University Portfolio Management and Investment Report

VerifiedAdded on 2021/04/21

|7

|656

|111

Report

AI Summary

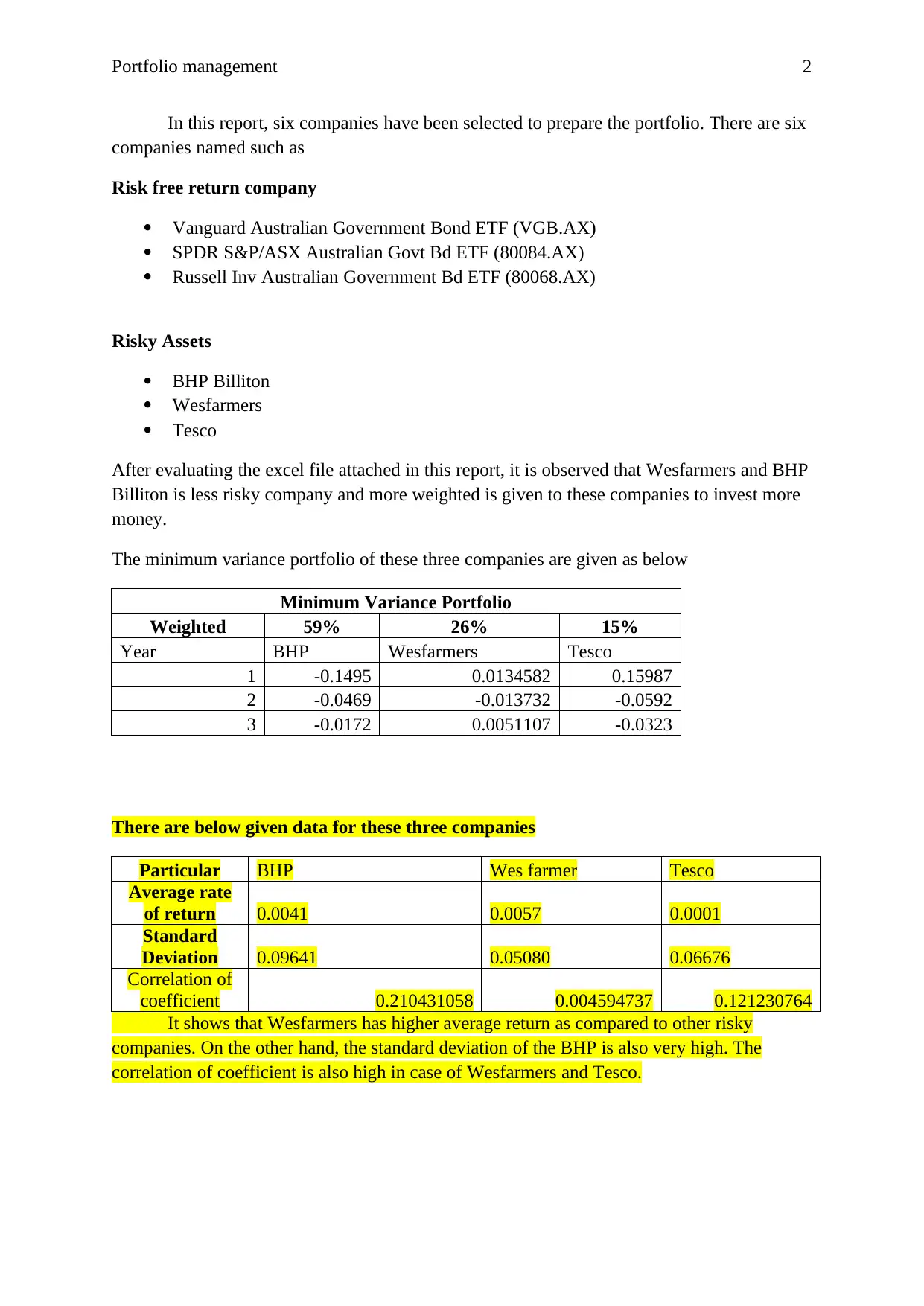

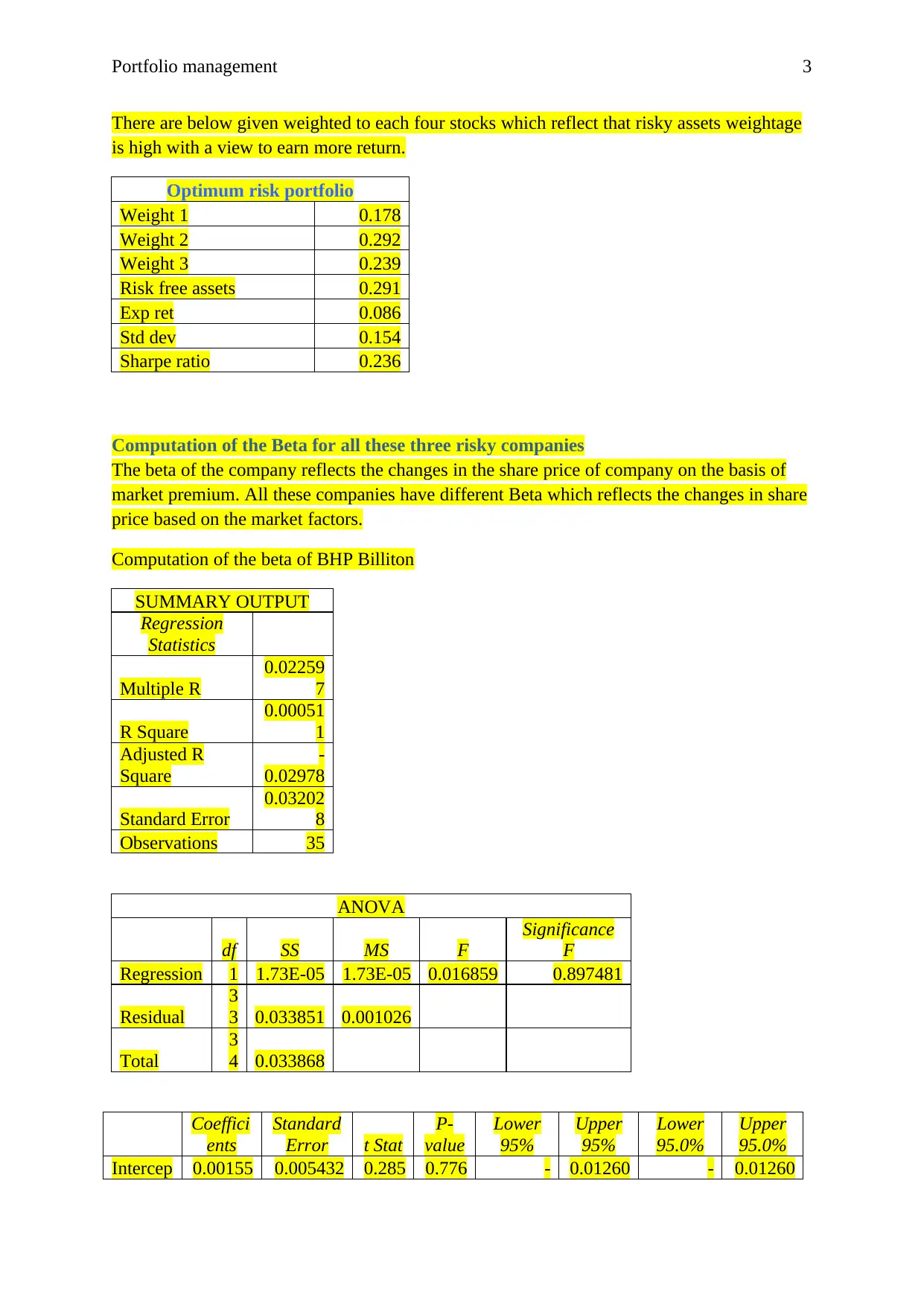

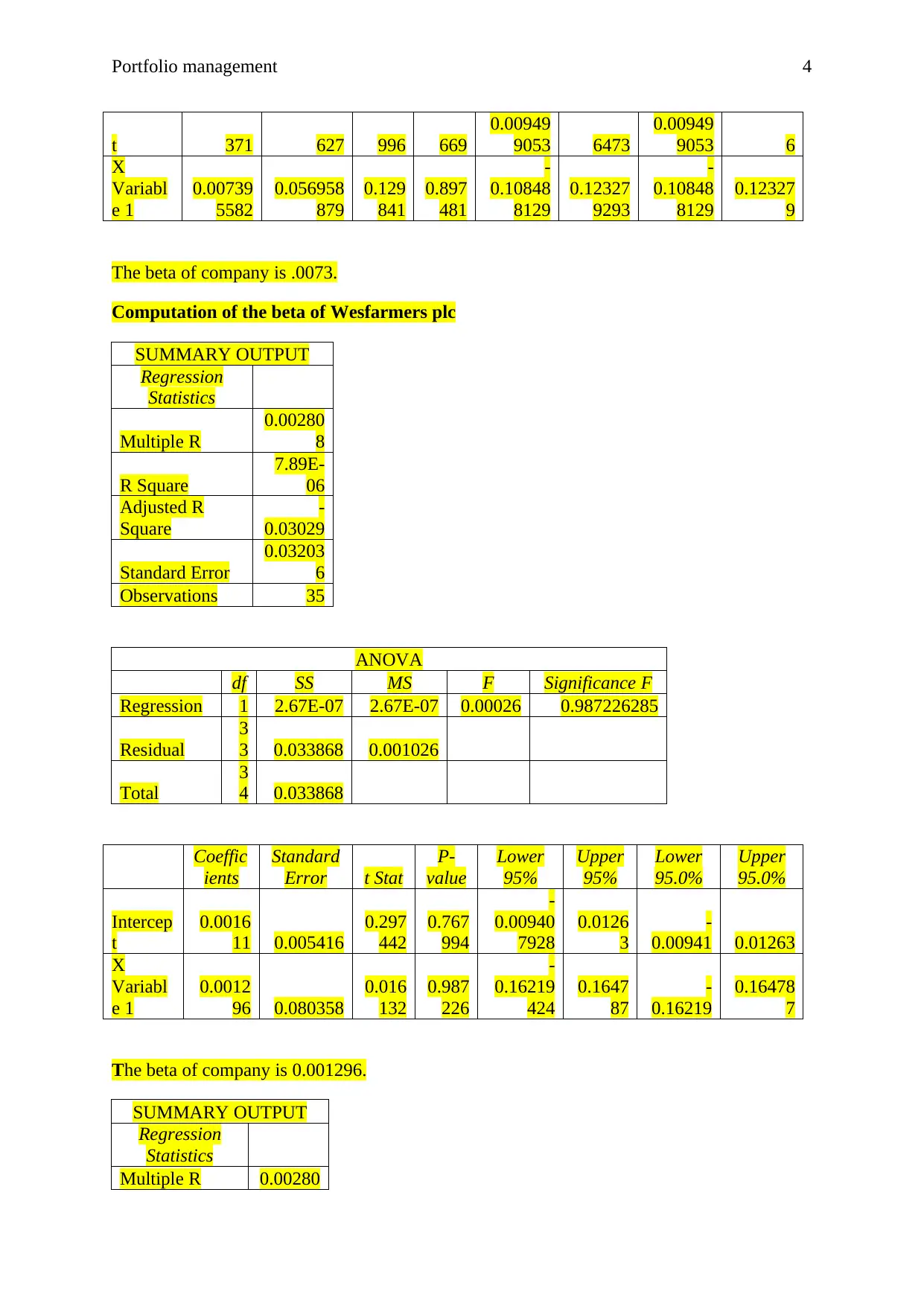

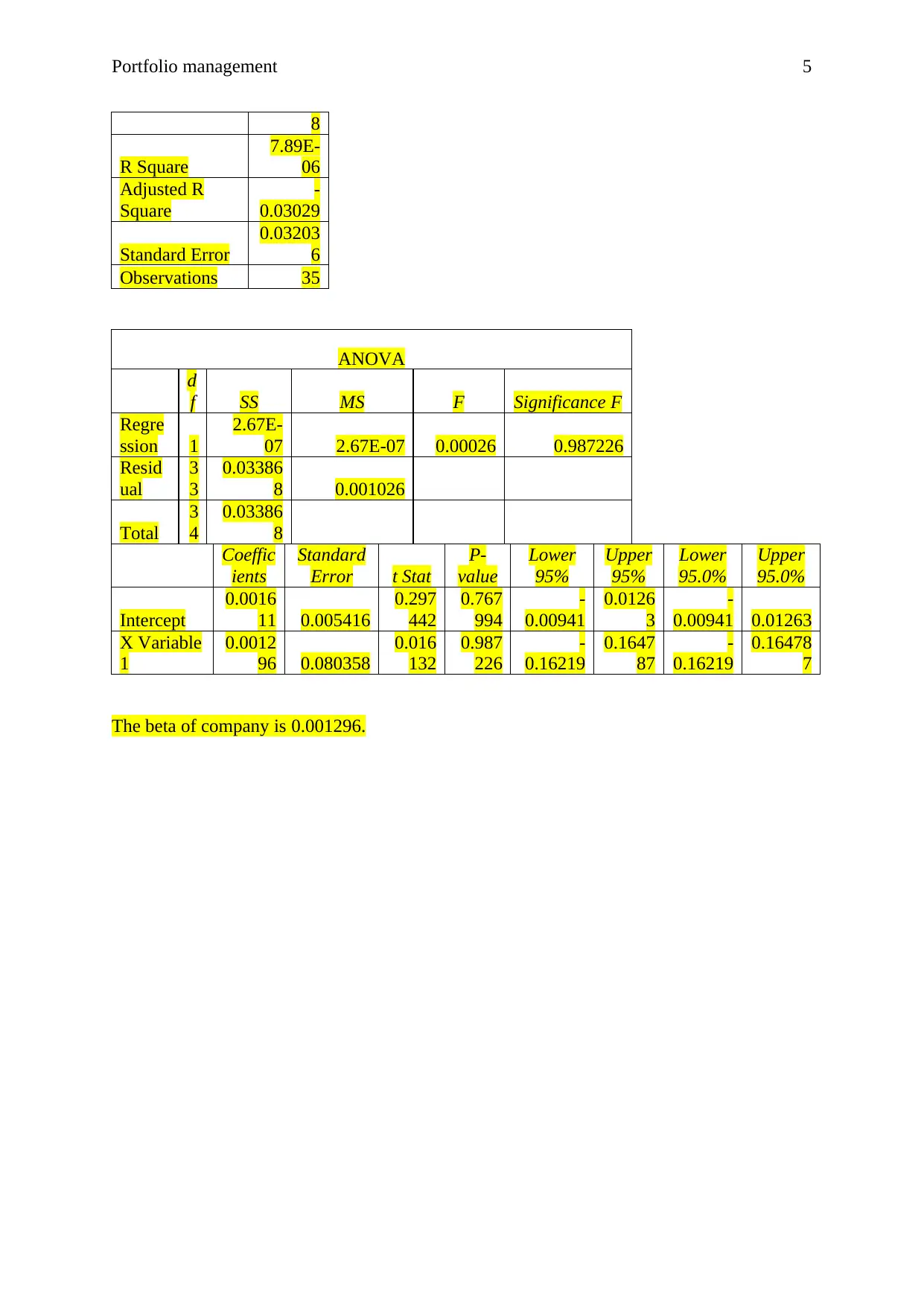

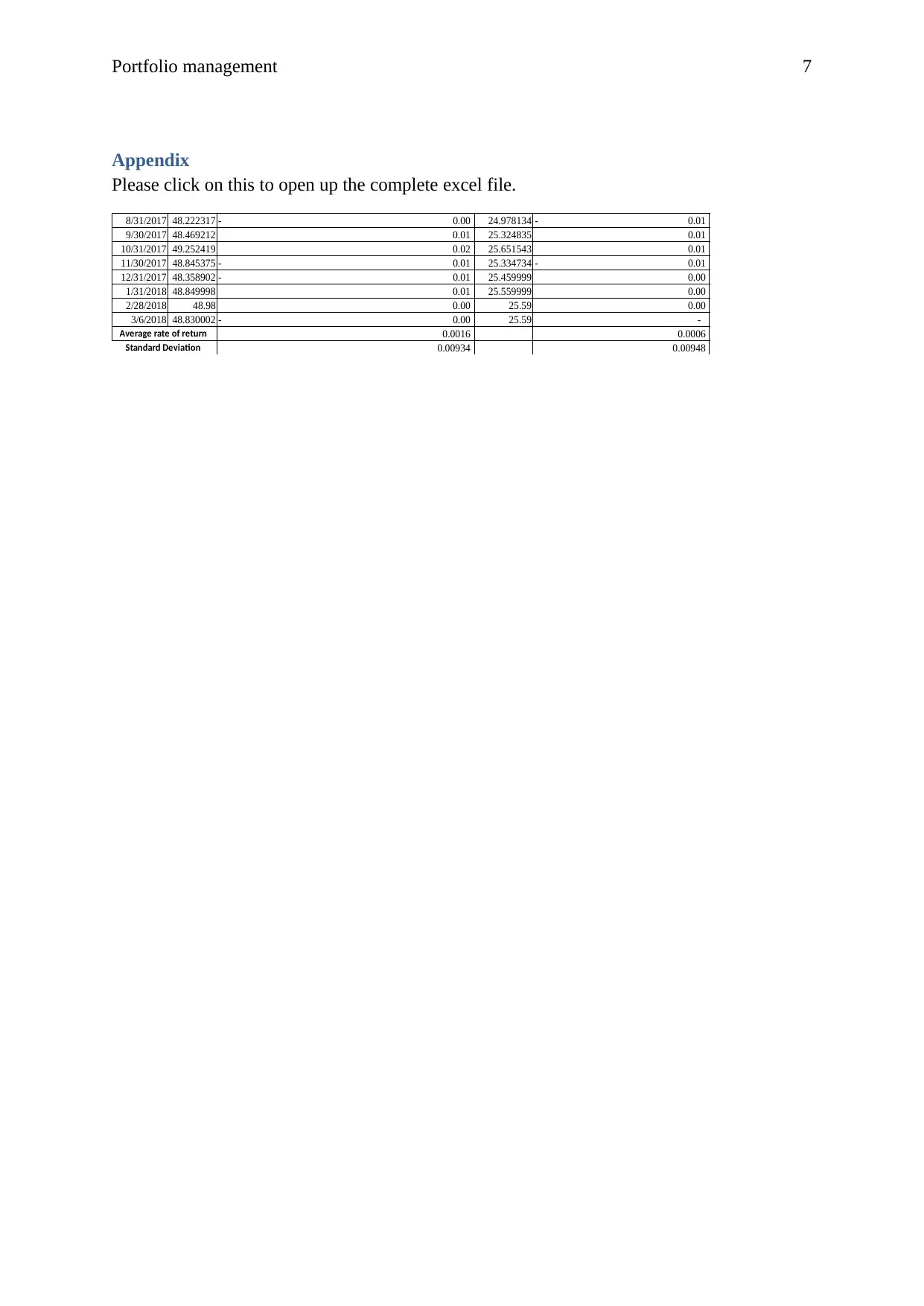

This report, prepared for a university course, analyzes portfolio management strategies using data from six companies, including risk-free assets and risky assets like BHP Billiton, Wesfarmers, and Tesco. The analysis includes calculating the minimum variance portfolio and an optimum risk portfolio, along with the computation of the beta for each risky company. The report highlights Wesfarmers' higher average return compared to other risky companies and discusses the implications of the calculated betas on share price changes based on market factors. The conclusion suggests that the tangency portfolio offers a higher return with a less risky investment plan. The report includes statistical data, correlation coefficients, and Sharpe ratios to support the findings, with an Excel file as an appendix for detailed data.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.