ACC320 Contemporary Issues in Accounting Research Proposal

VerifiedAdded on 2022/12/30

|17

|3230

|58

Report

AI Summary

This report, prepared by a student for the ACC320 course, examines contemporary issues in accounting with a specific focus on corporate governance. The introduction defines the issue, highlighting its importance and theoretical basis. The practical motivation section emphasizes the significance of corporate governance in accounting practices, particularly in relation to regulatory compliance. The theoretical motivation section discusses the application of agency theory and king theory in understanding corporate governance. The literature review synthesizes ideas from various authors, emphasizing the role of corporate governance in ensuring the suitability of accounting systems and compliance with regulations. The research explores the negative impact of disregarding corporate governance on a company's financial condition and proposes that corporate governance is essential for mitigating risks faced by shareholders and improving financial outcomes. The research methodology involves collecting data from primary and secondary sources, including interviews and published materials. The report aims to provide insights into the critical contemporary issues within the accounting field.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s note

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

Contemporary issues in accounting can arise due to contemporary accounting practices which

relates the different forms of accounting activities with the economic environment. One of

these activities could be reporting of financial statements such as balance sheet and cash flow

statement. One of the issues that is prominent in recent days is being unethical in following of

the rules and regulations laid down by the regulatory authorities regarding accounting system.

In this context, corporate governance can be brought into light which provides the regulations

to be followed by the organisations regarding accounting practices. The paper structures in a

way that starts with the introduction of the issue and its importance. It further moves over to

the theoretical and practical motivation of the concept that briefs about its application in

theories as well in practical phenomena. The literature review provides ideas and concepts of

different authors in relation to corporate governance. The last section states a hypothetical

statement about the research and further the methodology of the research is described in

short.

Abstract

Contemporary issues in accounting can arise due to contemporary accounting practices which

relates the different forms of accounting activities with the economic environment. One of

these activities could be reporting of financial statements such as balance sheet and cash flow

statement. One of the issues that is prominent in recent days is being unethical in following of

the rules and regulations laid down by the regulatory authorities regarding accounting system.

In this context, corporate governance can be brought into light which provides the regulations

to be followed by the organisations regarding accounting practices. The paper structures in a

way that starts with the introduction of the issue and its importance. It further moves over to

the theoretical and practical motivation of the concept that briefs about its application in

theories as well in practical phenomena. The literature review provides ideas and concepts of

different authors in relation to corporate governance. The last section states a hypothetical

statement about the research and further the methodology of the research is described in

short.

2CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................3

Literature Review.......................................................................................................................3

Hypothesis..................................................................................................................................6

Research Method........................................................................................................................7

References..................................................................................................................................8

Appendix..................................................................................................................................10

Table – Annotated Bibliography for Selected Articles............................................................10

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................3

Literature Review.......................................................................................................................3

Hypothesis..................................................................................................................................6

Research Method........................................................................................................................7

References..................................................................................................................................8

Appendix..................................................................................................................................10

Table – Annotated Bibliography for Selected Articles............................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Contemporary accounting practices are related to the understanding of accounting

activities that are required enormously for the development of a business in today’s complex

environment. In the contemporary accounting model, theories are analysed for linking

accounting with the economic environment. In this context, it becomes very important to

outline the issues that arise due to contemporary accounting. The types of issues that occur in

presence of contemporary accounting could be many. The research would be conducted

keeping in focus one of the major contemporary issues, that is corporate governance.

Corporate governance ensures the suitability and applicability of the accounting system in

relation to regulations set by the regulatory authorities. Issues come up for not abiding by the

rules of accounting. Therefore, this topic becomes a very significant topic of research.

Practical Motivation

Corporate governance plays a vital role in the formulation of accounting practices of

an organisation (Tricker and Tricker 2015). Due to failure in corporate governance there is a

disruption in the functioning of accounts and the figures highlighted in the annual report

might show discrepancies. It has been realised by the different accountants that corporate

governance is required for providing a direction to the companies on the basis of accounting

activities rather than controlling them. Importance of corporate governance was completely

made clear when the issues arose due to implementation of a weak corporate governance

(Krechovská and Procházková 2014). There was a series of meltdowns along with fraudulent

activities and other catastrophes which have led to the destruction of the wealth of the

shareholders, loss of jobs of different employees, criminal investigation of executives as well

as a lot of bankruptcy filings (Rahim and Alam 2014). All these problems pave way for the

improvement and reformation of corporate governance at different structural levels such as

business, national as well as international levels.

Introduction

Contemporary accounting practices are related to the understanding of accounting

activities that are required enormously for the development of a business in today’s complex

environment. In the contemporary accounting model, theories are analysed for linking

accounting with the economic environment. In this context, it becomes very important to

outline the issues that arise due to contemporary accounting. The types of issues that occur in

presence of contemporary accounting could be many. The research would be conducted

keeping in focus one of the major contemporary issues, that is corporate governance.

Corporate governance ensures the suitability and applicability of the accounting system in

relation to regulations set by the regulatory authorities. Issues come up for not abiding by the

rules of accounting. Therefore, this topic becomes a very significant topic of research.

Practical Motivation

Corporate governance plays a vital role in the formulation of accounting practices of

an organisation (Tricker and Tricker 2015). Due to failure in corporate governance there is a

disruption in the functioning of accounts and the figures highlighted in the annual report

might show discrepancies. It has been realised by the different accountants that corporate

governance is required for providing a direction to the companies on the basis of accounting

activities rather than controlling them. Importance of corporate governance was completely

made clear when the issues arose due to implementation of a weak corporate governance

(Krechovská and Procházková 2014). There was a series of meltdowns along with fraudulent

activities and other catastrophes which have led to the destruction of the wealth of the

shareholders, loss of jobs of different employees, criminal investigation of executives as well

as a lot of bankruptcy filings (Rahim and Alam 2014). All these problems pave way for the

improvement and reformation of corporate governance at different structural levels such as

business, national as well as international levels.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

Theoretical Motivation

The research would be based on different theoretical frameworks of corporate

governance such as agency theory and king theory (Pande and Ansari 2014). Agency theory

relates to the difference in opinion between the agents and the shareholders of the

organisation. This agency theory proposes to mitigate the problems that occur due to conflict

of interest between the managers and the shareholders (Shi, Connelly and Hoskisson 2017).

The managers are regarded as the agents while the shareholders are regarded as the principal

of the organisation. Another problem occurs due to the risk sharing appetite of the managers

and the shareholders. Another theory that best explains corporate governance is the king

theory (McDonnell, King, and Soule 2015). This theory has a broad area of interest and

explains various parts of corporate governance such as risk management, compliance of the

accounting practices with the laws, regulations, rules as well as standards and managing

relationship with the stakeholders (Brown, Preiato and Tarca 2014).

Literature Review

The first paper chosen for this research unveils corporate governance as a solution to

the major issues in recent business environment. According to the authors, there should be

proper structure for establishing in the business that would ensure efficient operation of the

accounting system. The structure should be able to guide the accounting system for properly

abiding by the regulations (Alsharari, Dixon and Youssef 2015). It should be one of the

important functions of the organisations to operate in accordance with the surrounding

environment in order to maintain a high quality of accounting functions.

It has been analysed by the authorities and different accountants that an independent

structure of corporate governance can facilitate a healthy organisational environment. This

would also enhance the quality of accounting system and quality of reporting of financial

reports. Other factors that influence the accounting conservatism and quality of reporting

Theoretical Motivation

The research would be based on different theoretical frameworks of corporate

governance such as agency theory and king theory (Pande and Ansari 2014). Agency theory

relates to the difference in opinion between the agents and the shareholders of the

organisation. This agency theory proposes to mitigate the problems that occur due to conflict

of interest between the managers and the shareholders (Shi, Connelly and Hoskisson 2017).

The managers are regarded as the agents while the shareholders are regarded as the principal

of the organisation. Another problem occurs due to the risk sharing appetite of the managers

and the shareholders. Another theory that best explains corporate governance is the king

theory (McDonnell, King, and Soule 2015). This theory has a broad area of interest and

explains various parts of corporate governance such as risk management, compliance of the

accounting practices with the laws, regulations, rules as well as standards and managing

relationship with the stakeholders (Brown, Preiato and Tarca 2014).

Literature Review

The first paper chosen for this research unveils corporate governance as a solution to

the major issues in recent business environment. According to the authors, there should be

proper structure for establishing in the business that would ensure efficient operation of the

accounting system. The structure should be able to guide the accounting system for properly

abiding by the regulations (Alsharari, Dixon and Youssef 2015). It should be one of the

important functions of the organisations to operate in accordance with the surrounding

environment in order to maintain a high quality of accounting functions.

It has been analysed by the authorities and different accountants that an independent

structure of corporate governance can facilitate a healthy organisational environment. This

would also enhance the quality of accounting system and quality of reporting of financial

reports. Other factors that influence the accounting conservatism and quality of reporting

5CONTEMPORARY ISSUES IN ACCOUNTING

could be public ownership, institutional ownership, and sometimes managerial ownership

(Alsharari, Dixon and Youssef 2015). Healthy internal business environment would help in

carrying out smooth internal controls, transparency among the corporate and effective

allocation of resources. One of the examples of corporate governance is incentive

compensation in management. Studies have shown that organisations not adopting this

concept has brought about accounting irregularities and ineffectiveness of the internal

control. Another example can be function of the audit committee which is required for the

proper presentation of the annual reports without numerical discrepancies.

Another paper thoroughly talks about the practical implication of corporate

governance which is presented in the form of a case study of a developing country (Al-

Malkawi, Pillai and Bhatti 2014). According to the different authors, the definition of

corporate governance could be enhancement and fortification of the rules and principles that

are required for providing a direction to the operation of the companies. Studies and surveys

conducted in South Africa have revealed that the term corporate governance is showing its

association progressively only with the listed companies.

Another section of the paper provides a theoretical framework to corporate

governance and the importance of the auditing function. Another corporate governance

method discussed in the paper is the accountability and transparency of the financial

information. In order to provide information without discrepancies, there should be effective

communication between all the levels of the organisation (Al-Malkawi, Pillai and Bhatti

2014). There should be a section provided for disclosure which would consist of different

forms of information in the financial statements like cash flow statement, balance sheet and

others. There should be a system of internal control which would require identification of

objectives and risks along with the measurement of the performance of staff, systems and

processes. Another system would monitor the effectiveness of the identified risk.

could be public ownership, institutional ownership, and sometimes managerial ownership

(Alsharari, Dixon and Youssef 2015). Healthy internal business environment would help in

carrying out smooth internal controls, transparency among the corporate and effective

allocation of resources. One of the examples of corporate governance is incentive

compensation in management. Studies have shown that organisations not adopting this

concept has brought about accounting irregularities and ineffectiveness of the internal

control. Another example can be function of the audit committee which is required for the

proper presentation of the annual reports without numerical discrepancies.

Another paper thoroughly talks about the practical implication of corporate

governance which is presented in the form of a case study of a developing country (Al-

Malkawi, Pillai and Bhatti 2014). According to the different authors, the definition of

corporate governance could be enhancement and fortification of the rules and principles that

are required for providing a direction to the operation of the companies. Studies and surveys

conducted in South Africa have revealed that the term corporate governance is showing its

association progressively only with the listed companies.

Another section of the paper provides a theoretical framework to corporate

governance and the importance of the auditing function. Another corporate governance

method discussed in the paper is the accountability and transparency of the financial

information. In order to provide information without discrepancies, there should be effective

communication between all the levels of the organisation (Al-Malkawi, Pillai and Bhatti

2014). There should be a section provided for disclosure which would consist of different

forms of information in the financial statements like cash flow statement, balance sheet and

others. There should be a system of internal control which would require identification of

objectives and risks along with the measurement of the performance of staff, systems and

processes. Another system would monitor the effectiveness of the identified risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

The third paper focusses on the framework developed for the behavioural perspectives

of corporate governance. One such behavioural aspect could be creation of accountability.

The research on corporate governance has been carried on since 1990s for giving importance

to the protection of stakes of the investors (Elghuweel et al. 2017). Creation of

accountability can be defined as the bridging of the gap between the expected performance of

the board and the actual task performance that is observed. The applicability of corporate

governance can be attributed to the external perspectives of accountability (Elghuweel et al.

2017). One such theory is the agency theory that explains the circumvent behaviour of the

corporate managers to the interests of the shareholders. As a result of incompetent behaviour,

there has been cases of hostile takeovers by other companies existing in the market.

A different section of the theoretical framework describes an alternative trend of

corporate governance where the stakeholders have been given importance greater than that of

managers. This situation is related to the different crises that have occurred such as the Enron

case. The crises exemplified the global consequences of the investors which were negative

(Elghuweel et al. 2017). After such dramatic cases, corporate governance has been

reintroduced in the corporations and the internal people have been made aware of their

corporate and social responsibilities.

Different other studies of paper revealed the relation of accountability and the

mechanisms of accountability with the corporate governance. A general review of the

traditional corporate governance and the research of the accountability would be useful for

acquiring potential opportunities in the business environment. Some studies provide an

analytical framework to this concept. Different research works have overestimated the value

of corporate profitability and shareholders in financial environment and these elements have

been considered superior to corporate governance (Grossi, Papenfuß and Tremblay 2015).

However, a thorough research conducted on the importance of corporate governance has

The third paper focusses on the framework developed for the behavioural perspectives

of corporate governance. One such behavioural aspect could be creation of accountability.

The research on corporate governance has been carried on since 1990s for giving importance

to the protection of stakes of the investors (Elghuweel et al. 2017). Creation of

accountability can be defined as the bridging of the gap between the expected performance of

the board and the actual task performance that is observed. The applicability of corporate

governance can be attributed to the external perspectives of accountability (Elghuweel et al.

2017). One such theory is the agency theory that explains the circumvent behaviour of the

corporate managers to the interests of the shareholders. As a result of incompetent behaviour,

there has been cases of hostile takeovers by other companies existing in the market.

A different section of the theoretical framework describes an alternative trend of

corporate governance where the stakeholders have been given importance greater than that of

managers. This situation is related to the different crises that have occurred such as the Enron

case. The crises exemplified the global consequences of the investors which were negative

(Elghuweel et al. 2017). After such dramatic cases, corporate governance has been

reintroduced in the corporations and the internal people have been made aware of their

corporate and social responsibilities.

Different other studies of paper revealed the relation of accountability and the

mechanisms of accountability with the corporate governance. A general review of the

traditional corporate governance and the research of the accountability would be useful for

acquiring potential opportunities in the business environment. Some studies provide an

analytical framework to this concept. Different research works have overestimated the value

of corporate profitability and shareholders in financial environment and these elements have

been considered superior to corporate governance (Grossi, Papenfuß and Tremblay 2015).

However, a thorough research conducted on the importance of corporate governance has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

revealed that the different takeover activities of the firms wuch as mergers and acquisitions,

all come under the purview of agency theory related to corporate governance (Gajevszky

2014). Improvement of the role of corporate governance can be carried out through the

performance of institutional investors. These investors can be regarded as the sole element of

corporate management and henceforth, can prove to be worthy of bringing corporate

governance improvement within the organisation.

All the above papers describe the role of corporate governance in one form or the

other. It is evident that the usage of corporate governance is necessary for minimising

problems that are related to the non-compliance of the accounting system with the regulations

set up by the regulatory authorities. Therefore, corporate governance is necessary for

overcoming the critical issues of corporate accounting.

Hypothesis

Null Hypothesis: One of the critical issues of contemporary accounting is

disregarding of corporate governance that has a direct negative impact on the financial

condition of the company. There could be fraudulent cases which would be filed for

disrespecting the corporate governance. Corporate governance should be implemented in

order to cope up with the risks faced by the shareholders and also for the financial betterment

of the company.

Research Method

The research method that would be followed in the process of research would be

collection of data from both the primary as well as secondary sources. The primary sources

could be direct interview or conversation with the employees of the organisation and finding

relevant data related to the implementation of corporate governance. The secondary research

would be done through the secondary data collected from different kinds of articles,

revealed that the different takeover activities of the firms wuch as mergers and acquisitions,

all come under the purview of agency theory related to corporate governance (Gajevszky

2014). Improvement of the role of corporate governance can be carried out through the

performance of institutional investors. These investors can be regarded as the sole element of

corporate management and henceforth, can prove to be worthy of bringing corporate

governance improvement within the organisation.

All the above papers describe the role of corporate governance in one form or the

other. It is evident that the usage of corporate governance is necessary for minimising

problems that are related to the non-compliance of the accounting system with the regulations

set up by the regulatory authorities. Therefore, corporate governance is necessary for

overcoming the critical issues of corporate accounting.

Hypothesis

Null Hypothesis: One of the critical issues of contemporary accounting is

disregarding of corporate governance that has a direct negative impact on the financial

condition of the company. There could be fraudulent cases which would be filed for

disrespecting the corporate governance. Corporate governance should be implemented in

order to cope up with the risks faced by the shareholders and also for the financial betterment

of the company.

Research Method

The research method that would be followed in the process of research would be

collection of data from both the primary as well as secondary sources. The primary sources

could be direct interview or conversation with the employees of the organisation and finding

relevant data related to the implementation of corporate governance. The secondary research

would be done through the secondary data collected from different kinds of articles,

8CONTEMPORARY ISSUES IN ACCOUNTING

newsletters, official websites or any other source of information published by the

organisation in relation to corporate government.

newsletters, official websites or any other source of information published by the

organisation in relation to corporate government.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

References

Al-Malkawi, H.A.N., Pillai, R. and Bhatti, M.I., 2014. Corporate governance practices in

emerging markets: The case of GCC countries. Economic Modelling, 38, pp.133-141.

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting change:

critical review and a new contextual framework. Journal of Accounting & Organizational

Change, 11(4), pp.476-502.

Brown, P., Preiato, J. and Tarca, A., 2014. Measuring country differences in enforcement of

accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), pp.1-52.

Elghuweel, M.I., Ntim, C.G., Opong, K.K. and Avison, L., 2017. Corporate governance,

Islamic governance and earnings management in Oman: A new empirical insights from a

behavioural theoretical framework. Journal of Accounting in Emerging Economies, 7(2),

pp.190-224.

Gajevszky, A., 2014. Audit quality and corporate governance: evidence from the bucharest

stock exchange. Journal of economic and social developmen, 1(2), pp.0-0.

Grossi, G., Papenfuß, U. and Tremblay, M.S., 2015. Corporate governance and accountability

of state-owned enterprises: relevance for science and society and interdisciplinary research

perspectives. International Journal of Public Sector Management, 28(4/5), pp.274-285.

Krechovská, M. and Procházková, P.T., 2014. Sustainability and its integration into corporate

governance focusing on corporate performance management and reporting. Procedia

Engineering, 69, pp.1144-1151.

References

Al-Malkawi, H.A.N., Pillai, R. and Bhatti, M.I., 2014. Corporate governance practices in

emerging markets: The case of GCC countries. Economic Modelling, 38, pp.133-141.

Alsharari, N.M., Dixon, R. and Youssef, M.A.E.A., 2015. Management accounting change:

critical review and a new contextual framework. Journal of Accounting & Organizational

Change, 11(4), pp.476-502.

Brown, P., Preiato, J. and Tarca, A., 2014. Measuring country differences in enforcement of

accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), pp.1-52.

Elghuweel, M.I., Ntim, C.G., Opong, K.K. and Avison, L., 2017. Corporate governance,

Islamic governance and earnings management in Oman: A new empirical insights from a

behavioural theoretical framework. Journal of Accounting in Emerging Economies, 7(2),

pp.190-224.

Gajevszky, A., 2014. Audit quality and corporate governance: evidence from the bucharest

stock exchange. Journal of economic and social developmen, 1(2), pp.0-0.

Grossi, G., Papenfuß, U. and Tremblay, M.S., 2015. Corporate governance and accountability

of state-owned enterprises: relevance for science and society and interdisciplinary research

perspectives. International Journal of Public Sector Management, 28(4/5), pp.274-285.

Krechovská, M. and Procházková, P.T., 2014. Sustainability and its integration into corporate

governance focusing on corporate performance management and reporting. Procedia

Engineering, 69, pp.1144-1151.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

McDonnell, M.H., King, B.G. and Soule, S.A., 2015. A dynamic process model of private

politics: Activist targeting and corporate receptivity to social challenges. American

Sociological Review, 80(3), pp.654-678.

Pande, S. and Ansari, V.A., 2014. A theoretical framework for corporate governance. Indian

Journal of Corporate Governance, 7(1), pp.56-72.

Rahim, M.M. and Alam, S., 2014. Convergence of corporate social responsibility and

corporate governance in weak economies: The case of Bangladesh. Journal of Business

Ethics, 121(4), pp.607-620.

Shi, W., Connelly, B.L. and Hoskisson, R.E., 2017. External corporate governance and

financial fraud: Cognitive evaluation theory insights on agency theory

prescriptions. Strategic Management Journal, 38(6), pp.1268-1286.

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press, USA.

McDonnell, M.H., King, B.G. and Soule, S.A., 2015. A dynamic process model of private

politics: Activist targeting and corporate receptivity to social challenges. American

Sociological Review, 80(3), pp.654-678.

Pande, S. and Ansari, V.A., 2014. A theoretical framework for corporate governance. Indian

Journal of Corporate Governance, 7(1), pp.56-72.

Rahim, M.M. and Alam, S., 2014. Convergence of corporate social responsibility and

corporate governance in weak economies: The case of Bangladesh. Journal of Business

Ethics, 121(4), pp.607-620.

Shi, W., Connelly, B.L. and Hoskisson, R.E., 2017. External corporate governance and

financial fraud: Cognitive evaluation theory insights on agency theory

prescriptions. Strategic Management Journal, 38(6), pp.1268-1286.

Tricker, R.B. and Tricker, R.I., 2015. Corporate governance: Principles, policies, and

practices. Oxford University Press, USA.

11CONTEMPORARY ISSUES IN ACCOUNTING

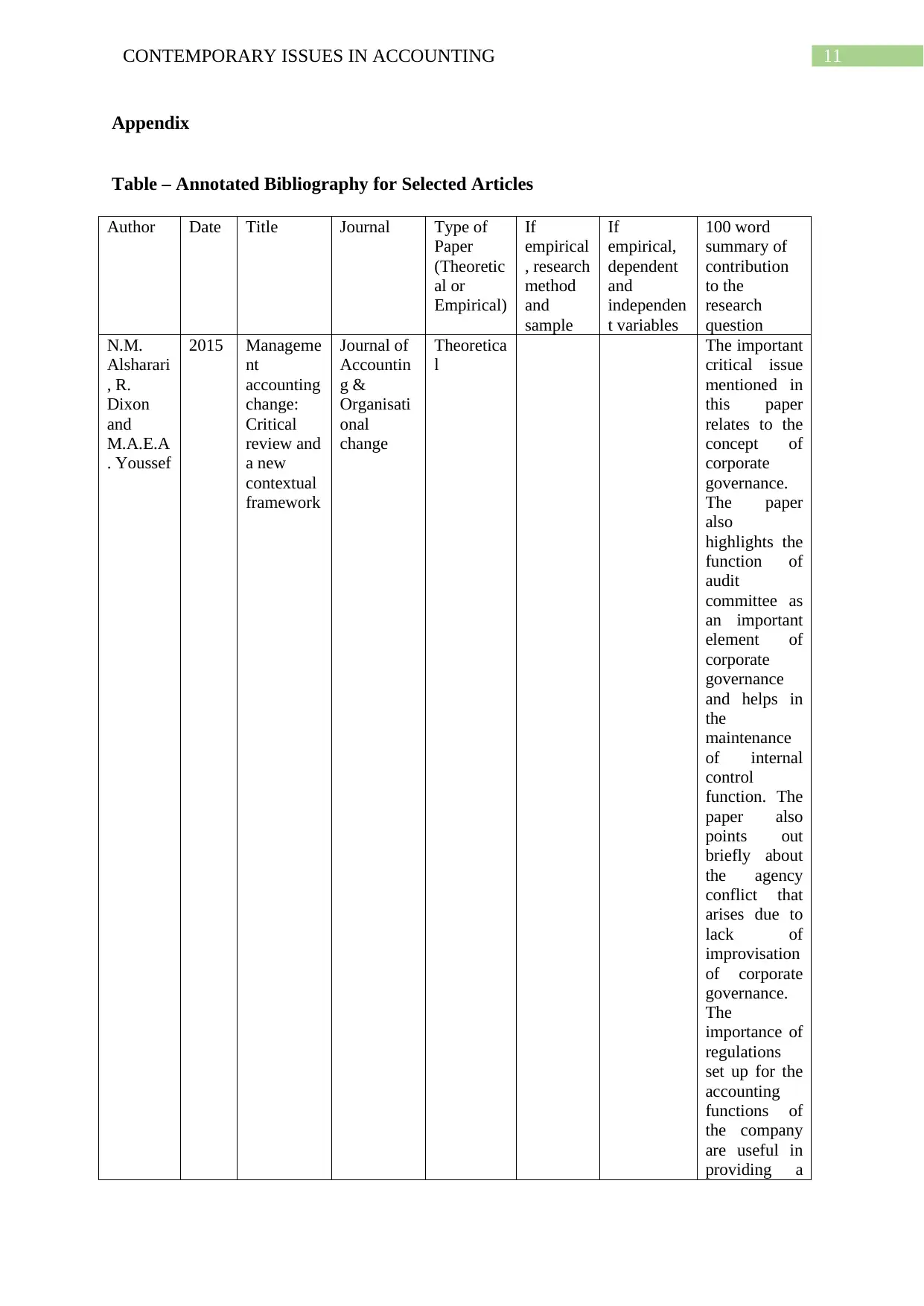

Appendix

Table – Annotated Bibliography for Selected Articles

Author Date Title Journal Type of

Paper

(Theoretic

al or

Empirical)

If

empirical

, research

method

and

sample

If

empirical,

dependent

and

independen

t variables

100 word

summary of

contribution

to the

research

question

N.M.

Alsharari

, R.

Dixon

and

M.A.E.A

. Youssef

2015 Manageme

nt

accounting

change:

Critical

review and

a new

contextual

framework

Journal of

Accountin

g &

Organisati

onal

change

Theoretica

l

The important

critical issue

mentioned in

this paper

relates to the

concept of

corporate

governance.

The paper

also

highlights the

function of

audit

committee as

an important

element of

corporate

governance

and helps in

the

maintenance

of internal

control

function. The

paper also

points out

briefly about

the agency

conflict that

arises due to

lack of

improvisation

of corporate

governance.

The

importance of

regulations

set up for the

accounting

functions of

the company

are useful in

providing a

Appendix

Table – Annotated Bibliography for Selected Articles

Author Date Title Journal Type of

Paper

(Theoretic

al or

Empirical)

If

empirical

, research

method

and

sample

If

empirical,

dependent

and

independen

t variables

100 word

summary of

contribution

to the

research

question

N.M.

Alsharari

, R.

Dixon

and

M.A.E.A

. Youssef

2015 Manageme

nt

accounting

change:

Critical

review and

a new

contextual

framework

Journal of

Accountin

g &

Organisati

onal

change

Theoretica

l

The important

critical issue

mentioned in

this paper

relates to the

concept of

corporate

governance.

The paper

also

highlights the

function of

audit

committee as

an important

element of

corporate

governance

and helps in

the

maintenance

of internal

control

function. The

paper also

points out

briefly about

the agency

conflict that

arises due to

lack of

improvisation

of corporate

governance.

The

importance of

regulations

set up for the

accounting

functions of

the company

are useful in

providing a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.