Comprehensive Analysis: Bond and Stock Valuation in Corporate Finance

VerifiedAdded on 2021/09/18

|5

|1280

|99

Report

AI Summary

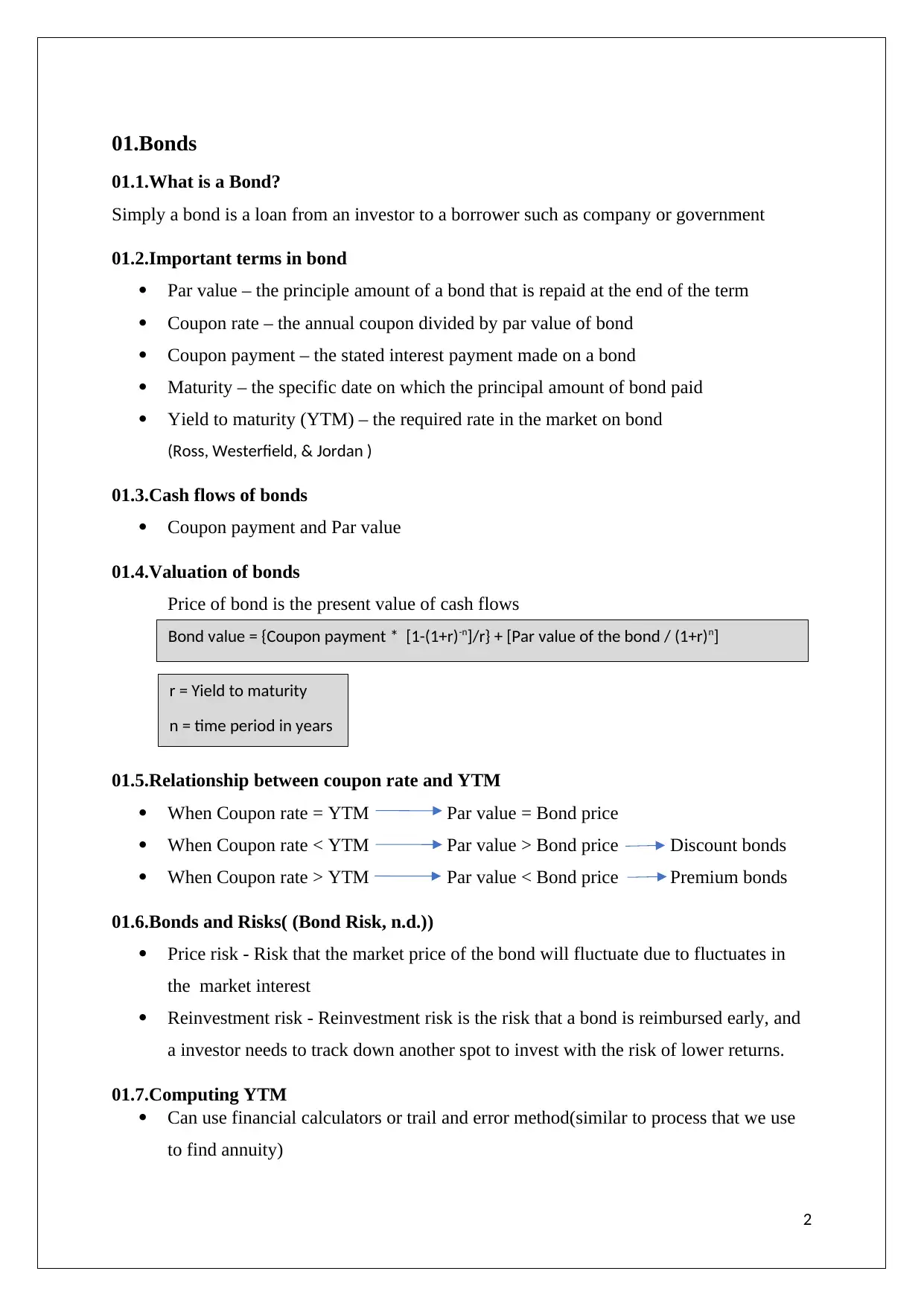

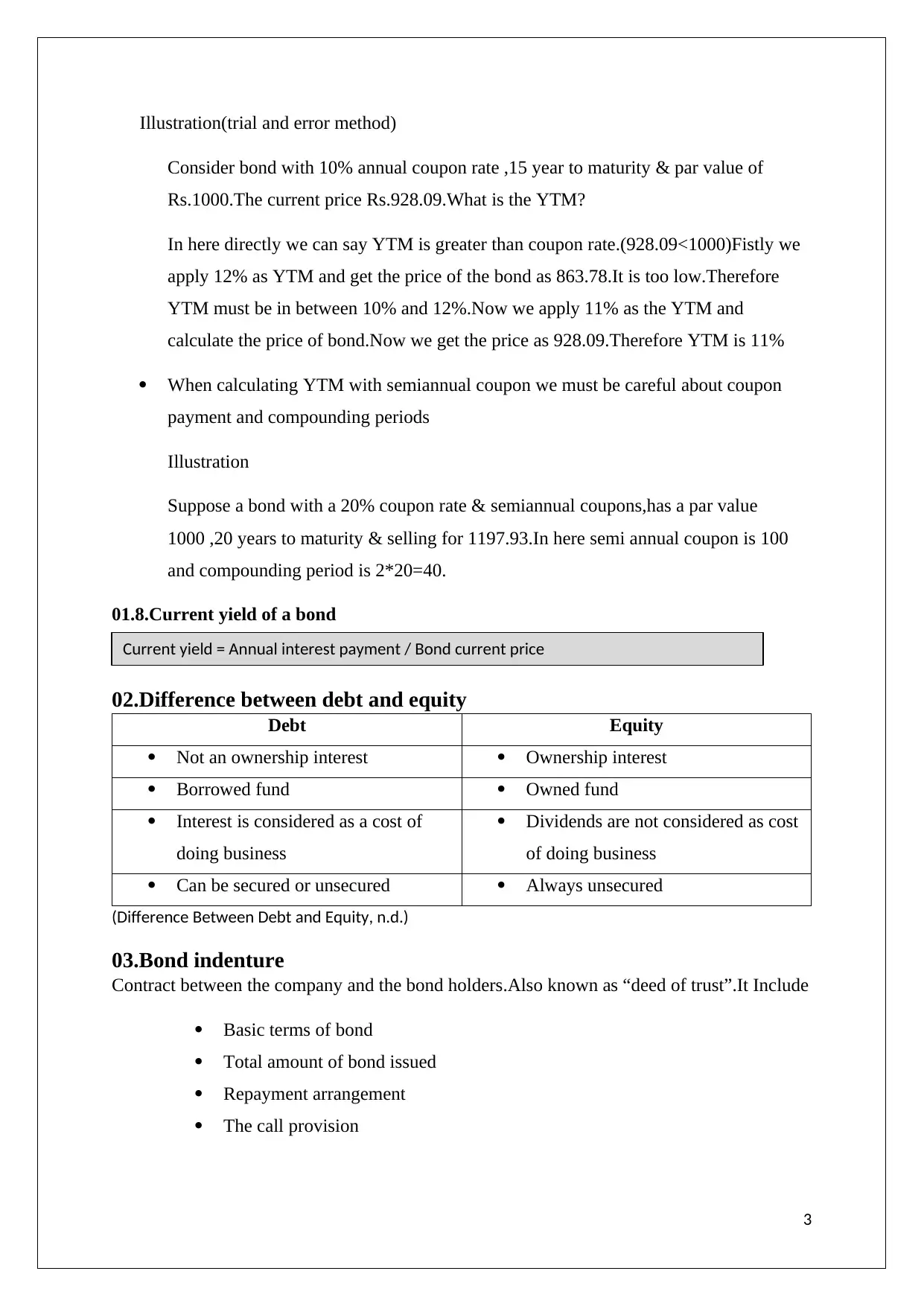

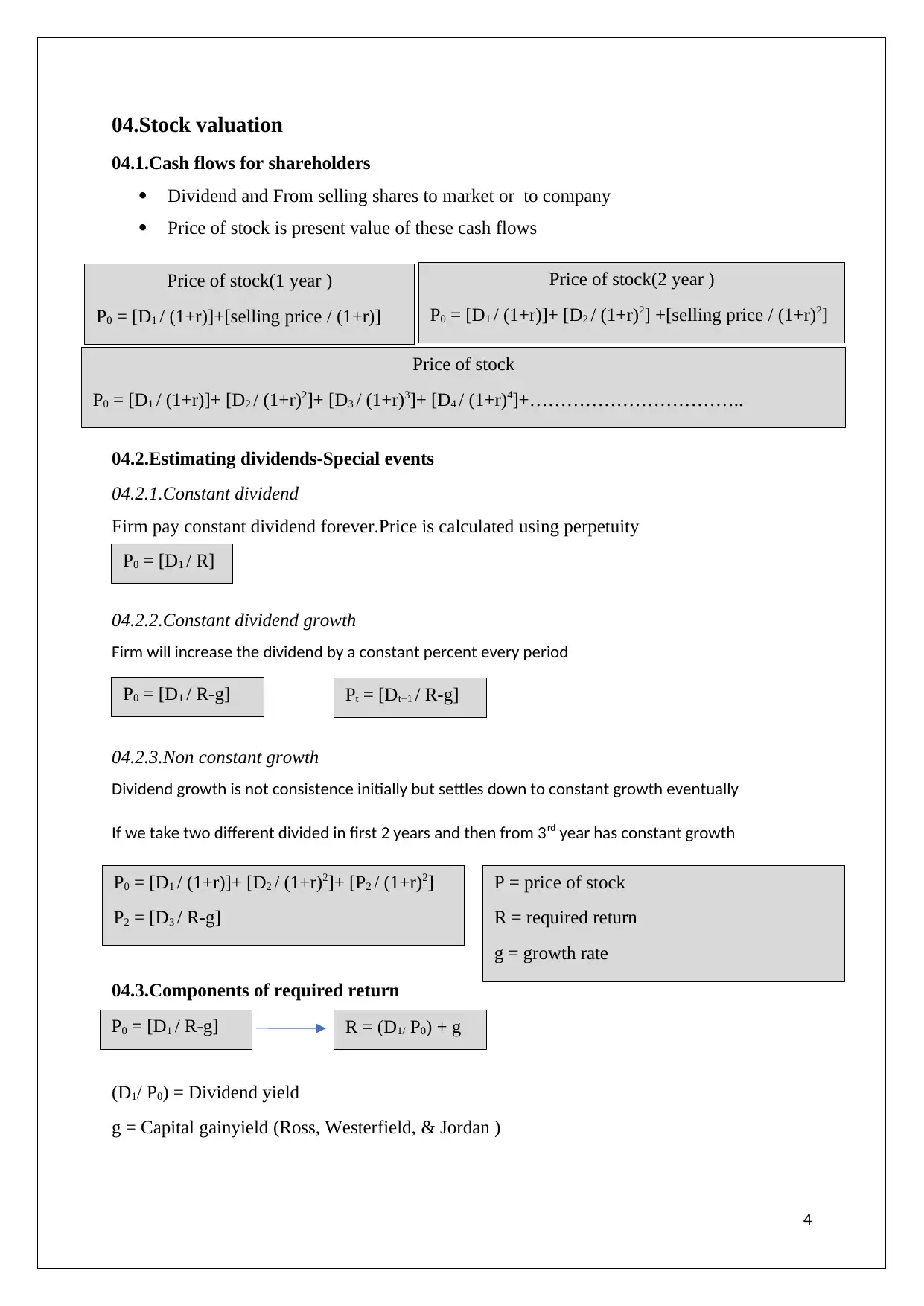

This report provides a comprehensive analysis of bond and stock valuation, essential concepts in corporate finance. It begins by defining bonds, detailing important terms like par value, coupon rate, and yield to maturity (YTM), and explaining the cash flows associated with bonds. The report then explores the valuation of bonds, including the relationship between coupon rate and YTM, and the risks associated with bonds like price risk and reinvestment risk. It also covers how to compute YTM using the trial and error method. The report contrasts debt and equity, and explains the bond indenture. Subsequently, it delves into stock valuation, outlining cash flows for shareholders, and different dividend estimation models, including constant dividend, constant dividend growth, and non-constant growth models. It also examines the components of required return. The report concludes by summarizing key takeaways, emphasizing the inverse relationship between bond value and interest rates, and the importance of understanding dividend-based stock valuation.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.