Detailed Management Accounting Report: Unit 5 for Vectair Holdings

VerifiedAdded on 2020/06/04

|17

|5160

|60

Report

AI Summary

This report focuses on management accounting practices, specifically analyzing the operations of Vectair Holdings. It begins by defining management accounting and exploring various types, such as inventory management, cost accounting, job costing, and price optimization. The report then discusses different management accounting reporting methods, including segmental reports, performance reports, inventory management reports, accounts receivables aging reports, and job cost reports. Furthermore, it delves into the calculation of absorption and marginal costing, highlighting the differences between them. The report also covers various planning tools used in the business, like NPV, ARR, and IRR. Finally, it examines how the company responds to financial problems by adopting management accounting systems. The report provides a comprehensive overview of how management accounting aids in internal decision-making and achieving financial stability within the organization.

UNIT 5 MNG

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Defining management accounting and discussing various types of it.............................1

P2. Discussing various methods used for management accounting reporting.......................4

TASK 2............................................................................................................................................6

P3. Calculation of absorption and marginal costing and discussing differences between them.6

TASK 3 ...........................................................................................................................................9

P4. Various types of planning tools in the business...............................................................9

P5. Enumerate how company is responding to financial problems by adopting management

accounting systems...............................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Defining management accounting and discussing various types of it.............................1

P2. Discussing various methods used for management accounting reporting.......................4

TASK 2............................................................................................................................................6

P3. Calculation of absorption and marginal costing and discussing differences between them.6

TASK 3 ...........................................................................................................................................9

P4. Various types of planning tools in the business...............................................................9

P5. Enumerate how company is responding to financial problems by adopting management

accounting systems...............................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting information is quite useful for management so that it may be

able to have better and effective decisions. It is useful for management to take internal decisions

for organisation in the best possible way. The present report deals with Vectair holdings, which

uses management accounting in daily operations quite effectually. The management accounting

information is helpful for managers to remove deficiencies in effective way so that profit may be

earned by satisfying customers. This report also highlights various methods of management

accounting reports and also methods which are being used by company for effectual results.

Moreover, marginal and absorption costing is also discussed in the same. Budgetary control tools

such as NPV, ARR and IRR are also discussed which are relevant to management for making

decisions concerning investment. Furthermore, it also discusses how financial problems are

effectively handled by organisation with the help of management accounting information.

TASK 1

To: General Manager

Vectair Holdings

From: Management accounting officer

Subject: Presenting report to General Manager in Vectair Holdings

Introduction:

Management accounting techniques needs to be used by Vectair holdings so that it may

have better internal efficiency in the organisation. This will help to have financial stability in

the organisation with much ease.

P1. Defining management accounting and discussing various types of it.

Management accounting is useful in organisation be it small, medium or large. This

guides management to take better and effective internal decisions for betterment of the company.

Vectair holdings is also benefited by using management accounting techniques and various

methods for better growth and effective functioning in the market. It is defined as the process of

analysis and interpretation of financial data collected with the help of financial and cost

accounting both. This branch draws conclusion from both accounting in order to assist

1

Management accounting information is quite useful for management so that it may be

able to have better and effective decisions. It is useful for management to take internal decisions

for organisation in the best possible way. The present report deals with Vectair holdings, which

uses management accounting in daily operations quite effectually. The management accounting

information is helpful for managers to remove deficiencies in effective way so that profit may be

earned by satisfying customers. This report also highlights various methods of management

accounting reports and also methods which are being used by company for effectual results.

Moreover, marginal and absorption costing is also discussed in the same. Budgetary control tools

such as NPV, ARR and IRR are also discussed which are relevant to management for making

decisions concerning investment. Furthermore, it also discusses how financial problems are

effectively handled by organisation with the help of management accounting information.

TASK 1

To: General Manager

Vectair Holdings

From: Management accounting officer

Subject: Presenting report to General Manager in Vectair Holdings

Introduction:

Management accounting techniques needs to be used by Vectair holdings so that it may

have better internal efficiency in the organisation. This will help to have financial stability in

the organisation with much ease.

P1. Defining management accounting and discussing various types of it.

Management accounting is useful in organisation be it small, medium or large. This

guides management to take better and effective internal decisions for betterment of the company.

Vectair holdings is also benefited by using management accounting techniques and various

methods for better growth and effective functioning in the market. It is defined as the process of

analysis and interpretation of financial data collected with the help of financial and cost

accounting both. This branch draws conclusion from both accounting in order to assist

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management in the process of decision-making. Thus, it is clear from the above definition that

management accounting information is used to take internal decisions so that it may be helpful

for management to take better decisions (Albelda, 2011).

This type of accounting information is only available to management to take decisions

and as such this is not provided to users of accounting information. This information remains

within the hands of management of the company. Vectair holdings is much benefited by this

information as through this, it can analyse strengths and weaknesses of company. Thus,

management can strict action to remove such defects which hinders performance with much

ease. This is possible only because relevant and meaningful information imparted to managers.

Management accounting is a process of summarizing information, which is provided by

financial accounting through recording of business transactions in the books of accounts. As

such, cost accounting is concerned with controlling cost so that revenue may exceed expenses.

This information of cost and financial accounting is compiled in the form of management

accounting information, which is then provided to managers for taking decisions. However,

maintaining management accounting is not required by law but firm may prepare managerial

reports for the betterment of company (Burritt, Schaltegger and Zvezdov, 2011). The different

types of management accounting and essential requirements in company is listed below:

1. Inventory management system-

The inventory management system is not a static process but is a ongoing process as

production of goods is required so that goods may be produced at regular intervals. The

inventory is required to be updated so that no wastage may occur. If stock is more in quantity,

then it leads to unnecessary spoilage and adds to cost. Thus, inventory should be in adequate

manner so that no such wastage occurs which reduces profit of company. This management

technique helps Vectair holdings to effectively managed inventory at daily basis as it takes order

from customers and then timely ship products so that they may be satisfied with it quite effectual

way. It is a complex process, which has to be dealt by management of company in effective way

so that proper inventory system in organisation may be made with much ease.

2. Cost accounting-

2

management accounting information is used to take internal decisions so that it may be helpful

for management to take better decisions (Albelda, 2011).

This type of accounting information is only available to management to take decisions

and as such this is not provided to users of accounting information. This information remains

within the hands of management of the company. Vectair holdings is much benefited by this

information as through this, it can analyse strengths and weaknesses of company. Thus,

management can strict action to remove such defects which hinders performance with much

ease. This is possible only because relevant and meaningful information imparted to managers.

Management accounting is a process of summarizing information, which is provided by

financial accounting through recording of business transactions in the books of accounts. As

such, cost accounting is concerned with controlling cost so that revenue may exceed expenses.

This information of cost and financial accounting is compiled in the form of management

accounting information, which is then provided to managers for taking decisions. However,

maintaining management accounting is not required by law but firm may prepare managerial

reports for the betterment of company (Burritt, Schaltegger and Zvezdov, 2011). The different

types of management accounting and essential requirements in company is listed below:

1. Inventory management system-

The inventory management system is not a static process but is a ongoing process as

production of goods is required so that goods may be produced at regular intervals. The

inventory is required to be updated so that no wastage may occur. If stock is more in quantity,

then it leads to unnecessary spoilage and adds to cost. Thus, inventory should be in adequate

manner so that no such wastage occurs which reduces profit of company. This management

technique helps Vectair holdings to effectively managed inventory at daily basis as it takes order

from customers and then timely ship products so that they may be satisfied with it quite effectual

way. It is a complex process, which has to be dealt by management of company in effective way

so that proper inventory system in organisation may be made with much ease.

2. Cost accounting-

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting is another useful method of management accounting, which is essential

requirement in firm as it helps management of Vectair holdings to control costs in effective way.

This is important technique as it determine cost of production in effectual way. To ascertain and

determine cost is required so that expenses may be controlled and even reduced which eventually

helps to increase profits of firm in the best possible way. This is required so that organisation

may not waste scarce resources on unproductive activities, which provides nothing but adds to

cost (Caglio and Ditillo, 2012). For initiating this, it is required that firm may analyse firstly

which activities generate profitable operations. Then those products may be analysed which are

not profitable. As such, calculation of costs may be correctly ascertained. This helps company to

reduce unwanted expenses in the best possible way.

3. Job costing-

It is also another useful method, which is used by management to reduce the costs

incurred on each jobs, which is helping in the production process. By ascertaining correct cost of

each job helps Vectair holdings to reduce expenditures on unproductive jobs, which are

deteriorating profits, or in simple words, cost of jobs may not exceed revenue of firm. This

method helps to accumulate information about costs that are associated to particular job in the

organisation. This is information is useful for management as controls costs that are related to

specific jobs in effective way. This also provides transparency and clarity to allocate cost to

factors of production keeping in mind, how profit may be generated by employing such factors

of production in effectual way. As a result, job costing aids to management for better decision-

making.

4. Price optimisation-

Price optimisation technique is basically preparing mathematical models to determine

price level of products at a particular price. This is done by management to judge whether

customers will be attracted to products at quoted price. This provides clarity to firm to quote

price at prevailing market price or that by price which customers willing to pay for it (Otley,

2016). This is a technique to analyse how demand of the company’s product varies at different

prices and as such, suitable price is quoted by organisation by predicting profit margin, stock

levels and then recommending competitive price, which will provide increased profits to

company in quite effectual way with much ease. Thus, price optimisation is quite effective and

3

requirement in firm as it helps management of Vectair holdings to control costs in effective way.

This is important technique as it determine cost of production in effectual way. To ascertain and

determine cost is required so that expenses may be controlled and even reduced which eventually

helps to increase profits of firm in the best possible way. This is required so that organisation

may not waste scarce resources on unproductive activities, which provides nothing but adds to

cost (Caglio and Ditillo, 2012). For initiating this, it is required that firm may analyse firstly

which activities generate profitable operations. Then those products may be analysed which are

not profitable. As such, calculation of costs may be correctly ascertained. This helps company to

reduce unwanted expenses in the best possible way.

3. Job costing-

It is also another useful method, which is used by management to reduce the costs

incurred on each jobs, which is helping in the production process. By ascertaining correct cost of

each job helps Vectair holdings to reduce expenditures on unproductive jobs, which are

deteriorating profits, or in simple words, cost of jobs may not exceed revenue of firm. This

method helps to accumulate information about costs that are associated to particular job in the

organisation. This is information is useful for management as controls costs that are related to

specific jobs in effective way. This also provides transparency and clarity to allocate cost to

factors of production keeping in mind, how profit may be generated by employing such factors

of production in effectual way. As a result, job costing aids to management for better decision-

making.

4. Price optimisation-

Price optimisation technique is basically preparing mathematical models to determine

price level of products at a particular price. This is done by management to judge whether

customers will be attracted to products at quoted price. This provides clarity to firm to quote

price at prevailing market price or that by price which customers willing to pay for it (Otley,

2016). This is a technique to analyse how demand of the company’s product varies at different

prices and as such, suitable price is quoted by organisation by predicting profit margin, stock

levels and then recommending competitive price, which will provide increased profits to

company in quite effectual way with much ease. Thus, price optimisation is quite effective and

3

useful technique which is used by management to analyse demand of the product in the market in

the best possible way.

P2. Discussing various methods used for management accounting reporting

The various methods, which are used, for reporting purpose are as follows:

1. Segmental report:

The segmental report is basically a report that consists of operating segments of company

which is being disclosed with reference to financial statements of the company in quite effective

way. This helps management to take better and effective decisions with much ease. It is required

only for public entities and not for private ones to grasp information to take decisions in effectual

way (Cooper, Ezzamel and Qu, 2017). However, the segment report is provided to stakeholders

such as creditors and investors regarding financial position of operating departments of the

company so that they may be able to take decisions about the soundness of organisation in quite

effective way.

Vectair holdings quite effectively take decisions for the betterment of it by relying on the

segmental reports. This report include information such as depreciation, amortisation, type of

products, which are sold by each segment of the firm and many more. Moreover, it also includes

information related to non-cash items, material expenditure items etc. which are much beneficial

to creditors and investors to take enhanced decisions in the best possible way.

2. Performance report:

The performance report deals with much needed information to management with

reference to individual performance of workers. This is essential so that budgeting output may be

easily compared with that of actual performance and if any deviations exist then corrective

actions are taken by management. This whole procedure is attained or done in a specific period

so that performance of employees’ may be analysed quite effectively with much ease. The

performance report measures or provides results of employee during specific period with much

ease. Thus, it ensures that overall performance of workers are not declined and if such happens

then corrective actions are taken to remove such deviations by the management (Tappura, 2015).

The deviations, which exist, is called variance. It can be favourable or unfavourable

depending upon the high or low deviations, which has occurred from the relative standards

4

the best possible way.

P2. Discussing various methods used for management accounting reporting

The various methods, which are used, for reporting purpose are as follows:

1. Segmental report:

The segmental report is basically a report that consists of operating segments of company

which is being disclosed with reference to financial statements of the company in quite effective

way. This helps management to take better and effective decisions with much ease. It is required

only for public entities and not for private ones to grasp information to take decisions in effectual

way (Cooper, Ezzamel and Qu, 2017). However, the segment report is provided to stakeholders

such as creditors and investors regarding financial position of operating departments of the

company so that they may be able to take decisions about the soundness of organisation in quite

effective way.

Vectair holdings quite effectively take decisions for the betterment of it by relying on the

segmental reports. This report include information such as depreciation, amortisation, type of

products, which are sold by each segment of the firm and many more. Moreover, it also includes

information related to non-cash items, material expenditure items etc. which are much beneficial

to creditors and investors to take enhanced decisions in the best possible way.

2. Performance report:

The performance report deals with much needed information to management with

reference to individual performance of workers. This is essential so that budgeting output may be

easily compared with that of actual performance and if any deviations exist then corrective

actions are taken by management. This whole procedure is attained or done in a specific period

so that performance of employees’ may be analysed quite effectively with much ease. The

performance report measures or provides results of employee during specific period with much

ease. Thus, it ensures that overall performance of workers are not declined and if such happens

then corrective actions are taken to remove such deviations by the management (Tappura, 2015).

The deviations, which exist, is called variance. It can be favourable or unfavourable

depending upon the high or low deviations, which has occurred from the relative standards

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

quoted by management in effective way. As such, performance reports are quite useful for

management to assess performance of employee so that it can be enhanced in a better way and

eventually firm may be able to earn more profits in the best possible way.

3. Inventory management report:

The inventory is required to be maintained in sufficient quantity so that it may not lead to

wastage. Inventory management report is one such report, which provides information to

management related to inventory. Stock means goods which may or may not be in the form of

raw material are being kept in the warehouse of the company which are required for future

production purpose. As such, it is essential that company must order only required quantity of

inventory so that it may used in a stated period and as such no handling cost is incurred by it

(Chenhall and Moers, 2015).

Inventory management report provides information regarding current inventory in the

warehouse and as such, this information is being used by management to analyse whether

sufficient amount of inventory is available or production department needs to have more stock to

carry out production process without any interruption. As a result, inventory is being analysed

and as such, no wastage and spoilage is made.

4. Accounts receivables ageing report:

The accounts receivables ageing report is basically used by management to determine

how much money is required to be received by company from the credit customers in a particular

period. This is important to collect money from the customers so that it can be effectively

utilised by company in carrying out daily operations in quite effectual manner. If much of the

payment is outstanding from the customers, then strict credit policies may be implemented by

Vectair holdings so that it may get timely payments with much ease (Fourie and et.al, 2015).

This report consists of all the unpaid invoices, which are of credit customers and have

become overdue for the payment of the same. Moreover, accounts receivables report also

includes unused credit memos in accordance with date ranges. This report deals with contact

information of the customers which are then approached by management so that they pay their

unpaid invoices which had become overdue for payment in quite effective way. As such, this

5

management to assess performance of employee so that it can be enhanced in a better way and

eventually firm may be able to earn more profits in the best possible way.

3. Inventory management report:

The inventory is required to be maintained in sufficient quantity so that it may not lead to

wastage. Inventory management report is one such report, which provides information to

management related to inventory. Stock means goods which may or may not be in the form of

raw material are being kept in the warehouse of the company which are required for future

production purpose. As such, it is essential that company must order only required quantity of

inventory so that it may used in a stated period and as such no handling cost is incurred by it

(Chenhall and Moers, 2015).

Inventory management report provides information regarding current inventory in the

warehouse and as such, this information is being used by management to analyse whether

sufficient amount of inventory is available or production department needs to have more stock to

carry out production process without any interruption. As a result, inventory is being analysed

and as such, no wastage and spoilage is made.

4. Accounts receivables ageing report:

The accounts receivables ageing report is basically used by management to determine

how much money is required to be received by company from the credit customers in a particular

period. This is important to collect money from the customers so that it can be effectively

utilised by company in carrying out daily operations in quite effectual manner. If much of the

payment is outstanding from the customers, then strict credit policies may be implemented by

Vectair holdings so that it may get timely payments with much ease (Fourie and et.al, 2015).

This report consists of all the unpaid invoices, which are of credit customers and have

become overdue for the payment of the same. Moreover, accounts receivables report also

includes unused credit memos in accordance with date ranges. This report deals with contact

information of the customers which are then approached by management so that they pay their

unpaid invoices which had become overdue for payment in quite effective way. As such, this

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

report is quite relevant and powerful tool for company to call for unpaid invoices and as such,

Vectair holdings may have effective credit policies in the best possible way.

5. Job cost report:

This report deals with various jobs, which are associated with the production process. This report

provides information to management in effective way so that it may be able to analyse costs

associated with such jobs. Through this report, management is able to determine whether profit is

being generated by such jobs or not and as such, it decides to control expenses in the best

possible way by analysing job cost report. Thus, this report is worth for management to take

effective decisions for the betterment of firm quite easily (RAHNAMAYE and ROSTAMI,

2015).

Job cost report shows expenditures, which are, incurred on specific jobs and as such,

management analyses it and control the cost in effective way so that revenue may exceed costs.

As a result, job cost report is effectively utilised by management to take effective and better

decisions so that costs may be controlled effectually.

The benefits of management accounting systems in company

Management accounting is quite useful for management to control on expenditures and

various costs that are incurred on specific jobs and as such, profits can be earned by using

benefits of management accounting information with much ease. Vectair holdings can use this

information as it provides with transparency of various costs which are obtained in the process of

production. By using this information, customer's requirements may be forecasted by company

and as such, it helps to assess needs of customers' by analysing demand and as a result,

management accounting systems are beneficial for company.

TASK 2

P3. Calculation of absorption and marginal costing and discussing differences between them

Computation of Marginal costing for Vectair Holdings

6

Vectair holdings may have effective credit policies in the best possible way.

5. Job cost report:

This report deals with various jobs, which are associated with the production process. This report

provides information to management in effective way so that it may be able to analyse costs

associated with such jobs. Through this report, management is able to determine whether profit is

being generated by such jobs or not and as such, it decides to control expenses in the best

possible way by analysing job cost report. Thus, this report is worth for management to take

effective decisions for the betterment of firm quite easily (RAHNAMAYE and ROSTAMI,

2015).

Job cost report shows expenditures, which are, incurred on specific jobs and as such,

management analyses it and control the cost in effective way so that revenue may exceed costs.

As a result, job cost report is effectively utilised by management to take effective and better

decisions so that costs may be controlled effectually.

The benefits of management accounting systems in company

Management accounting is quite useful for management to control on expenditures and

various costs that are incurred on specific jobs and as such, profits can be earned by using

benefits of management accounting information with much ease. Vectair holdings can use this

information as it provides with transparency of various costs which are obtained in the process of

production. By using this information, customer's requirements may be forecasted by company

and as such, it helps to assess needs of customers' by analysing demand and as a result,

management accounting systems are beneficial for company.

TASK 2

P3. Calculation of absorption and marginal costing and discussing differences between them

Computation of Marginal costing for Vectair Holdings

6

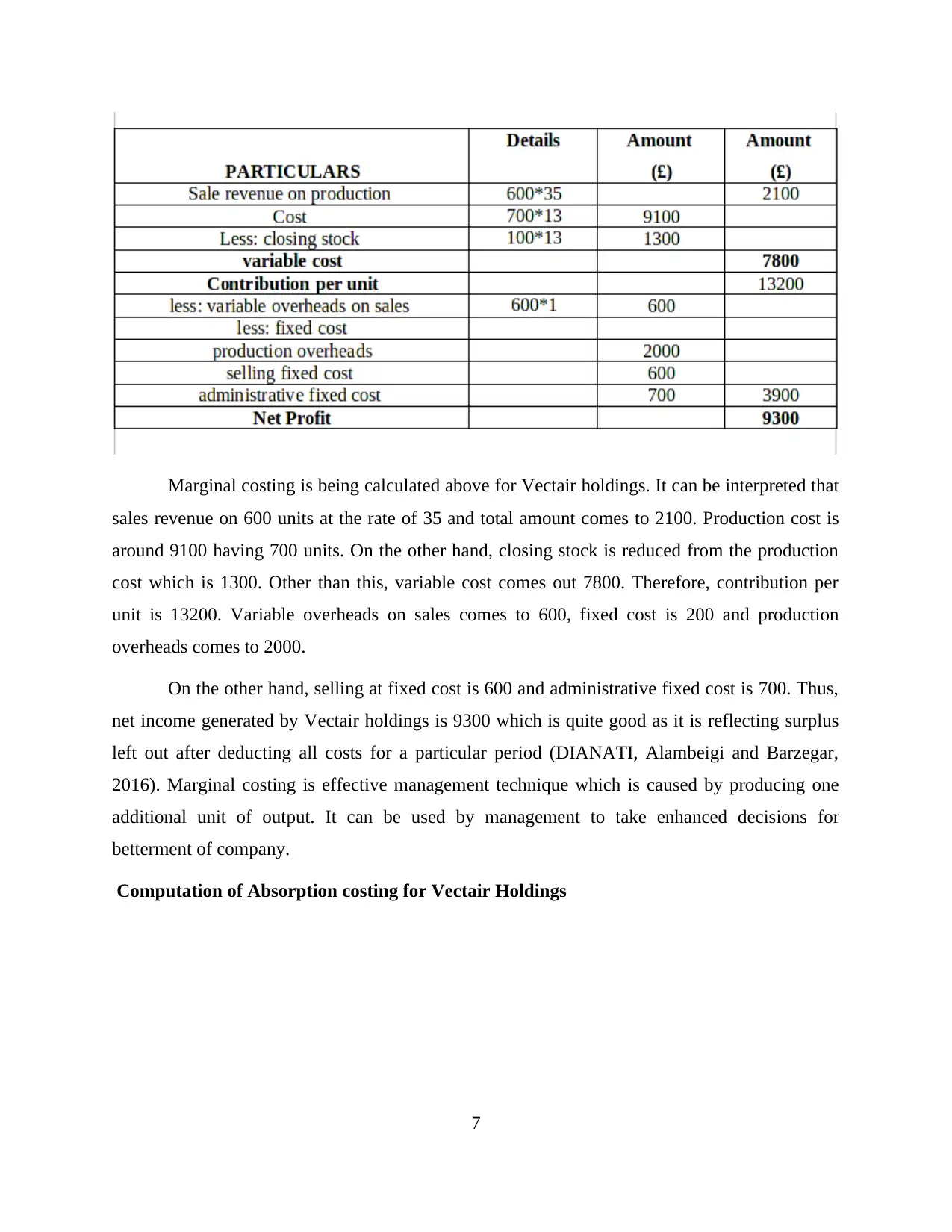

Marginal costing is being calculated above for Vectair holdings. It can be interpreted that

sales revenue on 600 units at the rate of 35 and total amount comes to 2100. Production cost is

around 9100 having 700 units. On the other hand, closing stock is reduced from the production

cost which is 1300. Other than this, variable cost comes out 7800. Therefore, contribution per

unit is 13200. Variable overheads on sales comes to 600, fixed cost is 200 and production

overheads comes to 2000.

On the other hand, selling at fixed cost is 600 and administrative fixed cost is 700. Thus,

net income generated by Vectair holdings is 9300 which is quite good as it is reflecting surplus

left out after deducting all costs for a particular period (DIANATI, Alambeigi and Barzegar,

2016). Marginal costing is effective management technique which is caused by producing one

additional unit of output. It can be used by management to take enhanced decisions for

betterment of company.

Computation of Absorption costing for Vectair Holdings

7

sales revenue on 600 units at the rate of 35 and total amount comes to 2100. Production cost is

around 9100 having 700 units. On the other hand, closing stock is reduced from the production

cost which is 1300. Other than this, variable cost comes out 7800. Therefore, contribution per

unit is 13200. Variable overheads on sales comes to 600, fixed cost is 200 and production

overheads comes to 2000.

On the other hand, selling at fixed cost is 600 and administrative fixed cost is 700. Thus,

net income generated by Vectair holdings is 9300 which is quite good as it is reflecting surplus

left out after deducting all costs for a particular period (DIANATI, Alambeigi and Barzegar,

2016). Marginal costing is effective management technique which is caused by producing one

additional unit of output. It can be used by management to take enhanced decisions for

betterment of company.

Computation of Absorption costing for Vectair Holdings

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption costing is computed for Vectair holdings. This is quite useful tool in

manufacturing cost absorption in organisation. Direct and indirect expenditures are taken and

then accordingly absorbed in the production of goods. The above calculation may be interpreted

that sales on production is around 2100 having 600 units at the rate of 35. Manufacturing cost is

11200 which has extracted out of 700 units at the rate of 16. For inventories, value is 1600 in

which 100 units at the rate of 16 per unit. On the other hand, fixed production overheads which is

deducted from sales is 100. By deducting all these expenditures, gross profit is being arrived

which has come to 11500.

After arriving at gross profit, various costs are deducted. These costs are variable

overheads on sales as 600, fixed cost at selling as 600 and administrative cost as 700. After

reducing above costs, net profit is produced as 9600 which is overall good as after absorbing

manufacturing costs, firm has generated 9600 amount of net income (Coad, Jack and Kholeif,

2015).

The differences between absorption and marginal costing are as follows:

1. Marginal costing is calculated by applying only variable cost as fixed costs are being ignored.

On the other hand, fixed costs are used while calculating absorption costing.

2. Profit calculated is different from both methods. As such, individual sales of products are

being attained to calculate profits and this will provide more profits as compared to profits

calculated by absorption costing method.

8

manufacturing cost absorption in organisation. Direct and indirect expenditures are taken and

then accordingly absorbed in the production of goods. The above calculation may be interpreted

that sales on production is around 2100 having 600 units at the rate of 35. Manufacturing cost is

11200 which has extracted out of 700 units at the rate of 16. For inventories, value is 1600 in

which 100 units at the rate of 16 per unit. On the other hand, fixed production overheads which is

deducted from sales is 100. By deducting all these expenditures, gross profit is being arrived

which has come to 11500.

After arriving at gross profit, various costs are deducted. These costs are variable

overheads on sales as 600, fixed cost at selling as 600 and administrative cost as 700. After

reducing above costs, net profit is produced as 9600 which is overall good as after absorbing

manufacturing costs, firm has generated 9600 amount of net income (Coad, Jack and Kholeif,

2015).

The differences between absorption and marginal costing are as follows:

1. Marginal costing is calculated by applying only variable cost as fixed costs are being ignored.

On the other hand, fixed costs are used while calculating absorption costing.

2. Profit calculated is different from both methods. As such, individual sales of products are

being attained to calculate profits and this will provide more profits as compared to profits

calculated by absorption costing method.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Contribution margin is used is deducted from overhead to calculate profit under marginal

costing whereas, under absorption costing, gross profit is used to ascertain profits of the concern.

4. Financial reporting is not required under marginal costing. Besides this, it is required for

absorption costing. As such, both methods have their own importance in organisation to

determine cost quite effectively (Shields, 2015).

Management accounting methods and financial reporting-

The method used in management accounting are revaluation accounting and cost

variance. Revaluation accounting is a technique which is made to analyse current market rate of

assets by making certain adjustment to derive current rate of company's assets in the best

possible way. On the other hand, cost variance is the difference which is extracted out of

budgeted costs and actual costs. This is essential and deviations or variance is resolved by taking

corrective actions. As such, it is useful for financial reporting as well.

TASK 3

P4. Various types of planning tools in the business

1. Zero based budgeting-

Zero based budgeting is quite essential as unlike other budgeting tools which takes

previous year budget to make current year one, this completely differs from them. It does not use

past year figures to prepare budget and prepare from zero or scratch base.

Advantages:

1. Inflated budgets are completely ignored as everything is prepared from scratch base.

Proper allocation of resources are also found in this budget (Anessi-Pessina and et.al,

2017).

2. Zero based budget is quite useful as it helps to identify wastages and eliminates it easily.

Disadvantages:

1. This method is time consuming as necessary expenditures are sometimes difficult to

obtain. Basic limitation of this method is that takes lot of time to extract plenty of

expenses.

9

costing whereas, under absorption costing, gross profit is used to ascertain profits of the concern.

4. Financial reporting is not required under marginal costing. Besides this, it is required for

absorption costing. As such, both methods have their own importance in organisation to

determine cost quite effectively (Shields, 2015).

Management accounting methods and financial reporting-

The method used in management accounting are revaluation accounting and cost

variance. Revaluation accounting is a technique which is made to analyse current market rate of

assets by making certain adjustment to derive current rate of company's assets in the best

possible way. On the other hand, cost variance is the difference which is extracted out of

budgeted costs and actual costs. This is essential and deviations or variance is resolved by taking

corrective actions. As such, it is useful for financial reporting as well.

TASK 3

P4. Various types of planning tools in the business

1. Zero based budgeting-

Zero based budgeting is quite essential as unlike other budgeting tools which takes

previous year budget to make current year one, this completely differs from them. It does not use

past year figures to prepare budget and prepare from zero or scratch base.

Advantages:

1. Inflated budgets are completely ignored as everything is prepared from scratch base.

Proper allocation of resources are also found in this budget (Anessi-Pessina and et.al,

2017).

2. Zero based budget is quite useful as it helps to identify wastages and eliminates it easily.

Disadvantages:

1. This method is time consuming as necessary expenditures are sometimes difficult to

obtain. Basic limitation of this method is that takes lot of time to extract plenty of

expenses.

9

2. It requires more man power such as technical people which are managers to justify each

expenses in the organisation. This requires more technical knowledge of manager and as

such, proper training is required to be imparted to them.

2. IRR (Internal Rate of Return)-

This planning tool is quite relevant to company in determining whether to invest in

particular project or not. It is a method which is used for estimating profitability of investment in

the project. As such, it is quite useful for Vectair holdings to invest in the project by having

rough estimate of profit that might be generated by the project (Messner, 2016).

Advantages:

1. This method of capital appraisal takes into consideration time value of money while

evaluating project effectiveness which is ignored in other techniques.

2. This method is simple to calculate and as such, results are interpreted quite effectively

and used by management to check viability of project under consideration.

Disadvantages:

1. The basic disadvantage of IRR method is that it ignores economies of scale. In simple

words, actual benefit in value is ignored by it.

2. Another limitation of IRR is that it involves large calculations which sometimes initiates

complexity. This gives importance only to profitability of the project and does not take

other essential aspects.

3. NPV (Net Present Value)-

This method of capital appraisal assess or determine present value of cash flow and then

proceeds with the investment after assessing present value. Thus, if Vectair holdings need to

have effective gain from the investment, it can use this technique for ascertaining value of cash

flow with much ease (Englund and Gerdin, 2018).

Advantages:

10

expenses in the organisation. This requires more technical knowledge of manager and as

such, proper training is required to be imparted to them.

2. IRR (Internal Rate of Return)-

This planning tool is quite relevant to company in determining whether to invest in

particular project or not. It is a method which is used for estimating profitability of investment in

the project. As such, it is quite useful for Vectair holdings to invest in the project by having

rough estimate of profit that might be generated by the project (Messner, 2016).

Advantages:

1. This method of capital appraisal takes into consideration time value of money while

evaluating project effectiveness which is ignored in other techniques.

2. This method is simple to calculate and as such, results are interpreted quite effectively

and used by management to check viability of project under consideration.

Disadvantages:

1. The basic disadvantage of IRR method is that it ignores economies of scale. In simple

words, actual benefit in value is ignored by it.

2. Another limitation of IRR is that it involves large calculations which sometimes initiates

complexity. This gives importance only to profitability of the project and does not take

other essential aspects.

3. NPV (Net Present Value)-

This method of capital appraisal assess or determine present value of cash flow and then

proceeds with the investment after assessing present value. Thus, if Vectair holdings need to

have effective gain from the investment, it can use this technique for ascertaining value of cash

flow with much ease (Englund and Gerdin, 2018).

Advantages:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.