Management Accounting: Value Chain Analysis of Natural Pulp Ltd

VerifiedAdded on 2023/06/14

|9

|2055

|289

Report

AI Summary

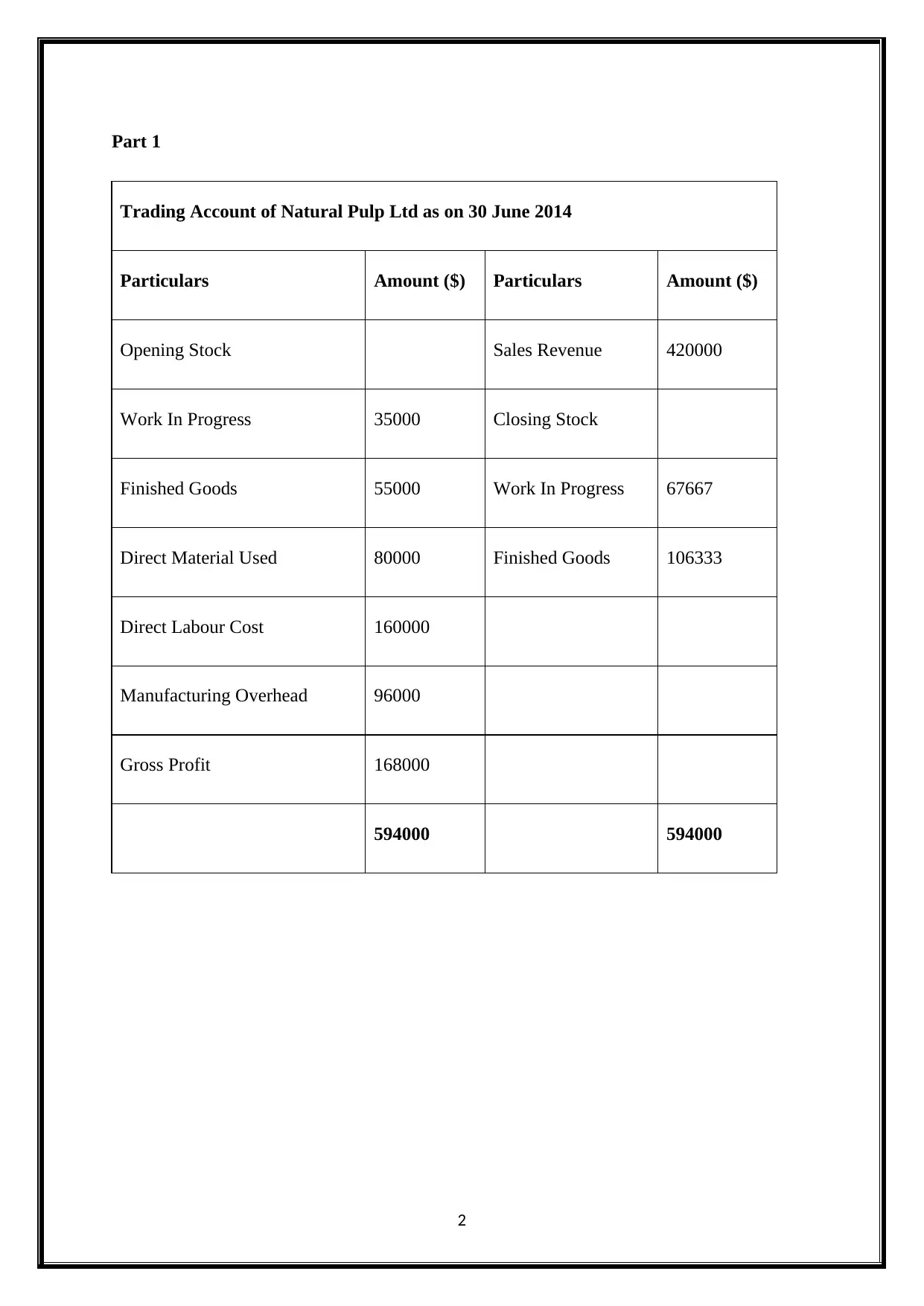

This assignment provides a comprehensive management accounting analysis of Natural Pulp Ltd, beginning with the preparation of a trading account as of June 30, 2014, detailing sales revenue, opening and closing stock, direct material, labor costs, and manufacturing overhead to arrive at a gross profit figure. It then delves into value chain analysis, emphasizing its importance in identifying cost-saving opportunities by adding value at different stages of production. The report outlines the five primary activities essential for value addition and discusses internal cost analysis, including identifying value-creating processes, determining cost portions, identifying cost drivers, linking processes, and evaluating opportunities for cost advantage. It further segments the value chain into inbound logistics, operations, outbound logistics, marketing and sales, and service, explaining the costs associated with each segment. The report also explores the major purposes of the value chain and its implementation in Austal Ships, focusing on building a competitive advantage through cost reduction and efficient resource management. The analysis draws upon various academic sources to support its arguments and provide a well-rounded perspective on management accounting and value chain principles.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.