Unit 5: Management Accounting Report - Unilever Analysis

VerifiedAdded on 2022/12/30

|22

|5891

|91

Report

AI Summary

This report delves into the core concepts of management accounting (MA) and its practical applications within organizations, using Unilever as a case study. It outlines how MA is used to identify, measure, and analyze financial information for decision-making, covering both short-term and long-term strategies. The report explores various MA techniques, including product costing, cash flow analysis, constraint analysis, accounts receivable management, trend analysis and forecasting, and inventory turnover analysis. Furthermore, it examines different reporting methods like budgeting, performance analysis, job costing, capital budgeting, inventory and manufacturing reports, pro forma cash flow, sales reports, and item cost reports, along with an explanation of marginal and absorption costing. The report highlights how MA supports financial planning, operational efficiency, and strategic investment decisions, providing a comprehensive understanding of its role in business management.

Unit 5-Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

This study speaks about MA and its concepts used in organisations. MA is the branch of

accounting utilised by accountants to report entries, transactions happening within a fixed period

of time say quarterly or annually. This is for the referral of managers who use it to make short-

term and long-term decisions. It helps business managers to identify, measure, analyse

information and pursue business goals. The company on which study is based is Unilever.

Unilever is a UK based FMCG company catering to home care, beauty care, personal care and

foods and refreshment category products. The study also summarizes the benefits of different

management accounting systems and different methods of reporting used in organisation. The

range of management accounting techniques with reference to different types of costing have

been explained. The forecasting tools used in MA have been explained and the methods in which

organisation uses MA techniques to respond to financial issues have emphasised.

MAIN BODY

MA and its different forms

Management accounting is framework of identifying, to analyse, to interpret and

communication of information to mangers in which entries of transactions is recorded for a

period. The system helps managers make investment decisions regarding short-term and long-

term basis. It informs business about cost of goods and services purchased during a period,

financial planning to be made and performance of various sections according to the budget

allotted. The different types and benefits of management accounting are as follows:

a) Product Costing: This technique involves calculation of product's cost per unit and then

fixing the price at a profit margin. In manufacturing, many different costs like procurement of

raw material, fixed costs, its overheads, variable costs and its overheads are taken in account till

the production has ended. The total units produced is divided by summation for all cost to reach

out cost / unit of the units produced (Ameen, Ahmed and Abd Hafez, 2018).

Clift Joinery calculates its overall production cost as its operations are widely

distributed and the process involves a number of costs to be computed. The company is then able

This study speaks about MA and its concepts used in organisations. MA is the branch of

accounting utilised by accountants to report entries, transactions happening within a fixed period

of time say quarterly or annually. This is for the referral of managers who use it to make short-

term and long-term decisions. It helps business managers to identify, measure, analyse

information and pursue business goals. The company on which study is based is Unilever.

Unilever is a UK based FMCG company catering to home care, beauty care, personal care and

foods and refreshment category products. The study also summarizes the benefits of different

management accounting systems and different methods of reporting used in organisation. The

range of management accounting techniques with reference to different types of costing have

been explained. The forecasting tools used in MA have been explained and the methods in which

organisation uses MA techniques to respond to financial issues have emphasised.

MAIN BODY

MA and its different forms

Management accounting is framework of identifying, to analyse, to interpret and

communication of information to mangers in which entries of transactions is recorded for a

period. The system helps managers make investment decisions regarding short-term and long-

term basis. It informs business about cost of goods and services purchased during a period,

financial planning to be made and performance of various sections according to the budget

allotted. The different types and benefits of management accounting are as follows:

a) Product Costing: This technique involves calculation of product's cost per unit and then

fixing the price at a profit margin. In manufacturing, many different costs like procurement of

raw material, fixed costs, its overheads, variable costs and its overheads are taken in account till

the production has ended. The total units produced is divided by summation for all cost to reach

out cost / unit of the units produced (Ameen, Ahmed and Abd Hafez, 2018).

Clift Joinery calculates its overall production cost as its operations are widely

distributed and the process involves a number of costs to be computed. The company is then able

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to ascertain the price of products by setting a profit margin which is in consideration with market

prices.

This technique thus helps in accurate determining of the products and cost computing.

b) Cash flow analysis: Business decisions and their implementation involve cash inflow and

outflow on investment in a project. The manager will require the information of the financial

impact of the transactions taking place. For e.g. company planning to buy an equipment can do it

either by purchasing through company capital or by using debt in form of a bank loan. The

outcomes in form of cash flows regarding purchase using both options will be weighed and the

more profitable investment will be given nod (Abdusalomova, 2019).

Clift joinery uses the method to make investments while diversifying wooden products

as to the costs involved and the optimization of cash flow to be achieved and maintain the

working capital.

c) Constraint Analysis: Management accounting here helps in identifying the constraints which

may be coming in production or sales process. This helps in identifying the bottlenecks which

may be occurring in the process and the impact they are having on revenue and cash flow.

Managers thus think of suitable measures to help in eradication of bottlenecks and improve

efficiencies in the process (Ameen, Ahmed and Abd Hafez, 2018).

Clift Joinery uses constraint analysis to overcome constraints in production process. For

e.g. company taking key widgets in production from only one supplier who may be operating at

its full operational capacity can be a bottleneck as it may happen due to circumstances supplier is

not able to reach company's increasing order. Hence, management will have to increase suppliers

in this group and consider its additional cost for future returns.

d) Accounts Receivable Management: The company categorizes its account receivables i.e.

money pending from its debtors according to time length such as 30 days, 30+ days, more than

60 days etc. Management accounting categorises these by the period of time they are

outstanding. The faster the company is able to receive the credit, the better it is for the

company's working capital. It can also help in realising whether the company requires to do a

change in credit policy if there are many defaulters.

prices.

This technique thus helps in accurate determining of the products and cost computing.

b) Cash flow analysis: Business decisions and their implementation involve cash inflow and

outflow on investment in a project. The manager will require the information of the financial

impact of the transactions taking place. For e.g. company planning to buy an equipment can do it

either by purchasing through company capital or by using debt in form of a bank loan. The

outcomes in form of cash flows regarding purchase using both options will be weighed and the

more profitable investment will be given nod (Abdusalomova, 2019).

Clift joinery uses the method to make investments while diversifying wooden products

as to the costs involved and the optimization of cash flow to be achieved and maintain the

working capital.

c) Constraint Analysis: Management accounting here helps in identifying the constraints which

may be coming in production or sales process. This helps in identifying the bottlenecks which

may be occurring in the process and the impact they are having on revenue and cash flow.

Managers thus think of suitable measures to help in eradication of bottlenecks and improve

efficiencies in the process (Ameen, Ahmed and Abd Hafez, 2018).

Clift Joinery uses constraint analysis to overcome constraints in production process. For

e.g. company taking key widgets in production from only one supplier who may be operating at

its full operational capacity can be a bottleneck as it may happen due to circumstances supplier is

not able to reach company's increasing order. Hence, management will have to increase suppliers

in this group and consider its additional cost for future returns.

d) Accounts Receivable Management: The company categorizes its account receivables i.e.

money pending from its debtors according to time length such as 30 days, 30+ days, more than

60 days etc. Management accounting categorises these by the period of time they are

outstanding. The faster the company is able to receive the credit, the better it is for the

company's working capital. It can also help in realising whether the company requires to do a

change in credit policy if there are many defaulters.

Clift Joinery records its account receivables according to length period of time and has

been able to speed up its recovery process for smooth functioning of its operations.

e) Trend analysis and Forecasting: This type of management accounting helps in making

decisions about future faring of the organisation. The upcoming market trends which affect the

organisation are considered and accordingly, financial planning is done for investment in general

and administrative expenses, operational expenses and capital expenditure in various

departments and forecasts are done for the company's future sales to occur.

Clift Joinery has benefited by doing financial planning for its upcoming expenses in

advance and channelising its investments according to trend analysis and forecast methods

estimations (Abdusalomova, 2019).

f) Inventory Turnover Analysis: This approach of management accounting focuses on how

efficiently a company is able to manage its inventory and how fast the inventory is sold and

replaced. This helps company to plan its order in advance for its next purchase of inventory.

Optimum utilisation of inventory is when the storage cost of inventory does not start affecting

the cash flow and does not bind capital for long. This method also helps in defining Economic

Order quantity for the company and reduce excessive storage costs (Alborov and et.al., 2017).

Clift Joinery has been able to do its Economic Order Quantity and has been able to

maintain the storage costs under control. This has ensured optimal utilisation of inventory as

well as the free up of cash for company's operations.

Different methods of management accounting reporting

The methods used for reporting management accounting are:

Budgeting: Every company has its own list of income and expenses in various departments. A

channelised statement which can record money going in these transactions and the amount of

money required in excess to complete the operations comes in the form of budgeting.

Management accounting takes in consideration the financial statements of previous years and

accordingly judges the expenditure department wise. This leads to categorisation of the budget

and is easy to administer. The requirements of the department in future considering time period

of one year is taken in consideration and accordingly finance is allotted under which the

department has to achi MA has supported eve its goals without exceeding the budget. Similarly,

been able to speed up its recovery process for smooth functioning of its operations.

e) Trend analysis and Forecasting: This type of management accounting helps in making

decisions about future faring of the organisation. The upcoming market trends which affect the

organisation are considered and accordingly, financial planning is done for investment in general

and administrative expenses, operational expenses and capital expenditure in various

departments and forecasts are done for the company's future sales to occur.

Clift Joinery has benefited by doing financial planning for its upcoming expenses in

advance and channelising its investments according to trend analysis and forecast methods

estimations (Abdusalomova, 2019).

f) Inventory Turnover Analysis: This approach of management accounting focuses on how

efficiently a company is able to manage its inventory and how fast the inventory is sold and

replaced. This helps company to plan its order in advance for its next purchase of inventory.

Optimum utilisation of inventory is when the storage cost of inventory does not start affecting

the cash flow and does not bind capital for long. This method also helps in defining Economic

Order quantity for the company and reduce excessive storage costs (Alborov and et.al., 2017).

Clift Joinery has been able to do its Economic Order Quantity and has been able to

maintain the storage costs under control. This has ensured optimal utilisation of inventory as

well as the free up of cash for company's operations.

Different methods of management accounting reporting

The methods used for reporting management accounting are:

Budgeting: Every company has its own list of income and expenses in various departments. A

channelised statement which can record money going in these transactions and the amount of

money required in excess to complete the operations comes in the form of budgeting.

Management accounting takes in consideration the financial statements of previous years and

accordingly judges the expenditure department wise. This leads to categorisation of the budget

and is easy to administer. The requirements of the department in future considering time period

of one year is taken in consideration and accordingly finance is allotted under which the

department has to achi MA has supported eve its goals without exceeding the budget. Similarly,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

draft is prepared for other departments and company is able to know its investment of capital

over one year on an estimation basis.

Performance Analysis: At the end of the financial year, it is seen how well each department has

performed. This is generally done by a technique known as variance analysis. It is seen whether

the budget allotted to the department has been sufficient to it for reaching the goals set or

whether the budget has been exceeded. A favourable result is declared for the department if it is

able to achieve the results within the budget and unfavourable if it has exceeded the budget. The

degree of variance is also examined as to how much company needs to spend more finance on

meeting operational goals (Suprunova,2018).

Job costing: A project a company is currently pursuing although has its own investment analysis

using methods like NPV but to check whether the project is going on profitability bench mark at

present, it is divided in fragments known as job. Job incurs the expenditures and cash flows of

the company and the management is able to decide whether it has been able to cover expenses

and moving towards rate of return or not. If job is experiencing losses, then company may

rethink to continue with the project or not. Various costs involved like procurement of raw

material, fixed expenses, overhead expenses, variable expenses, variable overheads are

calculated and accordingly cash inflow of funds regarding expected revenue is compared to

check the profitability value of the job (Alborov, R.A. and et.al., 2017).

Capital Budgeting: The investment of the company to acquire new machinery or equipment or

to invest in a new project is done by an investment analysis approach. The capital expenditure to

be done in the project and the cash flows which can be expected to come as a return are

estimated. Generally, this is done by using methods like calculating NPV and IRR. Speaking of

NPV, it uses a discount rate for estimation of future cash flows as it takes time value in

consideration. Cash flows arriving in future holds what amount of present value today is gauged

and their total sum is taken minus the expenditure to take out net profitability. IRR, that is

internal rate of return is yet another tool to gauge the profitability of a project which can also be

stated as compounded annual rate of return (Lasyoud, and Alsharari, 2017).

MA has supported

over one year on an estimation basis.

Performance Analysis: At the end of the financial year, it is seen how well each department has

performed. This is generally done by a technique known as variance analysis. It is seen whether

the budget allotted to the department has been sufficient to it for reaching the goals set or

whether the budget has been exceeded. A favourable result is declared for the department if it is

able to achieve the results within the budget and unfavourable if it has exceeded the budget. The

degree of variance is also examined as to how much company needs to spend more finance on

meeting operational goals (Suprunova,2018).

Job costing: A project a company is currently pursuing although has its own investment analysis

using methods like NPV but to check whether the project is going on profitability bench mark at

present, it is divided in fragments known as job. Job incurs the expenditures and cash flows of

the company and the management is able to decide whether it has been able to cover expenses

and moving towards rate of return or not. If job is experiencing losses, then company may

rethink to continue with the project or not. Various costs involved like procurement of raw

material, fixed expenses, overhead expenses, variable expenses, variable overheads are

calculated and accordingly cash inflow of funds regarding expected revenue is compared to

check the profitability value of the job (Alborov, R.A. and et.al., 2017).

Capital Budgeting: The investment of the company to acquire new machinery or equipment or

to invest in a new project is done by an investment analysis approach. The capital expenditure to

be done in the project and the cash flows which can be expected to come as a return are

estimated. Generally, this is done by using methods like calculating NPV and IRR. Speaking of

NPV, it uses a discount rate for estimation of future cash flows as it takes time value in

consideration. Cash flows arriving in future holds what amount of present value today is gauged

and their total sum is taken minus the expenditure to take out net profitability. IRR, that is

internal rate of return is yet another tool to gauge the profitability of a project which can also be

stated as compounded annual rate of return (Lasyoud, and Alsharari, 2017).

MA has supported

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory and manufacturing reports: The inventory costs comprising of storage and

handling inventory, labour cost, overhead costs and wastages which can occur due to damaged

inventory apart from other administrative expenses are all prepared in a report. Also costs

involving direct and indirect expenses in manufacturing are all summarized in form of a report.

This helps to check how much extra expenditure is there and where the company needs to take

measures to reduce operational expenses.

Pro forma cash flow: The money projected to come in short term and medium term accounting

periods and expenditure forecasted is reflected in pro forma cash flow. It shows month by month

summary of cash inflow and outflow, and gives an indication to company when to expect

shortages and when to expect surpluses. As it is usually done on a short-term basis, the chance of

inaccuracies are less (Suprunova, 2018).

Sales Reports: These reports depict the company's performance in its diversified product

range and the method of selling which is more profitable. This lays light on the sources which

are generating higher revenues for the company and which sections need to be improved. The

report also helps in realising which employees are performing well up to the expectations and

which employees need to be motiv This ated to perform better.

Item cost reports: This method reflects the category wise distribution of expenses

involving each type of product. The costs involved such as labour, materials and expenses such

as licenses etc. are shown category wise. Also the sales achieved in that product category is also

calculated. Then the expenditure is reduced from the sales to calculate profit achieved from

category. This break down of costs will help company to realise its operational expenses and

where they can be reduced. Also, it will be able to know the category of products which are

under-performing and need a boost. It can also add on new features to the range of products

which are doing well (Lasyoud and Alsharari, 2017).

Calculation of cost and preparation of income statement from marginal and absorption costing

Meaning of cost: Cost refers to the amount of cash which is spend for getting something

in return. In every business cost is the main matter to be concerned because it must be always as

minimum as possible in order to maximise profits. Companies incur various costs for the

purpose of accomplishment of the end goals. Costs of the any company may include production

handling inventory, labour cost, overhead costs and wastages which can occur due to damaged

inventory apart from other administrative expenses are all prepared in a report. Also costs

involving direct and indirect expenses in manufacturing are all summarized in form of a report.

This helps to check how much extra expenditure is there and where the company needs to take

measures to reduce operational expenses.

Pro forma cash flow: The money projected to come in short term and medium term accounting

periods and expenditure forecasted is reflected in pro forma cash flow. It shows month by month

summary of cash inflow and outflow, and gives an indication to company when to expect

shortages and when to expect surpluses. As it is usually done on a short-term basis, the chance of

inaccuracies are less (Suprunova, 2018).

Sales Reports: These reports depict the company's performance in its diversified product

range and the method of selling which is more profitable. This lays light on the sources which

are generating higher revenues for the company and which sections need to be improved. The

report also helps in realising which employees are performing well up to the expectations and

which employees need to be motiv This ated to perform better.

Item cost reports: This method reflects the category wise distribution of expenses

involving each type of product. The costs involved such as labour, materials and expenses such

as licenses etc. are shown category wise. Also the sales achieved in that product category is also

calculated. Then the expenditure is reduced from the sales to calculate profit achieved from

category. This break down of costs will help company to realise its operational expenses and

where they can be reduced. Also, it will be able to know the category of products which are

under-performing and need a boost. It can also add on new features to the range of products

which are doing well (Lasyoud and Alsharari, 2017).

Calculation of cost and preparation of income statement from marginal and absorption costing

Meaning of cost: Cost refers to the amount of cash which is spend for getting something

in return. In every business cost is the main matter to be concerned because it must be always as

minimum as possible in order to maximise profits. Companies incur various costs for the

purpose of accomplishment of the end goals. Costs of the any company may include production

cost, cost of acquiring various assets, employment cost, etc. These costs are shown as expenses

or expenditure in the final accounts of the company.

There are many types of costing techniques used by companies for its different purposes such as:

Marginal costing: Marginal costing cab be defined as a tool for evaluating costs which

is concerned about how much cost has increased with the change in volume of output (Drury,

2018). This cost is calculated in terms of increase in variable costs including both prime and

overheads. Marginal cost has major consideration for variable cost changes due to increase in

one unit of output. Under this costing technique, the overall cost of production is divided into

basically two categories, variable and fixed cost. Fixed cost has nothing to do with the level of

production and incurred even at zero level of production but the variable cost remain changing

with the change in unit output.

Absorption costing: Absorption costing as the name suggests that the total costs are

absorbed by the products produced and takes into consideration both fixed and variable cost for

valuing inventories (Collis and Hussey, 2017). Both direct and indirect costs such material costs,

labour costs, rent and insurance related expenses are accounted for determining unit cost. As the

entered in the product costs, so to the closing inventory, the profit figures under this costing is

higher than other costing techniques.

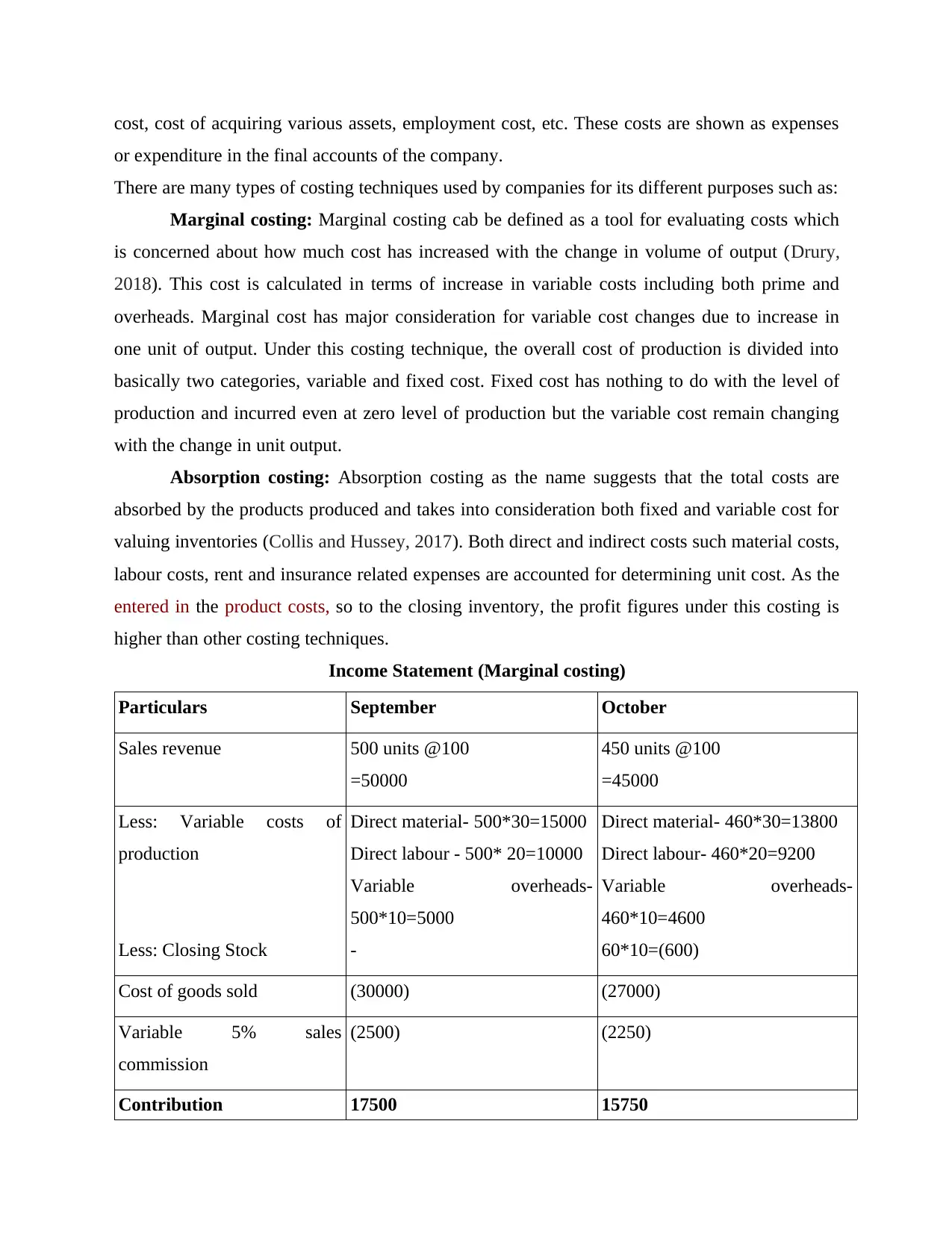

Income Statement (Marginal costing)

Particulars September October

Sales revenue 500 units @100

=50000

450 units @100

=45000

Less: Variable costs of

production

Less: Closing Stock

Direct material- 500*30=15000

Direct labour - 500* 20=10000

Variable overheads-

500*10=5000

-

Direct material- 460*30=13800

Direct labour- 460*20=9200

Variable overheads-

460*10=4600

60*10=(600)

Cost of goods sold (30000) (27000)

Variable 5% sales

commission

(2500) (2250)

Contribution 17500 15750

or expenditure in the final accounts of the company.

There are many types of costing techniques used by companies for its different purposes such as:

Marginal costing: Marginal costing cab be defined as a tool for evaluating costs which

is concerned about how much cost has increased with the change in volume of output (Drury,

2018). This cost is calculated in terms of increase in variable costs including both prime and

overheads. Marginal cost has major consideration for variable cost changes due to increase in

one unit of output. Under this costing technique, the overall cost of production is divided into

basically two categories, variable and fixed cost. Fixed cost has nothing to do with the level of

production and incurred even at zero level of production but the variable cost remain changing

with the change in unit output.

Absorption costing: Absorption costing as the name suggests that the total costs are

absorbed by the products produced and takes into consideration both fixed and variable cost for

valuing inventories (Collis and Hussey, 2017). Both direct and indirect costs such material costs,

labour costs, rent and insurance related expenses are accounted for determining unit cost. As the

entered in the product costs, so to the closing inventory, the profit figures under this costing is

higher than other costing techniques.

Income Statement (Marginal costing)

Particulars September October

Sales revenue 500 units @100

=50000

450 units @100

=45000

Less: Variable costs of

production

Less: Closing Stock

Direct material- 500*30=15000

Direct labour - 500* 20=10000

Variable overheads-

500*10=5000

-

Direct material- 460*30=13800

Direct labour- 460*20=9200

Variable overheads-

460*10=4600

60*10=(600)

Cost of goods sold (30000) (27000)

Variable 5% sales

commission

(2500) (2250)

Contribution 17500 15750

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Fixed costs

Production overhead 5000 5000

Selling cost 2000 2000

Administration cost 2000 2000

Profit 8500 6750

Income Statement (Absorption costing)

Particular September October

Sales revenue 500*100

50000

450*100

=45000

Less: Variable cost

Direct Material 500*30= 15000 460*30= 13800

Direct Labour 500*20= 10000 460*20= 9200

Variable Overheads 500*10= 5000 460*10= 4600

Fixed Production Overhead 500*10= 5000 460*10= 4600

Cost of goods before sales 35000 32200

(-)Closing stk. - 10*70=700

COGS 35000 31500

Contribution 15000 13500

(-) Fixed cost of selling 2000 2000

Administration Cost 2000 2000

5% sales commission 2500 2250

Profit 8500 7250

Production overhead 5000 5000

Selling cost 2000 2000

Administration cost 2000 2000

Profit 8500 6750

Income Statement (Absorption costing)

Particular September October

Sales revenue 500*100

50000

450*100

=45000

Less: Variable cost

Direct Material 500*30= 15000 460*30= 13800

Direct Labour 500*20= 10000 460*20= 9200

Variable Overheads 500*10= 5000 460*10= 4600

Fixed Production Overhead 500*10= 5000 460*10= 4600

Cost of goods before sales 35000 32200

(-)Closing stk. - 10*70=700

COGS 35000 31500

Contribution 15000 13500

(-) Fixed cost of selling 2000 2000

Administration Cost 2000 2000

5% sales commission 2500 2250

Profit 8500 7250

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

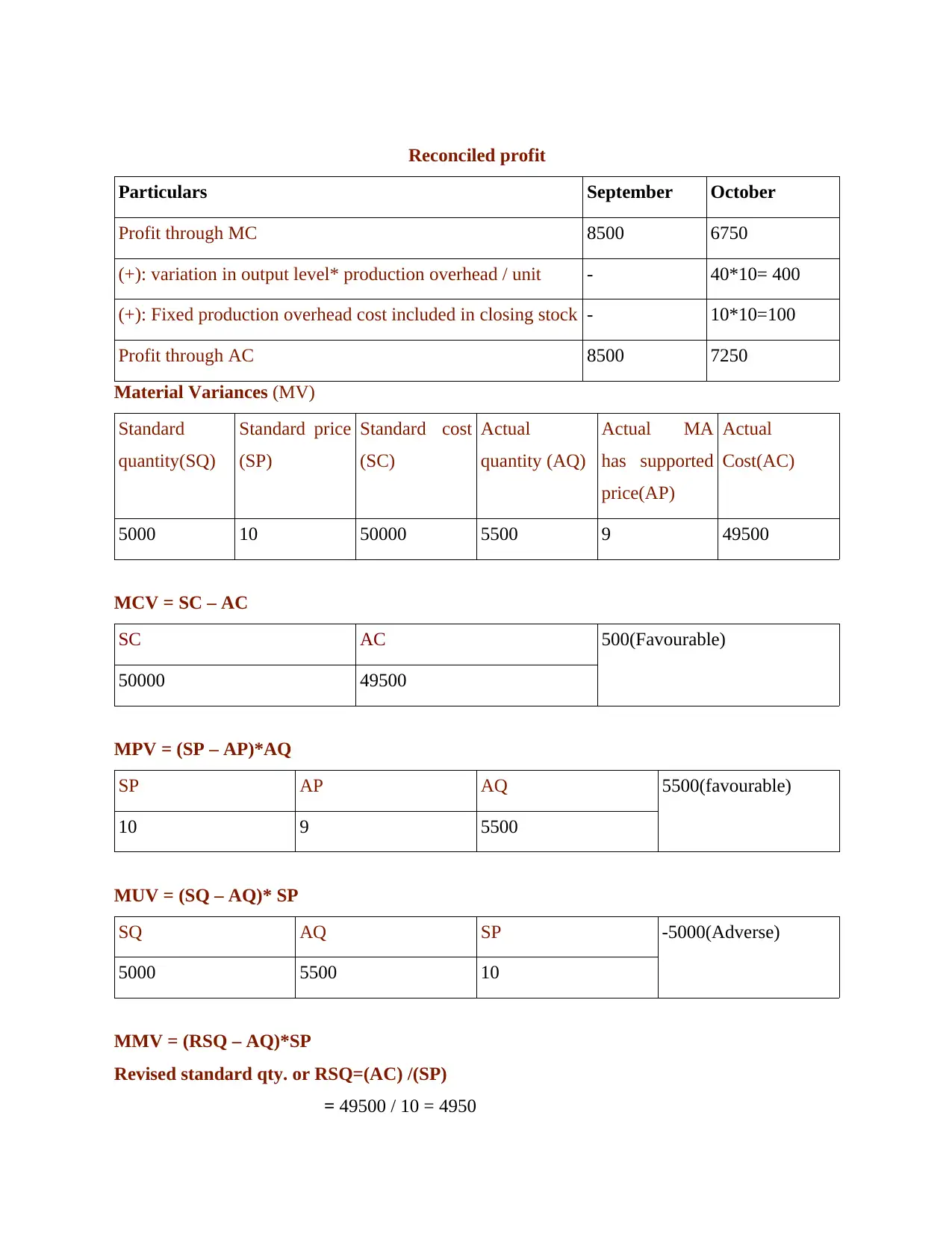

Reconciled profit

Particulars September October

Profit through MC 8500 6750

(+): variation in output level* production overhead / unit - 40*10= 400

(+): Fixed production overhead cost included in closing stock - 10*10=100

Profit through AC 8500 7250

Material Variances (MV)

Standard

quantity(SQ)

Standard price

(SP)

Standard cost

(SC)

Actual

quantity (AQ)

Actual MA

has supported

price(AP)

Actual

Cost(AC)

5000 10 50000 5500 9 49500

MCV = SC – AC

SC AC 500(Favourable)

50000 49500

MPV = (SP – AP)*AQ

SP AP AQ 5500(favourable)

10 9 5500

MUV = (SQ – AQ)* SP

SQ AQ SP -5000(Adverse)

5000 5500 10

MMV = (RSQ – AQ)*SP

Revised standard qty. or RSQ=(AC) /(SP)

= 49500 / 10 = 4950

Particulars September October

Profit through MC 8500 6750

(+): variation in output level* production overhead / unit - 40*10= 400

(+): Fixed production overhead cost included in closing stock - 10*10=100

Profit through AC 8500 7250

Material Variances (MV)

Standard

quantity(SQ)

Standard price

(SP)

Standard cost

(SC)

Actual

quantity (AQ)

Actual MA

has supported

price(AP)

Actual

Cost(AC)

5000 10 50000 5500 9 49500

MCV = SC – AC

SC AC 500(Favourable)

50000 49500

MPV = (SP – AP)*AQ

SP AP AQ 5500(favourable)

10 9 5500

MUV = (SQ – AQ)* SP

SQ AQ SP -5000(Adverse)

5000 5500 10

MMV = (RSQ – AQ)*SP

Revised standard qty. or RSQ=(AC) /(SP)

= 49500 / 10 = 4950

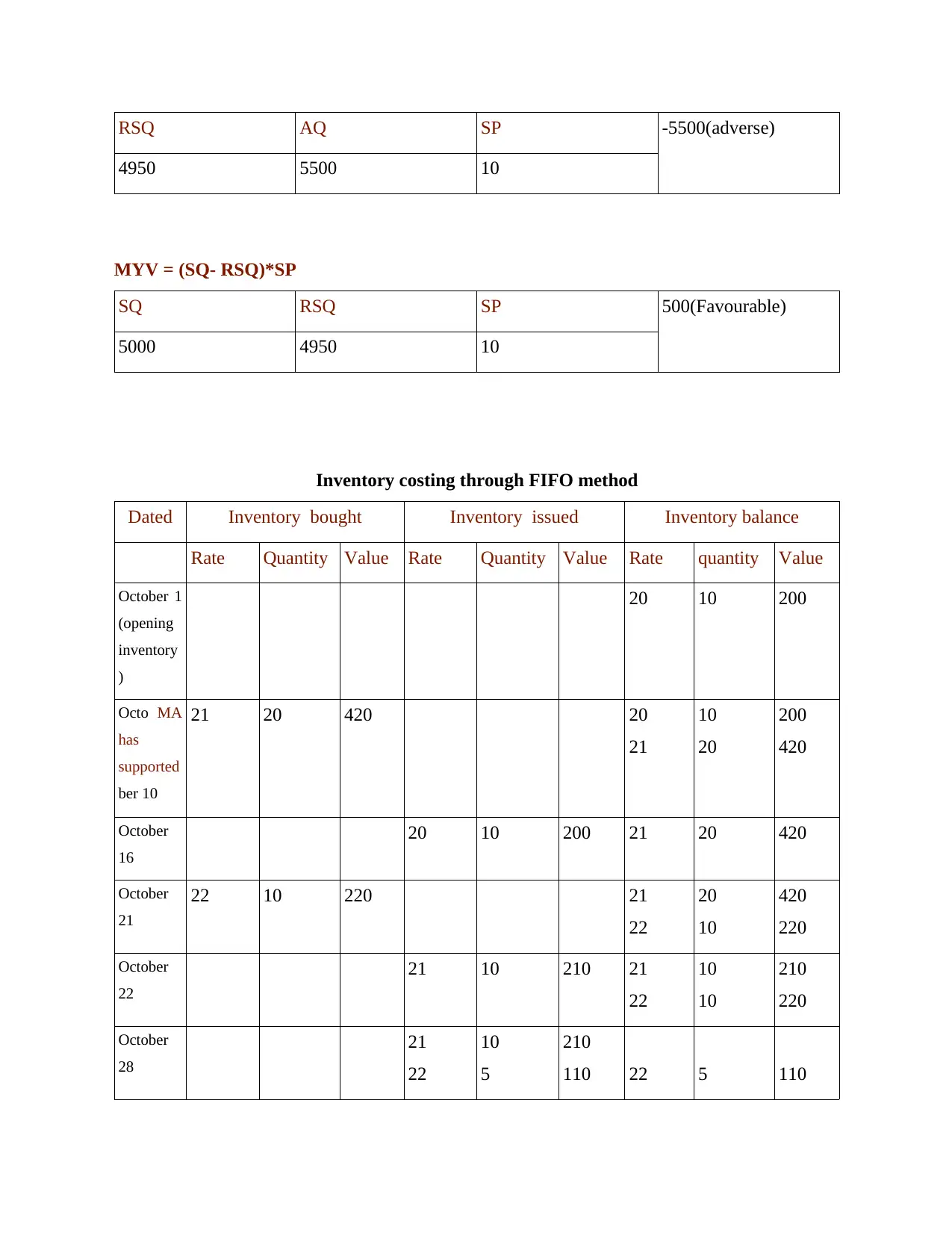

RSQ AQ SP -5500(adverse)

4950 5500 10

MYV = (SQ- RSQ)*SP

SQ RSQ SP 500(Favourable)

5000 4950 10

Inventory costing through FIFO method

Dated Inventory bought Inventory issued Inventory balance

Rate Quantity Value Rate Quantity Value Rate quantity Value

October 1

(opening

inventory

)

20 10 200

Octo MA

has

supported

ber 10

21 20 420 20

21

10

20

200

420

October

16

20 10 200 21 20 420

October

21

22 10 220 21

22

20

10

420

220

October

22

21 10 210 21

22

10

10

210

220

October

28

21

22

10

5

210

110 22 5 110

4950 5500 10

MYV = (SQ- RSQ)*SP

SQ RSQ SP 500(Favourable)

5000 4950 10

Inventory costing through FIFO method

Dated Inventory bought Inventory issued Inventory balance

Rate Quantity Value Rate Quantity Value Rate quantity Value

October 1

(opening

inventory

)

20 10 200

Octo MA

has

supported

ber 10

21 20 420 20

21

10

20

200

420

October

16

20 10 200 21 20 420

October

21

22 10 220 21

22

20

10

420

220

October

22

21 10 210 21

22

10

10

210

220

October

28

21

22

10

5

210

110 22 5 110

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.