UUAC5300 Accounting & Finance: Interwood & Audit Analysis

VerifiedAdded on 2023/06/13

|18

|4424

|90

Homework Assignment

AI Summary

This accounting assignment consists of two questions. The first question discusses the differences between cash and accrual basis accounting, the responsibilities of an external auditor, the auditor's opinion on Air New Zealand's financial statements, an analysis of net profit and net cash inflow, the role of the audit committee, and contingent liabilities. The second question involves preparing a worksheet, balance sheet, and income statement for Interwood, along with a computation and analysis of net working capital. The assignment provides detailed workings and explanations for each calculation and analysis. Desklib offers a platform to explore similar solved assignments and past papers for students.

Running head: ACCOUNTING

Accounting

Name of the Student:

Student’s ID:

Lecturer’s Name:

Author’s Note

Accounting

Name of the Student:

Student’s ID:

Lecturer’s Name:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Cash Versus Accrual Basis of Accounting..................................................................................2

Responsibility of an External Auditor.........................................................................................3

Opinion of the Auditor.................................................................................................................4

Analysis of Net profit and Net Cash Inflow from Operating Activities......................................4

Audit Committee of the Company...............................................................................................5

Contingent liability......................................................................................................................5

Answer to Question 2:.....................................................................................................................6

Worksheet of Interwood..............................................................................................................6

Balance Sheet and Income Statement of Interwood....................................................................7

Computation and Analysis of Net Working Capital....................................................................9

Workings:....................................................................................................................................9

Reference.......................................................................................................................................17

ACCOUNTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Cash Versus Accrual Basis of Accounting..................................................................................2

Responsibility of an External Auditor.........................................................................................3

Opinion of the Auditor.................................................................................................................4

Analysis of Net profit and Net Cash Inflow from Operating Activities......................................4

Audit Committee of the Company...............................................................................................5

Contingent liability......................................................................................................................5

Answer to Question 2:.....................................................................................................................6

Worksheet of Interwood..............................................................................................................6

Balance Sheet and Income Statement of Interwood....................................................................7

Computation and Analysis of Net Working Capital....................................................................9

Workings:....................................................................................................................................9

Reference.......................................................................................................................................17

2

ACCOUNTING

Answer to Question 1:

Cash Versus Accrual Basis of Accounting

Cash Basis of Accounting and Accrual Basis of Accounting are the two most widely used

method in accounting for the purpose of recording and recognizing accounting transactions. The

methods are popular and recognized for recording of accounting treatments (Newberry 2014,

p.283).

In cash basis of recording transactions, all entries are recognized on cash basis which

means that as and when cash is received or paid, the transactions are recognized (Ibanichucka &

Aca 2014, p.69). In the case of accrual basis of accounting, transactions are recorded when they

actually take place such as when the income is actually earned or when the expenses are actually

incurred even if there is no cash received or paid. In other words, accrual basis of accounting is

not dependent on the cash received or cash paid for recognizing and recording of transactions.

The main difference between cash basis accounting and accrual basis of accounting is that the

timing of transaction under both the methods are different (Libby 2017, p.42). The difference is

the timing of recognition of revenue is the main cause for the different value under cash basis

and accrual basis of accounting. In general, large business firms use accrual basis of recording,

for the methods recognize as and when the transactions take place and is necessary for the

matching principle of accounting (Collier 2015). In addition to this, large businesses have to get

their financial statements audited before the financial statements are published which can only

happen if the financial statements are prepared following accrual basis of accounting (Biondi &

Soverchia 2014, p.179). The auditor looks for the accrual system of auditing and whether the

financial statement is prepared on the same basis or not. On the other hand, cash basis of

accounting is used by small business who do not that much of a turnover and deal in small

profits. This helps to maintain simplicity in the accounting process. In general, however most of

the businesses nowadays use accrual basis of accounting even the smaller businesses.

The basic advantage of following cash basis of accounting is that the method of

accounting is very simple and easy to implement and follow. In addition to this, it is convenient

for the business to a keep a track of cash inflows and outflows of the business (Brusca,

Caperchione, Cohen & Rossi 2015, p.235). The method also has an implication which is

different for accrual system in the case of taxable income as tax is charged on the money which

is banked. On the other hand, accrual system of accounting is followed on the principle of

ACCOUNTING

Answer to Question 1:

Cash Versus Accrual Basis of Accounting

Cash Basis of Accounting and Accrual Basis of Accounting are the two most widely used

method in accounting for the purpose of recording and recognizing accounting transactions. The

methods are popular and recognized for recording of accounting treatments (Newberry 2014,

p.283).

In cash basis of recording transactions, all entries are recognized on cash basis which

means that as and when cash is received or paid, the transactions are recognized (Ibanichucka &

Aca 2014, p.69). In the case of accrual basis of accounting, transactions are recorded when they

actually take place such as when the income is actually earned or when the expenses are actually

incurred even if there is no cash received or paid. In other words, accrual basis of accounting is

not dependent on the cash received or cash paid for recognizing and recording of transactions.

The main difference between cash basis accounting and accrual basis of accounting is that the

timing of transaction under both the methods are different (Libby 2017, p.42). The difference is

the timing of recognition of revenue is the main cause for the different value under cash basis

and accrual basis of accounting. In general, large business firms use accrual basis of recording,

for the methods recognize as and when the transactions take place and is necessary for the

matching principle of accounting (Collier 2015). In addition to this, large businesses have to get

their financial statements audited before the financial statements are published which can only

happen if the financial statements are prepared following accrual basis of accounting (Biondi &

Soverchia 2014, p.179). The auditor looks for the accrual system of auditing and whether the

financial statement is prepared on the same basis or not. On the other hand, cash basis of

accounting is used by small business who do not that much of a turnover and deal in small

profits. This helps to maintain simplicity in the accounting process. In general, however most of

the businesses nowadays use accrual basis of accounting even the smaller businesses.

The basic advantage of following cash basis of accounting is that the method of

accounting is very simple and easy to implement and follow. In addition to this, it is convenient

for the business to a keep a track of cash inflows and outflows of the business (Brusca,

Caperchione, Cohen & Rossi 2015, p.235). The method also has an implication which is

different for accrual system in the case of taxable income as tax is charged on the money which

is banked. On the other hand, accrual system of accounting is followed on the principle of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING

matching expenses and income as they occur which is the core advantage of following the

accounting system. The application of this method allows businesses to have a clear idea as to

how much profit or loss the business will be earning at the end of the year. The only limitation of

following this method is that the method is complex and consumes a lot of time.

In the case study which is provided in the question, the services which is provided by

Alpha ltd relates to online services to airline which is situated in New Zealand. The company

follows accrual basis of accounting and recording of transactions and the difference which arises

in the value which is obtained under cash basis and accrual basis is due to the difference in

accounting treatment of depreciation which is shown as $ 96,000 and also due to the difference

in treatment of unallocated revenue of $ 43,000. The main advantage due to which accrual basis

of accounting is followed is because it helps in matching the expenses and revenues of the

business (Penman 2016, p.106). The net profit of the company is calculated by following accrual

basis of accounting and the cash generated from operations is calculated by following cash basis

of accounting.

Responsibility of an External Auditor

The primary responsibility of an external auditor is to investigate the financial statement

of the company in order to form an opinion whether the financial statements is depicting true and

fair view or not. The role of the financial statement is to provide financial information to the

potential investors of the company on the basis of which investment decisions are to be taken.

The role of auditor is to form an opinion on the annual reports of the company which will be

based on effective presentation and preparation of financial statement and fairness of the items

which are presented in the financial statement (Klassen, Lisowsky & Mescall 2015, p.179). The

external auditor is also to comment on any frauds and errors which may be present in the

financial statements which the auditor comes across while conducting the audit. It is the

misconception of many companies that the primary role of an auditor is to detect frauds and

errors. The auditor is responsible for only forming an opinion and inspecting whether the

financial statement is showing true and fair view.

Therefore, from the above discussion it is clear that the auditor is responsible for

providing an opinion on the financial statements on the basis of which the potential investors of

the company decide whether or not to invest in the financial statements of the company

ACCOUNTING

matching expenses and income as they occur which is the core advantage of following the

accounting system. The application of this method allows businesses to have a clear idea as to

how much profit or loss the business will be earning at the end of the year. The only limitation of

following this method is that the method is complex and consumes a lot of time.

In the case study which is provided in the question, the services which is provided by

Alpha ltd relates to online services to airline which is situated in New Zealand. The company

follows accrual basis of accounting and recording of transactions and the difference which arises

in the value which is obtained under cash basis and accrual basis is due to the difference in

accounting treatment of depreciation which is shown as $ 96,000 and also due to the difference

in treatment of unallocated revenue of $ 43,000. The main advantage due to which accrual basis

of accounting is followed is because it helps in matching the expenses and revenues of the

business (Penman 2016, p.106). The net profit of the company is calculated by following accrual

basis of accounting and the cash generated from operations is calculated by following cash basis

of accounting.

Responsibility of an External Auditor

The primary responsibility of an external auditor is to investigate the financial statement

of the company in order to form an opinion whether the financial statements is depicting true and

fair view or not. The role of the financial statement is to provide financial information to the

potential investors of the company on the basis of which investment decisions are to be taken.

The role of auditor is to form an opinion on the annual reports of the company which will be

based on effective presentation and preparation of financial statement and fairness of the items

which are presented in the financial statement (Klassen, Lisowsky & Mescall 2015, p.179). The

external auditor is also to comment on any frauds and errors which may be present in the

financial statements which the auditor comes across while conducting the audit. It is the

misconception of many companies that the primary role of an auditor is to detect frauds and

errors. The auditor is responsible for only forming an opinion and inspecting whether the

financial statement is showing true and fair view.

Therefore, from the above discussion it is clear that the auditor is responsible for

providing an opinion on the financial statements on the basis of which the potential investors of

the company decide whether or not to invest in the financial statements of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING

(Hellmann 2016, p.39). The auditor is expected to act in the best interest of the company and

potential investors of the company.

Opinion of the Auditor

As per the case study provided, Air New Zealand’s Financial statements is provided on

the basis of which analysis is to be conducted. The different questions which are given in the

assignment is to done on the basis of the case study provided.

The financial report of Air New Zealand for the year 2016 is audited by the auditing firm

of Deloitte which provides audit and other non-services to its client. As per Deloitte, the

financial reports of the company are prepared fairly and the same has been presented in manner

which is appropriate as per the requirements of the New Zealand relevant standards which is

similar to the International Financial Reporting Standard and Financial Reporting Standard. The

annual reports of Air New Zealand comprise of Statement of profit and loss, Statement showing

financial position of the company, cash flow statement and a statement showing changes in

equity of the company. The financial statements are showing true and fair view as per the

opinion of the auditor. The auditor has issued unqualified report and as per the auditor the

statements are showing true and fair view and is based on all relevant standards of accounting

which is followed in New Zealand.

A qualified audit report is issued by an auditor when there is a presence of material

misstatement in the financial statements of the company. In addition to this, an auditor can also

issue a qualified report if there is any restriction imposed on the auditor by the management of

the company. Such restrictions may be not allowing the auditor to have access to books of

accounts or certain ledger books, not providing management representation even when the

auditors ask for the same (Dao & Pham 2014, p.490). Such types of audit opinions are issued to

inform the investors that the financial statements contain some material misstatements or there

has been some restriction on the part of the management.

Analysis of Net profit and Net Cash Inflow from Operating Activities

The net profit as per the financial statement of Air New Zealand show that it earned a

figure of $ 463 million. The cash from operations of the company is shown at $ 1074 million as

per the cash flow statement as on 2016. The cash from operation is more than the net profit of the

company as per the cash flow statement and profit and loss statement. The cause for the

difference between cash generated from operations and net profit is due to the different

ACCOUNTING

(Hellmann 2016, p.39). The auditor is expected to act in the best interest of the company and

potential investors of the company.

Opinion of the Auditor

As per the case study provided, Air New Zealand’s Financial statements is provided on

the basis of which analysis is to be conducted. The different questions which are given in the

assignment is to done on the basis of the case study provided.

The financial report of Air New Zealand for the year 2016 is audited by the auditing firm

of Deloitte which provides audit and other non-services to its client. As per Deloitte, the

financial reports of the company are prepared fairly and the same has been presented in manner

which is appropriate as per the requirements of the New Zealand relevant standards which is

similar to the International Financial Reporting Standard and Financial Reporting Standard. The

annual reports of Air New Zealand comprise of Statement of profit and loss, Statement showing

financial position of the company, cash flow statement and a statement showing changes in

equity of the company. The financial statements are showing true and fair view as per the

opinion of the auditor. The auditor has issued unqualified report and as per the auditor the

statements are showing true and fair view and is based on all relevant standards of accounting

which is followed in New Zealand.

A qualified audit report is issued by an auditor when there is a presence of material

misstatement in the financial statements of the company. In addition to this, an auditor can also

issue a qualified report if there is any restriction imposed on the auditor by the management of

the company. Such restrictions may be not allowing the auditor to have access to books of

accounts or certain ledger books, not providing management representation even when the

auditors ask for the same (Dao & Pham 2014, p.490). Such types of audit opinions are issued to

inform the investors that the financial statements contain some material misstatements or there

has been some restriction on the part of the management.

Analysis of Net profit and Net Cash Inflow from Operating Activities

The net profit as per the financial statement of Air New Zealand show that it earned a

figure of $ 463 million. The cash from operations of the company is shown at $ 1074 million as

per the cash flow statement as on 2016. The cash from operation is more than the net profit of the

company as per the cash flow statement and profit and loss statement. The cause for the

difference between cash generated from operations and net profit is due to the different

5

ACCOUNTING

treatments which is carried out in case of calculations of actual cash inflows of the company. In

the computation of net profit, various non-cash expenses are also deducted from total revenue to

arrive at the results. Such non- cash expenses are added back to the net profit to obtain actual

cash inflows of the company. an example of such a non-cash expenses is depreciation, gain or

loss from sale of assets and impairment losses.

Audit Committee of the Company

As per the financial Statement of the Air New Zealand, the directors who are members of

the audit committee are Tony Crater, Jan Dawson and Jonathan Mason. The role of the audit

committee is to look after the financial and reporting disclosures of the company. The committee

also looks after the whole of the audit process and ensures whether relevant standards and norms

are being followed or not by the auditor of the company. the role of an audit committee is

considered to be crucial for the overall management of the company. The primary responsibility

of an audit committee is supervision of the audit process, financial reporting, internal controls

and laws and regulations system of the company.

Contingent liability

The directors of the company have recognized a contingent liability which is shown at a

combined amount of $ 33 million. Such contingent liability comprises of Letter of credit and

performance of bonds (Lubbe, Modack & Watson 2014, p.283). The definition of contingent

liability states that any liability which can happen due to future uncertain events from either

occurring or non-occurring and which cannot be measured effectively.

ACCOUNTING

treatments which is carried out in case of calculations of actual cash inflows of the company. In

the computation of net profit, various non-cash expenses are also deducted from total revenue to

arrive at the results. Such non- cash expenses are added back to the net profit to obtain actual

cash inflows of the company. an example of such a non-cash expenses is depreciation, gain or

loss from sale of assets and impairment losses.

Audit Committee of the Company

As per the financial Statement of the Air New Zealand, the directors who are members of

the audit committee are Tony Crater, Jan Dawson and Jonathan Mason. The role of the audit

committee is to look after the financial and reporting disclosures of the company. The committee

also looks after the whole of the audit process and ensures whether relevant standards and norms

are being followed or not by the auditor of the company. the role of an audit committee is

considered to be crucial for the overall management of the company. The primary responsibility

of an audit committee is supervision of the audit process, financial reporting, internal controls

and laws and regulations system of the company.

Contingent liability

The directors of the company have recognized a contingent liability which is shown at a

combined amount of $ 33 million. Such contingent liability comprises of Letter of credit and

performance of bonds (Lubbe, Modack & Watson 2014, p.283). The definition of contingent

liability states that any liability which can happen due to future uncertain events from either

occurring or non-occurring and which cannot be measured effectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING

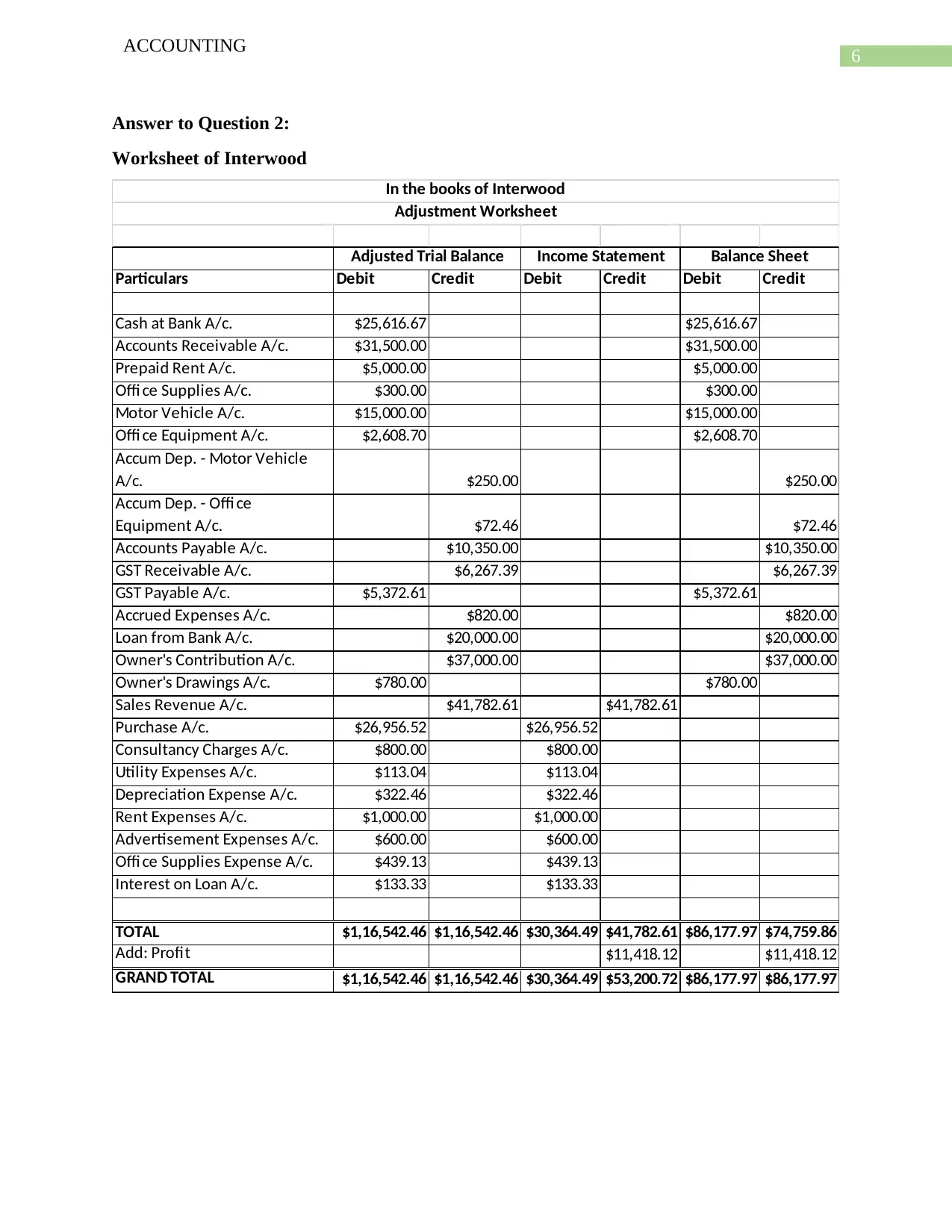

Answer to Question 2:

Worksheet of Interwood

Particulars Debit Credit Debit Credit Debit Credit

Cash at Bank A/c. $25,616.67 $25,616.67

Accounts Receivable A/c. $31,500.00 $31,500.00

Prepaid Rent A/c. $5,000.00 $5,000.00

Offi ce Supplies A/c. $300.00 $300.00

Motor Vehicle A/c. $15,000.00 $15,000.00

Offi ce Equipment A/c. $2,608.70 $2,608.70

Accum Dep. - Motor Vehicle

A/c. $250.00 $250.00

Accum Dep. - Offi ce

Equipment A/c. $72.46 $72.46

Accounts Payable A/c. $10,350.00 $10,350.00

GST Receivable A/c. $6,267.39 $6,267.39

GST Payable A/c. $5,372.61 $5,372.61

Accrued Expenses A/c. $820.00 $820.00

Loan from Bank A/c. $20,000.00 $20,000.00

Owner's Contribution A/c. $37,000.00 $37,000.00

Owner's Drawings A/c. $780.00 $780.00

Sales Revenue A/c. $41,782.61 $41,782.61

Purchase A/c. $26,956.52 $26,956.52

Consultancy Charges A/c. $800.00 $800.00

Utility Expenses A/c. $113.04 $113.04

Depreciation Expense A/c. $322.46 $322.46

Rent Expenses A/c. $1,000.00 $1,000.00

Advertisement Expenses A/c. $600.00 $600.00

Offi ce Supplies Expense A/c. $439.13 $439.13

Interest on Loan A/c. $133.33 $133.33

TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $41,782.61 $86,177.97 $74,759.86

Add: Profit $11,418.12 $11,418.12

GRAND TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $53,200.72 $86,177.97 $86,177.97

Adjusted Trial Balance Income Statement Balance Sheet

In the books of Interwood

Adjustment Worksheet

ACCOUNTING

Answer to Question 2:

Worksheet of Interwood

Particulars Debit Credit Debit Credit Debit Credit

Cash at Bank A/c. $25,616.67 $25,616.67

Accounts Receivable A/c. $31,500.00 $31,500.00

Prepaid Rent A/c. $5,000.00 $5,000.00

Offi ce Supplies A/c. $300.00 $300.00

Motor Vehicle A/c. $15,000.00 $15,000.00

Offi ce Equipment A/c. $2,608.70 $2,608.70

Accum Dep. - Motor Vehicle

A/c. $250.00 $250.00

Accum Dep. - Offi ce

Equipment A/c. $72.46 $72.46

Accounts Payable A/c. $10,350.00 $10,350.00

GST Receivable A/c. $6,267.39 $6,267.39

GST Payable A/c. $5,372.61 $5,372.61

Accrued Expenses A/c. $820.00 $820.00

Loan from Bank A/c. $20,000.00 $20,000.00

Owner's Contribution A/c. $37,000.00 $37,000.00

Owner's Drawings A/c. $780.00 $780.00

Sales Revenue A/c. $41,782.61 $41,782.61

Purchase A/c. $26,956.52 $26,956.52

Consultancy Charges A/c. $800.00 $800.00

Utility Expenses A/c. $113.04 $113.04

Depreciation Expense A/c. $322.46 $322.46

Rent Expenses A/c. $1,000.00 $1,000.00

Advertisement Expenses A/c. $600.00 $600.00

Offi ce Supplies Expense A/c. $439.13 $439.13

Interest on Loan A/c. $133.33 $133.33

TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $41,782.61 $86,177.97 $74,759.86

Add: Profit $11,418.12 $11,418.12

GRAND TOTAL $1,16,542.46 $1,16,542.46 $30,364.49 $53,200.72 $86,177.97 $86,177.97

Adjusted Trial Balance Income Statement Balance Sheet

In the books of Interwood

Adjustment Worksheet

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING

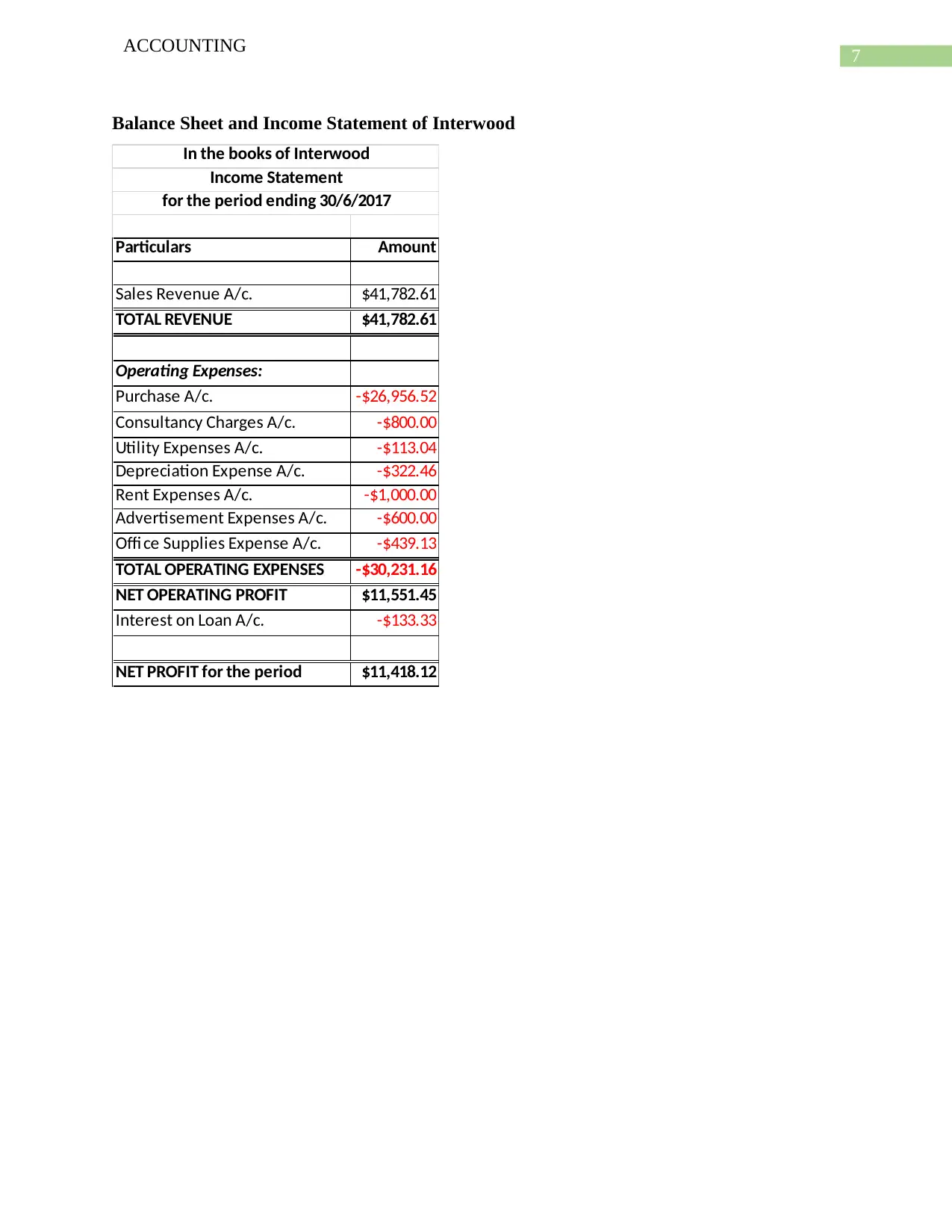

Balance Sheet and Income Statement of Interwood

Particulars Amount

Sales Revenue A/c. $41,782.61

TOTAL REVENUE $41,782.61

Operating Expenses:

Purchase A/c. -$26,956.52

Consultancy Charges A/c. -$800.00

Utility Expenses A/c. -$113.04

Depreciation Expense A/c. -$322.46

Rent Expenses A/c. -$1,000.00

Advertisement Expenses A/c. -$600.00

Offi ce Supplies Expense A/c. -$439.13

TOTAL OPERATING EXPENSES -$30,231.16

NET OPERATING PROFIT $11,551.45

Interest on Loan A/c. -$133.33

NET PROFIT for the period $11,418.12

In the books of Interwood

Income Statement

for the period ending 30/6/2017

ACCOUNTING

Balance Sheet and Income Statement of Interwood

Particulars Amount

Sales Revenue A/c. $41,782.61

TOTAL REVENUE $41,782.61

Operating Expenses:

Purchase A/c. -$26,956.52

Consultancy Charges A/c. -$800.00

Utility Expenses A/c. -$113.04

Depreciation Expense A/c. -$322.46

Rent Expenses A/c. -$1,000.00

Advertisement Expenses A/c. -$600.00

Offi ce Supplies Expense A/c. -$439.13

TOTAL OPERATING EXPENSES -$30,231.16

NET OPERATING PROFIT $11,551.45

Interest on Loan A/c. -$133.33

NET PROFIT for the period $11,418.12

In the books of Interwood

Income Statement

for the period ending 30/6/2017

8

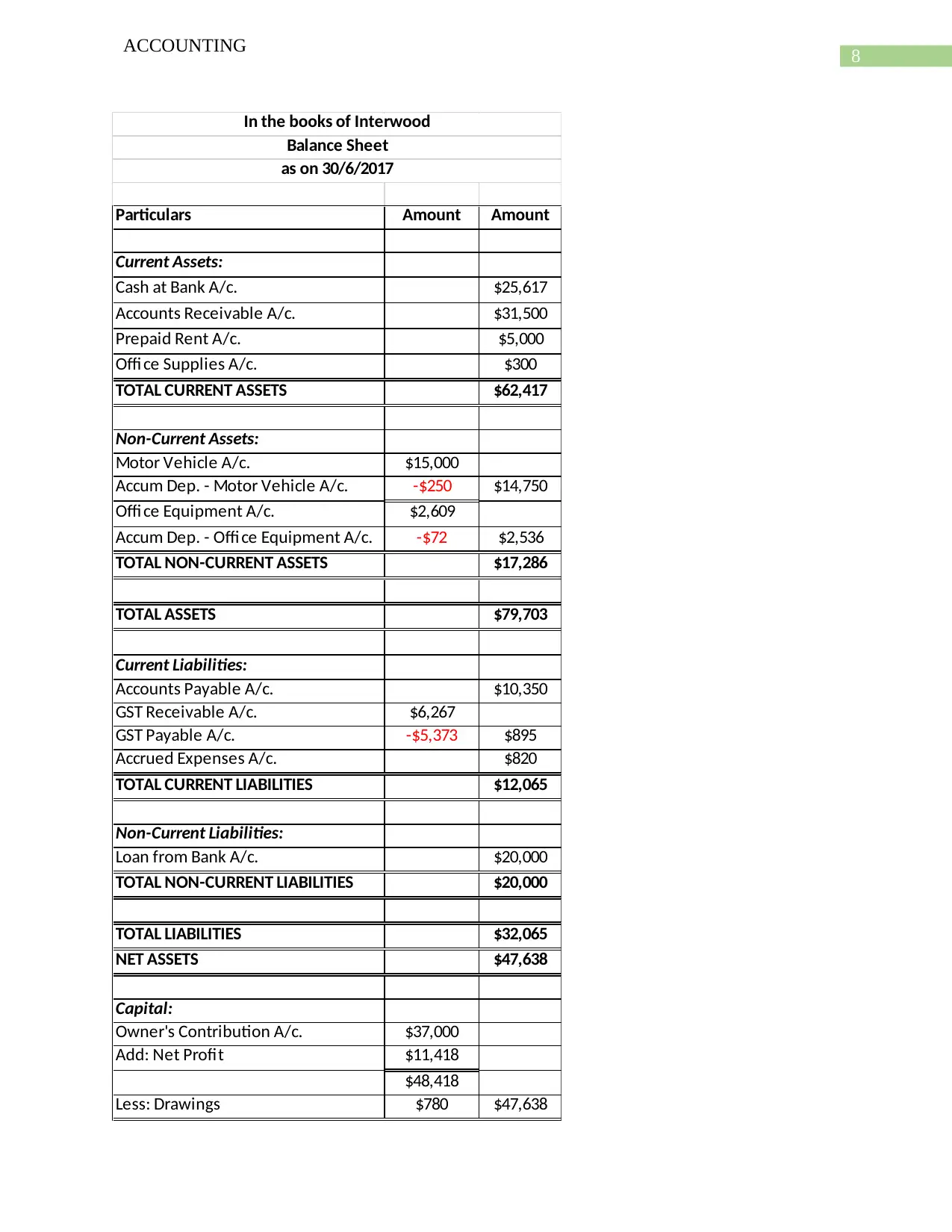

ACCOUNTING

Particulars Amount Amount

Current Assets:

Cash at Bank A/c. $25,617

Accounts Receivable A/c. $31,500

Prepaid Rent A/c. $5,000

Offi ce Supplies A/c. $300

TOTAL CURRENT ASSETS $62,417

Non-Current Assets:

Motor Vehicle A/c. $15,000

Accum Dep. - Motor Vehicle A/c. -$250 $14,750

Offi ce Equipment A/c. $2,609

Accum Dep. - Offi ce Equipment A/c. -$72 $2,536

TOTAL NON-CURRENT ASSETS $17,286

TOTAL ASSETS $79,703

Current Liabilities:

Accounts Payable A/c. $10,350

GST Receivable A/c. $6,267

GST Payable A/c. -$5,373 $895

Accrued Expenses A/c. $820

TOTAL CURRENT LIABILITIES $12,065

Non-Current Liabilities:

Loan from Bank A/c. $20,000

TOTAL NON-CURRENT LIABILITIES $20,000

TOTAL LIABILITIES $32,065

NET ASSETS $47,638

Capital:

Owner's Contribution A/c. $37,000

Add: Net Profit $11,418

$48,418

Less: Drawings $780 $47,638

TOTAL CAPITAL $47,638

In the books of Interwood

Balance Sheet

as on 30/6/2017

ACCOUNTING

Particulars Amount Amount

Current Assets:

Cash at Bank A/c. $25,617

Accounts Receivable A/c. $31,500

Prepaid Rent A/c. $5,000

Offi ce Supplies A/c. $300

TOTAL CURRENT ASSETS $62,417

Non-Current Assets:

Motor Vehicle A/c. $15,000

Accum Dep. - Motor Vehicle A/c. -$250 $14,750

Offi ce Equipment A/c. $2,609

Accum Dep. - Offi ce Equipment A/c. -$72 $2,536

TOTAL NON-CURRENT ASSETS $17,286

TOTAL ASSETS $79,703

Current Liabilities:

Accounts Payable A/c. $10,350

GST Receivable A/c. $6,267

GST Payable A/c. -$5,373 $895

Accrued Expenses A/c. $820

TOTAL CURRENT LIABILITIES $12,065

Non-Current Liabilities:

Loan from Bank A/c. $20,000

TOTAL NON-CURRENT LIABILITIES $20,000

TOTAL LIABILITIES $32,065

NET ASSETS $47,638

Capital:

Owner's Contribution A/c. $37,000

Add: Net Profit $11,418

$48,418

Less: Drawings $780 $47,638

TOTAL CAPITAL $47,638

In the books of Interwood

Balance Sheet

as on 30/6/2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING

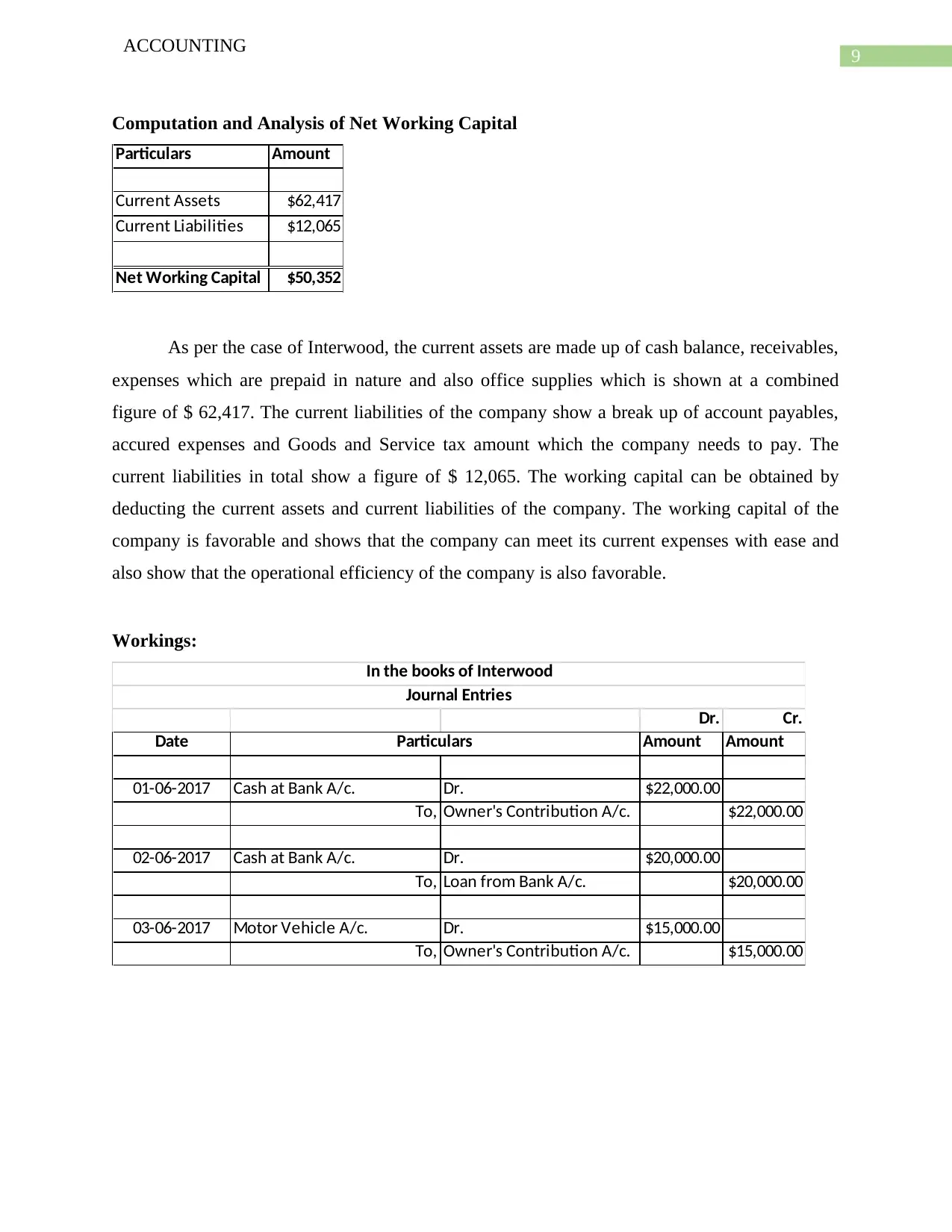

Computation and Analysis of Net Working Capital

Particulars Amount

Current Assets $62,417

Current Liabilities $12,065

Net Working Capital $50,352

As per the case of Interwood, the current assets are made up of cash balance, receivables,

expenses which are prepaid in nature and also office supplies which is shown at a combined

figure of $ 62,417. The current liabilities of the company show a break up of account payables,

accured expenses and Goods and Service tax amount which the company needs to pay. The

current liabilities in total show a figure of $ 12,065. The working capital can be obtained by

deducting the current assets and current liabilities of the company. The working capital of the

company is favorable and shows that the company can meet its current expenses with ease and

also show that the operational efficiency of the company is also favorable.

Workings:

Dr. Cr.

Date Amount Amount

01-06-2017 Cash at Bank A/c. Dr. $22,000.00

To, Owner's Contribution A/c. $22,000.00

02-06-2017 Cash at Bank A/c. Dr. $20,000.00

To, Loan from Bank A/c. $20,000.00

03-06-2017 Motor Vehicle A/c. Dr. $15,000.00

To, Owner's Contribution A/c. $15,000.00

Particulars

In the books of Interwood

Journal Entries

ACCOUNTING

Computation and Analysis of Net Working Capital

Particulars Amount

Current Assets $62,417

Current Liabilities $12,065

Net Working Capital $50,352

As per the case of Interwood, the current assets are made up of cash balance, receivables,

expenses which are prepaid in nature and also office supplies which is shown at a combined

figure of $ 62,417. The current liabilities of the company show a break up of account payables,

accured expenses and Goods and Service tax amount which the company needs to pay. The

current liabilities in total show a figure of $ 12,065. The working capital can be obtained by

deducting the current assets and current liabilities of the company. The working capital of the

company is favorable and shows that the company can meet its current expenses with ease and

also show that the operational efficiency of the company is also favorable.

Workings:

Dr. Cr.

Date Amount Amount

01-06-2017 Cash at Bank A/c. Dr. $22,000.00

To, Owner's Contribution A/c. $22,000.00

02-06-2017 Cash at Bank A/c. Dr. $20,000.00

To, Loan from Bank A/c. $20,000.00

03-06-2017 Motor Vehicle A/c. Dr. $15,000.00

To, Owner's Contribution A/c. $15,000.00

Particulars

In the books of Interwood

Journal Entries

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING

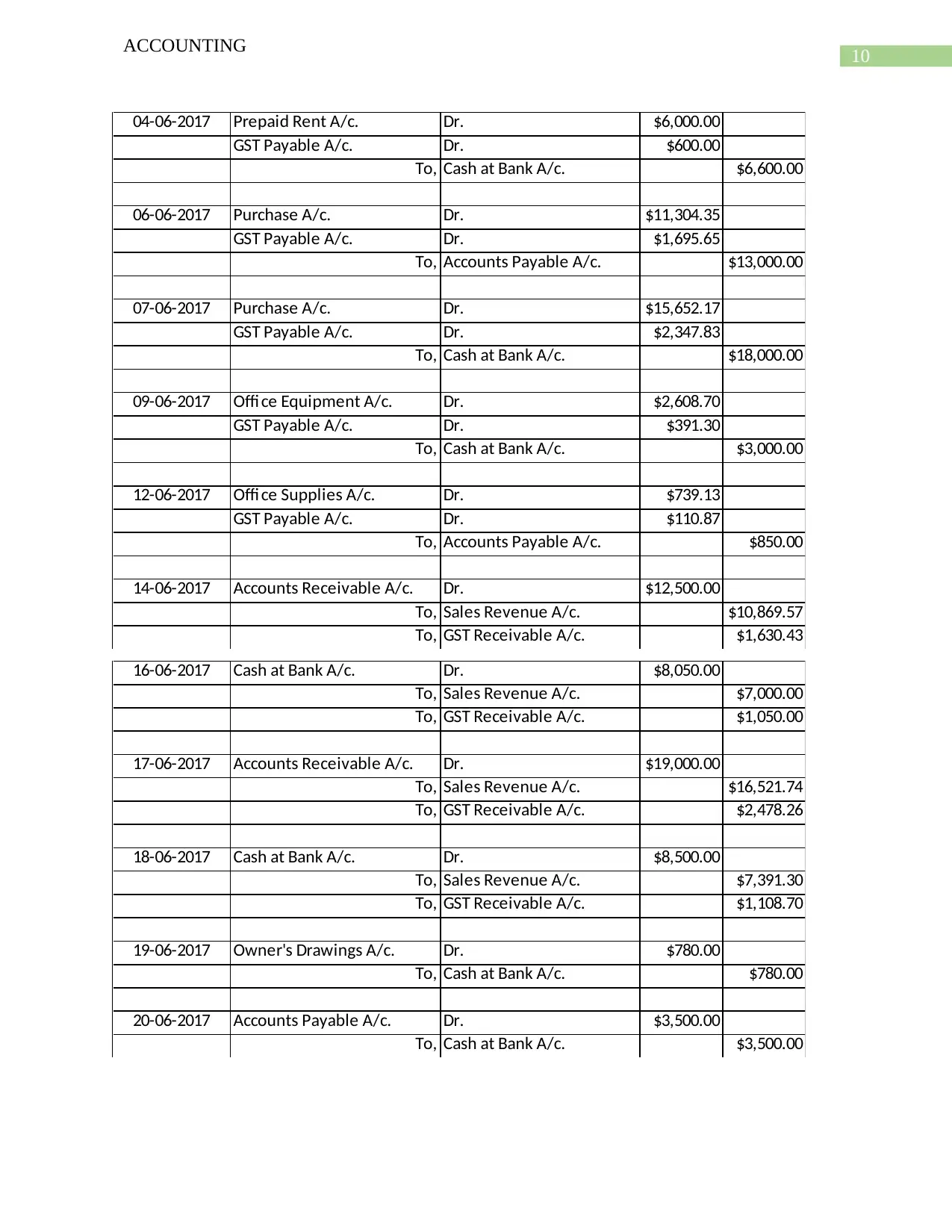

04-06-2017 Prepaid Rent A/c. Dr. $6,000.00

GST Payable A/c. Dr. $600.00

To, Cash at Bank A/c. $6,600.00

06-06-2017 Purchase A/c. Dr. $11,304.35

GST Payable A/c. Dr. $1,695.65

To, Accounts Payable A/c. $13,000.00

07-06-2017 Purchase A/c. Dr. $15,652.17

GST Payable A/c. Dr. $2,347.83

To, Cash at Bank A/c. $18,000.00

09-06-2017 Offi ce Equipment A/c. Dr. $2,608.70

GST Payable A/c. Dr. $391.30

To, Cash at Bank A/c. $3,000.00

12-06-2017 Offi ce Supplies A/c. Dr. $739.13

GST Payable A/c. Dr. $110.87

To, Accounts Payable A/c. $850.00

14-06-2017 Accounts Receivable A/c. Dr. $12,500.00

To, Sales Revenue A/c. $10,869.57

To, GST Receivable A/c. $1,630.43

16-06-2017 Cash at Bank A/c. Dr. $8,050.00

To, Sales Revenue A/c. $7,000.00

To, GST Receivable A/c. $1,050.00

17-06-2017 Accounts Receivable A/c. Dr. $19,000.00

To, Sales Revenue A/c. $16,521.74

To, GST Receivable A/c. $2,478.26

18-06-2017 Cash at Bank A/c. Dr. $8,500.00

To, Sales Revenue A/c. $7,391.30

To, GST Receivable A/c. $1,108.70

19-06-2017 Owner's Drawings A/c. Dr. $780.00

To, Cash at Bank A/c. $780.00

20-06-2017 Accounts Payable A/c. Dr. $3,500.00

To, Cash at Bank A/c. $3,500.00

ACCOUNTING

04-06-2017 Prepaid Rent A/c. Dr. $6,000.00

GST Payable A/c. Dr. $600.00

To, Cash at Bank A/c. $6,600.00

06-06-2017 Purchase A/c. Dr. $11,304.35

GST Payable A/c. Dr. $1,695.65

To, Accounts Payable A/c. $13,000.00

07-06-2017 Purchase A/c. Dr. $15,652.17

GST Payable A/c. Dr. $2,347.83

To, Cash at Bank A/c. $18,000.00

09-06-2017 Offi ce Equipment A/c. Dr. $2,608.70

GST Payable A/c. Dr. $391.30

To, Cash at Bank A/c. $3,000.00

12-06-2017 Offi ce Supplies A/c. Dr. $739.13

GST Payable A/c. Dr. $110.87

To, Accounts Payable A/c. $850.00

14-06-2017 Accounts Receivable A/c. Dr. $12,500.00

To, Sales Revenue A/c. $10,869.57

To, GST Receivable A/c. $1,630.43

16-06-2017 Cash at Bank A/c. Dr. $8,050.00

To, Sales Revenue A/c. $7,000.00

To, GST Receivable A/c. $1,050.00

17-06-2017 Accounts Receivable A/c. Dr. $19,000.00

To, Sales Revenue A/c. $16,521.74

To, GST Receivable A/c. $2,478.26

18-06-2017 Cash at Bank A/c. Dr. $8,500.00

To, Sales Revenue A/c. $7,391.30

To, GST Receivable A/c. $1,108.70

19-06-2017 Owner's Drawings A/c. Dr. $780.00

To, Cash at Bank A/c. $780.00

20-06-2017 Accounts Payable A/c. Dr. $3,500.00

To, Cash at Bank A/c. $3,500.00

11

ACCOUNTING

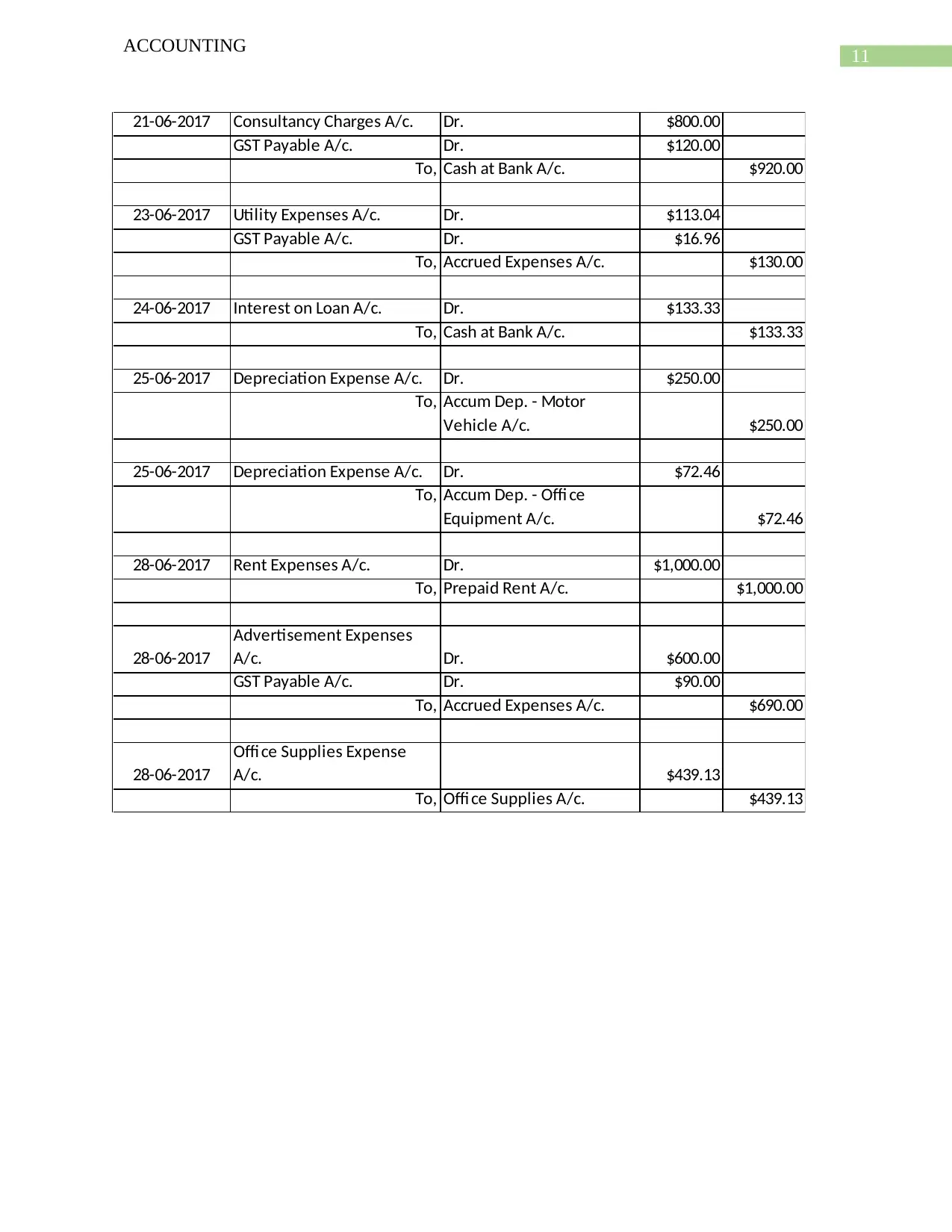

21-06-2017 Consultancy Charges A/c. Dr. $800.00

GST Payable A/c. Dr. $120.00

To, Cash at Bank A/c. $920.00

23-06-2017 Utility Expenses A/c. Dr. $113.04

GST Payable A/c. Dr. $16.96

To, Accrued Expenses A/c. $130.00

24-06-2017 Interest on Loan A/c. Dr. $133.33

To, Cash at Bank A/c. $133.33

25-06-2017 Depreciation Expense A/c. Dr. $250.00

To, Accum Dep. - Motor

Vehicle A/c. $250.00

25-06-2017 Depreciation Expense A/c. Dr. $72.46

To, Accum Dep. - Offi ce

Equipment A/c. $72.46

28-06-2017 Rent Expenses A/c. Dr. $1,000.00

To, Prepaid Rent A/c. $1,000.00

28-06-2017

Advertisement Expenses

A/c. Dr. $600.00

GST Payable A/c. Dr. $90.00

To, Accrued Expenses A/c. $690.00

28-06-2017

Offi ce Supplies Expense

A/c. $439.13

To, Offi ce Supplies A/c. $439.13

ACCOUNTING

21-06-2017 Consultancy Charges A/c. Dr. $800.00

GST Payable A/c. Dr. $120.00

To, Cash at Bank A/c. $920.00

23-06-2017 Utility Expenses A/c. Dr. $113.04

GST Payable A/c. Dr. $16.96

To, Accrued Expenses A/c. $130.00

24-06-2017 Interest on Loan A/c. Dr. $133.33

To, Cash at Bank A/c. $133.33

25-06-2017 Depreciation Expense A/c. Dr. $250.00

To, Accum Dep. - Motor

Vehicle A/c. $250.00

25-06-2017 Depreciation Expense A/c. Dr. $72.46

To, Accum Dep. - Offi ce

Equipment A/c. $72.46

28-06-2017 Rent Expenses A/c. Dr. $1,000.00

To, Prepaid Rent A/c. $1,000.00

28-06-2017

Advertisement Expenses

A/c. Dr. $600.00

GST Payable A/c. Dr. $90.00

To, Accrued Expenses A/c. $690.00

28-06-2017

Offi ce Supplies Expense

A/c. $439.13

To, Offi ce Supplies A/c. $439.13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.