FINA 481 Winter 2020: U.S. Banking Industry Regulation and Trends

VerifiedAdded on 2022/08/30

|8

|1856

|19

Report

AI Summary

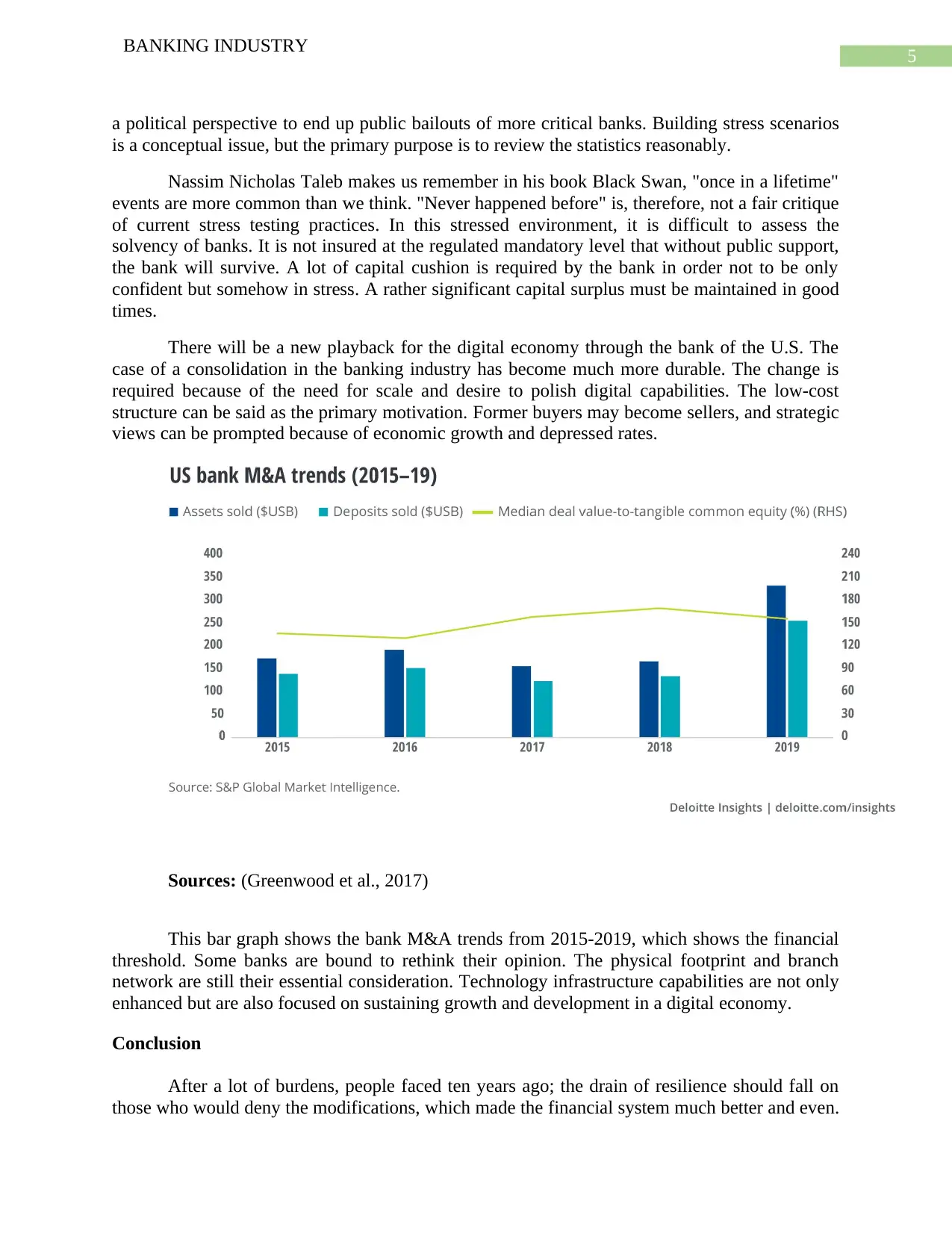

This report provides a comprehensive analysis of the U.S. banking industry. It begins with an executive summary, followed by an introduction that explores the historical context of banking regulations and the establishment of the first Bank of the U.S. The discussion section delves into the impact of the 2008 financial crisis, the Dodd-Frank Act, and the debate surrounding easing regulations on banks. The report examines the role of stress tests, capital requirements, and liquidity standards. It also includes a bar graph illustrating bank M&A trends from 2015-2019. The report concludes with a summary of key findings, emphasizing the importance of considering the benefits to society when discussing banking regulations. The references section provides sources such as Johnston (2019) and Greenwood et al. (2017), which are utilized to support the analysis. The report highlights the dynamic nature of the banking industry and the ongoing discussions surrounding regulation and its impact on the economy.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.