Indirect Tax: VAT Regulations and Compliance Report

VerifiedAdded on 2020/12/24

|12

|3904

|327

Report

AI Summary

This report delves into the intricacies of Value Added Tax (VAT) regulations, providing a comprehensive overview of its various aspects. The introduction defines indirect tax and its significance, followed by a detailed exploration of VAT. Task 1 focuses on identifying sources of VAT information, the interaction between organizations and government agencies (HMRC), VAT registration requirements, business documentation, reporting frequencies for different VAT schemes, and the importance of staying updated with regulatory changes. Task 2 covers extracting relevant data from accounting systems, calculating input and output VAT, determining VAT liabilities, and submitting VAT returns within statutory deadlines. Task 3 addresses the implications of non-compliance, including penalties, and the procedures for correcting errors. Finally, Task 4 examines the impact of VAT payments on organizations and provides guidance on adapting to VAT legislation changes. The report concludes with a summary of key findings and includes references to support the analysis.

Indirect Tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Identification of sources of information on VAT.................................................................1

1.2 Interaction between organisation and relevant government agency.....................................2

1.3 VAT Registration requirements............................................................................................2

1.4 Information need to be disclosed as business documentation of VAT registered businesses

.....................................................................................................................................................2

1.5 Requirements and frequency of reporting for various VAT schemes...................................3

1.6 Maintenance of up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extract relevant data for a specific period from the accounting system...............................4

2.2 Calculations of Input and Output VAT for data extracted....................................................5

2.3 Calculate the VAT due to, or from, the relevant tax authority.............................................6

2.4 Submission of a completed VAT return and any associated payment within the statutory

time limits....................................................................................................................................7

TASK 3............................................................................................................................................7

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................7

3.2 Adjustments and declarations for any errors or omission identified in previous VAT

periods.........................................................................................................................................8

TASK 4............................................................................................................................................8

4.1 Providing information of impact of VAT payment may have on an organisation................8

4.2 Advise to relevant people about changes in VAT legislation which would have an effect of

an organisation............................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Identification of sources of information on VAT.................................................................1

1.2 Interaction between organisation and relevant government agency.....................................2

1.3 VAT Registration requirements............................................................................................2

1.4 Information need to be disclosed as business documentation of VAT registered businesses

.....................................................................................................................................................2

1.5 Requirements and frequency of reporting for various VAT schemes...................................3

1.6 Maintenance of up-to-date knowledge of changes to codes of practice, regulation or

legislation....................................................................................................................................4

TASK 2............................................................................................................................................4

2.1 Extract relevant data for a specific period from the accounting system...............................4

2.2 Calculations of Input and Output VAT for data extracted....................................................5

2.3 Calculate the VAT due to, or from, the relevant tax authority.............................................6

2.4 Submission of a completed VAT return and any associated payment within the statutory

time limits....................................................................................................................................7

TASK 3............................................................................................................................................7

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations...................................................................................................................................7

3.2 Adjustments and declarations for any errors or omission identified in previous VAT

periods.........................................................................................................................................8

TASK 4............................................................................................................................................8

4.1 Providing information of impact of VAT payment may have on an organisation................8

4.2 Advise to relevant people about changes in VAT legislation which would have an effect of

an organisation............................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Indirect tax is an amount which is charged on purchase or sales of goods and services

rather than profits or revenues of the organisation. It is collected by a mediator from the

institutions which are bearing eventual economical encumbrance of taxation. At last a return is

filed by the intermediary to the government. All such types of taxes are flexible (Indirect tax,

2019). There are various types of such expenses like central sales, excise duty, security

transactions, VAT and others. These are paid by the consumers by paying extra amount for a

particular product at the time of purchase. In this project report various aspects are discussed

such as understanding of VAT regulations and completion of VAT returns accurately and in a

timely manner. Detailed information of penalties, adjustments for errors related to VAT and it

information is also being covered under this assignment.

TASK 1

1.1 Identification of sources of information on VAT

VAT is an indirect tax which is applied on all the products and services that are bought or

sold within a country. It is a consumption taxation which was introduced in year 1973 and the

third largest source of legal bodies to acquire revenues. It is considered as indirect because it is

not paid directly to the government by the consumers. VAT is charged by sellers from customers

by adding value of it in the total selling price of a product or service. In UK predetermined

percentage of this tax is 20% which was increased in year 2011 from 17.5%. It may be charged

on items such as commission, canteen meals sold to staff, gifts, selling assets of a business

(Abbott and et.al., 2016). The amount of VAT Payable by a taxable person is calculated by

subtracting inputs used for production of goods and services from cost of products incurred on

their production. Taxable persons include any legal entity(s) operating as a VAT registered

business. However, VAT is not applicable for all cities, some places are exempted from this tax.

Sources of information on VAT can be identified by using the information that is

promptly available from federal government sites and portals. Another source of information is

available from HM revenue and customs (HMRC) portals that is responsible for tax collection

across UK. All the relevant information regarding tax or any other issue for paying tax is

considered by the HMRC and it provide solutions to the tax payers.

1

Indirect tax is an amount which is charged on purchase or sales of goods and services

rather than profits or revenues of the organisation. It is collected by a mediator from the

institutions which are bearing eventual economical encumbrance of taxation. At last a return is

filed by the intermediary to the government. All such types of taxes are flexible (Indirect tax,

2019). There are various types of such expenses like central sales, excise duty, security

transactions, VAT and others. These are paid by the consumers by paying extra amount for a

particular product at the time of purchase. In this project report various aspects are discussed

such as understanding of VAT regulations and completion of VAT returns accurately and in a

timely manner. Detailed information of penalties, adjustments for errors related to VAT and it

information is also being covered under this assignment.

TASK 1

1.1 Identification of sources of information on VAT

VAT is an indirect tax which is applied on all the products and services that are bought or

sold within a country. It is a consumption taxation which was introduced in year 1973 and the

third largest source of legal bodies to acquire revenues. It is considered as indirect because it is

not paid directly to the government by the consumers. VAT is charged by sellers from customers

by adding value of it in the total selling price of a product or service. In UK predetermined

percentage of this tax is 20% which was increased in year 2011 from 17.5%. It may be charged

on items such as commission, canteen meals sold to staff, gifts, selling assets of a business

(Abbott and et.al., 2016). The amount of VAT Payable by a taxable person is calculated by

subtracting inputs used for production of goods and services from cost of products incurred on

their production. Taxable persons include any legal entity(s) operating as a VAT registered

business. However, VAT is not applicable for all cities, some places are exempted from this tax.

Sources of information on VAT can be identified by using the information that is

promptly available from federal government sites and portals. Another source of information is

available from HM revenue and customs (HMRC) portals that is responsible for tax collection

across UK. All the relevant information regarding tax or any other issue for paying tax is

considered by the HMRC and it provide solutions to the tax payers.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 Interaction between organisation and relevant government agency

HMRC or HM Revenue and customs is a government department responsible for

collection and payment of taxes in the country from and to the registered VAT businesses

respectively. From registration procedures to the time a taxable person exits or ceases to be

recognised as a VAT registered business, HMRC provisions for easier access and administration

of VAT accounts created for organisations and individuals through Making Tax Digital (MTD)

program. This program helps easier tax administration making the process of registering,

submitting and applying for any kind of returns or grievance (Agell, Englund and Södersten,

2016).

1.3 VAT Registration requirements

HM Revenue & Customs (HMRC) provides a detailed procedure that is required to be

followed by a taxable person. An organization needs to register for VAT if the VAT taxable

turnover exceeds £85,000. VAT Taxable turnover refers to the sum of everything an organisation

sells that is not exempted from VAT or total value of all taxable supplies except exempt supplies.

Businesses need to register with HMRC for VAT returns Once the organisation registers

with HMRC as a registered business, a VAT number is issued. Registration can be completed

either by filling a form online or offline through an agent which is usually a rare situation. For

offline registration the organisations may appoint an agent to do it on their behalf. Different

forms are needed to be filled for different types of businesses (Bahl, 2018). For instance, forms

such as VAT1A needs to be filled by distance sellers at the time of registration, VAT1B I is for

importers and VAT1C is required to be filled and submitted if a VAT registered business needs

to dispose off their assets.

1.4 Information need to be disclosed as business documentation of VAT registered businesses

HM Revenue and Customs demands its taxable persons to comply with the proper

business documentation of their operations at the time of registration. Following information

needs to be disclosed as business documentation of VAT registered business:

National Insurance (NI) number

Tax identifier i.e. Unique Taxpayer’s reference (UTR) number

Certificate of incorporation/incorporation details

Business bank accounts details

Information on all associated businesses within the last two years

2

HMRC or HM Revenue and customs is a government department responsible for

collection and payment of taxes in the country from and to the registered VAT businesses

respectively. From registration procedures to the time a taxable person exits or ceases to be

recognised as a VAT registered business, HMRC provisions for easier access and administration

of VAT accounts created for organisations and individuals through Making Tax Digital (MTD)

program. This program helps easier tax administration making the process of registering,

submitting and applying for any kind of returns or grievance (Agell, Englund and Södersten,

2016).

1.3 VAT Registration requirements

HM Revenue & Customs (HMRC) provides a detailed procedure that is required to be

followed by a taxable person. An organization needs to register for VAT if the VAT taxable

turnover exceeds £85,000. VAT Taxable turnover refers to the sum of everything an organisation

sells that is not exempted from VAT or total value of all taxable supplies except exempt supplies.

Businesses need to register with HMRC for VAT returns Once the organisation registers

with HMRC as a registered business, a VAT number is issued. Registration can be completed

either by filling a form online or offline through an agent which is usually a rare situation. For

offline registration the organisations may appoint an agent to do it on their behalf. Different

forms are needed to be filled for different types of businesses (Bahl, 2018). For instance, forms

such as VAT1A needs to be filled by distance sellers at the time of registration, VAT1B I is for

importers and VAT1C is required to be filled and submitted if a VAT registered business needs

to dispose off their assets.

1.4 Information need to be disclosed as business documentation of VAT registered businesses

HM Revenue and Customs demands its taxable persons to comply with the proper

business documentation of their operations at the time of registration. Following information

needs to be disclosed as business documentation of VAT registered business:

National Insurance (NI) number

Tax identifier i.e. Unique Taxpayer’s reference (UTR) number

Certificate of incorporation/incorporation details

Business bank accounts details

Information on all associated businesses within the last two years

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All the documentation relating to filing of VAT return needs to be done online unless the

business is subject to an insolvency procedure, objections to usage of computer systems on

religious grounds or conformed to any disability. Generally two types of records are maintained

by businesses as per HMRC regulations- VAT account and VAT invoices. The VAT account

includes a record of day-to-day operations of a business whereas VAT invoices mainly relate to

suppliers and their operations (Brondolo, Silvani and Le Borgne, 2014).

1.5 Requirements and frequency of reporting for various VAT schemes

For better compliance and disclosure of returns for VAT, HMRC has launched various

kinds of VAT schemes. These schemes have been described below:

Flat-rate VAT accounting scheme: In this method the tax is calculating is multiplying

flat rate by inclusive turnover of VAT. For example, if turnover of a company is 20000

and the flat rate is 15% then an amount of 3000 will be paid VAT. In this method VAT is

paid on a fixed rate.

VAT Cash Accounting scheme: Cash accounting system is followed in this scheme in

which date when payments are made is considered. In this method VAT is paid at the

time of scale and collected when payment is made to the supplier.

Annual Accounting Scheme: As the name suggests, the annual accounting scheme

enables a registered business to pay tax on its VAT account either in nine monthly or

three quarterly payments. A business can, however, pay its returns if its estimated taxable

turnover does not exceed £1.35m with a minimum turnover of £1.6m per year. This

scheme can be combined with flat rate VAT and VAT cash accounting scheme under

special circumstances.

Retail and VAT margin schemes: These schemes are applicable on different registered

businesses based on their retail turnovers ranging below £1m, between £1m and £130m

or above. Small sized businesses falling under the purview of cash accounting and annual

accounting schemes have the benefit of availing retail schemes only (Buenker, 2018).

1.6 Maintenance of up-to-date knowledge of changes to codes of practice, regulation or

legislation

It is very important for all the business entities to follow codes of practice, regulation or

legislation. It is also essential to be aware about the changes that may take place in these

elements. All of them are as follows:

3

business is subject to an insolvency procedure, objections to usage of computer systems on

religious grounds or conformed to any disability. Generally two types of records are maintained

by businesses as per HMRC regulations- VAT account and VAT invoices. The VAT account

includes a record of day-to-day operations of a business whereas VAT invoices mainly relate to

suppliers and their operations (Brondolo, Silvani and Le Borgne, 2014).

1.5 Requirements and frequency of reporting for various VAT schemes

For better compliance and disclosure of returns for VAT, HMRC has launched various

kinds of VAT schemes. These schemes have been described below:

Flat-rate VAT accounting scheme: In this method the tax is calculating is multiplying

flat rate by inclusive turnover of VAT. For example, if turnover of a company is 20000

and the flat rate is 15% then an amount of 3000 will be paid VAT. In this method VAT is

paid on a fixed rate.

VAT Cash Accounting scheme: Cash accounting system is followed in this scheme in

which date when payments are made is considered. In this method VAT is paid at the

time of scale and collected when payment is made to the supplier.

Annual Accounting Scheme: As the name suggests, the annual accounting scheme

enables a registered business to pay tax on its VAT account either in nine monthly or

three quarterly payments. A business can, however, pay its returns if its estimated taxable

turnover does not exceed £1.35m with a minimum turnover of £1.6m per year. This

scheme can be combined with flat rate VAT and VAT cash accounting scheme under

special circumstances.

Retail and VAT margin schemes: These schemes are applicable on different registered

businesses based on their retail turnovers ranging below £1m, between £1m and £130m

or above. Small sized businesses falling under the purview of cash accounting and annual

accounting schemes have the benefit of availing retail schemes only (Buenker, 2018).

1.6 Maintenance of up-to-date knowledge of changes to codes of practice, regulation or

legislation

It is very important for all the business entities to follow codes of practice, regulation or

legislation. It is also essential to be aware about the changes that may take place in these

elements. All of them are as follows:

3

Enterprises should have appropriate knowledge of the may in which statistics can be

made.

Keep the important data safe by using good software.

Reduce works on paper and follow the concept of paperless work so that work load of

employees can be decreased.

It is very important for all the businesses it is very important to be aware of such changes

so that business can be operated in appropriate manner. It helps to maintain relevant data that

belongs to taxes in more effective way. It also reduces the chances of mistakes and conflicts

among employees and managers as top authority is aware of the modifications in legislations

(Fuentes and Lillo-Bañuls, 2015).

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

(1) Data extracted for the calculation of standard supplies, zero-rated supplies and

exempt supplies:

Keen will commence trading in the near future. He operates a mid-sized boat, and is considering

three alternative types of business. These are:

grooming, in which case all sales will be standard rated for VAT calculations

conveyance, in which case all sales will be zero-rated for VAT, and

an marine paramedic service, in which case all sales will be exempt from VAT.

For each alternative Keen forecasts sales worth £70,000 per month (exclusive of VAT), and

standard rated expenses will be £10,000 per month (inclusive of VAT) (Imam and Jacobs, 2014).

Data extracted for the calculation of input and output VAT on exports and imports:

Moon Ltd is registered for VAT in the UK. The company has the choice of purchasing goods

costing £1,500 (exclusive of VAT) from either a UK supplier or from a supplier situated outside

the European Union. Ascertain how the input and output VAT shall be calculated on such

imports.

2.2 Calculations of Input and Output VAT for data extracted

Calculation of of input and output VAT on standard supplies, zero-rated supplies

and exempt supplies:

Standard rated supplies:

4

made.

Keep the important data safe by using good software.

Reduce works on paper and follow the concept of paperless work so that work load of

employees can be decreased.

It is very important for all the businesses it is very important to be aware of such changes

so that business can be operated in appropriate manner. It helps to maintain relevant data that

belongs to taxes in more effective way. It also reduces the chances of mistakes and conflicts

among employees and managers as top authority is aware of the modifications in legislations

(Fuentes and Lillo-Bañuls, 2015).

TASK 2

2.1 Extract relevant data for a specific period from the accounting system

(1) Data extracted for the calculation of standard supplies, zero-rated supplies and

exempt supplies:

Keen will commence trading in the near future. He operates a mid-sized boat, and is considering

three alternative types of business. These are:

grooming, in which case all sales will be standard rated for VAT calculations

conveyance, in which case all sales will be zero-rated for VAT, and

an marine paramedic service, in which case all sales will be exempt from VAT.

For each alternative Keen forecasts sales worth £70,000 per month (exclusive of VAT), and

standard rated expenses will be £10,000 per month (inclusive of VAT) (Imam and Jacobs, 2014).

Data extracted for the calculation of input and output VAT on exports and imports:

Moon Ltd is registered for VAT in the UK. The company has the choice of purchasing goods

costing £1,500 (exclusive of VAT) from either a UK supplier or from a supplier situated outside

the European Union. Ascertain how the input and output VAT shall be calculated on such

imports.

2.2 Calculations of Input and Output VAT for data extracted

Calculation of of input and output VAT on standard supplies, zero-rated supplies

and exempt supplies:

Standard rated supplies:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Since Keen plans to start a profitable venture for training inclusive of standard rated sales

for VAT , she will be required to register for VAT as she is making taxable supplies.

Standard rated supplies, as the name suggests, are those items prescribed under the law that have

a general applicable rate of 20% applicable on them. Output and Input VAT have been calculated

below:

Output VAT = 70,000 x 20%= £14,000

£14,000 per month will be due as Output VAT

Input VAT = 10,000 x 20/120= £1,667

£1,667 per month will be recoverable.

Zero-rated supplies:

If Keen plans to start a profitable venture for transport inclusive of zero-rated sales for

VAT , she will be able to apply for exemption from registration for VAT since such supplies

have a nil percent rate applicable on them. However, she should still register as these are taxable

supplies. Output and Input VAT have been calculated below:

Output VAT will not be due in this case (Johannesen, N., 2014).

Input VAT of £1,667 per month will be recoverable.

Exempt supplies:

Keen will not be required or permitted to register for VAT as she will not be making

taxable supplies.

No Output VAT will be due.

No Input VAT will be reclaimable.

Calculation of of input and output VAT on exports and imports:

A VAT registered business can import goods from outside the European Union, in such a

case VAT has to be paid at the time of importation known as Output VAT. This amount can then

can be reclaimed as input VAT on the VAT return for the period during which the goods were

imported.

If Moon Ltd. Chooses to purchase goods worth £1,000 from a UK supplier, standard rate

of 20% shall be applicable. This has been calculated as follows:

Output VAT= £1,500 x 20% = £300

Input VAT = £300 (reclaimable)

5

for VAT , she will be required to register for VAT as she is making taxable supplies.

Standard rated supplies, as the name suggests, are those items prescribed under the law that have

a general applicable rate of 20% applicable on them. Output and Input VAT have been calculated

below:

Output VAT = 70,000 x 20%= £14,000

£14,000 per month will be due as Output VAT

Input VAT = 10,000 x 20/120= £1,667

£1,667 per month will be recoverable.

Zero-rated supplies:

If Keen plans to start a profitable venture for transport inclusive of zero-rated sales for

VAT , she will be able to apply for exemption from registration for VAT since such supplies

have a nil percent rate applicable on them. However, she should still register as these are taxable

supplies. Output and Input VAT have been calculated below:

Output VAT will not be due in this case (Johannesen, N., 2014).

Input VAT of £1,667 per month will be recoverable.

Exempt supplies:

Keen will not be required or permitted to register for VAT as she will not be making

taxable supplies.

No Output VAT will be due.

No Input VAT will be reclaimable.

Calculation of of input and output VAT on exports and imports:

A VAT registered business can import goods from outside the European Union, in such a

case VAT has to be paid at the time of importation known as Output VAT. This amount can then

can be reclaimed as input VAT on the VAT return for the period during which the goods were

imported.

If Moon Ltd. Chooses to purchase goods worth £1,000 from a UK supplier, standard rate

of 20% shall be applicable. This has been calculated as follows:

Output VAT= £1,500 x 20% = £300

Input VAT = £300 (reclaimable)

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If the goods are instead purchased from a supplier situated outside the European Union:

Output VAT (paid to HMRC)= £1,500 x 20% = £300

Payment made to supplier= £1,500 to the supplier

Input VAT (reclaimable)= £300.

In each case Moon Ltd has paid £1,800 and reclaimed £300.On the other hand, the

business can postpone the payment of VAT on importation by setting up an account with HM

Revenue & Customs for the same. For this, it is necessary to provide a bank guarantee with

monthly reporting of VAT. When a UK VAT registered business exports goods outside of the

European Union then the supply is zero-rated (Johnson and Koyama, 2014).

2.3 Calculate the VAT due to, or from, the relevant tax authority

Standard Supplies:

For standard supplies, VAT is calculated at the general rate of 20%. Keen will be liable to

pay £14,000 as her Output VAT return for quarterly basis to HMRC and entitled to receive

reclaim on Input VAT return of £1,667.

Zero-Rated Supplies:

As Zero-Rated supplies have zero percent of VAT rate applicable on them, Keen will not

be liable to pay any tax to HMRC as his VAT return for the year. However, she will entitled to

receive reclaim on Input VAT return of £1,667.

Exempt Supplies:

Exempt supplies are not permitted to be included for VAT returns. These may include

supplies such as medic services, in such case, Keen will not be liable to pay nor permitted to pay

any tax to HMRC as his VAT return for the year.

2.4 Submission of a completed VAT return and any associated payment within the statutory time

limits

HMRC requires registered businesses to file VAT return based on statutory time limits.

This is usually done quarterly. VAT is illustrated below:

6

Output VAT (paid to HMRC)= £1,500 x 20% = £300

Payment made to supplier= £1,500 to the supplier

Input VAT (reclaimable)= £300.

In each case Moon Ltd has paid £1,800 and reclaimed £300.On the other hand, the

business can postpone the payment of VAT on importation by setting up an account with HM

Revenue & Customs for the same. For this, it is necessary to provide a bank guarantee with

monthly reporting of VAT. When a UK VAT registered business exports goods outside of the

European Union then the supply is zero-rated (Johnson and Koyama, 2014).

2.3 Calculate the VAT due to, or from, the relevant tax authority

Standard Supplies:

For standard supplies, VAT is calculated at the general rate of 20%. Keen will be liable to

pay £14,000 as her Output VAT return for quarterly basis to HMRC and entitled to receive

reclaim on Input VAT return of £1,667.

Zero-Rated Supplies:

As Zero-Rated supplies have zero percent of VAT rate applicable on them, Keen will not

be liable to pay any tax to HMRC as his VAT return for the year. However, she will entitled to

receive reclaim on Input VAT return of £1,667.

Exempt Supplies:

Exempt supplies are not permitted to be included for VAT returns. These may include

supplies such as medic services, in such case, Keen will not be liable to pay nor permitted to pay

any tax to HMRC as his VAT return for the year.

2.4 Submission of a completed VAT return and any associated payment within the statutory time

limits

HMRC requires registered businesses to file VAT return based on statutory time limits.

This is usually done quarterly. VAT is illustrated below:

6

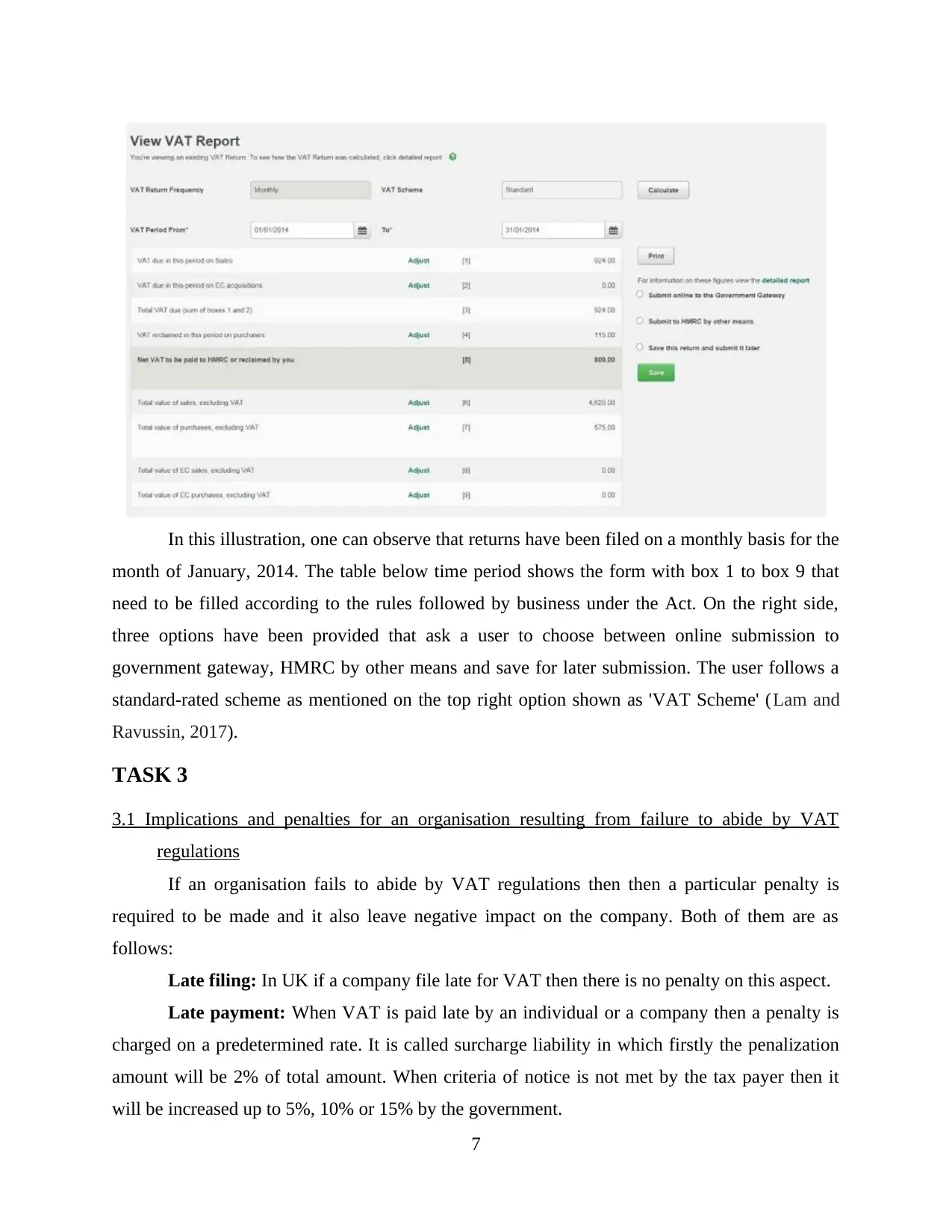

In this illustration, one can observe that returns have been filed on a monthly basis for the

month of January, 2014. The table below time period shows the form with box 1 to box 9 that

need to be filled according to the rules followed by business under the Act. On the right side,

three options have been provided that ask a user to choose between online submission to

government gateway, HMRC by other means and save for later submission. The user follows a

standard-rated scheme as mentioned on the top right option shown as 'VAT Scheme' (Lam and

Ravussin, 2017).

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

If an organisation fails to abide by VAT regulations then then a particular penalty is

required to be made and it also leave negative impact on the company. Both of them are as

follows:

Late filing: In UK if a company file late for VAT then there is no penalty on this aspect.

Late payment: When VAT is paid late by an individual or a company then a penalty is

charged on a predetermined rate. It is called surcharge liability in which firstly the penalization

amount will be 2% of total amount. When criteria of notice is not met by the tax payer then it

will be increased up to 5%, 10% or 15% by the government.

7

month of January, 2014. The table below time period shows the form with box 1 to box 9 that

need to be filled according to the rules followed by business under the Act. On the right side,

three options have been provided that ask a user to choose between online submission to

government gateway, HMRC by other means and save for later submission. The user follows a

standard-rated scheme as mentioned on the top right option shown as 'VAT Scheme' (Lam and

Ravussin, 2017).

TASK 3

3.1 Implications and penalties for an organisation resulting from failure to abide by VAT

regulations

If an organisation fails to abide by VAT regulations then then a particular penalty is

required to be made and it also leave negative impact on the company. Both of them are as

follows:

Late filing: In UK if a company file late for VAT then there is no penalty on this aspect.

Late payment: When VAT is paid late by an individual or a company then a penalty is

charged on a predetermined rate. It is called surcharge liability in which firstly the penalization

amount will be 2% of total amount. When criteria of notice is not met by the tax payer then it

will be increased up to 5%, 10% or 15% by the government.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Late registration: In UK no penalty or punishment is made when an organisation

register late for VAT.

Implications: When an organisation fails to abide VAT then strict action can be taken by

the government if it is made in an illegal manner. It will also affect the market image of an

organisation if any legal activity is performed against it.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT periods

There are various errors and omission are made by the organisation that are identified in

previous year. These are as follows:

An error related to reporting threshold such as VAT 652.

A mistake made purposely to misguide VAT correction team.

A fault which is made in a financial period up to 4 previous years (Parker, 2018.).

Adjustments and declarations:

If the error is more then 10000 pound then it will not be handled VAT correction team

but transferred to HMRC. Deliberate mistakes are also required to be reported to the authority

which is responsible for the collection of tax. When the error is resulted due to additional

payments to the tax authorities then total extra amount will be adjusted in the net year.

TASK 4

4.1 Providing information of impact of VAT payment may have on an organisation

VAT is a composition tax which is imposed on the goods and services that are purchased

or sold in boundary of a country. It is very important for the companies to pay VAT every year.

There are various impacts of VAT payment on cash flow and financial forecasts of an

organisation. All of them are as follows:

When proper process is not followed for VAT than a sudden payment can take place in

the form of penalty which will affect the cash flow (Riedel, 2018).

The organisations which are providing products to the clients on credit or buying on

credit and late payments are received by the company then it may result in late payments

of VAT which will create more penalties for the enterprise. It will also affect cash flow of

the entity.

Unplanned enhancement in the percentage of VAT may also affect financial forecasts of

the company as it will affect the strategies that are made by managers in previous year.

8

register late for VAT.

Implications: When an organisation fails to abide VAT then strict action can be taken by

the government if it is made in an illegal manner. It will also affect the market image of an

organisation if any legal activity is performed against it.

3.2 Adjustments and declarations for any errors or omission identified in previous VAT periods

There are various errors and omission are made by the organisation that are identified in

previous year. These are as follows:

An error related to reporting threshold such as VAT 652.

A mistake made purposely to misguide VAT correction team.

A fault which is made in a financial period up to 4 previous years (Parker, 2018.).

Adjustments and declarations:

If the error is more then 10000 pound then it will not be handled VAT correction team

but transferred to HMRC. Deliberate mistakes are also required to be reported to the authority

which is responsible for the collection of tax. When the error is resulted due to additional

payments to the tax authorities then total extra amount will be adjusted in the net year.

TASK 4

4.1 Providing information of impact of VAT payment may have on an organisation

VAT is a composition tax which is imposed on the goods and services that are purchased

or sold in boundary of a country. It is very important for the companies to pay VAT every year.

There are various impacts of VAT payment on cash flow and financial forecasts of an

organisation. All of them are as follows:

When proper process is not followed for VAT than a sudden payment can take place in

the form of penalty which will affect the cash flow (Riedel, 2018).

The organisations which are providing products to the clients on credit or buying on

credit and late payments are received by the company then it may result in late payments

of VAT which will create more penalties for the enterprise. It will also affect cash flow of

the entity.

Unplanned enhancement in the percentage of VAT may also affect financial forecasts of

the company as it will affect the strategies that are made by managers in previous year.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is essential to pay VAT regularly some times it create problems for organisation that

may lead to insufficient funds such as working capital requirements.

4.2 Advise to relevant people about changes in VAT legislation which would have an effect of

an organisation

Government and legal authorities make changes in their regulations according to the

economic situation of the country. These modifications may affect on reporting system of the

organisations because they have to make alteration in their reports due to such changes. It is very

important for them to gather information of them so that reports can be modified accordingly

(Penu, 2016).

Such type of changes will also leave impact on the accounting system of the business

entity which has been followed in prior years. Sometimes the rate is changed at the end of a

financial year and all the records are maintained on previous rate in this conditions major

changes are made by the company. It is done to meet the legal requirements and follow all the

legislations of the government.

CONCLUSION

From the above report, indirect taxation, specifically VAT, can be clearly understood and

one can develop an understanding on how it is implemented in the country, what are the

requirements a taxable person or organisation needs to adhere to for the purpose of being

recognised as a VAT registered business, various schemes currently implemented and what input

and output VAT is. Apart from this, it can be seen that a slight a change in VAT rates can have a

drastic impact on the organizational structures of a business and can hamper its forecasting plans,

cash flow management as well as accounting systems greatly. Thus, it is important for managers

to have an updated knowledge about such legislation modifications beforehand to plan

accordingly.

9

may lead to insufficient funds such as working capital requirements.

4.2 Advise to relevant people about changes in VAT legislation which would have an effect of

an organisation

Government and legal authorities make changes in their regulations according to the

economic situation of the country. These modifications may affect on reporting system of the

organisations because they have to make alteration in their reports due to such changes. It is very

important for them to gather information of them so that reports can be modified accordingly

(Penu, 2016).

Such type of changes will also leave impact on the accounting system of the business

entity which has been followed in prior years. Sometimes the rate is changed at the end of a

financial year and all the records are maintained on previous rate in this conditions major

changes are made by the company. It is done to meet the legal requirements and follow all the

legislations of the government.

CONCLUSION

From the above report, indirect taxation, specifically VAT, can be clearly understood and

one can develop an understanding on how it is implemented in the country, what are the

requirements a taxable person or organisation needs to adhere to for the purpose of being

recognised as a VAT registered business, various schemes currently implemented and what input

and output VAT is. Apart from this, it can be seen that a slight a change in VAT rates can have a

drastic impact on the organizational structures of a business and can hamper its forecasting plans,

cash flow management as well as accounting systems greatly. Thus, it is important for managers

to have an updated knowledge about such legislation modifications beforehand to plan

accordingly.

9

REFERENCES

Books and Journals:

Abbott, K. W. and et.al., 2016. Two logics of indirect governance: Delegation and

orchestration. British Journal of Political Science. 46(4). pp.719-729.

Agell, J., Englund, P. and Södersten, J., 2016. Incentives and redistribution in the welfare state:

The Swedish tax reform. Springer.

Bahl, R., 2018. The Guatemalan tax reform. Routledge.

Brondolo, J., Silvani, C. and Le Borgne, E., 2014. Tax administration reform and fi scal

adjustment: the case of Indonesia (2001–7). In Macroeconomic Policies in

Indonesia(pp. 156-221). Routledge.

Buenker, J. D., 2018. The Income Tax and the Progressive Era. Routledge.

Fuentes, R. and Lillo-Bañuls, A., 2015. Smoothed bootstrap Malmquist index based on DEA

model to compute productivity of tax offices. Expert systems with applications. 42(5).

pp.2442-2450.

Imam, P. A. and Jacobs, D., 2014. Effect of corruption on tax revenues in the Middle

East. Review of Middle East Economics and Finance Rev. Middle East Econ. Fin..

10(1). pp.1-24.

Johannesen, N., 2014. Tax evasion and Swiss bank deposits. Journal of Public Economics. 111.

pp.46-62.

Johnson, N. D. and Koyama, M., 2014. Tax farming and the origins of state capacity in England

and France. Explorations in Economic History. 51. pp.1-20.

Lam, Y. Y. and Ravussin, E., 2017. Indirect calorimetry: an indispensable tool to understand and

predict obesity. European journal of clinical nutrition. 71(3). p.318.

Parker, H., 2018. Instead of the Dole: An enquiry into integration of the tax and benefit systems.

Routledge.

Penu, D., 2016. Indirect taxes in Romania: an econometric analysis.

Riedel, N., 2018. Quantifying international tax avoidance: A review of the academic

literature. Review of Economics. 69(2). pp.169-181.

Online

Indirect tax. 2019. [Online]. Available through:

<https://www.pwc.co.uk/services/tax/indirect-taxes.html>

10

Books and Journals:

Abbott, K. W. and et.al., 2016. Two logics of indirect governance: Delegation and

orchestration. British Journal of Political Science. 46(4). pp.719-729.

Agell, J., Englund, P. and Södersten, J., 2016. Incentives and redistribution in the welfare state:

The Swedish tax reform. Springer.

Bahl, R., 2018. The Guatemalan tax reform. Routledge.

Brondolo, J., Silvani, C. and Le Borgne, E., 2014. Tax administration reform and fi scal

adjustment: the case of Indonesia (2001–7). In Macroeconomic Policies in

Indonesia(pp. 156-221). Routledge.

Buenker, J. D., 2018. The Income Tax and the Progressive Era. Routledge.

Fuentes, R. and Lillo-Bañuls, A., 2015. Smoothed bootstrap Malmquist index based on DEA

model to compute productivity of tax offices. Expert systems with applications. 42(5).

pp.2442-2450.

Imam, P. A. and Jacobs, D., 2014. Effect of corruption on tax revenues in the Middle

East. Review of Middle East Economics and Finance Rev. Middle East Econ. Fin..

10(1). pp.1-24.

Johannesen, N., 2014. Tax evasion and Swiss bank deposits. Journal of Public Economics. 111.

pp.46-62.

Johnson, N. D. and Koyama, M., 2014. Tax farming and the origins of state capacity in England

and France. Explorations in Economic History. 51. pp.1-20.

Lam, Y. Y. and Ravussin, E., 2017. Indirect calorimetry: an indispensable tool to understand and

predict obesity. European journal of clinical nutrition. 71(3). p.318.

Parker, H., 2018. Instead of the Dole: An enquiry into integration of the tax and benefit systems.

Routledge.

Penu, D., 2016. Indirect taxes in Romania: an econometric analysis.

Riedel, N., 2018. Quantifying international tax avoidance: A review of the academic

literature. Review of Economics. 69(2). pp.169-181.

Online

Indirect tax. 2019. [Online]. Available through:

<https://www.pwc.co.uk/services/tax/indirect-taxes.html>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.