LAW 511 Taxation Law Assignment: Income and Residency Analysis

VerifiedAdded on 2022/09/14

|18

|1947

|10

Homework Assignment

AI Summary

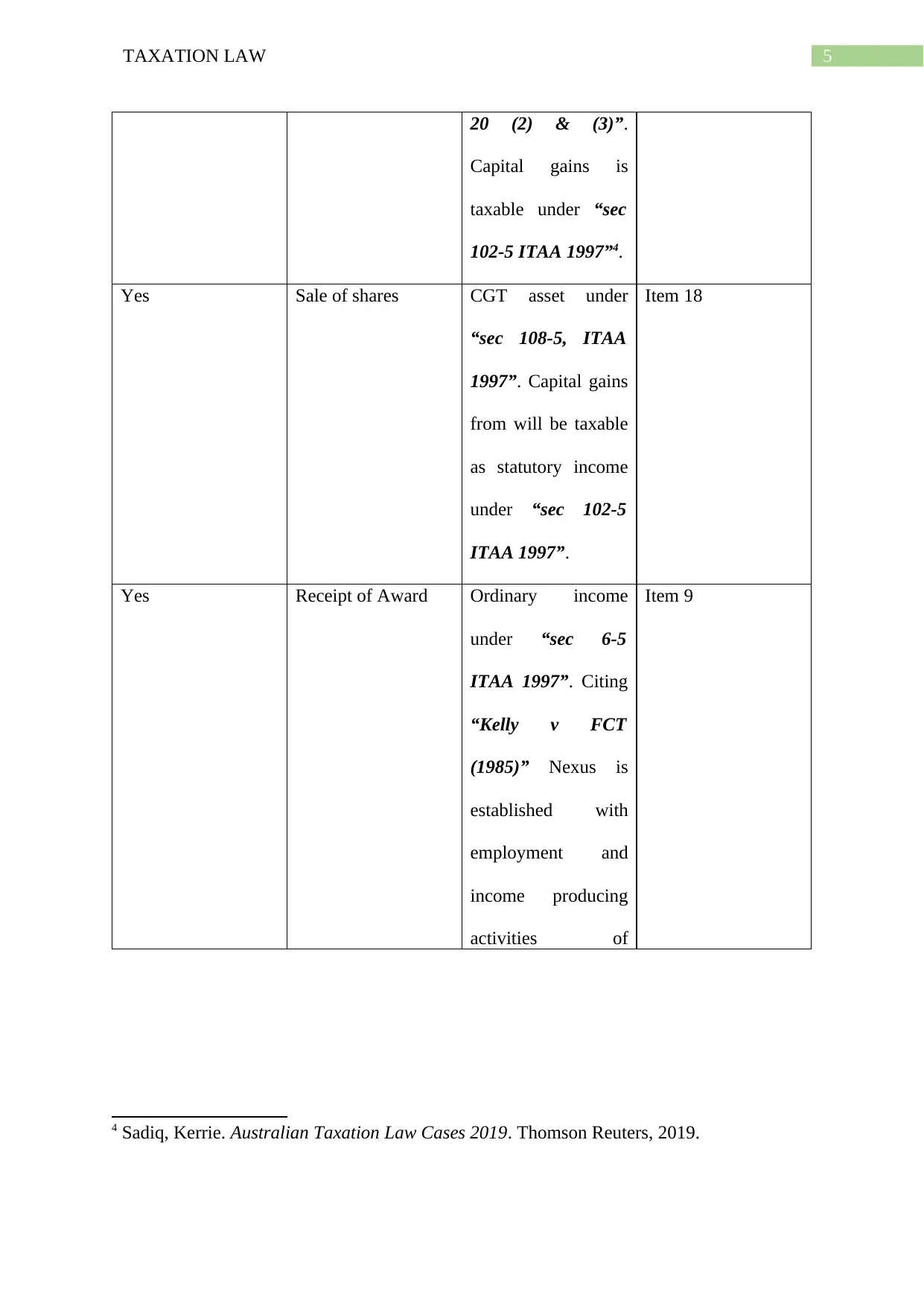

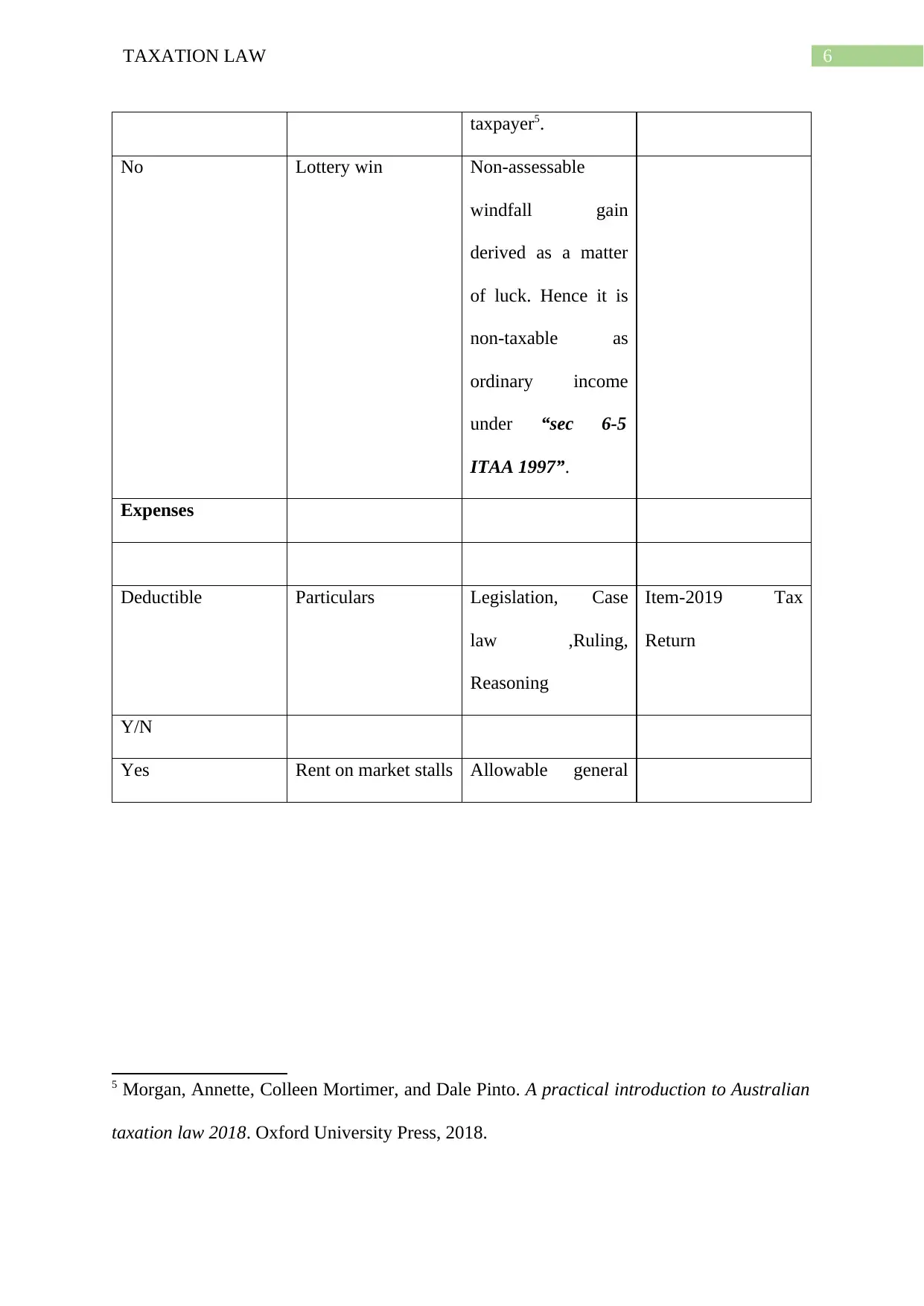

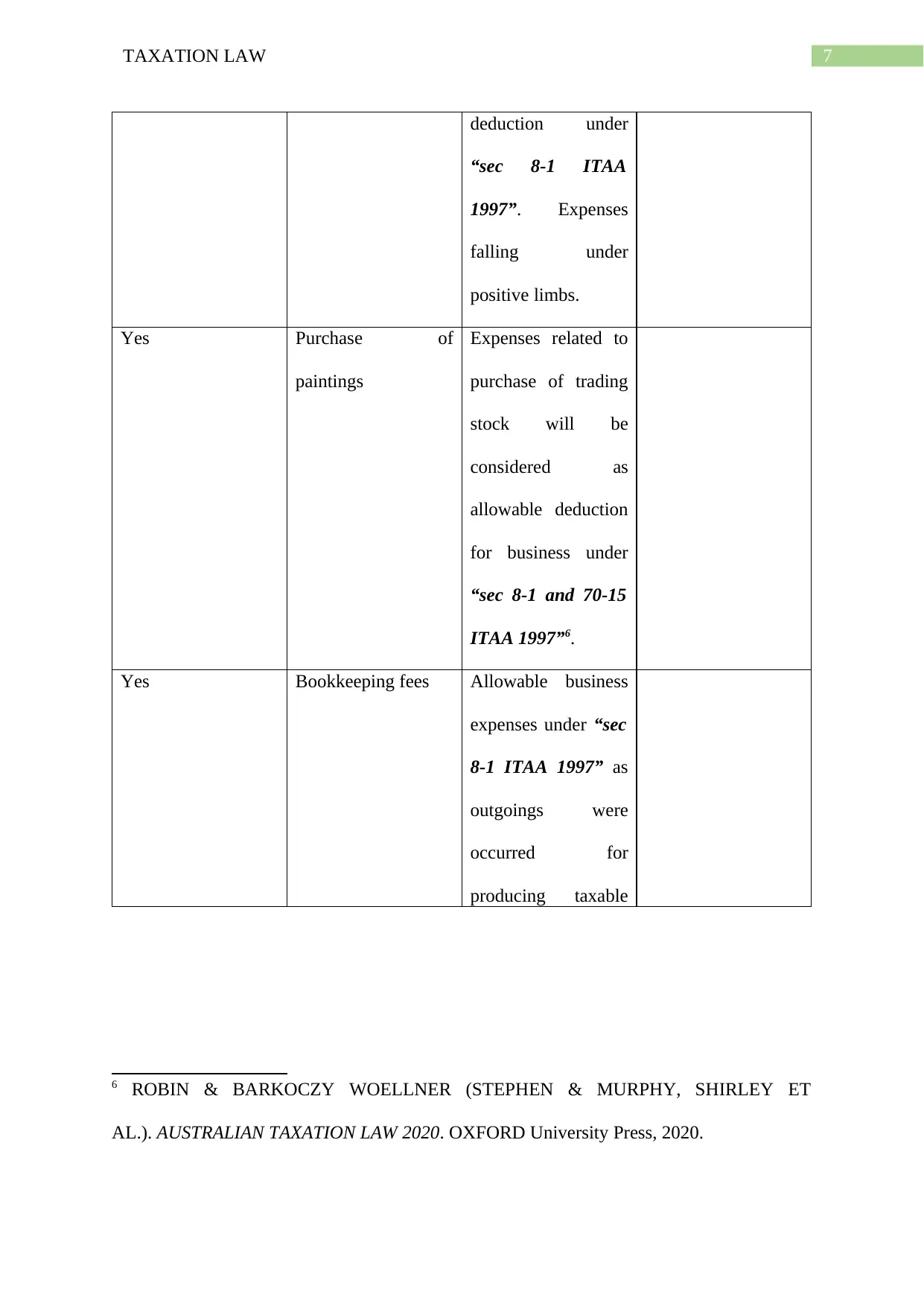

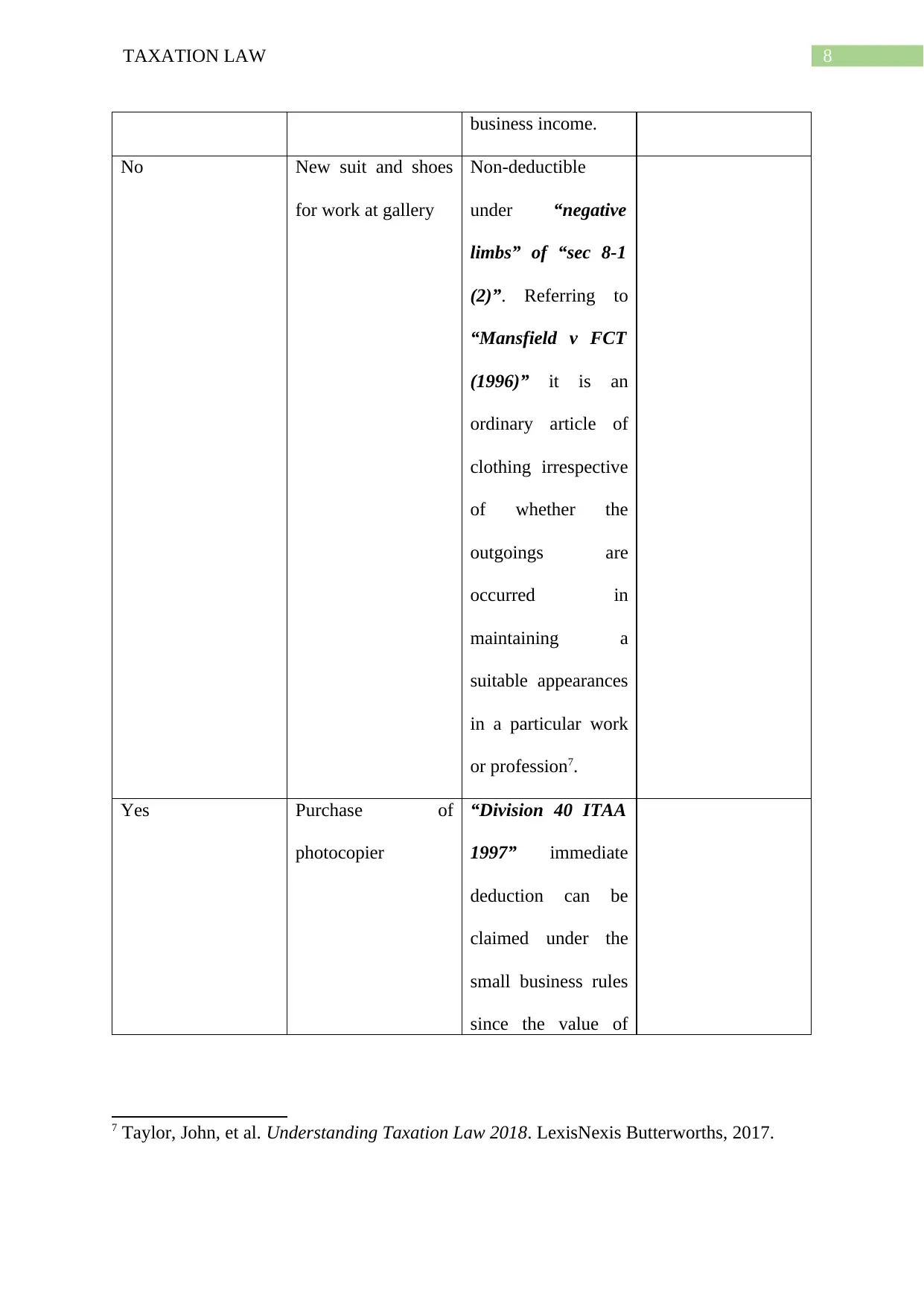

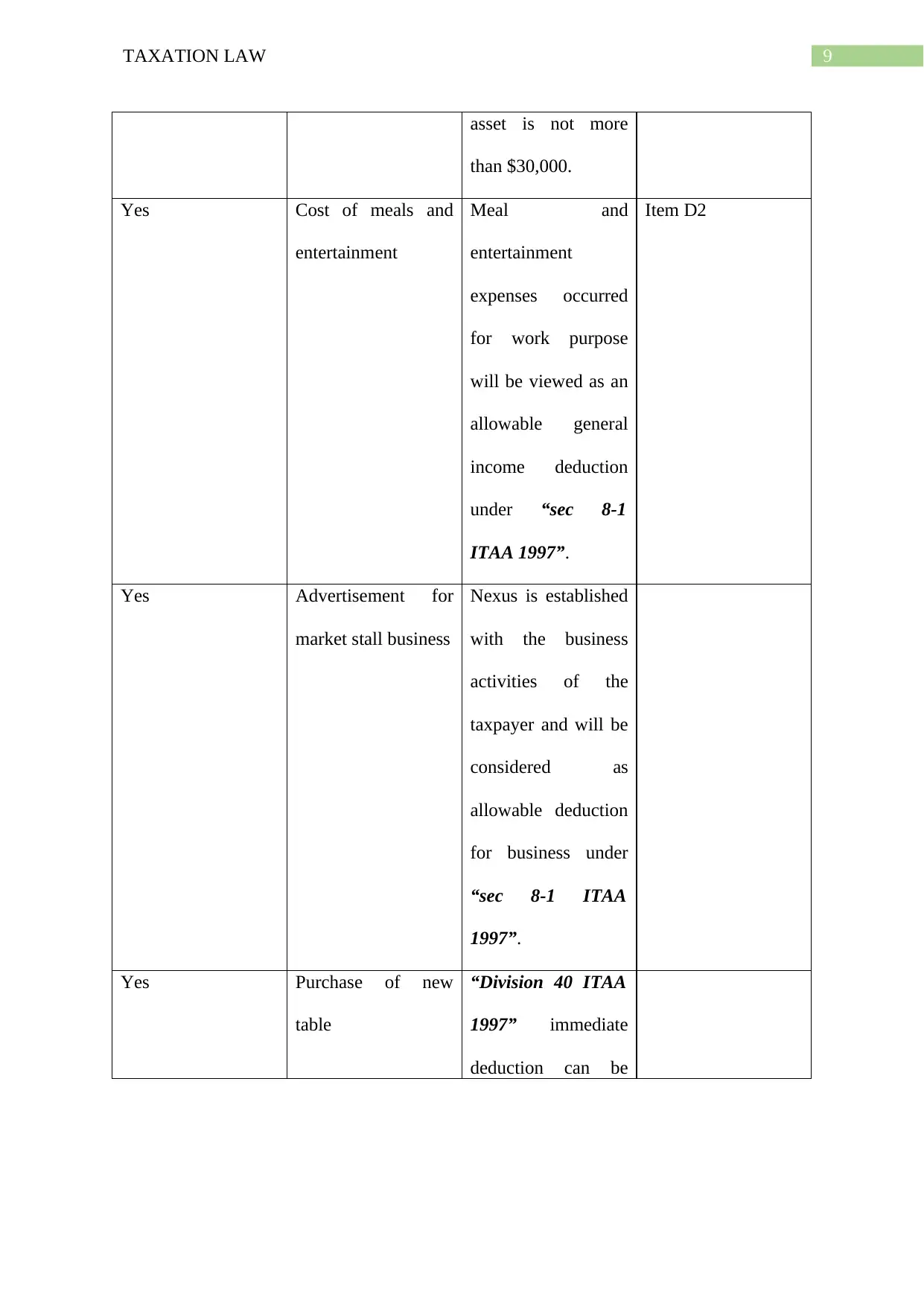

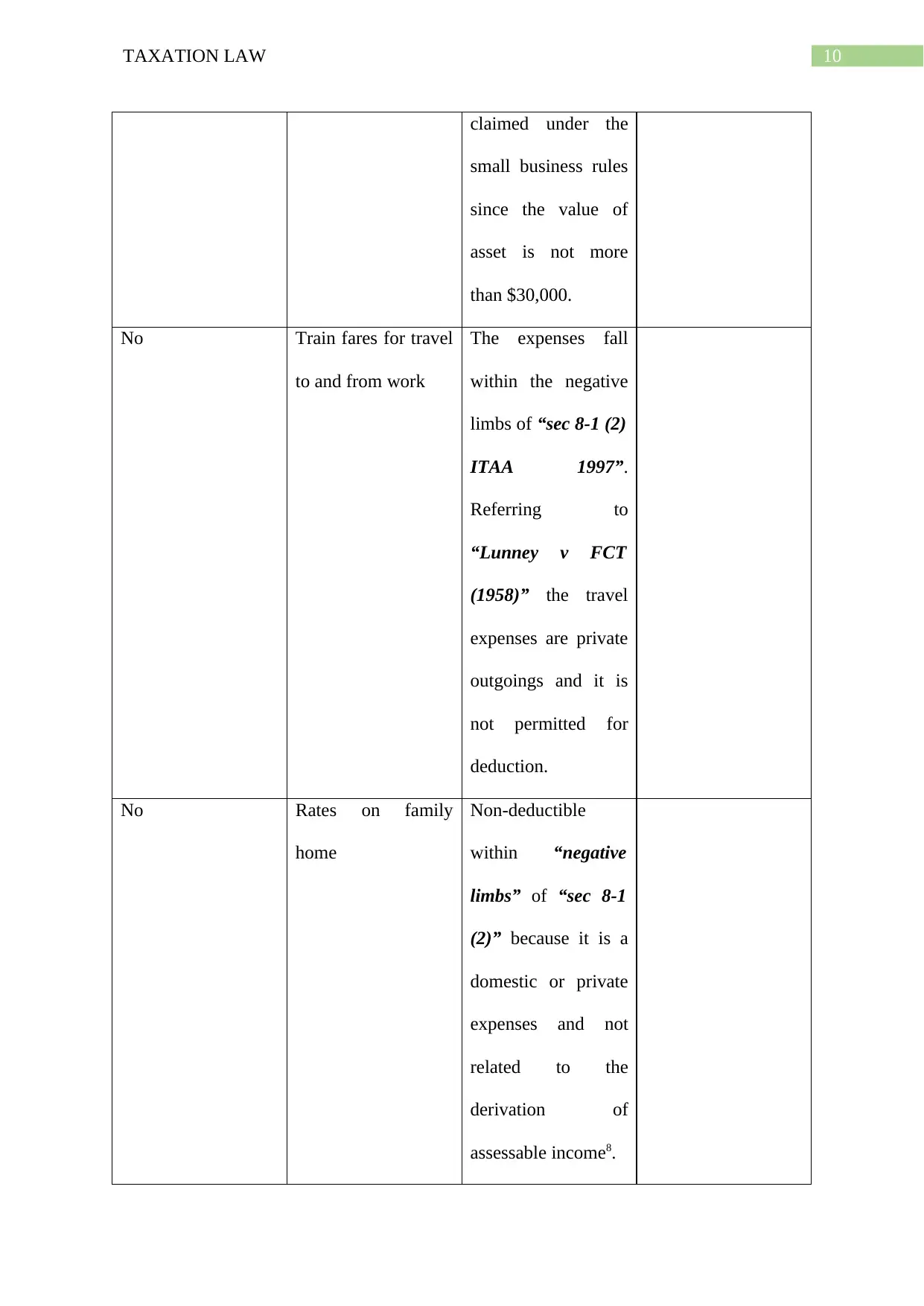

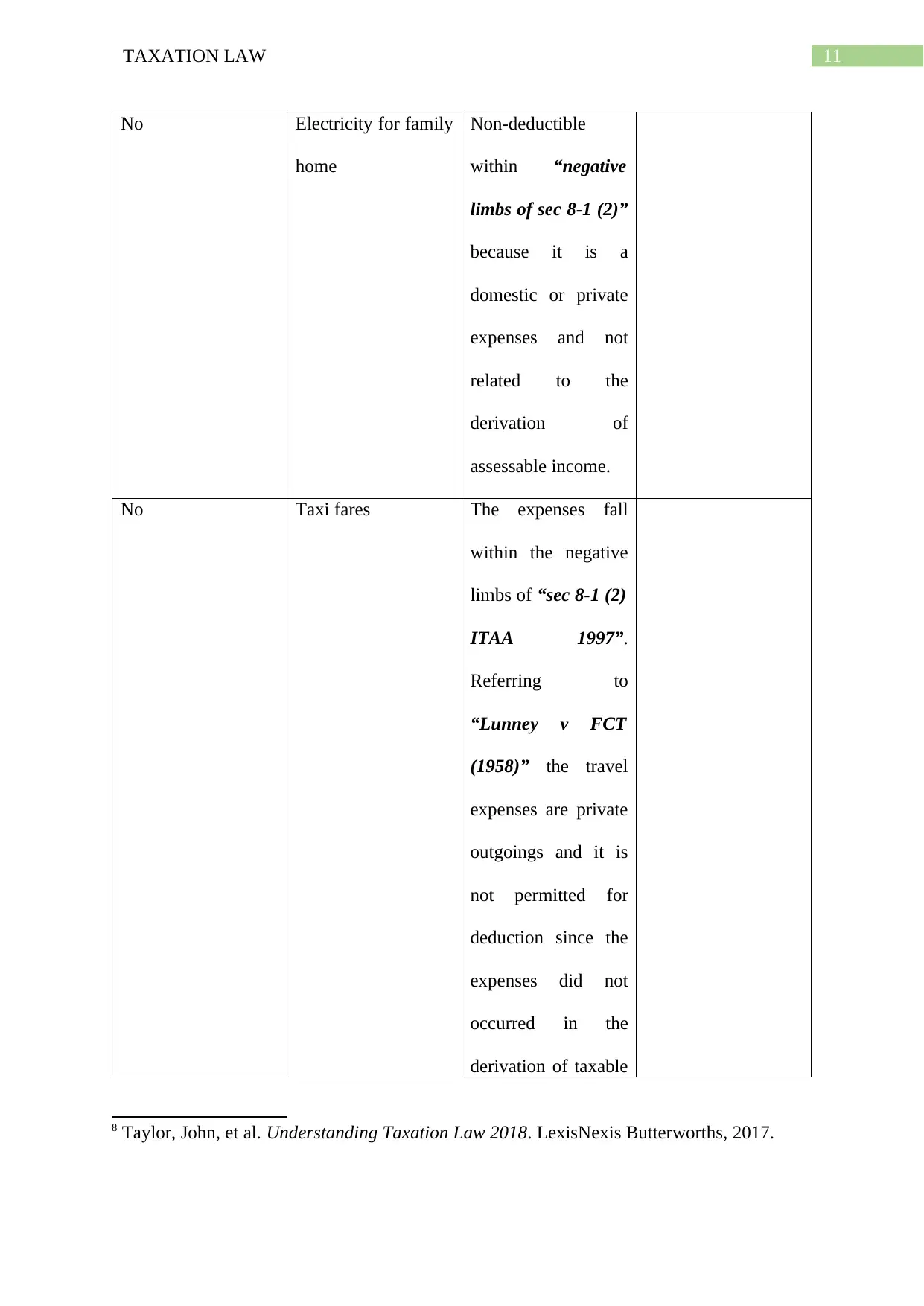

This document presents a comprehensive solution to a taxation law assignment, addressing both income assessment and residency determination. Part A of the assignment meticulously analyzes Harry's various income sources and expenses for the financial year ending June 30, 2019, classifying each item as assessable income or deductible expense and providing detailed reasoning based on relevant legislation, case law, and rulings. The analysis covers diverse income types, including sales of paintings, salary, interest, capital gains from the sale of shares and motor vehicles, and a lottery win, as well as various expenses like rent, purchase of paintings, bookkeeping fees, advertising, and travel expenses. Part B delves into the complex issue of Harry's residency status, considering his potential work outside of Australia for an extended period. It examines the relevant rules and tests outlined in the Income Tax Assessment Act 1936 (ITAA 1936), including the resides test, domicile test, 183-day test, and the Commonwealth superannuation fund test, while also considering the implications of the Harding v Commissioner of Taxation [2019] FCAFC 29 case. The solution provides a detailed application of these rules to Harry's situation, considering factors such as his intentions, family ties, and financial connections to Australia. The document concludes with an analysis of the potential consequences of Harry's decision to work overseas and its effect on his Australian tax residency.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.