Comparative Analysis: US GAAP and Indian GAAP in Financial Reporting

VerifiedAdded on 2022/08/16

|12

|703

|13

Report

AI Summary

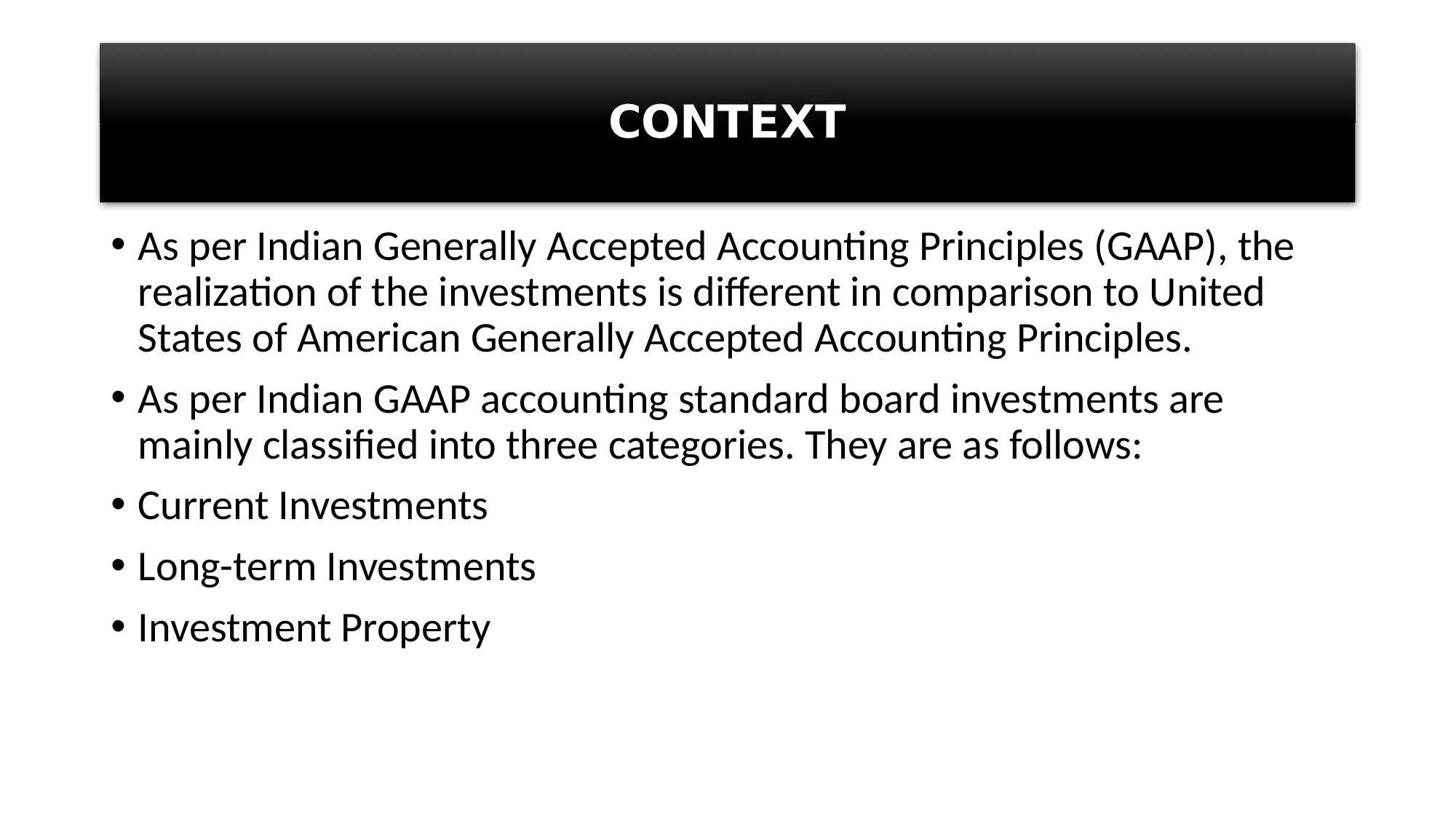

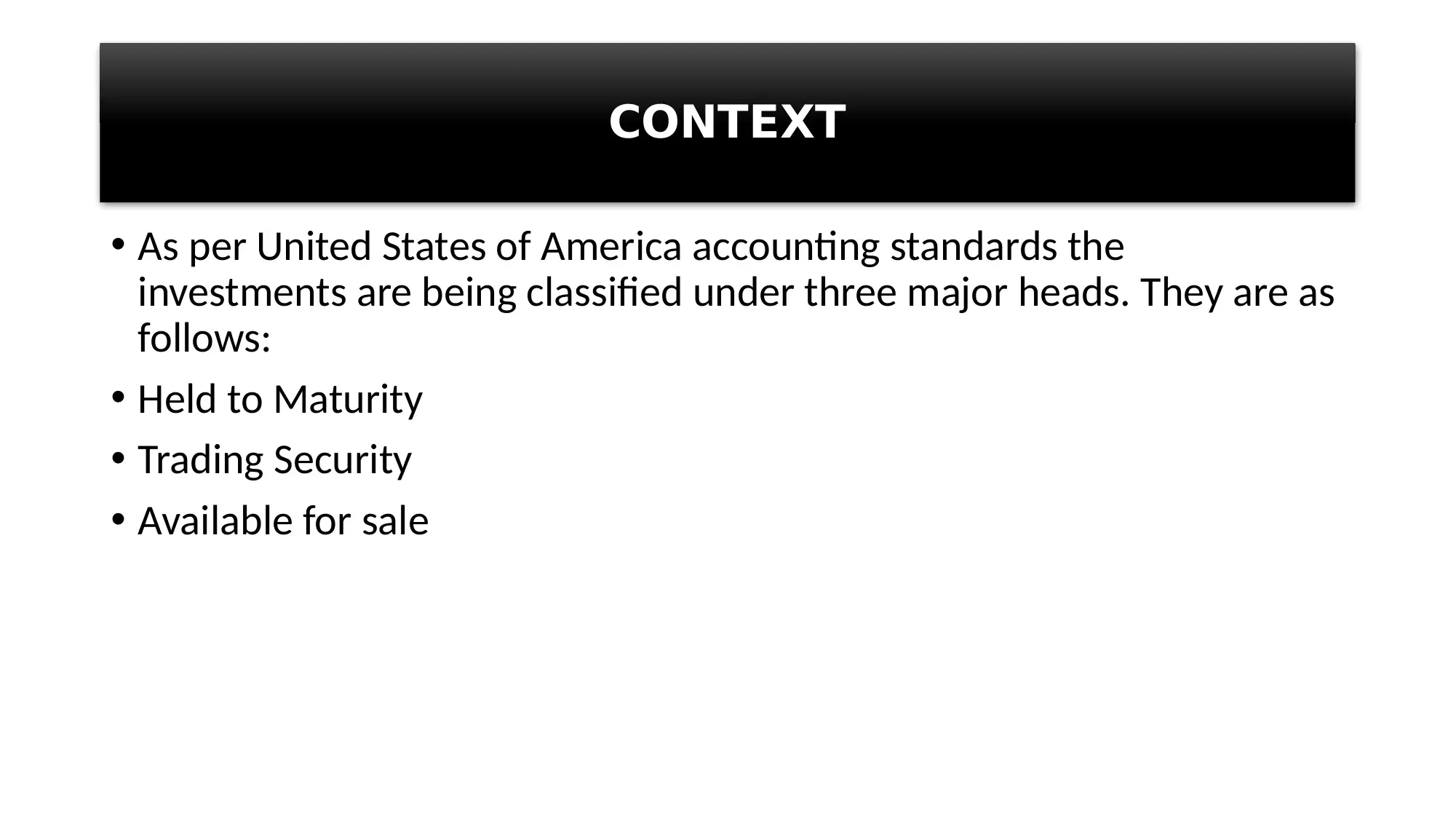

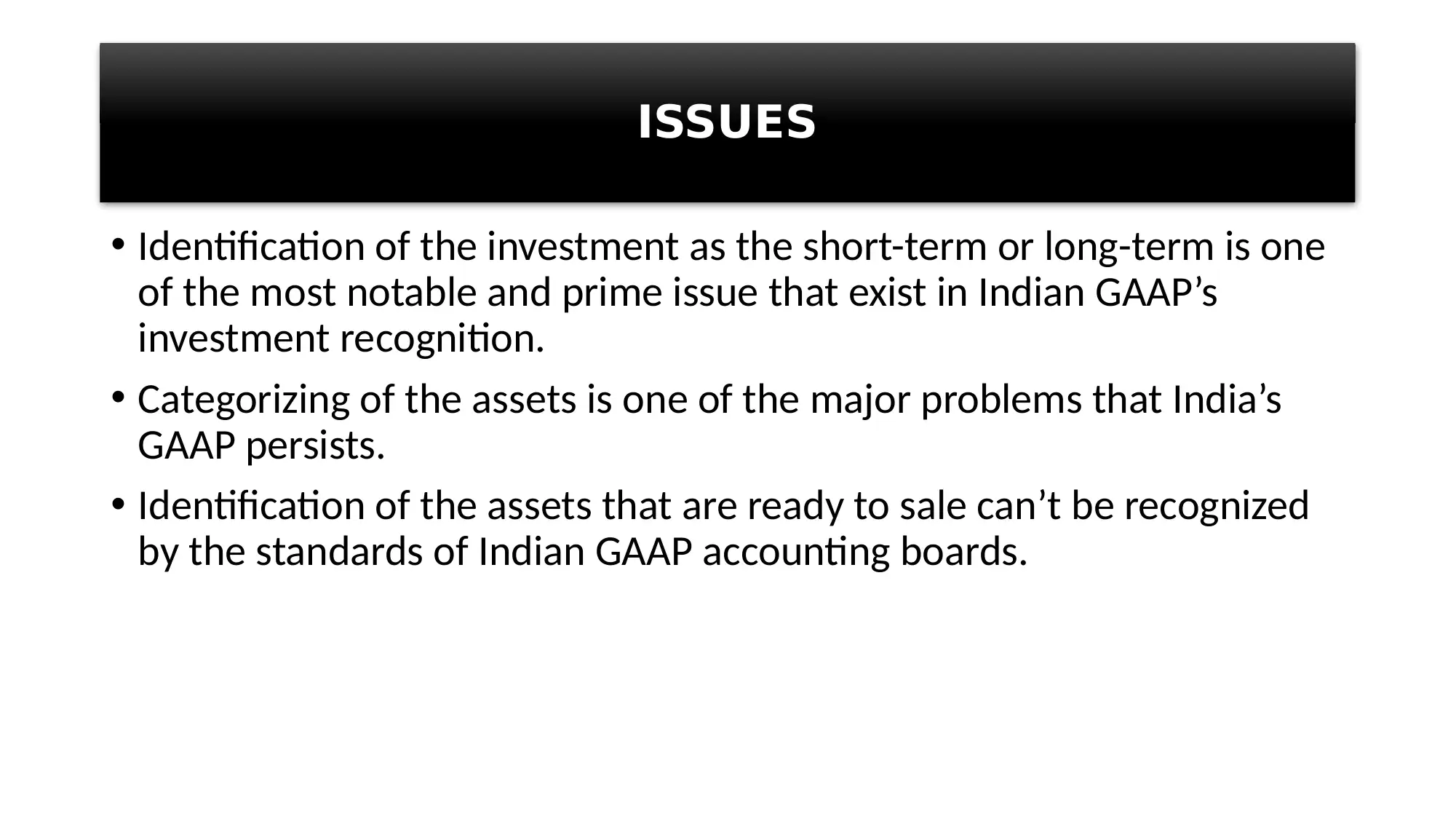

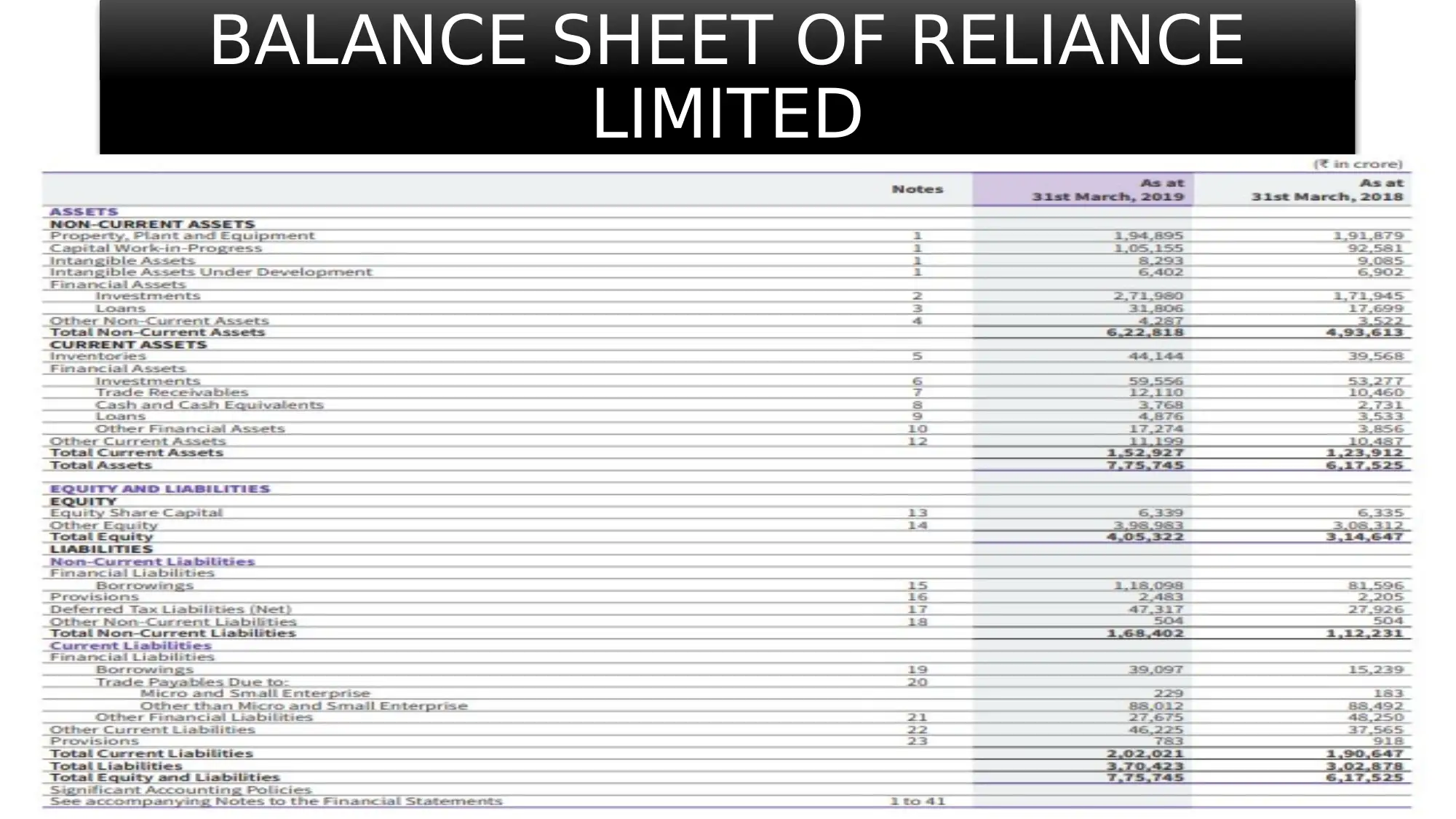

This report provides a comparative analysis of United States Generally Accepted Accounting Principles (US GAAP) and Indian Generally Accepted Accounting Principles (Indian GAAP). It highlights key differences in financial reporting, including the format of financial statements, presentation of cash flow statements, depreciation methods, and the treatment of long-term debts. A significant focus is placed on the classification and realization of investments, contrasting the approaches of both GAAP systems. The report examines the limitations of Indian GAAP, using Reliance Industries Limited as a case study, and contrasts it with the advantages of US GAAP, exemplified by Amazon.com, Inc. The report concludes that US GAAP offers a more efficient approach to investment categorization, emphasizing the importance of segregating investments based on maturity periods and sales amounts. The study references relevant academic sources to support its findings.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.