Taxation Report: Financial Analysis, University Course

VerifiedAdded on 2020/04/07

|9

|1655

|95

Report

AI Summary

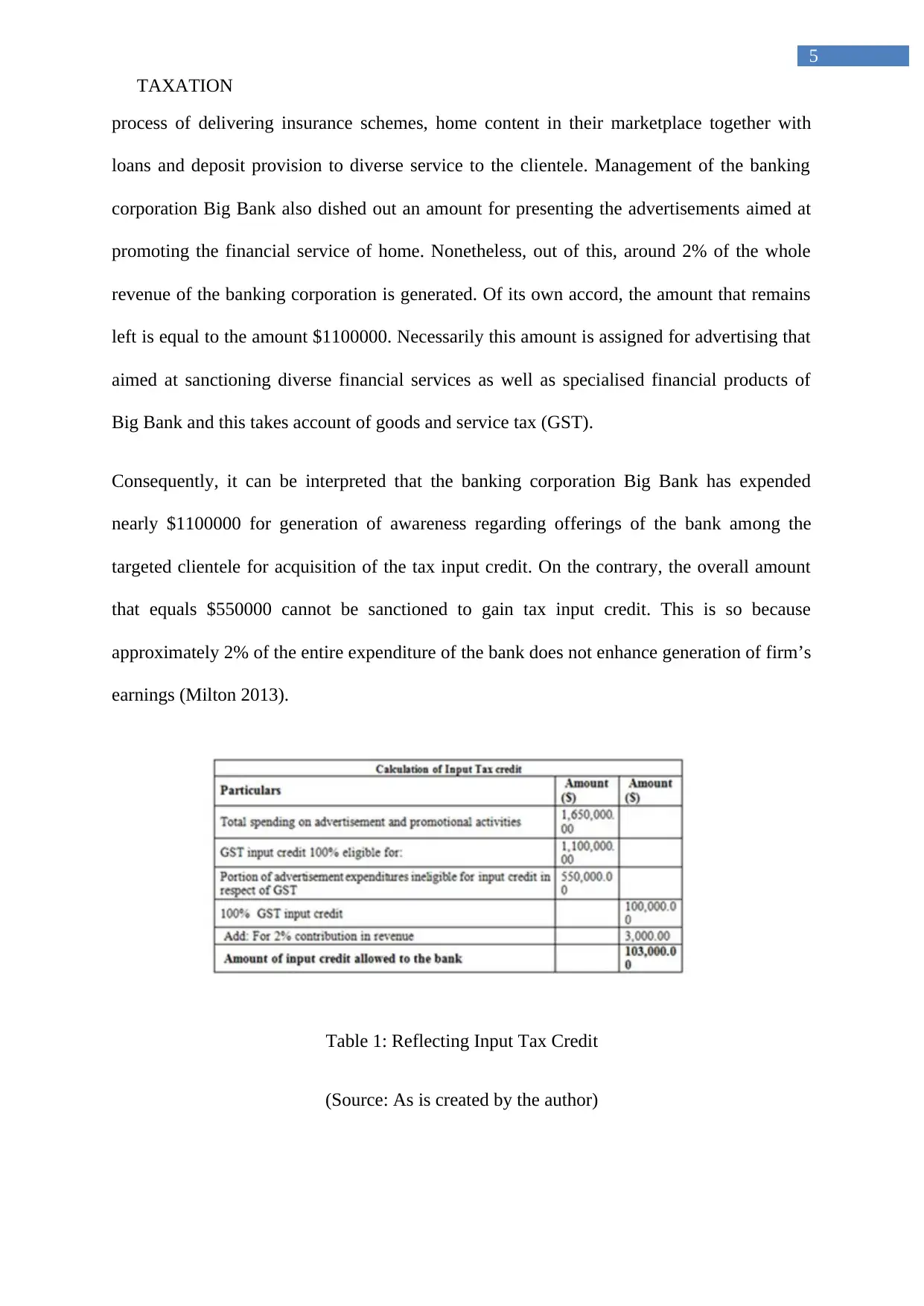

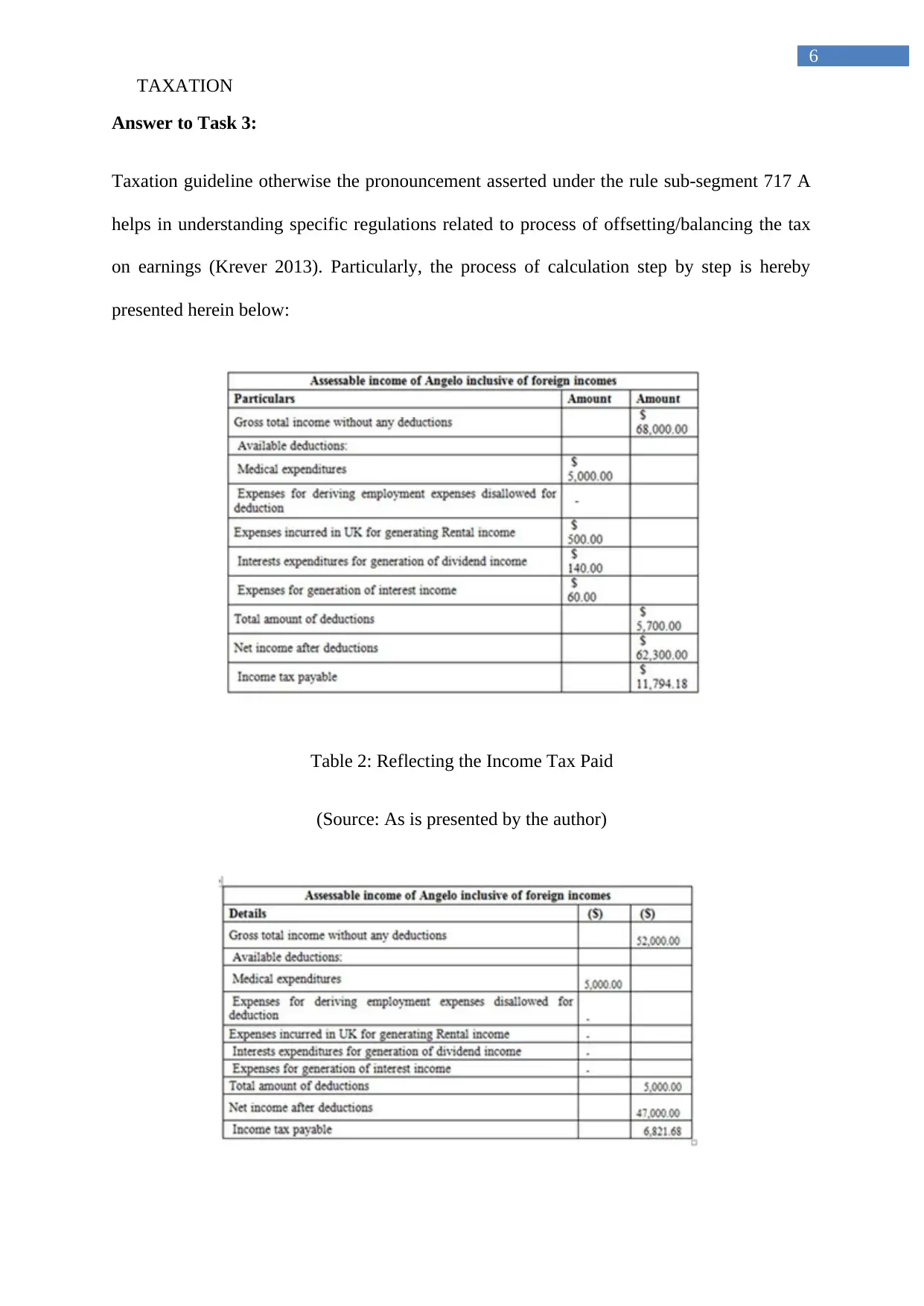

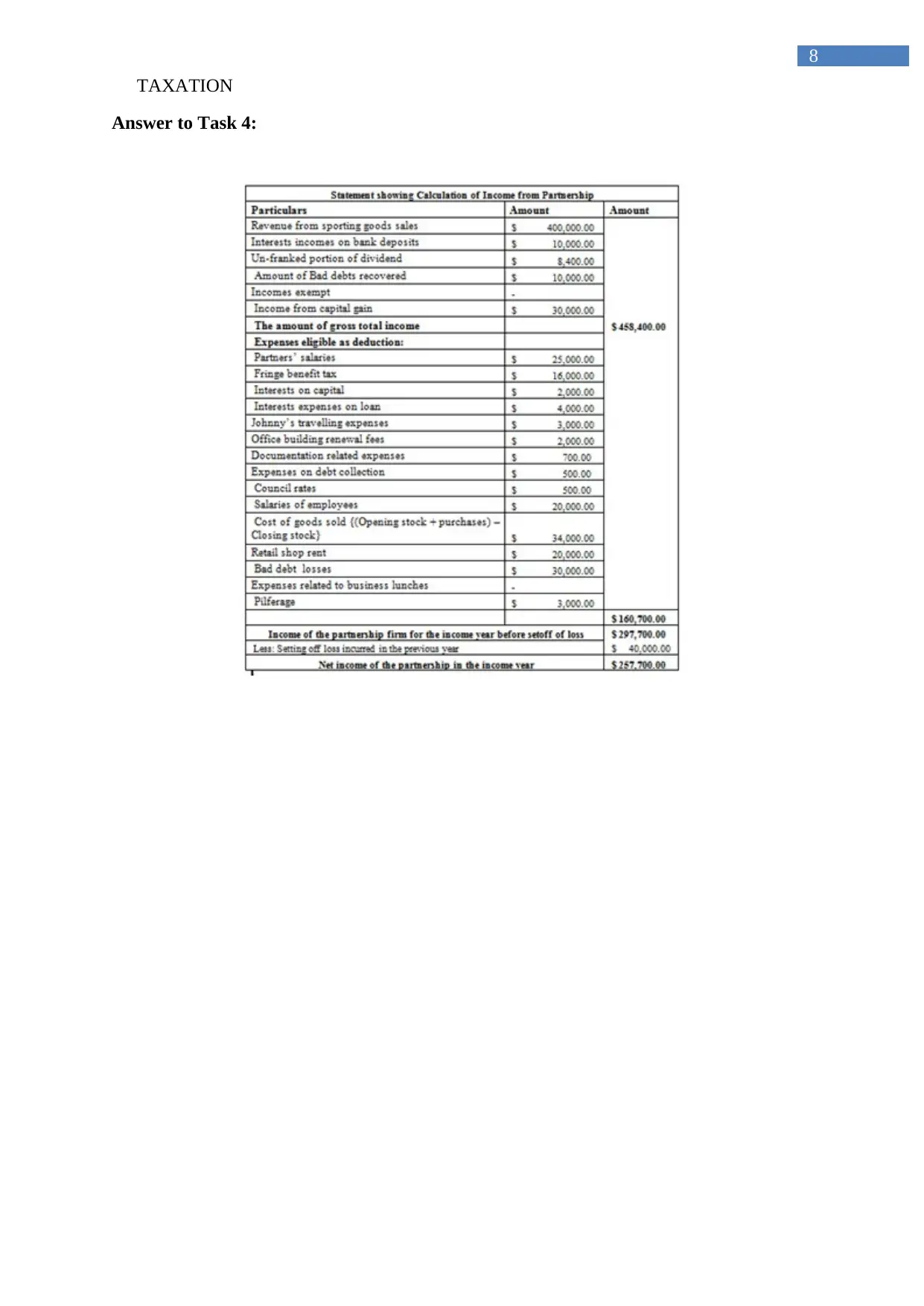

This report delves into the intricacies of taxation, providing a comprehensive analysis of key concepts and applications. It begins by outlining the principles of assessable earnings and deductible expenses, referencing relevant sections of the Income Tax Assessment Act 1997. The report then examines specific scenarios, such as the deductibility of machinery expenses and the treatment of re-assessment costs. A significant portion of the report focuses on a case study involving a banking corporation, Big Bank, and its application of GST, including input tax credit for advertising expenditures. The analysis considers the relevant tax directives and their practical implications. Finally, the report addresses the process of offsetting foreign taxation, providing step-by-step calculations and examples to illustrate the procedures. The report incorporates tables to present financial data and calculations, and it concludes with a list of cited references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.