University Financial Reporting: Analysis of Accounting Principles

VerifiedAdded on 2020/04/21

|14

|2206

|89

Homework Assignment

AI Summary

This assignment, prepared by a student, delves into the core concepts of financial reporting. It commences with an exploration of fundamental accounting principles, including the accounting entity assumption and the significance of a fixed asset register. The assignment proceeds to examine journal entries, the impact of asset sales, and the treatment of unearned income and doubtful debts. It provides detailed examples of balance day adjustments, including accruals and deferrals. Furthermore, the assignment includes practical applications of depreciation methods such as straight-line, double-declining balance, and the sum-of-the-digits method, with comprehensive depreciation schedules and journal entries. The document provides a thorough understanding of key accounting practices, making it a valuable resource for students studying finance and accounting.

Running head: PREPARE FINANCIAL REPORTS

Prepare Financial Reports (Assessment 1)

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Prepare Financial Reports (Assessment 1)

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PREPARE FINANCIAL REPORTS

Table of Contents

Task 1:............................................................................................................................. 2

Answer to Question 1:..................................................................................................2

Answer to Question 2:..................................................................................................2

Answer to Question 3:..................................................................................................3

Answer to Question 4:..................................................................................................3

Answer to Question 5:..................................................................................................3

Answer to Question 6:..................................................................................................4

Answer to Question 7:..................................................................................................6

Answer to Question 8:..................................................................................................6

Answer to Part A:......................................................................................................6

Answer to Part B:......................................................................................................6

Answer to Part C:......................................................................................................7

Answer to Part D:......................................................................................................8

Answer to Part E:......................................................................................................8

Answer to Part F:...................................................................................................... 8

Answer to Question 9:..................................................................................................9

Task 2: Depreciation of assets.......................................................................................10

Straight-line method:.................................................................................................. 10

Double declining balance method:..............................................................................11

Sum of the digits method:...........................................................................................12

References:....................................................................................................................14

Student Name:

Student Number:

1

Table of Contents

Task 1:............................................................................................................................. 2

Answer to Question 1:..................................................................................................2

Answer to Question 2:..................................................................................................2

Answer to Question 3:..................................................................................................3

Answer to Question 4:..................................................................................................3

Answer to Question 5:..................................................................................................3

Answer to Question 6:..................................................................................................4

Answer to Question 7:..................................................................................................6

Answer to Question 8:..................................................................................................6

Answer to Part A:......................................................................................................6

Answer to Part B:......................................................................................................6

Answer to Part C:......................................................................................................7

Answer to Part D:......................................................................................................8

Answer to Part E:......................................................................................................8

Answer to Part F:...................................................................................................... 8

Answer to Question 9:..................................................................................................9

Task 2: Depreciation of assets.......................................................................................10

Straight-line method:.................................................................................................. 10

Double declining balance method:..............................................................................11

Sum of the digits method:...........................................................................................12

References:....................................................................................................................14

Student Name:

Student Number:

1

PREPARE FINANCIAL REPORTS

Student Name:

Student Number:

2

Student Name:

Student Number:

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PREPARE FINANCIAL REPORTS

Task 1:

Answer to Question 1:

According to the accounting entity assumption, a business has a separate

financial status and the position is distinct from the funding of its owners, staffs or

stockholders. This implies that the accounting data from the business are separated and

these would remain identical irrespective of the personal finances of the owners

(Benson, Faff and Smith 2014). This doctrine is applied to entities, partnerships and

sole proprietorships. For sole proprietorship business, the owner could still report

business income by filing personal income tax return and the personal funds could be

placed directly into the business.

In addition, with the help of this assumption, the accountants are able to

investigate businesses in isolation irrespective of the status of ownership. It paves the

path of developing financial statements that depict the performance of a business, even

if there is different public perception due to the financial activities on the part of the

owner. Along with this, this assumption states that each transaction needs to be

apportioned to a single corporation, which restricts the accountants to deal with

duplicate accounting entries.

Answer to Question 2:

Fixed asset register is a complete document that depicts the assets owned on

the part of an organisation. These assets might take into account buildings and

improvements, land, plant and equipment, copyrights, trademarks and others. Fixed

asset register is highly important for a business because of the following reasons:

An effective asset register depicts significant planning tool, since it enables the

organisation to keep track of the details of all fixed assets including the date of

purchase and risk assessment.

Student Name:

Student Number:

3

Task 1:

Answer to Question 1:

According to the accounting entity assumption, a business has a separate

financial status and the position is distinct from the funding of its owners, staffs or

stockholders. This implies that the accounting data from the business are separated and

these would remain identical irrespective of the personal finances of the owners

(Benson, Faff and Smith 2014). This doctrine is applied to entities, partnerships and

sole proprietorships. For sole proprietorship business, the owner could still report

business income by filing personal income tax return and the personal funds could be

placed directly into the business.

In addition, with the help of this assumption, the accountants are able to

investigate businesses in isolation irrespective of the status of ownership. It paves the

path of developing financial statements that depict the performance of a business, even

if there is different public perception due to the financial activities on the part of the

owner. Along with this, this assumption states that each transaction needs to be

apportioned to a single corporation, which restricts the accountants to deal with

duplicate accounting entries.

Answer to Question 2:

Fixed asset register is a complete document that depicts the assets owned on

the part of an organisation. These assets might take into account buildings and

improvements, land, plant and equipment, copyrights, trademarks and others. Fixed

asset register is highly important for a business because of the following reasons:

An effective asset register depicts significant planning tool, since it enables the

organisation to keep track of the details of all fixed assets including the date of

purchase and risk assessment.

Student Name:

Student Number:

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PREPARE FINANCIAL REPORTS

Fraud could be prevented with the help of asset register, when there are

accurate controls in place. This minimises the theft of assets and opportunity to

lose assets at customer sites and service providers (Franks 2014).

By tracking the asset movement, a business could optimise the asset utilisation

including increased billings. With the help of asset register, the assets of an

organisation are protected from any threat that would influence the ability of the

business in maximising revenue.

Answer to Question 3:

Journal is termed as the basic book of accounting. More precisely, it is the book

of prime entry and the procedure of recording transactions into journal is called

journalising. Journal could be explained as a book where the transactions are recorded

in the chronological order. The basic functions of journal in the process of accounting

are depicted briefly as follows:

To evaluate each transaction into credit and debit for enabling their posting into

the ledger

To make chronological arrangement of the transactions in order of date

Answer to Question 4:

If an organisation sells an asset by incurring loss, three different accounts would

be affected in the process, which include the following:

The cash received

The asset sold

Loss incurred on asset sale

Therefore, the following journal entry would be passed to record the transaction:

Cash Account/ Bank Account Debit Real Account Debit- what comes in

Loss on Sale of Asset Account Debit Nominal Account Debit- all losses

To Sale of Asset Account Credit Real Account Credit- what goes out

Student Name:

Student Number:

4

Fraud could be prevented with the help of asset register, when there are

accurate controls in place. This minimises the theft of assets and opportunity to

lose assets at customer sites and service providers (Franks 2014).

By tracking the asset movement, a business could optimise the asset utilisation

including increased billings. With the help of asset register, the assets of an

organisation are protected from any threat that would influence the ability of the

business in maximising revenue.

Answer to Question 3:

Journal is termed as the basic book of accounting. More precisely, it is the book

of prime entry and the procedure of recording transactions into journal is called

journalising. Journal could be explained as a book where the transactions are recorded

in the chronological order. The basic functions of journal in the process of accounting

are depicted briefly as follows:

To evaluate each transaction into credit and debit for enabling their posting into

the ledger

To make chronological arrangement of the transactions in order of date

Answer to Question 4:

If an organisation sells an asset by incurring loss, three different accounts would

be affected in the process, which include the following:

The cash received

The asset sold

Loss incurred on asset sale

Therefore, the following journal entry would be passed to record the transaction:

Cash Account/ Bank Account Debit Real Account Debit- what comes in

Loss on Sale of Asset Account Debit Nominal Account Debit- all losses

To Sale of Asset Account Credit Real Account Credit- what goes out

Student Name:

Student Number:

4

PREPARE FINANCIAL REPORTS

Answer to Question 5:

Unearned income is an internal revenue service term for income, which is not

gathered by participating in a trade or business like bonuses and salaries, commissions,

wages and tips. It takes into account dividends, interest, pensions, unemployment

benefits, social security, child support and alimony. For instance, a person works in the

operations department for the company ABC. His salary is $75,000 per annum and in

this year, he received a bonus of $5,000 as well. Therefore, his earned income is

$(75,000 + 5,000) = $80,000. The person owns some dividend stocks as well and he

receives pension from his initial career as a sportsperson. He receives $300 per month

in dividends and $1,000 per month from his pension. Therefore, the unearned income of

the person is $(300 + 1,000) x 12 = $15,600.

An organisation should recognise income, when it fulfils the below-stated criteria:

The price is fixed substantially at the date of sale.

The seller has been paid or the purchaser is under an obligation to pay the seller.

There is no contingency of the payment on the buyer reselling the product

(Loughran and McDonald 2016).

There is no change on the obligation of the purchaser in case of destruction or

damage of the product

There is economic substance of the buyer besides from the seller

There is no additional performance obligations associated with sale on the part of

the seller

There is reasonable estimation on the amount of future returns on the part of the

seller

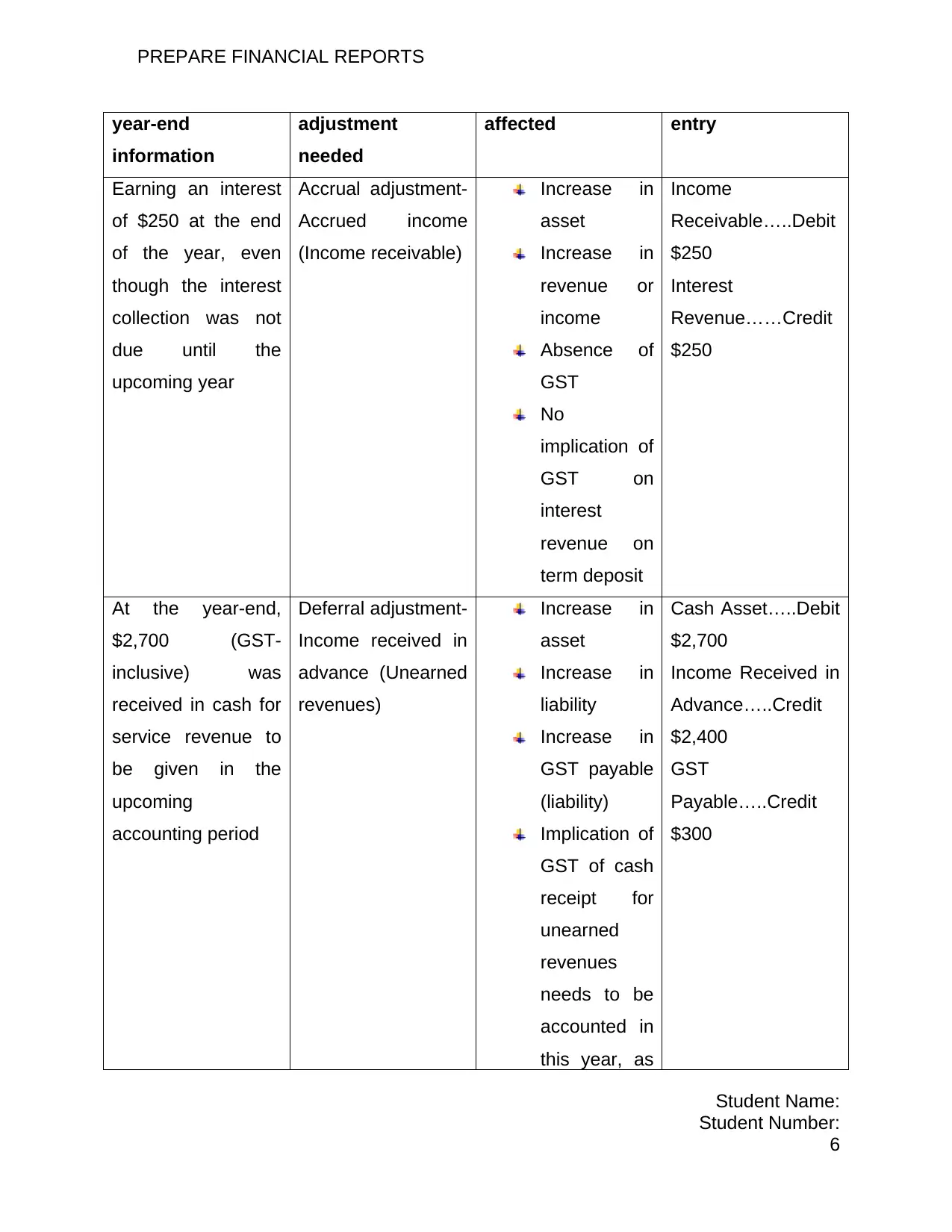

Answer to Question 6:

The two instances of balance day adjustments that an organisation needs to

record before issuing the final financial report at the end of accounting periods are

represented as follows:

Availability of Type of Type of accounts Adjusting journal

Student Name:

Student Number:

5

Answer to Question 5:

Unearned income is an internal revenue service term for income, which is not

gathered by participating in a trade or business like bonuses and salaries, commissions,

wages and tips. It takes into account dividends, interest, pensions, unemployment

benefits, social security, child support and alimony. For instance, a person works in the

operations department for the company ABC. His salary is $75,000 per annum and in

this year, he received a bonus of $5,000 as well. Therefore, his earned income is

$(75,000 + 5,000) = $80,000. The person owns some dividend stocks as well and he

receives pension from his initial career as a sportsperson. He receives $300 per month

in dividends and $1,000 per month from his pension. Therefore, the unearned income of

the person is $(300 + 1,000) x 12 = $15,600.

An organisation should recognise income, when it fulfils the below-stated criteria:

The price is fixed substantially at the date of sale.

The seller has been paid or the purchaser is under an obligation to pay the seller.

There is no contingency of the payment on the buyer reselling the product

(Loughran and McDonald 2016).

There is no change on the obligation of the purchaser in case of destruction or

damage of the product

There is economic substance of the buyer besides from the seller

There is no additional performance obligations associated with sale on the part of

the seller

There is reasonable estimation on the amount of future returns on the part of the

seller

Answer to Question 6:

The two instances of balance day adjustments that an organisation needs to

record before issuing the final financial report at the end of accounting periods are

represented as follows:

Availability of Type of Type of accounts Adjusting journal

Student Name:

Student Number:

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PREPARE FINANCIAL REPORTS

year-end

information

adjustment

needed

affected entry

Earning an interest

of $250 at the end

of the year, even

though the interest

collection was not

due until the

upcoming year

Accrual adjustment-

Accrued income

(Income receivable)

Increase in

asset

Increase in

revenue or

income

Absence of

GST

No

implication of

GST on

interest

revenue on

term deposit

Income

Receivable…..Debit

$250

Interest

Revenue……Credit

$250

At the year-end,

$2,700 (GST-

inclusive) was

received in cash for

service revenue to

be given in the

upcoming

accounting period

Deferral adjustment-

Income received in

advance (Unearned

revenues)

Increase in

asset

Increase in

liability

Increase in

GST payable

(liability)

Implication of

GST of cash

receipt for

unearned

revenues

needs to be

accounted in

this year, as

Cash Asset…..Debit

$2,700

Income Received in

Advance…..Credit

$2,400

GST

Payable…..Credit

$300

Student Name:

Student Number:

6

year-end

information

adjustment

needed

affected entry

Earning an interest

of $250 at the end

of the year, even

though the interest

collection was not

due until the

upcoming year

Accrual adjustment-

Accrued income

(Income receivable)

Increase in

asset

Increase in

revenue or

income

Absence of

GST

No

implication of

GST on

interest

revenue on

term deposit

Income

Receivable…..Debit

$250

Interest

Revenue……Credit

$250

At the year-end,

$2,700 (GST-

inclusive) was

received in cash for

service revenue to

be given in the

upcoming

accounting period

Deferral adjustment-

Income received in

advance (Unearned

revenues)

Increase in

asset

Increase in

liability

Increase in

GST payable

(liability)

Implication of

GST of cash

receipt for

unearned

revenues

needs to be

accounted in

this year, as

Cash Asset…..Debit

$2,700

Income Received in

Advance…..Credit

$2,400

GST

Payable…..Credit

$300

Student Name:

Student Number:

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PREPARE FINANCIAL REPORTS

the GST has

been

received in

cash, which

is payable to

ATO

Answer to Question 7:

An amount for doubtful debts is a reserve in contrast to the future realisation of

certain accounts receivable in the form of being uncollectible. For instance, if an

organisation issues invoices of $1 million to the customers in a provided month having

an experience of 5% bad debts on its billings, it would be appropriate in creating a

provision for bad debt for $50,000 (which is 5% of $1 million).

The steps that could be taken to compute the allowance are depicted as follows:

Recording the journal entry to realise sale on credit

Recording the journal entry to create the allowance for doubtful account

Adjusting the balance of the allowance account, as required

Recording the journal entry to realise uncollectible account (McLaney and Atrill

2014)

Reversing the entry on payment

Answer to Question 8:

Answer to Part A:

Date Particulars

Debit amount

(in $)

Credit amount

(in $)

30/06/2012 Wages Expense Account…………...Dr 2,650

To Wages Payable Account 2,

Student Name:

Student Number:

7

the GST has

been

received in

cash, which

is payable to

ATO

Answer to Question 7:

An amount for doubtful debts is a reserve in contrast to the future realisation of

certain accounts receivable in the form of being uncollectible. For instance, if an

organisation issues invoices of $1 million to the customers in a provided month having

an experience of 5% bad debts on its billings, it would be appropriate in creating a

provision for bad debt for $50,000 (which is 5% of $1 million).

The steps that could be taken to compute the allowance are depicted as follows:

Recording the journal entry to realise sale on credit

Recording the journal entry to create the allowance for doubtful account

Adjusting the balance of the allowance account, as required

Recording the journal entry to realise uncollectible account (McLaney and Atrill

2014)

Reversing the entry on payment

Answer to Question 8:

Answer to Part A:

Date Particulars

Debit amount

(in $)

Credit amount

(in $)

30/06/2012 Wages Expense Account…………...Dr 2,650

To Wages Payable Account 2,

Student Name:

Student Number:

7

PREPARE FINANCIAL REPORTS

650

(To record wages unpaid at the end of

June)

Answer to Part B:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

1/12/2011 Rent Account……………..Dr

10,80

0

GST Account……………….Dr

1,2

00

To Cash/Bank Account

12,0

00

(To record rent paid inclusive of GST)

Answer to Part C:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

1/12/2011 Bank Account………Dr

20,00

0

To Loan Account

20,0

00

(To withhold cash by bank)

1/12/2011 Interest Expense Account………..Dr

5,4

00

To Loan Account

5,4

00

(To record monthly interest @4.5%

Student Name:

Student Number:

8

650

(To record wages unpaid at the end of

June)

Answer to Part B:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

1/12/2011 Rent Account……………..Dr

10,80

0

GST Account……………….Dr

1,2

00

To Cash/Bank Account

12,0

00

(To record rent paid inclusive of GST)

Answer to Part C:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

1/12/2011 Bank Account………Dr

20,00

0

To Loan Account

20,0

00

(To withhold cash by bank)

1/12/2011 Interest Expense Account………..Dr

5,4

00

To Loan Account

5,4

00

(To record monthly interest @4.5%

Student Name:

Student Number:

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

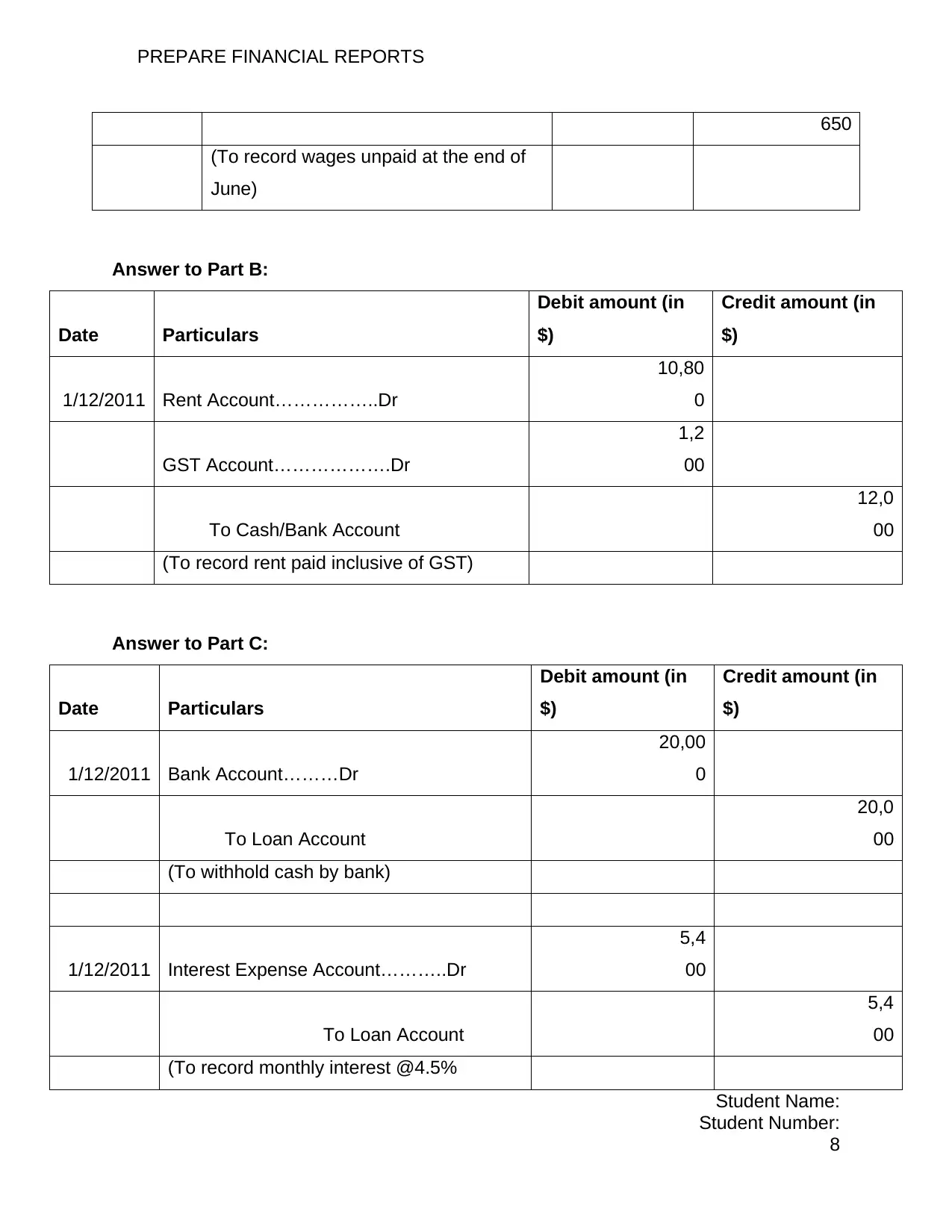

PREPARE FINANCIAL REPORTS

30/06/201

2 Loan Account………Dr

25,40

0

To Bank Account

25,4

00

(To issue bank guarantee)

Answer to Part D:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

30/06/201

2 Unearned Service Revenue Account…..Dr

2,0

00

To Service Revenue

Account

2,0

00

(To record unearned service revenue)

Answer to Part E:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

30/06/201

2 Cash/Bank Account…………..Dr

13,5

00

To Inventory Account

13,5

00

(To adjust overstatement of inventory)

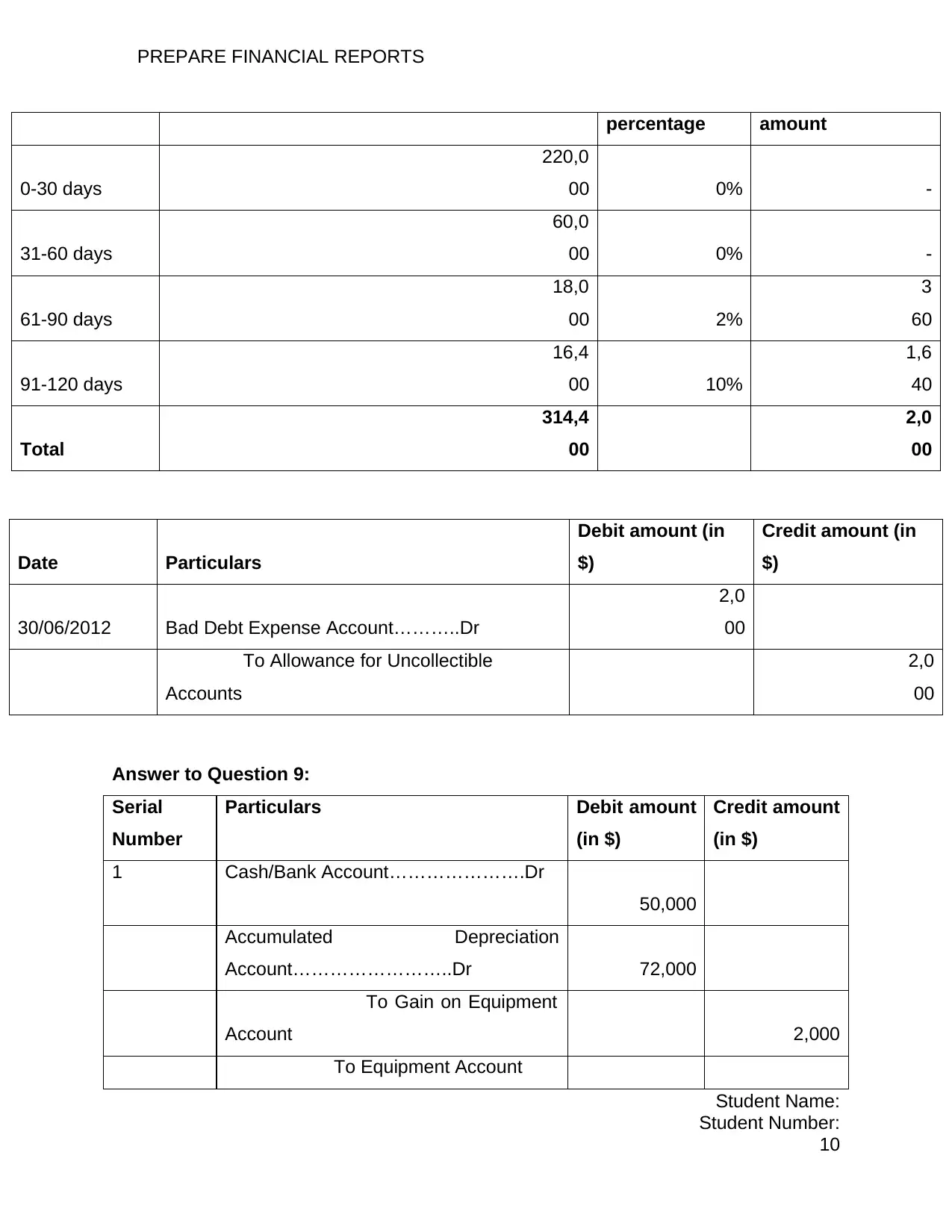

Answer to Part F:

Age of

account Category dollar amount

Estimated

uncollectible

Estimated

uncollectible dollar

Student Name:

Student Number:

9

30/06/201

2 Loan Account………Dr

25,40

0

To Bank Account

25,4

00

(To issue bank guarantee)

Answer to Part D:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

30/06/201

2 Unearned Service Revenue Account…..Dr

2,0

00

To Service Revenue

Account

2,0

00

(To record unearned service revenue)

Answer to Part E:

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

30/06/201

2 Cash/Bank Account…………..Dr

13,5

00

To Inventory Account

13,5

00

(To adjust overstatement of inventory)

Answer to Part F:

Age of

account Category dollar amount

Estimated

uncollectible

Estimated

uncollectible dollar

Student Name:

Student Number:

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PREPARE FINANCIAL REPORTS

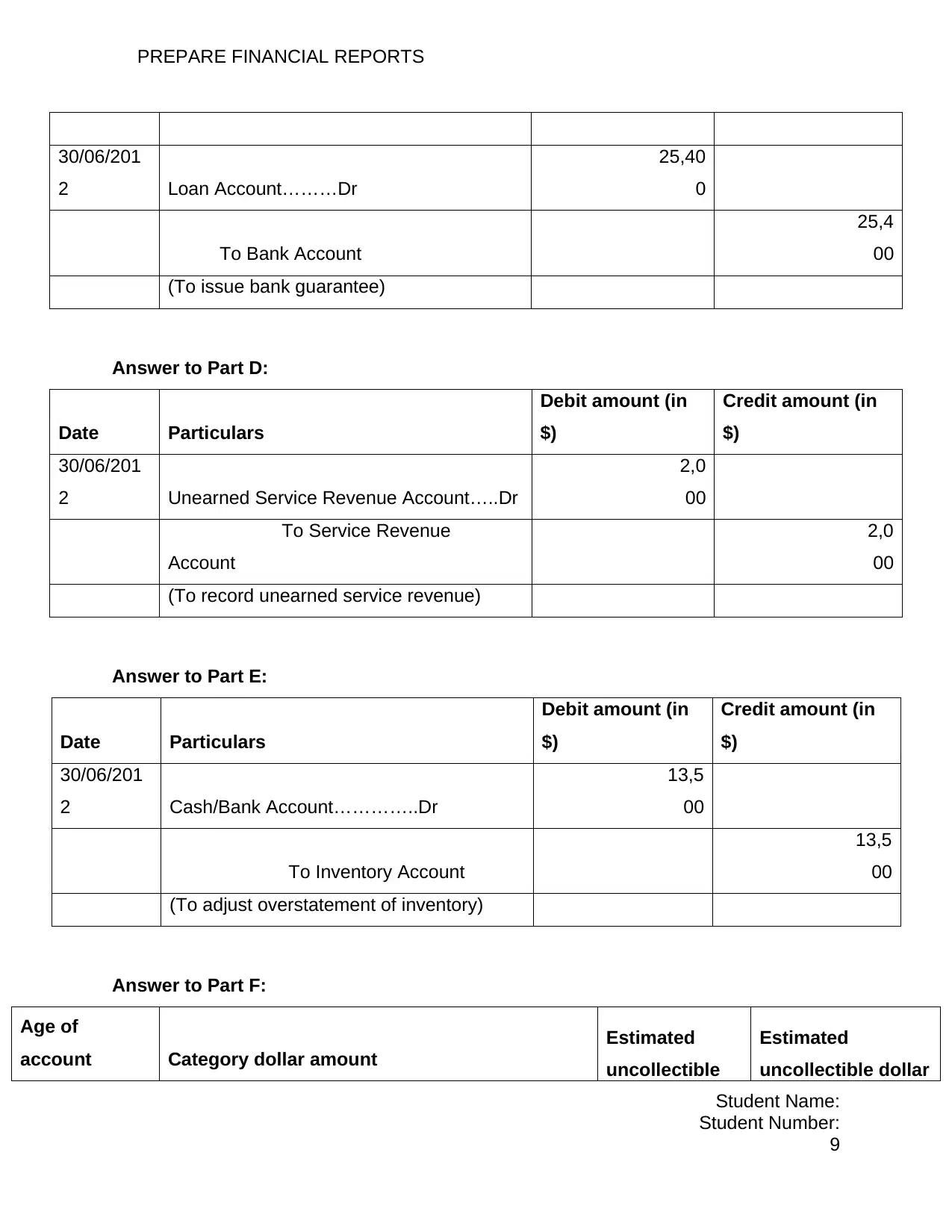

percentage amount

0-30 days

220,0

00 0% -

31-60 days

60,0

00 0% -

61-90 days

18,0

00 2%

3

60

91-120 days

16,4

00 10%

1,6

40

Total

314,4

00

2,0

00

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

30/06/2012 Bad Debt Expense Account………..Dr

2,0

00

To Allowance for Uncollectible

Accounts

2,0

00

Answer to Question 9:

Serial

Number

Particulars Debit amount

(in $)

Credit amount

(in $)

1 Cash/Bank Account………………….Dr

50,000

Accumulated Depreciation

Account……………………..Dr 72,000

To Gain on Equipment

Account 2,000

To Equipment Account

Student Name:

Student Number:

10

percentage amount

0-30 days

220,0

00 0% -

31-60 days

60,0

00 0% -

61-90 days

18,0

00 2%

3

60

91-120 days

16,4

00 10%

1,6

40

Total

314,4

00

2,0

00

Date Particulars

Debit amount (in

$)

Credit amount (in

$)

30/06/2012 Bad Debt Expense Account………..Dr

2,0

00

To Allowance for Uncollectible

Accounts

2,0

00

Answer to Question 9:

Serial

Number

Particulars Debit amount

(in $)

Credit amount

(in $)

1 Cash/Bank Account………………….Dr

50,000

Accumulated Depreciation

Account……………………..Dr 72,000

To Gain on Equipment

Account 2,000

To Equipment Account

Student Name:

Student Number:

10

PREPARE FINANCIAL REPORTS

120,000

(To record disposal of gain on

equipment)

2 Cash/Bank Account………………….Dr

20,000

Accumulated Depreciation

Account……………………..Dr 40,000

Loss on Asset Disposal

Account…………………Dr 20,000

To Motor Vehicle Account

80,000

(To record disposal of loss on

equipment)

Task 2: Depreciation of assets

Straight-line method:

Date

Asset

cost

Depreciation for the year

Accumulate

d

depreciation

Book

value

Depreciabl

e cost

Depreciatio

n rate (in

years)

Depreciatio

n expense

1/12/2011

$

1,750

$

1,750

31/12/201

5 (Salvage

value)

$

250

Student Name:

Student Number:

11

120,000

(To record disposal of gain on

equipment)

2 Cash/Bank Account………………….Dr

20,000

Accumulated Depreciation

Account……………………..Dr 40,000

Loss on Asset Disposal

Account…………………Dr 20,000

To Motor Vehicle Account

80,000

(To record disposal of loss on

equipment)

Task 2: Depreciation of assets

Straight-line method:

Date

Asset

cost

Depreciation for the year

Accumulate

d

depreciation

Book

value

Depreciabl

e cost

Depreciatio

n rate (in

years)

Depreciatio

n expense

1/12/2011

$

1,750

$

1,750

31/12/201

5 (Salvage

value)

$

250

Student Name:

Student Number:

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.