Management Accounting Assignment - UGB222 Analysis & Solutions

VerifiedAdded on 2023/01/05

|14

|3064

|89

Homework Assignment

AI Summary

This document presents a comprehensive solution to a management accounting assignment, addressing key concepts and practical applications. It begins with a schedule of the cost of goods manufactured and an accompanying income statement, followed by a differential analysis comparing absorption and marginal costing methods, including the calculation of cost per unit and income statements for both. The assignment then delves into variance analysis, demonstrating material, labor, and overhead variances. Finally, it concludes with calculations of contribution margin and break-even point, along with detailed explanations of the underlying principles and calculations. The assignment covers the key areas of managerial accounting, including cost accounting, variance analysis, and break-even analysis, providing a solid foundation for understanding financial and non-financial information within a business context.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Question 2...................................................................................................................................3

Question 3...................................................................................................................................5

Question 4...................................................................................................................................7

Question 6.................................................................................................................................10

Conclusion.....................................................................................................................................12

References .....................................................................................................................................13

2

Introduction......................................................................................................................................3

Main Body.......................................................................................................................................3

Question 2...................................................................................................................................3

Question 3...................................................................................................................................5

Question 4...................................................................................................................................7

Question 6.................................................................................................................................10

Conclusion.....................................................................................................................................12

References .....................................................................................................................................13

2

Introduction

Management accounting is a form of accounting which focuses on both financial and non

financial information in a business (Hirsch, Seubert and Sohn, 2015). In the project undertaken,

it was specified that four questions out of six have to be attempted which presents different forms

of financial part of managerial accounting. At first, a schedule of the cost of goods manufactured

is presented and accompanying it is an income statement based on that cost of goods

manufactured. Next part presents a differential analysis in the two forms of costing i.e.

absorption costing and marginal costing. Calculation of cost per unit and income statement has

been prepared for both the forms. Next is the calculation of variance analysis. Demonstration of

material, labour and overhead variances has been presented below. In the final part, calculations

of contribution, break even point have been demonstrated.

Main Body

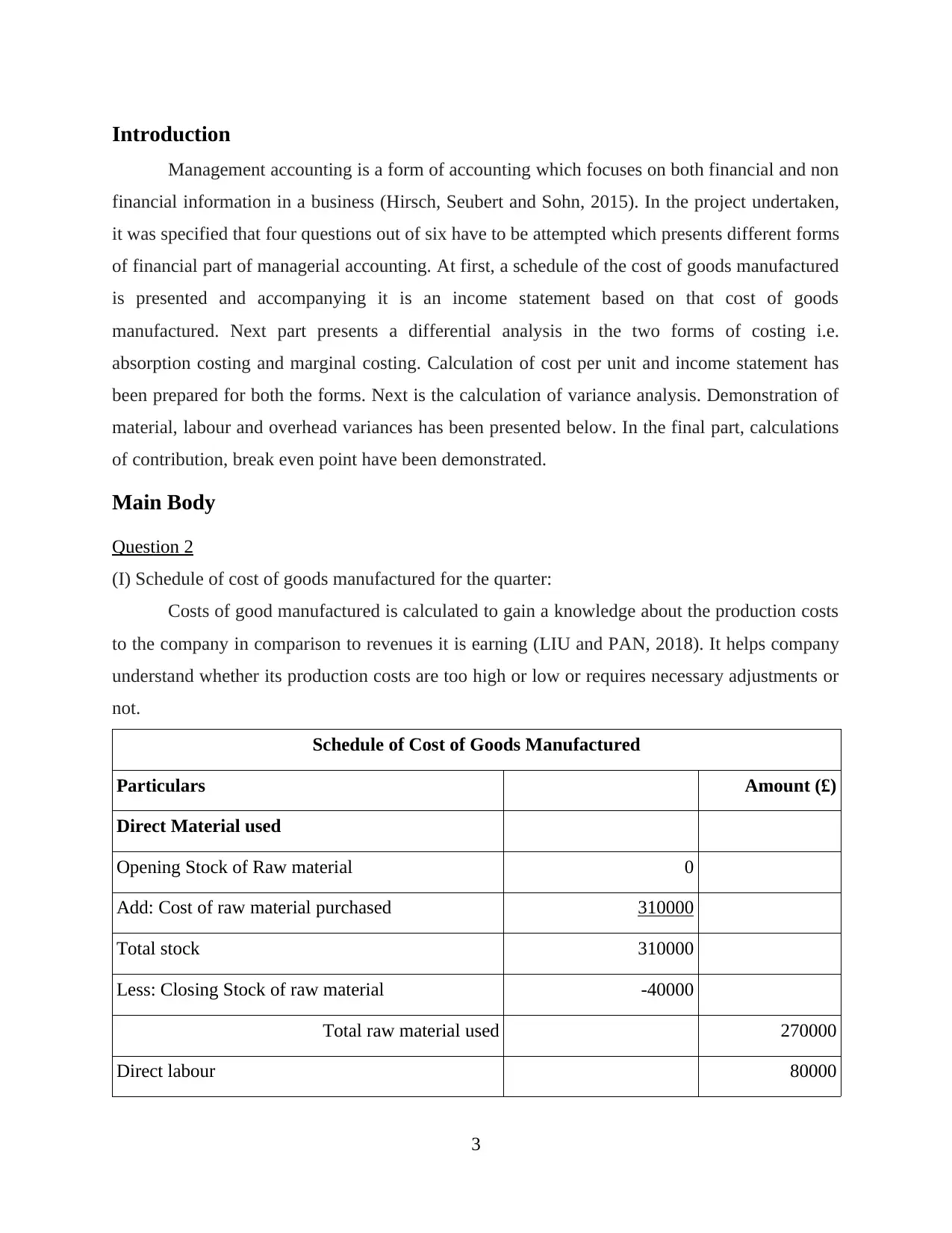

Question 2

(I) Schedule of cost of goods manufactured for the quarter:

Costs of good manufactured is calculated to gain a knowledge about the production costs

to the company in comparison to revenues it is earning (LIU and PAN, 2018). It helps company

understand whether its production costs are too high or low or requires necessary adjustments or

not.

Schedule of Cost of Goods Manufactured

Particulars Amount (£)

Direct Material used

Opening Stock of Raw material 0

Add: Cost of raw material purchased 310000

Total stock 310000

Less: Closing Stock of raw material -40000

Total raw material used 270000

Direct labour 80000

3

Management accounting is a form of accounting which focuses on both financial and non

financial information in a business (Hirsch, Seubert and Sohn, 2015). In the project undertaken,

it was specified that four questions out of six have to be attempted which presents different forms

of financial part of managerial accounting. At first, a schedule of the cost of goods manufactured

is presented and accompanying it is an income statement based on that cost of goods

manufactured. Next part presents a differential analysis in the two forms of costing i.e.

absorption costing and marginal costing. Calculation of cost per unit and income statement has

been prepared for both the forms. Next is the calculation of variance analysis. Demonstration of

material, labour and overhead variances has been presented below. In the final part, calculations

of contribution, break even point have been demonstrated.

Main Body

Question 2

(I) Schedule of cost of goods manufactured for the quarter:

Costs of good manufactured is calculated to gain a knowledge about the production costs

to the company in comparison to revenues it is earning (LIU and PAN, 2018). It helps company

understand whether its production costs are too high or low or requires necessary adjustments or

not.

Schedule of Cost of Goods Manufactured

Particulars Amount (£)

Direct Material used

Opening Stock of Raw material 0

Add: Cost of raw material purchased 310000

Total stock 310000

Less: Closing Stock of raw material -40000

Total raw material used 270000

Direct labour 80000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

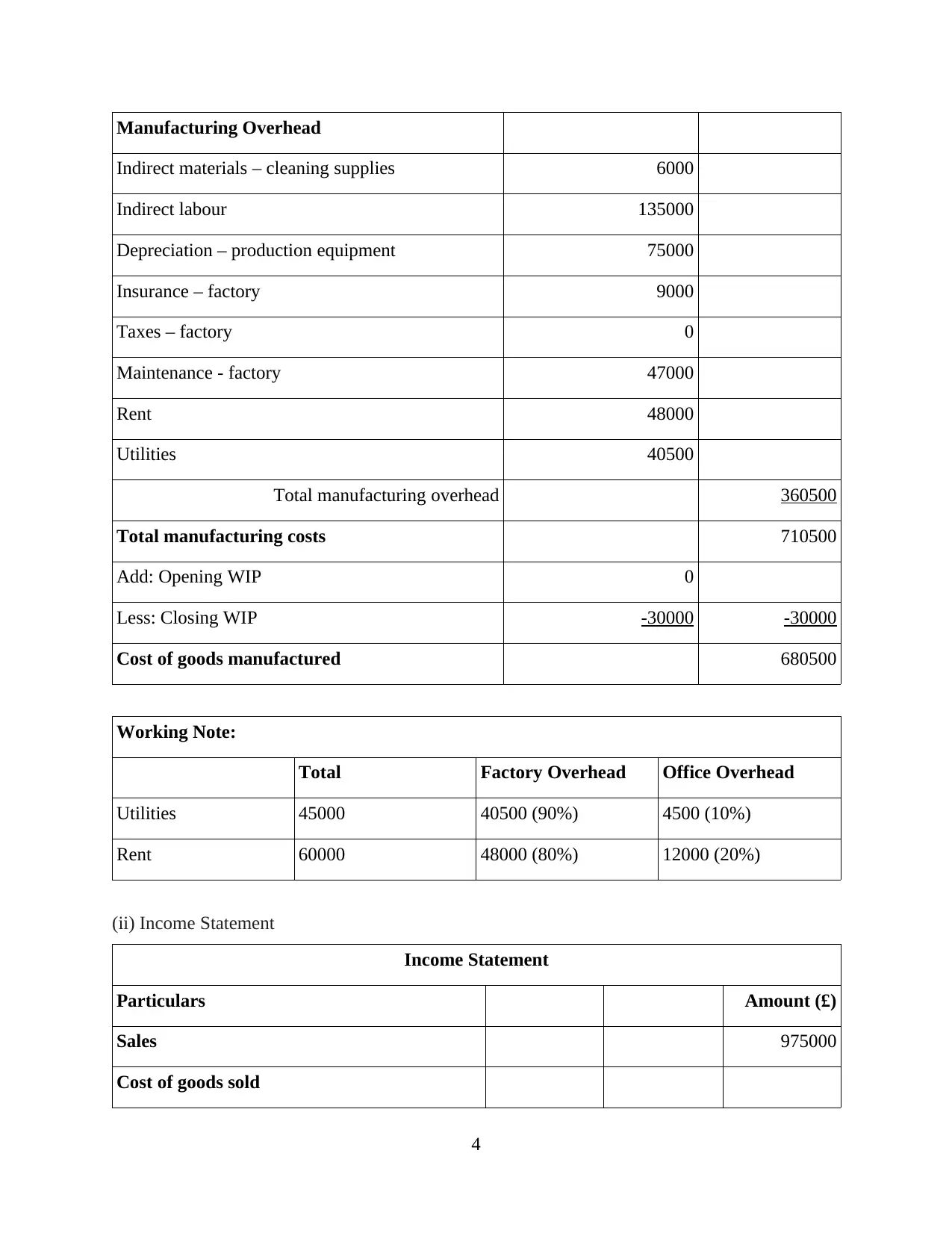

Manufacturing Overhead

Indirect materials – cleaning supplies 6000

Indirect labour 135000

Depreciation – production equipment 75000

Insurance – factory 9000

Taxes – factory 0

Maintenance - factory 47000

Rent 48000

Utilities 40500

Total manufacturing overhead 360500

Total manufacturing costs 710500

Add: Opening WIP 0

Less: Closing WIP -30000 -30000

Cost of goods manufactured 680500

Working Note:

Total Factory Overhead Office Overhead

Utilities 45000 40500 (90%) 4500 (10%)

Rent 60000 48000 (80%) 12000 (20%)

(ii) Income Statement

Income Statement

Particulars Amount (£)

Sales 975000

Cost of goods sold

4

Indirect materials – cleaning supplies 6000

Indirect labour 135000

Depreciation – production equipment 75000

Insurance – factory 9000

Taxes – factory 0

Maintenance - factory 47000

Rent 48000

Utilities 40500

Total manufacturing overhead 360500

Total manufacturing costs 710500

Add: Opening WIP 0

Less: Closing WIP -30000 -30000

Cost of goods manufactured 680500

Working Note:

Total Factory Overhead Office Overhead

Utilities 45000 40500 (90%) 4500 (10%)

Rent 60000 48000 (80%) 12000 (20%)

(ii) Income Statement

Income Statement

Particulars Amount (£)

Sales 975000

Cost of goods sold

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

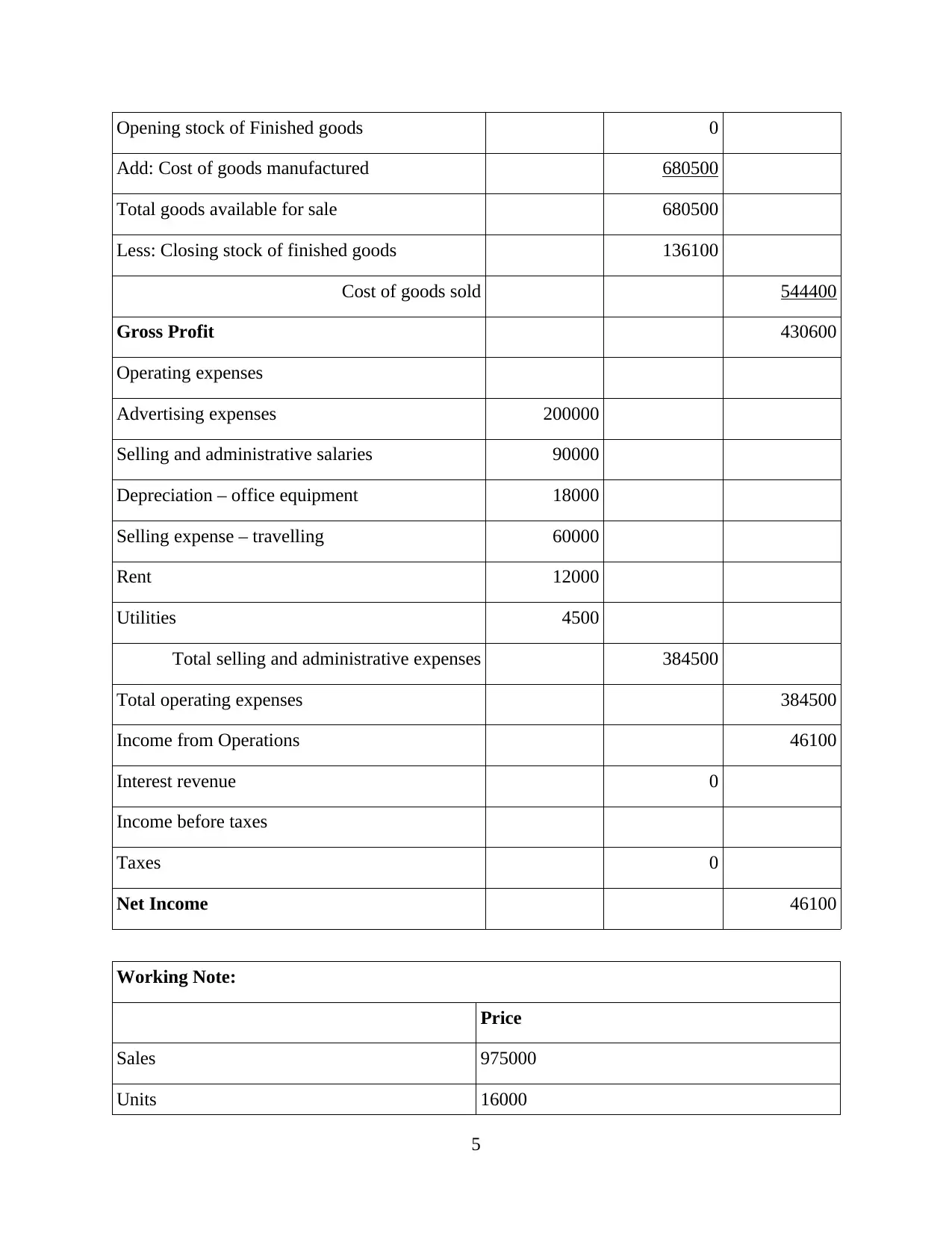

Opening stock of Finished goods 0

Add: Cost of goods manufactured 680500

Total goods available for sale 680500

Less: Closing stock of finished goods 136100

Cost of goods sold 544400

Gross Profit 430600

Operating expenses

Advertising expenses 200000

Selling and administrative salaries 90000

Depreciation – office equipment 18000

Selling expense – travelling 60000

Rent 12000

Utilities 4500

Total selling and administrative expenses 384500

Total operating expenses 384500

Income from Operations 46100

Interest revenue 0

Income before taxes

Taxes 0

Net Income 46100

Working Note:

Price

Sales 975000

Units 16000

5

Add: Cost of goods manufactured 680500

Total goods available for sale 680500

Less: Closing stock of finished goods 136100

Cost of goods sold 544400

Gross Profit 430600

Operating expenses

Advertising expenses 200000

Selling and administrative salaries 90000

Depreciation – office equipment 18000

Selling expense – travelling 60000

Rent 12000

Utilities 4500

Total selling and administrative expenses 384500

Total operating expenses 384500

Income from Operations 46100

Interest revenue 0

Income before taxes

Taxes 0

Net Income 46100

Working Note:

Price

Sales 975000

Units 16000

5

Selling Price per unit 60.94

Cost of goods manufactured 680500

Units 20000

Cost Price per unit 34.03

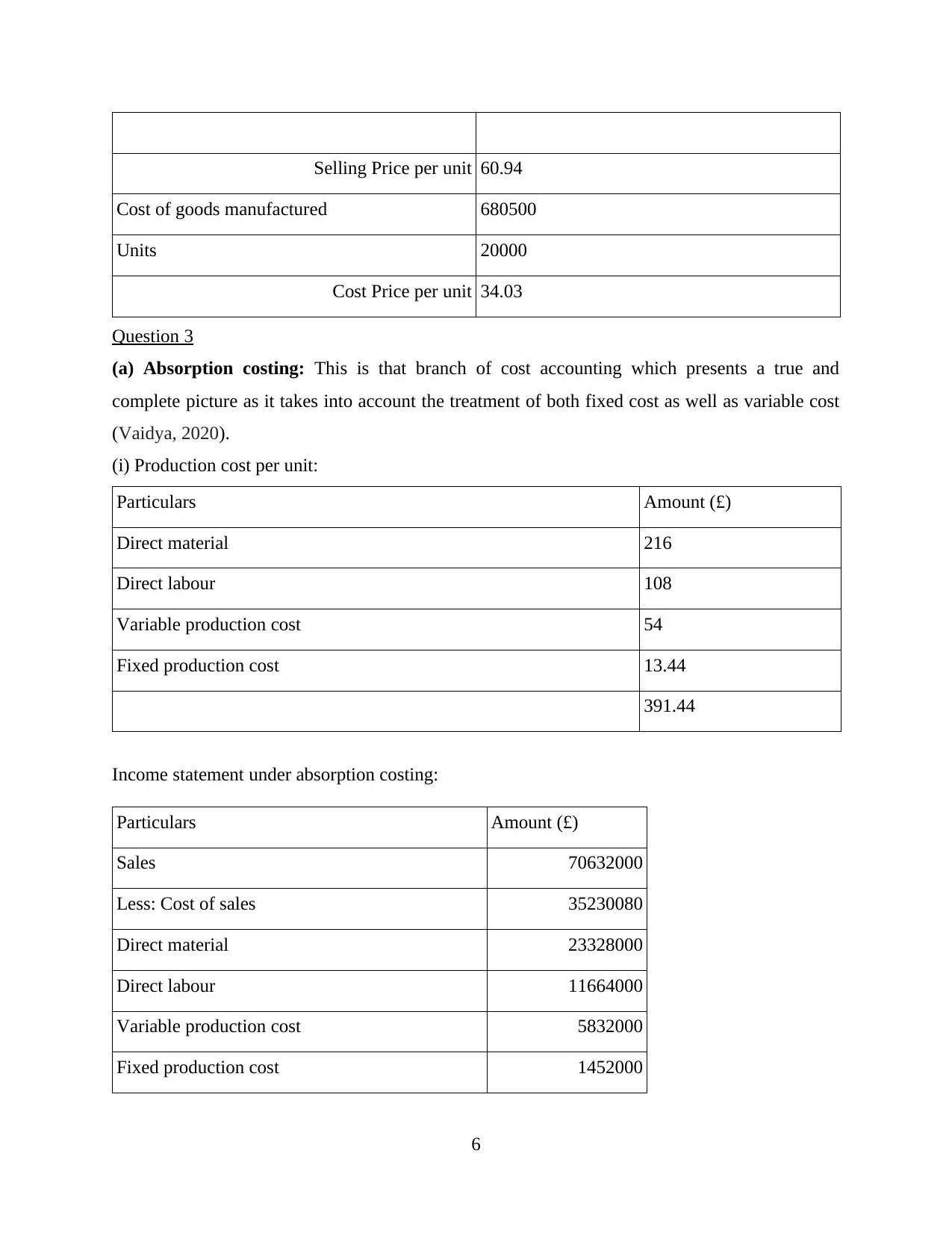

Question 3

(a) Absorption costing: This is that branch of cost accounting which presents a true and

complete picture as it takes into account the treatment of both fixed cost as well as variable cost

(Vaidya, 2020).

(i) Production cost per unit:

Particulars Amount (£)

Direct material 216

Direct labour 108

Variable production cost 54

Fixed production cost 13.44

391.44

Income statement under absorption costing:

Particulars Amount (£)

Sales 70632000

Less: Cost of sales 35230080

Direct material 23328000

Direct labour 11664000

Variable production cost 5832000

Fixed production cost 1452000

6

Cost of goods manufactured 680500

Units 20000

Cost Price per unit 34.03

Question 3

(a) Absorption costing: This is that branch of cost accounting which presents a true and

complete picture as it takes into account the treatment of both fixed cost as well as variable cost

(Vaidya, 2020).

(i) Production cost per unit:

Particulars Amount (£)

Direct material 216

Direct labour 108

Variable production cost 54

Fixed production cost 13.44

391.44

Income statement under absorption costing:

Particulars Amount (£)

Sales 70632000

Less: Cost of sales 35230080

Direct material 23328000

Direct labour 11664000

Variable production cost 5832000

Fixed production cost 1452000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

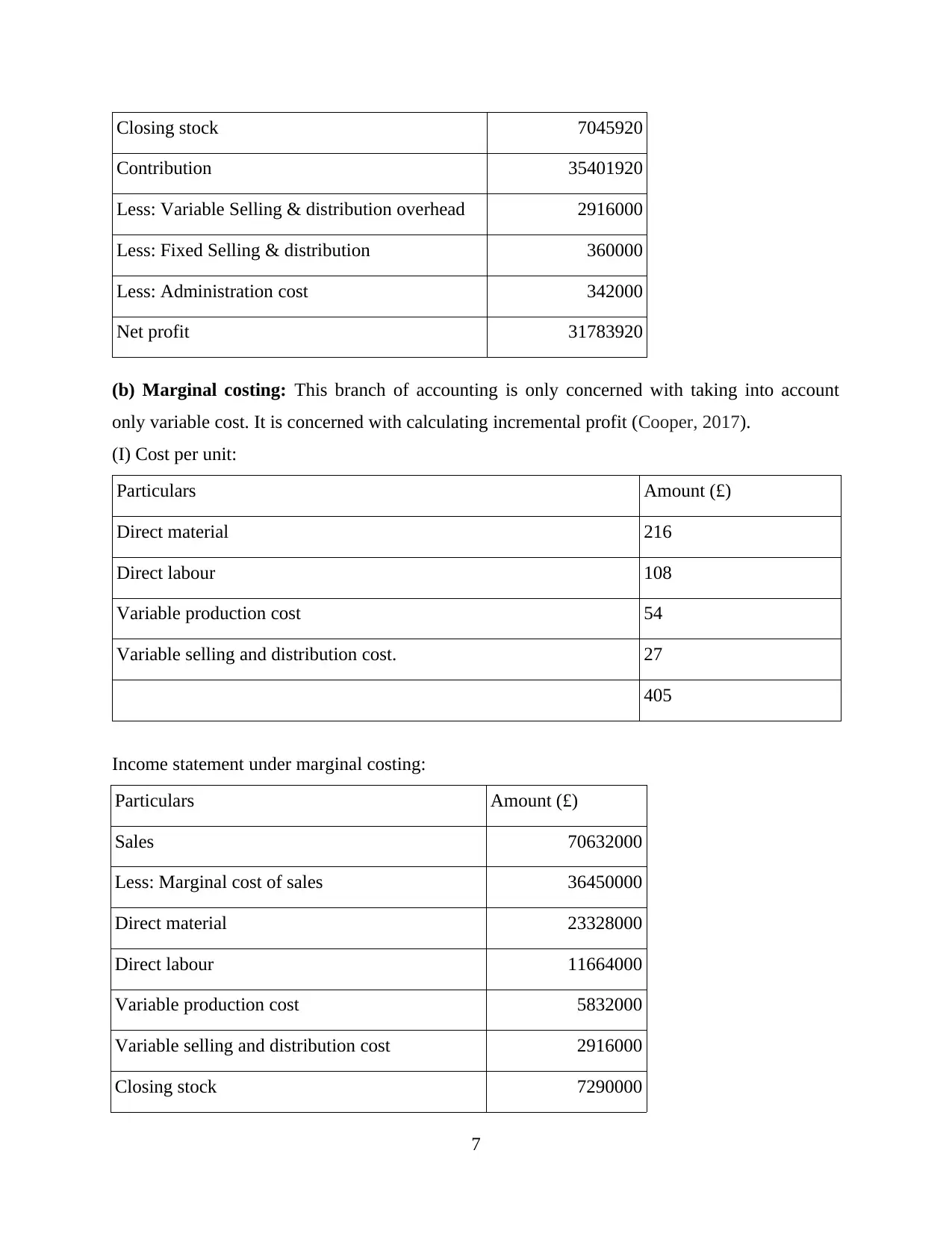

Closing stock 7045920

Contribution 35401920

Less: Variable Selling & distribution overhead 2916000

Less: Fixed Selling & distribution 360000

Less: Administration cost 342000

Net profit 31783920

(b) Marginal costing: This branch of accounting is only concerned with taking into account

only variable cost. It is concerned with calculating incremental profit (Cooper, 2017).

(I) Cost per unit:

Particulars Amount (£)

Direct material 216

Direct labour 108

Variable production cost 54

Variable selling and distribution cost. 27

405

Income statement under marginal costing:

Particulars Amount (£)

Sales 70632000

Less: Marginal cost of sales 36450000

Direct material 23328000

Direct labour 11664000

Variable production cost 5832000

Variable selling and distribution cost 2916000

Closing stock 7290000

7

Contribution 35401920

Less: Variable Selling & distribution overhead 2916000

Less: Fixed Selling & distribution 360000

Less: Administration cost 342000

Net profit 31783920

(b) Marginal costing: This branch of accounting is only concerned with taking into account

only variable cost. It is concerned with calculating incremental profit (Cooper, 2017).

(I) Cost per unit:

Particulars Amount (£)

Direct material 216

Direct labour 108

Variable production cost 54

Variable selling and distribution cost. 27

405

Income statement under marginal costing:

Particulars Amount (£)

Sales 70632000

Less: Marginal cost of sales 36450000

Direct material 23328000

Direct labour 11664000

Variable production cost 5832000

Variable selling and distribution cost 2916000

Closing stock 7290000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

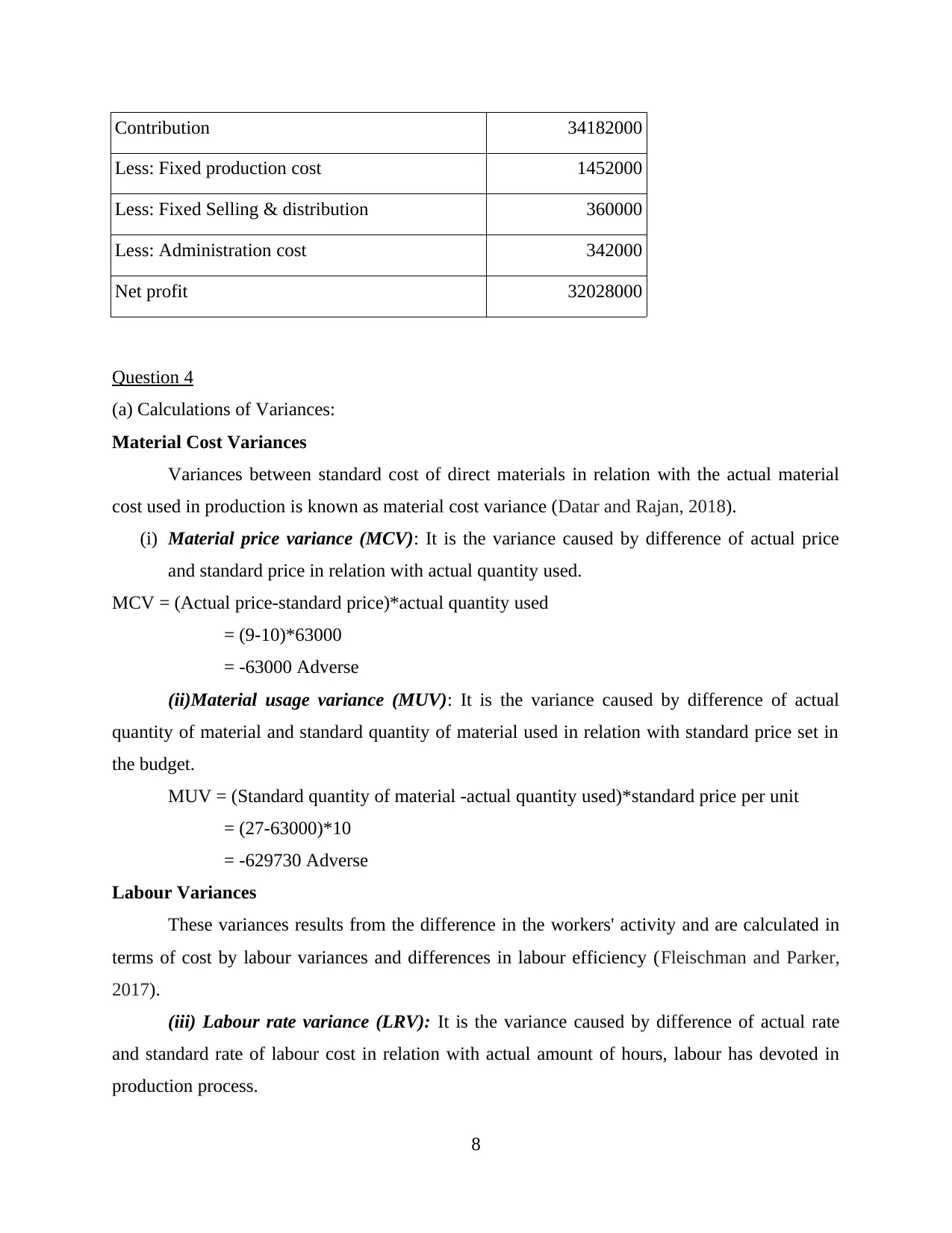

Contribution 34182000

Less: Fixed production cost 1452000

Less: Fixed Selling & distribution 360000

Less: Administration cost 342000

Net profit 32028000

Question 4

(a) Calculations of Variances:

Material Cost Variances

Variances between standard cost of direct materials in relation with the actual material

cost used in production is known as material cost variance (Datar and Rajan, 2018).

(i) Material price variance (MCV): It is the variance caused by difference of actual price

and standard price in relation with actual quantity used.

MCV = (Actual price-standard price)*actual quantity used

= (9-10)*63000

= -63000 Adverse

(ii)Material usage variance (MUV): It is the variance caused by difference of actual

quantity of material and standard quantity of material used in relation with standard price set in

the budget.

MUV = (Standard quantity of material -actual quantity used)*standard price per unit

= (27-63000)*10

= -629730 Adverse

Labour Variances

These variances results from the difference in the workers' activity and are calculated in

terms of cost by labour variances and differences in labour efficiency (Fleischman and Parker,

2017).

(iii) Labour rate variance (LRV): It is the variance caused by difference of actual rate

and standard rate of labour cost in relation with actual amount of hours, labour has devoted in

production process.

8

Less: Fixed production cost 1452000

Less: Fixed Selling & distribution 360000

Less: Administration cost 342000

Net profit 32028000

Question 4

(a) Calculations of Variances:

Material Cost Variances

Variances between standard cost of direct materials in relation with the actual material

cost used in production is known as material cost variance (Datar and Rajan, 2018).

(i) Material price variance (MCV): It is the variance caused by difference of actual price

and standard price in relation with actual quantity used.

MCV = (Actual price-standard price)*actual quantity used

= (9-10)*63000

= -63000 Adverse

(ii)Material usage variance (MUV): It is the variance caused by difference of actual

quantity of material and standard quantity of material used in relation with standard price set in

the budget.

MUV = (Standard quantity of material -actual quantity used)*standard price per unit

= (27-63000)*10

= -629730 Adverse

Labour Variances

These variances results from the difference in the workers' activity and are calculated in

terms of cost by labour variances and differences in labour efficiency (Fleischman and Parker,

2017).

(iii) Labour rate variance (LRV): It is the variance caused by difference of actual rate

and standard rate of labour cost in relation with actual amount of hours, labour has devoted in

production process.

8

LRV = (Actual rate-standard rate)*actual hour worked

= (7-9.6)*45000

= -431993 Adverse

(iv) Labour efficiency variance (LEV): It is the variance caused by difference of actual

hours and standard hours that labour has worked in the company in relation with budgetary

standard set by the company (Turvey, 2017).

LEV = (Actual hours-standard hour)*standard rate

= (45000-20)*7

=44980*7

= 314860 Favourable

Variable Overhead Variance

These variances are the result of difference between the actual variable overhead and

standard variable overhead which derive their base from the budgets set by the company

management (Jiambalvo, 2019).

(v) Variable overhead rate (VOR): It is the variance caused by difference of actual hours

and standard hours that has arise in the performance of the company jobs in relation with

budgetary standard set by the company.

VOR = (Actual hours-standard hours)*standard rate

= (31050-15)*5

= 31035*5

= 155175 Favourable

(vi) Variable overhead efficiency:

VOE = (Actual hours* standard rate) – (Standard hours*standard rate)

= (31050*5)-(15*5)

= 155250-75

=155175 Favourable

(b) Causes of variance:

(I) Material usage variance: Inferior material – Whenever businesses uses inferior quality of material than what was

determined while setting standards, leads to variances. Or, may be there is loss due to

9

= (7-9.6)*45000

= -431993 Adverse

(iv) Labour efficiency variance (LEV): It is the variance caused by difference of actual

hours and standard hours that labour has worked in the company in relation with budgetary

standard set by the company (Turvey, 2017).

LEV = (Actual hours-standard hour)*standard rate

= (45000-20)*7

=44980*7

= 314860 Favourable

Variable Overhead Variance

These variances are the result of difference between the actual variable overhead and

standard variable overhead which derive their base from the budgets set by the company

management (Jiambalvo, 2019).

(v) Variable overhead rate (VOR): It is the variance caused by difference of actual hours

and standard hours that has arise in the performance of the company jobs in relation with

budgetary standard set by the company.

VOR = (Actual hours-standard hours)*standard rate

= (31050-15)*5

= 31035*5

= 155175 Favourable

(vi) Variable overhead efficiency:

VOE = (Actual hours* standard rate) – (Standard hours*standard rate)

= (31050*5)-(15*5)

= 155250-75

=155175 Favourable

(b) Causes of variance:

(I) Material usage variance: Inferior material – Whenever businesses uses inferior quality of material than what was

determined while setting standards, leads to variances. Or, may be there is loss due to

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

pilferage which has gone unnoticed and added into usage of material or more material

was need to be procured, which get reflected as variances. Upfront standard – When standards set are too high to be followed in the actual terms, it

results in variances between actual and standards (Cooper, 2017). Or, may be during

production process, proper induction of material was not adopted, which resulted in

variances between standards set and the materials left post usage. Workers and equipments – The plants and machinery might not be in proper condition as

defined in standards. Therefore, more material could be used. Another reason may be

untrained workers. When the workers are not trained to use a material or equipment, it

results in wastage, which causes variances between standards and actual usage of

material. Or, workers might not use materials carefully, it will also result in wastage.

Therefore, carelessness and inefficiency of workers can also be said a reason for

variances.

Different material mix – One more reason of variance could be the use of different

material mix then what was determined in standard mix or, there could be changes in

product design, which could lead to different product mix. At last, there can be

accounting mistakes such as either the entries related to material were not made properly

or transferred to various jobs, etc.

(II) Labour efficiency variances: Labour skills – Skills of the labour can be one of the reasons for variance (Mitra, 2016).

For example, Labours are highly skilled for the job, then they will not consider the work

of their level and will not co-operate with others. This might result in differences in

efficiency standards and the actual job performance. Training – Suppose while setting the standards, management realises that workers need

training to operate some machinery or other equipment. They set up training process for

them but does not take into account the improvements caused by training. As a result,

employee performance will be improved in the actual performance, and will reflect as

variance. Raw material – There is change in raw material or the product mix or product design,

which is either not easy for workers to adopt or so facilitating that it results in a

10

was need to be procured, which get reflected as variances. Upfront standard – When standards set are too high to be followed in the actual terms, it

results in variances between actual and standards (Cooper, 2017). Or, may be during

production process, proper induction of material was not adopted, which resulted in

variances between standards set and the materials left post usage. Workers and equipments – The plants and machinery might not be in proper condition as

defined in standards. Therefore, more material could be used. Another reason may be

untrained workers. When the workers are not trained to use a material or equipment, it

results in wastage, which causes variances between standards and actual usage of

material. Or, workers might not use materials carefully, it will also result in wastage.

Therefore, carelessness and inefficiency of workers can also be said a reason for

variances.

Different material mix – One more reason of variance could be the use of different

material mix then what was determined in standard mix or, there could be changes in

product design, which could lead to different product mix. At last, there can be

accounting mistakes such as either the entries related to material were not made properly

or transferred to various jobs, etc.

(II) Labour efficiency variances: Labour skills – Skills of the labour can be one of the reasons for variance (Mitra, 2016).

For example, Labours are highly skilled for the job, then they will not consider the work

of their level and will not co-operate with others. This might result in differences in

efficiency standards and the actual job performance. Training – Suppose while setting the standards, management realises that workers need

training to operate some machinery or other equipment. They set up training process for

them but does not take into account the improvements caused by training. As a result,

employee performance will be improved in the actual performance, and will reflect as

variance. Raw material – There is change in raw material or the product mix or product design,

which is either not easy for workers to adopt or so facilitating that it results in a

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

considerable improvement in their performance. Both the cases, will lead to generation of

a deviation or variances in the efficiency of labour.

Time lag – There can be a difference or lag in the time when the budget or the standards

were set for the measuring the efficiency and the actual performance by the workers. This

can also lead to variance in estimated labour efficiency and the real performance. Also,

there might be a chance that due to some changes in the process or other thing, employee

morale is down, which will increase their idle time and reduce their efficiency.

(C) Determination of appropriate variance

Variance analysis refers to the process of identifying the lags or difference between

budgeted targets and actual performance. It form the basis of control functions by managers. It

helps them identify the reasons for deviations in the performance from the standards set by the

budgets (Warren, Jonick and Schneider, 2020). A company prepares multiple budgets which

form the basis of the performance management in different aspect under different criteria. It uses

the budgets and analysis of performance as per requirement. For example, a company is

performing its employee performance management. Then, it will desire to check their efficiency

and productivity level. So, it will make use of labour efficiency variance. If it happens to be

performing inventory management. It will check the amount of orders made for raw materials by

company, their processing, storage, handling, usage, etc. In such conditions, it will apply

variances like material price variance and material usage variances. If the company is performing

cost management, it will check all expenses and overheads it is incurring and its application.

Then, it will check variances like overhead variance – variable overhead variance or fixed

overhead variances. To know about the differences in sales targets and the actual sales being

made, company will use sales volume variance, etc.

Question 6

Contribution margin: It is used to determine a product's price by taking into account all

associated variable costs while total contribution margin of an organisation comprises of all

earning available to it to pay for fixed costs so that it can generate a true picture of profit

(Hartley, 2017).

(a) Contribution: Sales-variable expense

= 3000000-(300000+1387500+150000+127500+60000)

= 3000000-2025000

11

a deviation or variances in the efficiency of labour.

Time lag – There can be a difference or lag in the time when the budget or the standards

were set for the measuring the efficiency and the actual performance by the workers. This

can also lead to variance in estimated labour efficiency and the real performance. Also,

there might be a chance that due to some changes in the process or other thing, employee

morale is down, which will increase their idle time and reduce their efficiency.

(C) Determination of appropriate variance

Variance analysis refers to the process of identifying the lags or difference between

budgeted targets and actual performance. It form the basis of control functions by managers. It

helps them identify the reasons for deviations in the performance from the standards set by the

budgets (Warren, Jonick and Schneider, 2020). A company prepares multiple budgets which

form the basis of the performance management in different aspect under different criteria. It uses

the budgets and analysis of performance as per requirement. For example, a company is

performing its employee performance management. Then, it will desire to check their efficiency

and productivity level. So, it will make use of labour efficiency variance. If it happens to be

performing inventory management. It will check the amount of orders made for raw materials by

company, their processing, storage, handling, usage, etc. In such conditions, it will apply

variances like material price variance and material usage variances. If the company is performing

cost management, it will check all expenses and overheads it is incurring and its application.

Then, it will check variances like overhead variance – variable overhead variance or fixed

overhead variances. To know about the differences in sales targets and the actual sales being

made, company will use sales volume variance, etc.

Question 6

Contribution margin: It is used to determine a product's price by taking into account all

associated variable costs while total contribution margin of an organisation comprises of all

earning available to it to pay for fixed costs so that it can generate a true picture of profit

(Hartley, 2017).

(a) Contribution: Sales-variable expense

= 3000000-(300000+1387500+150000+127500+60000)

= 3000000-2025000

11

= 975000

or 6.5 per unit (975000/150000)

Break Even point – It is that point of production in accounting where, cost of production

at a level is equal to revenue of that product, being produced at that level (Massy, 2016).

(b) BEP in units: Fixed cost/ contribution per unit

= (525000+240000+90000)/6.5

= 855000/6.5

= 131538 units

(c) Number of units to be sold: Fixed cost+desired profit/contribution per unit

= 855000+180000/6.5

= 159230 Units

(d) Current sales price: 20

reducing by 15%

New sales price: 20-3

= 17

Variable cost per unit: 2025000/150000

= 13.5

Contribution per unit: 17-13.5

= 3.5 per unit

BEP in units: Fixed cost/contribution per unit

= 855000/3.5

= 244285 Units

(e) Old variable cost per unit: 13.5

Change by 2.5 so new variable cost per unit: 16

Selling price per unit: 20

Contribution per unit: 20-16

= 4

12

or 6.5 per unit (975000/150000)

Break Even point – It is that point of production in accounting where, cost of production

at a level is equal to revenue of that product, being produced at that level (Massy, 2016).

(b) BEP in units: Fixed cost/ contribution per unit

= (525000+240000+90000)/6.5

= 855000/6.5

= 131538 units

(c) Number of units to be sold: Fixed cost+desired profit/contribution per unit

= 855000+180000/6.5

= 159230 Units

(d) Current sales price: 20

reducing by 15%

New sales price: 20-3

= 17

Variable cost per unit: 2025000/150000

= 13.5

Contribution per unit: 17-13.5

= 3.5 per unit

BEP in units: Fixed cost/contribution per unit

= 855000/3.5

= 244285 Units

(e) Old variable cost per unit: 13.5

Change by 2.5 so new variable cost per unit: 16

Selling price per unit: 20

Contribution per unit: 20-16

= 4

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.