Detailed Management Accounting Report: Oshodi Plc, Unit 5 Analysis

VerifiedAdded on 2021/02/19

|33

|7481

|64

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Oshodi Plc, a manufacturing company specializing in JOJO fruit juice. The report covers key aspects of management accounting, including the essential requirements of various accounting systems such as cost accounting, inventory management, price optimization, and job costing. It delves into the benefits of these systems, emphasizing their role in decision-making, cost reduction, and profit maximization. Furthermore, the report explores different management accounting reports, such as inventory management and accounts receivable reports, highlighting their significance in organizational processes. The report also examines cost analysis techniques using marginal and absorption costing, budgetary control planning tools, and the adaptation of management accounting systems to address financial challenges. The analysis includes the integration of reports within organizational processes and the contribution of management accounting to the sustainable success of Oshodi Plc, providing valuable insights for internal stakeholders and aiding in effective business management and decision-making.

Unit 5. Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of management accounting systems...1

M1 benefits of management Accounting systems......................................................................3

D1 Integration of management accounting system and report within organisational process....4

P2 Different methods of management accounting reports .........................................................4

TASK 2............................................................................................................................................6

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal

and absorption costing.................................................................................................................6

M2 Applying range of management accounting techniques.......................................................8

D2 Interpretation of above data...................................................................................................8

TASK 3............................................................................................................................................9

P4 Advantages of different planning tools used for budgetary control......................................9

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets ..................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Adoption of management accounting systems to respond financial problems ...................10

M4 Contribution of management accounting in sustainable success of the organisation while

responding financial problems..................................................................................................12

D3 Application of planning tools to respond financial issue along with attainment of

sustainable success ...................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and essential requirements of management accounting systems...1

M1 benefits of management Accounting systems......................................................................3

D1 Integration of management accounting system and report within organisational process....4

P2 Different methods of management accounting reports .........................................................4

TASK 2............................................................................................................................................6

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal

and absorption costing.................................................................................................................6

M2 Applying range of management accounting techniques.......................................................8

D2 Interpretation of above data...................................................................................................8

TASK 3............................................................................................................................................9

P4 Advantages of different planning tools used for budgetary control......................................9

M3 Analyse the use of different planning tools and their application for preparing and

forecasting budgets ..................................................................................................................10

TASK 4..........................................................................................................................................10

P5 Adoption of management accounting systems to respond financial problems ...................10

M4 Contribution of management accounting in sustainable success of the organisation while

responding financial problems..................................................................................................12

D3 Application of planning tools to respond financial issue along with attainment of

sustainable success ...................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the concept which includes analysis of business activities of

the internal management that facilitate in better decision making. This will includes the usage of

provisions of accounting to ascertain the financial and statistical information which further aid

effective controlling of business functions which results in accomplishment of organisational

objectives within stipulated period of time (Seal and Mattimoe, 2014). These will also know as

cost accounting which aid to analyse business costs that further aid in preparation of financial

reports that depicts the functioning of internal departments of the organisations. This will allows

the internal stakeholders of the organisations to perfectly align their interests with the procedures

of the organisation to bring efficiency in their own working. Oshodi Plc is a manufacturing

company which have specialisation in production of JOJO fruit juice across all age brackets. The

main objective behind the preparation of this report is to provide information to the internal

stakeholders of the organisation about the relation and functioning of the internal departments for

better decision making.

This report covers the concept of management accounting and the essential requirement

of different management accounting systems, different methods of management accounting

reports and usage of the appropriate techniques of cost analysis in preparation of income

statement using marginal and absorption costing. Also, analyse the advantages and disadvantages

of planning tools for budgetary control and adaptation of the management accounting systems to

respond financial problems is covered in the report.

TASK 1

P1 Management accounting and essential requirements of management accounting systems

Introduction: Management accounting system includes the preparation of different kind

of accounts which help to ascertain the information about the performance of internal

departments. The different systems which are prepared named as Cost accounting, job costing

etc. Oshodi is manufacturing organisation and operate their operations in respect of the

preparation of JOJO fruit juice. Through effective adoption of the management accounting and

its systems, organisation wants to improve their decision-making to get predetermined results.

This part covers concept of management accounting and requirement of different type of systems

(Al-Mawali, Zainuddin and Nasir Kader Ali, 2012).

1

Management accounting is the concept which includes analysis of business activities of

the internal management that facilitate in better decision making. This will includes the usage of

provisions of accounting to ascertain the financial and statistical information which further aid

effective controlling of business functions which results in accomplishment of organisational

objectives within stipulated period of time (Seal and Mattimoe, 2014). These will also know as

cost accounting which aid to analyse business costs that further aid in preparation of financial

reports that depicts the functioning of internal departments of the organisations. This will allows

the internal stakeholders of the organisations to perfectly align their interests with the procedures

of the organisation to bring efficiency in their own working. Oshodi Plc is a manufacturing

company which have specialisation in production of JOJO fruit juice across all age brackets. The

main objective behind the preparation of this report is to provide information to the internal

stakeholders of the organisation about the relation and functioning of the internal departments for

better decision making.

This report covers the concept of management accounting and the essential requirement

of different management accounting systems, different methods of management accounting

reports and usage of the appropriate techniques of cost analysis in preparation of income

statement using marginal and absorption costing. Also, analyse the advantages and disadvantages

of planning tools for budgetary control and adaptation of the management accounting systems to

respond financial problems is covered in the report.

TASK 1

P1 Management accounting and essential requirements of management accounting systems

Introduction: Management accounting system includes the preparation of different kind

of accounts which help to ascertain the information about the performance of internal

departments. The different systems which are prepared named as Cost accounting, job costing

etc. Oshodi is manufacturing organisation and operate their operations in respect of the

preparation of JOJO fruit juice. Through effective adoption of the management accounting and

its systems, organisation wants to improve their decision-making to get predetermined results.

This part covers concept of management accounting and requirement of different type of systems

(Al-Mawali, Zainuddin and Nasir Kader Ali, 2012).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting: This is the process of formulating accounts that provide

accurate statistical and financial information which is required by the mangers of the

organisation to made day to decisions (Management Accounting, 2018).

It is totally different from financial accounting where annual reports are prepared for the

use of external stakeholders. This will only include about the preparation of monthly and weekly

accounts for internal stakeholders of the organisation. The different kind of systems provides the

information in respect of the various terms like sales revenue generated, cash, B/R, B/P etc.

Management accounting systems: These are the systems which are prepared by the

management accountant to grab the information about the actual working ability of the different

departments of the organisations. The different type of systems which are generally formulated

by the accountant of the organisation includes cost accounting, job costing, price optimisation,

inventory management systems etc. The basic function which is further performing by the

management of the organisation through analysis of the information gathered from the different

accounts includes planning, organising, controlling and decision-making. All these accounts

have their own different aspect and advantage towards the organisation. The different kind of

benefits which are gathered by the management of Oshodi from consideration of these systems is

about effective decision-making, cost cutting, building higher profit margin etc. The essential

requirement of the different management accounting systems to Oshodi is understood from the

below description:-

Cost accounting system: It is an accounting method which is used by Oshodi to

ascertain the amount of total cost of production with the help of the analysis of input costs of

each step which indulge in production process. The same is used by Oshodi to analyse the cost

behind the preparation of JOJO fruit juice. In this regard, accountant first analyses and record

these costs individually and then after compare the input results with actual to ascertain the

financial performance (Chiu, Teoh and Tian, 2012). This will help an organisation get the

information about the contribution of the fruit juice in profit generation of company.

Inventory management system: This is the important account which is used by the

Oshodi to analyse and track the level of inventory, orders, sales and deliveries. The information

gathered from the usage of this accounting system is further used by the organisation in

formulation of work order, bill of materials and other production documents which indulge in the

process of the preparation of JOJO fruit juice. This is used by the management of Oshodi is

2

accurate statistical and financial information which is required by the mangers of the

organisation to made day to decisions (Management Accounting, 2018).

It is totally different from financial accounting where annual reports are prepared for the

use of external stakeholders. This will only include about the preparation of monthly and weekly

accounts for internal stakeholders of the organisation. The different kind of systems provides the

information in respect of the various terms like sales revenue generated, cash, B/R, B/P etc.

Management accounting systems: These are the systems which are prepared by the

management accountant to grab the information about the actual working ability of the different

departments of the organisations. The different type of systems which are generally formulated

by the accountant of the organisation includes cost accounting, job costing, price optimisation,

inventory management systems etc. The basic function which is further performing by the

management of the organisation through analysis of the information gathered from the different

accounts includes planning, organising, controlling and decision-making. All these accounts

have their own different aspect and advantage towards the organisation. The different kind of

benefits which are gathered by the management of Oshodi from consideration of these systems is

about effective decision-making, cost cutting, building higher profit margin etc. The essential

requirement of the different management accounting systems to Oshodi is understood from the

below description:-

Cost accounting system: It is an accounting method which is used by Oshodi to

ascertain the amount of total cost of production with the help of the analysis of input costs of

each step which indulge in production process. The same is used by Oshodi to analyse the cost

behind the preparation of JOJO fruit juice. In this regard, accountant first analyses and record

these costs individually and then after compare the input results with actual to ascertain the

financial performance (Chiu, Teoh and Tian, 2012). This will help an organisation get the

information about the contribution of the fruit juice in profit generation of company.

Inventory management system: This is the important account which is used by the

Oshodi to analyse and track the level of inventory, orders, sales and deliveries. The information

gathered from the usage of this accounting system is further used by the organisation in

formulation of work order, bill of materials and other production documents which indulge in the

process of the preparation of JOJO fruit juice. This is used by the management of Oshodi is

2

about tracking of the entire supply chain that covers everything from production to retail. This

will further aid in better decision making about the availability of the raw material and

continuous production of JOJO fruit juice. The different kind of methods which can be used in

the process of effective inventory calculation is about LIFO, FIFO and AVCO. At present, EOQ

is used by the organisation to analyse the time period about when they have to make re-order of

the raw material to continue their production activities without any infringements (DRURY,

2013).

Price optimisation system: This system is used by the accountant of the Oshodi to

analyse the behaviour of consumers to different price of their offerings. At present, this system is

used to ascertain the impact over the sales of JOJO fruit juice when management increase or

decrease the price of the same. This will help the management of the organisation to determine

the proper retail value of their fruit juice which they have to ask from their consumers in market

which results in ascertainment of maximum output in terms of sales revenue.

Job costing system: This system is used by the manufacturing organisation which has

different production activities and jobs. This will used normally use by the accountants to

analyse and track the cost and revenue generated by particular job. This will further aid in

ascertainment of the amount of profit that can be gathered from the effective performance of the

job. The same is used by the Oshodi in case of their JOJO fruit juice to ascertain the cost and

revenue from its production. Here, different job numbers are assigned to individual items of

expenses and revenues. This will provides an opportunity to the management to keep track over

the expenses and take necessary steps to improve their profit margin through reduction in cost.

Summary: It is concluded from this part that management accounting is important

concept which help in building effective relation in between the different departments of the

organisation. Also, different accounting systems provides the information about the different

aspects like expenses, sales and revenue which further improves the decision-making of the

management to improve profitability (Eierle and Schultze, 2013).

M1 benefits of management Accounting systems

Type of management accounting system Benefits

Cost accounting system It is linked with the controlling cost under

3

will further aid in better decision making about the availability of the raw material and

continuous production of JOJO fruit juice. The different kind of methods which can be used in

the process of effective inventory calculation is about LIFO, FIFO and AVCO. At present, EOQ

is used by the organisation to analyse the time period about when they have to make re-order of

the raw material to continue their production activities without any infringements (DRURY,

2013).

Price optimisation system: This system is used by the accountant of the Oshodi to

analyse the behaviour of consumers to different price of their offerings. At present, this system is

used to ascertain the impact over the sales of JOJO fruit juice when management increase or

decrease the price of the same. This will help the management of the organisation to determine

the proper retail value of their fruit juice which they have to ask from their consumers in market

which results in ascertainment of maximum output in terms of sales revenue.

Job costing system: This system is used by the manufacturing organisation which has

different production activities and jobs. This will used normally use by the accountants to

analyse and track the cost and revenue generated by particular job. This will further aid in

ascertainment of the amount of profit that can be gathered from the effective performance of the

job. The same is used by the Oshodi in case of their JOJO fruit juice to ascertain the cost and

revenue from its production. Here, different job numbers are assigned to individual items of

expenses and revenues. This will provides an opportunity to the management to keep track over

the expenses and take necessary steps to improve their profit margin through reduction in cost.

Summary: It is concluded from this part that management accounting is important

concept which help in building effective relation in between the different departments of the

organisation. Also, different accounting systems provides the information about the different

aspects like expenses, sales and revenue which further improves the decision-making of the

management to improve profitability (Eierle and Schultze, 2013).

M1 benefits of management Accounting systems

Type of management accounting system Benefits

Cost accounting system It is linked with the controlling cost under

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

standards. This system helps Oshodi to

measure the efficiency of different processes as

well as assist to bring further improvements.

Inventory management system This system is associated with tracking the

record of availability of materials in

warehouses. In above Oshodi company, it is

helping in improving accuracy of its inventory

order. As well as it is beneficial in effective

production of JOJO fruit juice

Price optimisation system It is related with the setting prices on an

effective level so that customers can afford. In

the above company, it is helping to ascertain

the behaviour of consumers based on different

prices of JOJO fruit juice. Along with, it is

helping to Oshodi to maximise its operating

profit with adoption of best prices

Job costing system

This is related to assigning cost to each job

separately. In the Oshodi company, it is

helping in estimation of all type of costs in

process of preparation of JOJO fruit juice. As

well as it is also helping in reduction of

duplication of efforts in Oshodi (Granlund and

Lukka, 2017).

D1 Integration of management accounting system and report within organisational process

Type of reporting & Systems Integration with organisational process

Inventory management report: This report

is prepared on the basis of the integration of

the information gathered from system.

Integration of report in organisational process is

understood from the point that it help Oshodi to

manage raw materials of JOJO fruit juice and

4

measure the efficiency of different processes as

well as assist to bring further improvements.

Inventory management system This system is associated with tracking the

record of availability of materials in

warehouses. In above Oshodi company, it is

helping in improving accuracy of its inventory

order. As well as it is beneficial in effective

production of JOJO fruit juice

Price optimisation system It is related with the setting prices on an

effective level so that customers can afford. In

the above company, it is helping to ascertain

the behaviour of consumers based on different

prices of JOJO fruit juice. Along with, it is

helping to Oshodi to maximise its operating

profit with adoption of best prices

Job costing system

This is related to assigning cost to each job

separately. In the Oshodi company, it is

helping in estimation of all type of costs in

process of preparation of JOJO fruit juice. As

well as it is also helping in reduction of

duplication of efforts in Oshodi (Granlund and

Lukka, 2017).

D1 Integration of management accounting system and report within organisational process

Type of reporting & Systems Integration with organisational process

Inventory management report: This report

is prepared on the basis of the integration of

the information gathered from system.

Integration of report in organisational process is

understood from the point that it help Oshodi to

manage raw materials of JOJO fruit juice and

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

estimation of required level of purchase orders

Performance report: This report is

prepared on the basis of the information

ascertained from contribution of different

systems. This will includes about the actual

performance of different departments of

Oshodi

The integration of this report in process is

ascertain from the fact that this will help in

getting specialisation in production of JOJO fruit

juice as all the deviations and misalliances are

removed with the contribution of this report.

P2 Different methods of management accounting reports

Introduction: Management accounting report is a document which includes the

information about departmental functioning analysed from systems. This part covers about

different of accounting reports and their importance to an organisation.

Management Accounting Report: Accounting reports are important in nature and

provide clear insight that how business is performing (Ittner, 2014.Lääts and Haldma, 2012). In

the present report, different reports are formulated by the management of the Oshodi to bring

interrelation in between functioning of the departments of the organisation to grab desired

results. These reports are prepared every quarter which provide holistic view of business

finances. The different kind of reports which are prepared includes Inventory management

report, Accounts receivable report etc. All these reports have their own different importance

towards an organisation. The basic kind of benefits that can be seen over Oshodi is about high

amount of productivity, profitability etc.

Inventory management report: This is the report which includes the information about

inventories. The main objective of this report is about bringing balance between inventory

investment and customer service. This report provides the information to Oshodi is about the

level of raw materials they have in proper preparation of JOJO fruit juice. The main benefit of

this report to the organisation is about the maintaining the level of stock and raw material and

have control over the unnecessary costs and expenses which ultimate results in improvement of

profit margin (Morden, 2016).

Accounts receivable report: It is the report which provides the information about unpaid

customer services invoices and unused credit memos by date range. This report is used by the

Oshodi to analyse the overdue payment of their different consumers or debtors. Further, this

5

Performance report: This report is

prepared on the basis of the information

ascertained from contribution of different

systems. This will includes about the actual

performance of different departments of

Oshodi

The integration of this report in process is

ascertain from the fact that this will help in

getting specialisation in production of JOJO fruit

juice as all the deviations and misalliances are

removed with the contribution of this report.

P2 Different methods of management accounting reports

Introduction: Management accounting report is a document which includes the

information about departmental functioning analysed from systems. This part covers about

different of accounting reports and their importance to an organisation.

Management Accounting Report: Accounting reports are important in nature and

provide clear insight that how business is performing (Ittner, 2014.Lääts and Haldma, 2012). In

the present report, different reports are formulated by the management of the Oshodi to bring

interrelation in between functioning of the departments of the organisation to grab desired

results. These reports are prepared every quarter which provide holistic view of business

finances. The different kind of reports which are prepared includes Inventory management

report, Accounts receivable report etc. All these reports have their own different importance

towards an organisation. The basic kind of benefits that can be seen over Oshodi is about high

amount of productivity, profitability etc.

Inventory management report: This is the report which includes the information about

inventories. The main objective of this report is about bringing balance between inventory

investment and customer service. This report provides the information to Oshodi is about the

level of raw materials they have in proper preparation of JOJO fruit juice. The main benefit of

this report to the organisation is about the maintaining the level of stock and raw material and

have control over the unnecessary costs and expenses which ultimate results in improvement of

profit margin (Morden, 2016).

Accounts receivable report: It is the report which provides the information about unpaid

customer services invoices and unused credit memos by date range. This report is used by the

Oshodi to analyse the overdue payment of their different consumers or debtors. Further, this

5

report also help to look the credit period given to them and compare how much time is passed

from which the payment is due from such consumers or debtors. The importance of this report is

ascertained from the fact that this will help to tighten the credit policies and recover their due

amount within the time period which results to make the organisation financially sound.

Performance report: This report includes the information in respect of the performance

of something. This report is used by the management of Oshodi to analyse the performance of

their employees and working of the different departments that from their current performance

organisation is able to accomplish their desired targets or not. The main benefit which is

associated with this report is about ascertainment of the deviation in the performance in

comparison to the standards and takes appropriate corrective action. Such action allows

improving the performance and attainment of objective (Mussnig, 2013).

Conclusion: It has been concluded from the above part that reports have their own

contribution in success of the organisation as these will allows getting the information and taking

appropriate corrective action.

TASK 2

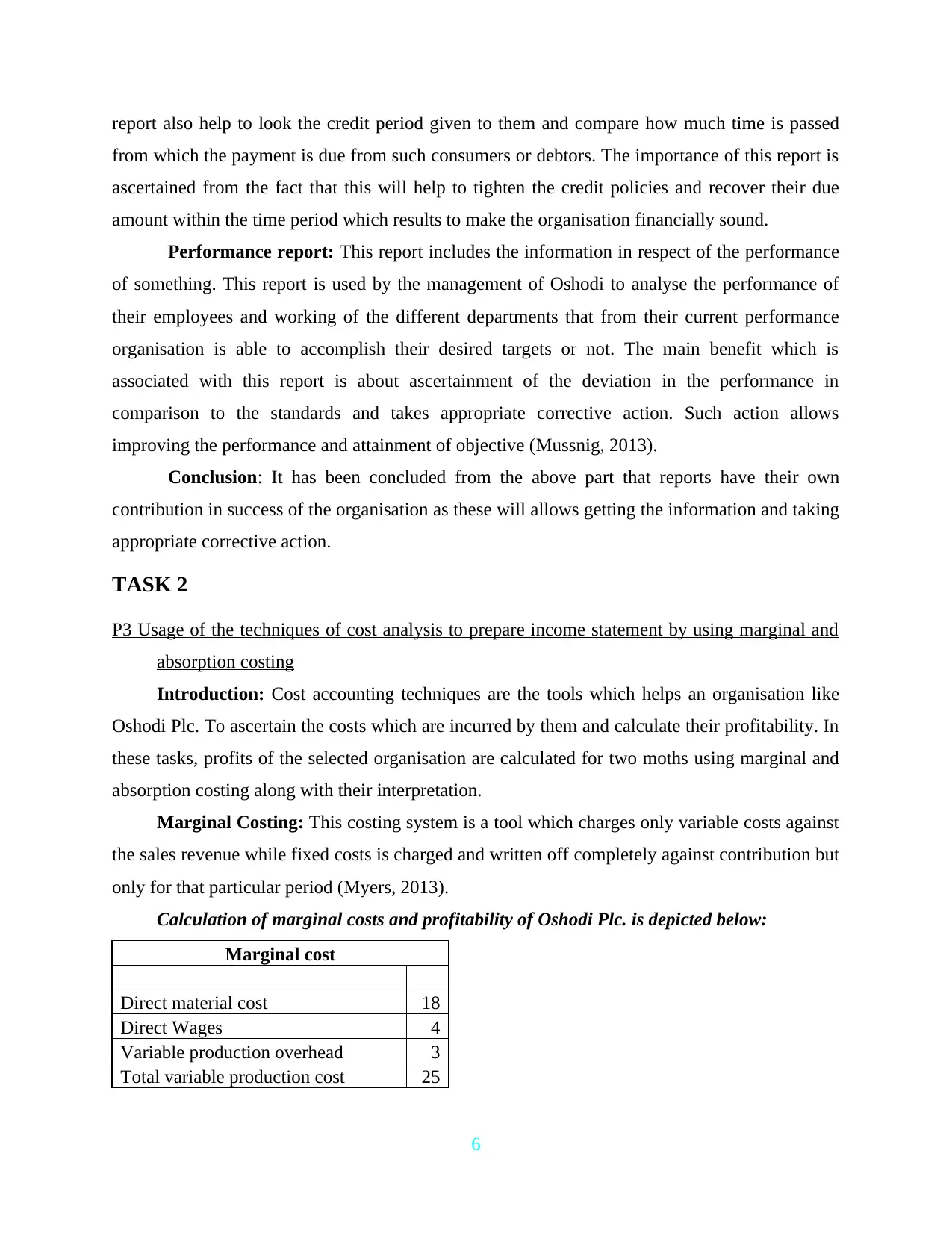

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing

Introduction: Cost accounting techniques are the tools which helps an organisation like

Oshodi Plc. To ascertain the costs which are incurred by them and calculate their profitability. In

these tasks, profits of the selected organisation are calculated for two moths using marginal and

absorption costing along with their interpretation.

Marginal Costing: This costing system is a tool which charges only variable costs against

the sales revenue while fixed costs is charged and written off completely against contribution but

only for that particular period (Myers, 2013).

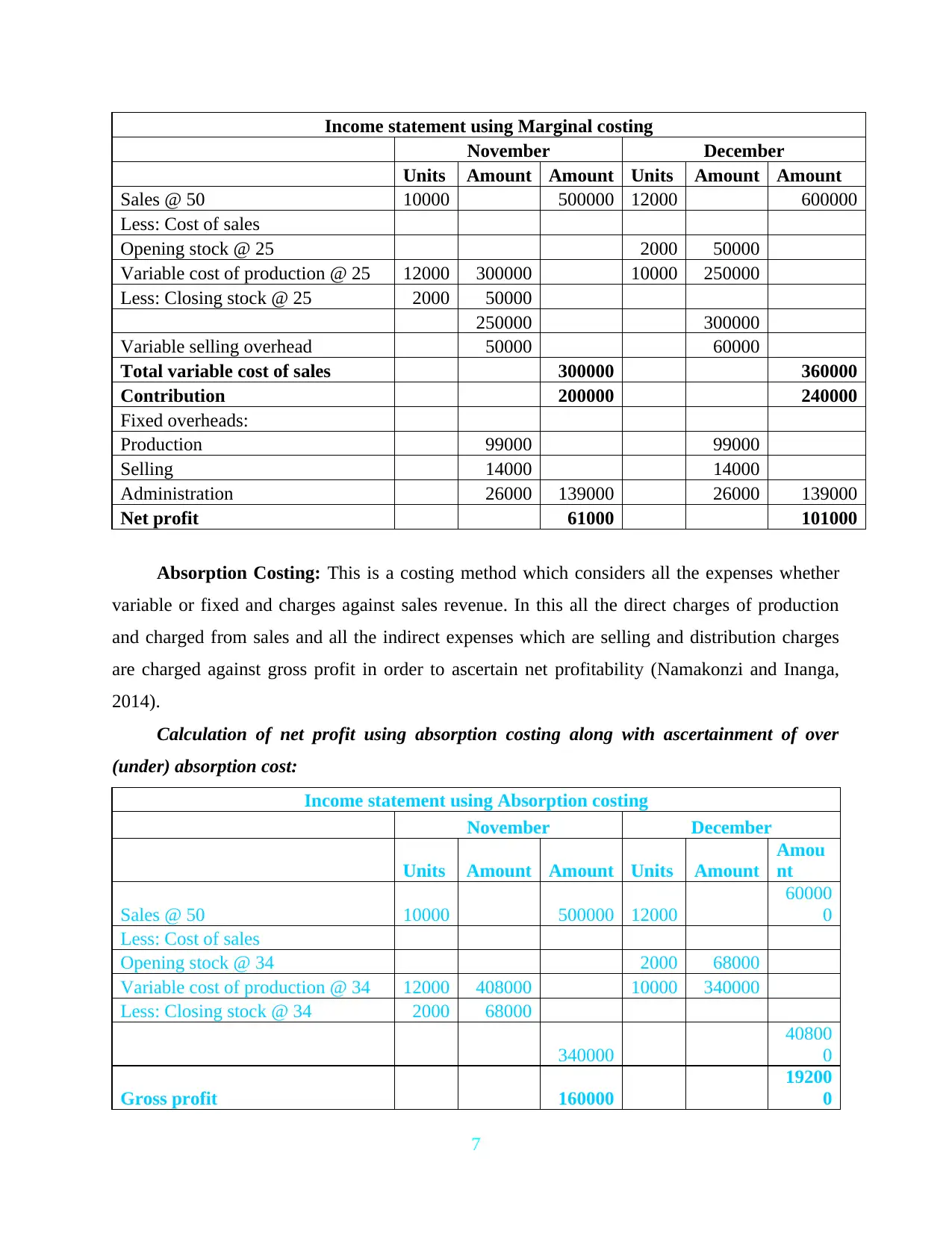

Calculation of marginal costs and profitability of Oshodi Plc. is depicted below:

Marginal cost

Direct material cost 18

Direct Wages 4

Variable production overhead 3

Total variable production cost 25

6

from which the payment is due from such consumers or debtors. The importance of this report is

ascertained from the fact that this will help to tighten the credit policies and recover their due

amount within the time period which results to make the organisation financially sound.

Performance report: This report includes the information in respect of the performance

of something. This report is used by the management of Oshodi to analyse the performance of

their employees and working of the different departments that from their current performance

organisation is able to accomplish their desired targets or not. The main benefit which is

associated with this report is about ascertainment of the deviation in the performance in

comparison to the standards and takes appropriate corrective action. Such action allows

improving the performance and attainment of objective (Mussnig, 2013).

Conclusion: It has been concluded from the above part that reports have their own

contribution in success of the organisation as these will allows getting the information and taking

appropriate corrective action.

TASK 2

P3 Usage of the techniques of cost analysis to prepare income statement by using marginal and

absorption costing

Introduction: Cost accounting techniques are the tools which helps an organisation like

Oshodi Plc. To ascertain the costs which are incurred by them and calculate their profitability. In

these tasks, profits of the selected organisation are calculated for two moths using marginal and

absorption costing along with their interpretation.

Marginal Costing: This costing system is a tool which charges only variable costs against

the sales revenue while fixed costs is charged and written off completely against contribution but

only for that particular period (Myers, 2013).

Calculation of marginal costs and profitability of Oshodi Plc. is depicted below:

Marginal cost

Direct material cost 18

Direct Wages 4

Variable production overhead 3

Total variable production cost 25

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income statement using Marginal costing

November December

Units Amount Amount Units Amount Amount

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 25 2000 50000

Variable cost of production @ 25 12000 300000 10000 250000

Less: Closing stock @ 25 2000 50000

250000 300000

Variable selling overhead 50000 60000

Total variable cost of sales 300000 360000

Contribution 200000 240000

Fixed overheads:

Production 99000 99000

Selling 14000 14000

Administration 26000 139000 26000 139000

Net profit 61000 101000

Absorption Costing: This is a costing method which considers all the expenses whether

variable or fixed and charges against sales revenue. In this all the direct charges of production

and charged from sales and all the indirect expenses which are selling and distribution charges

are charged against gross profit in order to ascertain net profitability (Namakonzi and Inanga,

2014).

Calculation of net profit using absorption costing along with ascertainment of over

(under) absorption cost:

Income statement using Absorption costing

November December

Units Amount Amount Units Amount

Amou

nt

Sales @ 50 10000 500000 12000

60000

0

Less: Cost of sales

Opening stock @ 34 2000 68000

Variable cost of production @ 34 12000 408000 10000 340000

Less: Closing stock @ 34 2000 68000

340000

40800

0

Gross profit 160000

19200

0

7

November December

Units Amount Amount Units Amount Amount

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 25 2000 50000

Variable cost of production @ 25 12000 300000 10000 250000

Less: Closing stock @ 25 2000 50000

250000 300000

Variable selling overhead 50000 60000

Total variable cost of sales 300000 360000

Contribution 200000 240000

Fixed overheads:

Production 99000 99000

Selling 14000 14000

Administration 26000 139000 26000 139000

Net profit 61000 101000

Absorption Costing: This is a costing method which considers all the expenses whether

variable or fixed and charges against sales revenue. In this all the direct charges of production

and charged from sales and all the indirect expenses which are selling and distribution charges

are charged against gross profit in order to ascertain net profitability (Namakonzi and Inanga,

2014).

Calculation of net profit using absorption costing along with ascertainment of over

(under) absorption cost:

Income statement using Absorption costing

November December

Units Amount Amount Units Amount

Amou

nt

Sales @ 50 10000 500000 12000

60000

0

Less: Cost of sales

Opening stock @ 34 2000 68000

Variable cost of production @ 34 12000 408000 10000 340000

Less: Closing stock @ 34 2000 68000

340000

40800

0

Gross profit 160000

19200

0

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

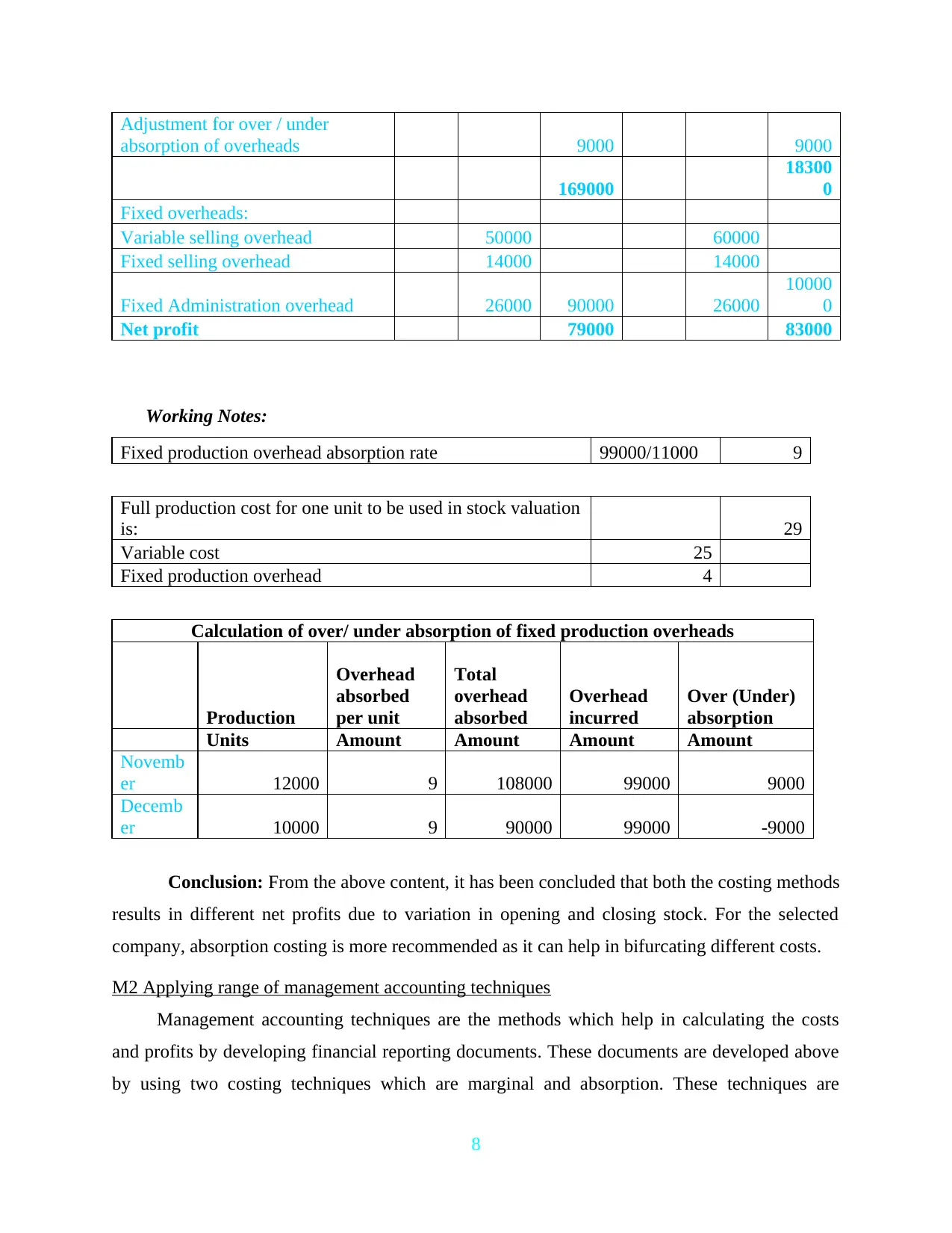

Adjustment for over / under

absorption of overheads 9000 9000

169000

18300

0

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000

10000

0

Net profit 79000 83000

Working Notes:

Fixed production overhead absorption rate 99000/11000 9

Full production cost for one unit to be used in stock valuation

is: 29

Variable cost 25

Fixed production overhead 4

Calculation of over/ under absorption of fixed production overheads

Production

Overhead

absorbed

per unit

Total

overhead

absorbed

Overhead

incurred

Over (Under)

absorption

Units Amount Amount Amount Amount

Novemb

er 12000 9 108000 99000 9000

Decemb

er 10000 9 90000 99000 -9000

Conclusion: From the above content, it has been concluded that both the costing methods

results in different net profits due to variation in opening and closing stock. For the selected

company, absorption costing is more recommended as it can help in bifurcating different costs.

M2 Applying range of management accounting techniques

Management accounting techniques are the methods which help in calculating the costs

and profits by developing financial reporting documents. These documents are developed above

by using two costing techniques which are marginal and absorption. These techniques are

8

absorption of overheads 9000 9000

169000

18300

0

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000

10000

0

Net profit 79000 83000

Working Notes:

Fixed production overhead absorption rate 99000/11000 9

Full production cost for one unit to be used in stock valuation

is: 29

Variable cost 25

Fixed production overhead 4

Calculation of over/ under absorption of fixed production overheads

Production

Overhead

absorbed

per unit

Total

overhead

absorbed

Overhead

incurred

Over (Under)

absorption

Units Amount Amount Amount Amount

Novemb

er 12000 9 108000 99000 9000

Decemb

er 10000 9 90000 99000 -9000

Conclusion: From the above content, it has been concluded that both the costing methods

results in different net profits due to variation in opening and closing stock. For the selected

company, absorption costing is more recommended as it can help in bifurcating different costs.

M2 Applying range of management accounting techniques

Management accounting techniques are the methods which help in calculating the costs

and profits by developing financial reporting documents. These documents are developed above

by using two costing techniques which are marginal and absorption. These techniques are

8

applied in order to determine profitability of a business organisation (Qian,Burritt and Chen,

2015).

D2 Interpretation of above data

By developing income statements, it has been interpreted that profits for the month of

November and December using marginal costing method is 61000 and 101000. Whereas, profits

using absorption costing is 79000 and 83000 for the month of November and December.

Profitability in December is more as sales revenue in this month is higher. The difference in the

profits in both the method is due to consideration of cost in different manner. Such as in the

absorption costing, fixed and variable costs are taken as unit cost. While in the marginal costing ,

fixed cost is taken as period cost and variable cost as unit cost. It is recommended to Oshodi that

they should adopt absorption costing over marginal as it includes proper allocation of all direct

and indirect costs.

TASK 3

P4 Advantages of different planning tools used for budgetary control

Introduction: Budget and budgetary control are the tools by which an organisation can

forecast their future expenses and revenues in order to grow sustainably. In below tasks, various

planning tools are analysed along with their merits and demerits.

Budget and Budgetary control: Budget is the tool which is developed an organisation in

order to predict future costs from past experiences. This technique helps in ascertaining future

circumstances and makes appropriate strategies (Schuster, 2015).

Budgetary control is a technique which ensures that the budget must be prepared in a way

that most accurate budgets can be prepared. It is a technique by which budgets are compared

with actual performances in order to find variations.

Various planning tools used for budgetary control:

1. PRODUCTION BUDGET: A production budget introduces as an effective financial plan that

includes lists of units to be manufactured during a time period. It is important budget which will

help an organisation by providing accurate data about the raw material. Such as in the above

Oshodi plc they use this budget for management of materials in an effective manner.

Advantages Disadvantages

9

2015).

D2 Interpretation of above data

By developing income statements, it has been interpreted that profits for the month of

November and December using marginal costing method is 61000 and 101000. Whereas, profits

using absorption costing is 79000 and 83000 for the month of November and December.

Profitability in December is more as sales revenue in this month is higher. The difference in the

profits in both the method is due to consideration of cost in different manner. Such as in the

absorption costing, fixed and variable costs are taken as unit cost. While in the marginal costing ,

fixed cost is taken as period cost and variable cost as unit cost. It is recommended to Oshodi that

they should adopt absorption costing over marginal as it includes proper allocation of all direct

and indirect costs.

TASK 3

P4 Advantages of different planning tools used for budgetary control

Introduction: Budget and budgetary control are the tools by which an organisation can

forecast their future expenses and revenues in order to grow sustainably. In below tasks, various

planning tools are analysed along with their merits and demerits.

Budget and Budgetary control: Budget is the tool which is developed an organisation in

order to predict future costs from past experiences. This technique helps in ascertaining future

circumstances and makes appropriate strategies (Schuster, 2015).

Budgetary control is a technique which ensures that the budget must be prepared in a way

that most accurate budgets can be prepared. It is a technique by which budgets are compared

with actual performances in order to find variations.

Various planning tools used for budgetary control:

1. PRODUCTION BUDGET: A production budget introduces as an effective financial plan that

includes lists of units to be manufactured during a time period. It is important budget which will

help an organisation by providing accurate data about the raw material. Such as in the above

Oshodi plc they use this budget for management of materials in an effective manner.

Advantages Disadvantages

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.