Management Accounting Report: Cost and Budget Analysis, Unilever

VerifiedAdded on 2023/01/19

|16

|3491

|86

Report

AI Summary

This report delves into the core concepts of management accounting, emphasizing its role in cost estimation and financial reporting within organizations. Using Unilever as a case study, the report explores various aspects, including management accounting systems like cost accounting and inventory management. It analyzes different reporting methods such as budget reports, job cost reports, and performance reports, alongside techniques for product cost calculation using marginal and absorption costing. The report also evaluates the advantages and disadvantages of planning tools used in budgetary control, such as zero-based budgets, cash budgets, and operating budgets. It includes case studies and financial statements to illustrate the application of these concepts, concluding with an overview of how management accounting systems can be used to address financial problems.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1. Management accounting as well as its essential requirements..............................................1

P2. Management accounting reports............................................................................................2

P3. Calculate cost of product by using effective techniques and develop income statement......3

P4. Evaluate the advantage or disadvantage of various planning tools that used in budgetary

control..........................................................................................................................................7

P5. Adopt management accounting system which used to respond financial problem.............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

P1. Management accounting as well as its essential requirements..............................................1

P2. Management accounting reports............................................................................................2

P3. Calculate cost of product by using effective techniques and develop income statement......3

P4. Evaluate the advantage or disadvantage of various planning tools that used in budgetary

control..........................................................................................................................................7

P5. Adopt management accounting system which used to respond financial problem.............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is the process which helps the organization to estimate their cost

of operations which further beneficial in order to develop financial report. It further used in

decision making process which taken by manager of the company. Report will be prepare for the

analysis of external parties such as customer, shareholders, potential investors or owner of the

organization (Bebbington, Unerman and O’DWYER, 2014). For the better understanding, this

report select Unilever which is UK based transnational consumer goods company. It is founded

in 1929 by William Lever and headquarter situated in Unilever House, London. This report

include various topics such as accounting systems or different methods of reporting which us

used to calculate cost of product with the help of appropriate techniques. In addition, planning

tools for budgetary control and resolve financial problems in the organization.

MAIN BODY

P1. Management accounting as well as its essential requirements.

Management accounting is far-famed concept involving combinations in decision

making, performance systems, devising plans addition to controlling assistances while

formulation plus implementing business strategies. Key elements associated with the concept are

planning, controlling as well as decision making. In context to Unilever, management accounting

is used for recognizing, gauging, collecting, studying, investigating, analysing and interpreting

information that is useful for management authorities so to plan, evaluate addition to control data

and ensuring usage with liabilities related to resources.

Management accounting systems: A futuristic method involving exercises for

maintaining operations, measuring price levels, providing information as well as facilitating

accounts control known as management accounting systems (Bobryshev and et.al., 2015). It

functions in planning, performance evaluation, controlling quantitative with qualitative

information and serves communication means. Various accounting systems used at Unilever are

as elaborated:

Cost accounting system: Framework that is utilized for estimation product costs so to

analyse profits and controlling costs is done through cost accounting system. In Unilever,

product managers uses the system for calculating exact commodity prices by accumulating

controllable, variable, opportunity, sunk, uncontrollable and production related costs. Essential

1

Management accounting is the process which helps the organization to estimate their cost

of operations which further beneficial in order to develop financial report. It further used in

decision making process which taken by manager of the company. Report will be prepare for the

analysis of external parties such as customer, shareholders, potential investors or owner of the

organization (Bebbington, Unerman and O’DWYER, 2014). For the better understanding, this

report select Unilever which is UK based transnational consumer goods company. It is founded

in 1929 by William Lever and headquarter situated in Unilever House, London. This report

include various topics such as accounting systems or different methods of reporting which us

used to calculate cost of product with the help of appropriate techniques. In addition, planning

tools for budgetary control and resolve financial problems in the organization.

MAIN BODY

P1. Management accounting as well as its essential requirements.

Management accounting is far-famed concept involving combinations in decision

making, performance systems, devising plans addition to controlling assistances while

formulation plus implementing business strategies. Key elements associated with the concept are

planning, controlling as well as decision making. In context to Unilever, management accounting

is used for recognizing, gauging, collecting, studying, investigating, analysing and interpreting

information that is useful for management authorities so to plan, evaluate addition to control data

and ensuring usage with liabilities related to resources.

Management accounting systems: A futuristic method involving exercises for

maintaining operations, measuring price levels, providing information as well as facilitating

accounts control known as management accounting systems (Bobryshev and et.al., 2015). It

functions in planning, performance evaluation, controlling quantitative with qualitative

information and serves communication means. Various accounting systems used at Unilever are

as elaborated:

Cost accounting system: Framework that is utilized for estimation product costs so to

analyse profits and controlling costs is done through cost accounting system. In Unilever,

product managers uses the system for calculating exact commodity prices by accumulating

controllable, variable, opportunity, sunk, uncontrollable and production related costs. Essential

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

requirement of the system at entities is to record together with report detailed costs information

that are required by management team for controlling existing operations addition to planning

ahead.

Price optimization system: One of the mathematical program or technique that helps in

computation of the ways in which demand changes as per distinct price levels. Further, the

system combines data with collected information of costs so to suggest fresh prices that can

improve profits. It is opted by management of Unilever so to understand customer perceptions

for current commodity prices and accordingly tailoring existing pricing strategies for market

segments in order to improve customer satisfactions together with exploding operating earnings.

The system has essential requirements at Unilever for forecasting demand, determining pricing

strategies and maintaining optimising consistency.

Inventory management system: To supervise flow of commodities from producers to

warehouses addition to place of sale needs inventory management system. In other words, it is a

collection of technology as well as procedures which monitors, supervises and maintains stocked

products of company. At Unilever, the system is used to identify inventory items along with all

the necessary information associated with the inventory (Chenhall and Moers, 2015). At

warehouses of Unilever, uses the system to locate references for each merchandise, generating

inventory reports as well as forecasting futuristic demands in order to place orders before the

inventory requirement in order to eliminate under-stocking circumstances. Essential requirement

of such system is for systematically tracking inventory addition to maintaining records of the

inventory that enters or leaves workplace.

All the above elaborated accounting systems are followed at Unilever so to frame

effective decisions that can leads to improving profit margins.

P2. Management accounting reports.

Accounting reports are mainly used to plan future activities, analysing current

performances addition to making decisions. With the reports, organisational administrators can

protect values of business along with analysing the aspects through which the business is going

through. Managers of Unilever prepares distinct reports and acknowledges transformational

areas where improvements are to be done so to acquire huge outcomes. Distinct methods that are

utilized in management accounting reporting are under beneath:

2

that are required by management team for controlling existing operations addition to planning

ahead.

Price optimization system: One of the mathematical program or technique that helps in

computation of the ways in which demand changes as per distinct price levels. Further, the

system combines data with collected information of costs so to suggest fresh prices that can

improve profits. It is opted by management of Unilever so to understand customer perceptions

for current commodity prices and accordingly tailoring existing pricing strategies for market

segments in order to improve customer satisfactions together with exploding operating earnings.

The system has essential requirements at Unilever for forecasting demand, determining pricing

strategies and maintaining optimising consistency.

Inventory management system: To supervise flow of commodities from producers to

warehouses addition to place of sale needs inventory management system. In other words, it is a

collection of technology as well as procedures which monitors, supervises and maintains stocked

products of company. At Unilever, the system is used to identify inventory items along with all

the necessary information associated with the inventory (Chenhall and Moers, 2015). At

warehouses of Unilever, uses the system to locate references for each merchandise, generating

inventory reports as well as forecasting futuristic demands in order to place orders before the

inventory requirement in order to eliminate under-stocking circumstances. Essential requirement

of such system is for systematically tracking inventory addition to maintaining records of the

inventory that enters or leaves workplace.

All the above elaborated accounting systems are followed at Unilever so to frame

effective decisions that can leads to improving profit margins.

P2. Management accounting reports.

Accounting reports are mainly used to plan future activities, analysing current

performances addition to making decisions. With the reports, organisational administrators can

protect values of business along with analysing the aspects through which the business is going

through. Managers of Unilever prepares distinct reports and acknowledges transformational

areas where improvements are to be done so to acquire huge outcomes. Distinct methods that are

utilized in management accounting reporting are under beneath:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

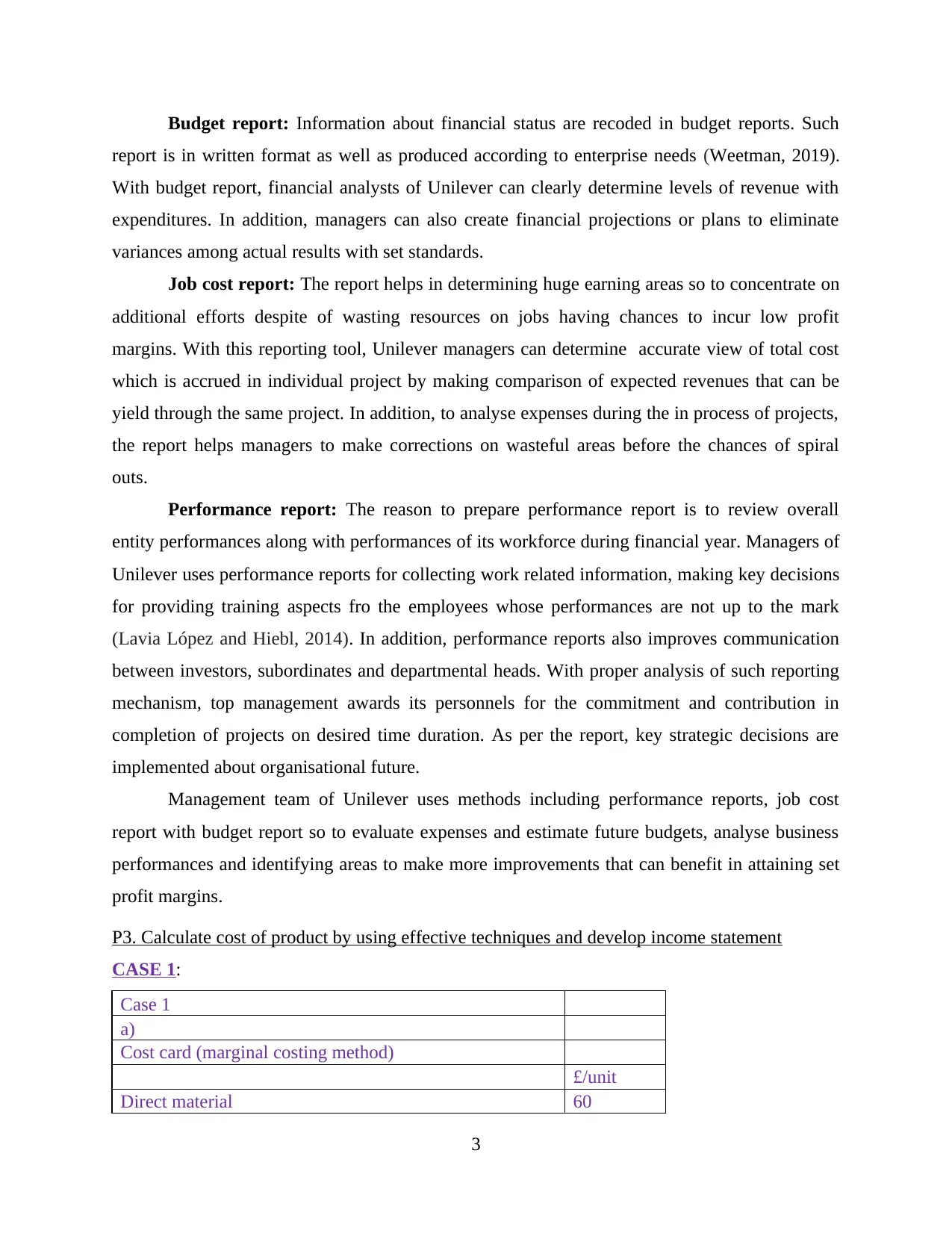

Budget report: Information about financial status are recoded in budget reports. Such

report is in written format as well as produced according to enterprise needs (Weetman, 2019).

With budget report, financial analysts of Unilever can clearly determine levels of revenue with

expenditures. In addition, managers can also create financial projections or plans to eliminate

variances among actual results with set standards.

Job cost report: The report helps in determining huge earning areas so to concentrate on

additional efforts despite of wasting resources on jobs having chances to incur low profit

margins. With this reporting tool, Unilever managers can determine accurate view of total cost

which is accrued in individual project by making comparison of expected revenues that can be

yield through the same project. In addition, to analyse expenses during the in process of projects,

the report helps managers to make corrections on wasteful areas before the chances of spiral

outs.

Performance report: The reason to prepare performance report is to review overall

entity performances along with performances of its workforce during financial year. Managers of

Unilever uses performance reports for collecting work related information, making key decisions

for providing training aspects fro the employees whose performances are not up to the mark

(Lavia López and Hiebl, 2014). In addition, performance reports also improves communication

between investors, subordinates and departmental heads. With proper analysis of such reporting

mechanism, top management awards its personnels for the commitment and contribution in

completion of projects on desired time duration. As per the report, key strategic decisions are

implemented about organisational future.

Management team of Unilever uses methods including performance reports, job cost

report with budget report so to evaluate expenses and estimate future budgets, analyse business

performances and identifying areas to make more improvements that can benefit in attaining set

profit margins.

P3. Calculate cost of product by using effective techniques and develop income statement

CASE 1:

Case 1

a)

Cost card (marginal costing method)

£/unit

Direct material 60

3

report is in written format as well as produced according to enterprise needs (Weetman, 2019).

With budget report, financial analysts of Unilever can clearly determine levels of revenue with

expenditures. In addition, managers can also create financial projections or plans to eliminate

variances among actual results with set standards.

Job cost report: The report helps in determining huge earning areas so to concentrate on

additional efforts despite of wasting resources on jobs having chances to incur low profit

margins. With this reporting tool, Unilever managers can determine accurate view of total cost

which is accrued in individual project by making comparison of expected revenues that can be

yield through the same project. In addition, to analyse expenses during the in process of projects,

the report helps managers to make corrections on wasteful areas before the chances of spiral

outs.

Performance report: The reason to prepare performance report is to review overall

entity performances along with performances of its workforce during financial year. Managers of

Unilever uses performance reports for collecting work related information, making key decisions

for providing training aspects fro the employees whose performances are not up to the mark

(Lavia López and Hiebl, 2014). In addition, performance reports also improves communication

between investors, subordinates and departmental heads. With proper analysis of such reporting

mechanism, top management awards its personnels for the commitment and contribution in

completion of projects on desired time duration. As per the report, key strategic decisions are

implemented about organisational future.

Management team of Unilever uses methods including performance reports, job cost

report with budget report so to evaluate expenses and estimate future budgets, analyse business

performances and identifying areas to make more improvements that can benefit in attaining set

profit margins.

P3. Calculate cost of product by using effective techniques and develop income statement

CASE 1:

Case 1

a)

Cost card (marginal costing method)

£/unit

Direct material 60

3

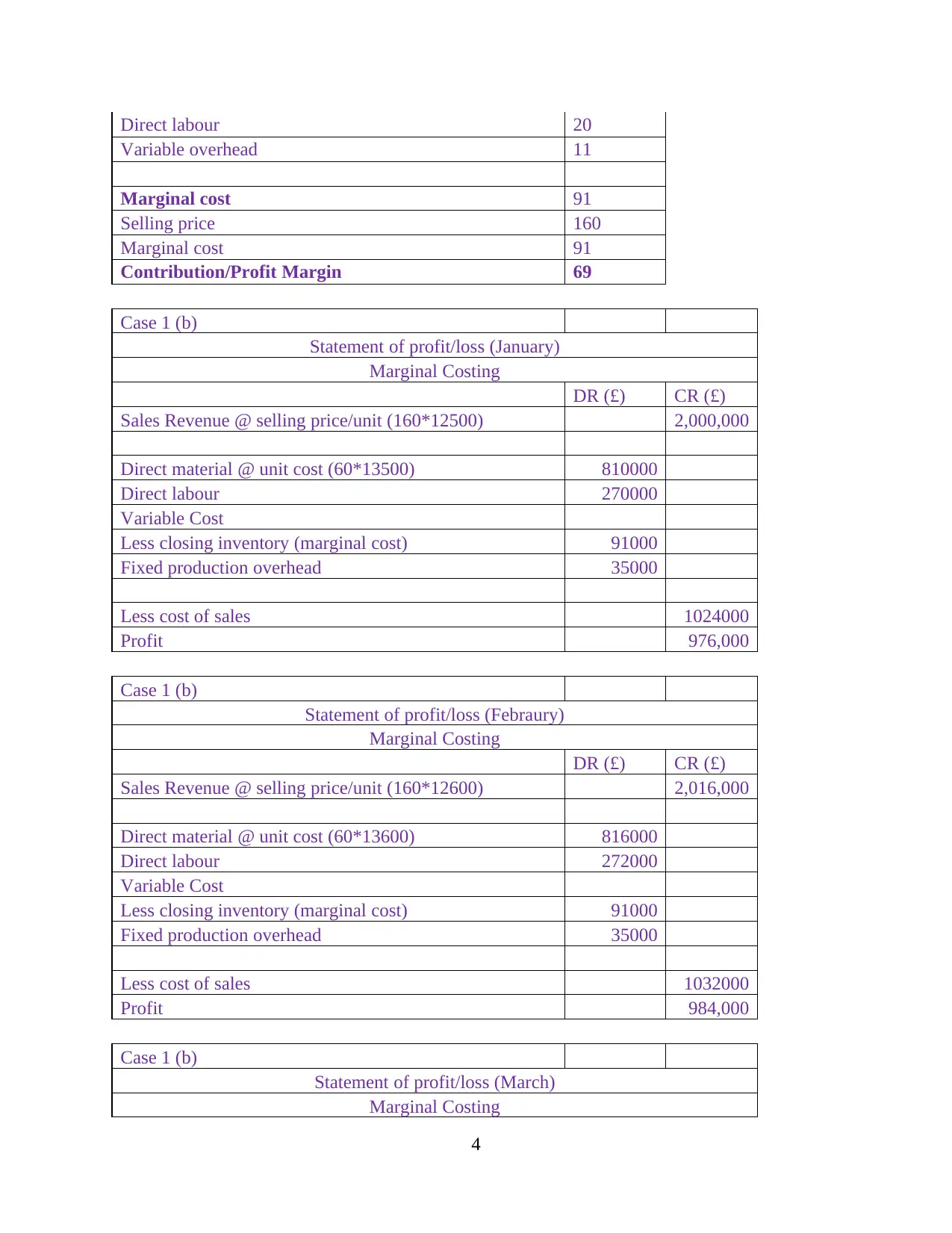

Direct labour 20

Variable overhead 11

Marginal cost 91

Selling price 160

Marginal cost 91

Contribution/Profit Margin 69

Case 1 (b)

Statement of profit/loss (January)

Marginal Costing

DR (£) CR (£)

Sales Revenue @ selling price/unit (160*12500) 2,000,000

Direct material @ unit cost (60*13500) 810000

Direct labour 270000

Variable Cost

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1024000

Profit 976,000

Case 1 (b)

Statement of profit/loss (Febraury)

Marginal Costing

DR (£) CR (£)

Sales Revenue @ selling price/unit (160*12600) 2,016,000

Direct material @ unit cost (60*13600) 816000

Direct labour 272000

Variable Cost

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1032000

Profit 984,000

Case 1 (b)

Statement of profit/loss (March)

Marginal Costing

4

Variable overhead 11

Marginal cost 91

Selling price 160

Marginal cost 91

Contribution/Profit Margin 69

Case 1 (b)

Statement of profit/loss (January)

Marginal Costing

DR (£) CR (£)

Sales Revenue @ selling price/unit (160*12500) 2,000,000

Direct material @ unit cost (60*13500) 810000

Direct labour 270000

Variable Cost

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1024000

Profit 976,000

Case 1 (b)

Statement of profit/loss (Febraury)

Marginal Costing

DR (£) CR (£)

Sales Revenue @ selling price/unit (160*12600) 2,016,000

Direct material @ unit cost (60*13600) 816000

Direct labour 272000

Variable Cost

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1032000

Profit 984,000

Case 1 (b)

Statement of profit/loss (March)

Marginal Costing

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

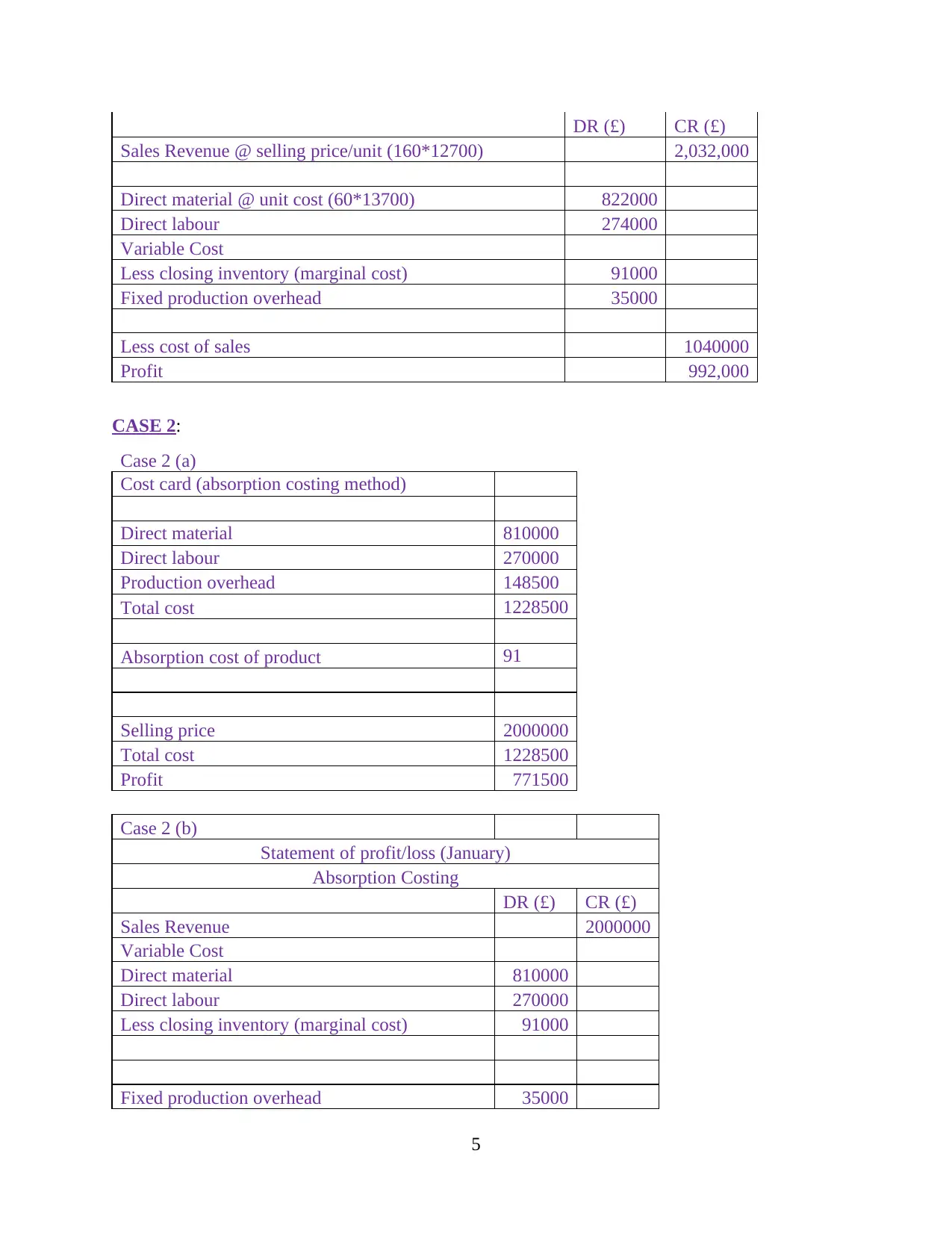

DR (£) CR (£)

Sales Revenue @ selling price/unit (160*12700) 2,032,000

Direct material @ unit cost (60*13700) 822000

Direct labour 274000

Variable Cost

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1040000

Profit 992,000

CASE 2:

Case 2 (a)

Cost card (absorption costing method)

Direct material 810000

Direct labour 270000

Production overhead 148500

Total cost 1228500

Absorption cost of product 91

Selling price 2000000

Total cost 1228500

Profit 771500

Case 2 (b)

Statement of profit/loss (January)

Absorption Costing

DR (£) CR (£)

Sales Revenue 2000000

Variable Cost

Direct material 810000

Direct labour 270000

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

5

Sales Revenue @ selling price/unit (160*12700) 2,032,000

Direct material @ unit cost (60*13700) 822000

Direct labour 274000

Variable Cost

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1040000

Profit 992,000

CASE 2:

Case 2 (a)

Cost card (absorption costing method)

Direct material 810000

Direct labour 270000

Production overhead 148500

Total cost 1228500

Absorption cost of product 91

Selling price 2000000

Total cost 1228500

Profit 771500

Case 2 (b)

Statement of profit/loss (January)

Absorption Costing

DR (£) CR (£)

Sales Revenue 2000000

Variable Cost

Direct material 810000

Direct labour 270000

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

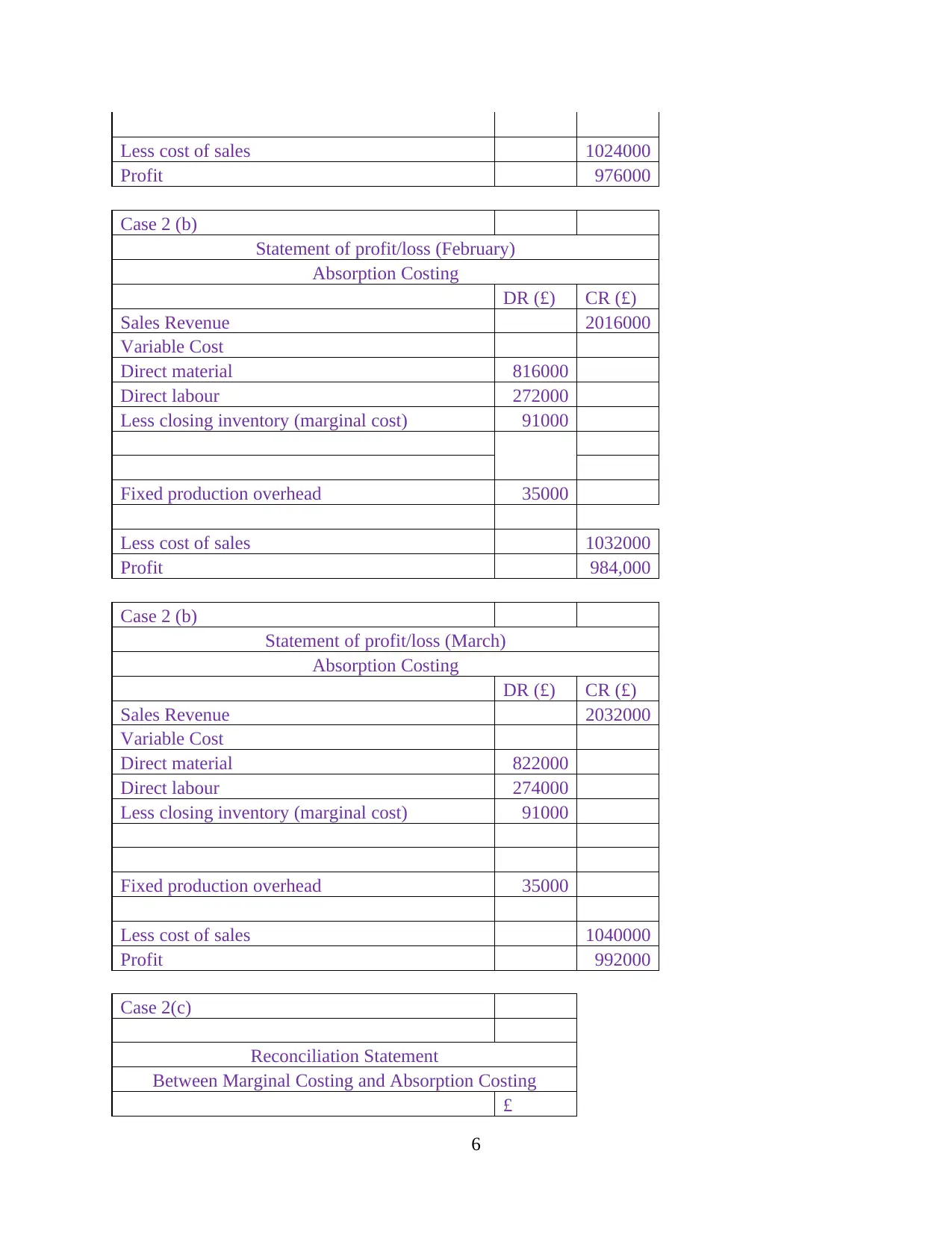

Less cost of sales 1024000

Profit 976000

Case 2 (b)

Statement of profit/loss (February)

Absorption Costing

DR (£) CR (£)

Sales Revenue 2016000

Variable Cost

Direct material 816000

Direct labour 272000

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1032000

Profit 984,000

Case 2 (b)

Statement of profit/loss (March)

Absorption Costing

DR (£) CR (£)

Sales Revenue 2032000

Variable Cost

Direct material 822000

Direct labour 274000

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1040000

Profit 992000

Case 2(c)

Reconciliation Statement

Between Marginal Costing and Absorption Costing

£

6

Profit 976000

Case 2 (b)

Statement of profit/loss (February)

Absorption Costing

DR (£) CR (£)

Sales Revenue 2016000

Variable Cost

Direct material 816000

Direct labour 272000

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1032000

Profit 984,000

Case 2 (b)

Statement of profit/loss (March)

Absorption Costing

DR (£) CR (£)

Sales Revenue 2032000

Variable Cost

Direct material 822000

Direct labour 274000

Less closing inventory (marginal cost) 91000

Fixed production overhead 35000

Less cost of sales 1040000

Profit 992000

Case 2(c)

Reconciliation Statement

Between Marginal Costing and Absorption Costing

£

6

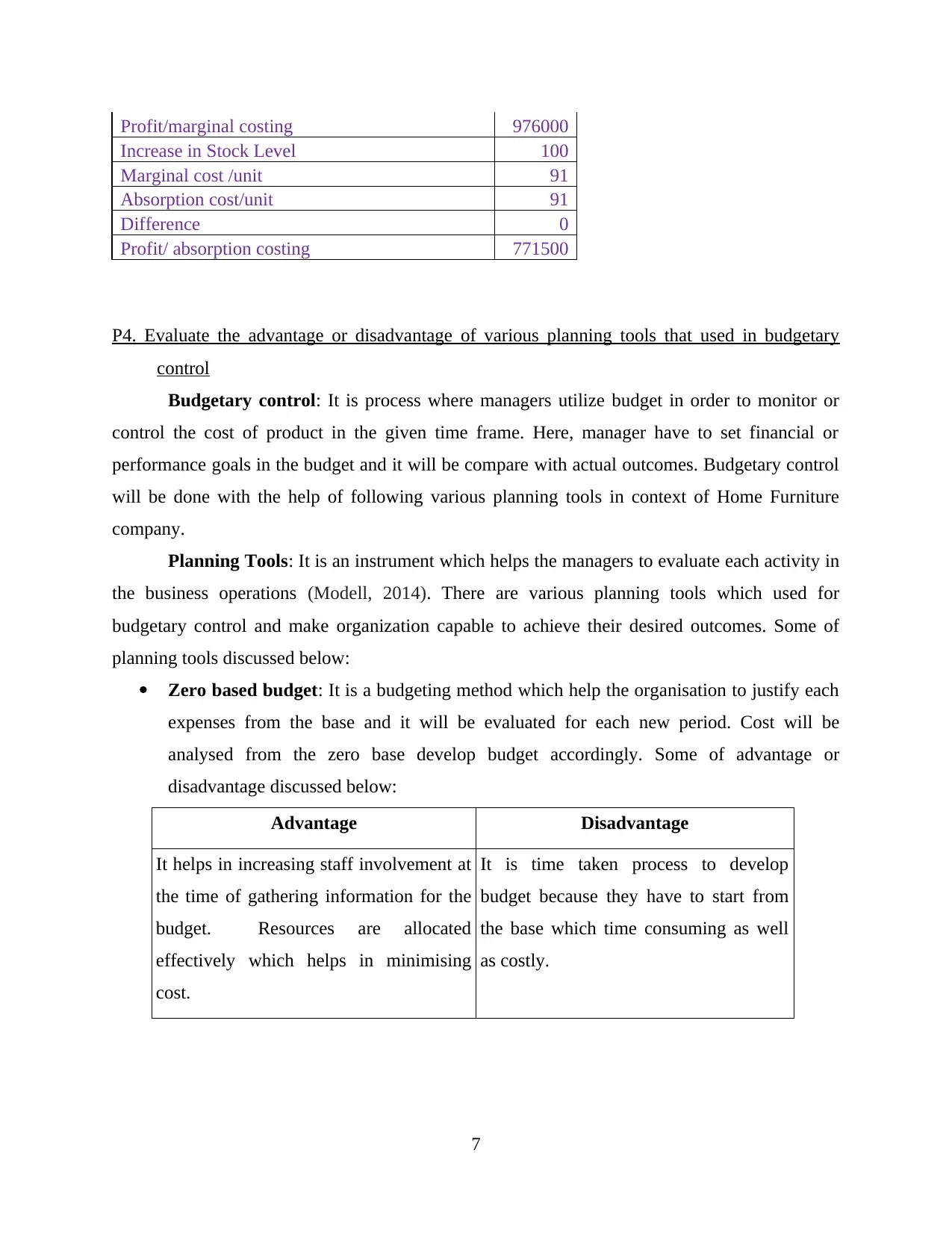

Profit/marginal costing 976000

Increase in Stock Level 100

Marginal cost /unit 91

Absorption cost/unit 91

Difference 0

Profit/ absorption costing 771500

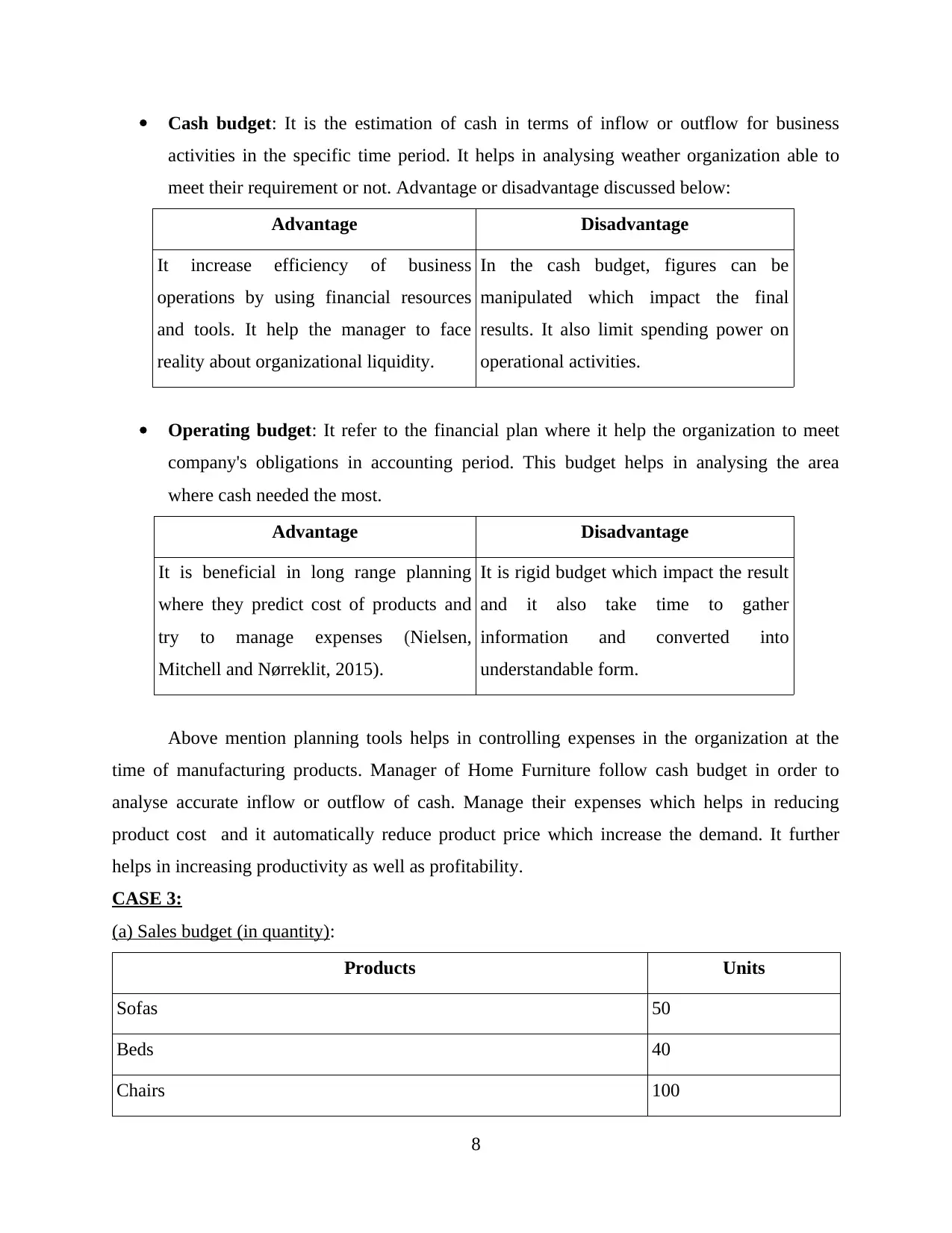

P4. Evaluate the advantage or disadvantage of various planning tools that used in budgetary

control

Budgetary control: It is process where managers utilize budget in order to monitor or

control the cost of product in the given time frame. Here, manager have to set financial or

performance goals in the budget and it will be compare with actual outcomes. Budgetary control

will be done with the help of following various planning tools in context of Home Furniture

company.

Planning Tools: It is an instrument which helps the managers to evaluate each activity in

the business operations (Modell, 2014). There are various planning tools which used for

budgetary control and make organization capable to achieve their desired outcomes. Some of

planning tools discussed below:

Zero based budget: It is a budgeting method which help the organisation to justify each

expenses from the base and it will be evaluated for each new period. Cost will be

analysed from the zero base develop budget accordingly. Some of advantage or

disadvantage discussed below:

Advantage Disadvantage

It helps in increasing staff involvement at

the time of gathering information for the

budget. Resources are allocated

effectively which helps in minimising

cost.

It is time taken process to develop

budget because they have to start from

the base which time consuming as well

as costly.

7

Increase in Stock Level 100

Marginal cost /unit 91

Absorption cost/unit 91

Difference 0

Profit/ absorption costing 771500

P4. Evaluate the advantage or disadvantage of various planning tools that used in budgetary

control

Budgetary control: It is process where managers utilize budget in order to monitor or

control the cost of product in the given time frame. Here, manager have to set financial or

performance goals in the budget and it will be compare with actual outcomes. Budgetary control

will be done with the help of following various planning tools in context of Home Furniture

company.

Planning Tools: It is an instrument which helps the managers to evaluate each activity in

the business operations (Modell, 2014). There are various planning tools which used for

budgetary control and make organization capable to achieve their desired outcomes. Some of

planning tools discussed below:

Zero based budget: It is a budgeting method which help the organisation to justify each

expenses from the base and it will be evaluated for each new period. Cost will be

analysed from the zero base develop budget accordingly. Some of advantage or

disadvantage discussed below:

Advantage Disadvantage

It helps in increasing staff involvement at

the time of gathering information for the

budget. Resources are allocated

effectively which helps in minimising

cost.

It is time taken process to develop

budget because they have to start from

the base which time consuming as well

as costly.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash budget: It is the estimation of cash in terms of inflow or outflow for business

activities in the specific time period. It helps in analysing weather organization able to

meet their requirement or not. Advantage or disadvantage discussed below:

Advantage Disadvantage

It increase efficiency of business

operations by using financial resources

and tools. It help the manager to face

reality about organizational liquidity.

In the cash budget, figures can be

manipulated which impact the final

results. It also limit spending power on

operational activities.

Operating budget: It refer to the financial plan where it help the organization to meet

company's obligations in accounting period. This budget helps in analysing the area

where cash needed the most.

Advantage Disadvantage

It is beneficial in long range planning

where they predict cost of products and

try to manage expenses (Nielsen,

Mitchell and Nørreklit, 2015).

It is rigid budget which impact the result

and it also take time to gather

information and converted into

understandable form.

Above mention planning tools helps in controlling expenses in the organization at the

time of manufacturing products. Manager of Home Furniture follow cash budget in order to

analyse accurate inflow or outflow of cash. Manage their expenses which helps in reducing

product cost and it automatically reduce product price which increase the demand. It further

helps in increasing productivity as well as profitability.

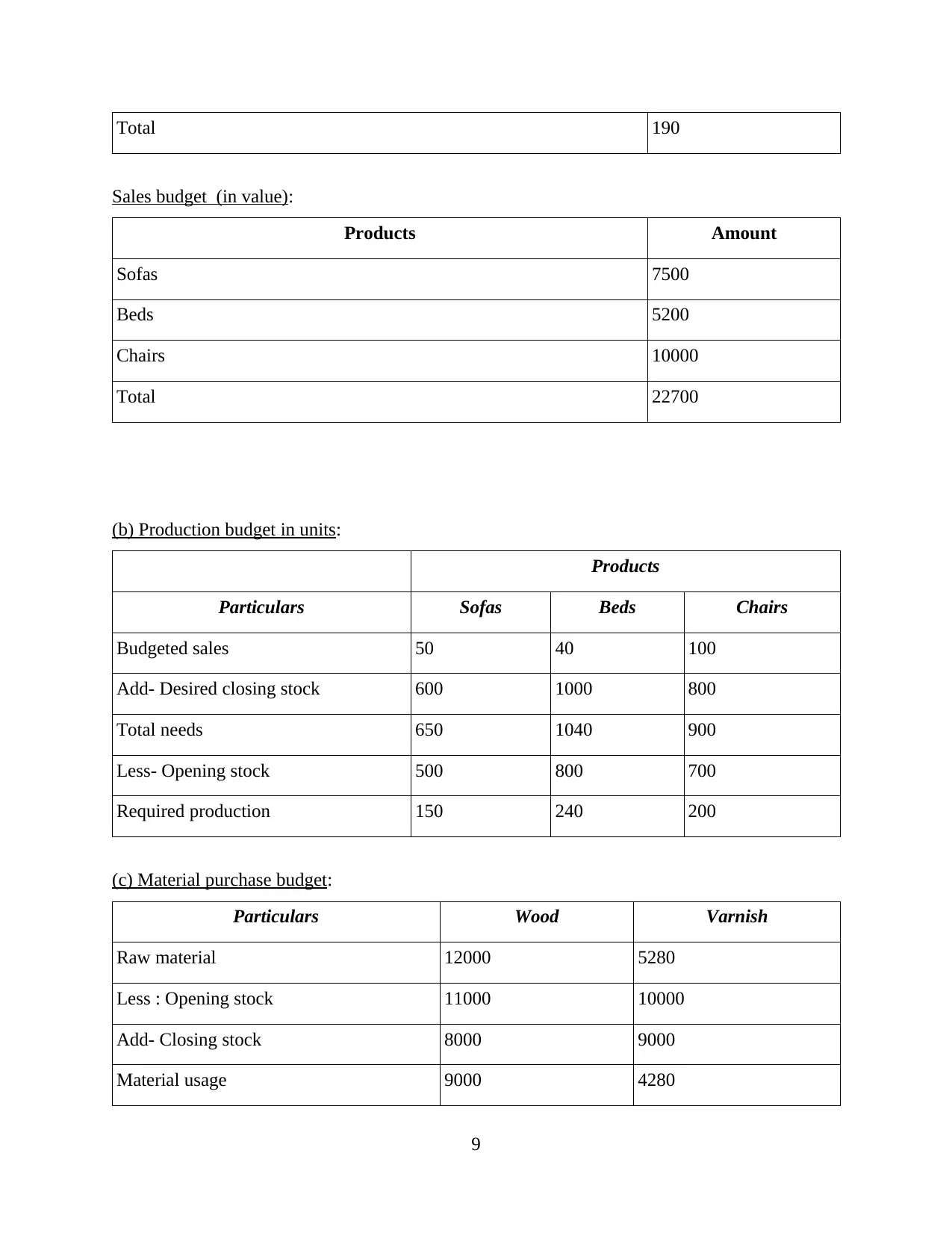

CASE 3:

(a) Sales budget (in quantity):

Products Units

Sofas 50

Beds 40

Chairs 100

8

activities in the specific time period. It helps in analysing weather organization able to

meet their requirement or not. Advantage or disadvantage discussed below:

Advantage Disadvantage

It increase efficiency of business

operations by using financial resources

and tools. It help the manager to face

reality about organizational liquidity.

In the cash budget, figures can be

manipulated which impact the final

results. It also limit spending power on

operational activities.

Operating budget: It refer to the financial plan where it help the organization to meet

company's obligations in accounting period. This budget helps in analysing the area

where cash needed the most.

Advantage Disadvantage

It is beneficial in long range planning

where they predict cost of products and

try to manage expenses (Nielsen,

Mitchell and Nørreklit, 2015).

It is rigid budget which impact the result

and it also take time to gather

information and converted into

understandable form.

Above mention planning tools helps in controlling expenses in the organization at the

time of manufacturing products. Manager of Home Furniture follow cash budget in order to

analyse accurate inflow or outflow of cash. Manage their expenses which helps in reducing

product cost and it automatically reduce product price which increase the demand. It further

helps in increasing productivity as well as profitability.

CASE 3:

(a) Sales budget (in quantity):

Products Units

Sofas 50

Beds 40

Chairs 100

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total 190

Sales budget (in value):

Products Amount

Sofas 7500

Beds 5200

Chairs 10000

Total 22700

(b) Production budget in units:

Products

Particulars Sofas Beds Chairs

Budgeted sales 50 40 100

Add- Desired closing stock 600 1000 800

Total needs 650 1040 900

Less- Opening stock 500 800 700

Required production 150 240 200

(c) Material purchase budget:

Particulars Wood Varnish

Raw material 12000 5280

Less : Opening stock 11000 10000

Add- Closing stock 8000 9000

Material usage 9000 4280

9

Sales budget (in value):

Products Amount

Sofas 7500

Beds 5200

Chairs 10000

Total 22700

(b) Production budget in units:

Products

Particulars Sofas Beds Chairs

Budgeted sales 50 40 100

Add- Desired closing stock 600 1000 800

Total needs 650 1040 900

Less- Opening stock 500 800 700

Required production 150 240 200

(c) Material purchase budget:

Particulars Wood Varnish

Raw material 12000 5280

Less : Opening stock 11000 10000

Add- Closing stock 8000 9000

Material usage 9000 4280

9

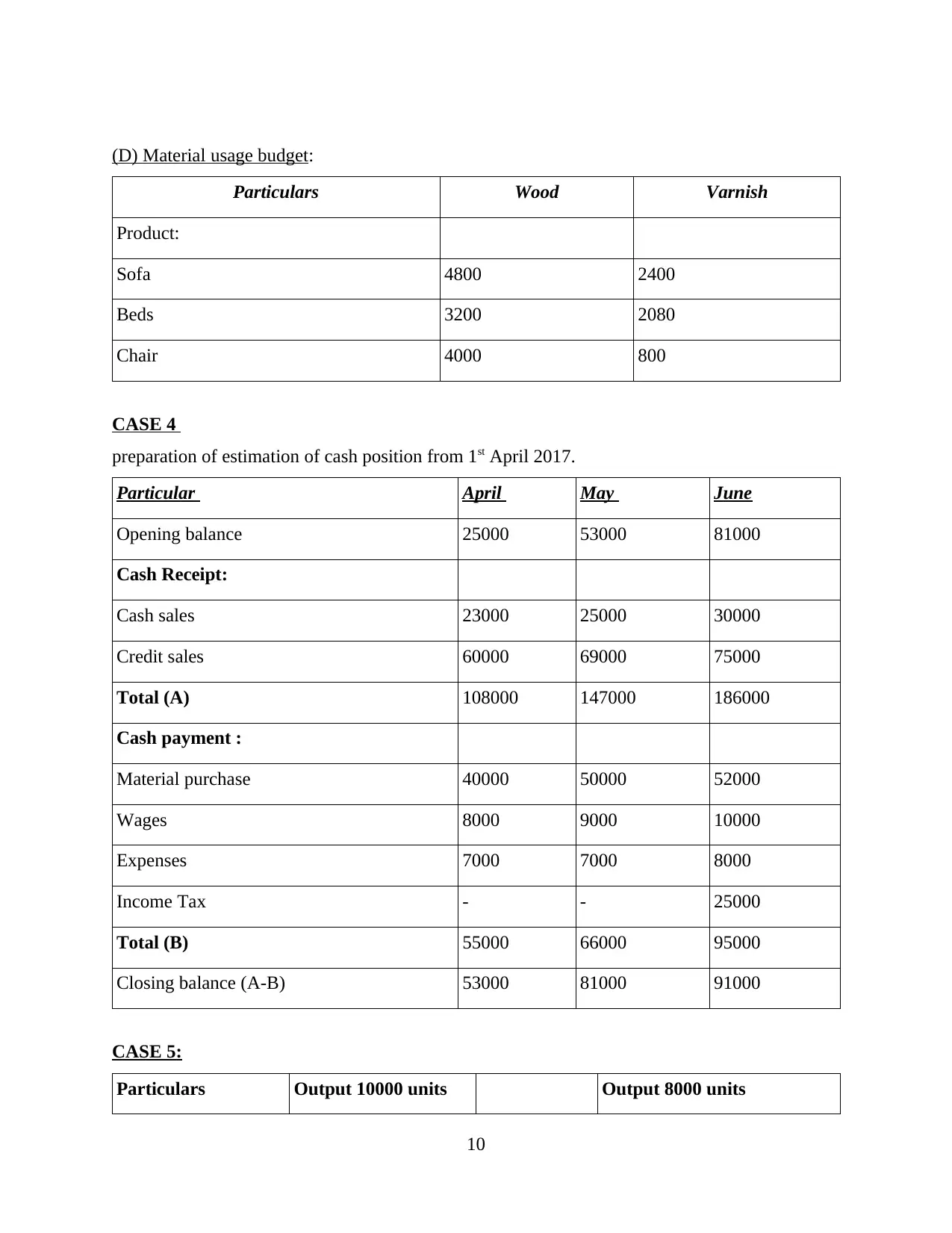

(D) Material usage budget:

Particulars Wood Varnish

Product:

Sofa 4800 2400

Beds 3200 2080

Chair 4000 800

CASE 4

preparation of estimation of cash position from 1st April 2017.

Particular April May June

Opening balance 25000 53000 81000

Cash Receipt:

Cash sales 23000 25000 30000

Credit sales 60000 69000 75000

Total (A) 108000 147000 186000

Cash payment :

Material purchase 40000 50000 52000

Wages 8000 9000 10000

Expenses 7000 7000 8000

Income Tax - - 25000

Total (B) 55000 66000 95000

Closing balance (A-B) 53000 81000 91000

CASE 5:

Particulars Output 10000 units Output 8000 units

10

Particulars Wood Varnish

Product:

Sofa 4800 2400

Beds 3200 2080

Chair 4000 800

CASE 4

preparation of estimation of cash position from 1st April 2017.

Particular April May June

Opening balance 25000 53000 81000

Cash Receipt:

Cash sales 23000 25000 30000

Credit sales 60000 69000 75000

Total (A) 108000 147000 186000

Cash payment :

Material purchase 40000 50000 52000

Wages 8000 9000 10000

Expenses 7000 7000 8000

Income Tax - - 25000

Total (B) 55000 66000 95000

Closing balance (A-B) 53000 81000 91000

CASE 5:

Particulars Output 10000 units Output 8000 units

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.