Financial Management Coursework Report: Bond and Stock Valuation

VerifiedAdded on 2019/12/03

|20

|4022

|111

Report

AI Summary

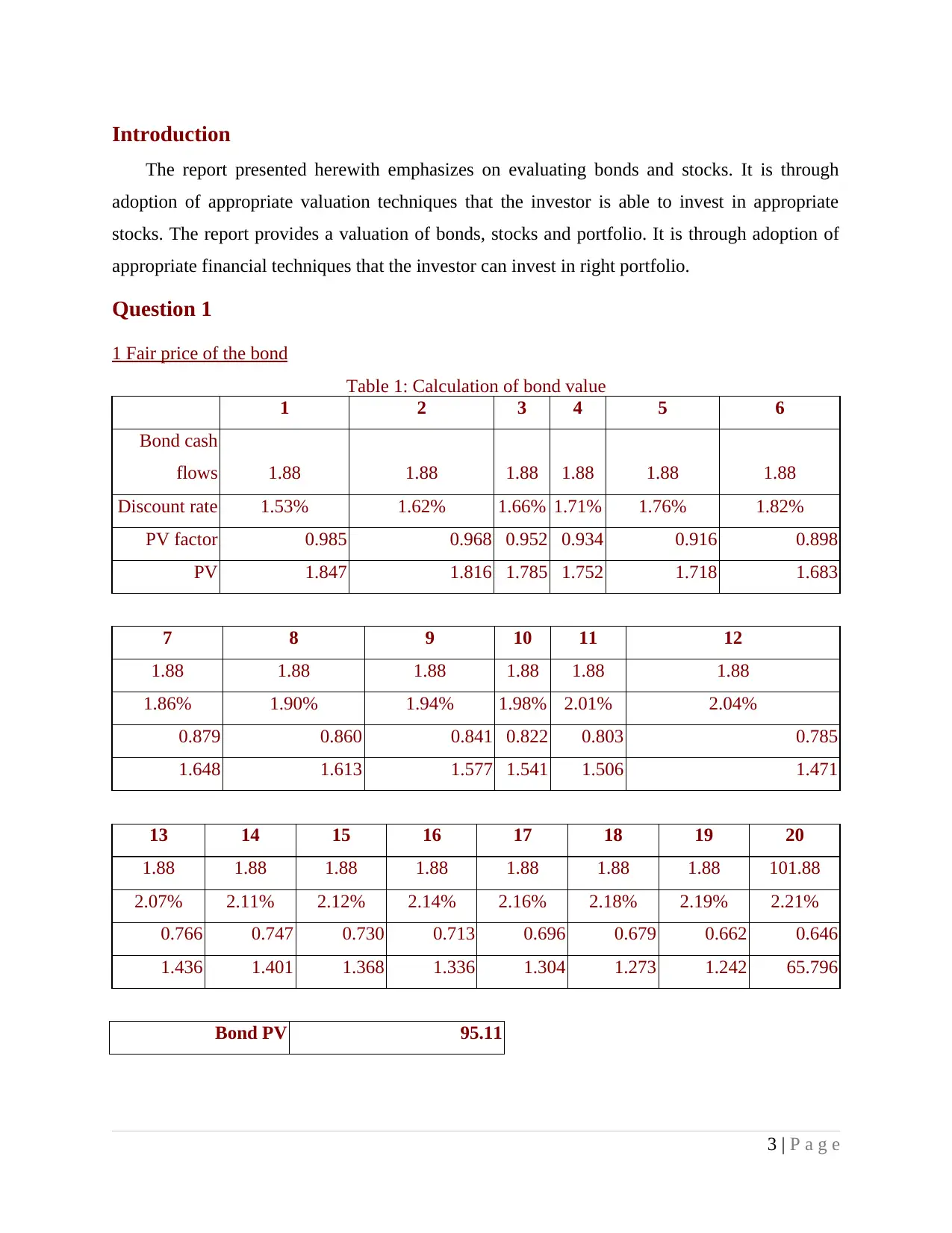

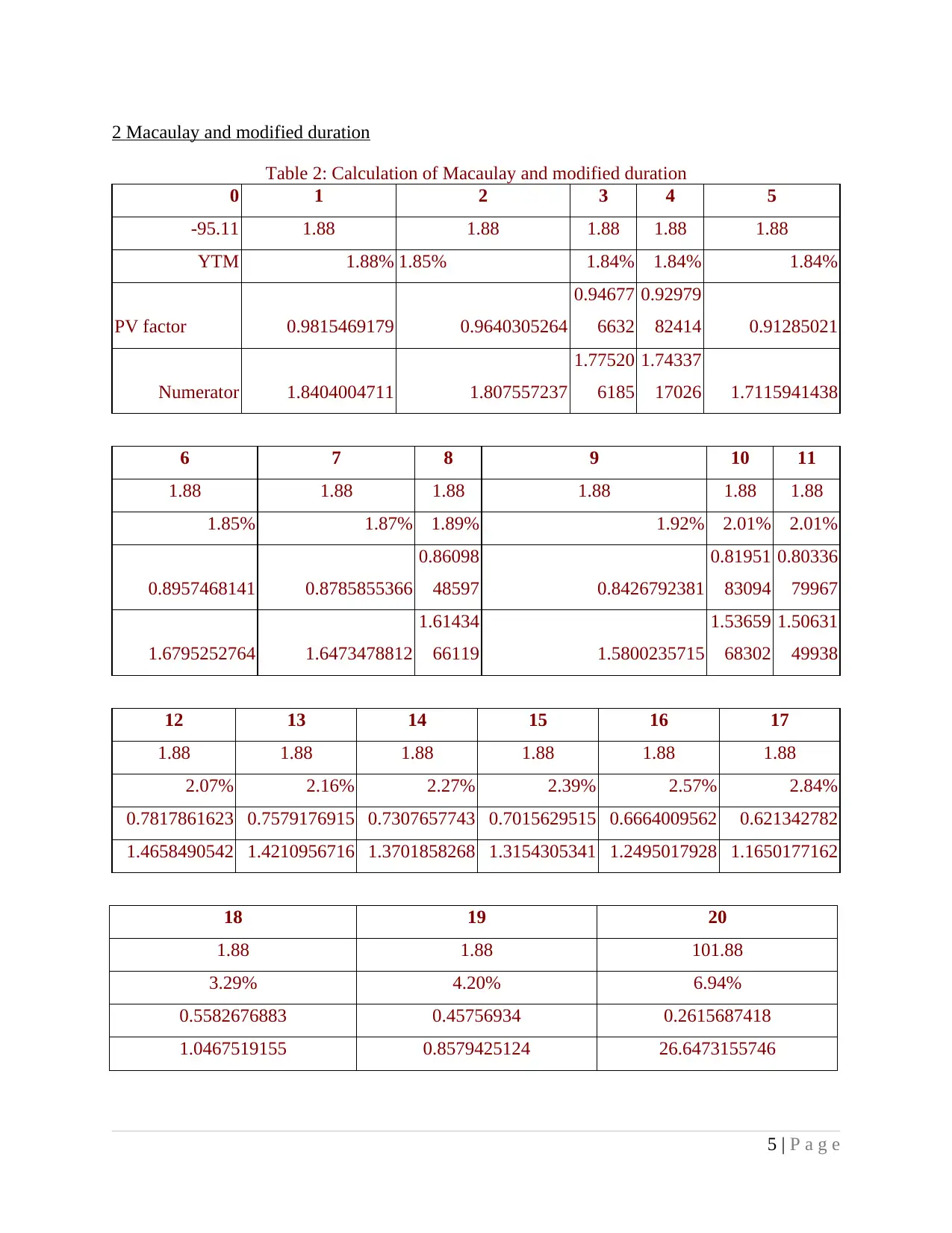

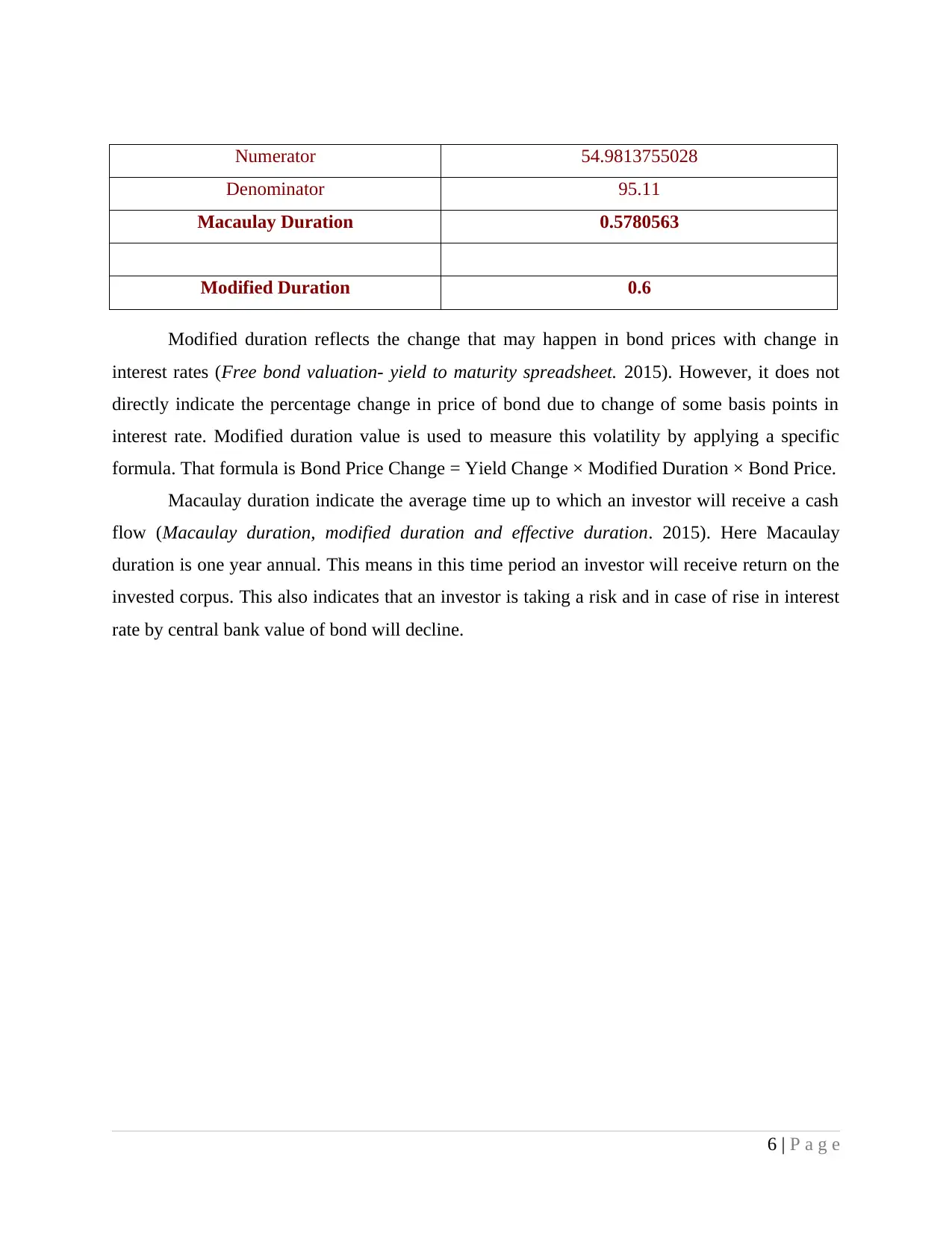

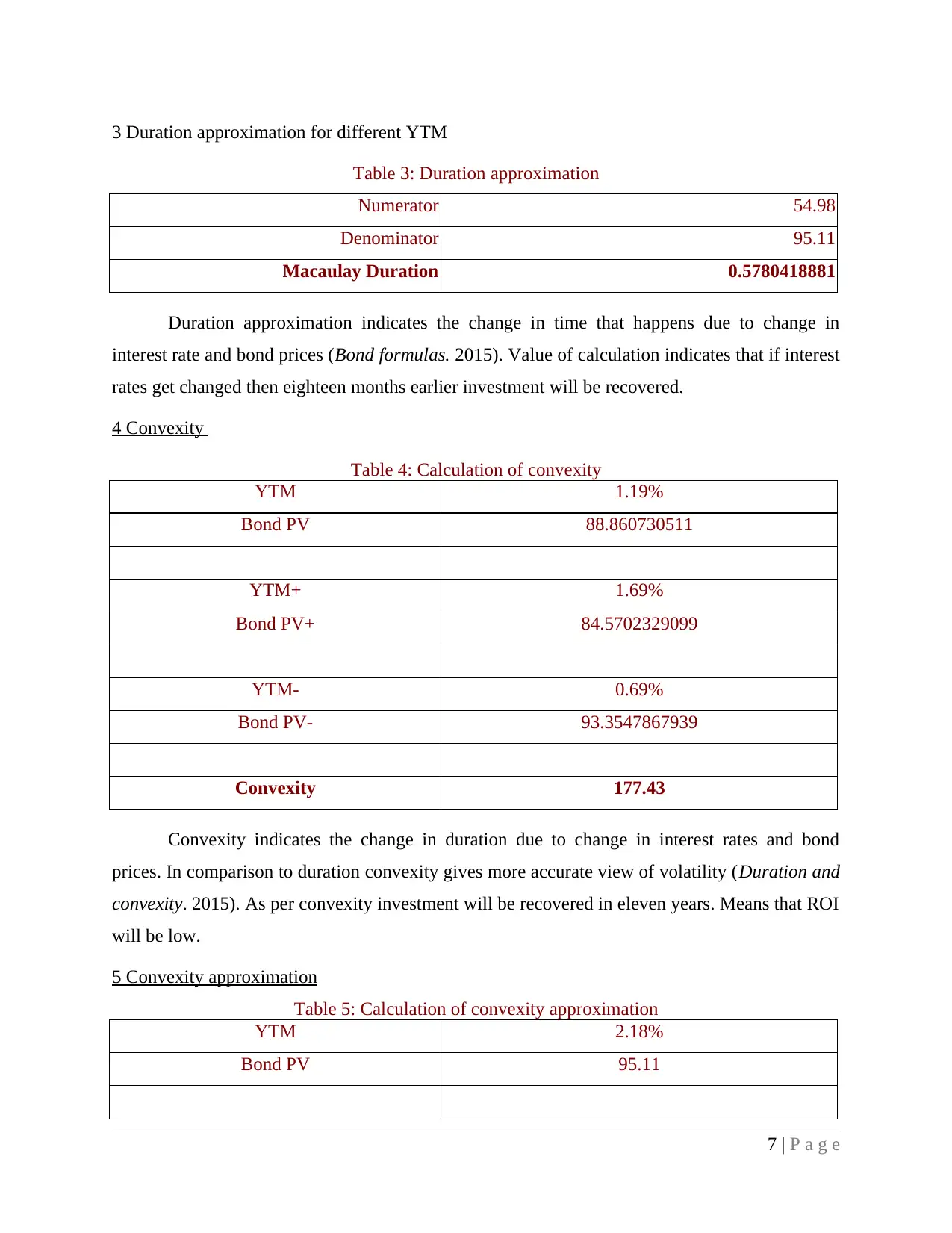

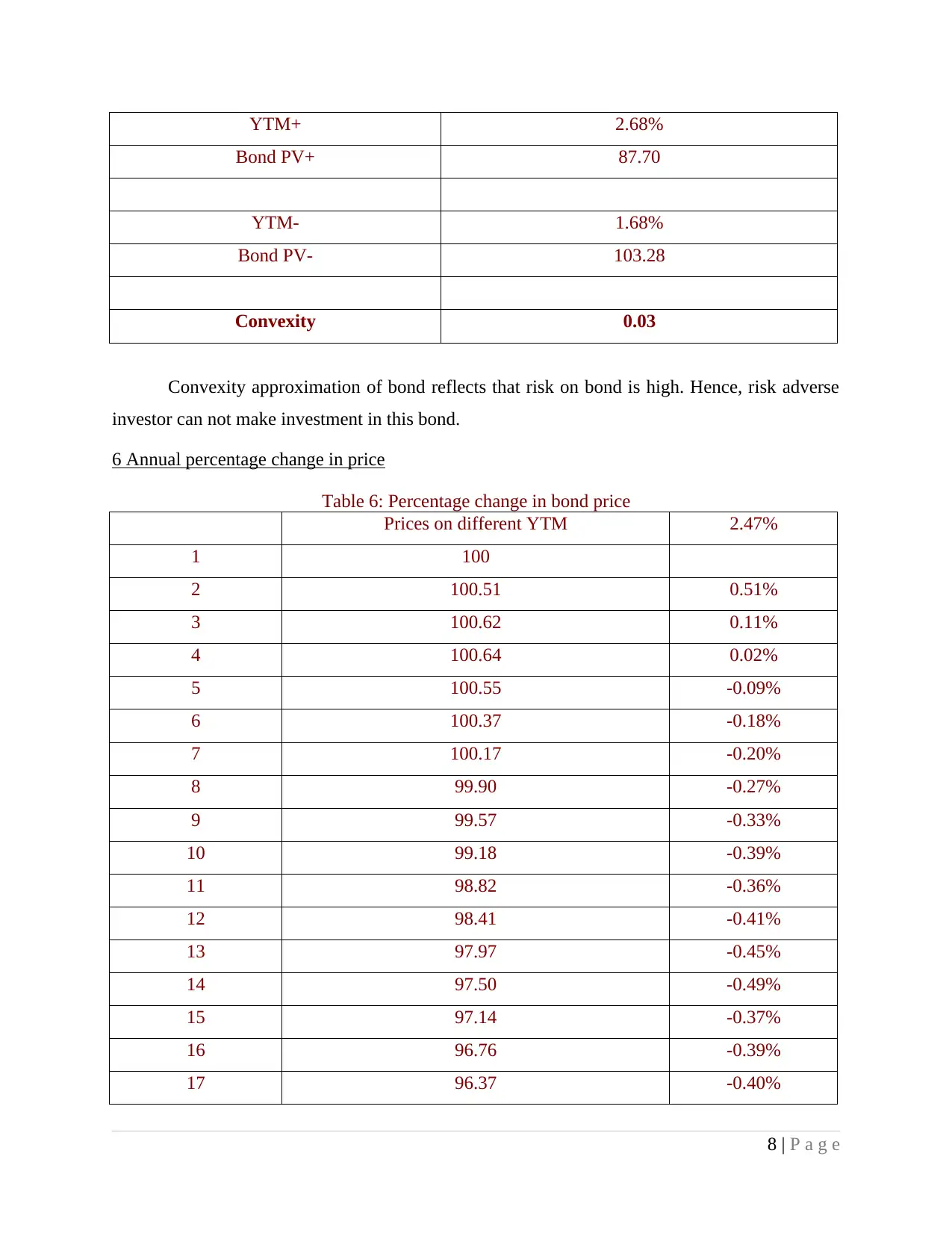

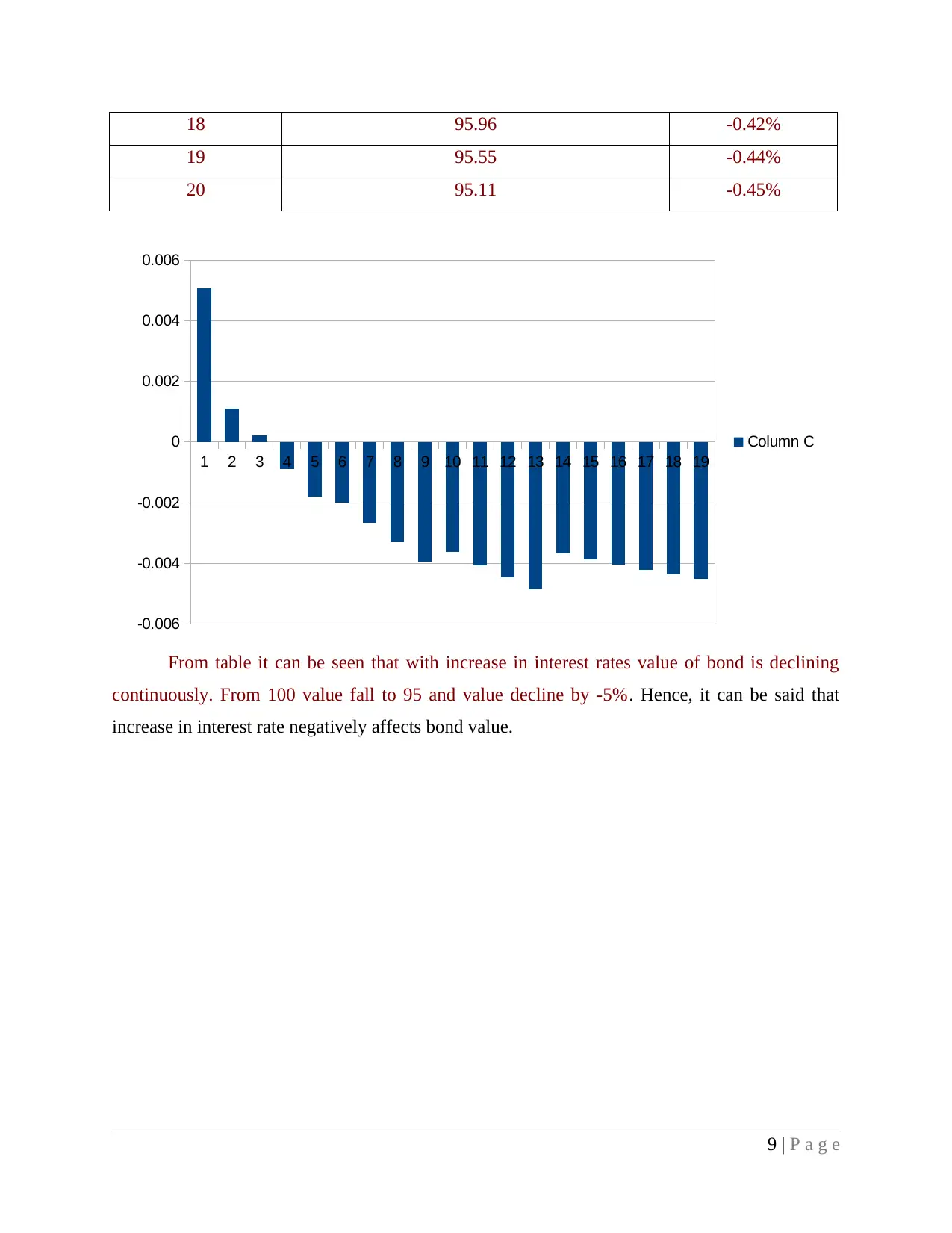

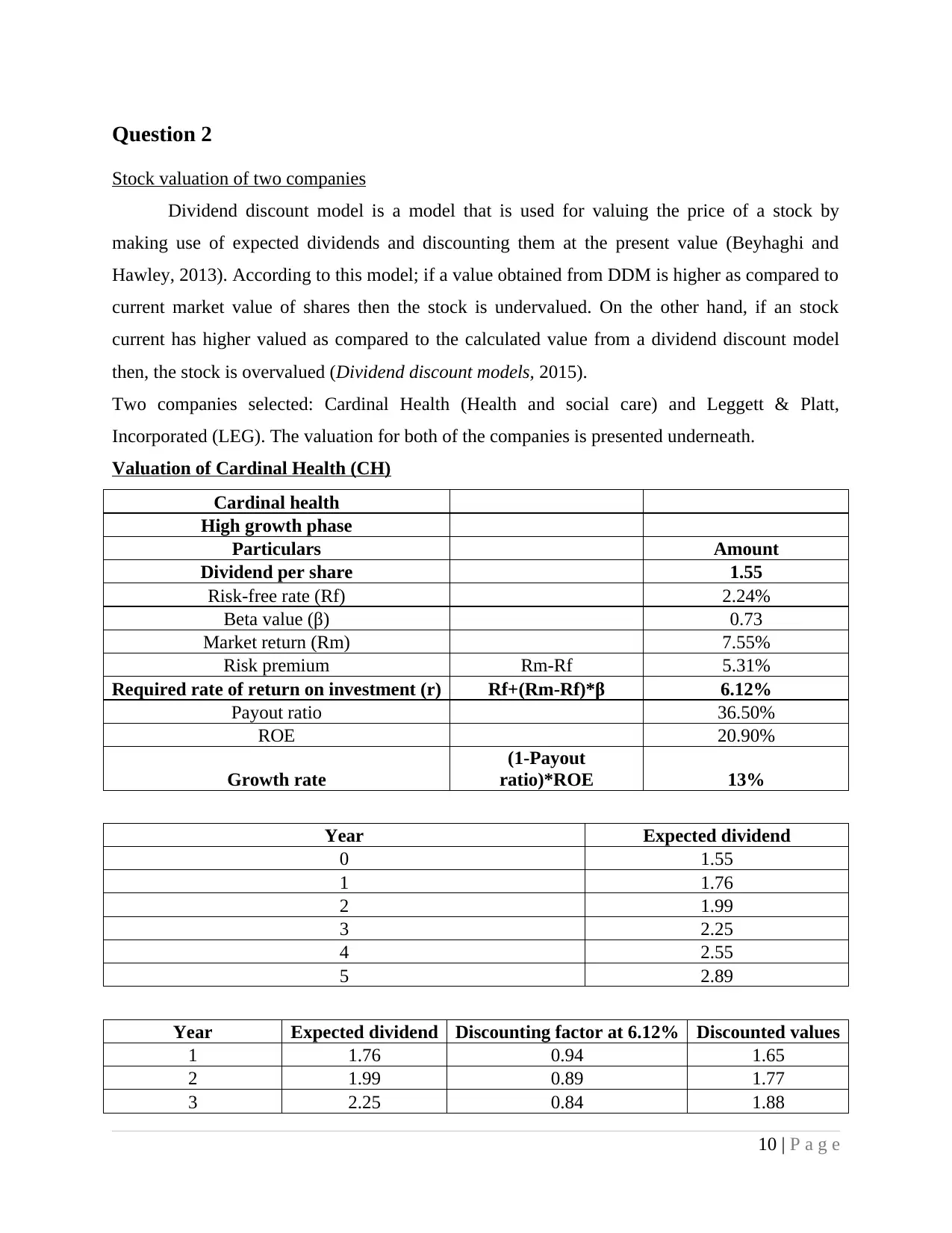

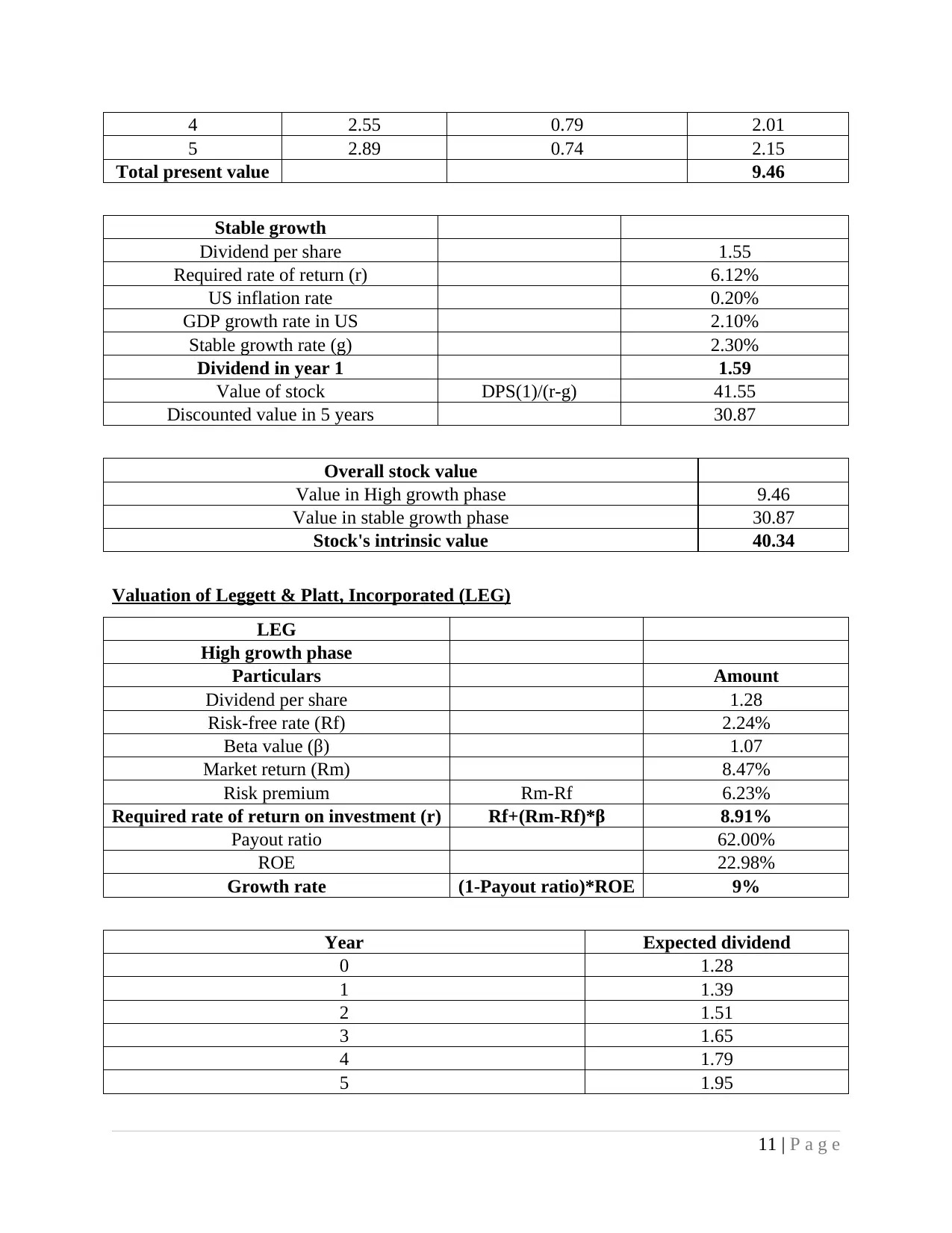

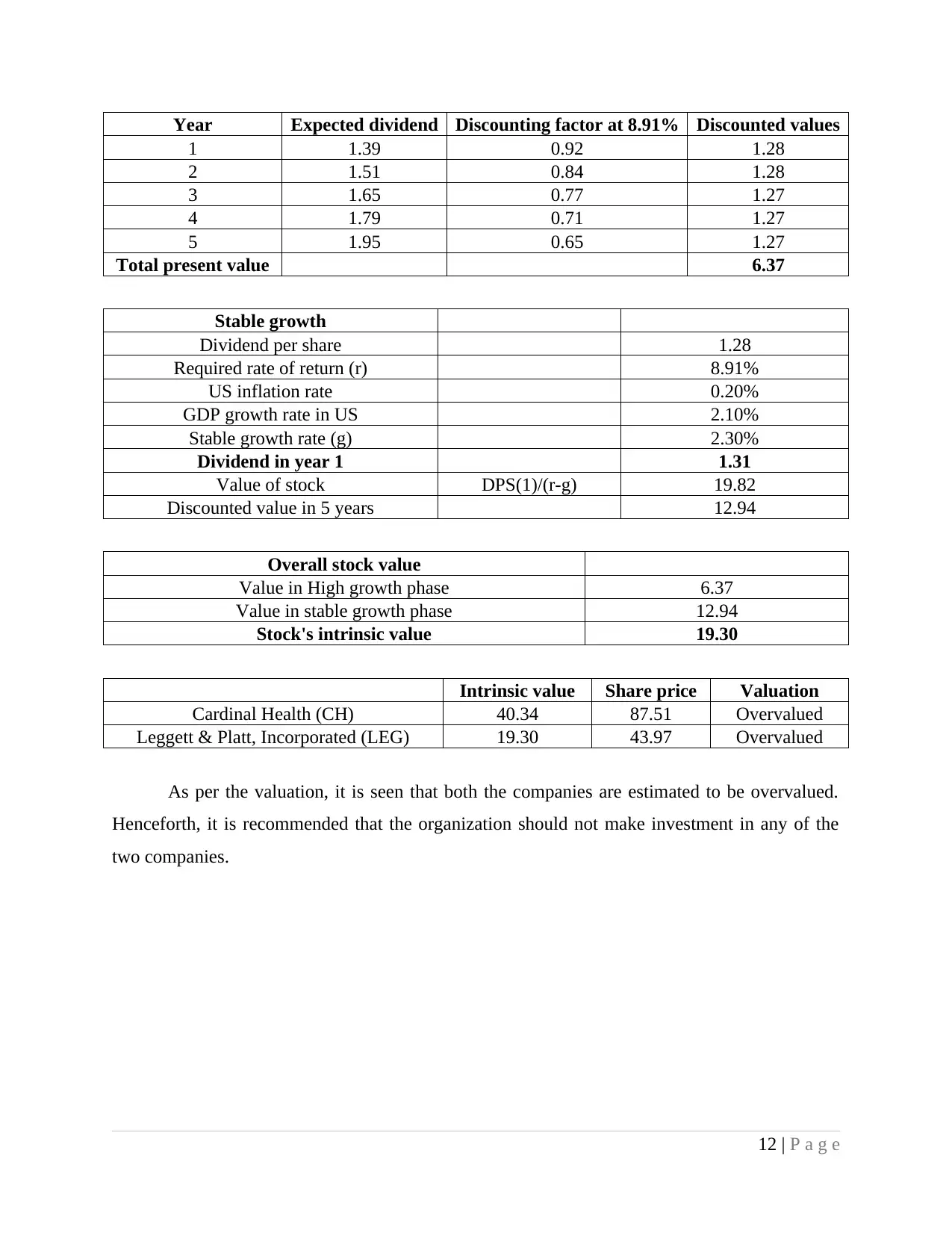

This financial management report provides a detailed analysis of bond and stock valuations, along with portfolio analysis, based on coursework submitted to the University of Greenwich. The report begins by valuing a bond, calculating its fair price, Macaulay and modified duration, convexity, and annual percentage change in price. It then moves on to stock valuation, applying the dividend discount model to two companies, Cardinal Health and Leggett & Platt, Incorporated, to determine their intrinsic values and provide buy/sell recommendations. The report also includes the collection of monthly share prices for 20 companies and calculates the expected return. The report uses appropriate financial techniques to guide investors in making informed decisions. The report provides a comprehensive overview of financial analysis techniques.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.