business as they divide the total fixed

costs of production with price of product per unit less the variable costs of the

production(Tappura and et. al., 2015). It analyse the level of fixed costs with respect to the profit

earned by each additional unit that is sold at Unilever. Here, business usually lower the fixed

costs and have lower break even point of sale.

The important of this analysis for the Unilever is as following:-

It determines the number of unit that business have sale in order to meet the profitability.

Basically, it helps Unilever in identifying the number of units that business have sale in

order to have break even that is the situation where no profit and no loss of the business is

there.

7

Gross profit 600,000

Marketing and admin expenses

(75,000 * £2)

150,000

Fixed marketing and admin

expenses

300,000 450,000

Net operating income 150000

Interpretation:-

From the above analyses it is been interpreted that the business have to use absorption as

it helps the business to evaluate the profitability and prices and also includes the fixed cost.

Question 6

The way Break even analysis works and its importance for the enterprise

The Break even analysis is a financial tool that is used by the organisations in order to

determine the respective stage where the business and new product will result in profit. It

determines the number of products that business should sell for covering the respective costs that

were involved(Shields, 2015).

Break even analyses work to determine the level of production and it depends on the

break even point calculation. This is been calculated by the business as they divide the total fixed

costs of production with price of product per unit less the variable costs of the

production(Tappura and et. al., 2015). It analyse the level of fixed costs with respect to the profit

earned by each additional unit that is sold at Unilever. Here, business usually lower the fixed

costs and have lower break even point of sale.

The important of this analysis for the Unilever is as following:-

It determines the number of unit that business have sale in order to meet the profitability.

Basically, it helps Unilever in identifying the number of units that business have sale in

order to have break even that is the situation where no profit and no loss of the business is

there.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps the business to make budget and set realistic target for the business. It also helps

the business to determine the margin of safety by determining the minimum level of sales

that is required to ensure that Unilever will make profits.

It also helps the business to have control on the cost and it monitors the business by

analysing the effect of changes to the costs.

Particulars Value

Sales units 10000

Selling price per unit 10

Variable cost per unit 5

Fixed cost 15000

Break even point calculation:-

Particulars Value

Selling price per unit 10

Variable cost per unit 5

Contribution per unit 5

Break even point 3000

Question 7

Net profit calculation and explanations of its importance for the management accountant and its

use in driving organisational objectives

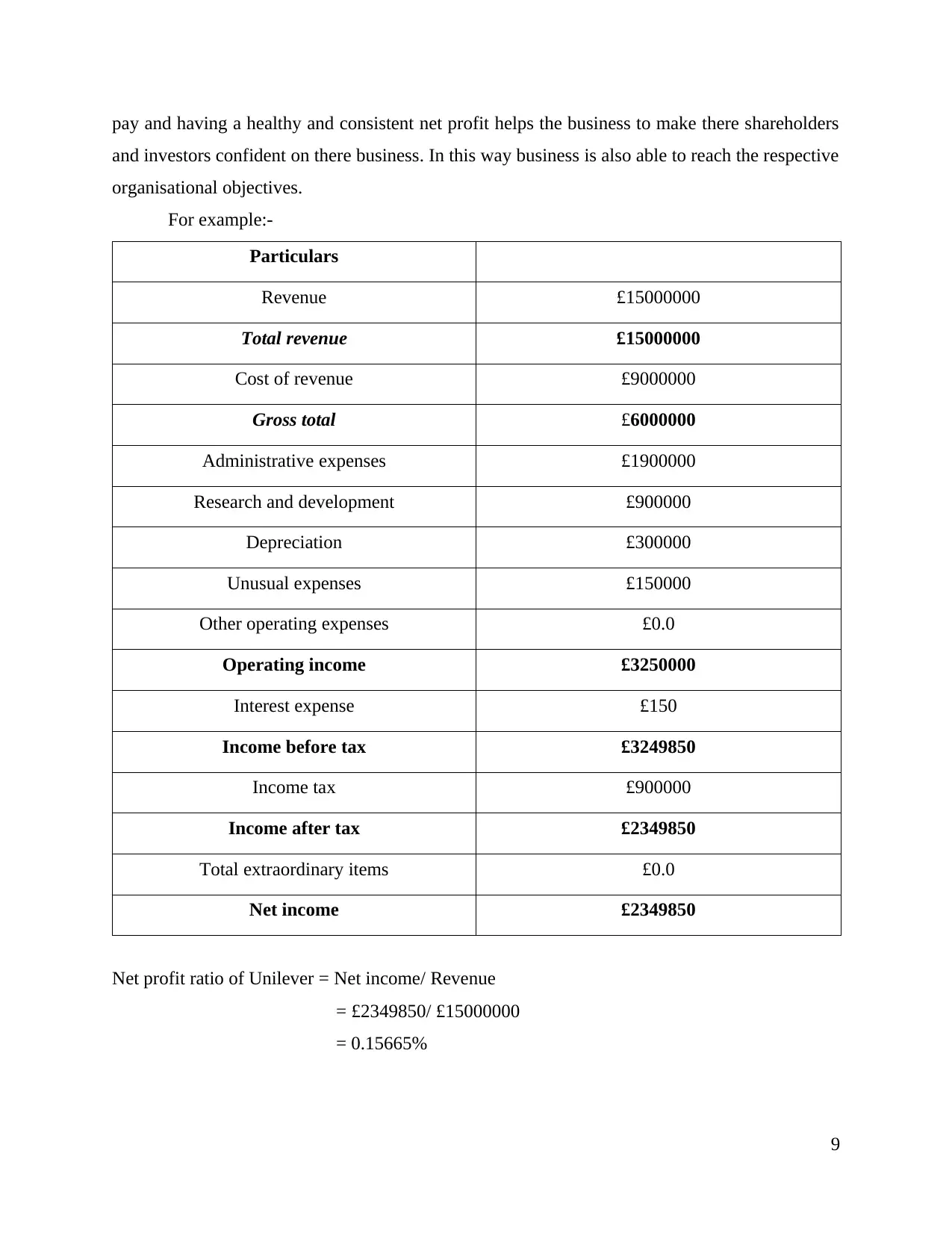

Net profit calculation is the financial ratio that business uses in order to calculate the

percentage of profit that company produces with respect to the total revenue. It includes

calculation of net profit margin ratio that is usually net profit per revenue and it is very important

for the financial analyst in order conduct the daily analysis of the business performance.

As the net profit calculation helps in demonstrating the success of the business, it plays

an important part(Tappura and et. al., 2015). It also indicates about the available money that

business have to invest back. It helps the business to calculate the amount of tax that they need to

8

the business to determine the margin of safety by determining the minimum level of sales

that is required to ensure that Unilever will make profits.

It also helps the business to have control on the cost and it monitors the business by

analysing the effect of changes to the costs.

Particulars Value

Sales units 10000

Selling price per unit 10

Variable cost per unit 5

Fixed cost 15000

Break even point calculation:-

Particulars Value

Selling price per unit 10

Variable cost per unit 5

Contribution per unit 5

Break even point 3000

Question 7

Net profit calculation and explanations of its importance for the management accountant and its

use in driving organisational objectives

Net profit calculation is the financial ratio that business uses in order to calculate the

percentage of profit that company produces with respect to the total revenue. It includes

calculation of net profit margin ratio that is usually net profit per revenue and it is very important

for the financial analyst in order conduct the daily analysis of the business performance.

As the net profit calculation helps in demonstrating the success of the business, it plays

an important part(Tappura and et. al., 2015). It also indicates about the available money that

business have to invest back. It helps the business to calculate the amount of tax that they need to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pay and having a healthy and consistent net profit helps the business to make there shareholders

and investors confident on there business. In this way business is also able to reach the respective

organisational objectives.

For example:-

Particulars

Revenue £15000000

Total revenue £15000000

Cost of revenue £9000000

Gross total £6000000

Administrative expenses £1900000

Research and development £900000

Depreciation £300000

Unusual expenses £150000

Other operating expenses £0.0

Operating income £3250000

Interest expense £150

Income before tax £3249850

Income tax £900000

Income after tax £2349850

Total extraordinary items £0.0

Net income £2349850

Net profit ratio of Unilever = Net income/ Revenue

= £2349850/ £15000000

= 0.15665%

9

and investors confident on there business. In this way business is also able to reach the respective

organisational objectives.

For example:-

Particulars

Revenue £15000000

Total revenue £15000000

Cost of revenue £9000000

Gross total £6000000

Administrative expenses £1900000

Research and development £900000

Depreciation £300000

Unusual expenses £150000

Other operating expenses £0.0

Operating income £3250000

Interest expense £150

Income before tax £3249850

Income tax £900000

Income after tax £2349850

Total extraordinary items £0.0

Net income £2349850

Net profit ratio of Unilever = Net income/ Revenue

= £2349850/ £15000000

= 0.15665%

9

CONCLUSION

It is been concluded from the report that MA generally plays a key role for organisation

and with its different function of the business. Report also concluded that MA is quite different

from that of financial accounting and the different cost report in MA leads to benefit for the

Unilever. Report also concluded that absorption cost is the best technique that business must

include. Report also concluded that break even analysis plays an important part for in identifying

the number of units that business have sale so that respective measures can be taken by Unilever

for taking right step for business profitability.

10

It is been concluded from the report that MA generally plays a key role for organisation

and with its different function of the business. Report also concluded that MA is quite different

from that of financial accounting and the different cost report in MA leads to benefit for the

Unilever. Report also concluded that absorption cost is the best technique that business must

include. Report also concluded that break even analysis plays an important part for in identifying

the number of units that business have sale so that respective measures can be taken by Unilever

for taking right step for business profitability.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.