Indirect Tax Report: VAT Regulations, Calculations, and Adjustments

VerifiedAdded on 2020/12/30

|17

|4018

|396

Report

AI Summary

This report provides a comprehensive analysis of indirect tax, with a specific focus on Value Added Tax (VAT). It begins with an introduction to indirect tax, explaining its nature and examples, and then delves into the specifics of VAT. The report covers key areas such as identifying sources of VAT information, understanding VAT registration requirements, and the information required on business documentation. It also examines the frequency of VAT reporting, and maintaining knowledge of changes to codes of practice, regulation, or legislation. The report includes practical calculations of VAT based on different scenarios, including standard, zero-rated, and exempt supplies, and details the process of completing and submitting VAT returns. Furthermore, it addresses the implications of non-compliance with VAT regulations, including penalties and adjustments for errors. The report also highlights the importance of communicating VAT information to management and advising on changes in VAT legislation. The report concludes with a summary of the key concepts and findings, along with a list of references.

INDIRECT

TAX

TAX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................2

1.1 Identifying sources of information on VAT..........................................................................2

1.2 Examining the manner according to which the organisation should interact with the

Government agency.....................................................................................................................2

1.3 Examining the VAT registration requirements......................................................................2

1.4 Identifying the information that must be included on business documentation of VAT.......2

1.5 Examining the requirements and the frequency of reporting for these VAT........................2

1.6 Maintaining an updated knowledge regarding the changes of codes of practices, regulation

or Legislation...............................................................................................................................2

TASK 2............................................................................................................................................2

2.1 Extracting relevant data for a specific period from the accounting system...........................2

2.2 Calculation regarding relevant inputs and outputs using these VAT classifications.............2

2.3Calculation regarding the VAT due to, or from, the relevant tax authority............................2

2.4 completion and submission a VAT return and any associated payment within the statutory

time

......................................................................................................................................................2

TASK 3............................................................................................................................................2

3.1 Explaining the implications and penalties for an organisation resulting from failure to

abide

......................................................................................................................................................2

by VAT regulations......................................................................................................................2

3.2 Preparing adjustments and declarations for the errors or ommissions identified in previous

VAT periods ................................................................................................................................2

TASK 4 ...........................................................................................................................................2

4.1 Informing the managers regarding the impacts that the VAT payment may have over the

organisation's cash flow and financial forecasts .........................................................................2

4.2 Advising regarding the relevant people of changes in VAT legislation which would have

an effect on over the organisation's recording systems................................................................2

CONCLUSION................................................................................................................................3

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................2

1.1 Identifying sources of information on VAT..........................................................................2

1.2 Examining the manner according to which the organisation should interact with the

Government agency.....................................................................................................................2

1.3 Examining the VAT registration requirements......................................................................2

1.4 Identifying the information that must be included on business documentation of VAT.......2

1.5 Examining the requirements and the frequency of reporting for these VAT........................2

1.6 Maintaining an updated knowledge regarding the changes of codes of practices, regulation

or Legislation...............................................................................................................................2

TASK 2............................................................................................................................................2

2.1 Extracting relevant data for a specific period from the accounting system...........................2

2.2 Calculation regarding relevant inputs and outputs using these VAT classifications.............2

2.3Calculation regarding the VAT due to, or from, the relevant tax authority............................2

2.4 completion and submission a VAT return and any associated payment within the statutory

time

......................................................................................................................................................2

TASK 3............................................................................................................................................2

3.1 Explaining the implications and penalties for an organisation resulting from failure to

abide

......................................................................................................................................................2

by VAT regulations......................................................................................................................2

3.2 Preparing adjustments and declarations for the errors or ommissions identified in previous

VAT periods ................................................................................................................................2

TASK 4 ...........................................................................................................................................2

4.1 Informing the managers regarding the impacts that the VAT payment may have over the

organisation's cash flow and financial forecasts .........................................................................2

4.2 Advising regarding the relevant people of changes in VAT legislation which would have

an effect on over the organisation's recording systems................................................................2

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The indirect tax refers to the tax amount which is mainly collected by the business

organisation in the supply chain(mainly the producers or retailers) and paid to the governmental

tax authorities. But it is actually charged from the consumers as part of the purchase cost of a

good or service. The total amount of tax is divided according to the quantity of the commodity

and the consumer borne the amount of tax imposed on goods and services. Furthermore, the

indirect tax refers to the kind of the tax where the tax amount and it's impact doesn't borne by the

entities(Bahl, 2018). The burden of such tax can be easily shifted from taxpayer to somebody

else. This affects and increase the prices of the goods and services.

The report pertain the knowledge regarding the meaning, source and examples of indirect

tax, Complete VAT returns accurately and in a timely manner, Understanding VAT penalties and

making adjustments for the previous errors and communicating VAT information.

TASK 1

1.1 Identifying sources of information on VAT

Value Added Tax or VAT refers to the ingestion tax which is currently applied on

purchase of goods and services with its value added on all phase of manufacture from production

to the point of sale. The tax of VAT basically paid by a taxable individual is evaluated by

deducting values of all inputs utilize for producing the goods and services from cost of

production. furthermore, VAT is not chargeable in all cities, some cities are free from payments

of VAT tax.

Essential content regarding this is promptly accessible from federal government sites.

Besides this, other relevant source of information is acquirable from HM revenue and customs

(HMRC) portals that is accountable for collecting tax across the entire UK(Cnossen, 2013). All

further relevant information in respect of tax or about any tax related issues is considered by the

HMRC and it renders the solutions for payment of tax by its payers.

1.2 Examining the manner according to which the organisation should interact with the

Government agency

At the time of VAT registration organisations have to follow the important procedures.

These procedures include registration form which is filled by organisation and with the relevant

1

The indirect tax refers to the tax amount which is mainly collected by the business

organisation in the supply chain(mainly the producers or retailers) and paid to the governmental

tax authorities. But it is actually charged from the consumers as part of the purchase cost of a

good or service. The total amount of tax is divided according to the quantity of the commodity

and the consumer borne the amount of tax imposed on goods and services. Furthermore, the

indirect tax refers to the kind of the tax where the tax amount and it's impact doesn't borne by the

entities(Bahl, 2018). The burden of such tax can be easily shifted from taxpayer to somebody

else. This affects and increase the prices of the goods and services.

The report pertain the knowledge regarding the meaning, source and examples of indirect

tax, Complete VAT returns accurately and in a timely manner, Understanding VAT penalties and

making adjustments for the previous errors and communicating VAT information.

TASK 1

1.1 Identifying sources of information on VAT

Value Added Tax or VAT refers to the ingestion tax which is currently applied on

purchase of goods and services with its value added on all phase of manufacture from production

to the point of sale. The tax of VAT basically paid by a taxable individual is evaluated by

deducting values of all inputs utilize for producing the goods and services from cost of

production. furthermore, VAT is not chargeable in all cities, some cities are free from payments

of VAT tax.

Essential content regarding this is promptly accessible from federal government sites.

Besides this, other relevant source of information is acquirable from HM revenue and customs

(HMRC) portals that is accountable for collecting tax across the entire UK(Cnossen, 2013). All

further relevant information in respect of tax or about any tax related issues is considered by the

HMRC and it renders the solutions for payment of tax by its payers.

1.2 Examining the manner according to which the organisation should interact with the

Government agency

At the time of VAT registration organisations have to follow the important procedures.

These procedures include registration form which is filled by organisation and with the relevant

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information. During registration process, user may face issues which are solved by the

government agencies. There are different type of registration form available according to type of

business. For the clarification of that issues government agencies will provide help to the

company.

1.3 Examining the VAT registration requirements

The VAT registration termed as the mandatory requirement for all business persons and

organisations who are engaging in producing and manufacturing of goods and services. VAT

termed as relatively same to the sales tax but its is proportionately more different from the sales

tax as it is charged from the customers once while purchasing of goods and services. There are

several requirements or documenting for the registration of the VAT, which are described

underneath.

Incorporation Certificate of the business entity(In case of company).

Memorandum of Association and Article of Association(only in case of company).

Specifics of people participating in the entity.

Address proof of Director or lease/ rent agreement.

Entity PAN card/ Individual PAN card in case of proprietorship.

Identity evidence of the Directors such as the PAN card/election card/ passport/ driving

license.

Rent Agreement/ lease agreement of the entity/proprietorship.

In case partnership entity- partnership agreement or deed.

Passport size photograph of director of the firm.

1.4 Identifying the information that must be included on business documentation of VAT

After getting the registration for VAT organisation have to obtain several documents and

have to variate the manner of business trade. When an organisation gets it's registration VAT the

organisation have to render the invoice of VAT to each of customer for their convenience. After

the process of registration organisation must follow the regulation 16 that rendered by the

regulatory authority for the issuance of the VAT invoice. There are few contents mentioned

under the regulation 16, which are described below.

An identified number.

The time and date of supplying of goods to be described in invoice.

Date of issuance of document must be mentioned.

2

government agencies. There are different type of registration form available according to type of

business. For the clarification of that issues government agencies will provide help to the

company.

1.3 Examining the VAT registration requirements

The VAT registration termed as the mandatory requirement for all business persons and

organisations who are engaging in producing and manufacturing of goods and services. VAT

termed as relatively same to the sales tax but its is proportionately more different from the sales

tax as it is charged from the customers once while purchasing of goods and services. There are

several requirements or documenting for the registration of the VAT, which are described

underneath.

Incorporation Certificate of the business entity(In case of company).

Memorandum of Association and Article of Association(only in case of company).

Specifics of people participating in the entity.

Address proof of Director or lease/ rent agreement.

Entity PAN card/ Individual PAN card in case of proprietorship.

Identity evidence of the Directors such as the PAN card/election card/ passport/ driving

license.

Rent Agreement/ lease agreement of the entity/proprietorship.

In case partnership entity- partnership agreement or deed.

Passport size photograph of director of the firm.

1.4 Identifying the information that must be included on business documentation of VAT

After getting the registration for VAT organisation have to obtain several documents and

have to variate the manner of business trade. When an organisation gets it's registration VAT the

organisation have to render the invoice of VAT to each of customer for their convenience. After

the process of registration organisation must follow the regulation 16 that rendered by the

regulatory authority for the issuance of the VAT invoice. There are few contents mentioned

under the regulation 16, which are described below.

An identified number.

The time and date of supplying of goods to be described in invoice.

Date of issuance of document must be mentioned.

2

At the top of VAT invoice there must be description about the name, address and

registration number of organisation or supplier must be mentioned.

Along with this the name, address and registration of customer also required to be

mentioned and in case if registration number not available then it may be left blank.

The invoice is required to pertain categories of supply which may be categorised as:

▪ A supply by sale

▪ A supply on hire purchase

▪ A supply by loan

▪ Supply by way of exchange

▪ Supply made through customers material

▪ Supply by sale on commission etc.

he invoice must contain the identification of goods or services supplied.

For every item they must include the rate of tax that is applicable on it in a separate

column.

In separate column MRP and amount of VAT must be entered so as to determine the

value of separately.

It should separately mention any of the cash discount if offered to supplier.

The company should also have maintain the books of accounts which help them to file

the VAT return and if any misstatement is found in the return that has been filed by company

then they have to furnish these books of accounts to authority(Cnossen, 2013). The company

should keep the record of all the invoices that are required by them.

1.5 Examining the requirements and the frequency of reporting for these VAT

Annual accounting scheme:- It refers to the scheme which facilitates services to the

entities for paying the taxes on an annual or yearly basis. Accordance with this scheme, the

taxable person pays their VAT returns only single time in a whole year instead of making t

payments quarterly basis.

Cash accounting scheme: - Basically the differentiated amount between sales invoices

and purchase invoices refers to the net value paid to HMRC as VAT Return. therefore,

accordance with this scheme, the VAT is payable on selling time and rescued when

payment is paid by the supplier by sellers. With the ,motive to be worthy tax payer or

3

registration number of organisation or supplier must be mentioned.

Along with this the name, address and registration of customer also required to be

mentioned and in case if registration number not available then it may be left blank.

The invoice is required to pertain categories of supply which may be categorised as:

▪ A supply by sale

▪ A supply on hire purchase

▪ A supply by loan

▪ Supply by way of exchange

▪ Supply made through customers material

▪ Supply by sale on commission etc.

he invoice must contain the identification of goods or services supplied.

For every item they must include the rate of tax that is applicable on it in a separate

column.

In separate column MRP and amount of VAT must be entered so as to determine the

value of separately.

It should separately mention any of the cash discount if offered to supplier.

The company should also have maintain the books of accounts which help them to file

the VAT return and if any misstatement is found in the return that has been filed by company

then they have to furnish these books of accounts to authority(Cnossen, 2013). The company

should keep the record of all the invoices that are required by them.

1.5 Examining the requirements and the frequency of reporting for these VAT

Annual accounting scheme:- It refers to the scheme which facilitates services to the

entities for paying the taxes on an annual or yearly basis. Accordance with this scheme, the

taxable person pays their VAT returns only single time in a whole year instead of making t

payments quarterly basis.

Cash accounting scheme: - Basically the differentiated amount between sales invoices

and purchase invoices refers to the net value paid to HMRC as VAT Return. therefore,

accordance with this scheme, the VAT is payable on selling time and rescued when

payment is paid by the supplier by sellers. With the ,motive to be worthy tax payer or

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

according to this scheme, VAT tax turnover should not exceed £1.35 million(Delgado,

Lago‐Peñas and Mayor, 2015).

Flat rate scheme:- This scheme is mainly specialised for the simplifying the records like

sales record and purchase record. This scheme facilitates the entities to apply fixed

percent or flat rates on entity's turnover to quantify VAT due. Fixed or flat rate percent

schemes relatively based on the size and category of business. The disparity among the

amount charged and amount paid held with the entities as earned income. Rescue on

VAT must not be asserted for purchasing except for definite capital assets eclipsing

£2,000. With an aim to be a worthy tax payer, according to this scheme, VAT taxable

turnover shouldn't be eclipsed £150,000.

Standard scheme:- According to this methodology entity pays VAT return on quarterly

basis instead of yearly in an accounting period. If any amount is due then it must be paid

on quarterly basis. If any entity have amount of sales higher than the cost of production

then there differentiated amount must be paid HMRC.

1.6 Maintaining an updated knowledge regarding the changes of codes of practices, regulation or

Legislation

All entities requires to adapt the knowledge regarding legislation and codes of best

operation for effectual work. Which are described underneath:

Entities must have adequate knowledge regarding the context of statistics.

Protecting data by computerized or advanced software

Minimising the records or informational data.

Awareness about governance information

Besides this, some essential legislations required to used for these informational data. If

any entity is not so wholly familiar with the legal thinkings then it affects the entity than they to

consult legal person.

Personal data

Sharing and re-use of data

Intellectual property and copyright

Accountability

4

Lago‐Peñas and Mayor, 2015).

Flat rate scheme:- This scheme is mainly specialised for the simplifying the records like

sales record and purchase record. This scheme facilitates the entities to apply fixed

percent or flat rates on entity's turnover to quantify VAT due. Fixed or flat rate percent

schemes relatively based on the size and category of business. The disparity among the

amount charged and amount paid held with the entities as earned income. Rescue on

VAT must not be asserted for purchasing except for definite capital assets eclipsing

£2,000. With an aim to be a worthy tax payer, according to this scheme, VAT taxable

turnover shouldn't be eclipsed £150,000.

Standard scheme:- According to this methodology entity pays VAT return on quarterly

basis instead of yearly in an accounting period. If any amount is due then it must be paid

on quarterly basis. If any entity have amount of sales higher than the cost of production

then there differentiated amount must be paid HMRC.

1.6 Maintaining an updated knowledge regarding the changes of codes of practices, regulation or

Legislation

All entities requires to adapt the knowledge regarding legislation and codes of best

operation for effectual work. Which are described underneath:

Entities must have adequate knowledge regarding the context of statistics.

Protecting data by computerized or advanced software

Minimising the records or informational data.

Awareness about governance information

Besides this, some essential legislations required to used for these informational data. If

any entity is not so wholly familiar with the legal thinkings then it affects the entity than they to

consult legal person.

Personal data

Sharing and re-use of data

Intellectual property and copyright

Accountability

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

2.1 Extracting relevant data for a specific period from the accounting system

1. Informational data for quantification of compatible Input and Output for Regular

Supplies (year 2012-13):

Zoe is under process for completion of her VAT tax for quarterly ended 31 March 2013.

The available information is mentioned underneath:

1. Sales invoices total amount £128,000 was expressed for ensuring the standard rated sales.

Standard rated expenses total amount to £24,800.

On 15 February 2013 Gwen acquired machinery of £24,150. This figure involves the

VAT. Unless stated otherwise all of the above figures are exclusive of VAT.

2. Data for quantification of compatible input and output for exempting the Supply:

Cathy plans to begins trading in future soon. She runs a small aeroplane, and is

considered three alternate kinds of businesses. These are (1) training, under which all sales will

be considered as standard rated for VAT, (2) transport, under which all sales will be zero-rated

for VAT, and (3) an air ambulance service, under which all sales will be exempt from VAT.

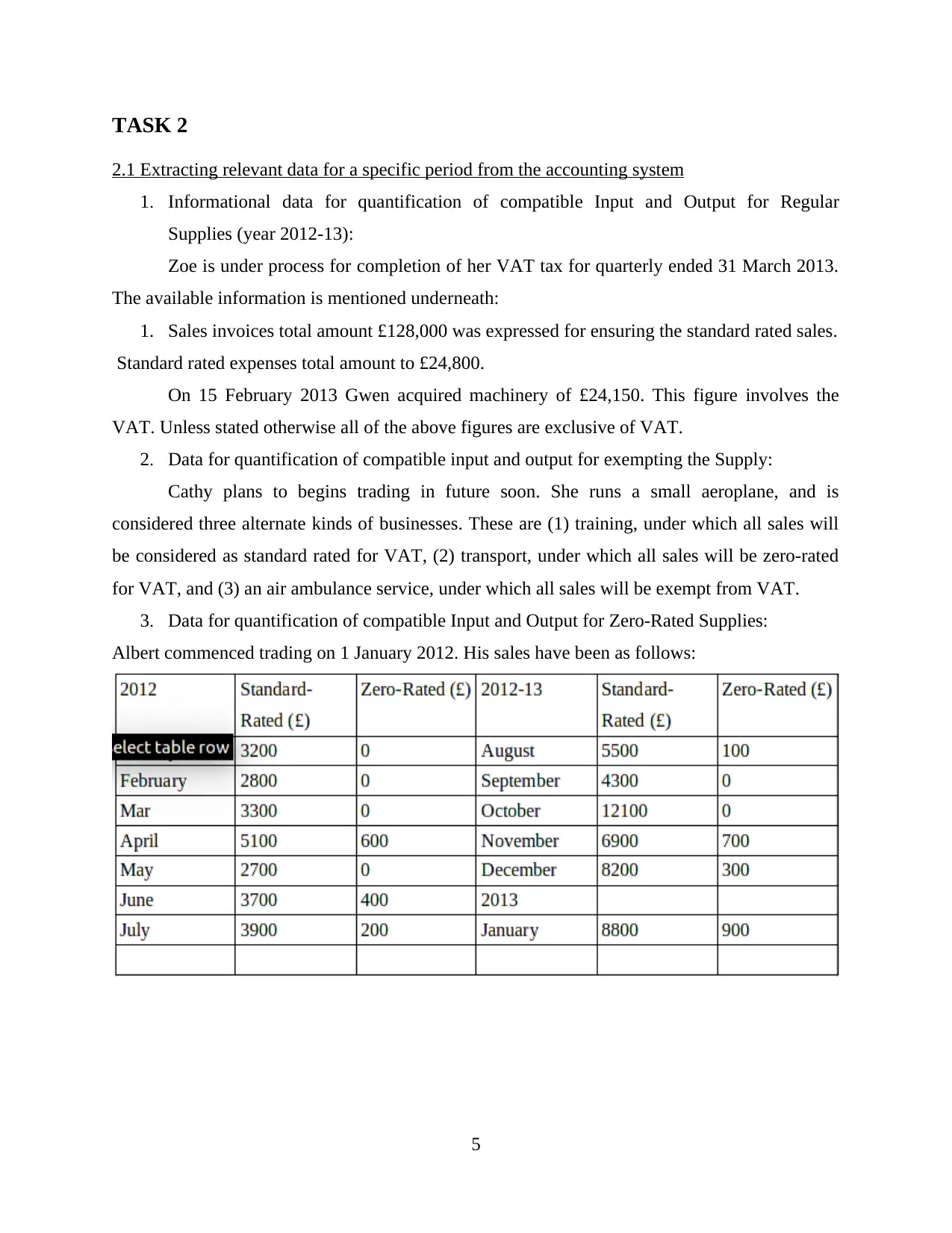

3. Data for quantification of compatible Input and Output for Zero-Rated Supplies:

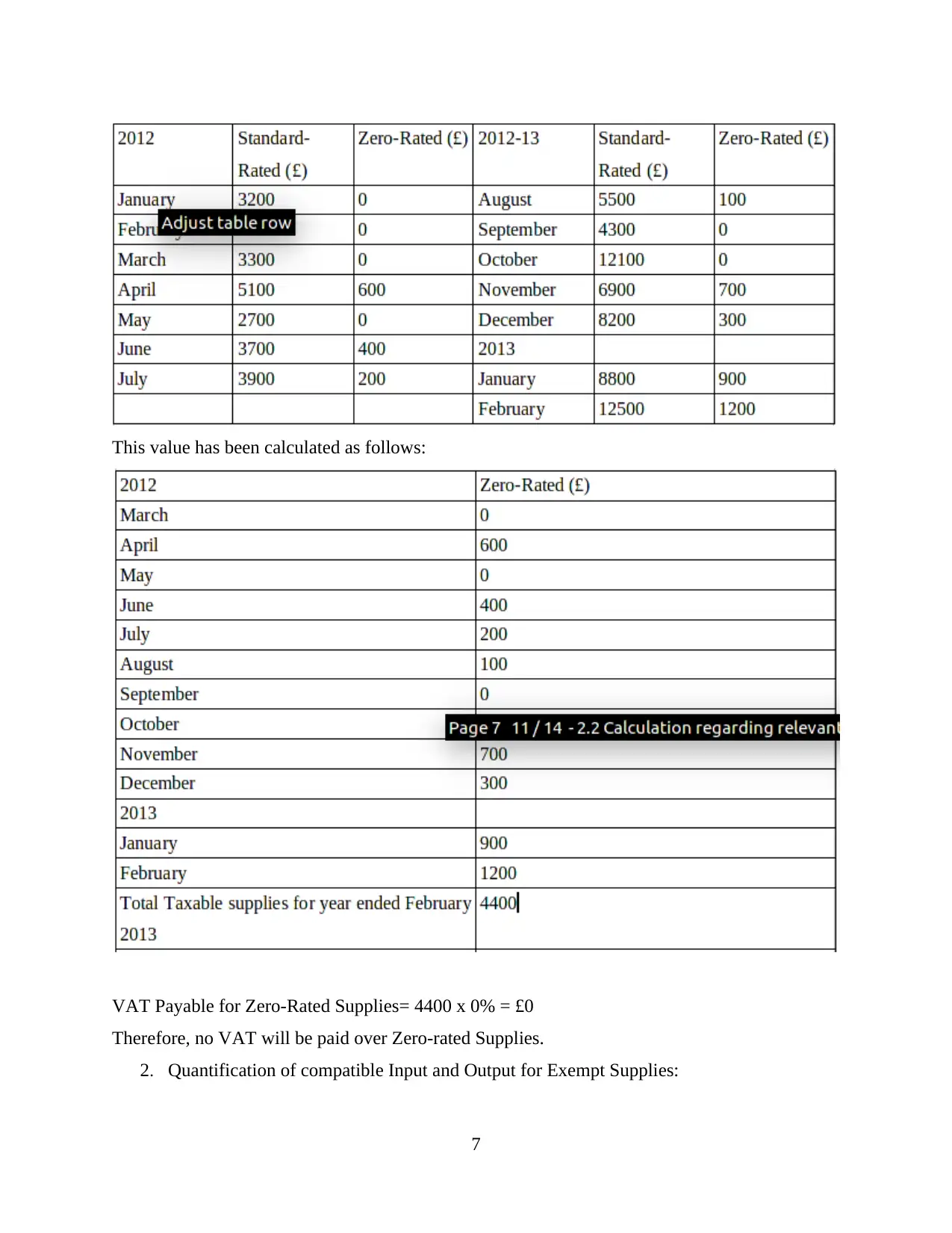

Albert commenced trading on 1 January 2012. His sales have been as follows:

5

2.1 Extracting relevant data for a specific period from the accounting system

1. Informational data for quantification of compatible Input and Output for Regular

Supplies (year 2012-13):

Zoe is under process for completion of her VAT tax for quarterly ended 31 March 2013.

The available information is mentioned underneath:

1. Sales invoices total amount £128,000 was expressed for ensuring the standard rated sales.

Standard rated expenses total amount to £24,800.

On 15 February 2013 Gwen acquired machinery of £24,150. This figure involves the

VAT. Unless stated otherwise all of the above figures are exclusive of VAT.

2. Data for quantification of compatible input and output for exempting the Supply:

Cathy plans to begins trading in future soon. She runs a small aeroplane, and is

considered three alternate kinds of businesses. These are (1) training, under which all sales will

be considered as standard rated for VAT, (2) transport, under which all sales will be zero-rated

for VAT, and (3) an air ambulance service, under which all sales will be exempt from VAT.

3. Data for quantification of compatible Input and Output for Zero-Rated Supplies:

Albert commenced trading on 1 January 2012. His sales have been as follows:

5

4. Data for quantification of Compatible Input and Output for Exports:from VAT is not

applied over the exported goods and services(Keen, 2013). It can be treated as a Zero-

Rated Item for calculation of VAT returns for any registered business.

2.2 Calculation regarding relevant inputs and outputs using these VAT classifications

According to the provisions of The VAT Act, 1994, a basic rate for VAT of 20% is

applied over the price of supply of goods or services. therefore, there are mainly three general

rates applicative over the nature of goods and services:

Deducted VAT rate at 5%

Zero VAT Rate at 0%

Standard VAT Rate at 20%

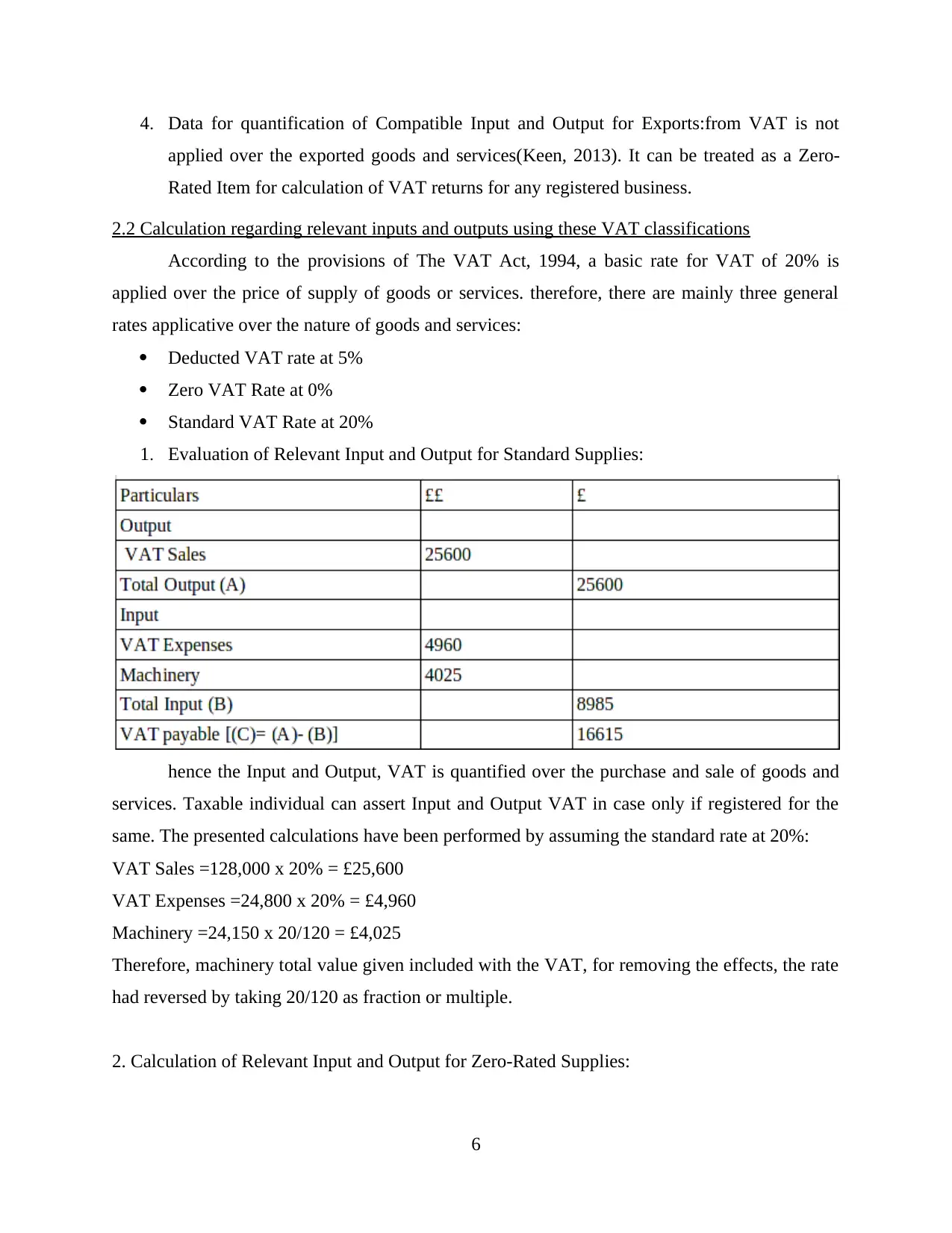

1. Evaluation of Relevant Input and Output for Standard Supplies:

hence the Input and Output, VAT is quantified over the purchase and sale of goods and

services. Taxable individual can assert Input and Output VAT in case only if registered for the

same. The presented calculations have been performed by assuming the standard rate at 20%:

VAT Sales =128,000 x 20% = £25,600

VAT Expenses =24,800 x 20% = £4,960

Machinery =24,150 x 20/120 = £4,025

Therefore, machinery total value given included with the VAT, for removing the effects, the rate

had reversed by taking 20/120 as fraction or multiple.

2. Calculation of Relevant Input and Output for Zero-Rated Supplies:

6

applied over the exported goods and services(Keen, 2013). It can be treated as a Zero-

Rated Item for calculation of VAT returns for any registered business.

2.2 Calculation regarding relevant inputs and outputs using these VAT classifications

According to the provisions of The VAT Act, 1994, a basic rate for VAT of 20% is

applied over the price of supply of goods or services. therefore, there are mainly three general

rates applicative over the nature of goods and services:

Deducted VAT rate at 5%

Zero VAT Rate at 0%

Standard VAT Rate at 20%

1. Evaluation of Relevant Input and Output for Standard Supplies:

hence the Input and Output, VAT is quantified over the purchase and sale of goods and

services. Taxable individual can assert Input and Output VAT in case only if registered for the

same. The presented calculations have been performed by assuming the standard rate at 20%:

VAT Sales =128,000 x 20% = £25,600

VAT Expenses =24,800 x 20% = £4,960

Machinery =24,150 x 20/120 = £4,025

Therefore, machinery total value given included with the VAT, for removing the effects, the rate

had reversed by taking 20/120 as fraction or multiple.

2. Calculation of Relevant Input and Output for Zero-Rated Supplies:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This value has been calculated as follows:

VAT Payable for Zero-Rated Supplies= 4400 x 0% = £0

Therefore, no VAT will be paid over Zero-rated Supplies.

2. Quantification of compatible Input and Output for Exempt Supplies:

7

VAT Payable for Zero-Rated Supplies= 4400 x 0% = £0

Therefore, no VAT will be paid over Zero-rated Supplies.

2. Quantification of compatible Input and Output for Exempt Supplies:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As the Exempt Supplies like an air ambulance service are not worthy for any tax levy

under VAT. Cathy wouldn't be require or permit to register under VAT as she would not be

operating taxable supplies. Similarly, Output VAT will not be due and no input VAT will be

eligible for reclaims from HMRC as per regulations.

2.3Calculation regarding the VAT due to, or from, the relevant tax authority

Standard Supplies:

VAT will be quantified at basic applied rate of 20%. Zoe will obligated to make payment

of £16,615 as her VAT tax accordance with quarterly basis to HMRC.

Zero-Rated Supplies:

According to the Zero-Rated supply pertain 0% of VAT rate app on them, Albert will

not be liable to pay any tax to HMRC as his VAT tax for the year(Kenyon, Langley and Paquin,

2012). Therefore, he shall have to make a payment 20% VAT over Standard-Rated Supplies and

also render relevant notification in situation of it's standard-rated supplies exceed £77,000.

Exempt Supplies:

Exempt supplies are tax immune from VAT. This all can involves supplies like

ambulance, in such case, Cathy would not be obligate to make a payment nor permitted to pay

any tax return to HMRC as his VAT return for the year.

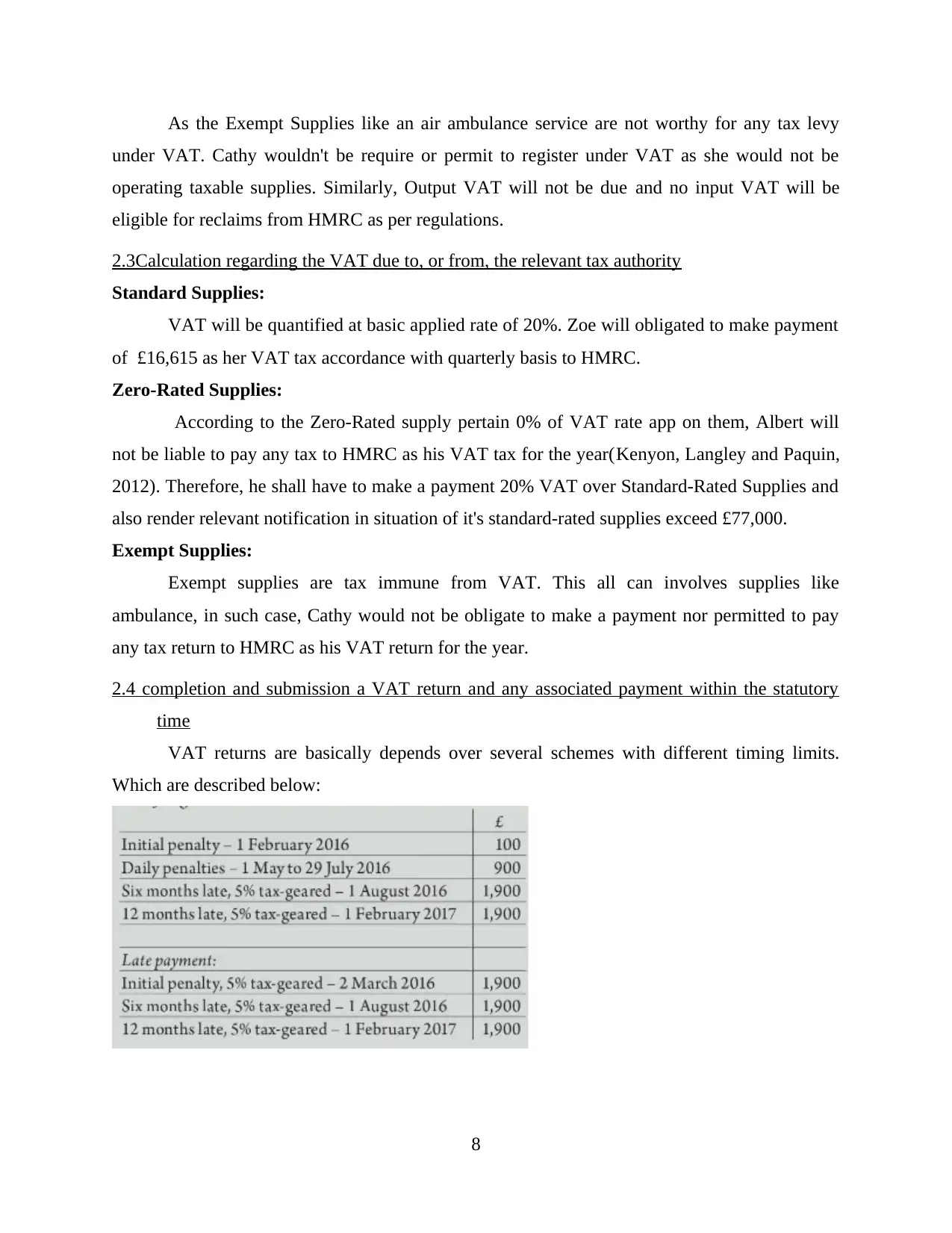

2.4 completion and submission a VAT return and any associated payment within the statutory

time

VAT returns are basically depends over several schemes with different timing limits.

Which are described below:

8

under VAT. Cathy wouldn't be require or permit to register under VAT as she would not be

operating taxable supplies. Similarly, Output VAT will not be due and no input VAT will be

eligible for reclaims from HMRC as per regulations.

2.3Calculation regarding the VAT due to, or from, the relevant tax authority

Standard Supplies:

VAT will be quantified at basic applied rate of 20%. Zoe will obligated to make payment

of £16,615 as her VAT tax accordance with quarterly basis to HMRC.

Zero-Rated Supplies:

According to the Zero-Rated supply pertain 0% of VAT rate app on them, Albert will

not be liable to pay any tax to HMRC as his VAT tax for the year(Kenyon, Langley and Paquin,

2012). Therefore, he shall have to make a payment 20% VAT over Standard-Rated Supplies and

also render relevant notification in situation of it's standard-rated supplies exceed £77,000.

Exempt Supplies:

Exempt supplies are tax immune from VAT. This all can involves supplies like

ambulance, in such case, Cathy would not be obligate to make a payment nor permitted to pay

any tax return to HMRC as his VAT return for the year.

2.4 completion and submission a VAT return and any associated payment within the statutory

time

VAT returns are basically depends over several schemes with different timing limits.

Which are described below:

8

TASK 3

3.1 Explaining the implications and penalties for an organisation resulting from failure to abide

by VAT regulations

Value Added Tax is regulated and controlled by The VAT Act, 1994 that defines the

categories of business entities, classified the supplies, calculating the Input and Output

according to the described rates and therefore the penalty and legal actioning, that the relevant

tax authority can legally takes against entities in case of defaulters. HM Revenues and Customs

are mainly responsive for collecting and amounts of taxes that renders the way on which

penalties will be applicable on defaulters.

A business entity makes initially a default in payment up to 12 months will make with a

cautionary instead of penalty from taxation authorities according to the section 59 known default

surcharge. In case the business entity had been default frequently, direct penalty will levied on

them(Lam and Ravussin, 2017). A day or month late payment will enforce same actions on both

cases.

A day late defaults force penalty of £100 automatic imposed by the system.

In partnership firms, £100 penalty is to be imposed on each partner Instead of entire

partnership firm. Only the active partner can request under any given circumstance rather

than individual partners.

Daily penalties of £10 per day for 90 days will be imposed over the business entity if

unable to pay returns to tax authorities up to 3 months. In case 6 months delay since the date of

paying return, an addition of 5% of tax due or £300, which may be higher will imposed which

will amount to another 5% levy or £300, whichever is higher.

3.2 Preparing adjustments and declarations for the errors or omissions identified in previous

VAT periods

Errors or omissions identified in previous

VAT periods:

Disclosing the errors, omissions or any type of deficiencies are essential. Such errors will

be reportable with filing a form VAT652 and submitted to VAT rectification Team. They are

categorised below:

an error identified that is above the reporting threshold.

9

3.1 Explaining the implications and penalties for an organisation resulting from failure to abide

by VAT regulations

Value Added Tax is regulated and controlled by The VAT Act, 1994 that defines the

categories of business entities, classified the supplies, calculating the Input and Output

according to the described rates and therefore the penalty and legal actioning, that the relevant

tax authority can legally takes against entities in case of defaulters. HM Revenues and Customs

are mainly responsive for collecting and amounts of taxes that renders the way on which

penalties will be applicable on defaulters.

A business entity makes initially a default in payment up to 12 months will make with a

cautionary instead of penalty from taxation authorities according to the section 59 known default

surcharge. In case the business entity had been default frequently, direct penalty will levied on

them(Lam and Ravussin, 2017). A day or month late payment will enforce same actions on both

cases.

A day late defaults force penalty of £100 automatic imposed by the system.

In partnership firms, £100 penalty is to be imposed on each partner Instead of entire

partnership firm. Only the active partner can request under any given circumstance rather

than individual partners.

Daily penalties of £10 per day for 90 days will be imposed over the business entity if

unable to pay returns to tax authorities up to 3 months. In case 6 months delay since the date of

paying return, an addition of 5% of tax due or £300, which may be higher will imposed which

will amount to another 5% levy or £300, whichever is higher.

3.2 Preparing adjustments and declarations for the errors or omissions identified in previous

VAT periods

Errors or omissions identified in previous

VAT periods:

Disclosing the errors, omissions or any type of deficiencies are essential. Such errors will

be reportable with filing a form VAT652 and submitted to VAT rectification Team. They are

categorised below:

an error identified that is above the reporting threshold.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.