University of Derby: Financial Strategy WACC Analysis of Harvey Norman

VerifiedAdded on 2023/04/07

|19

|3533

|484

Report

AI Summary

This report presents a comprehensive analysis of the Weighted Average Cost of Capital (WACC) for Harvey Norman, a representative company chosen to assess the cost of capital for Hubbard Computer Limited. The analysis includes the calculation of the cost of equity using the Capital Asset Pricing Model (CAPM) and the dividend discount model, along with an examination of the cost of long-term debt. The report delves into the latest book value of equity and debt, market capitalization, outstanding shares, and recent beta of Harvey Norman. It also addresses the different types of business loan rates and their implications. The report calculates the cost of equity and the weighted average cost of capital using both book value and market value weights, providing a detailed understanding of the financial structure and cost of capital for the company, as well as potential issues in the chosen approach. This report is a valuable resource for students studying financial strategy, providing practical application of financial concepts and models.

Weighted average cost of capital

Weighted Average Cost of Capital of Company

0

Weighted Average Cost of Capital of Company

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Weighted average cost of capital

Table of contents

Answers 2

Question 1 2

Question no.2 6

Question 3 10

4. Weighted average cost of capital using book value as weights and market value as weights.

13

5. Potential problems 15

1

Table of contents

Answers 2

Question 1 2

Question no.2 6

Question 3 10

4. Weighted average cost of capital using book value as weights and market value as weights.

13

5. Potential problems 15

1

Weighted average cost of capital

Part 2

Introduction

In this part the cost of capital of Hubbard computer limited will be calculated by the

representative company, Harvey Norman. The latest stock price, shares outstanding, latest annual

dividend of Harvey Norman has been analyzed in details. The cost of equity by applying capital

assets pricing have also been determined and analyzed. The weighted average cost of capital of

the representative company has been calculated. The issues has been discussed which can arise

with the approach of choosing pure play company.

Answers

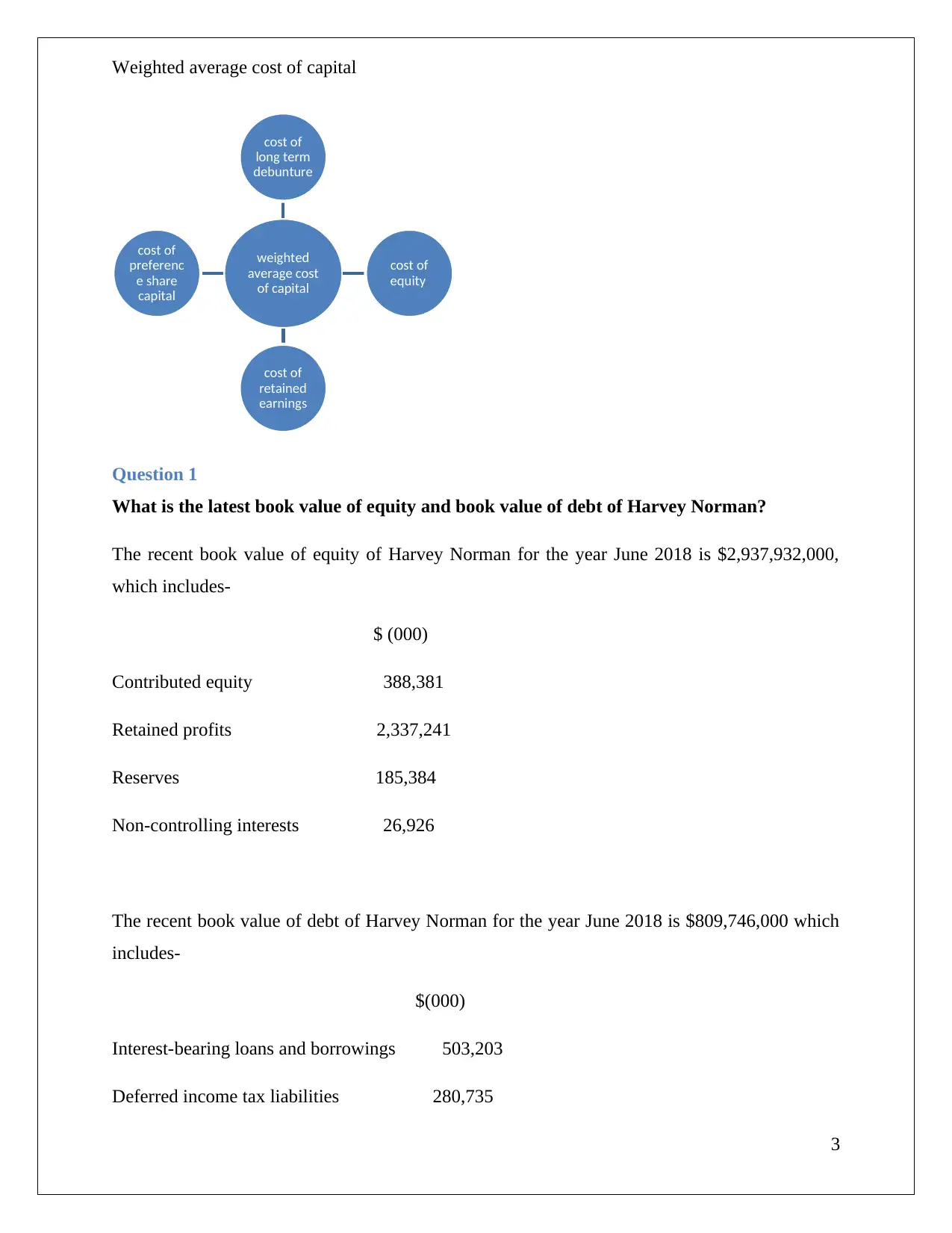

1. Weighted average cost of capital

Whenever a company needs fund to run their businesses efficiently and smoothly, they borrow

funds from the market. According to Baker and Wurgler (2015, p-320), the cost of capital is an

essential tool which is used to measure the expected return of the debenture holders or investors

or shareholders of the company. Financial analysts prefer weighted average cost of capital to

assess the minimum return which they expect from the company. Company raised funds through

different sources. To arrange sources of finance companies issues equity shares or preference

shares or long term debenture or bonds to run their businesses efficiently and effectively. To

arrange the funds from different sources, company has to incur some cost, which is known as

cost of capital. As it can be analyzed that Hubbard Computer limited is a privately owned

company and Bob Hubbard who is the founder of the company wants to measure the cost of

capital of company. So, the founder of Hubbard Computer limited has chosen Harvey Norman as

a pure play company or representative company to assists HCL to analyze the cost of capital. To

assess the weighted average cost of capital of HCL, it is necessary to calculate the cost of

different sources of the company such as:

2

Part 2

Introduction

In this part the cost of capital of Hubbard computer limited will be calculated by the

representative company, Harvey Norman. The latest stock price, shares outstanding, latest annual

dividend of Harvey Norman has been analyzed in details. The cost of equity by applying capital

assets pricing have also been determined and analyzed. The weighted average cost of capital of

the representative company has been calculated. The issues has been discussed which can arise

with the approach of choosing pure play company.

Answers

1. Weighted average cost of capital

Whenever a company needs fund to run their businesses efficiently and smoothly, they borrow

funds from the market. According to Baker and Wurgler (2015, p-320), the cost of capital is an

essential tool which is used to measure the expected return of the debenture holders or investors

or shareholders of the company. Financial analysts prefer weighted average cost of capital to

assess the minimum return which they expect from the company. Company raised funds through

different sources. To arrange sources of finance companies issues equity shares or preference

shares or long term debenture or bonds to run their businesses efficiently and effectively. To

arrange the funds from different sources, company has to incur some cost, which is known as

cost of capital. As it can be analyzed that Hubbard Computer limited is a privately owned

company and Bob Hubbard who is the founder of the company wants to measure the cost of

capital of company. So, the founder of Hubbard Computer limited has chosen Harvey Norman as

a pure play company or representative company to assists HCL to analyze the cost of capital. To

assess the weighted average cost of capital of HCL, it is necessary to calculate the cost of

different sources of the company such as:

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Weighted average cost of capital

Question 1

What is the latest book value of equity and book value of debt of Harvey Norman?

The recent book value of equity of Harvey Norman for the year June 2018 is $2,937,932,000,

which includes-

$ (000)

Contributed equity 388,381

Retained profits 2,337,241

Reserves 185,384

Non-controlling interests 26,926

The recent book value of debt of Harvey Norman for the year June 2018 is $809,746,000 which

includes-

$(000)

Interest-bearing loans and borrowings 503,203

Deferred income tax liabilities 280,735

3

weighted

average cost

of capital

cost of

long term

debunture

cost of

equity

cost of

retained

earnings

cost of

preferenc

e share

capital

Question 1

What is the latest book value of equity and book value of debt of Harvey Norman?

The recent book value of equity of Harvey Norman for the year June 2018 is $2,937,932,000,

which includes-

$ (000)

Contributed equity 388,381

Retained profits 2,337,241

Reserves 185,384

Non-controlling interests 26,926

The recent book value of debt of Harvey Norman for the year June 2018 is $809,746,000 which

includes-

$(000)

Interest-bearing loans and borrowings 503,203

Deferred income tax liabilities 280,735

3

weighted

average cost

of capital

cost of

long term

debunture

cost of

equity

cost of

retained

earnings

cost of

preferenc

e share

capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Weighted average cost of capital

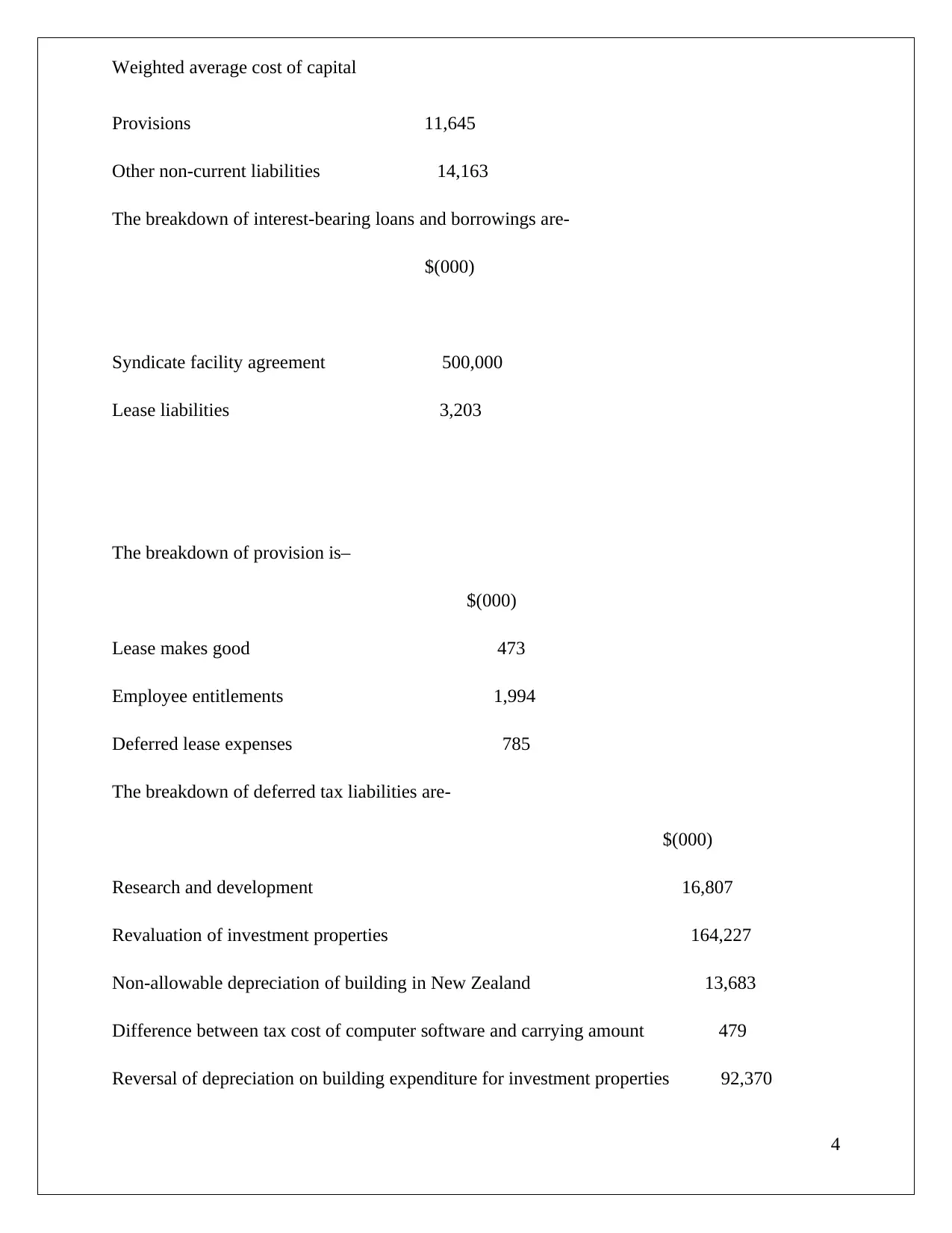

Provisions 11,645

Other non-current liabilities 14,163

The breakdown of interest-bearing loans and borrowings are-

$(000)

Syndicate facility agreement 500,000

Lease liabilities 3,203

The breakdown of provision is–

$(000)

Lease makes good 473

Employee entitlements 1,994

Deferred lease expenses 785

The breakdown of deferred tax liabilities are-

$(000)

Research and development 16,807

Revaluation of investment properties 164,227

Non-allowable depreciation of building in New Zealand 13,683

Difference between tax cost of computer software and carrying amount 479

Reversal of depreciation on building expenditure for investment properties 92,370

4

Provisions 11,645

Other non-current liabilities 14,163

The breakdown of interest-bearing loans and borrowings are-

$(000)

Syndicate facility agreement 500,000

Lease liabilities 3,203

The breakdown of provision is–

$(000)

Lease makes good 473

Employee entitlements 1,994

Deferred lease expenses 785

The breakdown of deferred tax liabilities are-

$(000)

Research and development 16,807

Revaluation of investment properties 164,227

Non-allowable depreciation of building in New Zealand 13,683

Difference between tax cost of computer software and carrying amount 479

Reversal of depreciation on building expenditure for investment properties 92,370

4

Weighted average cost of capital

Revaluations of land and building occupied by owner at fair value 36501

Other items 5487

2. Cost of equity

It is a well-known fact that equity share capital does not attract any cost. Cost of equity is the

expected rate of return of equity shareholders from a company which they expect and also get. If

the company is unable to meet the requirements of the investors and shareholders of the

company, then the investors will think of investing in some other company. According to

Dhaliwal et al. (2016, p-48), if the risk is higher the return on equity shares is also high and also

the cost of equity share capital will be high. As opined by Berger et al. (2018, p-49), if Hubbard

Computer limited measure its cost of equity then it can assess the attractiveness of company

investments of both external opportunities and internal projects. Cost of equity capital can assists

Hubbard computer limited to equate the current value of dividends which are expected by

company with the market price of share of company. The approaches which can be used for

calculating the cost of equity share capital are:

Dividend discount model

In the given case study, dividend discount model can be applied to assess the fair price of stock

of Harvey Norman by applying formula with minimum variables which are required as input.

According to Lazzati and Menichini (2015, p-1550018), the dividend discount model considers

the following assumptions while calculating the cost of equity:

It assumed that company is an equity company

Retained earnings are the only source used to finance the investment of the company

5

Cost of equity share

capital

Earning price approach

Dividend price approach

Capital assets pricing

model

Realized yield approach

Revaluations of land and building occupied by owner at fair value 36501

Other items 5487

2. Cost of equity

It is a well-known fact that equity share capital does not attract any cost. Cost of equity is the

expected rate of return of equity shareholders from a company which they expect and also get. If

the company is unable to meet the requirements of the investors and shareholders of the

company, then the investors will think of investing in some other company. According to

Dhaliwal et al. (2016, p-48), if the risk is higher the return on equity shares is also high and also

the cost of equity share capital will be high. As opined by Berger et al. (2018, p-49), if Hubbard

Computer limited measure its cost of equity then it can assess the attractiveness of company

investments of both external opportunities and internal projects. Cost of equity capital can assists

Hubbard computer limited to equate the current value of dividends which are expected by

company with the market price of share of company. The approaches which can be used for

calculating the cost of equity share capital are:

Dividend discount model

In the given case study, dividend discount model can be applied to assess the fair price of stock

of Harvey Norman by applying formula with minimum variables which are required as input.

According to Lazzati and Menichini (2015, p-1550018), the dividend discount model considers

the following assumptions while calculating the cost of equity:

It assumed that company is an equity company

Retained earnings are the only source used to finance the investment of the company

5

Cost of equity share

capital

Earning price approach

Dividend price approach

Capital assets pricing

model

Realized yield approach

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Weighted average cost of capital

The cost of equity of company remains constant

The rate of return on company investment remains constant

It assumed that the company has a constant retention ratio

It takes on the assumption that the life of the company is infinite

It takes on the assumption that the growth rate of company remains constant

The growth rate of the company is smaller than the cost of equity

No taxes are charged

Capital asset pricing model

In words of Squartini et al. (2017, p-032315), capital assets pricing model (CAPM) expresses the

interrelationship between return and risk of securities of a company. If market decreases or

increases by say10percent and the beta of company is 2.5, it signifies that the price of particular

stock of company will also decrease or increase by 25% (2.5*10). For instance, if the beta of

stock of company is more than 1, then it is known as aggressive beta stocks or as high beta stock.

As opined by Elbannan (2015, p-228), if beta of stock of company is less than 1, then it is known

as low beta stock or defensive stock.

Question no.2

What is the ASX code for the company Harvey Norman?

HVN is the ASX code for the company Harvey Norman.

What is the share price listed for the company Harvey Norman?

The latest share price which is listed for the company Harvey Norman is 3.81 on 22nd March

2019, as of 11.21Am AEDT Market open. (Harvey Norman, 2019)

What is the market capitalization of Harvey Norman or its equity value in the market?

The share price of the company on 22nd march, 2019 is 3.81 and if we will multiply the share

price with the number of shares outstanding on that date we will get the market value of Harvey

Norman i.e. 3.81*1.17034 = 4.459 billion dollars. So, the market value of Harvey Norman is

4.459 billion dollars as on 22nd march, 2019. (Harvey Norman, 2019).

6

The cost of equity of company remains constant

The rate of return on company investment remains constant

It assumed that the company has a constant retention ratio

It takes on the assumption that the life of the company is infinite

It takes on the assumption that the growth rate of company remains constant

The growth rate of the company is smaller than the cost of equity

No taxes are charged

Capital asset pricing model

In words of Squartini et al. (2017, p-032315), capital assets pricing model (CAPM) expresses the

interrelationship between return and risk of securities of a company. If market decreases or

increases by say10percent and the beta of company is 2.5, it signifies that the price of particular

stock of company will also decrease or increase by 25% (2.5*10). For instance, if the beta of

stock of company is more than 1, then it is known as aggressive beta stocks or as high beta stock.

As opined by Elbannan (2015, p-228), if beta of stock of company is less than 1, then it is known

as low beta stock or defensive stock.

Question no.2

What is the ASX code for the company Harvey Norman?

HVN is the ASX code for the company Harvey Norman.

What is the share price listed for the company Harvey Norman?

The latest share price which is listed for the company Harvey Norman is 3.81 on 22nd March

2019, as of 11.21Am AEDT Market open. (Harvey Norman, 2019)

What is the market capitalization of Harvey Norman or its equity value in the market?

The share price of the company on 22nd march, 2019 is 3.81 and if we will multiply the share

price with the number of shares outstanding on that date we will get the market value of Harvey

Norman i.e. 3.81*1.17034 = 4.459 billion dollars. So, the market value of Harvey Norman is

4.459 billion dollars as on 22nd march, 2019. (Harvey Norman, 2019).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Weighted average cost of capital

What are the latest outstanding shares for the company Harvey Norman?

The outstanding shares of a company can be assessed by simply dividing the market

capitalization of a company with market price of company. The outstanding shares of Harvey

Norman are 1.17034 billion (4.459/3.81).

What is the latest annual dividend declared by Harvey Norman?

The latest yearly dividend for the company Harvey Norman in monetary value is Australian

dollar 0.12000000 and it is 100 percent in case of fully franked dividend.

What is the recent Beta for the company Harvey Norman?

The recent Beta for the company Harvey Norman is 0.46 (Harvey Norman, 2019).

By applying the risk premium of historical market, indicate the cost of equity for the

company Harvey Norman as per the model CAPM?

Cost of equity can be determined by using the Capital asset pricing model (CAPM).

The cost of equity of Harvey Norman is 4.89%.

Risk-free rate of return 2.13000000%

Return from market 6%

Beta 0.46

formula Ke = Rf+B (Rm-Rf)

B=0.46

where, Rf=2.13000000%

Rf=risk free rate of

return Rm=6%

B=beta of stock

7

What are the latest outstanding shares for the company Harvey Norman?

The outstanding shares of a company can be assessed by simply dividing the market

capitalization of a company with market price of company. The outstanding shares of Harvey

Norman are 1.17034 billion (4.459/3.81).

What is the latest annual dividend declared by Harvey Norman?

The latest yearly dividend for the company Harvey Norman in monetary value is Australian

dollar 0.12000000 and it is 100 percent in case of fully franked dividend.

What is the recent Beta for the company Harvey Norman?

The recent Beta for the company Harvey Norman is 0.46 (Harvey Norman, 2019).

By applying the risk premium of historical market, indicate the cost of equity for the

company Harvey Norman as per the model CAPM?

Cost of equity can be determined by using the Capital asset pricing model (CAPM).

The cost of equity of Harvey Norman is 4.89%.

Risk-free rate of return 2.13000000%

Return from market 6%

Beta 0.46

formula Ke = Rf+B (Rm-Rf)

B=0.46

where, Rf=2.13000000%

Rf=risk free rate of

return Rm=6%

B=beta of stock

7

Weighted average cost of capital

Ke=cost of equity capital Ke=2.13000000%+0.46*6%

Rm= return from market 4.89%

The latest beta of Harvey Norman which is used as a pure play company to estimate the cost of

capital of Hubbard Computers limited. The risk-free rate of return of the security of company is

2.13000000 percent. The expected return from the market which an investor or shareholders

expect is 6 percent. The cost of equity comes to 4.89 percent after applying the capital assets

pricing model. For example, if the investors who want to put their money in equity shares of a

company and are expecting a minimum return of 4 percent from the company, then he will put

his money in the equity shares of the company because the cost of equity capital of company as

calculated above is more than the investor expectations. According to Valta (2016, p-229), it

means that the shareholders or investors are getting more return then the expected return, so they

will decide to invest in the company.

3. Cost of long term debt

According to Harford et al. (2018, p-452), debts instruments or external commercial borrowing

do not provide ownership to the finance providers. As per the companies act, 2013, debenture

holders cannot vote at the meeting of the company but they have given priority for redemption

earlier to preference shareholders and equity shareholders. The debenture holders have a charge

on earnings before taxes of the company. In words of Della Seta et al. (2017, p-270), the debts

which are long term include loans from different financial institutions, capital from bonds or

issuing debenture. If the company is able to give more then what the bondholders or debenture

holders expects then the debenture holders will purchase the debentures of the company. But if

the expected interest rate of debenture holder is more than the company cost of debt, then

debenture holders would not like to purchase the debenture or bonds of company.

Question 3

What is the current business loan rates equivalent for each of Harvey Norman debt?

8

Ke=cost of equity capital Ke=2.13000000%+0.46*6%

Rm= return from market 4.89%

The latest beta of Harvey Norman which is used as a pure play company to estimate the cost of

capital of Hubbard Computers limited. The risk-free rate of return of the security of company is

2.13000000 percent. The expected return from the market which an investor or shareholders

expect is 6 percent. The cost of equity comes to 4.89 percent after applying the capital assets

pricing model. For example, if the investors who want to put their money in equity shares of a

company and are expecting a minimum return of 4 percent from the company, then he will put

his money in the equity shares of the company because the cost of equity capital of company as

calculated above is more than the investor expectations. According to Valta (2016, p-229), it

means that the shareholders or investors are getting more return then the expected return, so they

will decide to invest in the company.

3. Cost of long term debt

According to Harford et al. (2018, p-452), debts instruments or external commercial borrowing

do not provide ownership to the finance providers. As per the companies act, 2013, debenture

holders cannot vote at the meeting of the company but they have given priority for redemption

earlier to preference shareholders and equity shareholders. The debenture holders have a charge

on earnings before taxes of the company. In words of Della Seta et al. (2017, p-270), the debts

which are long term include loans from different financial institutions, capital from bonds or

issuing debenture. If the company is able to give more then what the bondholders or debenture

holders expects then the debenture holders will purchase the debentures of the company. But if

the expected interest rate of debenture holder is more than the company cost of debt, then

debenture holders would not like to purchase the debenture or bonds of company.

Question 3

What is the current business loan rates equivalent for each of Harvey Norman debt?

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Weighted average cost of capital

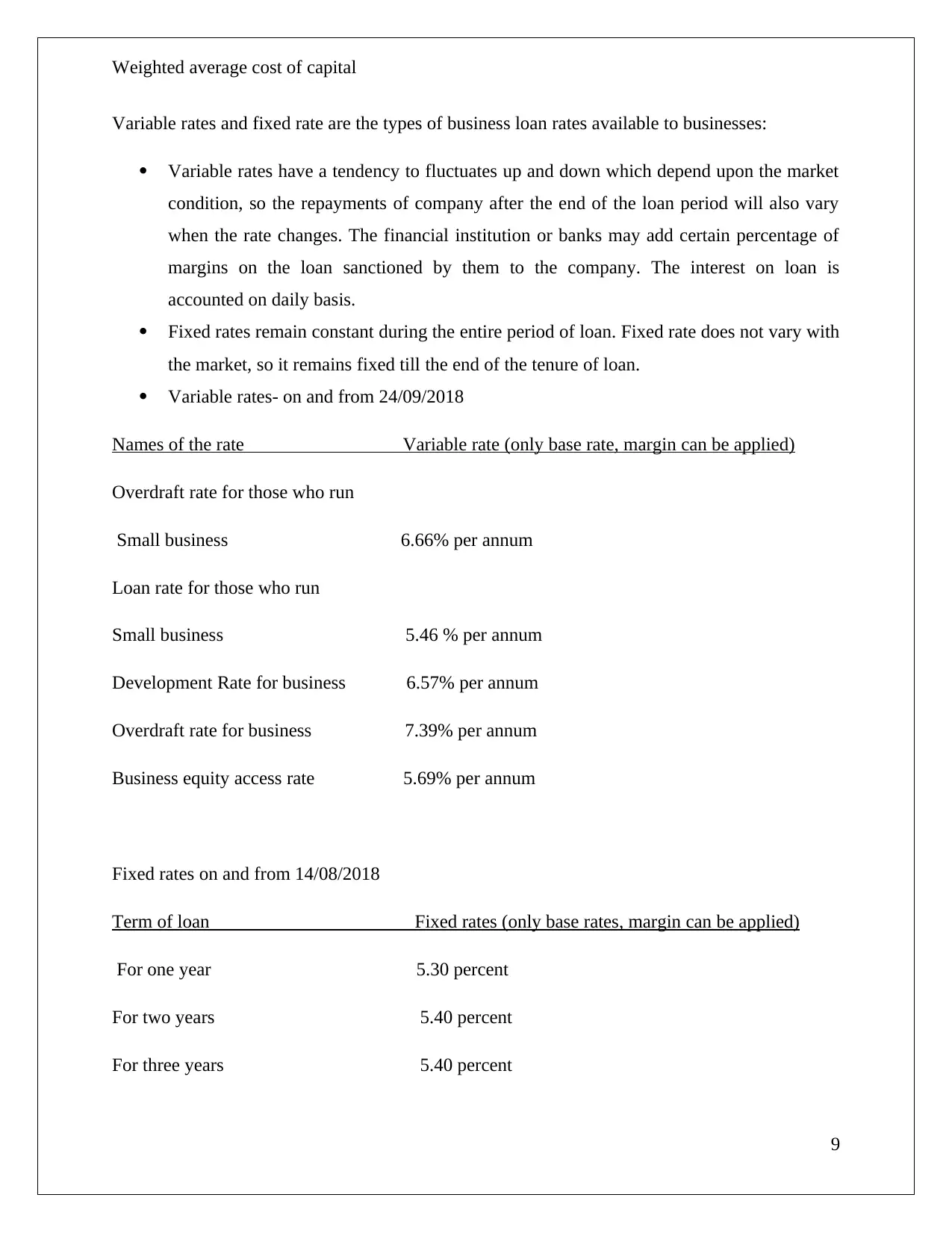

Variable rates and fixed rate are the types of business loan rates available to businesses:

Variable rates have a tendency to fluctuates up and down which depend upon the market

condition, so the repayments of company after the end of the loan period will also vary

when the rate changes. The financial institution or banks may add certain percentage of

margins on the loan sanctioned by them to the company. The interest on loan is

accounted on daily basis.

Fixed rates remain constant during the entire period of loan. Fixed rate does not vary with

the market, so it remains fixed till the end of the tenure of loan.

Variable rates- on and from 24/09/2018

Names of the rate Variable rate (only base rate, margin can be applied)

Overdraft rate for those who run

Small business 6.66% per annum

Loan rate for those who run

Small business 5.46 % per annum

Development Rate for business 6.57% per annum

Overdraft rate for business 7.39% per annum

Business equity access rate 5.69% per annum

Fixed rates on and from 14/08/2018

Term of loan Fixed rates (only base rates, margin can be applied)

For one year 5.30 percent

For two years 5.40 percent

For three years 5.40 percent

9

Variable rates and fixed rate are the types of business loan rates available to businesses:

Variable rates have a tendency to fluctuates up and down which depend upon the market

condition, so the repayments of company after the end of the loan period will also vary

when the rate changes. The financial institution or banks may add certain percentage of

margins on the loan sanctioned by them to the company. The interest on loan is

accounted on daily basis.

Fixed rates remain constant during the entire period of loan. Fixed rate does not vary with

the market, so it remains fixed till the end of the tenure of loan.

Variable rates- on and from 24/09/2018

Names of the rate Variable rate (only base rate, margin can be applied)

Overdraft rate for those who run

Small business 6.66% per annum

Loan rate for those who run

Small business 5.46 % per annum

Development Rate for business 6.57% per annum

Overdraft rate for business 7.39% per annum

Business equity access rate 5.69% per annum

Fixed rates on and from 14/08/2018

Term of loan Fixed rates (only base rates, margin can be applied)

For one year 5.30 percent

For two years 5.40 percent

For three years 5.40 percent

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Weighted average cost of capital

For four years 5.54 percent

For five years 5.62 percent

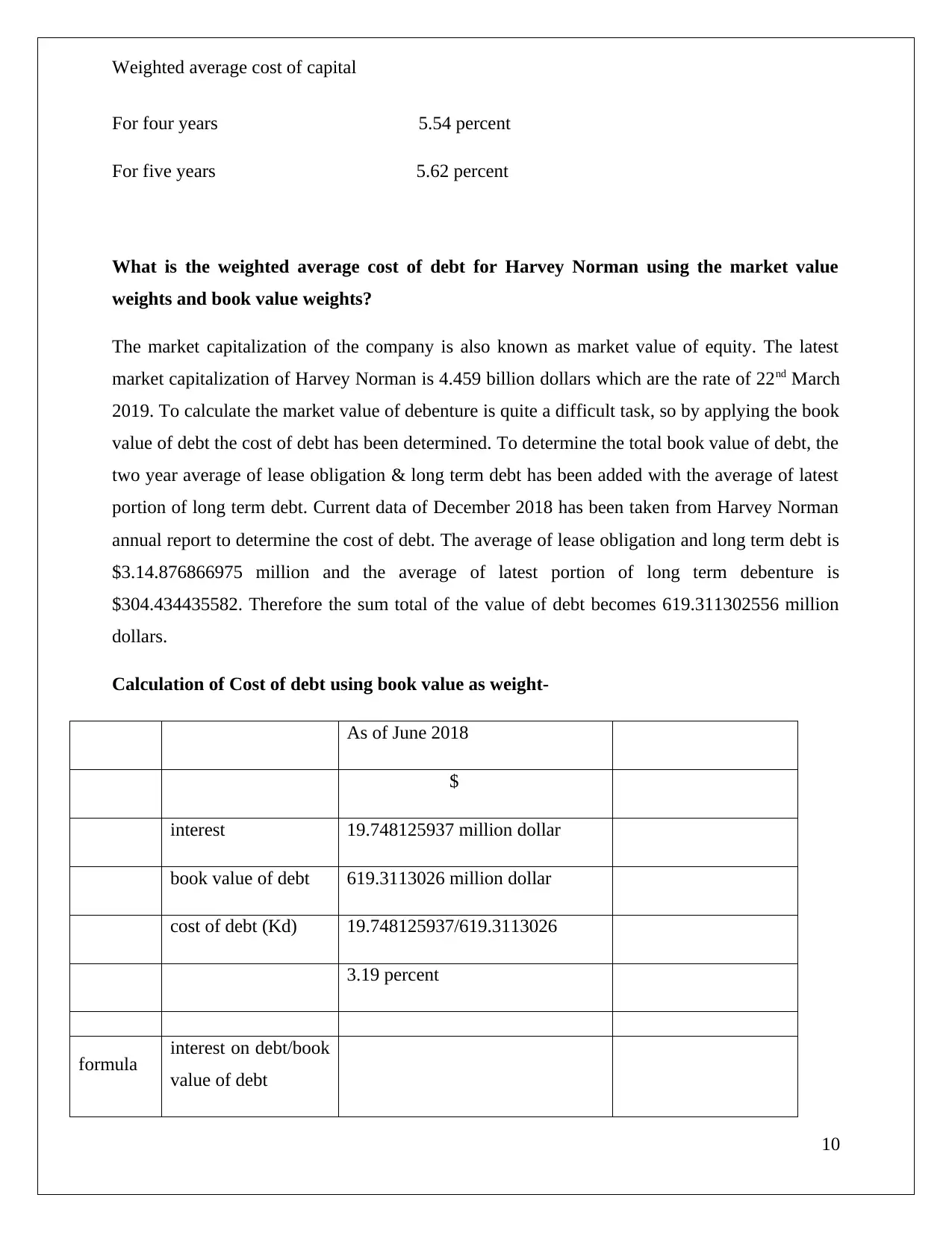

What is the weighted average cost of debt for Harvey Norman using the market value

weights and book value weights?

The market capitalization of the company is also known as market value of equity. The latest

market capitalization of Harvey Norman is 4.459 billion dollars which are the rate of 22nd March

2019. To calculate the market value of debenture is quite a difficult task, so by applying the book

value of debt the cost of debt has been determined. To determine the total book value of debt, the

two year average of lease obligation & long term debt has been added with the average of latest

portion of long term debt. Current data of December 2018 has been taken from Harvey Norman

annual report to determine the cost of debt. The average of lease obligation and long term debt is

$3.14.876866975 million and the average of latest portion of long term debenture is

$304.434435582. Therefore the sum total of the value of debt becomes 619.311302556 million

dollars.

Calculation of Cost of debt using book value as weight-

As of June 2018

$

interest 19.748125937 million dollar

book value of debt 619.3113026 million dollar

cost of debt (Kd) 19.748125937/619.3113026

3.19 percent

formula interest on debt/book

value of debt

10

For four years 5.54 percent

For five years 5.62 percent

What is the weighted average cost of debt for Harvey Norman using the market value

weights and book value weights?

The market capitalization of the company is also known as market value of equity. The latest

market capitalization of Harvey Norman is 4.459 billion dollars which are the rate of 22nd March

2019. To calculate the market value of debenture is quite a difficult task, so by applying the book

value of debt the cost of debt has been determined. To determine the total book value of debt, the

two year average of lease obligation & long term debt has been added with the average of latest

portion of long term debt. Current data of December 2018 has been taken from Harvey Norman

annual report to determine the cost of debt. The average of lease obligation and long term debt is

$3.14.876866975 million and the average of latest portion of long term debenture is

$304.434435582. Therefore the sum total of the value of debt becomes 619.311302556 million

dollars.

Calculation of Cost of debt using book value as weight-

As of June 2018

$

interest 19.748125937 million dollar

book value of debt 619.3113026 million dollar

cost of debt (Kd) 19.748125937/619.3113026

3.19 percent

formula interest on debt/book

value of debt

10

Weighted average cost of capital

As it can be observe that the cost of debt of Harvey Norman by using book value as weight is

3.19 percent. As opined by Berger et al. (2018, p-270), if the company uses the market value of

weights to calculate the cost of debt, the company will be able to meet the expectations of

debenture holders. According to Glover (2016, p-299), if book value weights are used by

company to determine its cost of debt, then the debenture holder’s expectations of giving high

rate of interest will not be met by the company.

Will be there any disagreement if we apply the market weights or book value weights as

per the case study?

Yes, of course, it will make a difference if we use market value weights or book value weights to

calculate the weighted average cost of debt. Book value-weighted average of cost of debt is

determined by using the book value weight of debt of company. Market value weighted average

cost of capital is calculated by using the market value weights of debt of company. The book

value weights are always available in the company's balance sheet. If the company is unlisted, it

becomes a difficult task to find the market value weights of that company. Market value

weighted average cost of debt is acceptable in the market because the shareholders would

demand expected rate of return on market value of debt and not in book value.

4. Weighted average cost of capital using book value as weights and market value as

weights.

Weighted average cost of capital of Harvey Norman can be calculated by using the market value

weights or book value weights. The debenture holders, investors, equity shareholders, and

preference shareholders use market value weights because it fulfills the investor expectation. The

percentage of different sources of finance which are used by the company is different. For

example, not all the companies would have same percentage of debt, preference share capital,

and equity share capital. So it is better not to apply simple average and to use weighted average

to determine the overall cost of capital of company.

11

As it can be observe that the cost of debt of Harvey Norman by using book value as weight is

3.19 percent. As opined by Berger et al. (2018, p-270), if the company uses the market value of

weights to calculate the cost of debt, the company will be able to meet the expectations of

debenture holders. According to Glover (2016, p-299), if book value weights are used by

company to determine its cost of debt, then the debenture holder’s expectations of giving high

rate of interest will not be met by the company.

Will be there any disagreement if we apply the market weights or book value weights as

per the case study?

Yes, of course, it will make a difference if we use market value weights or book value weights to

calculate the weighted average cost of debt. Book value-weighted average of cost of debt is

determined by using the book value weight of debt of company. Market value weighted average

cost of capital is calculated by using the market value weights of debt of company. The book

value weights are always available in the company's balance sheet. If the company is unlisted, it

becomes a difficult task to find the market value weights of that company. Market value

weighted average cost of debt is acceptable in the market because the shareholders would

demand expected rate of return on market value of debt and not in book value.

4. Weighted average cost of capital using book value as weights and market value as

weights.

Weighted average cost of capital of Harvey Norman can be calculated by using the market value

weights or book value weights. The debenture holders, investors, equity shareholders, and

preference shareholders use market value weights because it fulfills the investor expectation. The

percentage of different sources of finance which are used by the company is different. For

example, not all the companies would have same percentage of debt, preference share capital,

and equity share capital. So it is better not to apply simple average and to use weighted average

to determine the overall cost of capital of company.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.