Management Accounting Report: Unilever Financial Performance Analysis

VerifiedAdded on 2020/07/22

|16

|5194

|972

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within an organization like Unilever. It delves into various management accounting systems, emphasizing their role in financial data management and decision-making. The report explores different methods of management accounting reporting, including budget reporting, job cost reports, and income statements, highlighting their significance in assessing financial performance. It analyzes marginal and absorption costing methodologies, presenting income statements using both approaches. Furthermore, the report examines the advantages and disadvantages of planning tools used for budgetary control and evaluates how organizations adapt management accounting systems to address financial challenges. The content includes a detailed analysis of costing methods, reporting techniques, and their impact on financial outcomes, supported by practical examples and financial data.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explain management accounting and essential requirements of different types of

management accounting system..................................................................................................1

P.2. Explain different method used for management accounting reporting................................3

TASK 2............................................................................................................................................5

P.3.income statements using marginal and absorption costing methodologies..........................5

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control........................................................................................................................7

TASK 4..........................................................................................................................................10

P.5. Evaluate how organisations are adopting management accounting systems to respond to

financial problems.....................................................................................................................10

References................................................................................................................................ 13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explain management accounting and essential requirements of different types of

management accounting system..................................................................................................1

P.2. Explain different method used for management accounting reporting................................3

TASK 2............................................................................................................................................5

P.3.income statements using marginal and absorption costing methodologies..........................5

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control........................................................................................................................7

TASK 4..........................................................................................................................................10

P.5. Evaluate how organisations are adopting management accounting systems to respond to

financial problems.....................................................................................................................10

References................................................................................................................................ 13

INTRODUCTION

In this assignment, this study review about numbers of management accounting systems

which can assist the Unilever organisation in order to make their issues in more efficient form.

Moreover, this assignment review about difference method of management accounting reporting

which can help the Unilever company in respect to formation of appropriate reporting within the

firm in context of relevant planning of budgeting in appropriate form. Furthermore, this

investigation refer to some of effective marginal and absorption costing method by which

organisation can estimate some areas in which they are needed to make proper improvement.

Furthermore, it is also concluded that some management accounting systems which can be used

in proper respond of financial issues within the organisation in more effective manner. This

study also describe about to several budgeting approaches which can be used by the businesses

in order to proper development of budget in the organisation to proper planning of all financial

activities in sufficient form in context of achievement of organisational goals and objectives

efficiently.

TASK 1

P.1. Explain management accounting and essential requirements of different types of

management accounting system

In each organisation, management accounting plays very crucial role in order to

effectively manage financial data within the firm and it helps accounting manager in terms of

furnishing sufficient information regarding the company’s financial performances on yearly and

quarterly basis which could aid them to make proper decision regarding financial risk control

plus minimise the cost of production at the workplace effectively (Leitner, 2013). With the

assistance of management accounting tools and techniques, the manager of Unilever Company

can effectively manage their operational strategies, resources and customers plus costs as well.

Management accounting is a process in which management employees of the company can

analyse business critical data concerning the financial positioning of the business effectively.

Management accounting system consists of some essential financial data which can lead to high

financial performance of the company.

Cost accounting system: This is also called product costing system, a cost accounting

system is methodology which is utilised for analysing the cost of product and services in order to

have estimation of profitability, know about the inventory costing values in the firm and

1

In this assignment, this study review about numbers of management accounting systems

which can assist the Unilever organisation in order to make their issues in more efficient form.

Moreover, this assignment review about difference method of management accounting reporting

which can help the Unilever company in respect to formation of appropriate reporting within the

firm in context of relevant planning of budgeting in appropriate form. Furthermore, this

investigation refer to some of effective marginal and absorption costing method by which

organisation can estimate some areas in which they are needed to make proper improvement.

Furthermore, it is also concluded that some management accounting systems which can be used

in proper respond of financial issues within the organisation in more effective manner. This

study also describe about to several budgeting approaches which can be used by the businesses

in order to proper development of budget in the organisation to proper planning of all financial

activities in sufficient form in context of achievement of organisational goals and objectives

efficiently.

TASK 1

P.1. Explain management accounting and essential requirements of different types of

management accounting system

In each organisation, management accounting plays very crucial role in order to

effectively manage financial data within the firm and it helps accounting manager in terms of

furnishing sufficient information regarding the company’s financial performances on yearly and

quarterly basis which could aid them to make proper decision regarding financial risk control

plus minimise the cost of production at the workplace effectively (Leitner, 2013). With the

assistance of management accounting tools and techniques, the manager of Unilever Company

can effectively manage their operational strategies, resources and customers plus costs as well.

Management accounting is a process in which management employees of the company can

analyse business critical data concerning the financial positioning of the business effectively.

Management accounting system consists of some essential financial data which can lead to high

financial performance of the company.

Cost accounting system: This is also called product costing system, a cost accounting

system is methodology which is utilised for analysing the cost of product and services in order to

have estimation of profitability, know about the inventory costing values in the firm and

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

effective cost control in manufacturing process as well. According to this process, as a Junior

Account Manager in Unilever Company I need to estimate that which of your product is

profitable for the organisation and which is not. There are main tow kinds of cost accounting

which can be used in the organisation which is job order costing and process costing, Several

kinds of food and house hold products are manufacturing by the companies at their pant so they

need to utilise job costing approach at the workplace in terms of reduce the rate of production

within the organisation efficiently (Qu, Cooper and Ezzamel, 2010).

M.1. Benefits of management accounting system: This is a process in which Unilever

company need to calculate organisation's cost of production by involving the company's

expenses each stage of production and some of fixed expensed inclusion within the firm which

furnish overall values of cost accounting system for the business production level.

Job accounting system: Job accounting is an approach in which each job which is being

done at manufacturing level is estimated and calculated within the firm with the help of job

accounting system at the workplace in order to reduce the cost of each of their job stage expenses

at manufacturing plan efficiently. In case of job order costing method, accounting manager of

Unilever could estimate manufacture costing specifically to their each job has been done in the

organisation which furnishes each unique product costing rate efficiently and according to its

techniques, they can better manage each job costing rate at the workplace (Otley and Emmanuel,

2013). This is an approach which is used by Unilever when they produce different household and

food products within the firm.

M.1. Benefits of management accounting system: This accounting system give benefits

the company from Job costing approach furnishes the value in which the accounting manager of

the company need to formulate a proper job costing system of each job which is being done in

their different-different types of product, services and according to job costing accounting

system, they can minimise the cost of their each job which is being completed at manufacturing

plan, and decrease the rate of production at each job cost level within the organisation efficiently.

Process costing system: This is an approach which is utilised in the cost accounting

system, this process defines about the method in which various kinds of manufacturing costs are

associated and cost of unit production is estimated by accounting manager of Unilever in order to

have proper formation of their issues in efficient form. Apart from it, process costing refer to the

process in which each process costing estimated within the firm effectively and according to the

2

Account Manager in Unilever Company I need to estimate that which of your product is

profitable for the organisation and which is not. There are main tow kinds of cost accounting

which can be used in the organisation which is job order costing and process costing, Several

kinds of food and house hold products are manufacturing by the companies at their pant so they

need to utilise job costing approach at the workplace in terms of reduce the rate of production

within the organisation efficiently (Qu, Cooper and Ezzamel, 2010).

M.1. Benefits of management accounting system: This is a process in which Unilever

company need to calculate organisation's cost of production by involving the company's

expenses each stage of production and some of fixed expensed inclusion within the firm which

furnish overall values of cost accounting system for the business production level.

Job accounting system: Job accounting is an approach in which each job which is being

done at manufacturing level is estimated and calculated within the firm with the help of job

accounting system at the workplace in order to reduce the cost of each of their job stage expenses

at manufacturing plan efficiently. In case of job order costing method, accounting manager of

Unilever could estimate manufacture costing specifically to their each job has been done in the

organisation which furnishes each unique product costing rate efficiently and according to its

techniques, they can better manage each job costing rate at the workplace (Otley and Emmanuel,

2013). This is an approach which is used by Unilever when they produce different household and

food products within the firm.

M.1. Benefits of management accounting system: This accounting system give benefits

the company from Job costing approach furnishes the value in which the accounting manager of

the company need to formulate a proper job costing system of each job which is being done in

their different-different types of product, services and according to job costing accounting

system, they can minimise the cost of their each job which is being completed at manufacturing

plan, and decrease the rate of production at each job cost level within the organisation efficiently.

Process costing system: This is an approach which is utilised in the cost accounting

system, this process defines about the method in which various kinds of manufacturing costs are

associated and cost of unit production is estimated by accounting manager of Unilever in order to

have proper formation of their issues in efficient form. Apart from it, process costing refer to the

process in which each process costing estimated within the firm effectively and according to the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tools of cost accounting, Unilever company's manager can develop costing in which each of their

process costing rate can be minimised efficiently (Harris and Mongiello, 2012). In this process,

accounting manager need to estimate a production unit level and also make collection of several

production process until the output process gain. At manufacturing pant there are several

processes cost ii needed to be calculated efficiently which is total cost per process, unit cost per

processes etc.

M.1. Benefits of management accounting system: This management approach gives

benefits for the organisation at the ending stage of the production process the company's manager

can effectively estimate the unit production cost and with the help of tools and techniques of

process costing, accounting manager of Unilever firm can make decision in order to minimise

process costing rate. With the assistance of this approach, the manager of the company can easily

reduce the cost of production and increase profitability in the industry.

P.2. Explain different method used for management accounting reporting

Management accounting is a most vital part for manufacturing company, in case of

Unilever company, there are various kinds of reporting system are presented here in context of

formation of effective reporting to the business so that expected financial outcomes can be

gained by the business efficiently. With the assistance of reporting system, several kinds of

financial performance of Unilever company measured effectively.

There are various types of management accounting reporting as below:

Budget reporting: Several kinds of business financial fluctuation are being done in the

business in order to run business practices effectively on daily basis. Various financial status and

income and expenses statements and financial data changing rapidly within the organisation

effectively. Financial data and budget reporting is recoded at regular basis at the workplace by its

accounting manager efficiently (Hyvönen, 2010). Moreover, it is a financial statement in which

deep detailed of financial data is recorded in budget reporting system effectively. Accounting

manager of Unilever Company also need to make it in proper brief and easy way at the

workplace. This decision of making budget reporting also makes formation of their issues in

more efficient manner in order to proper development of their issues in more effective manner.

This decision of preparing budget reporting also affects the overall performances of the reporting

efficiently. Apart from it, it can be in different-different forma according to the financial need

and information available for the business effectively. In this budget reporting of Unilever

3

process costing rate can be minimised efficiently (Harris and Mongiello, 2012). In this process,

accounting manager need to estimate a production unit level and also make collection of several

production process until the output process gain. At manufacturing pant there are several

processes cost ii needed to be calculated efficiently which is total cost per process, unit cost per

processes etc.

M.1. Benefits of management accounting system: This management approach gives

benefits for the organisation at the ending stage of the production process the company's manager

can effectively estimate the unit production cost and with the help of tools and techniques of

process costing, accounting manager of Unilever firm can make decision in order to minimise

process costing rate. With the assistance of this approach, the manager of the company can easily

reduce the cost of production and increase profitability in the industry.

P.2. Explain different method used for management accounting reporting

Management accounting is a most vital part for manufacturing company, in case of

Unilever company, there are various kinds of reporting system are presented here in context of

formation of effective reporting to the business so that expected financial outcomes can be

gained by the business efficiently. With the assistance of reporting system, several kinds of

financial performance of Unilever company measured effectively.

There are various types of management accounting reporting as below:

Budget reporting: Several kinds of business financial fluctuation are being done in the

business in order to run business practices effectively on daily basis. Various financial status and

income and expenses statements and financial data changing rapidly within the organisation

effectively. Financial data and budget reporting is recoded at regular basis at the workplace by its

accounting manager efficiently (Hyvönen, 2010). Moreover, it is a financial statement in which

deep detailed of financial data is recorded in budget reporting system effectively. Accounting

manager of Unilever Company also need to make it in proper brief and easy way at the

workplace. This decision of making budget reporting also makes formation of their issues in

more efficient manner in order to proper development of their issues in more effective manner.

This decision of preparing budget reporting also affects the overall performances of the reporting

efficiently. Apart from it, it can be in different-different forma according to the financial need

and information available for the business effectively. In this budget reporting of Unilever

3

company also inclusion of general incomes of the company and sales data, fixed collection of the

data and net worth of the entire organisation in their common section of the budget reporting.

Two types of section entered in this reporting which is assets and liabilities. This is mainly

formulated by accounting manager at once time in smaller business and for big organisations, it

is needed to formulation in several times in order to examine financial expenses which are

known as quarterly reports. This is mostly used for the business plan and projection within the

firm effectively in order to accomplishment of Unilever firm's goals and objective efficiently.

Job cost report: It is an estimation of expenses and costs within the organisation. In job

costing report, you need to develop job costing by estimating each job in your manufacturing

plant is being done properly and make them specific form at the equal cost category so that

actual job costing can be utilised by accounting manager in this form. Moreover, it is a financial

reporting process in which several kinds of financial reporting data gathered (Amoako, 2013).

This is a report in which each job costing is listed by accounting manager in order to examine

accurate job cost on each of their job at manufacturing plant. Various kinds of job costing

included in this process which is Labour cost, material costs and filed overhead costs and

liquidated damages cost is included mainly in the job cost reporting. In case of Unilever

company, various kinds of job being done at their production plant so that company's accounting

manager need manage each jobs and according to their expenses add all expenses, manager of

company can easily identify each over job costing expenses within the firm and according to

them they can minimise the expenses on the job costing and increase the profitability of the

business efficiently.

Income statement: This is statement which is concerned about to the financial statement

that defines about the company's financial performances effectively during particular accounting

time period within the firm. Moreover, financial performances can be assessed with the help of

income statements in which Unilever company's accounting manager can easily examine that

which is part of their business operation if giving more revenue for the business and which

section of the business are making loss for the business (Moser, 2012). It could be analysed by

seeing the financial statements at regular basis by accounting manager of the company. It is

mainly used for to know about to the net profit and loss occurred in the business in particular

given financial time period in the industry. According to the information by income statement

about operating and non-operating activities in the firm, accounting manager of the enterprise

4

data and net worth of the entire organisation in their common section of the budget reporting.

Two types of section entered in this reporting which is assets and liabilities. This is mainly

formulated by accounting manager at once time in smaller business and for big organisations, it

is needed to formulation in several times in order to examine financial expenses which are

known as quarterly reports. This is mostly used for the business plan and projection within the

firm effectively in order to accomplishment of Unilever firm's goals and objective efficiently.

Job cost report: It is an estimation of expenses and costs within the organisation. In job

costing report, you need to develop job costing by estimating each job in your manufacturing

plant is being done properly and make them specific form at the equal cost category so that

actual job costing can be utilised by accounting manager in this form. Moreover, it is a financial

reporting process in which several kinds of financial reporting data gathered (Amoako, 2013).

This is a report in which each job costing is listed by accounting manager in order to examine

accurate job cost on each of their job at manufacturing plant. Various kinds of job costing

included in this process which is Labour cost, material costs and filed overhead costs and

liquidated damages cost is included mainly in the job cost reporting. In case of Unilever

company, various kinds of job being done at their production plant so that company's accounting

manager need manage each jobs and according to their expenses add all expenses, manager of

company can easily identify each over job costing expenses within the firm and according to

them they can minimise the expenses on the job costing and increase the profitability of the

business efficiently.

Income statement: This is statement which is concerned about to the financial statement

that defines about the company's financial performances effectively during particular accounting

time period within the firm. Moreover, financial performances can be assessed with the help of

income statements in which Unilever company's accounting manager can easily examine that

which is part of their business operation if giving more revenue for the business and which

section of the business are making loss for the business (Moser, 2012). It could be analysed by

seeing the financial statements at regular basis by accounting manager of the company. It is

mainly used for to know about to the net profit and loss occurred in the business in particular

given financial time period in the industry. According to the information by income statement

about operating and non-operating activities in the firm, accounting manager of the enterprise

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

could analyse that which part of their business is making more losses. In accordance with

analytical information, they need to make decision with the help of management accounting tools

to improve financial performance of the business effectively and increase the profitability of the

firm efficiently within the organisation.

TASK 2

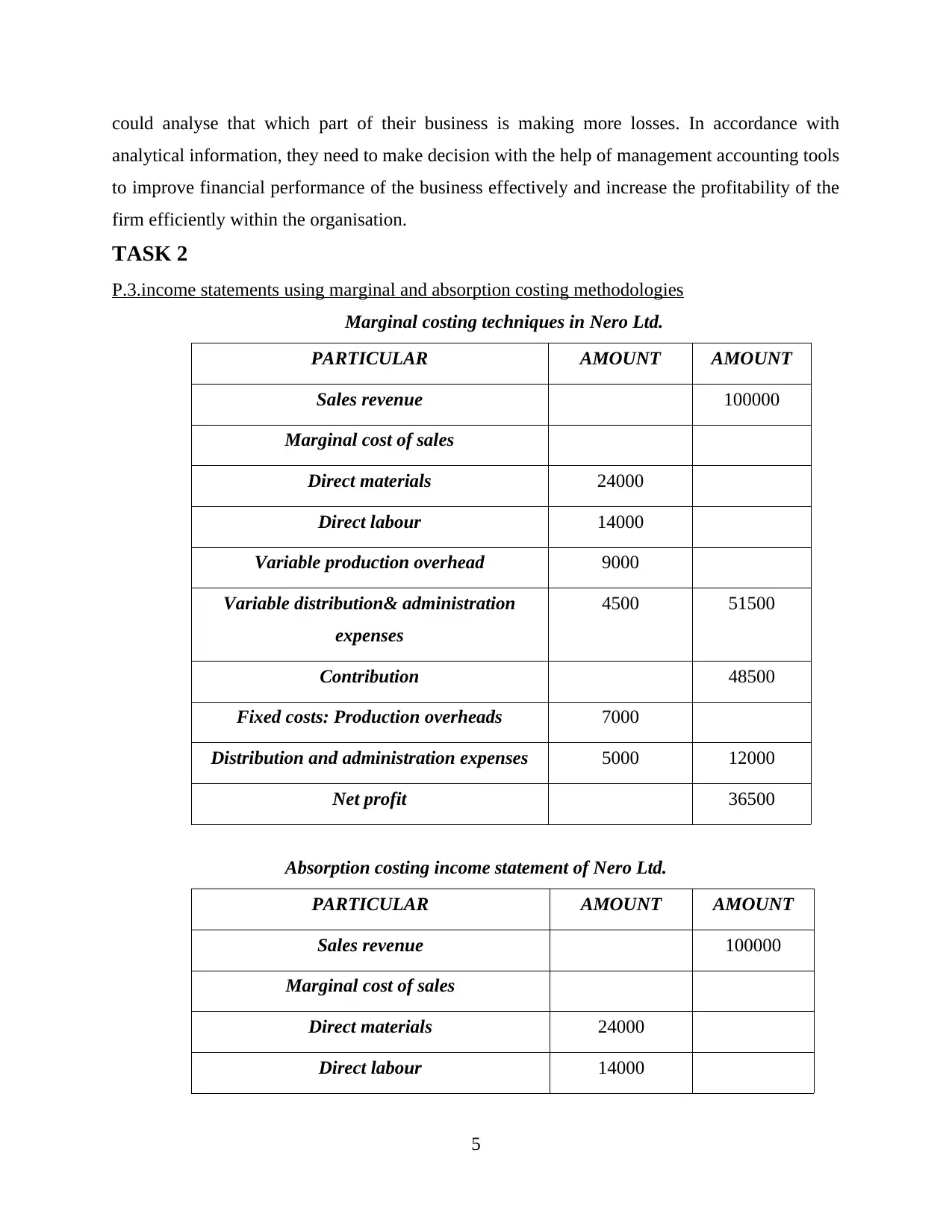

P.3.income statements using marginal and absorption costing methodologies

Marginal costing techniques in Nero Ltd.

PARTICULAR AMOUNT AMOUNT

Sales revenue 100000

Marginal cost of sales

Direct materials 24000

Direct labour 14000

Variable production overhead 9000

Variable distribution& administration

expenses

4500 51500

Contribution 48500

Fixed costs: Production overheads 7000

Distribution and administration expenses 5000 12000

Net profit 36500

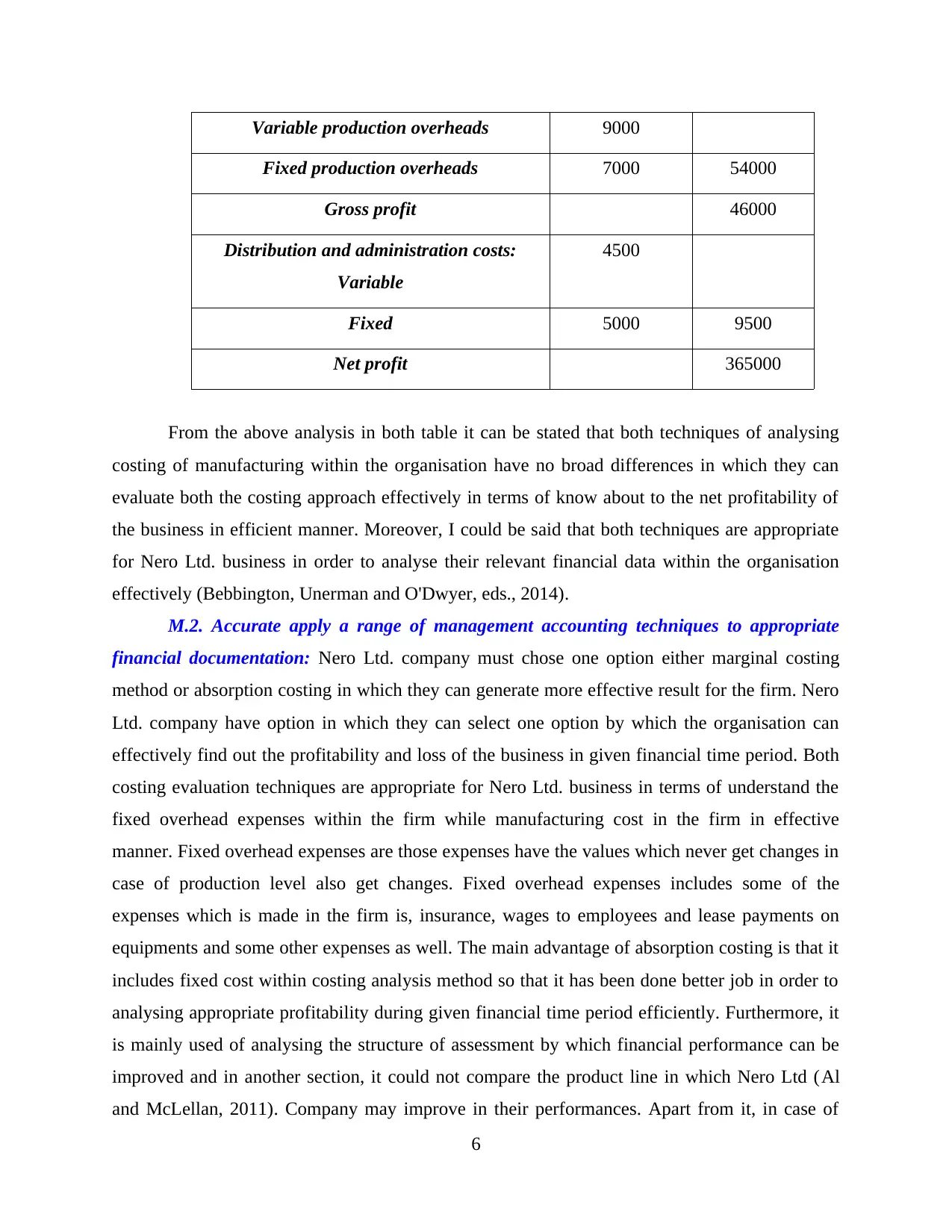

Absorption costing income statement of Nero Ltd.

PARTICULAR AMOUNT AMOUNT

Sales revenue 100000

Marginal cost of sales

Direct materials 24000

Direct labour 14000

5

analytical information, they need to make decision with the help of management accounting tools

to improve financial performance of the business effectively and increase the profitability of the

firm efficiently within the organisation.

TASK 2

P.3.income statements using marginal and absorption costing methodologies

Marginal costing techniques in Nero Ltd.

PARTICULAR AMOUNT AMOUNT

Sales revenue 100000

Marginal cost of sales

Direct materials 24000

Direct labour 14000

Variable production overhead 9000

Variable distribution& administration

expenses

4500 51500

Contribution 48500

Fixed costs: Production overheads 7000

Distribution and administration expenses 5000 12000

Net profit 36500

Absorption costing income statement of Nero Ltd.

PARTICULAR AMOUNT AMOUNT

Sales revenue 100000

Marginal cost of sales

Direct materials 24000

Direct labour 14000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable production overheads 9000

Fixed production overheads 7000 54000

Gross profit 46000

Distribution and administration costs:

Variable

4500

Fixed 5000 9500

Net profit 365000

From the above analysis in both table it can be stated that both techniques of analysing

costing of manufacturing within the organisation have no broad differences in which they can

evaluate both the costing approach effectively in terms of know about to the net profitability of

the business in efficient manner. Moreover, I could be said that both techniques are appropriate

for Nero Ltd. business in order to analyse their relevant financial data within the organisation

effectively (Bebbington, Unerman and O'Dwyer, eds., 2014).

M.2. Accurate apply a range of management accounting techniques to appropriate

financial documentation: Nero Ltd. company must chose one option either marginal costing

method or absorption costing in which they can generate more effective result for the firm. Nero

Ltd. company have option in which they can select one option by which the organisation can

effectively find out the profitability and loss of the business in given financial time period. Both

costing evaluation techniques are appropriate for Nero Ltd. business in terms of understand the

fixed overhead expenses within the firm while manufacturing cost in the firm in effective

manner. Fixed overhead expenses are those expenses have the values which never get changes in

case of production level also get changes. Fixed overhead expenses includes some of the

expenses which is made in the firm is, insurance, wages to employees and lease payments on

equipments and some other expenses as well. The main advantage of absorption costing is that it

includes fixed cost within costing analysis method so that it has been done better job in order to

analysing appropriate profitability during given financial time period efficiently. Furthermore, it

is mainly used of analysing the structure of assessment by which financial performance can be

improved and in another section, it could not compare the product line in which Nero Ltd (Al

and McLellan, 2011). Company may improve in their performances. Apart from it, in case of

6

Fixed production overheads 7000 54000

Gross profit 46000

Distribution and administration costs:

Variable

4500

Fixed 5000 9500

Net profit 365000

From the above analysis in both table it can be stated that both techniques of analysing

costing of manufacturing within the organisation have no broad differences in which they can

evaluate both the costing approach effectively in terms of know about to the net profitability of

the business in efficient manner. Moreover, I could be said that both techniques are appropriate

for Nero Ltd. business in order to analyse their relevant financial data within the organisation

effectively (Bebbington, Unerman and O'Dwyer, eds., 2014).

M.2. Accurate apply a range of management accounting techniques to appropriate

financial documentation: Nero Ltd. company must chose one option either marginal costing

method or absorption costing in which they can generate more effective result for the firm. Nero

Ltd. company have option in which they can select one option by which the organisation can

effectively find out the profitability and loss of the business in given financial time period. Both

costing evaluation techniques are appropriate for Nero Ltd. business in terms of understand the

fixed overhead expenses within the firm while manufacturing cost in the firm in effective

manner. Fixed overhead expenses are those expenses have the values which never get changes in

case of production level also get changes. Fixed overhead expenses includes some of the

expenses which is made in the firm is, insurance, wages to employees and lease payments on

equipments and some other expenses as well. The main advantage of absorption costing is that it

includes fixed cost within costing analysis method so that it has been done better job in order to

analysing appropriate profitability during given financial time period efficiently. Furthermore, it

is mainly used of analysing the structure of assessment by which financial performance can be

improved and in another section, it could not compare the product line in which Nero Ltd (Al

and McLellan, 2011). Company may improve in their performances. Apart from it, in case of

6

marginal costing, it is also the best alternative for Nero Ltd. organisation in order to analysing of

their costing within the firm in more effective manner. In terms of marginal costing method

variable costing in included in terms of generating income statement to know about to the net

profitability of the business in efficient form. Marginal costing is very easy to implement on the

business because of fixed costs are not included in this approach. This process in which

marginal costing mechanism could be associated with standard costing method within the

organisation in order to know sufficient profit and loss statements about to the organisation

efficiently. Marginal and absorption both techniques are appropriate for Nero Ltd. business in

order to analyse their quarterly basis financial progress and its information also help accounting

manager of enterprise in respect to make decision towards organisational profitability and

improvement in financial growth within the food industry sufficiently.

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control

Various types of planing tools can be used in order to effective budget control within the

firm effectively in order to gain financial growth in the market in more efficient form. Several

kinds of tools and techniques could be used by Nero Ltd. company's accounting manager in

terms of gaining proper development of budget in the business in order to gain future expected

growth in the market efficiently.

Cash budget: This is a most appropriate method of formation of budget within the

organisation. In the case budgeting accounting manager of Nero Ltd. need to estimate the cash

inflows and outflows of the enterprise during the given period time. It is helpful to know bout to

sufficient remain budget for the organisation in respect to relevant running of operational

activities within the firm effectively (Suomala and Lyly-Yrjänäinen, 2012). In context of

formation of cash budgeting, accounting manager of the company need to forecast about sales

and production level in the firm in given period and according to them make cash budgeting in

the business efficiently. Its furnish the information by which company get to know about to

available balance within the company in order to efficient run of business activities sufficiently.

Advantages of cash budgeting:

Cash budgeting make help the company's manager to identify those planned section

within the business which is not operating in the business according to their expectation.

According to them manager can improve in those areas (Kokubu and Kitada, 2015).

7

their costing within the firm in more effective manner. In terms of marginal costing method

variable costing in included in terms of generating income statement to know about to the net

profitability of the business in efficient form. Marginal costing is very easy to implement on the

business because of fixed costs are not included in this approach. This process in which

marginal costing mechanism could be associated with standard costing method within the

organisation in order to know sufficient profit and loss statements about to the organisation

efficiently. Marginal and absorption both techniques are appropriate for Nero Ltd. business in

order to analyse their quarterly basis financial progress and its information also help accounting

manager of enterprise in respect to make decision towards organisational profitability and

improvement in financial growth within the food industry sufficiently.

P.4. Explain the advantage and disadvantage of different types of planning tools used for

budgetary control

Various types of planing tools can be used in order to effective budget control within the

firm effectively in order to gain financial growth in the market in more efficient form. Several

kinds of tools and techniques could be used by Nero Ltd. company's accounting manager in

terms of gaining proper development of budget in the business in order to gain future expected

growth in the market efficiently.

Cash budget: This is a most appropriate method of formation of budget within the

organisation. In the case budgeting accounting manager of Nero Ltd. need to estimate the cash

inflows and outflows of the enterprise during the given period time. It is helpful to know bout to

sufficient remain budget for the organisation in respect to relevant running of operational

activities within the firm effectively (Suomala and Lyly-Yrjänäinen, 2012). In context of

formation of cash budgeting, accounting manager of the company need to forecast about sales

and production level in the firm in given period and according to them make cash budgeting in

the business efficiently. Its furnish the information by which company get to know about to

available balance within the company in order to efficient run of business activities sufficiently.

Advantages of cash budgeting:

Cash budgeting make help the company's manager to identify those planned section

within the business which is not operating in the business according to their expectation.

According to them manager can improve in those areas (Kokubu and Kitada, 2015).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Main advantage of cash budgeting is that it helps to manager to focus on the things in

which financial improvement can be gained more effectively. A cash budgeting can be useful for the making some of effective services in which they

can generate more efficient services in more effective manner.

Disadvantage of cash budgeting:

It is totally made on estimation on the firm in which they can generate cash budgeting on

proper estimation and most of the time budget can not be performed according to

forecasting on the business effectively (Burritt and et.al., 2011). It needs high cost to prepare within the organisation in terms of set of financial goals

within the business effectively.

Fixed budgeting: This is a budgeting approach which get never changed in the

organisation in given time period. This is a budget system which never change in every situation

in the business effectively whether sales and production level of the business increase or

decrease frequently (Abdel-Kader, ed., 2011). Nero Ltd. company's accounting manager need to

develop fixed budgeting system in the organisation in order to improvement in financial issues in

effective form in the firm. Large amount of dealing companies mostly use of this type of budget

in order to get actual budgeted outcomes from the organisation.

Advantage of fixed budgeting:

The major advantage of this budgeting is that it helps the manager to keep production

cost down in that range in which each of their customer can get afford.

Another main advantage of this budget is that it is easy to formulate within the firm and

there is no need to regular update in this kind of budgeting. It assists the manager to evaluate the budget at short terms and long term both level in

order to know that which of the cost line in the organisation is gong to overhead in the

firm.

Disadvantage of fixed budgeting:

The biggest disadvantage of fixed budgeting is that it has less flexibility and it never

changes in business envelopment, and most of the time manager need to change in their

budgeting planning according to the situation (Hopper and Bui, 2016).

If the company can find out the under-forming field within the business so that manager

can not take action to utilisation of extra resources towards the business.

8

which financial improvement can be gained more effectively. A cash budgeting can be useful for the making some of effective services in which they

can generate more efficient services in more effective manner.

Disadvantage of cash budgeting:

It is totally made on estimation on the firm in which they can generate cash budgeting on

proper estimation and most of the time budget can not be performed according to

forecasting on the business effectively (Burritt and et.al., 2011). It needs high cost to prepare within the organisation in terms of set of financial goals

within the business effectively.

Fixed budgeting: This is a budgeting approach which get never changed in the

organisation in given time period. This is a budget system which never change in every situation

in the business effectively whether sales and production level of the business increase or

decrease frequently (Abdel-Kader, ed., 2011). Nero Ltd. company's accounting manager need to

develop fixed budgeting system in the organisation in order to improvement in financial issues in

effective form in the firm. Large amount of dealing companies mostly use of this type of budget

in order to get actual budgeted outcomes from the organisation.

Advantage of fixed budgeting:

The major advantage of this budgeting is that it helps the manager to keep production

cost down in that range in which each of their customer can get afford.

Another main advantage of this budget is that it is easy to formulate within the firm and

there is no need to regular update in this kind of budgeting. It assists the manager to evaluate the budget at short terms and long term both level in

order to know that which of the cost line in the organisation is gong to overhead in the

firm.

Disadvantage of fixed budgeting:

The biggest disadvantage of fixed budgeting is that it has less flexibility and it never

changes in business envelopment, and most of the time manager need to change in their

budgeting planning according to the situation (Hopper and Bui, 2016).

If the company can find out the under-forming field within the business so that manager

can not take action to utilisation of extra resources towards the business.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It does not furnish proper guideline in which the manger feel difficulties to complete

them effectively within the business climate.

M.3. Analyse the use of different planning tools and their application for preparing

and forecasting budgets:

Zero base budgeting: Zero based budgeting is the process in which Nero Ltd. business

accounting manager should be recognised the each of their new time period in the organisation

effectively. As it name shows that it starts from the zero base within the organisation and each of

its function is examined with the helps of needs and costs within the organisation effectively.

Advantages of zero base budgeting:

Its tools and techniques help the business accounting manager to make decision regarding

to the cost reduction within the business which furnish accurate value for the organisation

in efficient form (Quinn, 2011).

It terms of resources in the organisation is assessed for the beneficial terms n which they

can use of effective utilisation of resources within the firm effectively. It another advantages if that it makes sure that careful planning within the organisation

efficiently.

Disadvantage of zero cash budgeting:

In terms of large businesses companies, several kinds of effective decision are made

under them and it includes more expenses within the organisation effectively. It generates threatening for organisational accounting manager when they formulate zero

base budgeting.

Capital budgeting method: Capital budgeting is most appropriate alternative for Nero Ltd.

business in order to decision-making method of investing a long term assets for the organisation

in order to formation of some kinds of services in efficient form. These assets are land, building

and essential equipments for the production as well.

Advantage of capital budgeting method:

Capital budgeting assist the business to assume the investment alternatives by which the

company can generate more profitability for the firm (Talha, Raja, and Seetharaman,

2010).

9

them effectively within the business climate.

M.3. Analyse the use of different planning tools and their application for preparing

and forecasting budgets:

Zero base budgeting: Zero based budgeting is the process in which Nero Ltd. business

accounting manager should be recognised the each of their new time period in the organisation

effectively. As it name shows that it starts from the zero base within the organisation and each of

its function is examined with the helps of needs and costs within the organisation effectively.

Advantages of zero base budgeting:

Its tools and techniques help the business accounting manager to make decision regarding

to the cost reduction within the business which furnish accurate value for the organisation

in efficient form (Quinn, 2011).

It terms of resources in the organisation is assessed for the beneficial terms n which they

can use of effective utilisation of resources within the firm effectively. It another advantages if that it makes sure that careful planning within the organisation

efficiently.

Disadvantage of zero cash budgeting:

In terms of large businesses companies, several kinds of effective decision are made

under them and it includes more expenses within the organisation effectively. It generates threatening for organisational accounting manager when they formulate zero

base budgeting.

Capital budgeting method: Capital budgeting is most appropriate alternative for Nero Ltd.

business in order to decision-making method of investing a long term assets for the organisation

in order to formation of some kinds of services in efficient form. These assets are land, building

and essential equipments for the production as well.

Advantage of capital budgeting method:

Capital budgeting assist the business to assume the investment alternatives by which the

company can generate more profitability for the firm (Talha, Raja, and Seetharaman,

2010).

9

Capital budgeting have also main advantage which is, it assists the business to

formulation of long terms strategic investment in order to proper development of their

issues in effective form.

Disadvantage of capital budgeting method:

It helps to make decision for long-term investment in the organisation and which never

get changed in the future. This budgeting process is very expensive for the organisation

in effective form.

This is the techniques, which is totally based on the forecasting and estimation about to

the future which is many of time uncertainty always on expected return on the business.

TASK 4

P.5. Evaluate how organisations are adopting management accounting systems to respond to

financial problems

From last few years, it has been seen that, several kinds of manufacturing companies

facing financial issues within the industry effectively (Waweru, 2010). There are several kinds of

issues which can generate in the financial department in the business and the firm need to

utilisation of some of effective management accounting systems in order to better response of

financial issues within the firm effectively. In case of Nero Ltd. company, it also needs

implementation of management accounting system on the business to effective resolve their

financial issues.

Key performance indicators: Key performance indicators are the tools which helps the

organisation in order to measure effective values that furnish examples of that the business is

accomplishing their objective how effectively within the firm in efficient form. Moreover, Nero

Ltd. organisation use of key performance indicators at the workplace in terms to know about to

their performance in financial sector and other business activities in respect to achieving

organisational goals and targets efficiently. Key performance indicator furnish the values in

which Nero Ltd. business can examine the values in which they can measure their performance

in the industry and make decision to improvement in their financial activities and remove the

barriers and issues which comes in the way of success of the business efficiently. With the help

of KPI tools and techniques Nero Ltd (Lukka and Vinnari, 2014). Organisation can sufficiently

analyse their performance and identify those areas in which they are needed to make efficient

changes and also help in removing their financial issues within the firm in efficient form.

10

formulation of long terms strategic investment in order to proper development of their

issues in effective form.

Disadvantage of capital budgeting method:

It helps to make decision for long-term investment in the organisation and which never

get changed in the future. This budgeting process is very expensive for the organisation

in effective form.

This is the techniques, which is totally based on the forecasting and estimation about to

the future which is many of time uncertainty always on expected return on the business.

TASK 4

P.5. Evaluate how organisations are adopting management accounting systems to respond to

financial problems

From last few years, it has been seen that, several kinds of manufacturing companies

facing financial issues within the industry effectively (Waweru, 2010). There are several kinds of

issues which can generate in the financial department in the business and the firm need to

utilisation of some of effective management accounting systems in order to better response of

financial issues within the firm effectively. In case of Nero Ltd. company, it also needs

implementation of management accounting system on the business to effective resolve their

financial issues.

Key performance indicators: Key performance indicators are the tools which helps the

organisation in order to measure effective values that furnish examples of that the business is

accomplishing their objective how effectively within the firm in efficient form. Moreover, Nero

Ltd. organisation use of key performance indicators at the workplace in terms to know about to

their performance in financial sector and other business activities in respect to achieving

organisational goals and targets efficiently. Key performance indicator furnish the values in

which Nero Ltd. business can examine the values in which they can measure their performance

in the industry and make decision to improvement in their financial activities and remove the

barriers and issues which comes in the way of success of the business efficiently. With the help

of KPI tools and techniques Nero Ltd (Lukka and Vinnari, 2014). Organisation can sufficiently

analyse their performance and identify those areas in which they are needed to make efficient

changes and also help in removing their financial issues within the firm in efficient form.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.