FINC 2011, University of Sydney: Corporate Finance Share Price Report

VerifiedAdded on 2022/11/25

|13

|3032

|438

Report

AI Summary

This report addresses the privatization of Information Technology Australia, advising the Commonwealth Government on a potential share price. The analysis begins with selecting proxy companies, Xero Limited and Wistech Global Limited, to determine beta values, which are then used in the Capital Asset Pricing Model (CAPM) to calculate the cost of equity. The report then employs the dividend discount model (DDM) to estimate the share price, providing recommendations based on both proxy companies. The report includes detailed calculations of beta, debt-to-equity ratios, CAPM returns, and share prices, offering a comprehensive financial analysis to guide the government's decision-making process. The report provides a detailed valuation of the company using the dividend discount model, considering the cost of equity to determine a suitable price range for the shares. The study provides a detailed analysis of the share price valuation, using Xero Limited and Wistech Global Limited as proxy companies.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note:

Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

1

Executive Summary:

The overall assessment directly aims in evaluating the calculations that is required by the

Commonwealth Government of Australia for issuing shares of Information Technology

Australia to normal shareholders. The assessment directly selects a proxy company for

information technology Australia to issue the relevant shares to its new shareholders. Capital

Asset pricing model and dividend discount model has a relatively help in determining the

adequate proxy company which could allow the government to complete the Desire of selling

the shares of Information Technology Australia. Hence, the information of Xero Limited and

Wistech Global Limited has been helpful in detecting the price range in which the

government can sell the shares of Information Technology Australia.

1

Executive Summary:

The overall assessment directly aims in evaluating the calculations that is required by the

Commonwealth Government of Australia for issuing shares of Information Technology

Australia to normal shareholders. The assessment directly selects a proxy company for

information technology Australia to issue the relevant shares to its new shareholders. Capital

Asset pricing model and dividend discount model has a relatively help in determining the

adequate proxy company which could allow the government to complete the Desire of selling

the shares of Information Technology Australia. Hence, the information of Xero Limited and

Wistech Global Limited has been helpful in detecting the price range in which the

government can sell the shares of Information Technology Australia.

FINANCE

2

Table of Contents

Introduction:...............................................................................................................................3

Selecting one of the companies that are possible fort detecting the beta for information

technology Australia:.................................................................................................................3

Using the data from Proxy Company to calculate its betas:......................................................4

Determining the appropriate beta for Information Technology Australia assuming the

company as expected market debt to equity ratio of 0.67:.........................................................8

Calculating the required return on equity Information Technology Australia using the Capital

Asset Pricing Model (CAPM):...................................................................................................8

Identifying the appropriate price for the government to sell Information Technology Australia

shares:.........................................................................................................................................9

Conclusion:................................................................................................................................9

Reference and Bibliography:....................................................................................................11

2

Table of Contents

Introduction:...............................................................................................................................3

Selecting one of the companies that are possible fort detecting the beta for information

technology Australia:.................................................................................................................3

Using the data from Proxy Company to calculate its betas:......................................................4

Determining the appropriate beta for Information Technology Australia assuming the

company as expected market debt to equity ratio of 0.67:.........................................................8

Calculating the required return on equity Information Technology Australia using the Capital

Asset Pricing Model (CAPM):...................................................................................................8

Identifying the appropriate price for the government to sell Information Technology Australia

shares:.........................................................................................................................................9

Conclusion:................................................................................................................................9

Reference and Bibliography:....................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

3

Introduction:

The overall assessment directly aims in evaluating the calculations that is required by

the Commonwealth Government of Australia for issuing shares of Information Technology

Australia to normal shareholders. The assessment directly selects a proxy company for

information technology Australia to issue the relevant shares to its new shareholders.

Adequate beta values are calculated for the proxy company, which is then used for the

calculation of Capital Asset pricing model for the information technology Australia. Lastly,

overall share price of the company that needs to be taken into consideration by the

government by selling the shares of Information Technology Australia is adequately depicted

with relevant calculation of dividend discount model.

Selecting one of the companies that are possible fort detecting the beta for information

technology Australia:

Two companies have been selected for information technology Australia, as a proxy

is Xero Limited and Wistech Global Limited. Proxy companies directly fall under the

Information Technology Sector of Australia, which can allow the government to identify the

relevant beta levels, which can be used in deriving the relevant calculation. The use of a

proxy company directly allows organizations to determine the level of Beta and market

exposure that they will face after the share issue. Moreover, the proxy companies are also

used in determining the future debt to Capital ratio and share price valuation that needs to be

conducted for a particular share issue. Damodaran (2016) stated that companies with the help

of proxy method are able to detect the level of share value that would be determined for their

share issue, which can allow them to detect whether the adequate investments from there IPO

will be generated to support their operations. Thanks from the valuation it could be

understood that organization such as Xero Limited and Wistech Global Limited has similar

operations, which can allow the government to determine the level of share value and cost of

equity that will be incurred by the company after the share issue. Therefore, the beta levels of

Xero Limited and Wistech Global Limited can be used as a proxy for Information

Technology Australia (Ehrhardt & Brigham, 2016). For calculating, the beta values the

overall Australian index name ALL ORDINARY INDEX is used, as it provides adequate

information about the current capital market movement of Australia.

3

Introduction:

The overall assessment directly aims in evaluating the calculations that is required by

the Commonwealth Government of Australia for issuing shares of Information Technology

Australia to normal shareholders. The assessment directly selects a proxy company for

information technology Australia to issue the relevant shares to its new shareholders.

Adequate beta values are calculated for the proxy company, which is then used for the

calculation of Capital Asset pricing model for the information technology Australia. Lastly,

overall share price of the company that needs to be taken into consideration by the

government by selling the shares of Information Technology Australia is adequately depicted

with relevant calculation of dividend discount model.

Selecting one of the companies that are possible fort detecting the beta for information

technology Australia:

Two companies have been selected for information technology Australia, as a proxy

is Xero Limited and Wistech Global Limited. Proxy companies directly fall under the

Information Technology Sector of Australia, which can allow the government to identify the

relevant beta levels, which can be used in deriving the relevant calculation. The use of a

proxy company directly allows organizations to determine the level of Beta and market

exposure that they will face after the share issue. Moreover, the proxy companies are also

used in determining the future debt to Capital ratio and share price valuation that needs to be

conducted for a particular share issue. Damodaran (2016) stated that companies with the help

of proxy method are able to detect the level of share value that would be determined for their

share issue, which can allow them to detect whether the adequate investments from there IPO

will be generated to support their operations. Thanks from the valuation it could be

understood that organization such as Xero Limited and Wistech Global Limited has similar

operations, which can allow the government to determine the level of share value and cost of

equity that will be incurred by the company after the share issue. Therefore, the beta levels of

Xero Limited and Wistech Global Limited can be used as a proxy for Information

Technology Australia (Ehrhardt & Brigham, 2016). For calculating, the beta values the

overall Australian index name ALL ORDINARY INDEX is used, as it provides adequate

information about the current capital market movement of Australia.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

4

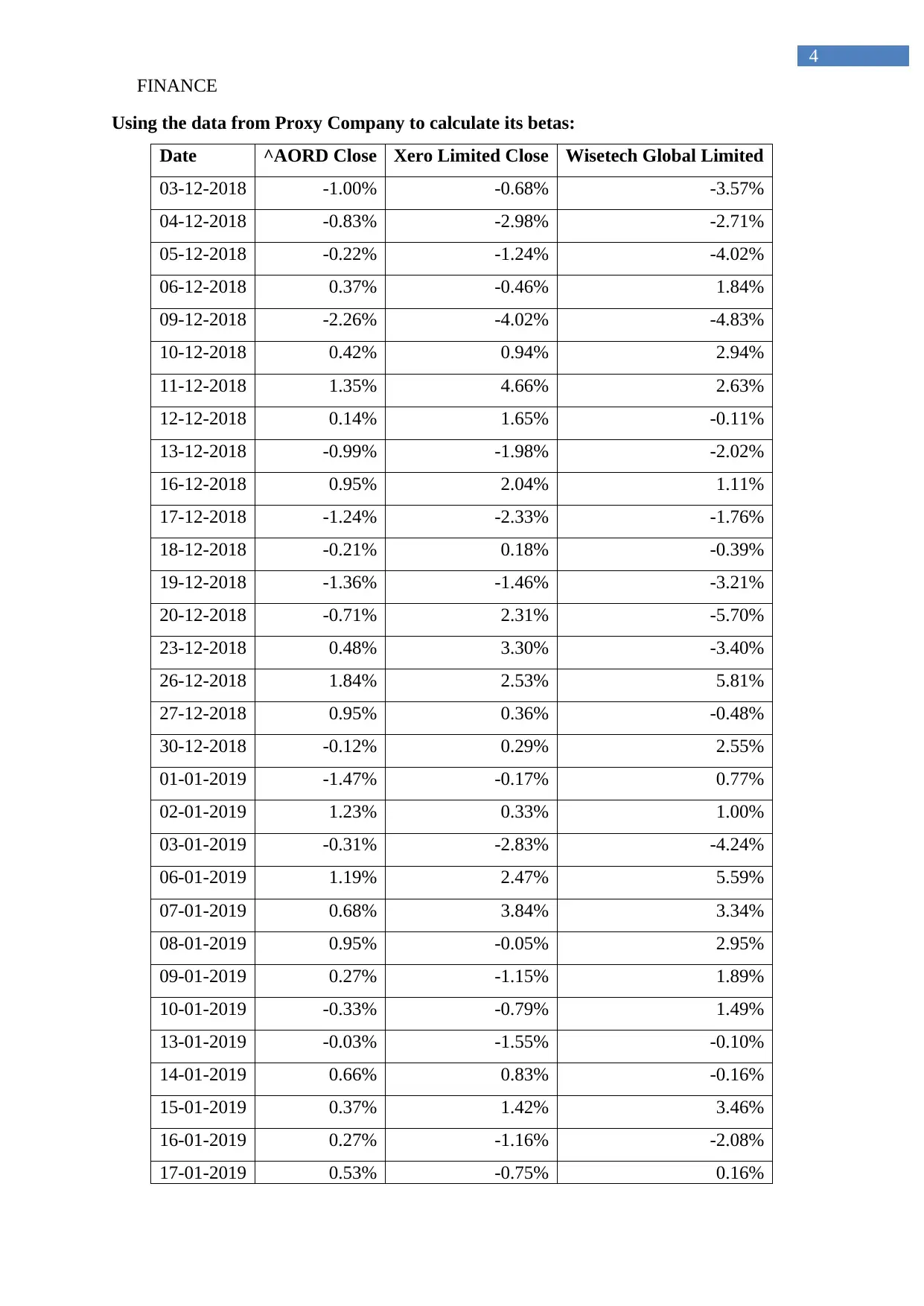

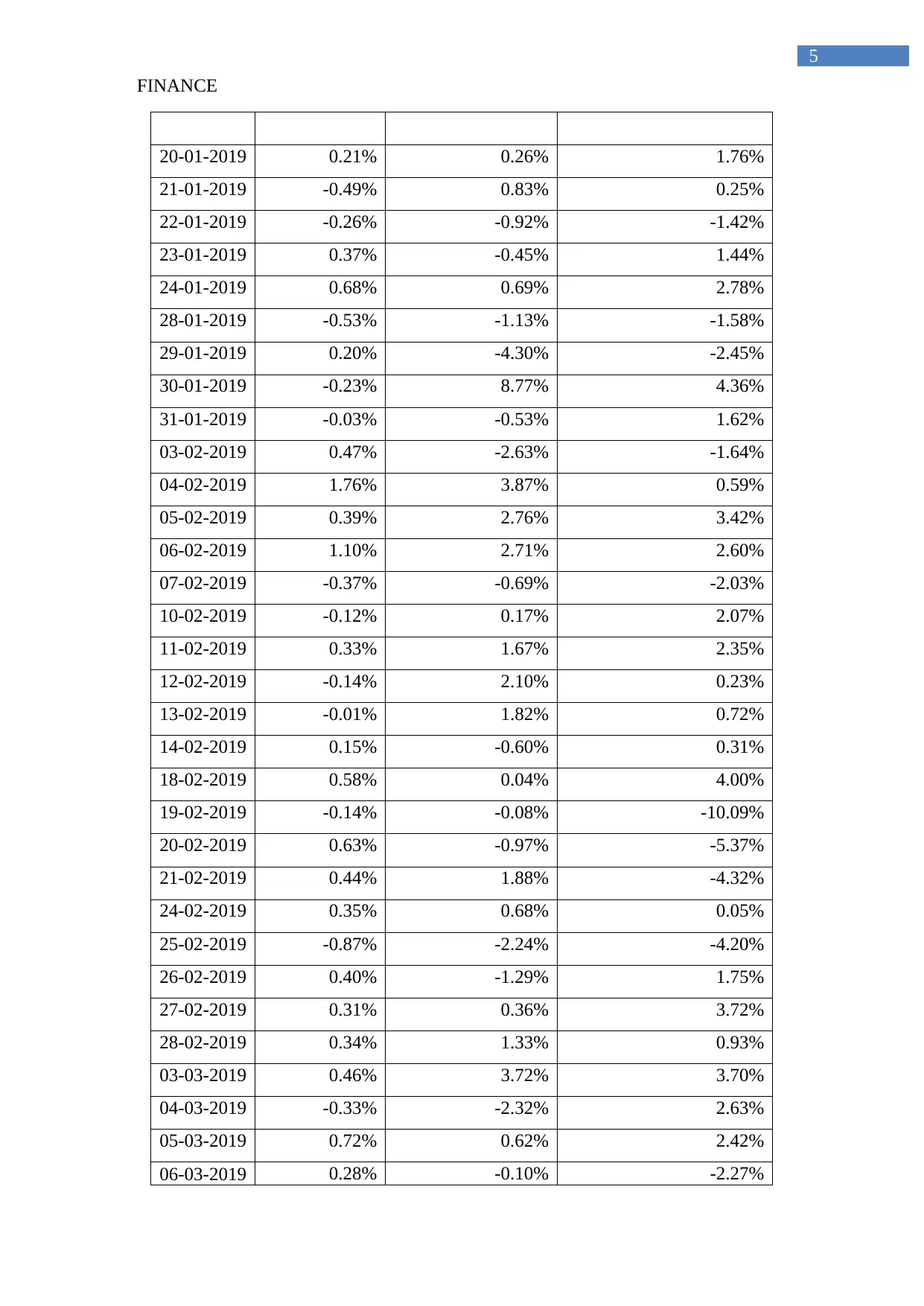

Using the data from Proxy Company to calculate its betas:

Date ^AORD Close Xero Limited Close Wisetech Global Limited

03-12-2018 -1.00% -0.68% -3.57%

04-12-2018 -0.83% -2.98% -2.71%

05-12-2018 -0.22% -1.24% -4.02%

06-12-2018 0.37% -0.46% 1.84%

09-12-2018 -2.26% -4.02% -4.83%

10-12-2018 0.42% 0.94% 2.94%

11-12-2018 1.35% 4.66% 2.63%

12-12-2018 0.14% 1.65% -0.11%

13-12-2018 -0.99% -1.98% -2.02%

16-12-2018 0.95% 2.04% 1.11%

17-12-2018 -1.24% -2.33% -1.76%

18-12-2018 -0.21% 0.18% -0.39%

19-12-2018 -1.36% -1.46% -3.21%

20-12-2018 -0.71% 2.31% -5.70%

23-12-2018 0.48% 3.30% -3.40%

26-12-2018 1.84% 2.53% 5.81%

27-12-2018 0.95% 0.36% -0.48%

30-12-2018 -0.12% 0.29% 2.55%

01-01-2019 -1.47% -0.17% 0.77%

02-01-2019 1.23% 0.33% 1.00%

03-01-2019 -0.31% -2.83% -4.24%

06-01-2019 1.19% 2.47% 5.59%

07-01-2019 0.68% 3.84% 3.34%

08-01-2019 0.95% -0.05% 2.95%

09-01-2019 0.27% -1.15% 1.89%

10-01-2019 -0.33% -0.79% 1.49%

13-01-2019 -0.03% -1.55% -0.10%

14-01-2019 0.66% 0.83% -0.16%

15-01-2019 0.37% 1.42% 3.46%

16-01-2019 0.27% -1.16% -2.08%

17-01-2019 0.53% -0.75% 0.16%

4

Using the data from Proxy Company to calculate its betas:

Date ^AORD Close Xero Limited Close Wisetech Global Limited

03-12-2018 -1.00% -0.68% -3.57%

04-12-2018 -0.83% -2.98% -2.71%

05-12-2018 -0.22% -1.24% -4.02%

06-12-2018 0.37% -0.46% 1.84%

09-12-2018 -2.26% -4.02% -4.83%

10-12-2018 0.42% 0.94% 2.94%

11-12-2018 1.35% 4.66% 2.63%

12-12-2018 0.14% 1.65% -0.11%

13-12-2018 -0.99% -1.98% -2.02%

16-12-2018 0.95% 2.04% 1.11%

17-12-2018 -1.24% -2.33% -1.76%

18-12-2018 -0.21% 0.18% -0.39%

19-12-2018 -1.36% -1.46% -3.21%

20-12-2018 -0.71% 2.31% -5.70%

23-12-2018 0.48% 3.30% -3.40%

26-12-2018 1.84% 2.53% 5.81%

27-12-2018 0.95% 0.36% -0.48%

30-12-2018 -0.12% 0.29% 2.55%

01-01-2019 -1.47% -0.17% 0.77%

02-01-2019 1.23% 0.33% 1.00%

03-01-2019 -0.31% -2.83% -4.24%

06-01-2019 1.19% 2.47% 5.59%

07-01-2019 0.68% 3.84% 3.34%

08-01-2019 0.95% -0.05% 2.95%

09-01-2019 0.27% -1.15% 1.89%

10-01-2019 -0.33% -0.79% 1.49%

13-01-2019 -0.03% -1.55% -0.10%

14-01-2019 0.66% 0.83% -0.16%

15-01-2019 0.37% 1.42% 3.46%

16-01-2019 0.27% -1.16% -2.08%

17-01-2019 0.53% -0.75% 0.16%

FINANCE

5

20-01-2019 0.21% 0.26% 1.76%

21-01-2019 -0.49% 0.83% 0.25%

22-01-2019 -0.26% -0.92% -1.42%

23-01-2019 0.37% -0.45% 1.44%

24-01-2019 0.68% 0.69% 2.78%

28-01-2019 -0.53% -1.13% -1.58%

29-01-2019 0.20% -4.30% -2.45%

30-01-2019 -0.23% 8.77% 4.36%

31-01-2019 -0.03% -0.53% 1.62%

03-02-2019 0.47% -2.63% -1.64%

04-02-2019 1.76% 3.87% 0.59%

05-02-2019 0.39% 2.76% 3.42%

06-02-2019 1.10% 2.71% 2.60%

07-02-2019 -0.37% -0.69% -2.03%

10-02-2019 -0.12% 0.17% 2.07%

11-02-2019 0.33% 1.67% 2.35%

12-02-2019 -0.14% 2.10% 0.23%

13-02-2019 -0.01% 1.82% 0.72%

14-02-2019 0.15% -0.60% 0.31%

18-02-2019 0.58% 0.04% 4.00%

19-02-2019 -0.14% -0.08% -10.09%

20-02-2019 0.63% -0.97% -5.37%

21-02-2019 0.44% 1.88% -4.32%

24-02-2019 0.35% 0.68% 0.05%

25-02-2019 -0.87% -2.24% -4.20%

26-02-2019 0.40% -1.29% 1.75%

27-02-2019 0.31% 0.36% 3.72%

28-02-2019 0.34% 1.33% 0.93%

03-03-2019 0.46% 3.72% 3.70%

04-03-2019 -0.33% -2.32% 2.63%

05-03-2019 0.72% 0.62% 2.42%

06-03-2019 0.28% -0.10% -2.27%

5

20-01-2019 0.21% 0.26% 1.76%

21-01-2019 -0.49% 0.83% 0.25%

22-01-2019 -0.26% -0.92% -1.42%

23-01-2019 0.37% -0.45% 1.44%

24-01-2019 0.68% 0.69% 2.78%

28-01-2019 -0.53% -1.13% -1.58%

29-01-2019 0.20% -4.30% -2.45%

30-01-2019 -0.23% 8.77% 4.36%

31-01-2019 -0.03% -0.53% 1.62%

03-02-2019 0.47% -2.63% -1.64%

04-02-2019 1.76% 3.87% 0.59%

05-02-2019 0.39% 2.76% 3.42%

06-02-2019 1.10% 2.71% 2.60%

07-02-2019 -0.37% -0.69% -2.03%

10-02-2019 -0.12% 0.17% 2.07%

11-02-2019 0.33% 1.67% 2.35%

12-02-2019 -0.14% 2.10% 0.23%

13-02-2019 -0.01% 1.82% 0.72%

14-02-2019 0.15% -0.60% 0.31%

18-02-2019 0.58% 0.04% 4.00%

19-02-2019 -0.14% -0.08% -10.09%

20-02-2019 0.63% -0.97% -5.37%

21-02-2019 0.44% 1.88% -4.32%

24-02-2019 0.35% 0.68% 0.05%

25-02-2019 -0.87% -2.24% -4.20%

26-02-2019 0.40% -1.29% 1.75%

27-02-2019 0.31% 0.36% 3.72%

28-02-2019 0.34% 1.33% 0.93%

03-03-2019 0.46% 3.72% 3.70%

04-03-2019 -0.33% -2.32% 2.63%

05-03-2019 0.72% 0.62% 2.42%

06-03-2019 0.28% -0.10% -2.27%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

6

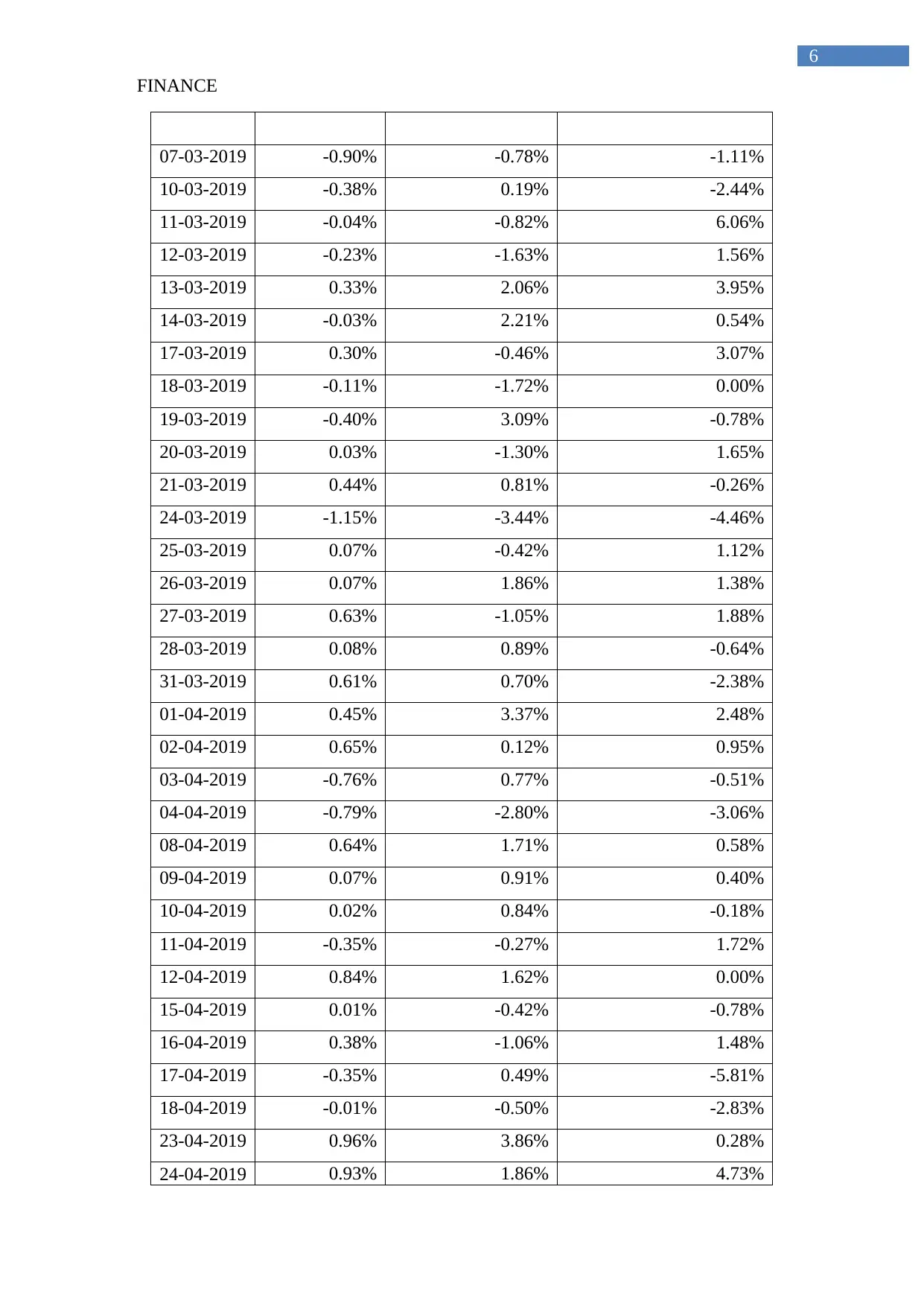

07-03-2019 -0.90% -0.78% -1.11%

10-03-2019 -0.38% 0.19% -2.44%

11-03-2019 -0.04% -0.82% 6.06%

12-03-2019 -0.23% -1.63% 1.56%

13-03-2019 0.33% 2.06% 3.95%

14-03-2019 -0.03% 2.21% 0.54%

17-03-2019 0.30% -0.46% 3.07%

18-03-2019 -0.11% -1.72% 0.00%

19-03-2019 -0.40% 3.09% -0.78%

20-03-2019 0.03% -1.30% 1.65%

21-03-2019 0.44% 0.81% -0.26%

24-03-2019 -1.15% -3.44% -4.46%

25-03-2019 0.07% -0.42% 1.12%

26-03-2019 0.07% 1.86% 1.38%

27-03-2019 0.63% -1.05% 1.88%

28-03-2019 0.08% 0.89% -0.64%

31-03-2019 0.61% 0.70% -2.38%

01-04-2019 0.45% 3.37% 2.48%

02-04-2019 0.65% 0.12% 0.95%

03-04-2019 -0.76% 0.77% -0.51%

04-04-2019 -0.79% -2.80% -3.06%

08-04-2019 0.64% 1.71% 0.58%

09-04-2019 0.07% 0.91% 0.40%

10-04-2019 0.02% 0.84% -0.18%

11-04-2019 -0.35% -0.27% 1.72%

12-04-2019 0.84% 1.62% 0.00%

15-04-2019 0.01% -0.42% -0.78%

16-04-2019 0.38% -1.06% 1.48%

17-04-2019 -0.35% 0.49% -5.81%

18-04-2019 -0.01% -0.50% -2.83%

23-04-2019 0.96% 3.86% 0.28%

24-04-2019 0.93% 1.86% 4.73%

6

07-03-2019 -0.90% -0.78% -1.11%

10-03-2019 -0.38% 0.19% -2.44%

11-03-2019 -0.04% -0.82% 6.06%

12-03-2019 -0.23% -1.63% 1.56%

13-03-2019 0.33% 2.06% 3.95%

14-03-2019 -0.03% 2.21% 0.54%

17-03-2019 0.30% -0.46% 3.07%

18-03-2019 -0.11% -1.72% 0.00%

19-03-2019 -0.40% 3.09% -0.78%

20-03-2019 0.03% -1.30% 1.65%

21-03-2019 0.44% 0.81% -0.26%

24-03-2019 -1.15% -3.44% -4.46%

25-03-2019 0.07% -0.42% 1.12%

26-03-2019 0.07% 1.86% 1.38%

27-03-2019 0.63% -1.05% 1.88%

28-03-2019 0.08% 0.89% -0.64%

31-03-2019 0.61% 0.70% -2.38%

01-04-2019 0.45% 3.37% 2.48%

02-04-2019 0.65% 0.12% 0.95%

03-04-2019 -0.76% 0.77% -0.51%

04-04-2019 -0.79% -2.80% -3.06%

08-04-2019 0.64% 1.71% 0.58%

09-04-2019 0.07% 0.91% 0.40%

10-04-2019 0.02% 0.84% -0.18%

11-04-2019 -0.35% -0.27% 1.72%

12-04-2019 0.84% 1.62% 0.00%

15-04-2019 0.01% -0.42% -0.78%

16-04-2019 0.38% -1.06% 1.48%

17-04-2019 -0.35% 0.49% -5.81%

18-04-2019 -0.01% -0.50% -2.83%

23-04-2019 0.96% 3.86% 0.28%

24-04-2019 0.93% 1.86% 4.73%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

7

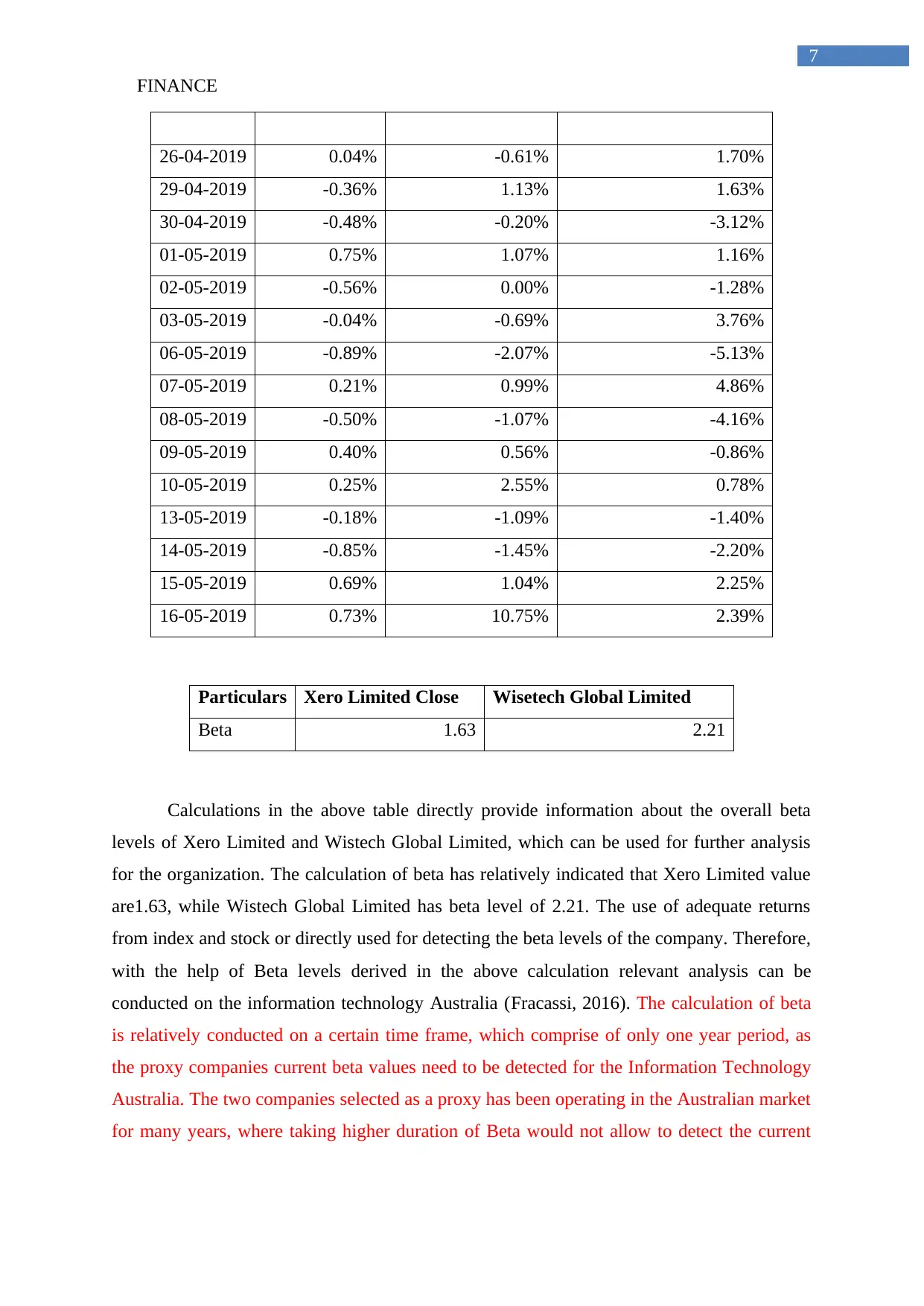

26-04-2019 0.04% -0.61% 1.70%

29-04-2019 -0.36% 1.13% 1.63%

30-04-2019 -0.48% -0.20% -3.12%

01-05-2019 0.75% 1.07% 1.16%

02-05-2019 -0.56% 0.00% -1.28%

03-05-2019 -0.04% -0.69% 3.76%

06-05-2019 -0.89% -2.07% -5.13%

07-05-2019 0.21% 0.99% 4.86%

08-05-2019 -0.50% -1.07% -4.16%

09-05-2019 0.40% 0.56% -0.86%

10-05-2019 0.25% 2.55% 0.78%

13-05-2019 -0.18% -1.09% -1.40%

14-05-2019 -0.85% -1.45% -2.20%

15-05-2019 0.69% 1.04% 2.25%

16-05-2019 0.73% 10.75% 2.39%

Particulars Xero Limited Close Wisetech Global Limited

Beta 1.63 2.21

Calculations in the above table directly provide information about the overall beta

levels of Xero Limited and Wistech Global Limited, which can be used for further analysis

for the organization. The calculation of beta has relatively indicated that Xero Limited value

are1.63, while Wistech Global Limited has beta level of 2.21. The use of adequate returns

from index and stock or directly used for detecting the beta levels of the company. Therefore,

with the help of Beta levels derived in the above calculation relevant analysis can be

conducted on the information technology Australia (Fracassi, 2016). The calculation of beta

is relatively conducted on a certain time frame, which comprise of only one year period, as

the proxy companies current beta values need to be detected for the Information Technology

Australia. The two companies selected as a proxy has been operating in the Australian market

for many years, where taking higher duration of Beta would not allow to detect the current

7

26-04-2019 0.04% -0.61% 1.70%

29-04-2019 -0.36% 1.13% 1.63%

30-04-2019 -0.48% -0.20% -3.12%

01-05-2019 0.75% 1.07% 1.16%

02-05-2019 -0.56% 0.00% -1.28%

03-05-2019 -0.04% -0.69% 3.76%

06-05-2019 -0.89% -2.07% -5.13%

07-05-2019 0.21% 0.99% 4.86%

08-05-2019 -0.50% -1.07% -4.16%

09-05-2019 0.40% 0.56% -0.86%

10-05-2019 0.25% 2.55% 0.78%

13-05-2019 -0.18% -1.09% -1.40%

14-05-2019 -0.85% -1.45% -2.20%

15-05-2019 0.69% 1.04% 2.25%

16-05-2019 0.73% 10.75% 2.39%

Particulars Xero Limited Close Wisetech Global Limited

Beta 1.63 2.21

Calculations in the above table directly provide information about the overall beta

levels of Xero Limited and Wistech Global Limited, which can be used for further analysis

for the organization. The calculation of beta has relatively indicated that Xero Limited value

are1.63, while Wistech Global Limited has beta level of 2.21. The use of adequate returns

from index and stock or directly used for detecting the beta levels of the company. Therefore,

with the help of Beta levels derived in the above calculation relevant analysis can be

conducted on the information technology Australia (Fracassi, 2016). The calculation of beta

is relatively conducted on a certain time frame, which comprise of only one year period, as

the proxy companies current beta values need to be detected for the Information Technology

Australia. The two companies selected as a proxy has been operating in the Australian market

for many years, where taking higher duration of Beta would not allow to detect the current

FINANCE

8

fluctuations in the industry. Hence, the selection of one year of data is conducted for

detecting the beta values, which can be used as a proxy for information technology Australia.

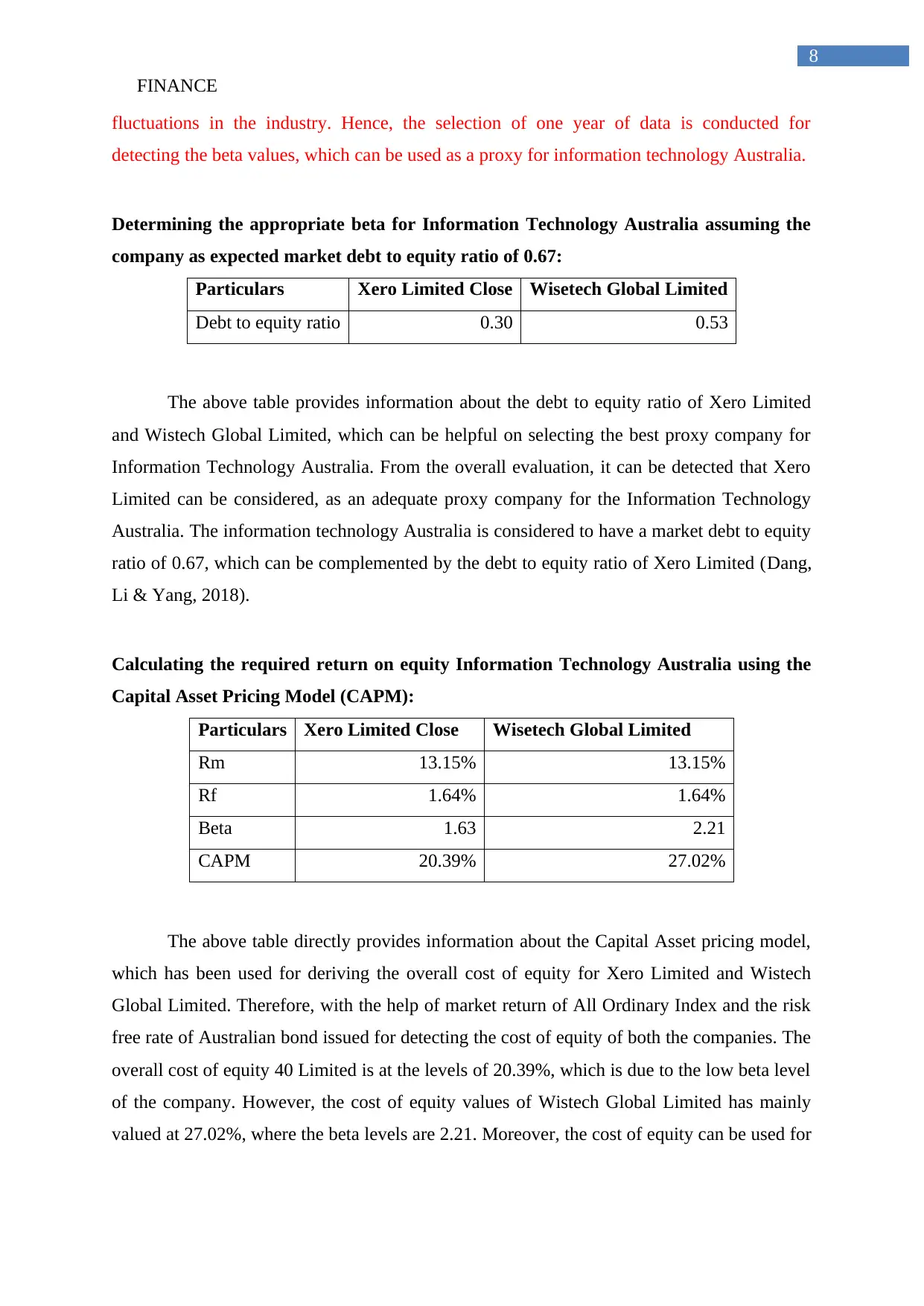

Determining the appropriate beta for Information Technology Australia assuming the

company as expected market debt to equity ratio of 0.67:

Particulars Xero Limited Close Wisetech Global Limited

Debt to equity ratio 0.30 0.53

The above table provides information about the debt to equity ratio of Xero Limited

and Wistech Global Limited, which can be helpful on selecting the best proxy company for

Information Technology Australia. From the overall evaluation, it can be detected that Xero

Limited can be considered, as an adequate proxy company for the Information Technology

Australia. The information technology Australia is considered to have a market debt to equity

ratio of 0.67, which can be complemented by the debt to equity ratio of Xero Limited (Dang,

Li & Yang, 2018).

Calculating the required return on equity Information Technology Australia using the

Capital Asset Pricing Model (CAPM):

Particulars Xero Limited Close Wisetech Global Limited

Rm 13.15% 13.15%

Rf 1.64% 1.64%

Beta 1.63 2.21

CAPM 20.39% 27.02%

The above table directly provides information about the Capital Asset pricing model,

which has been used for deriving the overall cost of equity for Xero Limited and Wistech

Global Limited. Therefore, with the help of market return of All Ordinary Index and the risk

free rate of Australian bond issued for detecting the cost of equity of both the companies. The

overall cost of equity 40 Limited is at the levels of 20.39%, which is due to the low beta level

of the company. However, the cost of equity values of Wistech Global Limited has mainly

valued at 27.02%, where the beta levels are 2.21. Moreover, the cost of equity can be used for

8

fluctuations in the industry. Hence, the selection of one year of data is conducted for

detecting the beta values, which can be used as a proxy for information technology Australia.

Determining the appropriate beta for Information Technology Australia assuming the

company as expected market debt to equity ratio of 0.67:

Particulars Xero Limited Close Wisetech Global Limited

Debt to equity ratio 0.30 0.53

The above table provides information about the debt to equity ratio of Xero Limited

and Wistech Global Limited, which can be helpful on selecting the best proxy company for

Information Technology Australia. From the overall evaluation, it can be detected that Xero

Limited can be considered, as an adequate proxy company for the Information Technology

Australia. The information technology Australia is considered to have a market debt to equity

ratio of 0.67, which can be complemented by the debt to equity ratio of Xero Limited (Dang,

Li & Yang, 2018).

Calculating the required return on equity Information Technology Australia using the

Capital Asset Pricing Model (CAPM):

Particulars Xero Limited Close Wisetech Global Limited

Rm 13.15% 13.15%

Rf 1.64% 1.64%

Beta 1.63 2.21

CAPM 20.39% 27.02%

The above table directly provides information about the Capital Asset pricing model,

which has been used for deriving the overall cost of equity for Xero Limited and Wistech

Global Limited. Therefore, with the help of market return of All Ordinary Index and the risk

free rate of Australian bond issued for detecting the cost of equity of both the companies. The

overall cost of equity 40 Limited is at the levels of 20.39%, which is due to the low beta level

of the company. However, the cost of equity values of Wistech Global Limited has mainly

valued at 27.02%, where the beta levels are 2.21. Moreover, the cost of equity can be used for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

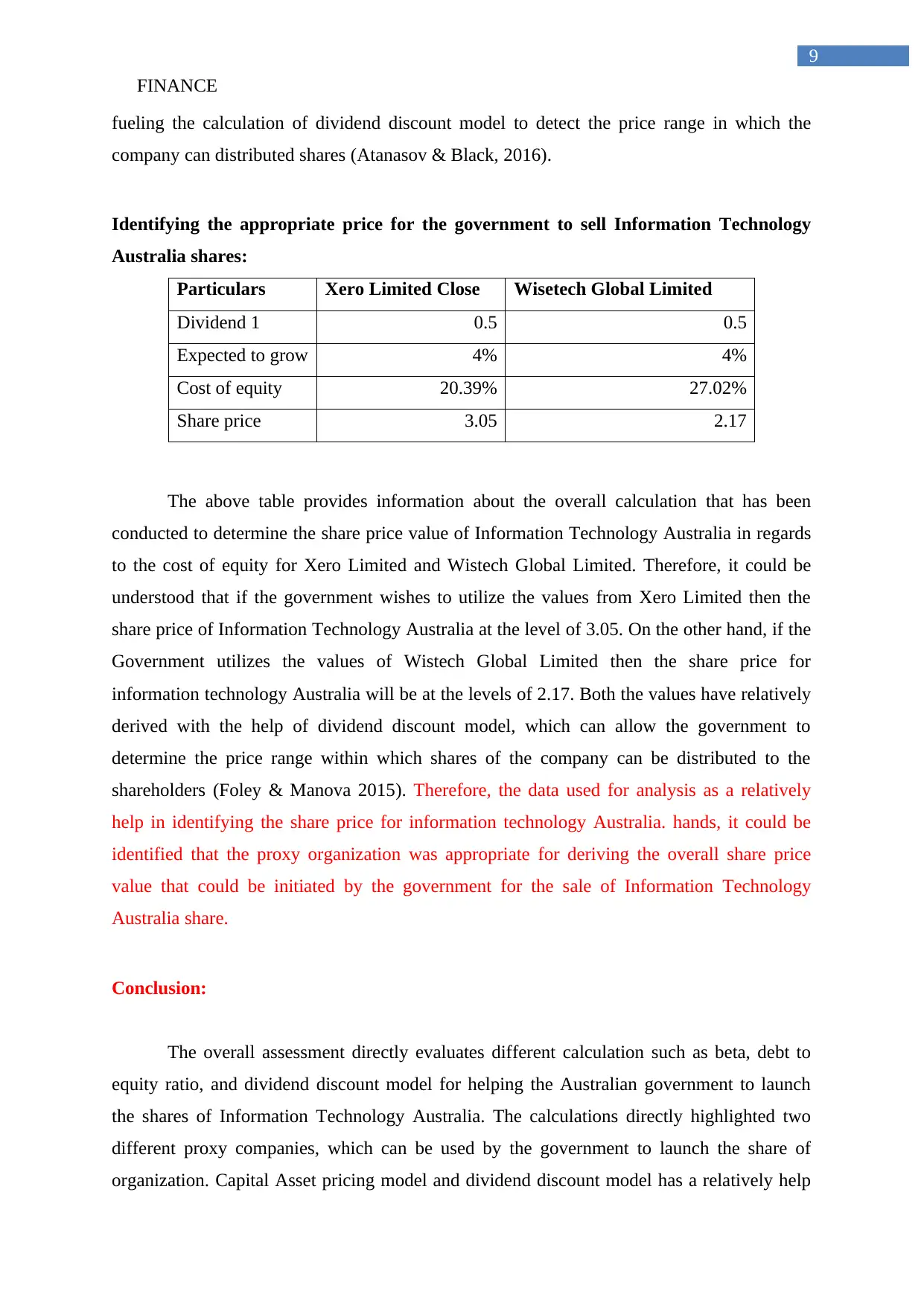

9

fueling the calculation of dividend discount model to detect the price range in which the

company can distributed shares (Atanasov & Black, 2016).

Identifying the appropriate price for the government to sell Information Technology

Australia shares:

Particulars Xero Limited Close Wisetech Global Limited

Dividend 1 0.5 0.5

Expected to grow 4% 4%

Cost of equity 20.39% 27.02%

Share price 3.05 2.17

The above table provides information about the overall calculation that has been

conducted to determine the share price value of Information Technology Australia in regards

to the cost of equity for Xero Limited and Wistech Global Limited. Therefore, it could be

understood that if the government wishes to utilize the values from Xero Limited then the

share price of Information Technology Australia at the level of 3.05. On the other hand, if the

Government utilizes the values of Wistech Global Limited then the share price for

information technology Australia will be at the levels of 2.17. Both the values have relatively

derived with the help of dividend discount model, which can allow the government to

determine the price range within which shares of the company can be distributed to the

shareholders (Foley & Manova 2015). Therefore, the data used for analysis as a relatively

help in identifying the share price for information technology Australia. hands, it could be

identified that the proxy organization was appropriate for deriving the overall share price

value that could be initiated by the government for the sale of Information Technology

Australia share.

Conclusion:

The overall assessment directly evaluates different calculation such as beta, debt to

equity ratio, and dividend discount model for helping the Australian government to launch

the shares of Information Technology Australia. The calculations directly highlighted two

different proxy companies, which can be used by the government to launch the share of

organization. Capital Asset pricing model and dividend discount model has a relatively help

9

fueling the calculation of dividend discount model to detect the price range in which the

company can distributed shares (Atanasov & Black, 2016).

Identifying the appropriate price for the government to sell Information Technology

Australia shares:

Particulars Xero Limited Close Wisetech Global Limited

Dividend 1 0.5 0.5

Expected to grow 4% 4%

Cost of equity 20.39% 27.02%

Share price 3.05 2.17

The above table provides information about the overall calculation that has been

conducted to determine the share price value of Information Technology Australia in regards

to the cost of equity for Xero Limited and Wistech Global Limited. Therefore, it could be

understood that if the government wishes to utilize the values from Xero Limited then the

share price of Information Technology Australia at the level of 3.05. On the other hand, if the

Government utilizes the values of Wistech Global Limited then the share price for

information technology Australia will be at the levels of 2.17. Both the values have relatively

derived with the help of dividend discount model, which can allow the government to

determine the price range within which shares of the company can be distributed to the

shareholders (Foley & Manova 2015). Therefore, the data used for analysis as a relatively

help in identifying the share price for information technology Australia. hands, it could be

identified that the proxy organization was appropriate for deriving the overall share price

value that could be initiated by the government for the sale of Information Technology

Australia share.

Conclusion:

The overall assessment directly evaluates different calculation such as beta, debt to

equity ratio, and dividend discount model for helping the Australian government to launch

the shares of Information Technology Australia. The calculations directly highlighted two

different proxy companies, which can be used by the government to launch the share of

organization. Capital Asset pricing model and dividend discount model has a relatively help

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

10

in determining the adequate proxy company which could allow the government to complete

the Desire of selling the shares of Information Technology Australia. Hence, the information

of Xero Limited and Wistech Global Limited has been helpful in detecting the price range in

which the government can sell the shares of Information Technology Australia.

10

in determining the adequate proxy company which could allow the government to complete

the Desire of selling the shares of Information Technology Australia. Hence, the information

of Xero Limited and Wistech Global Limited has been helpful in detecting the price range in

which the government can sell the shares of Information Technology Australia.

FINANCE

11

Reference and Bibliography:

Atanasov, V. A., & Black, B. S. (2016). Shock-based causal inference in corporate finance

and accounting research. Critical Finance Review, 5, 207-304.

Baek, J. S. (2015). Corporate finance for advancement in emerging markets. Emerging

Markets Finance and Trade, 51(sup3), 1-2.

Bebchuk, L. A., Brav, A., & Jiang, W. (2015). The long-term effects of hedge fund

activism (No. w21227). National Bureau of Economic Research.

Brusov, P., Filatova, T., Orekhova, N., & Eskindarov, M. (2015). Modern corporate finance,

investments and taxation(pp. 1-368). Berlin: Springer International Publishing.

Cai, Z., Chen, G., Xing, L., Yang, J., & Tan, X. (2019). Evaluating hedge fund downside risk

using a multi-objective neural network. Journal of Visual Communication and Image

Representation, 59, 433-438.

Cassar, G. J., Gerakos, J. J., Green, J. R., Hand, J. R., & Neal, M. (2017). Hedge fund

voluntary disclosure. The Accounting Review, 93(2), 117-135.

Cohen, F. (2017). What’s the Big Deal About Big Data Loss (Actually

Theft)?. EDPACS, 55(6), 6-11.

Damodaran, A. (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Dang, C., Li, Z. F., & Yang, C. (2018). Measuring firm size in empirical corporate

finance. Journal of Banking & Finance, 86, 159-176.

Dang, V. A., Kim, M., & Shin, Y. (2015). In search of robust methods for dynamic panel data

models in empirical corporate finance. Journal of Banking & Finance, 53, 84-98.

Dhaene, J., Van Hulle, C., Wuyts, G., Schoubben, F., & Schoutens, W. (2017). Is the capital

structure logic of corporate finance applicable to insurers? Review and analysis. Journal of

Economic Surveys, 31(1), 169-189.

Ehrhardt, M. C., & Brigham, E. F. (2016). Corporate finance: A focused approach. Cengage

learning.

11

Reference and Bibliography:

Atanasov, V. A., & Black, B. S. (2016). Shock-based causal inference in corporate finance

and accounting research. Critical Finance Review, 5, 207-304.

Baek, J. S. (2015). Corporate finance for advancement in emerging markets. Emerging

Markets Finance and Trade, 51(sup3), 1-2.

Bebchuk, L. A., Brav, A., & Jiang, W. (2015). The long-term effects of hedge fund

activism (No. w21227). National Bureau of Economic Research.

Brusov, P., Filatova, T., Orekhova, N., & Eskindarov, M. (2015). Modern corporate finance,

investments and taxation(pp. 1-368). Berlin: Springer International Publishing.

Cai, Z., Chen, G., Xing, L., Yang, J., & Tan, X. (2019). Evaluating hedge fund downside risk

using a multi-objective neural network. Journal of Visual Communication and Image

Representation, 59, 433-438.

Cassar, G. J., Gerakos, J. J., Green, J. R., Hand, J. R., & Neal, M. (2017). Hedge fund

voluntary disclosure. The Accounting Review, 93(2), 117-135.

Cohen, F. (2017). What’s the Big Deal About Big Data Loss (Actually

Theft)?. EDPACS, 55(6), 6-11.

Damodaran, A. (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Dang, C., Li, Z. F., & Yang, C. (2018). Measuring firm size in empirical corporate

finance. Journal of Banking & Finance, 86, 159-176.

Dang, V. A., Kim, M., & Shin, Y. (2015). In search of robust methods for dynamic panel data

models in empirical corporate finance. Journal of Banking & Finance, 53, 84-98.

Dhaene, J., Van Hulle, C., Wuyts, G., Schoubben, F., & Schoutens, W. (2017). Is the capital

structure logic of corporate finance applicable to insurers? Review and analysis. Journal of

Economic Surveys, 31(1), 169-189.

Ehrhardt, M. C., & Brigham, E. F. (2016). Corporate finance: A focused approach. Cengage

learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.