Indirect Tax and VAT Regulations Report for Aviva International

VerifiedAdded on 2020/11/23

|13

|4222

|321

Report

AI Summary

This report provides a comprehensive analysis of Value-Added Tax (VAT) regulations and their application to Aviva International Insurance Limited, a UK-based financial services company. It delves into the sources of information on VAT, emphasizing the role of HMRC and online resources. The report outlines VAT registration requirements, including necessary documentation, and explains the information that must be included on business documentation for VAT-registered entities. It also covers the requirements and frequency of reporting VAT schemes, such as the standard and flat rate schemes, and the importance of maintaining up-to-date knowledge of changes in codes of practice, regulations, and legislation. The report further explores the extraction of relevant data from accounting systems for VAT returns, the calculation of input and output VAT, and the completion and submission of VAT returns within statutory time limits. Additionally, it examines the implications and penalties for non-compliance with VAT regulations, as well as adjustments for errors or omissions. The report concludes by highlighting the importance of informing managers about the impact of VAT payments on cash flow and financial forecasts, and advising on changes in VAT legislation. Calculations for both standard and zero-rated supplies are included. The report emphasizes the importance of compliance with VAT regulations for businesses.

Indirect Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of information on VAT............................................................................................1

1.2 Organisation should interact with the relevant government agency.....................................1

1.3 VAT registration requirements.............................................................................................2

1.4 Information that must be included on business documentation of VAT registered

businesses....................................................................................................................................2

1.5 Requirements and the frequency of reporting VAT schemes...............................................3

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extract relevant data for a specific period from the accounting system...............................4

2.2 Inputs and outputs using these VAT ....................................................................................5

2.3 Calculation of VAT due to, or from, the relevant tax authority............................................7

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits............................................................................................................................................7

TASK 3............................................................................................................................................8

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................8

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods.........................................................................................................................................8

TASK 4 ...........................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts........................................................................................................9

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording system.......................................................................................................................10

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of information on VAT............................................................................................1

1.2 Organisation should interact with the relevant government agency.....................................1

1.3 VAT registration requirements.............................................................................................2

1.4 Information that must be included on business documentation of VAT registered

businesses....................................................................................................................................2

1.5 Requirements and the frequency of reporting VAT schemes...............................................3

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extract relevant data for a specific period from the accounting system...............................4

2.2 Inputs and outputs using these VAT ....................................................................................5

2.3 Calculation of VAT due to, or from, the relevant tax authority............................................7

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits............................................................................................................................................7

TASK 3............................................................................................................................................8

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................8

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods.........................................................................................................................................8

TASK 4 ...........................................................................................................................................9

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts........................................................................................................9

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording system.......................................................................................................................10

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

The indirect taxes are introduce as the levies made by state and central government on the

services, consumption, expenditure, privileges and rights yet not on the income or property

(Adema, Fron and Ladaique, 2014). For this report, chosen organisation is Aviva International

Insurance Limited which is a financial service industry and headquartered in London , UK. It

was established in 2000 by Sir Adrian Montague. This report divided into different parts which

includes concept of VAT regulations, and completion of VAT returns in timely and accurate

manner. Along with this, concept of VAT penalties and information related to this also covered

in this report.

TASK 1

1.1 Sources of information on VAT

In the UK, the Value-added tax (VAT) is introduce as the third-largest source of

government revenue and it was introduced in 1973. VAT is administered and gathered by HM

revenue and customs, firstly via the value added tax act 1994. It is levied on services provided by

the Aviva International Insurance Limited and imported from outside the EU. In addition, it is

collected and assessed on the value of services or goods that have been given every time there is

a transaction (Albayrak, 2017). In different countries, VAT are identify as a key revenue sources

as high rate of unemployment and low per capital income give other income sources inadequate.

One of the main source of information on VAT is HMRC pages of the United

Government websites like www.gov.uk. This authority cover entire taxes, where advice, notes,

publications and guidance are present to download. HMRC pages are mainly expect taxpayers to

identify the answers to any questions or queries on their own website (Bargain and et. al., 2015).

Yet, there is web chat facility and telephone enquiry line that can easily deal with unanswered

issues. Taxpayers can also apply an online enquiry form and also write to HMRC pages by post

for guidance.

1.2 Organisation should interact with the relevant government agency

Company should apply different rules and regulations for running their business

operations and activities in specific nation successfully. Government agency related to the value-

added tax is HMRC that play vital role in dealing with different number of taxes such as service

tax, VAT etc. Therefore all these taxes are essential and beneficial for the company to should

1

The indirect taxes are introduce as the levies made by state and central government on the

services, consumption, expenditure, privileges and rights yet not on the income or property

(Adema, Fron and Ladaique, 2014). For this report, chosen organisation is Aviva International

Insurance Limited which is a financial service industry and headquartered in London , UK. It

was established in 2000 by Sir Adrian Montague. This report divided into different parts which

includes concept of VAT regulations, and completion of VAT returns in timely and accurate

manner. Along with this, concept of VAT penalties and information related to this also covered

in this report.

TASK 1

1.1 Sources of information on VAT

In the UK, the Value-added tax (VAT) is introduce as the third-largest source of

government revenue and it was introduced in 1973. VAT is administered and gathered by HM

revenue and customs, firstly via the value added tax act 1994. It is levied on services provided by

the Aviva International Insurance Limited and imported from outside the EU. In addition, it is

collected and assessed on the value of services or goods that have been given every time there is

a transaction (Albayrak, 2017). In different countries, VAT are identify as a key revenue sources

as high rate of unemployment and low per capital income give other income sources inadequate.

One of the main source of information on VAT is HMRC pages of the United

Government websites like www.gov.uk. This authority cover entire taxes, where advice, notes,

publications and guidance are present to download. HMRC pages are mainly expect taxpayers to

identify the answers to any questions or queries on their own website (Bargain and et. al., 2015).

Yet, there is web chat facility and telephone enquiry line that can easily deal with unanswered

issues. Taxpayers can also apply an online enquiry form and also write to HMRC pages by post

for guidance.

1.2 Organisation should interact with the relevant government agency

Company should apply different rules and regulations for running their business

operations and activities in specific nation successfully. Government agency related to the value-

added tax is HMRC that play vital role in dealing with different number of taxes such as service

tax, VAT etc. Therefore all these taxes are essential and beneficial for the company to should

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

follow this and achieve better outcomes within predetermined period of time (Capéau, Decoster

and Phillips, 2014). HMRC is a government agency that direct interact with the company in

describing different number of indirect taxes including custom tax, VAT, services tax and many

other relevant tax. All these are identify as a main expenditure which should pay by company in

more. Therefore, in this different department of such type of government agency recruit

knowledge and experienced person who can easily solve such type of issue and help them in

accomplishing long term goals and objectives.

1.3 VAT registration requirements

VAT registration is mandatory for any enterprise if they register in this the income earned

in any consecutive 12 month period of time exceeded (Duclos, Makdissi and Araar, 2014). There

are different major requirements and documents for VAT registration which should followed by

each and every organisation. Some requirement are determined as under:

Incorporation certificate of company

MoA and AoA is require

Particulars of employees involved in the organisation

Address Proof of business owner or director

Company PAN card or Individual PAN card in case of proprietorship

ID Proof of business director including different documents such as Passport, Driving

licenses, Election card, Pan Card etc.

Lease, rental or proprietorship agreement of company

If business are owned by two and more partners, company should require partnership

deed.

Passport size photograph is also require by the director of company.

Therefore, above mentioned all these are identify main requirement for an organisation to

register for VAT. It is important and beneficial for the company to charge VAT on services and

goods sold to clients (Dustmann and Frattini, 2014). They also recover Value-added tax charged

on services and goods buy for the businesses from suppliers, other business etc.

1.4 Information that must be included on business documentation of VAT registered businesses

Value-added tax is followed to both services and goods in specific nations and is covered

in the final price of product and service. It is charged at the rate of 12.5%. Along with this, VAT

registered business must gather value-added tax from clients, submit such type of tax return and

2

and Phillips, 2014). HMRC is a government agency that direct interact with the company in

describing different number of indirect taxes including custom tax, VAT, services tax and many

other relevant tax. All these are identify as a main expenditure which should pay by company in

more. Therefore, in this different department of such type of government agency recruit

knowledge and experienced person who can easily solve such type of issue and help them in

accomplishing long term goals and objectives.

1.3 VAT registration requirements

VAT registration is mandatory for any enterprise if they register in this the income earned

in any consecutive 12 month period of time exceeded (Duclos, Makdissi and Araar, 2014). There

are different major requirements and documents for VAT registration which should followed by

each and every organisation. Some requirement are determined as under:

Incorporation certificate of company

MoA and AoA is require

Particulars of employees involved in the organisation

Address Proof of business owner or director

Company PAN card or Individual PAN card in case of proprietorship

ID Proof of business director including different documents such as Passport, Driving

licenses, Election card, Pan Card etc.

Lease, rental or proprietorship agreement of company

If business are owned by two and more partners, company should require partnership

deed.

Passport size photograph is also require by the director of company.

Therefore, above mentioned all these are identify main requirement for an organisation to

register for VAT. It is important and beneficial for the company to charge VAT on services and

goods sold to clients (Dustmann and Frattini, 2014). They also recover Value-added tax charged

on services and goods buy for the businesses from suppliers, other business etc.

1.4 Information that must be included on business documentation of VAT registered businesses

Value-added tax is followed to both services and goods in specific nations and is covered

in the final price of product and service. It is charged at the rate of 12.5%. Along with this, VAT

registered business must gather value-added tax from clients, submit such type of tax return and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

pay any value-added tax that they owe to the revenue division of the ministry of finance. Beside

this, VAT registered company can deduct any kind of VAT that they give when buying services

and goods for the organisation from the value-added tax that they gather from clients. If the VAT

amount that an enterprise gives is more than they gather, the country revenue division will return

the balance (Fabbri, 2015). For example: Business or individuals that sell services or goods

worth approximately $ 500,000.00 or more in 12 month period of time must register for VAT.

Business must also register or listed if they forecast net sales of $ 500,000.00 or addition in a 12

month. Registered business organisation that give up trading or transfer their enterprise must

follow for cancellation of value-added tax registration. Along with, this also follow company that

no longer yield revenue or income above the threshold amount of $ 500,000.00. There are some

importance information that must be included on business documentation (Aviva International

Insurance Limited) of VAT registered businesses are determined as under:

Completed VAT 1 application form subscribed by business director.

Completed VAT 2 application form, with the actual names, home addresses and

signatures of each and every directors.

Accountant’s name, address and contact numbers.

Main customers’ names, addresses and contact numbers etc.

1.5 Requirements and the frequency of reporting VAT schemes

There are different number of VAT schemes that are require by each and every company.

Value-added schemes are mainly depending on business type and size (Jiang and Shao, 2014).

In Aviva International Insurance Limited, there are some important VAT schemes which are

shown as under:

Standard Value-added tax scheme: It is mainly apply when the invoice is raised. So

when an organisation raise their sale invoice, it would automatically be covered in the next

value-added tax return (Keen, 2013). For example: If an organisation are guilty for putting via all

of their expenditure for value-added tax, whilst keeping back from modifying their sales

invoices, before moving their value-added tax return, to hold their value-added tax as low as

possible.

Flat rate scheme: It introduce as an another important scheme of VAT that HMRC has

given for smaller enterprise. The turnover must be under £150,000 to attend such scheme and if

the turnover rate threshold reaches about £230,000, the company must leave the scheme.

3

this, VAT registered company can deduct any kind of VAT that they give when buying services

and goods for the organisation from the value-added tax that they gather from clients. If the VAT

amount that an enterprise gives is more than they gather, the country revenue division will return

the balance (Fabbri, 2015). For example: Business or individuals that sell services or goods

worth approximately $ 500,000.00 or more in 12 month period of time must register for VAT.

Business must also register or listed if they forecast net sales of $ 500,000.00 or addition in a 12

month. Registered business organisation that give up trading or transfer their enterprise must

follow for cancellation of value-added tax registration. Along with, this also follow company that

no longer yield revenue or income above the threshold amount of $ 500,000.00. There are some

importance information that must be included on business documentation (Aviva International

Insurance Limited) of VAT registered businesses are determined as under:

Completed VAT 1 application form subscribed by business director.

Completed VAT 2 application form, with the actual names, home addresses and

signatures of each and every directors.

Accountant’s name, address and contact numbers.

Main customers’ names, addresses and contact numbers etc.

1.5 Requirements and the frequency of reporting VAT schemes

There are different number of VAT schemes that are require by each and every company.

Value-added schemes are mainly depending on business type and size (Jiang and Shao, 2014).

In Aviva International Insurance Limited, there are some important VAT schemes which are

shown as under:

Standard Value-added tax scheme: It is mainly apply when the invoice is raised. So

when an organisation raise their sale invoice, it would automatically be covered in the next

value-added tax return (Keen, 2013). For example: If an organisation are guilty for putting via all

of their expenditure for value-added tax, whilst keeping back from modifying their sales

invoices, before moving their value-added tax return, to hold their value-added tax as low as

possible.

Flat rate scheme: It introduce as an another important scheme of VAT that HMRC has

given for smaller enterprise. The turnover must be under £150,000 to attend such scheme and if

the turnover rate threshold reaches about £230,000, the company must leave the scheme.

3

Sometime, it is essential and important for the company by reducing burden of detail information

related to sales and purchase.

VAT Frequencies: It is identify as an essential for the company to describe their choice

about when they report their VAT returns. Beside this, HMRC can insist that an organisation

follows a monthly reporting frequency if the business director had previously had an entity that

went bankrupt, owing HMRC money (Kumar, 2014). Company can also call for HMRC to align

their value-added tax return reporting time in relation with their accounting year end. Therefore,

this makes it more easier for the financier to reconcile the VAT account at the ending year,

whilst setting the accounts. This can be completed whilst registering for value-added tax.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Changes in code of practice, legislation and regulation are highly effect on business

performance and activities in direct manner. Thus, it is a role of company to should aware and

have up-to-date knowledge about all legislation related to the VAT. It is suggested to have an

appropriate knowledge about different rules and regulations as well as codes of practices also

that are given by the government of UK. Therefore, company should follow all changes in

legislation or regulation systematic and accomplish better results within predetermined time

period (Li and Whalley, 2012). This also supports to keep entire informations about the finance

that relates to taxes in more accurate way. Any modification in the regulations and rules of

government may decrease loop gap that are existing in actual law. Thence for following changes

and variation in regulations more effectively, it is essential to maintain an up-to-date knowledge

and understanding about codes of practices. Chances of errors are reduced and misunderstanding

in the company decrease when each and every people in the business is aware regarding

alteration in the Statute or Civil law. Measurement of taxes according to new legislation also

support to decrease intervention of legal authority in business activities.

TASK 2

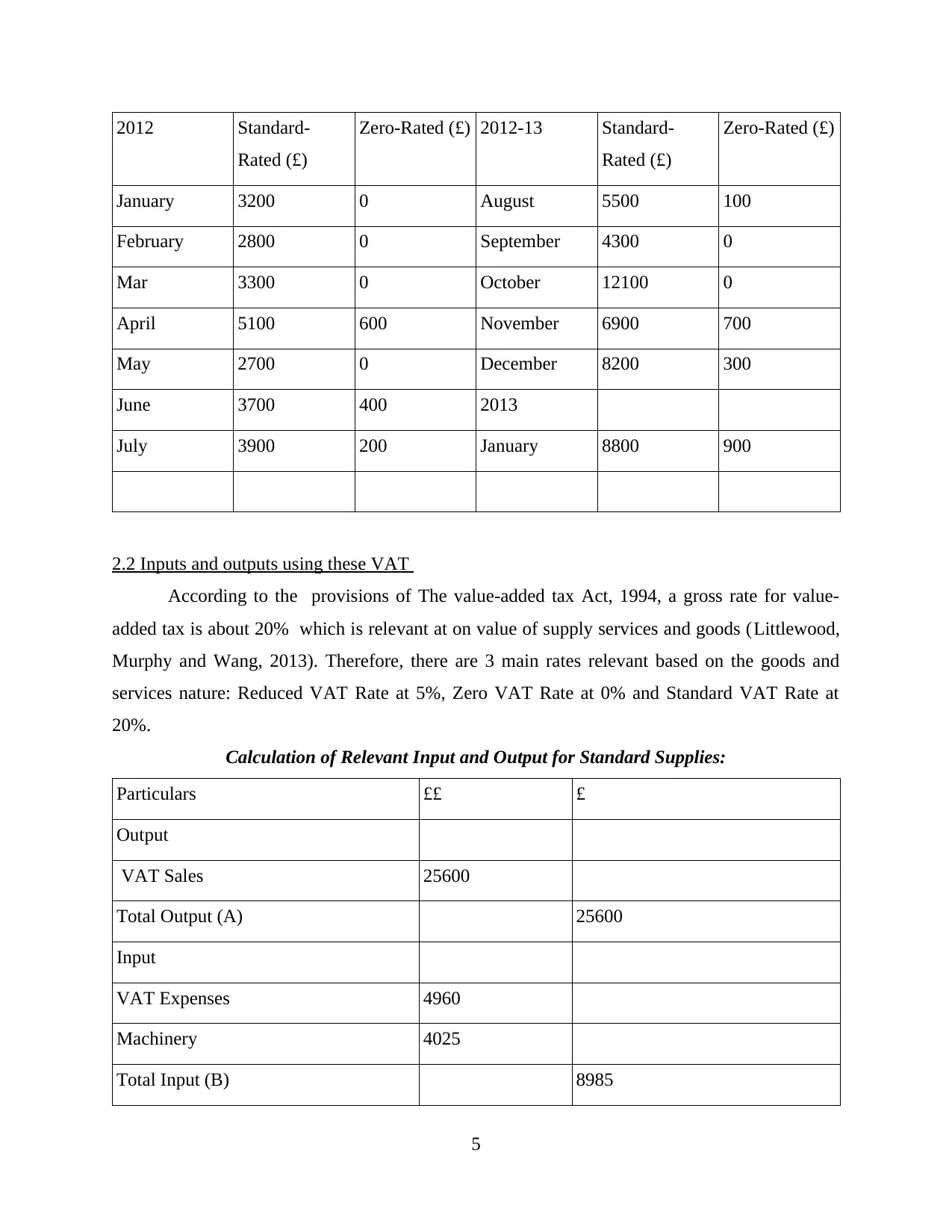

2.1 Extract relevant data for a specific period from the accounting system

In the United Kingdom, value-added tax returns can be suggest in monthly and quarterly

basis. Different number of returns are done on a quarterly basis. Following are the identify as an

important details for the extraction of accurate data or information for filing the VAT return for

the quarter ending 31st December.

4

related to sales and purchase.

VAT Frequencies: It is identify as an essential for the company to describe their choice

about when they report their VAT returns. Beside this, HMRC can insist that an organisation

follows a monthly reporting frequency if the business director had previously had an entity that

went bankrupt, owing HMRC money (Kumar, 2014). Company can also call for HMRC to align

their value-added tax return reporting time in relation with their accounting year end. Therefore,

this makes it more easier for the financier to reconcile the VAT account at the ending year,

whilst setting the accounts. This can be completed whilst registering for value-added tax.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Changes in code of practice, legislation and regulation are highly effect on business

performance and activities in direct manner. Thus, it is a role of company to should aware and

have up-to-date knowledge about all legislation related to the VAT. It is suggested to have an

appropriate knowledge about different rules and regulations as well as codes of practices also

that are given by the government of UK. Therefore, company should follow all changes in

legislation or regulation systematic and accomplish better results within predetermined time

period (Li and Whalley, 2012). This also supports to keep entire informations about the finance

that relates to taxes in more accurate way. Any modification in the regulations and rules of

government may decrease loop gap that are existing in actual law. Thence for following changes

and variation in regulations more effectively, it is essential to maintain an up-to-date knowledge

and understanding about codes of practices. Chances of errors are reduced and misunderstanding

in the company decrease when each and every people in the business is aware regarding

alteration in the Statute or Civil law. Measurement of taxes according to new legislation also

support to decrease intervention of legal authority in business activities.

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

In the United Kingdom, value-added tax returns can be suggest in monthly and quarterly

basis. Different number of returns are done on a quarterly basis. Following are the identify as an

important details for the extraction of accurate data or information for filing the VAT return for

the quarter ending 31st December.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2012 Standard-

Rated (£)

Zero-Rated (£) 2012-13 Standard-

Rated (£)

Zero-Rated (£)

January 3200 0 August 5500 100

February 2800 0 September 4300 0

Mar 3300 0 October 12100 0

April 5100 600 November 6900 700

May 2700 0 December 8200 300

June 3700 400 2013

July 3900 200 January 8800 900

2.2 Inputs and outputs using these VAT

According to the provisions of The value-added tax Act, 1994, a gross rate for value-

added tax is about 20% which is relevant at on value of supply services and goods (Littlewood,

Murphy and Wang, 2013). Therefore, there are 3 main rates relevant based on the goods and

services nature: Reduced VAT Rate at 5%, Zero VAT Rate at 0% and Standard VAT Rate at

20%.

Calculation of Relevant Input and Output for Standard Supplies:

Particulars ££ £

Output

VAT Sales 25600

Total Output (A) 25600

Input

VAT Expenses 4960

Machinery 4025

Total Input (B) 8985

5

Rated (£)

Zero-Rated (£) 2012-13 Standard-

Rated (£)

Zero-Rated (£)

January 3200 0 August 5500 100

February 2800 0 September 4300 0

Mar 3300 0 October 12100 0

April 5100 600 November 6900 700

May 2700 0 December 8200 300

June 3700 400 2013

July 3900 200 January 8800 900

2.2 Inputs and outputs using these VAT

According to the provisions of The value-added tax Act, 1994, a gross rate for value-

added tax is about 20% which is relevant at on value of supply services and goods (Littlewood,

Murphy and Wang, 2013). Therefore, there are 3 main rates relevant based on the goods and

services nature: Reduced VAT Rate at 5%, Zero VAT Rate at 0% and Standard VAT Rate at

20%.

Calculation of Relevant Input and Output for Standard Supplies:

Particulars ££ £

Output

VAT Sales 25600

Total Output (A) 25600

Input

VAT Expenses 4960

Machinery 4025

Total Input (B) 8985

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

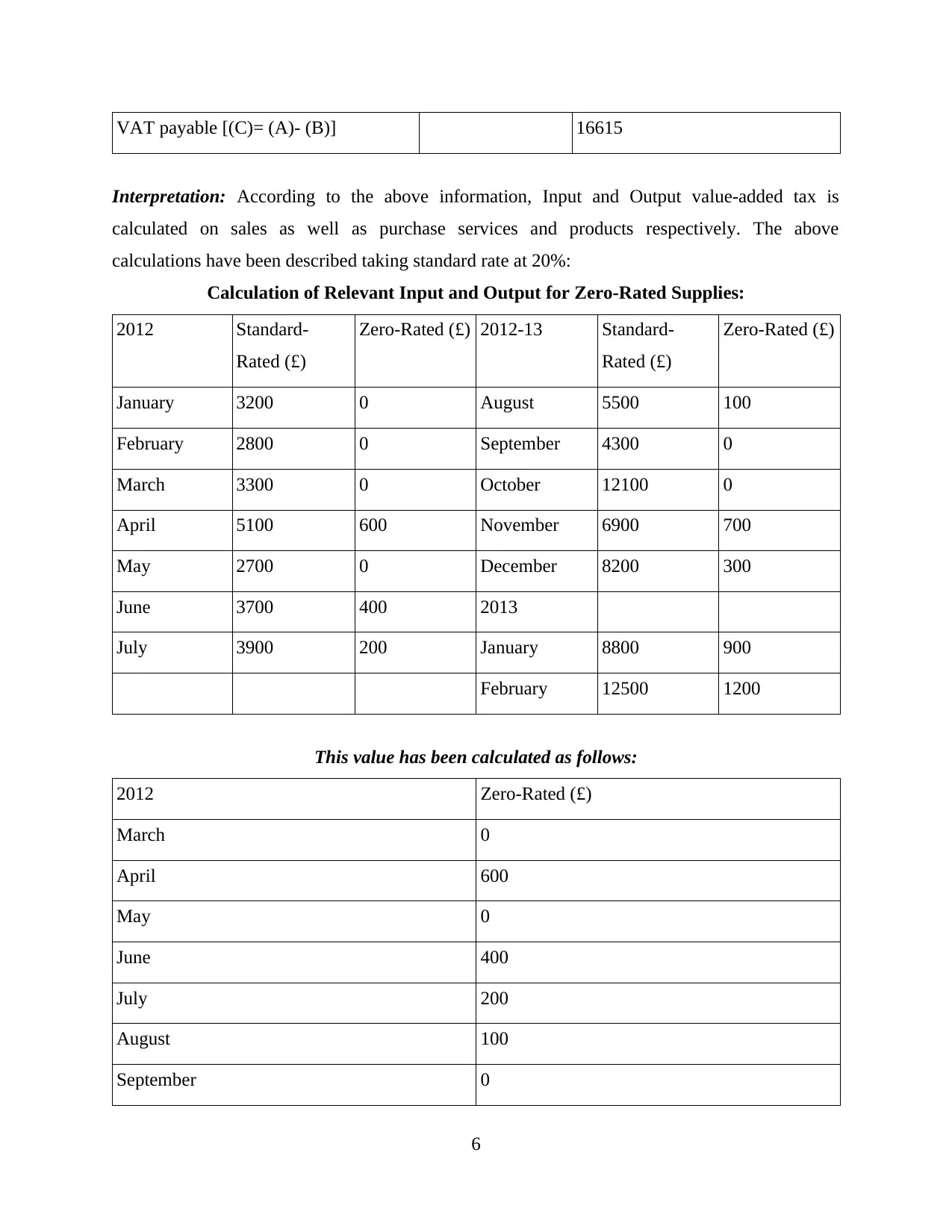

VAT payable [(C)= (A)- (B)] 16615

Interpretation: According to the above information, Input and Output value-added tax is

calculated on sales as well as purchase services and products respectively. The above

calculations have been described taking standard rate at 20%:

Calculation of Relevant Input and Output for Zero-Rated Supplies:

2012 Standard-

Rated (£)

Zero-Rated (£) 2012-13 Standard-

Rated (£)

Zero-Rated (£)

January 3200 0 August 5500 100

February 2800 0 September 4300 0

March 3300 0 October 12100 0

April 5100 600 November 6900 700

May 2700 0 December 8200 300

June 3700 400 2013

July 3900 200 January 8800 900

February 12500 1200

This value has been calculated as follows:

2012 Zero-Rated (£)

March 0

April 600

May 0

June 400

July 200

August 100

September 0

6

Interpretation: According to the above information, Input and Output value-added tax is

calculated on sales as well as purchase services and products respectively. The above

calculations have been described taking standard rate at 20%:

Calculation of Relevant Input and Output for Zero-Rated Supplies:

2012 Standard-

Rated (£)

Zero-Rated (£) 2012-13 Standard-

Rated (£)

Zero-Rated (£)

January 3200 0 August 5500 100

February 2800 0 September 4300 0

March 3300 0 October 12100 0

April 5100 600 November 6900 700

May 2700 0 December 8200 300

June 3700 400 2013

July 3900 200 January 8800 900

February 12500 1200

This value has been calculated as follows:

2012 Zero-Rated (£)

March 0

April 600

May 0

June 400

July 200

August 100

September 0

6

October 0

November 700

December 300

2013

January 900

February 1200

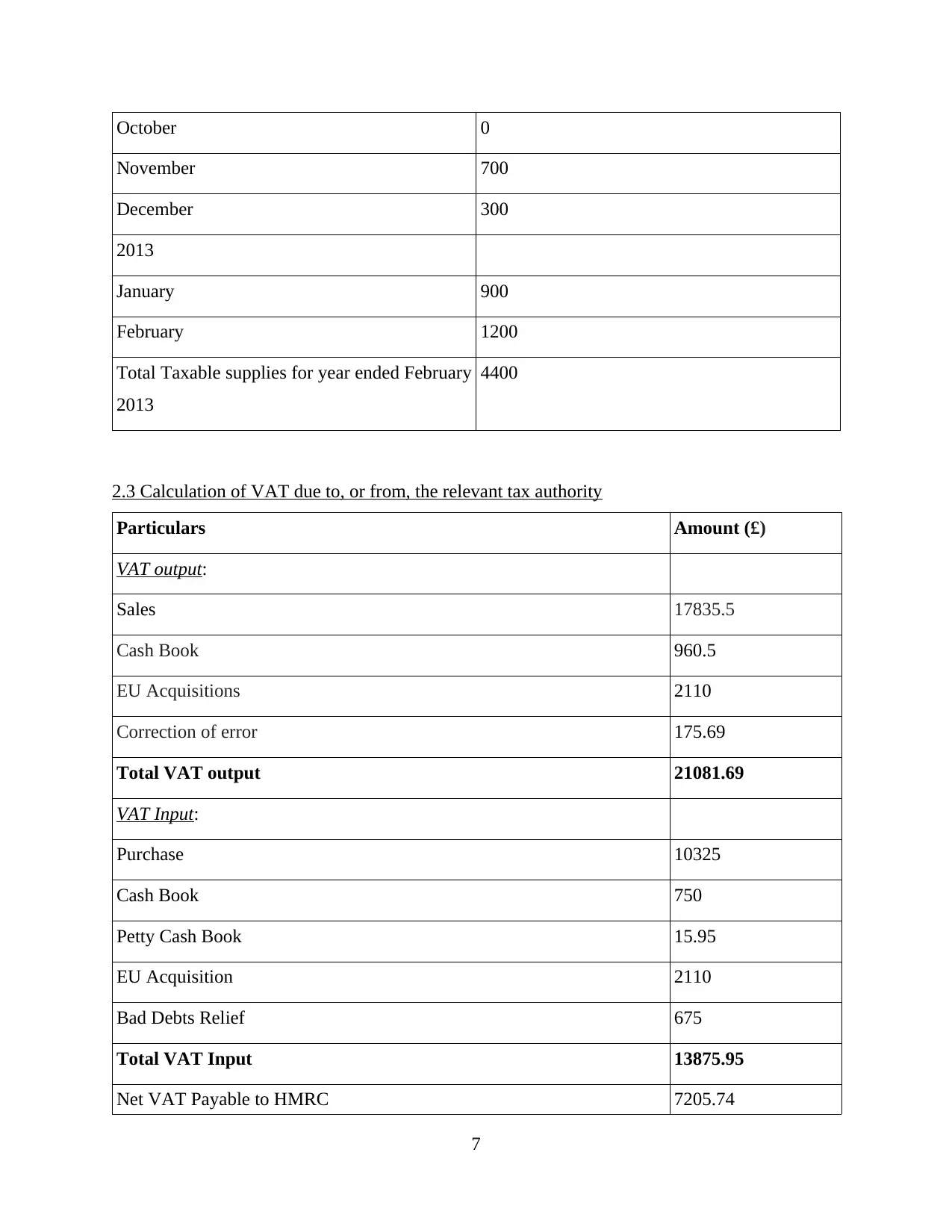

Total Taxable supplies for year ended February

2013

4400

2.3 Calculation of VAT due to, or from, the relevant tax authority

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

7

November 700

December 300

2013

January 900

February 1200

Total Taxable supplies for year ended February

2013

4400

2.3 Calculation of VAT due to, or from, the relevant tax authority

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

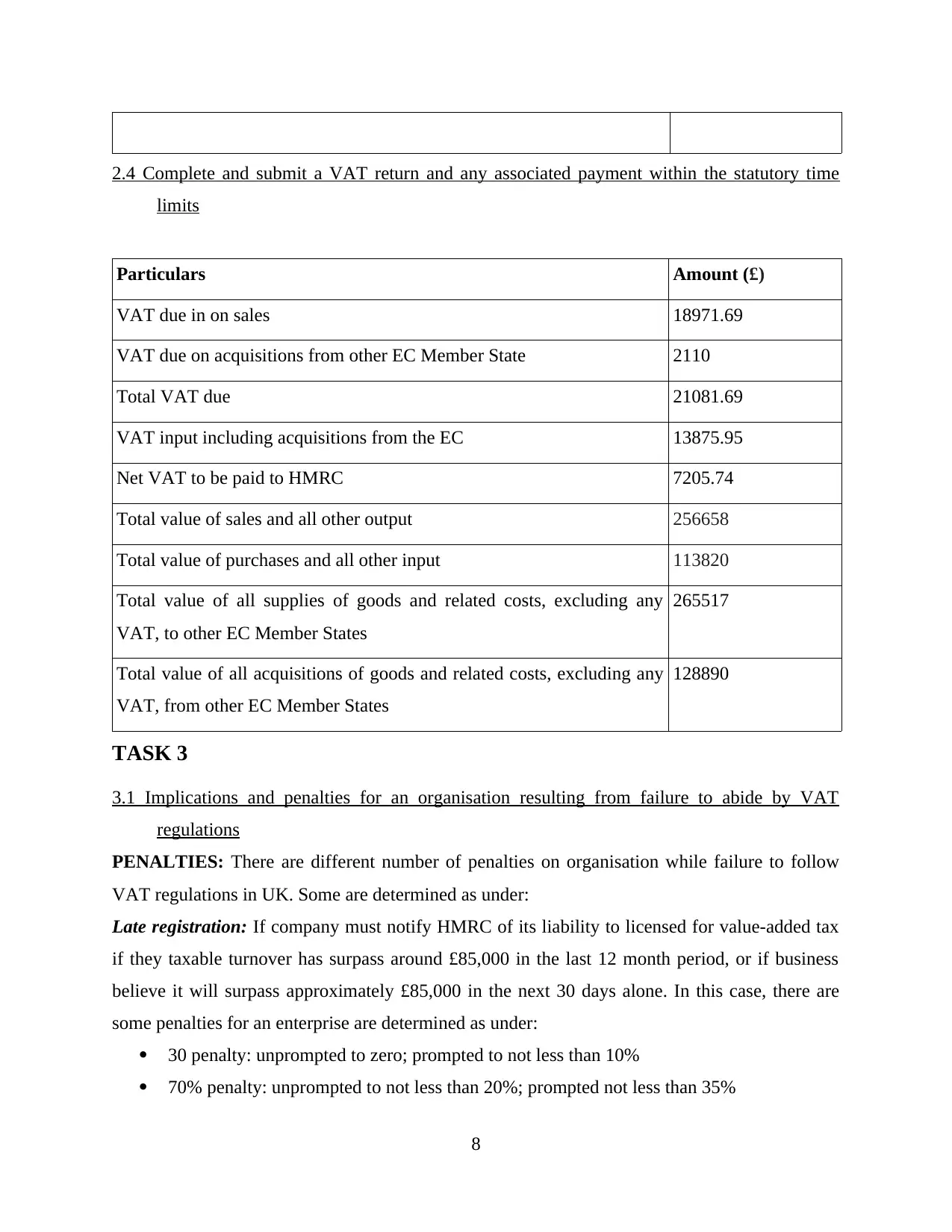

2.4 Complete and submit a VAT return and any associated payment within the statutory time

limits

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

PENALTIES: There are different number of penalties on organisation while failure to follow

VAT regulations in UK. Some are determined as under:

Late registration: If company must notify HMRC of its liability to licensed for value-added tax

if they taxable turnover has surpass around £85,000 in the last 12 month period, or if business

believe it will surpass approximately £85,000 in the next 30 days alone. In this case, there are

some penalties for an enterprise are determined as under:

30 penalty: unprompted to zero; prompted to not less than 10%

70% penalty: unprompted to not less than 20%; prompted not less than 35%

8

limits

Particulars Amount (£)

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

PENALTIES: There are different number of penalties on organisation while failure to follow

VAT regulations in UK. Some are determined as under:

Late registration: If company must notify HMRC of its liability to licensed for value-added tax

if they taxable turnover has surpass around £85,000 in the last 12 month period, or if business

believe it will surpass approximately £85,000 in the next 30 days alone. In this case, there are

some penalties for an enterprise are determined as under:

30 penalty: unprompted to zero; prompted to not less than 10%

70% penalty: unprompted to not less than 20%; prompted not less than 35%

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

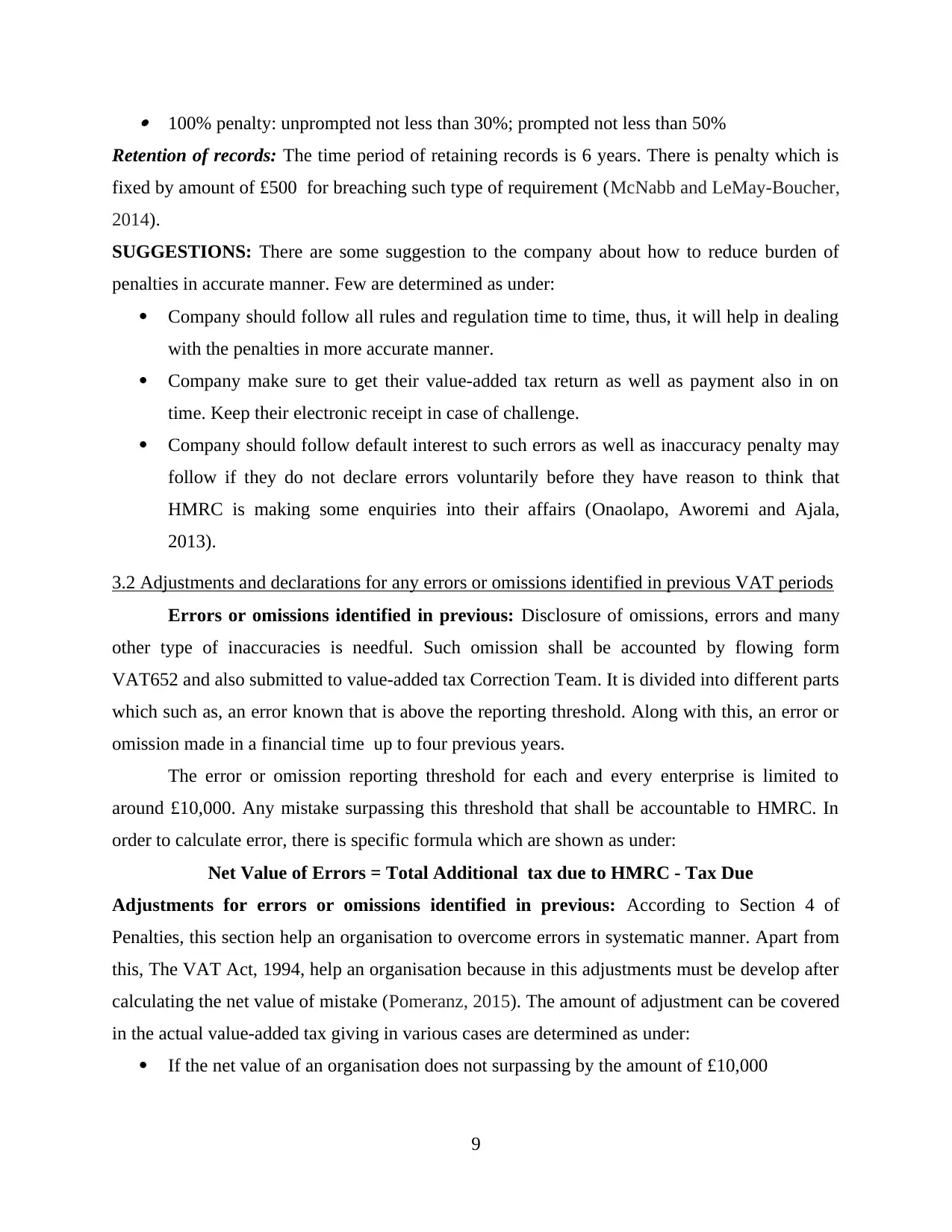

100% penalty: unprompted not less than 30%; prompted not less than 50%

Retention of records: The time period of retaining records is 6 years. There is penalty which is

fixed by amount of £500 for breaching such type of requirement (McNabb and LeMay-Boucher,

2014).

SUGGESTIONS: There are some suggestion to the company about how to reduce burden of

penalties in accurate manner. Few are determined as under:

Company should follow all rules and regulation time to time, thus, it will help in dealing

with the penalties in more accurate manner.

Company make sure to get their value-added tax return as well as payment also in on

time. Keep their electronic receipt in case of challenge.

Company should follow default interest to such errors as well as inaccuracy penalty may

follow if they do not declare errors voluntarily before they have reason to think that

HMRC is making some enquiries into their affairs (Onaolapo, Aworemi and Ajala,

2013).

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods

Errors or omissions identified in previous: Disclosure of omissions, errors and many

other type of inaccuracies is needful. Such omission shall be accounted by flowing form

VAT652 and also submitted to value-added tax Correction Team. It is divided into different parts

which such as, an error known that is above the reporting threshold. Along with this, an error or

omission made in a financial time up to four previous years.

The error or omission reporting threshold for each and every enterprise is limited to

around £10,000. Any mistake surpassing this threshold that shall be accountable to HMRC. In

order to calculate error, there is specific formula which are shown as under:

Net Value of Errors = Total Additional tax due to HMRC - Tax Due

Adjustments for errors or omissions identified in previous: According to Section 4 of

Penalties, this section help an organisation to overcome errors in systematic manner. Apart from

this, The VAT Act, 1994, help an organisation because in this adjustments must be develop after

calculating the net value of mistake (Pomeranz, 2015). The amount of adjustment can be covered

in the actual value-added tax giving in various cases are determined as under:

If the net value of an organisation does not surpassing by the amount of £10,000

9

Retention of records: The time period of retaining records is 6 years. There is penalty which is

fixed by amount of £500 for breaching such type of requirement (McNabb and LeMay-Boucher,

2014).

SUGGESTIONS: There are some suggestion to the company about how to reduce burden of

penalties in accurate manner. Few are determined as under:

Company should follow all rules and regulation time to time, thus, it will help in dealing

with the penalties in more accurate manner.

Company make sure to get their value-added tax return as well as payment also in on

time. Keep their electronic receipt in case of challenge.

Company should follow default interest to such errors as well as inaccuracy penalty may

follow if they do not declare errors voluntarily before they have reason to think that

HMRC is making some enquiries into their affairs (Onaolapo, Aworemi and Ajala,

2013).

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods

Errors or omissions identified in previous: Disclosure of omissions, errors and many

other type of inaccuracies is needful. Such omission shall be accounted by flowing form

VAT652 and also submitted to value-added tax Correction Team. It is divided into different parts

which such as, an error known that is above the reporting threshold. Along with this, an error or

omission made in a financial time up to four previous years.

The error or omission reporting threshold for each and every enterprise is limited to

around £10,000. Any mistake surpassing this threshold that shall be accountable to HMRC. In

order to calculate error, there is specific formula which are shown as under:

Net Value of Errors = Total Additional tax due to HMRC - Tax Due

Adjustments for errors or omissions identified in previous: According to Section 4 of

Penalties, this section help an organisation to overcome errors in systematic manner. Apart from

this, The VAT Act, 1994, help an organisation because in this adjustments must be develop after

calculating the net value of mistake (Pomeranz, 2015). The amount of adjustment can be covered

in the actual value-added tax giving in various cases are determined as under:

If the net value of an organisation does not surpassing by the amount of £10,000

9

If the net value relate between the amount of £10,000 and £60,000 but does not surpass

one percent of net outputs given in value-added tax return statement for the time in which

the omission is discovered.

TASK 4

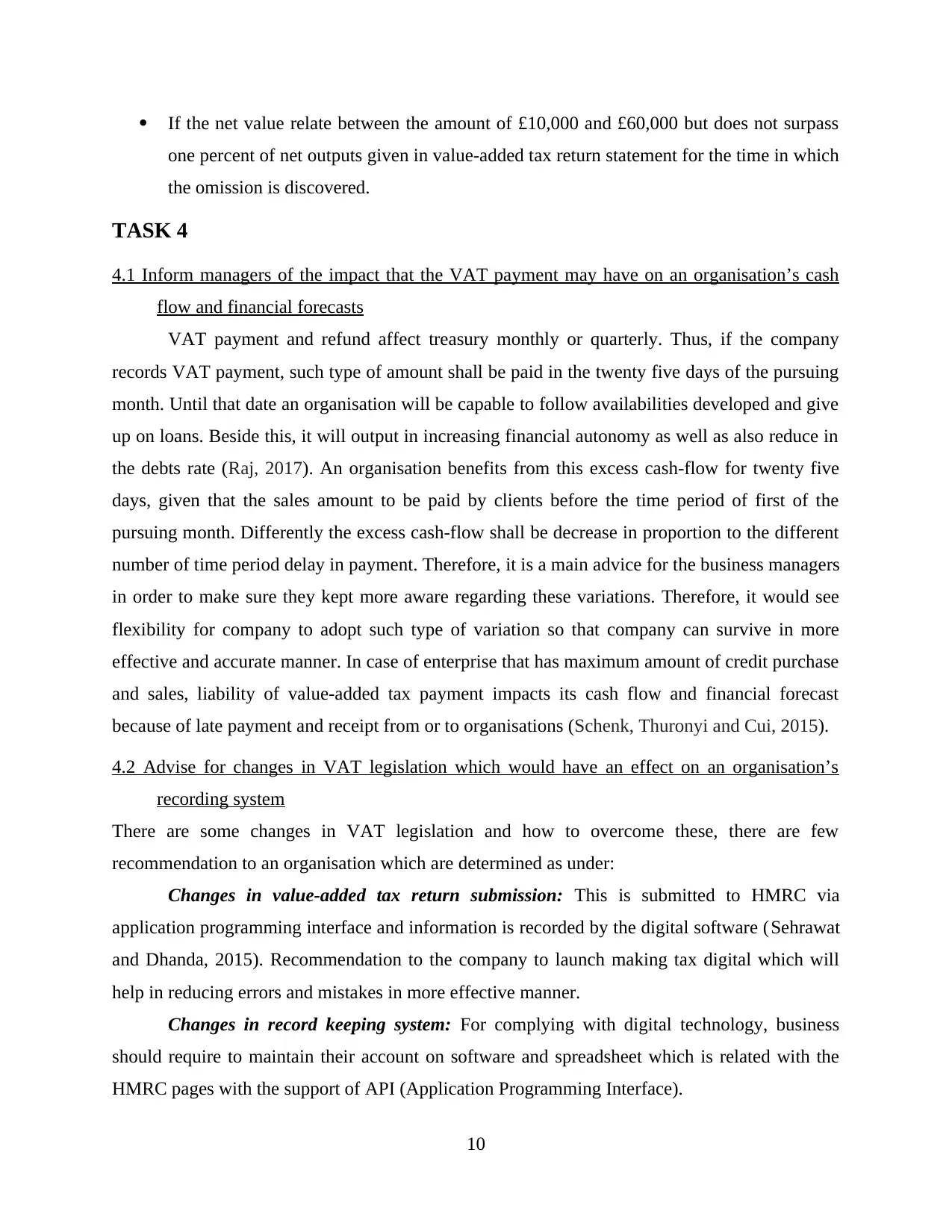

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

VAT payment and refund affect treasury monthly or quarterly. Thus, if the company

records VAT payment, such type of amount shall be paid in the twenty five days of the pursuing

month. Until that date an organisation will be capable to follow availabilities developed and give

up on loans. Beside this, it will output in increasing financial autonomy as well as also reduce in

the debts rate (Raj, 2017). An organisation benefits from this excess cash-flow for twenty five

days, given that the sales amount to be paid by clients before the time period of first of the

pursuing month. Differently the excess cash-flow shall be decrease in proportion to the different

number of time period delay in payment. Therefore, it is a main advice for the business managers

in order to make sure they kept more aware regarding these variations. Therefore, it would see

flexibility for company to adopt such type of variation so that company can survive in more

effective and accurate manner. In case of enterprise that has maximum amount of credit purchase

and sales, liability of value-added tax payment impacts its cash flow and financial forecast

because of late payment and receipt from or to organisations (Schenk, Thuronyi and Cui, 2015).

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording system

There are some changes in VAT legislation and how to overcome these, there are few

recommendation to an organisation which are determined as under:

Changes in value-added tax return submission: This is submitted to HMRC via

application programming interface and information is recorded by the digital software (Sehrawat

and Dhanda, 2015). Recommendation to the company to launch making tax digital which will

help in reducing errors and mistakes in more effective manner.

Changes in record keeping system: For complying with digital technology, business

should require to maintain their account on software and spreadsheet which is related with the

HMRC pages with the support of API (Application Programming Interface).

10

one percent of net outputs given in value-added tax return statement for the time in which

the omission is discovered.

TASK 4

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

VAT payment and refund affect treasury monthly or quarterly. Thus, if the company

records VAT payment, such type of amount shall be paid in the twenty five days of the pursuing

month. Until that date an organisation will be capable to follow availabilities developed and give

up on loans. Beside this, it will output in increasing financial autonomy as well as also reduce in

the debts rate (Raj, 2017). An organisation benefits from this excess cash-flow for twenty five

days, given that the sales amount to be paid by clients before the time period of first of the

pursuing month. Differently the excess cash-flow shall be decrease in proportion to the different

number of time period delay in payment. Therefore, it is a main advice for the business managers

in order to make sure they kept more aware regarding these variations. Therefore, it would see

flexibility for company to adopt such type of variation so that company can survive in more

effective and accurate manner. In case of enterprise that has maximum amount of credit purchase

and sales, liability of value-added tax payment impacts its cash flow and financial forecast

because of late payment and receipt from or to organisations (Schenk, Thuronyi and Cui, 2015).

4.2 Advise for changes in VAT legislation which would have an effect on an organisation’s

recording system

There are some changes in VAT legislation and how to overcome these, there are few

recommendation to an organisation which are determined as under:

Changes in value-added tax return submission: This is submitted to HMRC via

application programming interface and information is recorded by the digital software (Sehrawat

and Dhanda, 2015). Recommendation to the company to launch making tax digital which will

help in reducing errors and mistakes in more effective manner.

Changes in record keeping system: For complying with digital technology, business

should require to maintain their account on software and spreadsheet which is related with the

HMRC pages with the support of API (Application Programming Interface).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.