Comprehensive Financial Valuation of The Sherwin-Williams Company

VerifiedAdded on 2019/09/20

|23

|3413

|316

Homework Assignment

AI Summary

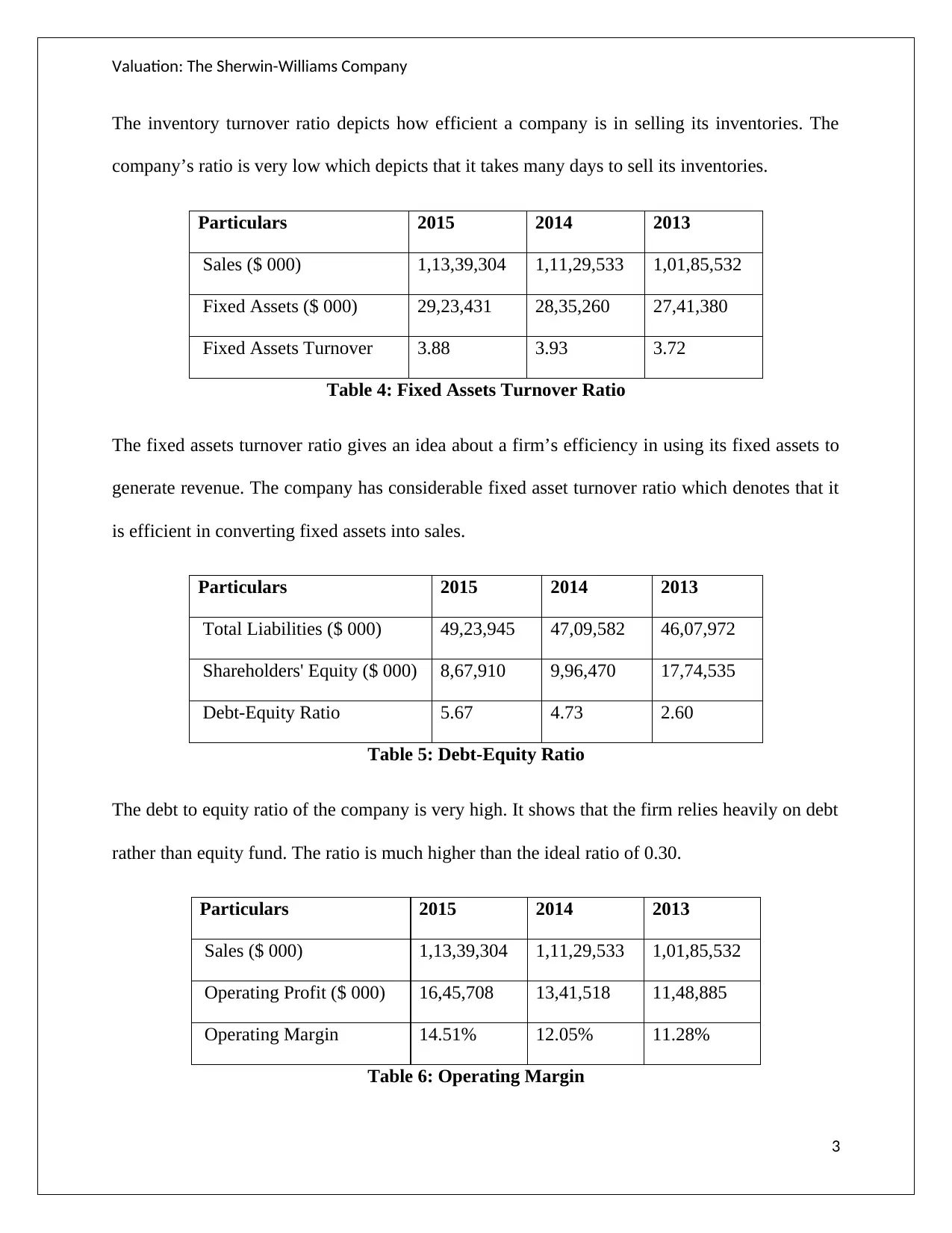

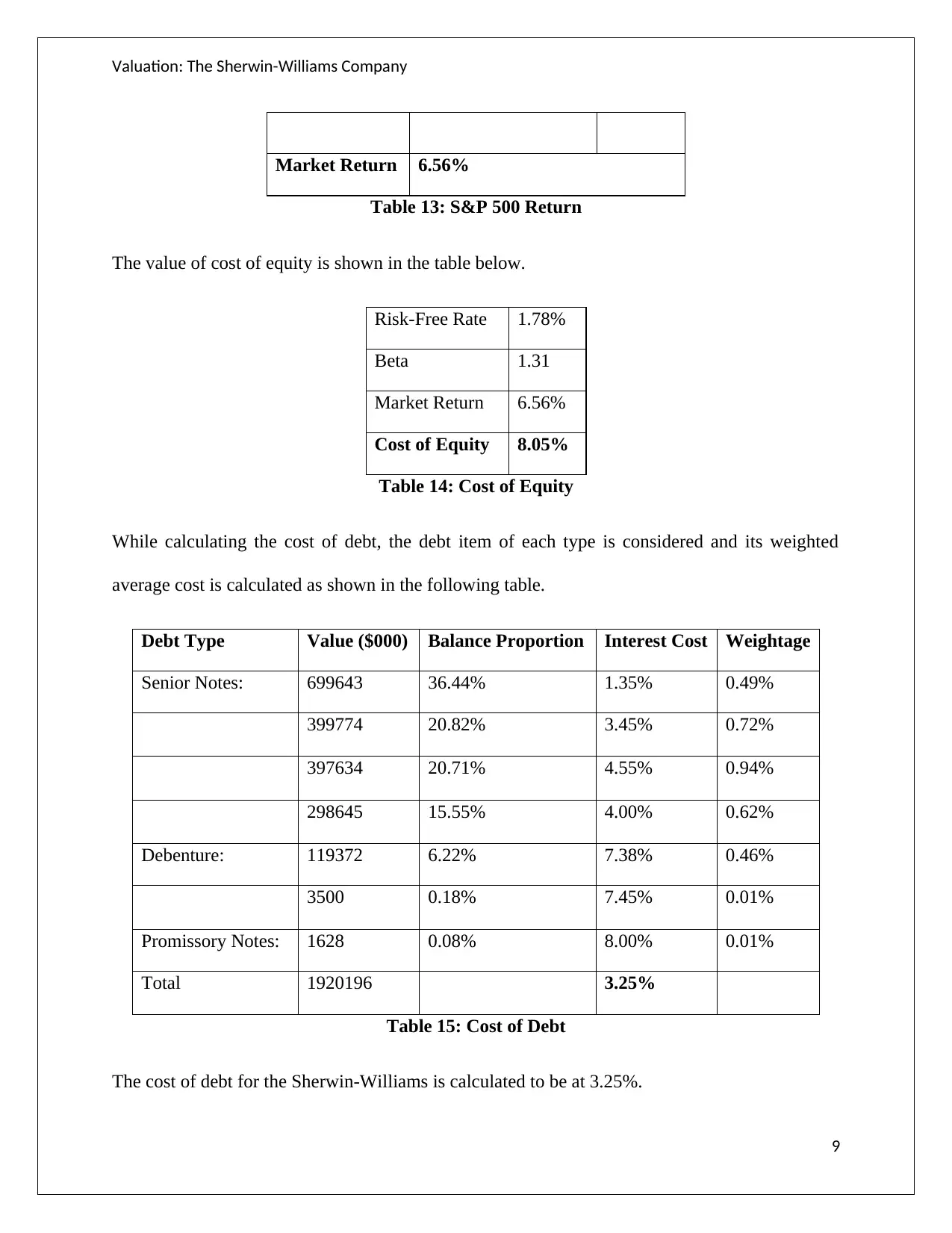

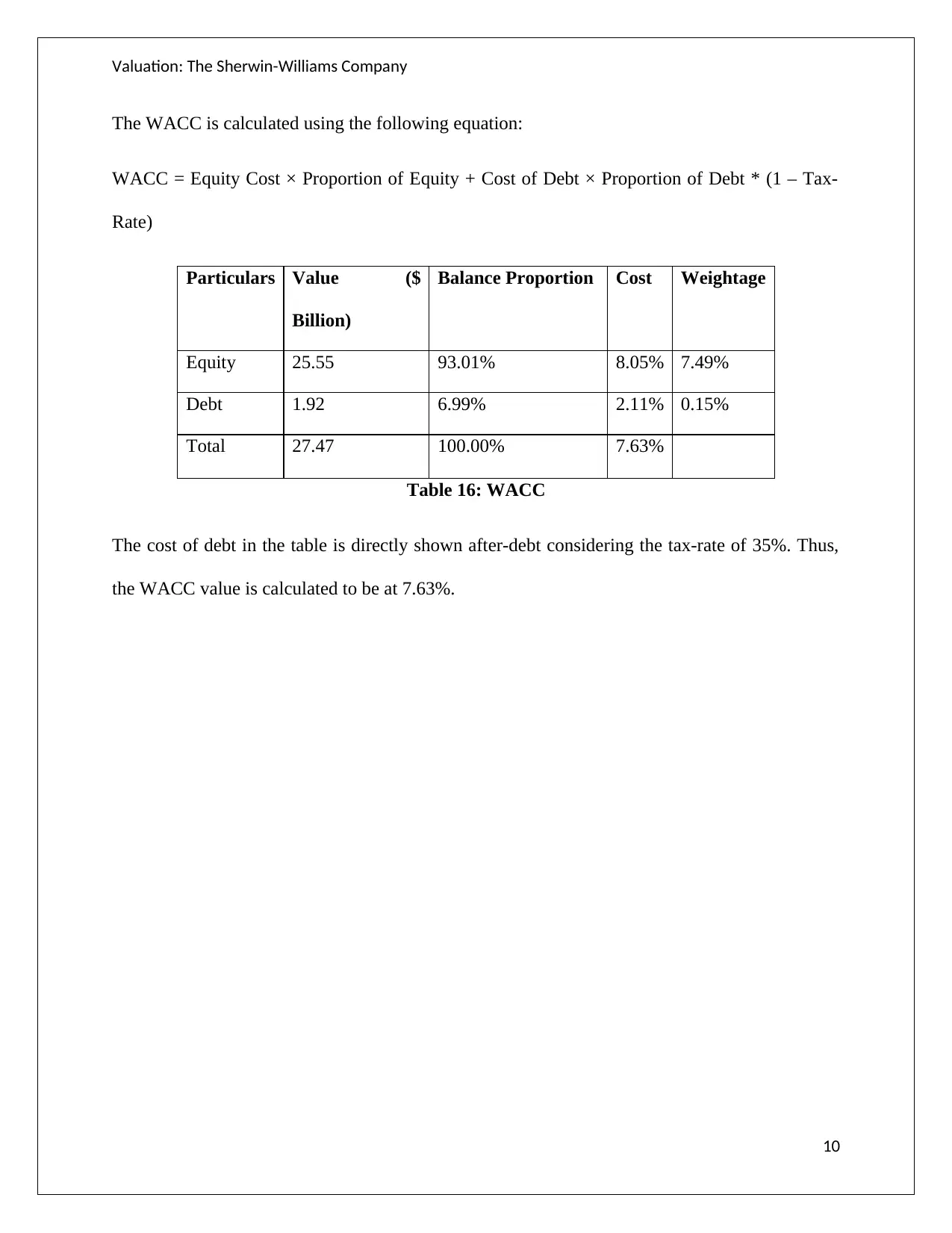

This assignment presents a comprehensive financial valuation of The Sherwin-Williams Company, analyzing its financial performance through various metrics and methodologies. The analysis begins with an examination of key financial ratios, including current ratio, receivable turnover, inventory turnover, fixed assets turnover, debt-equity ratio, operating margin, and net profit margin. The valuation then proceeds to calculate the free cash flow, Return on Equity (RoE), and Weighted Average Cost of Capital (WACC). Furthermore, the report estimates the terminal value, firm value, and intrinsic value per share using discounted cash flow analysis. Economic Value Added (EVA) and Market Value Added (MVA) are also calculated to assess the company's performance. Finally, the assignment examines the dividend payout ratio and applies Gordon's dividend growth model to determine intrinsic value per share. The student provides detailed calculations and interpretations of the financial data, concluding with a sensitivity analysis of the firm value based on different growth rates.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.