Detailed Analysis of Off-Market Swap Valuation Using Rate Methods

VerifiedAdded on 2023/01/17

|6

|1002

|34

Report

AI Summary

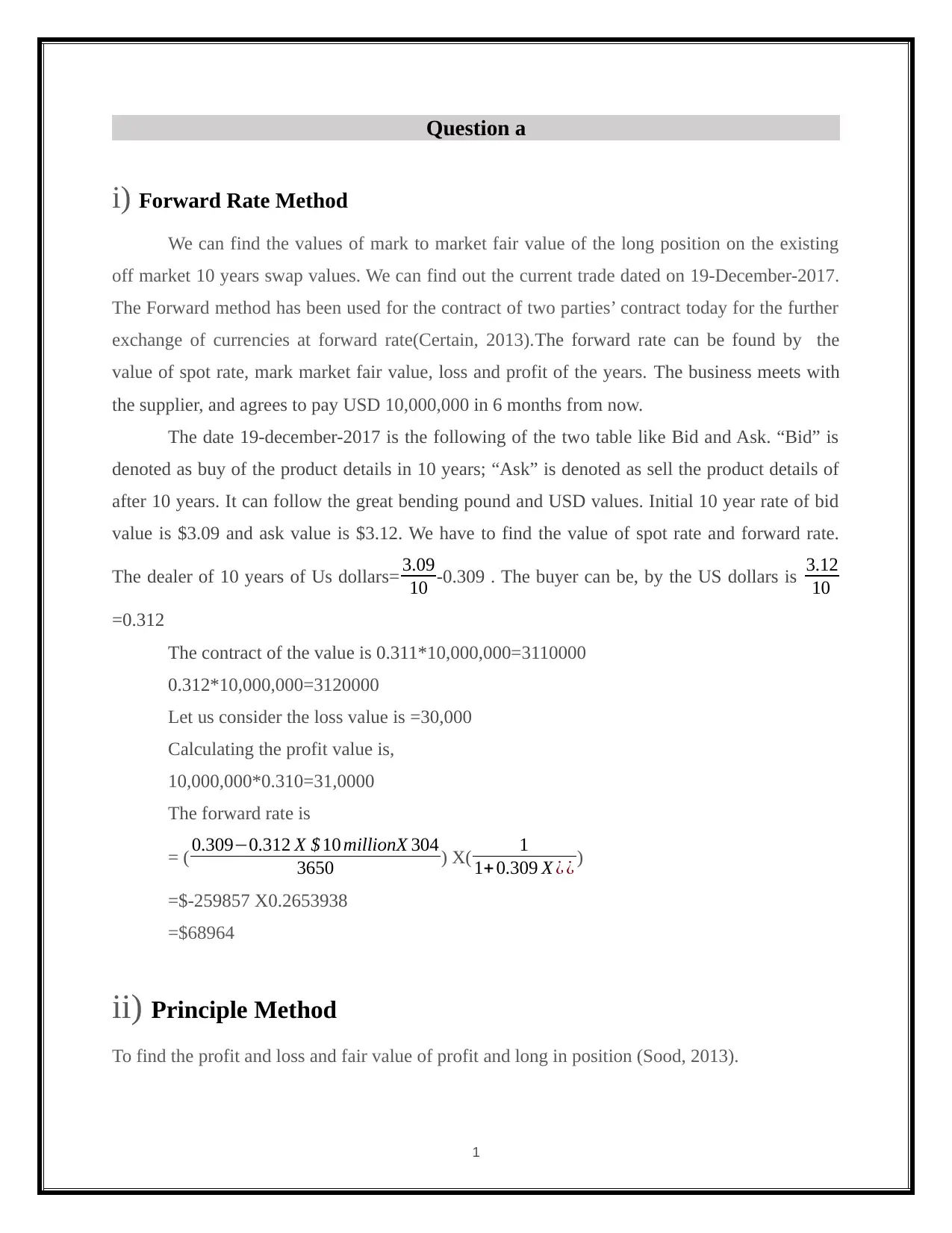

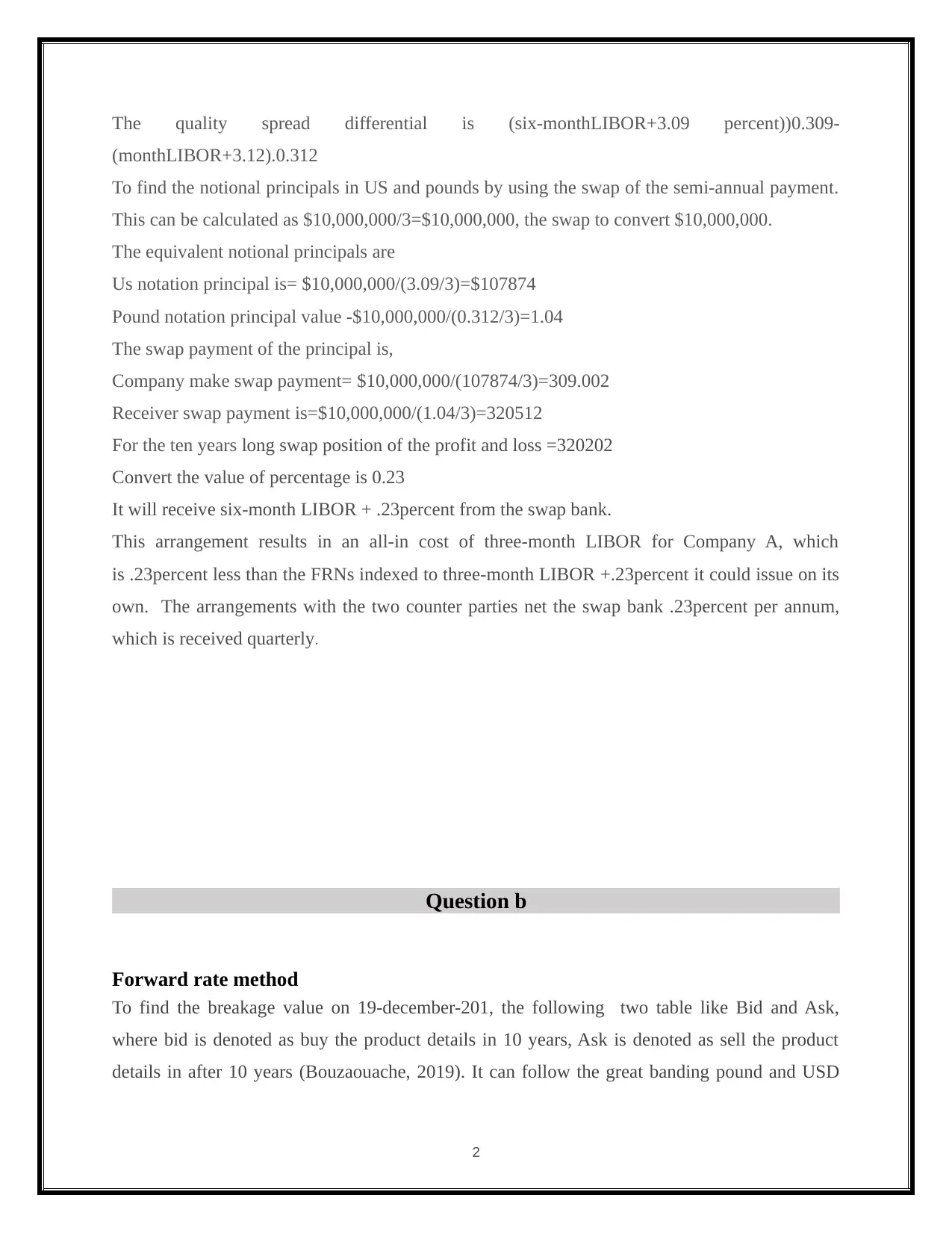

This report provides a detailed analysis of swap valuation using both the forward rate and principal methods. It begins by calculating the mark-to-market fair value of a long position on an existing off-market 10-year swap, using the forward rate method to determine values based on bid and ask rates. It then applies the principal method to find profit and loss, considering notional principals in US dollars and pounds, and calculating swap payments. The report extends this analysis to determine breakage value, again using both forward rate and principal methods, and detailing the calculations involved in determining profit, loss, and fair value. The analysis includes scenarios, such as profit and loss calculations, and conversion of values to percentages, to demonstrate how a company might receive LIBOR-based payments from a swap bank, impacting their overall costs.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.