UOB and OCBC Bank Financial Performance: A Management Services Study

VerifiedAdded on 2023/06/11

|11

|2584

|75

Report

AI Summary

This report offers a comparative analysis of United Overseas Bank (UOB) and Oversea-Chinese Banking Corporation (OCBC), evaluating their market performance based on profitability, credit position, liquidity, efficiency, and leverage. It examines ownership governance, net interest income, and non-interest income to assess overall performance. Key metrics like return on equity, return on assets, net interest margin, non-performing loan rates, and loan-to-deposit ratios are analyzed. The report finds that OCBC generally outperforms UOB in profitability and efficiency, while UOB demonstrates better liquidity management. Credit risk management appears stronger at UOB, though OCBC shows higher specific allowances. Ultimately, the report concludes that both banks exhibit strong financial policies, with OCBC showing superior profitability and UOB demonstrating better risk and liquidity management. Desklib provides access to this and other solved assignments for students.

Running Head: Bank management and financial services

1

UOB and OCBC

18

Bank management and

financial services

Comparative study

Student’s Name

1

UOB and OCBC

18

Bank management and

financial services

Comparative study

Student’s Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank management and financial services 2

Executive summary

In the report, UNITED OVERSEAS BANK LTD and OVERSEA-CHINESE

BANKING CORP LTD has been evaluated to identify the performance of both the banks in

the market on the basis of their profitability, credit position, liquidity level and efficiency and

leverage level of the company. The ownership governance structure and net revenue of both

the banks have also been evaluated to measure the entire performance of banks. The report

explains that the performance of OCBC bank is better than UOB bank.

Executive summary

In the report, UNITED OVERSEAS BANK LTD and OVERSEA-CHINESE

BANKING CORP LTD has been evaluated to identify the performance of both the banks in

the market on the basis of their profitability, credit position, liquidity level and efficiency and

leverage level of the company. The ownership governance structure and net revenue of both

the banks have also been evaluated to measure the entire performance of banks. The report

explains that the performance of OCBC bank is better than UOB bank.

Bank management and financial services 3

Contents

Background:......................................................................................................................4

Major shareholders:..........................................................................................................4

Bank’s net interest income and non-interest income:.......................................................6

Profitability ratio:..............................................................................................................6

Return on equity:..........................................................................................................6

Return on assets:...........................................................................................................7

Net interest margin:......................................................................................................7

Credit risk ratio:................................................................................................................7

Nonperforming loan rate:.............................................................................................8

Specific allowance / average loans:..............................................................................8

Liquidity risk ratio:...........................................................................................................8

Loan to deposit ratio:....................................................................................................8

Total customer’s deposit to total liabilities:..................................................................9

Other ratio:........................................................................................................................9

Efficiency ratio:............................................................................................................9

Leverage ratio:............................................................................................................10

Comparing UOB and OCBC:.........................................................................................10

References:.....................................................................................................................11

Contents

Background:......................................................................................................................4

Major shareholders:..........................................................................................................4

Bank’s net interest income and non-interest income:.......................................................6

Profitability ratio:..............................................................................................................6

Return on equity:..........................................................................................................6

Return on assets:...........................................................................................................7

Net interest margin:......................................................................................................7

Credit risk ratio:................................................................................................................7

Nonperforming loan rate:.............................................................................................8

Specific allowance / average loans:..............................................................................8

Liquidity risk ratio:...........................................................................................................8

Loan to deposit ratio:....................................................................................................8

Total customer’s deposit to total liabilities:..................................................................9

Other ratio:........................................................................................................................9

Efficiency ratio:............................................................................................................9

Leverage ratio:............................................................................................................10

Comparing UOB and OCBC:.........................................................................................10

References:.....................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank management and financial services 4

Background:

Managing the financial performance of an organization is quote crucial as it helped the

stakeholders and the other parties of the company to make better decision about the

performance of the company and compare among 2 or more companies to identify the

performance of the company. Financial performance of an organization could be evaluated on

the basis of the various financial items and the annual report of the company (Weston and

Brigham, 2015).

United overseas bank limited is a Singapore bank which is listed in SGX. The

company offers the financial services and investment banking services. The bank has been

founded as United Chinese bank is 1935. The bank is among the third largest bank in the area

of the south east (Home, 2018). The main services of the bank include corporate banking

services, private banking services, personal financial services, management services,

corporate finance etc.

Further, OCBC bank is also a public listen bank in Singapore stock exchange. The main

products of the company includes corporate banking services, private banking services,

personal financial services, management services, corporate finance etc. the main area of

business of the bank is East Asia and south east Asia (Home, 2018). The main mission of the

company is to grab more market to enhance the market base and revenues of the bank.

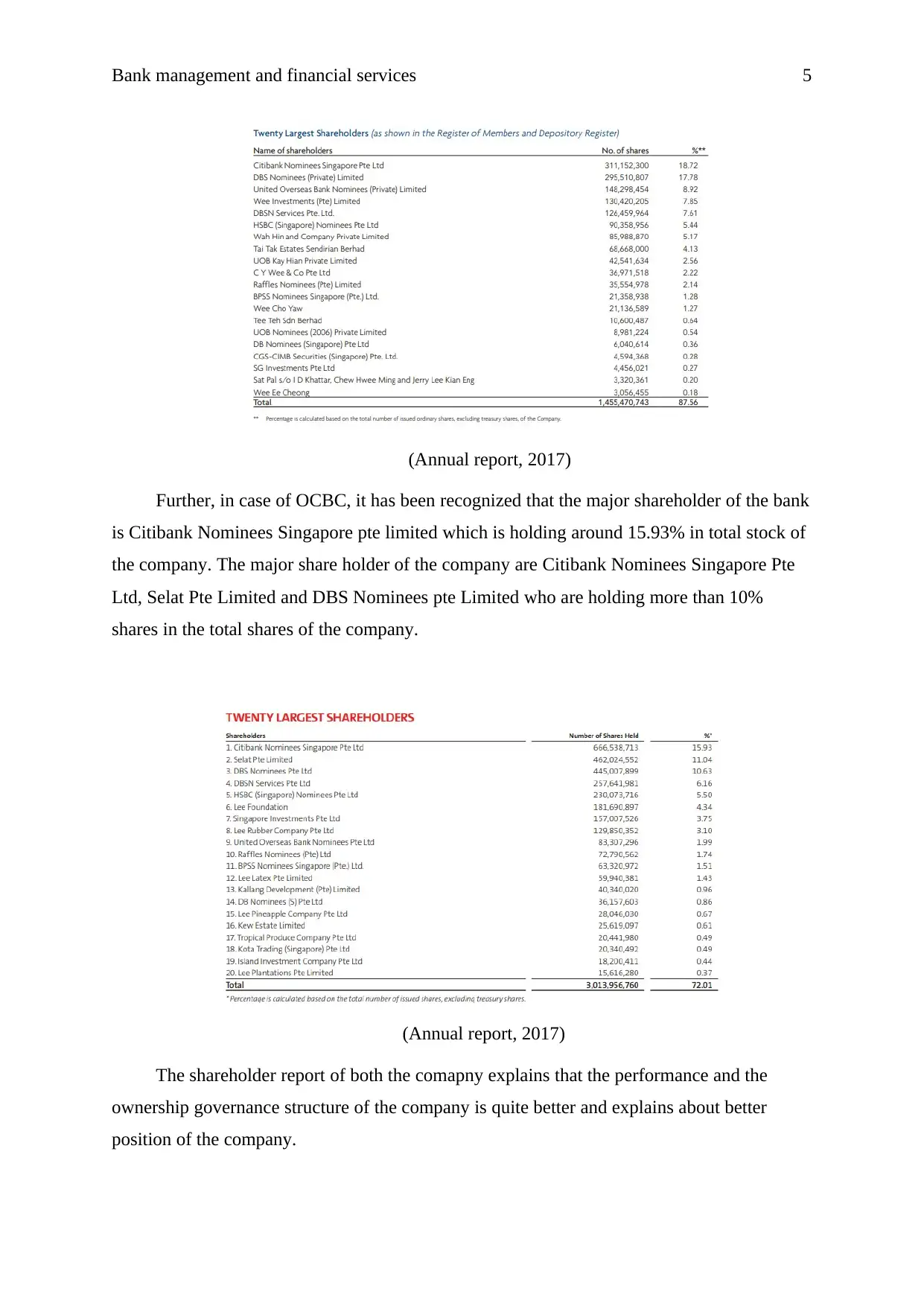

Major shareholders:

Major shareholders explain about those investors who has invested into the equity

shares of the company and currently they are holding huge number of shares of the company.

In case of UNITED OVERSEAS BANK LTD, it has been recognized that the major

shareholder of the bank is Citibank Nominees Singapore pte limited which is holding around

18.72% in total stock of the company. The major share holder of the company are Citibank

Nominees Singapore Pte Ltd and DBS Nominees (Private) Limited who are holding more

than 15% in the total shares of the company.

Background:

Managing the financial performance of an organization is quote crucial as it helped the

stakeholders and the other parties of the company to make better decision about the

performance of the company and compare among 2 or more companies to identify the

performance of the company. Financial performance of an organization could be evaluated on

the basis of the various financial items and the annual report of the company (Weston and

Brigham, 2015).

United overseas bank limited is a Singapore bank which is listed in SGX. The

company offers the financial services and investment banking services. The bank has been

founded as United Chinese bank is 1935. The bank is among the third largest bank in the area

of the south east (Home, 2018). The main services of the bank include corporate banking

services, private banking services, personal financial services, management services,

corporate finance etc.

Further, OCBC bank is also a public listen bank in Singapore stock exchange. The main

products of the company includes corporate banking services, private banking services,

personal financial services, management services, corporate finance etc. the main area of

business of the bank is East Asia and south east Asia (Home, 2018). The main mission of the

company is to grab more market to enhance the market base and revenues of the bank.

Major shareholders:

Major shareholders explain about those investors who has invested into the equity

shares of the company and currently they are holding huge number of shares of the company.

In case of UNITED OVERSEAS BANK LTD, it has been recognized that the major

shareholder of the bank is Citibank Nominees Singapore pte limited which is holding around

18.72% in total stock of the company. The major share holder of the company are Citibank

Nominees Singapore Pte Ltd and DBS Nominees (Private) Limited who are holding more

than 15% in the total shares of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank management and financial services 5

(Annual report, 2017)

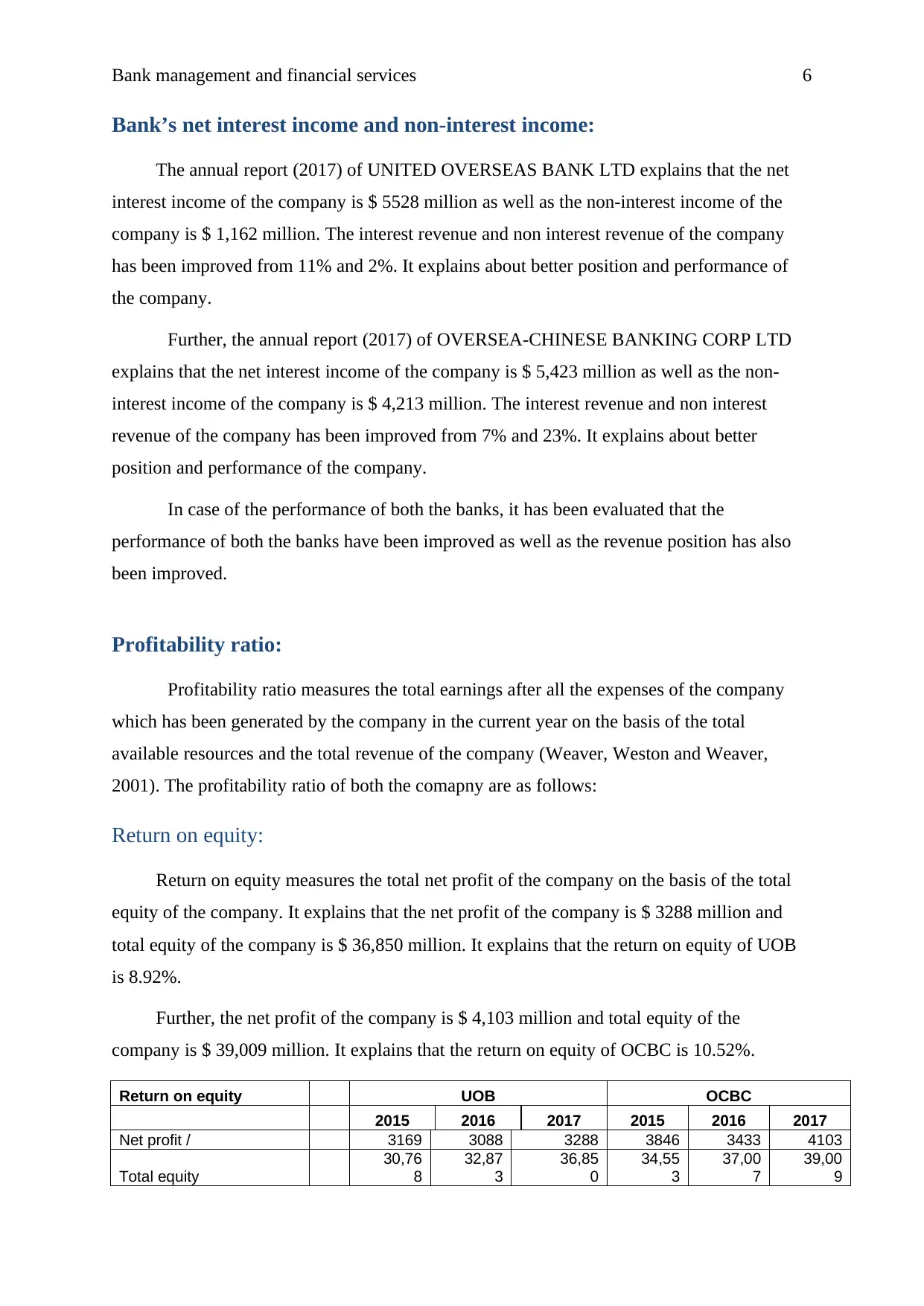

Further, in case of OCBC, it has been recognized that the major shareholder of the bank

is Citibank Nominees Singapore pte limited which is holding around 15.93% in total stock of

the company. The major share holder of the company are Citibank Nominees Singapore Pte

Ltd, Selat Pte Limited and DBS Nominees pte Limited who are holding more than 10%

shares in the total shares of the company.

(Annual report, 2017)

The shareholder report of both the comapny explains that the performance and the

ownership governance structure of the company is quite better and explains about better

position of the company.

(Annual report, 2017)

Further, in case of OCBC, it has been recognized that the major shareholder of the bank

is Citibank Nominees Singapore pte limited which is holding around 15.93% in total stock of

the company. The major share holder of the company are Citibank Nominees Singapore Pte

Ltd, Selat Pte Limited and DBS Nominees pte Limited who are holding more than 10%

shares in the total shares of the company.

(Annual report, 2017)

The shareholder report of both the comapny explains that the performance and the

ownership governance structure of the company is quite better and explains about better

position of the company.

Bank management and financial services 6

Bank’s net interest income and non-interest income:

The annual report (2017) of UNITED OVERSEAS BANK LTD explains that the net

interest income of the company is $ 5528 million as well as the non-interest income of the

company is $ 1,162 million. The interest revenue and non interest revenue of the company

has been improved from 11% and 2%. It explains about better position and performance of

the company.

Further, the annual report (2017) of OVERSEA-CHINESE BANKING CORP LTD

explains that the net interest income of the company is $ 5,423 million as well as the non-

interest income of the company is $ 4,213 million. The interest revenue and non interest

revenue of the company has been improved from 7% and 23%. It explains about better

position and performance of the company.

In case of the performance of both the banks, it has been evaluated that the

performance of both the banks have been improved as well as the revenue position has also

been improved.

Profitability ratio:

Profitability ratio measures the total earnings after all the expenses of the company

which has been generated by the company in the current year on the basis of the total

available resources and the total revenue of the company (Weaver, Weston and Weaver,

2001). The profitability ratio of both the comapny are as follows:

Return on equity:

Return on equity measures the total net profit of the company on the basis of the total

equity of the company. It explains that the net profit of the company is $ 3288 million and

total equity of the company is $ 36,850 million. It explains that the return on equity of UOB

is 8.92%.

Further, the net profit of the company is $ 4,103 million and total equity of the

company is $ 39,009 million. It explains that the return on equity of OCBC is 10.52%.

Return on equity UOB OCBC

2015 2016 2017 2015 2016 2017

Net profit / 3169 3088 3288 3846 3433 4103

Total equity

30,76

8

32,87

3

36,85

0

34,55

3

37,00

7

39,00

9

Bank’s net interest income and non-interest income:

The annual report (2017) of UNITED OVERSEAS BANK LTD explains that the net

interest income of the company is $ 5528 million as well as the non-interest income of the

company is $ 1,162 million. The interest revenue and non interest revenue of the company

has been improved from 11% and 2%. It explains about better position and performance of

the company.

Further, the annual report (2017) of OVERSEA-CHINESE BANKING CORP LTD

explains that the net interest income of the company is $ 5,423 million as well as the non-

interest income of the company is $ 4,213 million. The interest revenue and non interest

revenue of the company has been improved from 7% and 23%. It explains about better

position and performance of the company.

In case of the performance of both the banks, it has been evaluated that the

performance of both the banks have been improved as well as the revenue position has also

been improved.

Profitability ratio:

Profitability ratio measures the total earnings after all the expenses of the company

which has been generated by the company in the current year on the basis of the total

available resources and the total revenue of the company (Weaver, Weston and Weaver,

2001). The profitability ratio of both the comapny are as follows:

Return on equity:

Return on equity measures the total net profit of the company on the basis of the total

equity of the company. It explains that the net profit of the company is $ 3288 million and

total equity of the company is $ 36,850 million. It explains that the return on equity of UOB

is 8.92%.

Further, the net profit of the company is $ 4,103 million and total equity of the

company is $ 39,009 million. It explains that the return on equity of OCBC is 10.52%.

Return on equity UOB OCBC

2015 2016 2017 2015 2016 2017

Net profit / 3169 3088 3288 3846 3433 4103

Total equity

30,76

8

32,87

3

36,85

0

34,55

3

37,00

7

39,00

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank management and financial services 7

Answer: % 10.30% 9.39% 8.92% 11.13% 9.28% 10.52%

It explains that the performance of OCBC is better than UOB.

Return on assets:

Return on assets measures the total net profit of the company on the basis of the total

assets of the company. The below table explains that the return on assets of UOB and OCBC

is 0.9% and 0.9%. It explains that the profitability position of both the banks is quite similar.

Return on assets UOB OCBC

2015 2016 2017 2015 2016 2017

Net profit / 3,169 3,088 3,288 3,846 3,433 4,103

Total assets 3,16,011 3,40,028 3,58,592 3,90,190 4,09,884 4,54,938

Answer: % 1.0% 0.9% 0.9% 1.0% 0.8% 0.9%

Net interest margin:

Further, net profit margin measures the total net profit of the company on the basis of

the total revenues of the company. The below table explains that the net profit margin of

UOB and OCBC is 36.22% and 45%. It explains that the profitability position of OCBC is

way better than UOB (Higgins, 2012).

Net profit margin UOB OCBC

2015 2016 2017 2015 2016 2017

Net profit / 3,169 3,088 3,288 3,846 3,433 4,103

Total revenue % 7,826 8,291 9,077 8,486 8,368 9,118

Answer: 40.49% 37.25% 36.22% 45.32% 41.03% 45.00%

Credit risk ratio:

Credit risk ratio is calculated on the basis of the bank’s overall ability to repay the

loan. It measures the total special allowances and non performing loan amount of the

Answer: % 10.30% 9.39% 8.92% 11.13% 9.28% 10.52%

It explains that the performance of OCBC is better than UOB.

Return on assets:

Return on assets measures the total net profit of the company on the basis of the total

assets of the company. The below table explains that the return on assets of UOB and OCBC

is 0.9% and 0.9%. It explains that the profitability position of both the banks is quite similar.

Return on assets UOB OCBC

2015 2016 2017 2015 2016 2017

Net profit / 3,169 3,088 3,288 3,846 3,433 4,103

Total assets 3,16,011 3,40,028 3,58,592 3,90,190 4,09,884 4,54,938

Answer: % 1.0% 0.9% 0.9% 1.0% 0.8% 0.9%

Net interest margin:

Further, net profit margin measures the total net profit of the company on the basis of

the total revenues of the company. The below table explains that the net profit margin of

UOB and OCBC is 36.22% and 45%. It explains that the profitability position of OCBC is

way better than UOB (Higgins, 2012).

Net profit margin UOB OCBC

2015 2016 2017 2015 2016 2017

Net profit / 3,169 3,088 3,288 3,846 3,433 4,103

Total revenue % 7,826 8,291 9,077 8,486 8,368 9,118

Answer: 40.49% 37.25% 36.22% 45.32% 41.03% 45.00%

Credit risk ratio:

Credit risk ratio is calculated on the basis of the bank’s overall ability to repay the

loan. It measures the total special allowances and non performing loan amount of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank management and financial services 8

company on the basis of the total loan of the company (Lord, 2007). The credit risk ratio of

both the comapny are as follows:

Nonperforming loan rate:

Non performing loan rate ratio explains that the risk factor of OCBC is higher than

the UOB as the debtors of the company are not paying the debt amount to OCBC on time and

it is enhancing the credit risk of the bank.

Non-performing loan

rate UOB OCBC

2015 2016 2017 2015 2016 2017

Non-performing loan / 2,699 2,750 1,855 1,969 2,783 3,415

Total loan % 2,03,611 2,21,734 2,32,212 2,08,218 2,16,830 2,34,141

Answer: 1.33% 1.24% 0.80% 0.95% 1.28% 1.46%

Specific allowance / average loans:

Specific allowance / average loan ratio explains that the risk factor of OCBC is lower

than the UOB as the allowances and provisions of the company are quite higher in context

with the specific allowances of the company.

Specific allowance / average

loans UOB OCBC

2015 2016 2017 2015 2016 2017

Specific allownace / 1,609 1,754 1,407 -360 -616 1,236

Average loans %

2,03,61

1

2,21,73

4

2,32,21

2

2,08,21

8

2,16,83

0

2,34,14

1

Answer: (note the above needs to be x

365) 0.79% 0.79% 0.61% -0.17% -0.28% 0.53%

(Hillier, Grinblatt and Titman, 2011)

It explains that the credit risk of OCBC is higher and the bank is required to prepare

few new policies to manage the credit risk.

Liquidity risk ratio:

Liquidity risk ratio is calculated on the basis of the loan amount, liabilities and the

customer’s deposit of the company to measure the liquid ability of the bank. It measures that

whether the bank would be able to meet all the short term debt obligations (Lumby and Jones,

2007). The liquidity risk ratio of both the comapny are as follows:

company on the basis of the total loan of the company (Lord, 2007). The credit risk ratio of

both the comapny are as follows:

Nonperforming loan rate:

Non performing loan rate ratio explains that the risk factor of OCBC is higher than

the UOB as the debtors of the company are not paying the debt amount to OCBC on time and

it is enhancing the credit risk of the bank.

Non-performing loan

rate UOB OCBC

2015 2016 2017 2015 2016 2017

Non-performing loan / 2,699 2,750 1,855 1,969 2,783 3,415

Total loan % 2,03,611 2,21,734 2,32,212 2,08,218 2,16,830 2,34,141

Answer: 1.33% 1.24% 0.80% 0.95% 1.28% 1.46%

Specific allowance / average loans:

Specific allowance / average loan ratio explains that the risk factor of OCBC is lower

than the UOB as the allowances and provisions of the company are quite higher in context

with the specific allowances of the company.

Specific allowance / average

loans UOB OCBC

2015 2016 2017 2015 2016 2017

Specific allownace / 1,609 1,754 1,407 -360 -616 1,236

Average loans %

2,03,61

1

2,21,73

4

2,32,21

2

2,08,21

8

2,16,83

0

2,34,14

1

Answer: (note the above needs to be x

365) 0.79% 0.79% 0.61% -0.17% -0.28% 0.53%

(Hillier, Grinblatt and Titman, 2011)

It explains that the credit risk of OCBC is higher and the bank is required to prepare

few new policies to manage the credit risk.

Liquidity risk ratio:

Liquidity risk ratio is calculated on the basis of the loan amount, liabilities and the

customer’s deposit of the company to measure the liquid ability of the bank. It measures that

whether the bank would be able to meet all the short term debt obligations (Lumby and Jones,

2007). The liquidity risk ratio of both the comapny are as follows:

Bank management and financial services 9

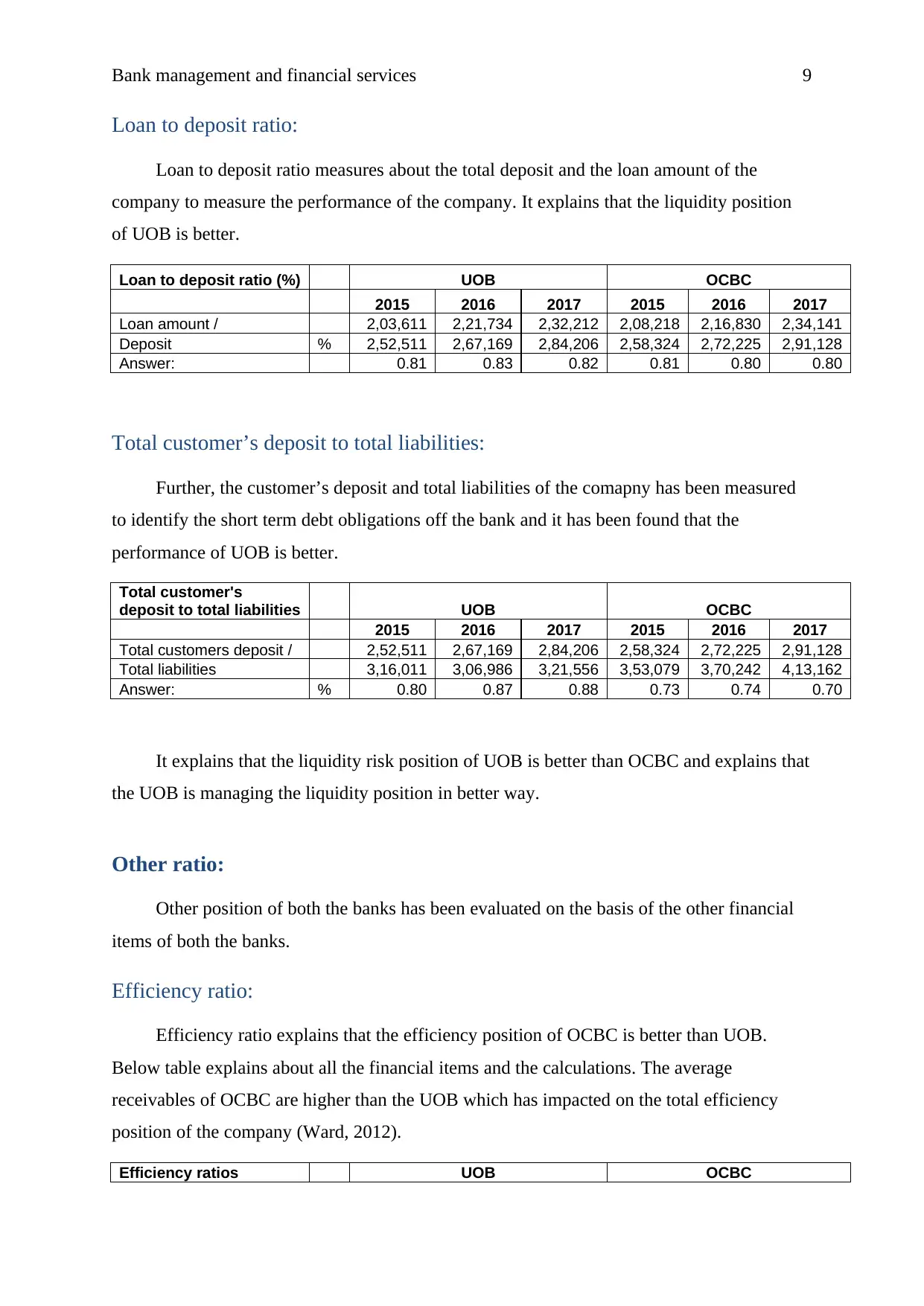

Loan to deposit ratio:

Loan to deposit ratio measures about the total deposit and the loan amount of the

company to measure the performance of the company. It explains that the liquidity position

of UOB is better.

Loan to deposit ratio (%) UOB OCBC

2015 2016 2017 2015 2016 2017

Loan amount / 2,03,611 2,21,734 2,32,212 2,08,218 2,16,830 2,34,141

Deposit % 2,52,511 2,67,169 2,84,206 2,58,324 2,72,225 2,91,128

Answer: 0.81 0.83 0.82 0.81 0.80 0.80

Total customer’s deposit to total liabilities:

Further, the customer’s deposit and total liabilities of the comapny has been measured

to identify the short term debt obligations off the bank and it has been found that the

performance of UOB is better.

Total customer's

deposit to total liabilities UOB OCBC

2015 2016 2017 2015 2016 2017

Total customers deposit / 2,52,511 2,67,169 2,84,206 2,58,324 2,72,225 2,91,128

Total liabilities 3,16,011 3,06,986 3,21,556 3,53,079 3,70,242 4,13,162

Answer: % 0.80 0.87 0.88 0.73 0.74 0.70

It explains that the liquidity risk position of UOB is better than OCBC and explains that

the UOB is managing the liquidity position in better way.

Other ratio:

Other position of both the banks has been evaluated on the basis of the other financial

items of both the banks.

Efficiency ratio:

Efficiency ratio explains that the efficiency position of OCBC is better than UOB.

Below table explains about all the financial items and the calculations. The average

receivables of OCBC are higher than the UOB which has impacted on the total efficiency

position of the company (Ward, 2012).

Efficiency ratios UOB OCBC

Loan to deposit ratio:

Loan to deposit ratio measures about the total deposit and the loan amount of the

company to measure the performance of the company. It explains that the liquidity position

of UOB is better.

Loan to deposit ratio (%) UOB OCBC

2015 2016 2017 2015 2016 2017

Loan amount / 2,03,611 2,21,734 2,32,212 2,08,218 2,16,830 2,34,141

Deposit % 2,52,511 2,67,169 2,84,206 2,58,324 2,72,225 2,91,128

Answer: 0.81 0.83 0.82 0.81 0.80 0.80

Total customer’s deposit to total liabilities:

Further, the customer’s deposit and total liabilities of the comapny has been measured

to identify the short term debt obligations off the bank and it has been found that the

performance of UOB is better.

Total customer's

deposit to total liabilities UOB OCBC

2015 2016 2017 2015 2016 2017

Total customers deposit / 2,52,511 2,67,169 2,84,206 2,58,324 2,72,225 2,91,128

Total liabilities 3,16,011 3,06,986 3,21,556 3,53,079 3,70,242 4,13,162

Answer: % 0.80 0.87 0.88 0.73 0.74 0.70

It explains that the liquidity risk position of UOB is better than OCBC and explains that

the UOB is managing the liquidity position in better way.

Other ratio:

Other position of both the banks has been evaluated on the basis of the other financial

items of both the banks.

Efficiency ratio:

Efficiency ratio explains that the efficiency position of OCBC is better than UOB.

Below table explains about all the financial items and the calculations. The average

receivables of OCBC are higher than the UOB which has impacted on the total efficiency

position of the company (Ward, 2012).

Efficiency ratios UOB OCBC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank management and financial services 10

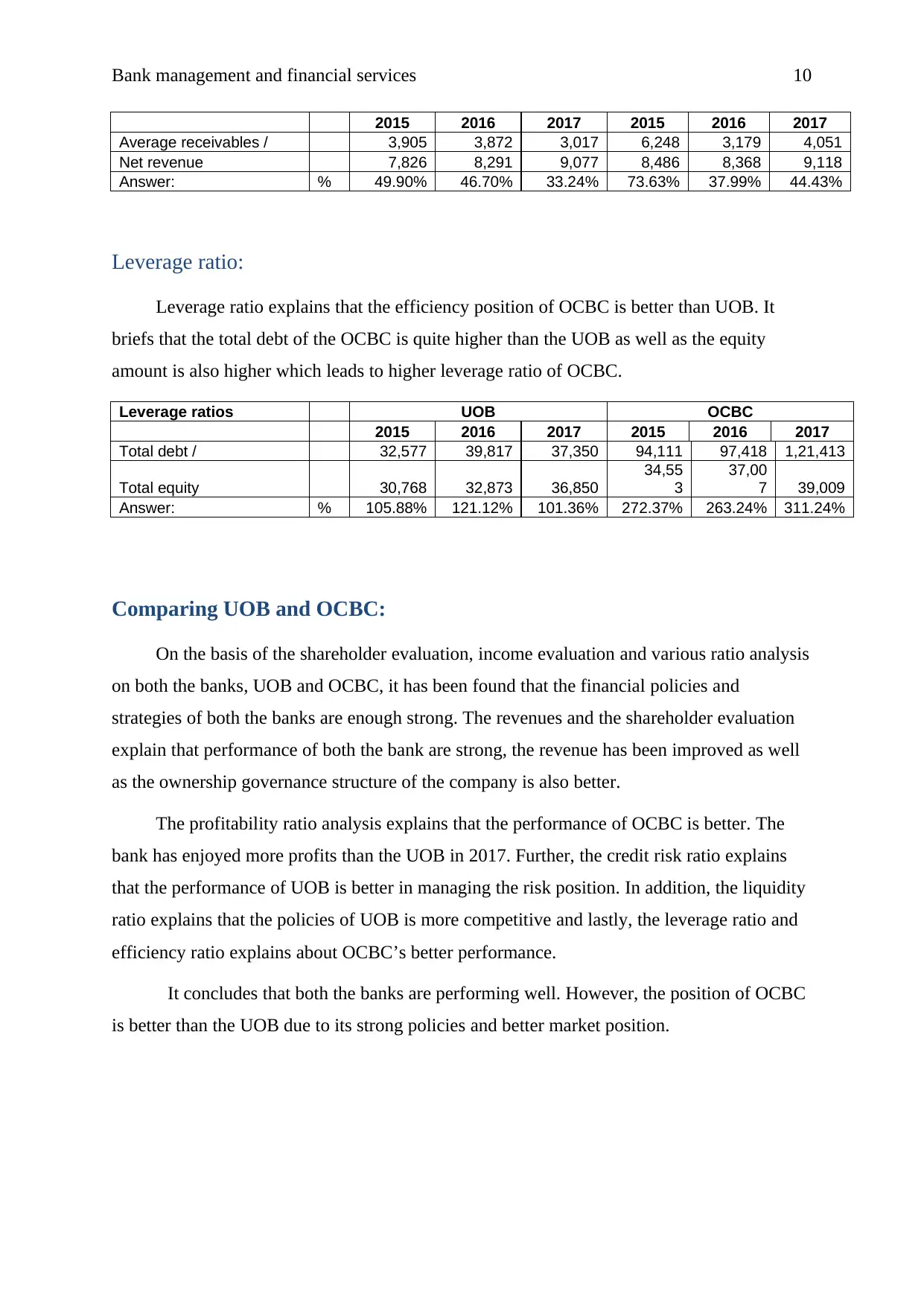

2015 2016 2017 2015 2016 2017

Average receivables / 3,905 3,872 3,017 6,248 3,179 4,051

Net revenue 7,826 8,291 9,077 8,486 8,368 9,118

Answer: % 49.90% 46.70% 33.24% 73.63% 37.99% 44.43%

Leverage ratio:

Leverage ratio explains that the efficiency position of OCBC is better than UOB. It

briefs that the total debt of the OCBC is quite higher than the UOB as well as the equity

amount is also higher which leads to higher leverage ratio of OCBC.

Leverage ratios UOB OCBC

2015 2016 2017 2015 2016 2017

Total debt / 32,577 39,817 37,350 94,111 97,418 1,21,413

Total equity 30,768 32,873 36,850

34,55

3

37,00

7 39,009

Answer: % 105.88% 121.12% 101.36% 272.37% 263.24% 311.24%

Comparing UOB and OCBC:

On the basis of the shareholder evaluation, income evaluation and various ratio analysis

on both the banks, UOB and OCBC, it has been found that the financial policies and

strategies of both the banks are enough strong. The revenues and the shareholder evaluation

explain that performance of both the bank are strong, the revenue has been improved as well

as the ownership governance structure of the company is also better.

The profitability ratio analysis explains that the performance of OCBC is better. The

bank has enjoyed more profits than the UOB in 2017. Further, the credit risk ratio explains

that the performance of UOB is better in managing the risk position. In addition, the liquidity

ratio explains that the policies of UOB is more competitive and lastly, the leverage ratio and

efficiency ratio explains about OCBC’s better performance.

It concludes that both the banks are performing well. However, the position of OCBC

is better than the UOB due to its strong policies and better market position.

2015 2016 2017 2015 2016 2017

Average receivables / 3,905 3,872 3,017 6,248 3,179 4,051

Net revenue 7,826 8,291 9,077 8,486 8,368 9,118

Answer: % 49.90% 46.70% 33.24% 73.63% 37.99% 44.43%

Leverage ratio:

Leverage ratio explains that the efficiency position of OCBC is better than UOB. It

briefs that the total debt of the OCBC is quite higher than the UOB as well as the equity

amount is also higher which leads to higher leverage ratio of OCBC.

Leverage ratios UOB OCBC

2015 2016 2017 2015 2016 2017

Total debt / 32,577 39,817 37,350 94,111 97,418 1,21,413

Total equity 30,768 32,873 36,850

34,55

3

37,00

7 39,009

Answer: % 105.88% 121.12% 101.36% 272.37% 263.24% 311.24%

Comparing UOB and OCBC:

On the basis of the shareholder evaluation, income evaluation and various ratio analysis

on both the banks, UOB and OCBC, it has been found that the financial policies and

strategies of both the banks are enough strong. The revenues and the shareholder evaluation

explain that performance of both the bank are strong, the revenue has been improved as well

as the ownership governance structure of the company is also better.

The profitability ratio analysis explains that the performance of OCBC is better. The

bank has enjoyed more profits than the UOB in 2017. Further, the credit risk ratio explains

that the performance of UOB is better in managing the risk position. In addition, the liquidity

ratio explains that the policies of UOB is more competitive and lastly, the leverage ratio and

efficiency ratio explains about OCBC’s better performance.

It concludes that both the banks are performing well. However, the position of OCBC

is better than the UOB due to its strong policies and better market position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank management and financial services 11

References:

Annual report. 2018. OCBC bank. [online]. Accessed on:

https://www.ocbc.com/assets/pdf/annual%20reports/2017/ocbc_ar17_fullreport_english.pdf

(available 30/5/2018).

Annual report. 2018. UOB group. [online]. Accessed on:

https://www.uob.com.sg/AR2017/documents/Full-Annual-Report-2017.pdf (available

30/5/2018).

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Home. 2018. OCBC bank. [online]. Accessed on: https://www.ocbc.com/group/group-

home.html (available 30/5/2018).

Home. 2018. UOB group. [online]. Accessed on: https://www.uobgroup.com/ (available

30/5/2018).

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3.

Lumby,S and Jones,C,.2007. Corporate finance theory & practice, 7th edition, Thomson,

London

Ward, K., 2012. Strategic management accounting. Australia: Routledge.

Weaver, S.C., Weston, J.F. and Weaver, S., 2001. Finance and accounting for nonfinancial

managers. New York: McGraw-Hill.

Weston, J.F. and Brigham, E.F., 2015. Managerial finance. Hinsdale, IL: Dryden Press.

References:

Annual report. 2018. OCBC bank. [online]. Accessed on:

https://www.ocbc.com/assets/pdf/annual%20reports/2017/ocbc_ar17_fullreport_english.pdf

(available 30/5/2018).

Annual report. 2018. UOB group. [online]. Accessed on:

https://www.uob.com.sg/AR2017/documents/Full-Annual-Report-2017.pdf (available

30/5/2018).

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hillier, D., Grinblatt, M. and Titman, S., 2011. Financial markets and corporate strategy.

McGraw Hill.

Home. 2018. OCBC bank. [online]. Accessed on: https://www.ocbc.com/group/group-

home.html (available 30/5/2018).

Home. 2018. UOB group. [online]. Accessed on: https://www.uobgroup.com/ (available

30/5/2018).

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3.

Lumby,S and Jones,C,.2007. Corporate finance theory & practice, 7th edition, Thomson,

London

Ward, K., 2012. Strategic management accounting. Australia: Routledge.

Weaver, S.C., Weston, J.F. and Weaver, S., 2001. Finance and accounting for nonfinancial

managers. New York: McGraw-Hill.

Weston, J.F. and Brigham, E.F., 2015. Managerial finance. Hinsdale, IL: Dryden Press.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.