Management Accounting Report on Unilever's Financial Performance

VerifiedAdded on 2021/08/03

|27

|7364

|484

Report

AI Summary

This report, prepared for a BTEC Business unit on Management Accounting, provides a comprehensive analysis of Unilever's accounting practices. It begins with an introduction to the company and definitions of management accounting, including its role and principles, distinguishing it from financial accounting. The report then delves into Unilever's management accounting systems, specifically job costing and inventory management. It further examines management accounting reporting, including cost of production and sales reports, along with the methods used in creating these reports. Finally, the report analyzes Unilever's financial statements, including the balance sheet, cash flow statement, and income statement, along with an analysis of fundamental ratios. The report aims to provide a detailed overview of Unilever's financial performance and accounting strategies.

1

PROGRAM TITLE: BTEC BUSINESS

UNIT TITLE: MANAGEMENT ACCOUNTING

ASSIGNMENT NUMBER: 1

ASSIGNMENT NAME: 1

SUBMISSION DATE: February 2nd 2021

DATE RECEIVED: February 11th 2021

TUTORIAL LECTURER: Ms. Pham Huong Thuy

WORD COUNT: 4456 words

STUDENT NAME: Hoang Thi Phuong Thao

STUDENT ID: BKC1909

MOBILE NUMBER: (+84) 382 021 786

PROGRAM TITLE: BTEC BUSINESS

UNIT TITLE: MANAGEMENT ACCOUNTING

ASSIGNMENT NUMBER: 1

ASSIGNMENT NAME: 1

SUBMISSION DATE: February 2nd 2021

DATE RECEIVED: February 11th 2021

TUTORIAL LECTURER: Ms. Pham Huong Thuy

WORD COUNT: 4456 words

STUDENT NAME: Hoang Thi Phuong Thao

STUDENT ID: BKC1909

MOBILE NUMBER: (+84) 382 021 786

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Summative Feedback:

Internal verification:

Summative Feedback:

Internal verification:

3

TABLE OF CONTENT

I. PREFACE .............................................................................................................................. 5

II. COMPANY INTRODUCTION ........................................................................................ 5

III. MANAGEMENT ACCOUNTING DEFINITIONS AND EXPLANATIONS ............. 6

1. Management accounting definitions ................................................................................. 6

2. Explanations the role and principles of management accounting ................................. 6

a. The role of management accounting ................................................................................. 6

b. The principles of management accounting ....................................................................... 7

3. Explanations the distinction between management and financial accounting ............. 9

IV. MANAGEMENT ACCOUNTING SYSTEMS................................................................ 1

1. Job - costing system ............................................................................................................ 1

a. Essntial requirements for Job - costing system ................................................................. 1

b. The benefits are of a Job - costing systems....................................................................... 3

2. Inventory management system .......................................................................................... 4

a. Essential requirements for Inventory management systems ............................................. 4

b. The benefits of a Inventory management systems ............................................................ 5

V. MANAGEMENT ACCOUNTING REPORTING .............................................................. 5

1. Cost of production reports ................................................................................................. 5

a. Methods of making Cost of production reports ................................................................ 5

b. How to use Unilever's Cost production report .................................................................. 6

2. Sales report .......................................................................................................................... 8

a. Methods of making Sales report ....................................................................................... 8

b. How to use Unilever's Sales report ................................................................................... 8

VI. FINANCIAL STATEMENTS AND FUNDAMENTAL RATIOS ANALYSIS ........... 9

1. Balance Sheet .................................................................................................................... 10

2. Cash Flow Statement ........................................................................................................ 12

TABLE OF CONTENT

I. PREFACE .............................................................................................................................. 5

II. COMPANY INTRODUCTION ........................................................................................ 5

III. MANAGEMENT ACCOUNTING DEFINITIONS AND EXPLANATIONS ............. 6

1. Management accounting definitions ................................................................................. 6

2. Explanations the role and principles of management accounting ................................. 6

a. The role of management accounting ................................................................................. 6

b. The principles of management accounting ....................................................................... 7

3. Explanations the distinction between management and financial accounting ............. 9

IV. MANAGEMENT ACCOUNTING SYSTEMS................................................................ 1

1. Job - costing system ............................................................................................................ 1

a. Essntial requirements for Job - costing system ................................................................. 1

b. The benefits are of a Job - costing systems....................................................................... 3

2. Inventory management system .......................................................................................... 4

a. Essential requirements for Inventory management systems ............................................. 4

b. The benefits of a Inventory management systems ............................................................ 5

V. MANAGEMENT ACCOUNTING REPORTING .............................................................. 5

1. Cost of production reports ................................................................................................. 5

a. Methods of making Cost of production reports ................................................................ 5

b. How to use Unilever's Cost production report .................................................................. 6

2. Sales report .......................................................................................................................... 8

a. Methods of making Sales report ....................................................................................... 8

b. How to use Unilever's Sales report ................................................................................... 8

VI. FINANCIAL STATEMENTS AND FUNDAMENTAL RATIOS ANALYSIS ........... 9

1. Balance Sheet .................................................................................................................... 10

2. Cash Flow Statement ........................................................................................................ 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

3. Income Statement ............................................................................................................. 13

VII. CONCLUSION ................................................................................................................. 16

VIII. REFERENCE LIST ...................................................................................................... 17

3. Income Statement ............................................................................................................. 13

VII. CONCLUSION ................................................................................................................. 16

VIII. REFERENCE LIST ...................................................................................................... 17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

I. PREFACE

In the current fierce competition among technology companies in the world, it is a very big

challenge for businesses to stand firm in the market. And it can be said that management

accounting plays a very important role in making budget and cost plans to help the company spend

reasonably in the process of development and compete with strong competitors.

Therefore, to help people understand more about the management accounting and the content of

the accounting relativity, the accounting department of Unilever has released this report.

The report will consist of five main parts. The opening is to introduce Unilever with basic

information. Next is the definition and the roles and principles of management accounting along

with explanations of the differences between management and financial accounting. The

management accounting systems Unilever applies will be clearly analyzed in Part IV. In addition,

the report also provides management accounting reports that the company frequently uses. Part VI

of the report will analyze and evaluate the financial statements and fundamental ratios of Unilever

in 2019.

II. COMPANY INTRODUCTION

Picture 1: Logo of Unilever by CafeBiz

Unilever is a multinational company founded on September 2nd 1929 with the combination of

Lever Brothers (the soap maker in the UK) and Margarine Unilever (a Dutch food butter

manufacturer). Currently, Unilever has two headquarters in the UK city of London and the Dutch

city of Rotterdam.

I. PREFACE

In the current fierce competition among technology companies in the world, it is a very big

challenge for businesses to stand firm in the market. And it can be said that management

accounting plays a very important role in making budget and cost plans to help the company spend

reasonably in the process of development and compete with strong competitors.

Therefore, to help people understand more about the management accounting and the content of

the accounting relativity, the accounting department of Unilever has released this report.

The report will consist of five main parts. The opening is to introduce Unilever with basic

information. Next is the definition and the roles and principles of management accounting along

with explanations of the differences between management and financial accounting. The

management accounting systems Unilever applies will be clearly analyzed in Part IV. In addition,

the report also provides management accounting reports that the company frequently uses. Part VI

of the report will analyze and evaluate the financial statements and fundamental ratios of Unilever

in 2019.

II. COMPANY INTRODUCTION

Picture 1: Logo of Unilever by CafeBiz

Unilever is a multinational company founded on September 2nd 1929 with the combination of

Lever Brothers (the soap maker in the UK) and Margarine Unilever (a Dutch food butter

manufacturer). Currently, Unilever has two headquarters in the UK city of London and the Dutch

city of Rotterdam.

6

Unilever is a world-famous brand in the field of manufacturing fast-moving consumer products,

including personal and home hygiene products, food, tea and tea drinks, and products sold in more

than 190 countries. Unilever's food, home and personal care brand is trusted by consumers around

the world - the average consumer buys 170 billion packages of Unilever products each year.

Unilever's typical brands are widely consumed and accepted worldwide such as Lipton, Knorr,

Cornetto, Omo, Lux, Vim, Lifebuoy, Dove, Close-Up, Sunsilk, Clear, Pond's, Hazeline, Vaseline,

etcs. With sales of over millions of dollars per brand, it is proving that Unilever is one of the most

successful companies in the world in the consumer healthcare business.

III. MANAGEMENT ACCOUNTING DEFINITIONS AND EXPLANATIONS

1. Management accounting definitions

Accounting is the process of identifying, measuring and communicating financial information

about an entity to permit informed judgements and decisions by users of the information. (Pauline

Weetman, 2006)

Management accounting is the process of preparing reports about business operations that help

managers make short-term and long-term decisions. It helps a business pursue its goals by

identifying, measuring, analyzing, interpreting and communicating information to managers.

(Freshbooks, nd)

Management accounting is the process of identification, measurement, accumulation, analysis,

preparation, interpretation, and communication of information that assists executives in fulfilling

organizational objectives. (iEduNote, nd)

2. Explanations the role and principles of management accounting

a. The role of management accounting

The role of management accounting include:

❖ Make-or-Buy decision

Management accounting insights on cost and production availability are deciding factors in

purchasing choices. Data from managerial accounting empower decision-making at both an

operational and strategic level. (Freshbooks, nd)

❖ Forecasting cash flows

Unilever is a world-famous brand in the field of manufacturing fast-moving consumer products,

including personal and home hygiene products, food, tea and tea drinks, and products sold in more

than 190 countries. Unilever's food, home and personal care brand is trusted by consumers around

the world - the average consumer buys 170 billion packages of Unilever products each year.

Unilever's typical brands are widely consumed and accepted worldwide such as Lipton, Knorr,

Cornetto, Omo, Lux, Vim, Lifebuoy, Dove, Close-Up, Sunsilk, Clear, Pond's, Hazeline, Vaseline,

etcs. With sales of over millions of dollars per brand, it is proving that Unilever is one of the most

successful companies in the world in the consumer healthcare business.

III. MANAGEMENT ACCOUNTING DEFINITIONS AND EXPLANATIONS

1. Management accounting definitions

Accounting is the process of identifying, measuring and communicating financial information

about an entity to permit informed judgements and decisions by users of the information. (Pauline

Weetman, 2006)

Management accounting is the process of preparing reports about business operations that help

managers make short-term and long-term decisions. It helps a business pursue its goals by

identifying, measuring, analyzing, interpreting and communicating information to managers.

(Freshbooks, nd)

Management accounting is the process of identification, measurement, accumulation, analysis,

preparation, interpretation, and communication of information that assists executives in fulfilling

organizational objectives. (iEduNote, nd)

2. Explanations the role and principles of management accounting

a. The role of management accounting

The role of management accounting include:

❖ Make-or-Buy decision

Management accounting insights on cost and production availability are deciding factors in

purchasing choices. Data from managerial accounting empower decision-making at both an

operational and strategic level. (Freshbooks, nd)

❖ Forecasting cash flows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Estimating cash flows and the impact of cash flows on the business is essential. Considering where

the costs companies will incur in the future and where its revenue will come from can help a

business make its next moves. Management accounting involves creating budgets and trend chars

that managers use to decide how to allocate money and resources to generate the projected revenue

growth. (Freshbooks, nd)

❖ Understand performance variances

Performance discrepancies in business are variances between what was predicted and what was

achieved. Using analytical techniques, management accounting helps management build on

positive variances and manage the negative ones. (Freshbooks, nd)

❖ Analyzing the rate of return

Knowing the rate of return (ROR) is essential to know before embarking on a project that requires

a lot of investments. The management accountant must know to choose the project that is most

profitable and the fastest break-even for the company among other projects. And must estimate

the cash flow to be invested in that project is suitable for the company. (Freshbooks, nd)

b. The principles of management accounting

❖ Influence

Communication presents insight which is crucial. Communication constitutes the start and end of

the management accounting. It strengthens the process of making decisions by corresponding

insightful details at all phases of decision making. Sound communication of critical information

makes it possible for management accounting to cut across silos as well as encourages integrated

thought process. The impact of actions taken in one division of the business on the other divisions

can be easily comprehended, approved, or modified.

By discussing the requirements of the business decision makers, it is a lot simpler to devise and

assess the most pertinent information. It implies that recommendations are important for the

decision makers and also to gain authority.

(Alika Cooper, 2020)

❖ Relevance

Information is valuable for one and all. Management accounting checks for the best available

resources for information pertinent to the decision that is being taken, the people making the

Estimating cash flows and the impact of cash flows on the business is essential. Considering where

the costs companies will incur in the future and where its revenue will come from can help a

business make its next moves. Management accounting involves creating budgets and trend chars

that managers use to decide how to allocate money and resources to generate the projected revenue

growth. (Freshbooks, nd)

❖ Understand performance variances

Performance discrepancies in business are variances between what was predicted and what was

achieved. Using analytical techniques, management accounting helps management build on

positive variances and manage the negative ones. (Freshbooks, nd)

❖ Analyzing the rate of return

Knowing the rate of return (ROR) is essential to know before embarking on a project that requires

a lot of investments. The management accountant must know to choose the project that is most

profitable and the fastest break-even for the company among other projects. And must estimate

the cash flow to be invested in that project is suitable for the company. (Freshbooks, nd)

b. The principles of management accounting

❖ Influence

Communication presents insight which is crucial. Communication constitutes the start and end of

the management accounting. It strengthens the process of making decisions by corresponding

insightful details at all phases of decision making. Sound communication of critical information

makes it possible for management accounting to cut across silos as well as encourages integrated

thought process. The impact of actions taken in one division of the business on the other divisions

can be easily comprehended, approved, or modified.

By discussing the requirements of the business decision makers, it is a lot simpler to devise and

assess the most pertinent information. It implies that recommendations are important for the

decision makers and also to gain authority.

(Alika Cooper, 2020)

❖ Relevance

Information is valuable for one and all. Management accounting checks for the best available

resources for information pertinent to the decision that is being taken, the people making the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

decision along with the decision method being employed. By getting to grips with the requirements

of shareholders, the most relevant and useful information for decision-making is determined,

obtained, and arranged for evaluation.

It needs maintaining a proper balance between: Past, present, as well as future-dependent info;

External and Internal information; Financial as well as nonfinancial details, such as ecological and

social concerns.

(Alika Cooper, 2020)

❖ Value

The influence on value is estimated. Management accounting links the organization’s processes to

its core enterprise model and demands an intensive knowledge of the broader macroeconomic

atmosphere. It entails assessing information along the value-generation pathway, gauging possible

opportunities, and concentrating on the risks, expenses as well as the value-generation possibility

of opportunities.

Situation analysis adds rigor to the review of organizational decisions. By using situation models

to assess the effect of specific opportunities and challenges, businesses can make better decisions

regarding terminating or taking advantage of them. The models furthermore allow firms to

quantify the possibility of a chance to become successful or risk arising and the value which needs

to be produced or eroded.

(Alika Cooper, 2020)

❖ Credibility

Stewardship forms credibility. Responsibility and scrutiny help in making the decision-making

process a lot more purposeful. Managing near-term business interests against long-run value for

shareholders improves trust as well as reliability. Management accounting experts are known to

be ethical, responsible, and aware of the organization’s ideals, governance prerequisites, and

interpersonal commitments.

Being aware of inconsistent interests boosts stakeholder management and is also an essential factor

when it comes to prioritizing stakeholder units. Proactively trying to get feedback and being

receptive to queries or bad feedback allows for surveillance by people that have a vested interest

in the organization’s overall productivity. This improves the credibility, reputation, and

authenticity of the company and bears a favorable effect on strengthening processes and authority.

decision along with the decision method being employed. By getting to grips with the requirements

of shareholders, the most relevant and useful information for decision-making is determined,

obtained, and arranged for evaluation.

It needs maintaining a proper balance between: Past, present, as well as future-dependent info;

External and Internal information; Financial as well as nonfinancial details, such as ecological and

social concerns.

(Alika Cooper, 2020)

❖ Value

The influence on value is estimated. Management accounting links the organization’s processes to

its core enterprise model and demands an intensive knowledge of the broader macroeconomic

atmosphere. It entails assessing information along the value-generation pathway, gauging possible

opportunities, and concentrating on the risks, expenses as well as the value-generation possibility

of opportunities.

Situation analysis adds rigor to the review of organizational decisions. By using situation models

to assess the effect of specific opportunities and challenges, businesses can make better decisions

regarding terminating or taking advantage of them. The models furthermore allow firms to

quantify the possibility of a chance to become successful or risk arising and the value which needs

to be produced or eroded.

(Alika Cooper, 2020)

❖ Credibility

Stewardship forms credibility. Responsibility and scrutiny help in making the decision-making

process a lot more purposeful. Managing near-term business interests against long-run value for

shareholders improves trust as well as reliability. Management accounting experts are known to

be ethical, responsible, and aware of the organization’s ideals, governance prerequisites, and

interpersonal commitments.

Being aware of inconsistent interests boosts stakeholder management and is also an essential factor

when it comes to prioritizing stakeholder units. Proactively trying to get feedback and being

receptive to queries or bad feedback allows for surveillance by people that have a vested interest

in the organization’s overall productivity. This improves the credibility, reputation, and

authenticity of the company and bears a favorable effect on strengthening processes and authority.

9

(Alika Cooper, 2020)

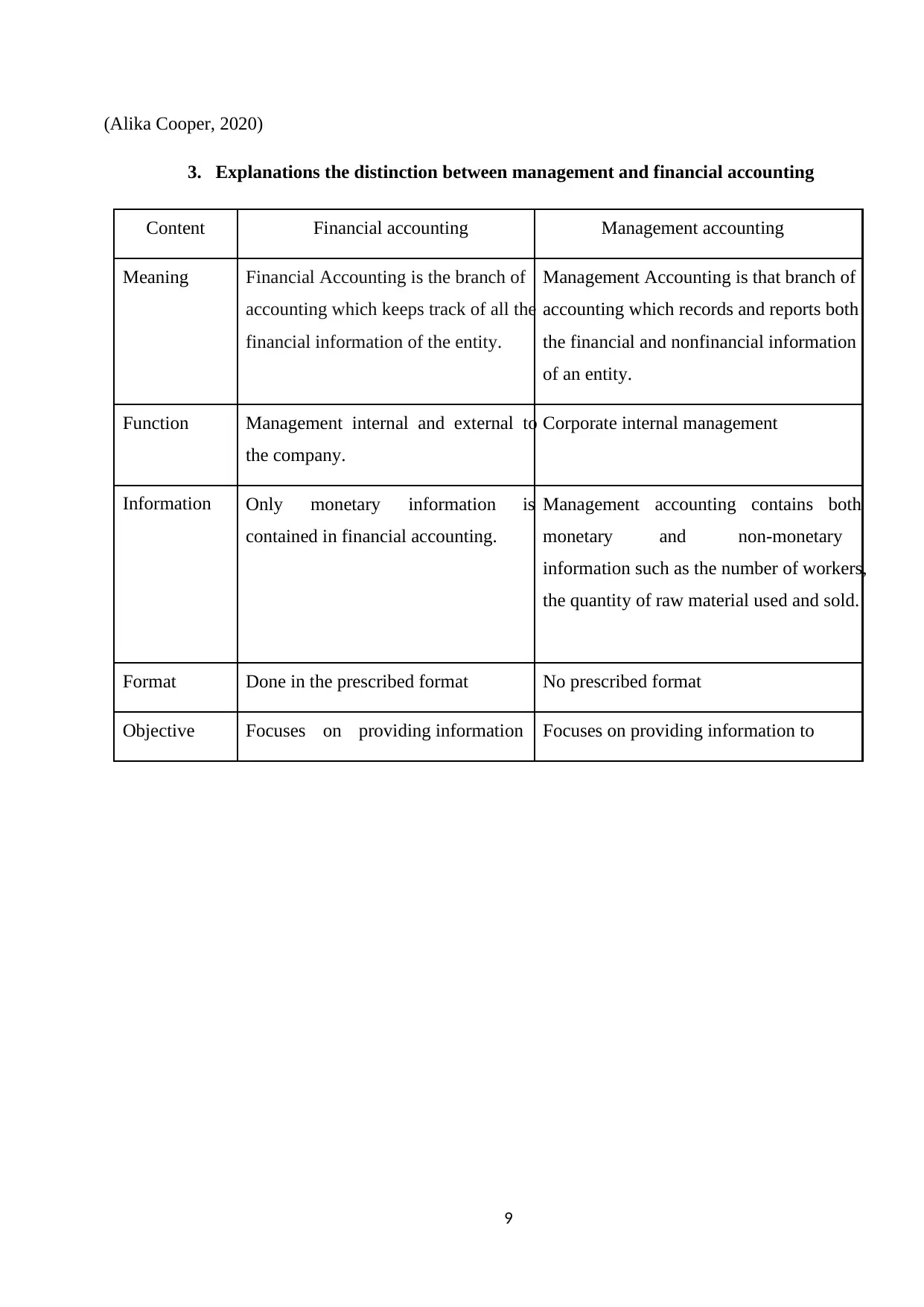

3. Explanations the distinction between management and financial accounting

Content Financial accounting Management accounting

Meaning Financial Accounting is the branch of

accounting which keeps track of all the

financial information of the entity.

Management Accounting is that branch of

accounting which records and reports both

the financial and nonfinancial information

of an entity.

Function Management internal and external to

the company.

Corporate internal management

Information Only monetary information is

contained in financial accounting.

Management accounting contains both

monetary and non-monetary

information such as the number of workers,

the quantity of raw material used and sold.

Format Done in the prescribed format No prescribed format

Objective Focuses on providing information Focuses on providing information to

(Alika Cooper, 2020)

3. Explanations the distinction between management and financial accounting

Content Financial accounting Management accounting

Meaning Financial Accounting is the branch of

accounting which keeps track of all the

financial information of the entity.

Management Accounting is that branch of

accounting which records and reports both

the financial and nonfinancial information

of an entity.

Function Management internal and external to

the company.

Corporate internal management

Information Only monetary information is

contained in financial accounting.

Management accounting contains both

monetary and non-monetary

information such as the number of workers,

the quantity of raw material used and sold.

Format Done in the prescribed format No prescribed format

Objective Focuses on providing information Focuses on providing information to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1

about the functioning of the entity’s

business to its users.

help them in evaluating the performance

and devising plans for the future.

Time Frame Financial Accounting is mainly done

for a specific period, which is usually

one year.

The management accounting is done as

per the needs of the management say

quarterly, half yearly.

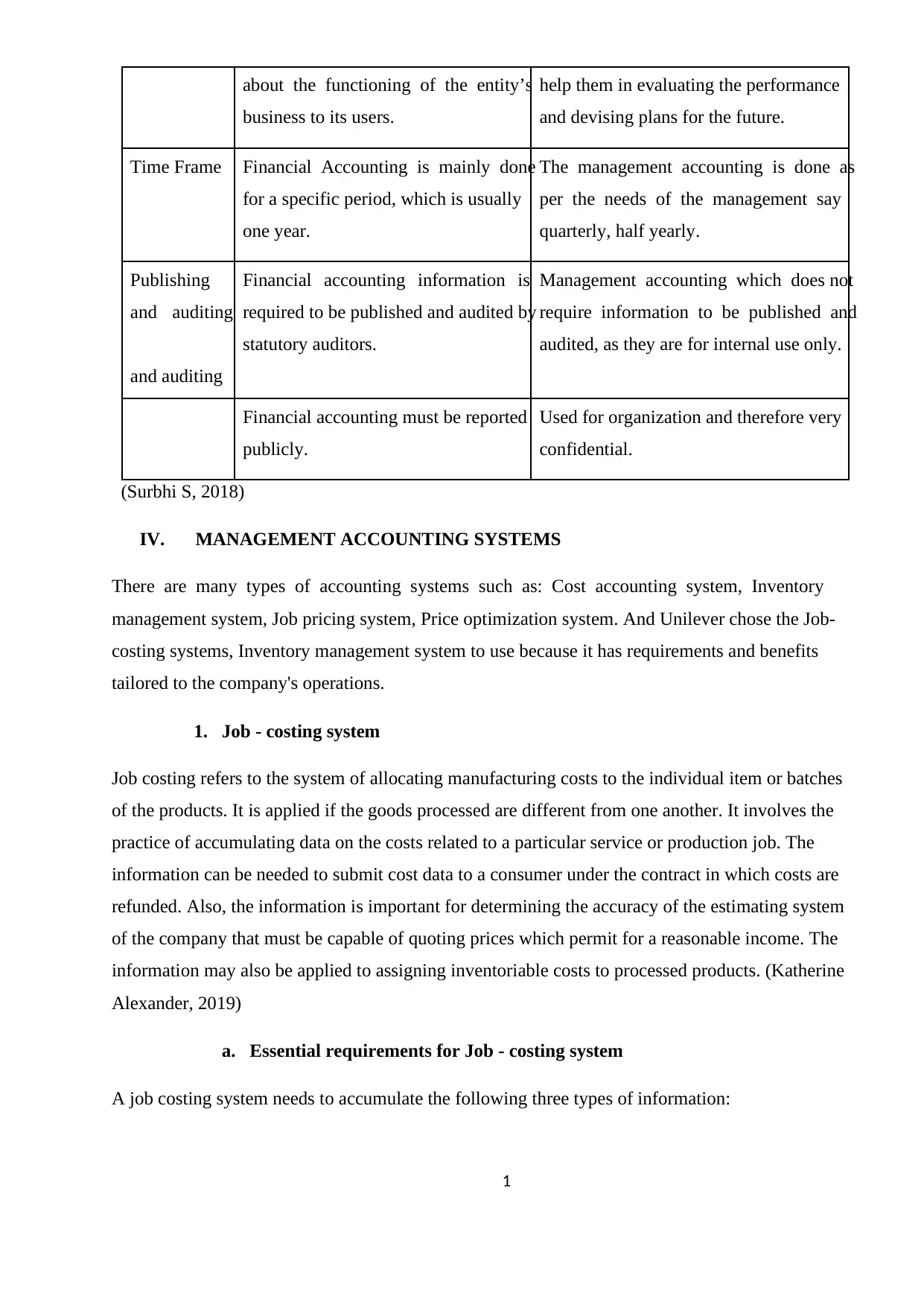

Publishing

and auditing

and auditing

Financial accounting information is

required to be published and audited by

statutory auditors.

Management accounting which does not

require information to be published and

audited, as they are for internal use only.

Financial accounting must be reported

publicly.

Used for organization and therefore very

confidential.

(Surbhi S, 2018)

IV. MANAGEMENT ACCOUNTING SYSTEMS

There are many types of accounting systems such as: Cost accounting system, Inventory

management system, Job pricing system, Price optimization system. And Unilever chose the Job-

costing systems, Inventory management system to use because it has requirements and benefits

tailored to the company's operations.

1. Job - costing system

Job costing refers to the system of allocating manufacturing costs to the individual item or batches

of the products. It is applied if the goods processed are different from one another. It involves the

practice of accumulating data on the costs related to a particular service or production job. The

information can be needed to submit cost data to a consumer under the contract in which costs are

refunded. Also, the information is important for determining the accuracy of the estimating system

of the company that must be capable of quoting prices which permit for a reasonable income. The

information may also be applied to assigning inventoriable costs to processed products. (Katherine

Alexander, 2019)

a. Essential requirements for Job - costing system

A job costing system needs to accumulate the following three types of information:

about the functioning of the entity’s

business to its users.

help them in evaluating the performance

and devising plans for the future.

Time Frame Financial Accounting is mainly done

for a specific period, which is usually

one year.

The management accounting is done as

per the needs of the management say

quarterly, half yearly.

Publishing

and auditing

and auditing

Financial accounting information is

required to be published and audited by

statutory auditors.

Management accounting which does not

require information to be published and

audited, as they are for internal use only.

Financial accounting must be reported

publicly.

Used for organization and therefore very

confidential.

(Surbhi S, 2018)

IV. MANAGEMENT ACCOUNTING SYSTEMS

There are many types of accounting systems such as: Cost accounting system, Inventory

management system, Job pricing system, Price optimization system. And Unilever chose the Job-

costing systems, Inventory management system to use because it has requirements and benefits

tailored to the company's operations.

1. Job - costing system

Job costing refers to the system of allocating manufacturing costs to the individual item or batches

of the products. It is applied if the goods processed are different from one another. It involves the

practice of accumulating data on the costs related to a particular service or production job. The

information can be needed to submit cost data to a consumer under the contract in which costs are

refunded. Also, the information is important for determining the accuracy of the estimating system

of the company that must be capable of quoting prices which permit for a reasonable income. The

information may also be applied to assigning inventoriable costs to processed products. (Katherine

Alexander, 2019)

a. Essential requirements for Job - costing system

A job costing system needs to accumulate the following three types of information:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

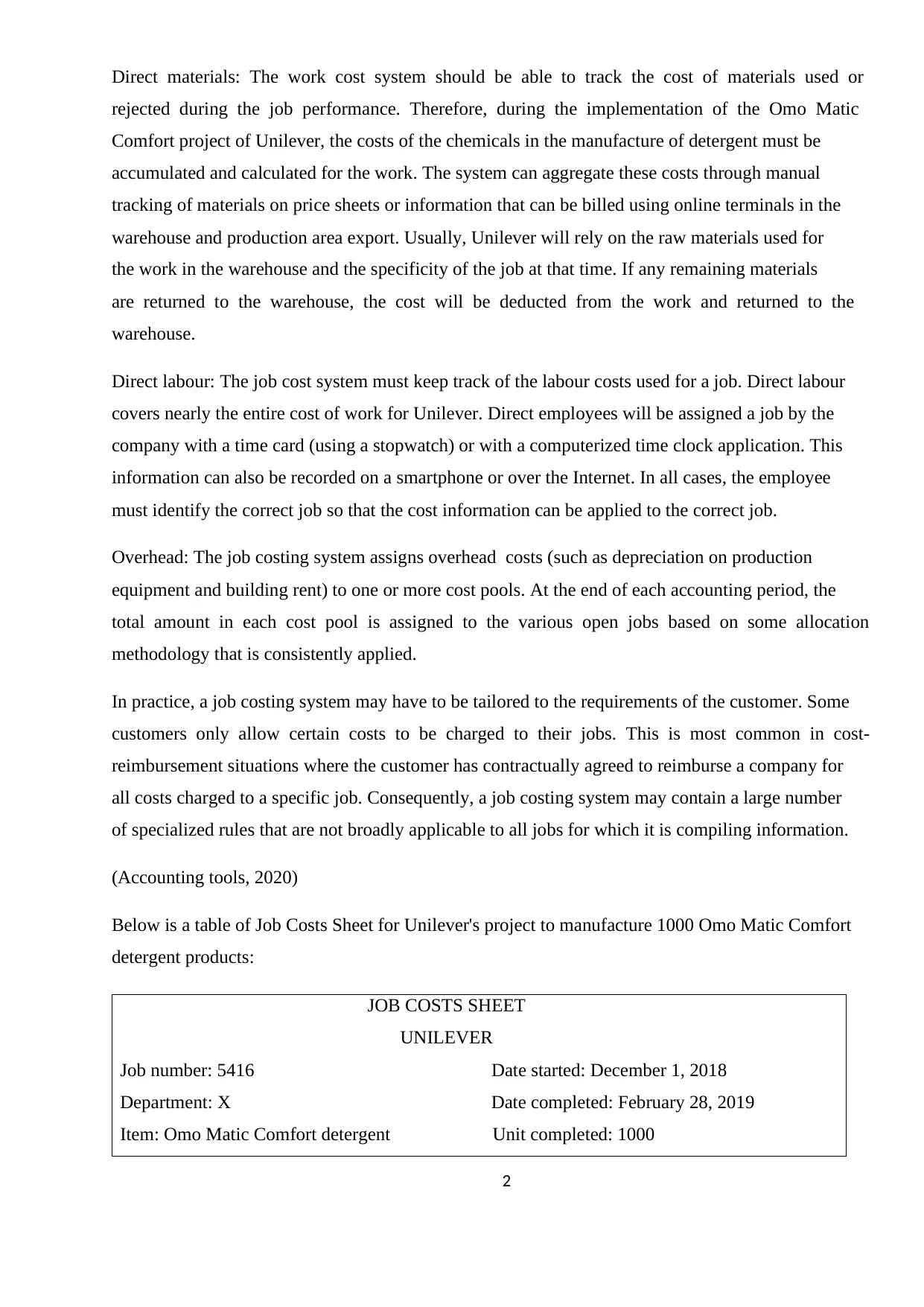

Direct materials: The work cost system should be able to track the cost of materials used or

rejected during the job performance. Therefore, during the implementation of the Omo Matic

Comfort project of Unilever, the costs of the chemicals in the manufacture of detergent must be

accumulated and calculated for the work. The system can aggregate these costs through manual

tracking of materials on price sheets or information that can be billed using online terminals in the

warehouse and production area export. Usually, Unilever will rely on the raw materials used for

the work in the warehouse and the specificity of the job at that time. If any remaining materials

are returned to the warehouse, the cost will be deducted from the work and returned to the

warehouse.

Direct labour: The job cost system must keep track of the labour costs used for a job. Direct labour

covers nearly the entire cost of work for Unilever. Direct employees will be assigned a job by the

company with a time card (using a stopwatch) or with a computerized time clock application. This

information can also be recorded on a smartphone or over the Internet. In all cases, the employee

must identify the correct job so that the cost information can be applied to the correct job.

Overhead: The job costing system assigns overhead costs (such as depreciation on production

equipment and building rent) to one or more cost pools. At the end of each accounting period, the

total amount in each cost pool is assigned to the various open jobs based on some allocation

methodology that is consistently applied.

In practice, a job costing system may have to be tailored to the requirements of the customer. Some

customers only allow certain costs to be charged to their jobs. This is most common in cost-

reimbursement situations where the customer has contractually agreed to reimburse a company for

all costs charged to a specific job. Consequently, a job costing system may contain a large number

of specialized rules that are not broadly applicable to all jobs for which it is compiling information.

(Accounting tools, 2020)

Below is a table of Job Costs Sheet for Unilever's project to manufacture 1000 Omo Matic Comfort

detergent products:

JOB COSTS SHEET

UNILEVER

Job number: 5416 Date started: December 1, 2018

Department: X Date completed: February 28, 2019

Item: Omo Matic Comfort detergent Unit completed: 1000

Direct materials: The work cost system should be able to track the cost of materials used or

rejected during the job performance. Therefore, during the implementation of the Omo Matic

Comfort project of Unilever, the costs of the chemicals in the manufacture of detergent must be

accumulated and calculated for the work. The system can aggregate these costs through manual

tracking of materials on price sheets or information that can be billed using online terminals in the

warehouse and production area export. Usually, Unilever will rely on the raw materials used for

the work in the warehouse and the specificity of the job at that time. If any remaining materials

are returned to the warehouse, the cost will be deducted from the work and returned to the

warehouse.

Direct labour: The job cost system must keep track of the labour costs used for a job. Direct labour

covers nearly the entire cost of work for Unilever. Direct employees will be assigned a job by the

company with a time card (using a stopwatch) or with a computerized time clock application. This

information can also be recorded on a smartphone or over the Internet. In all cases, the employee

must identify the correct job so that the cost information can be applied to the correct job.

Overhead: The job costing system assigns overhead costs (such as depreciation on production

equipment and building rent) to one or more cost pools. At the end of each accounting period, the

total amount in each cost pool is assigned to the various open jobs based on some allocation

methodology that is consistently applied.

In practice, a job costing system may have to be tailored to the requirements of the customer. Some

customers only allow certain costs to be charged to their jobs. This is most common in cost-

reimbursement situations where the customer has contractually agreed to reimburse a company for

all costs charged to a specific job. Consequently, a job costing system may contain a large number

of specialized rules that are not broadly applicable to all jobs for which it is compiling information.

(Accounting tools, 2020)

Below is a table of Job Costs Sheet for Unilever's project to manufacture 1000 Omo Matic Comfort

detergent products:

JOB COSTS SHEET

UNILEVER

Job number: 5416 Date started: December 1, 2018

Department: X Date completed: February 28, 2019

Item: Omo Matic Comfort detergent Unit completed: 1000

3

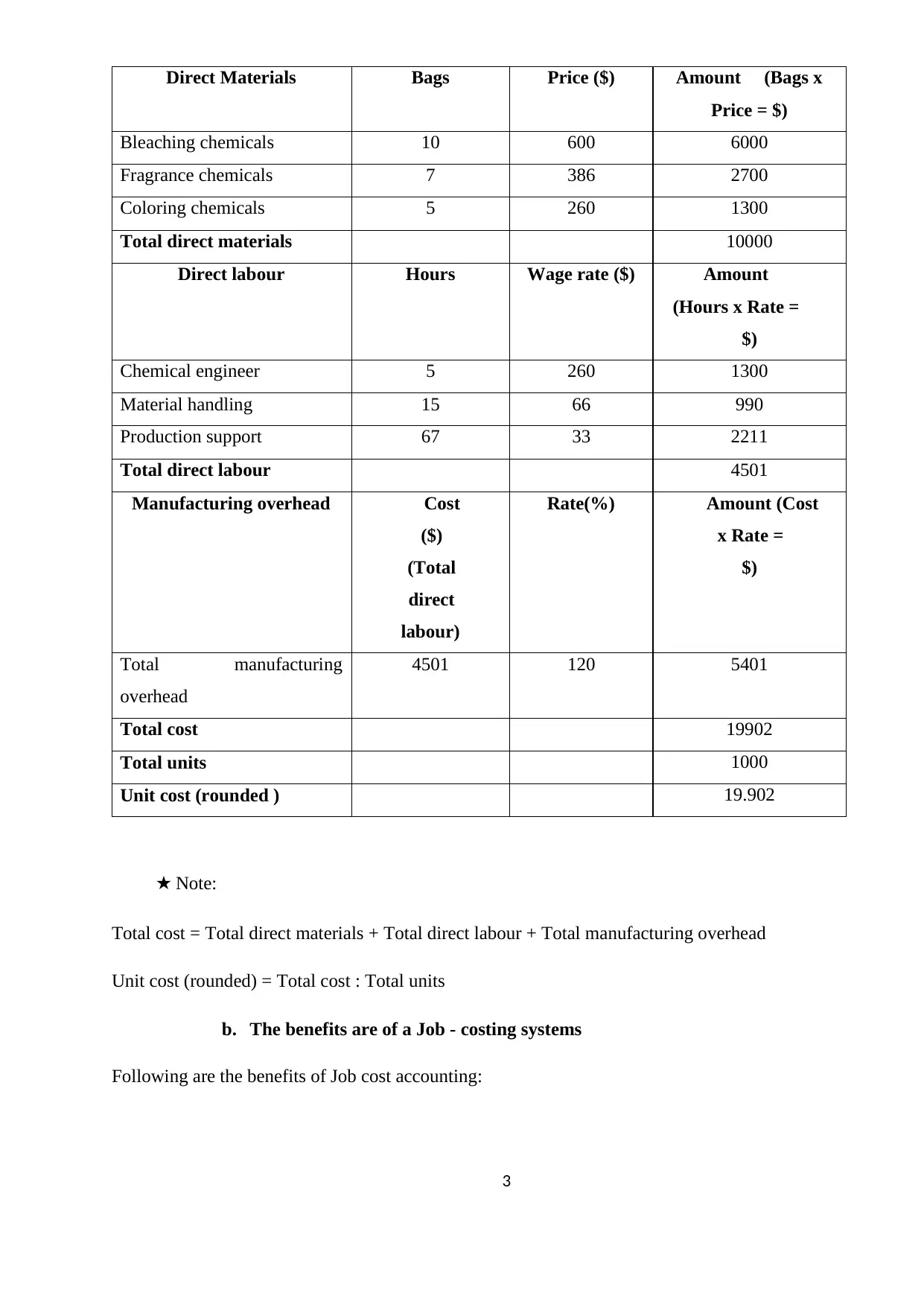

Direct Materials Bags Price ($) Amount (Bags x

Price = $)

Bleaching chemicals 10 600 6000

Fragrance chemicals 7 386 2700

Coloring chemicals 5 260 1300

Total direct materials 10000

Direct labour Hours Wage rate ($) Amount

(Hours x Rate =

$)

Chemical engineer 5 260 1300

Material handling 15 66 990

Production support 67 33 2211

Total direct labour 4501

Manufacturing overhead Cost

($)

(Total

direct

labour)

Rate(%) Amount (Cost

x Rate =

$)

Total manufacturing

overhead

4501 120 5401

Total cost 19902

Total units 1000

Unit cost (rounded ) 19.902

★ Note:

Total cost = Total direct materials + Total direct labour + Total manufacturing overhead

Unit cost (rounded) = Total cost : Total units

b. The benefits are of a Job - costing systems

Following are the benefits of Job cost accounting:

Direct Materials Bags Price ($) Amount (Bags x

Price = $)

Bleaching chemicals 10 600 6000

Fragrance chemicals 7 386 2700

Coloring chemicals 5 260 1300

Total direct materials 10000

Direct labour Hours Wage rate ($) Amount

(Hours x Rate =

$)

Chemical engineer 5 260 1300

Material handling 15 66 990

Production support 67 33 2211

Total direct labour 4501

Manufacturing overhead Cost

($)

(Total

direct

labour)

Rate(%) Amount (Cost

x Rate =

$)

Total manufacturing

overhead

4501 120 5401

Total cost 19902

Total units 1000

Unit cost (rounded ) 19.902

★ Note:

Total cost = Total direct materials + Total direct labour + Total manufacturing overhead

Unit cost (rounded) = Total cost : Total units

b. The benefits are of a Job - costing systems

Following are the benefits of Job cost accounting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.