Case Study: Vino Pte Ltd - Finance Function Consolidation Analysis

VerifiedAdded on 2023/01/19

|12

|1031

|59

Case Study

AI Summary

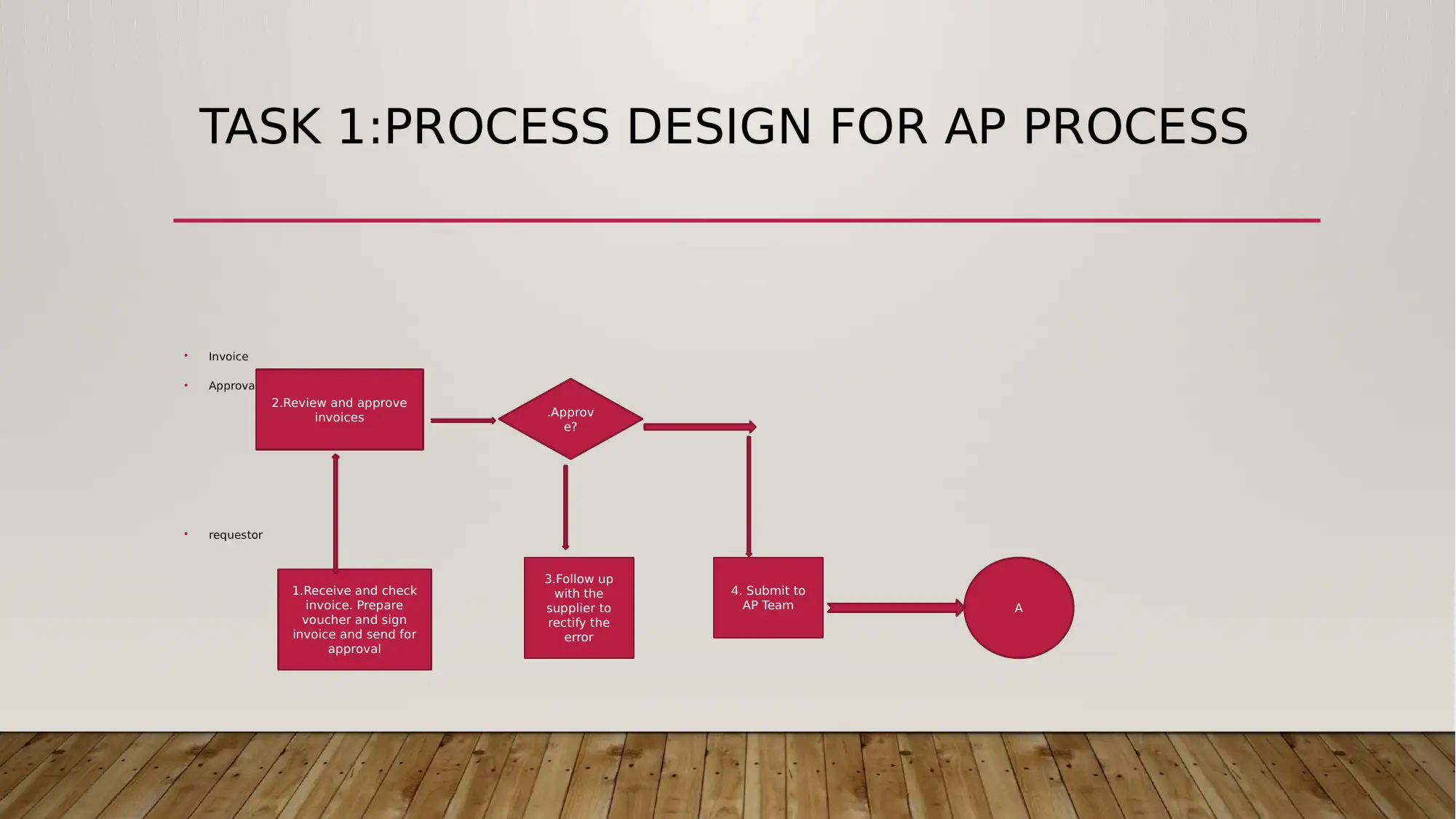

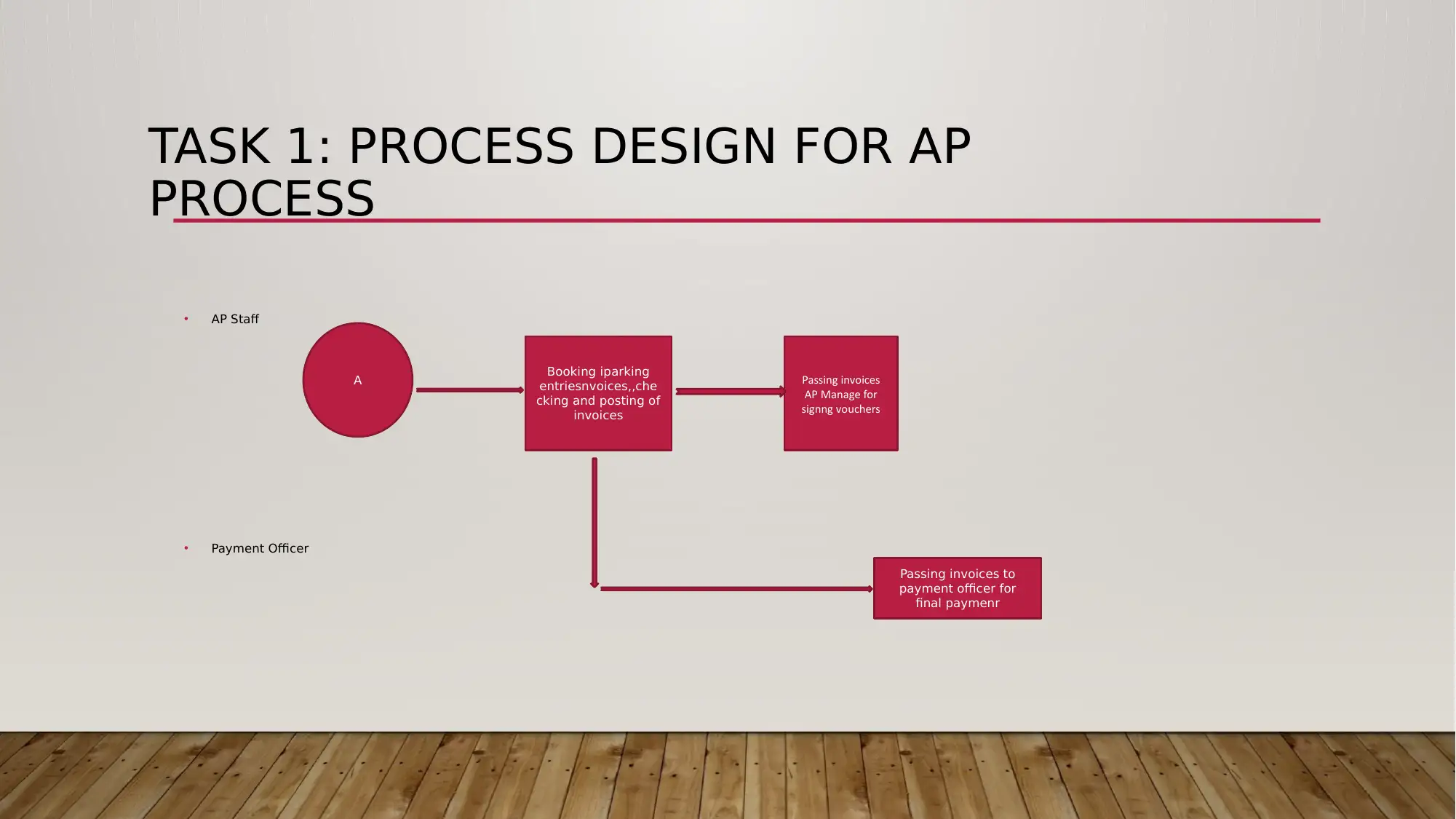

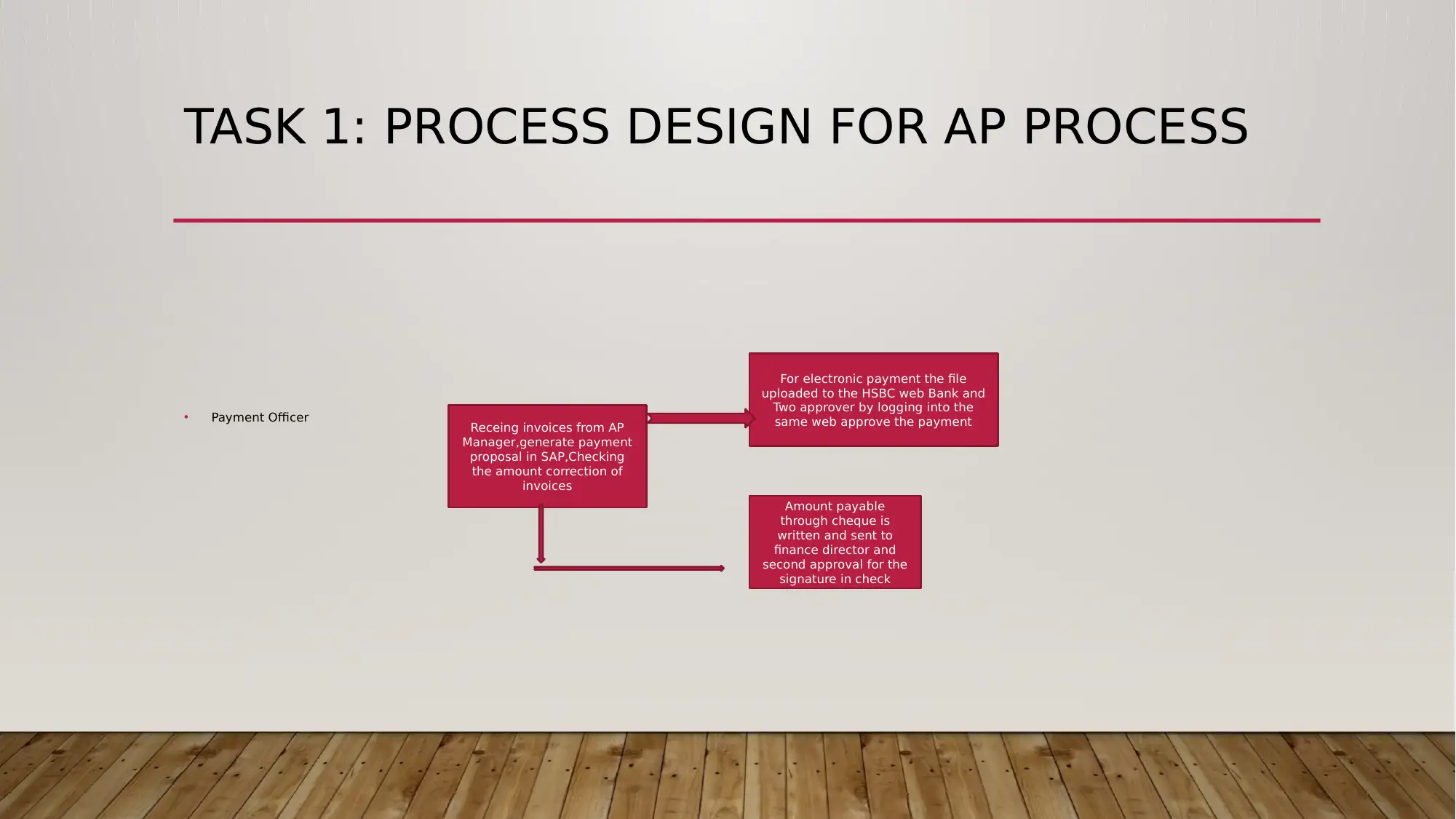

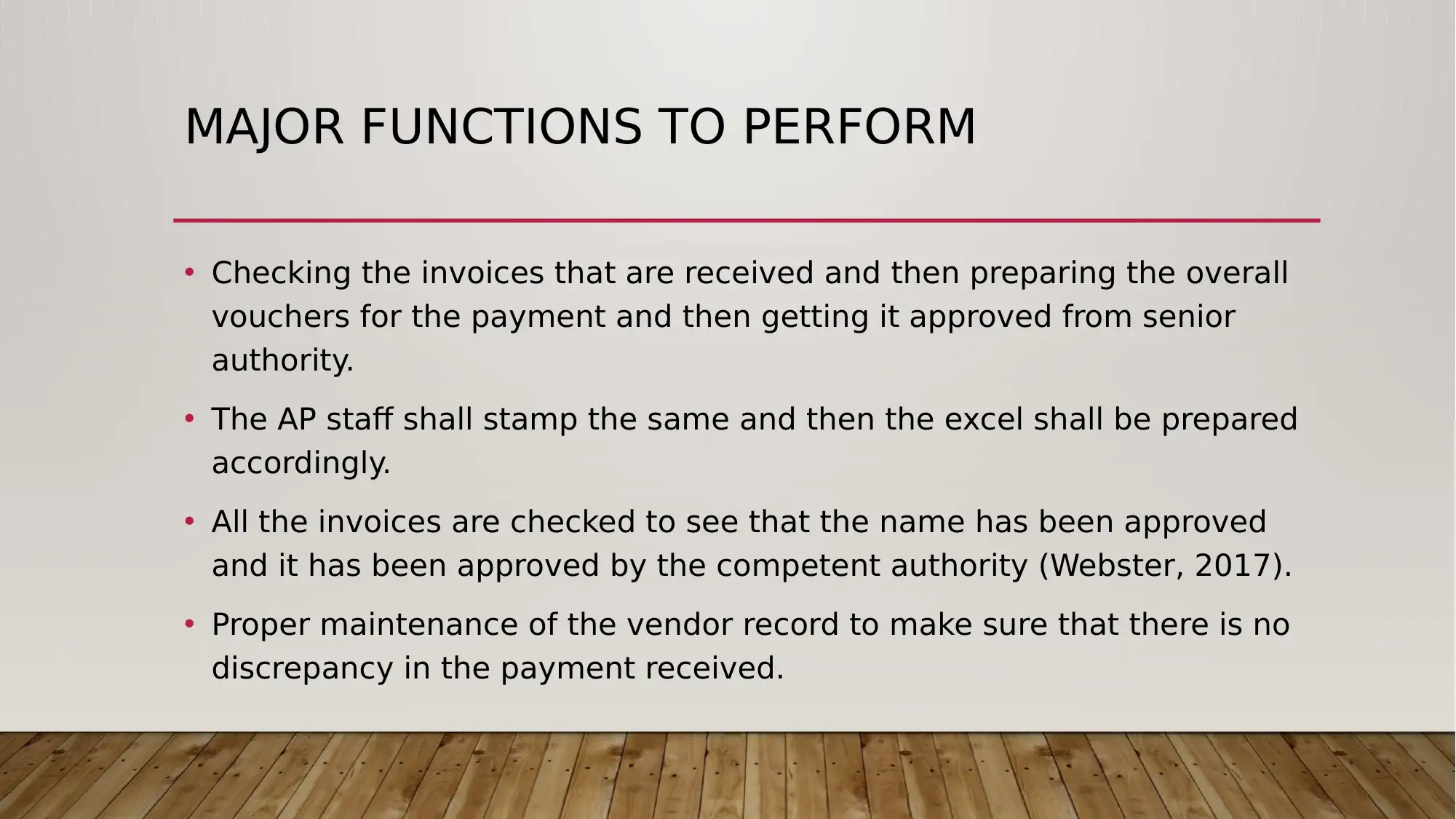

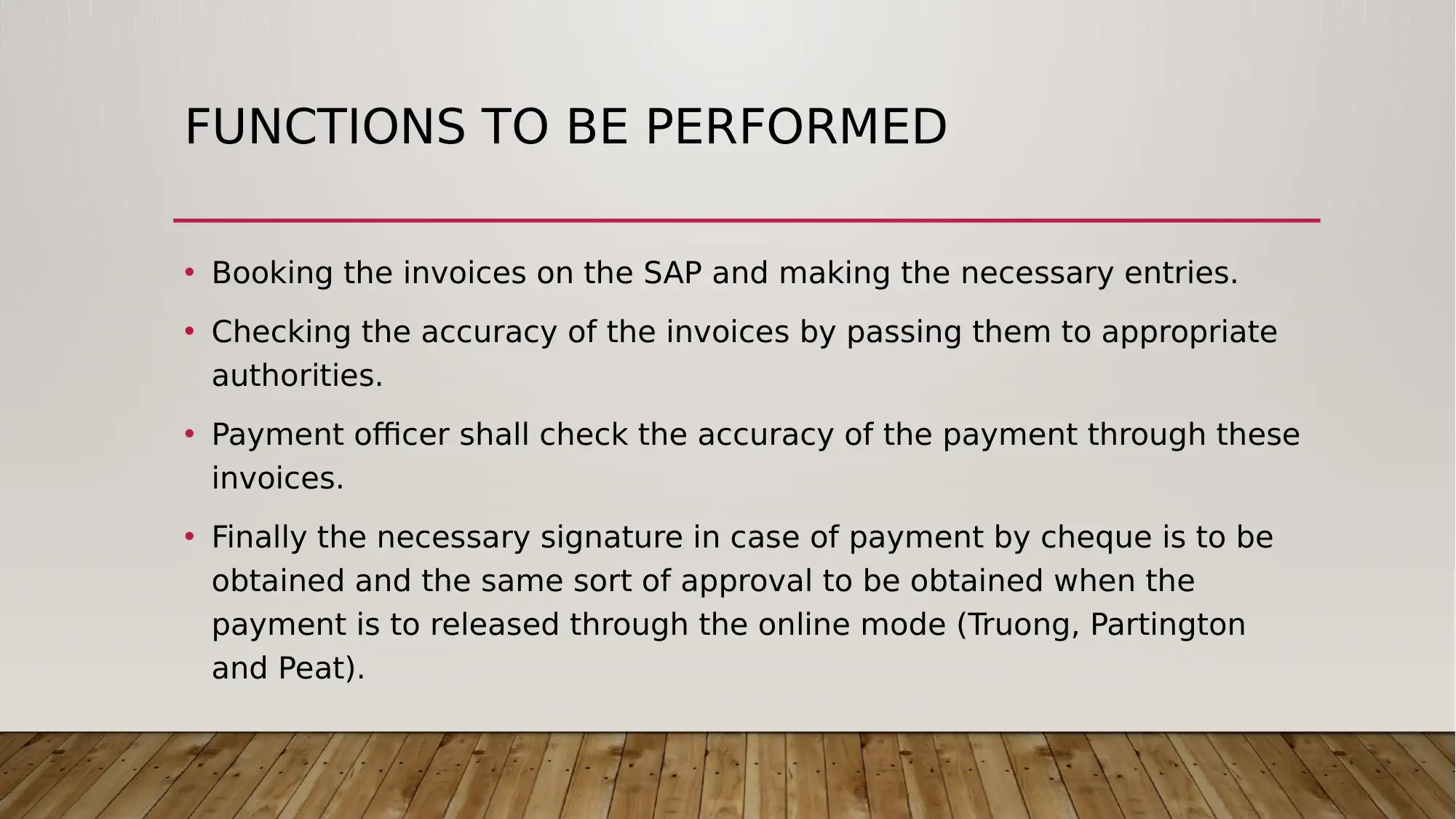

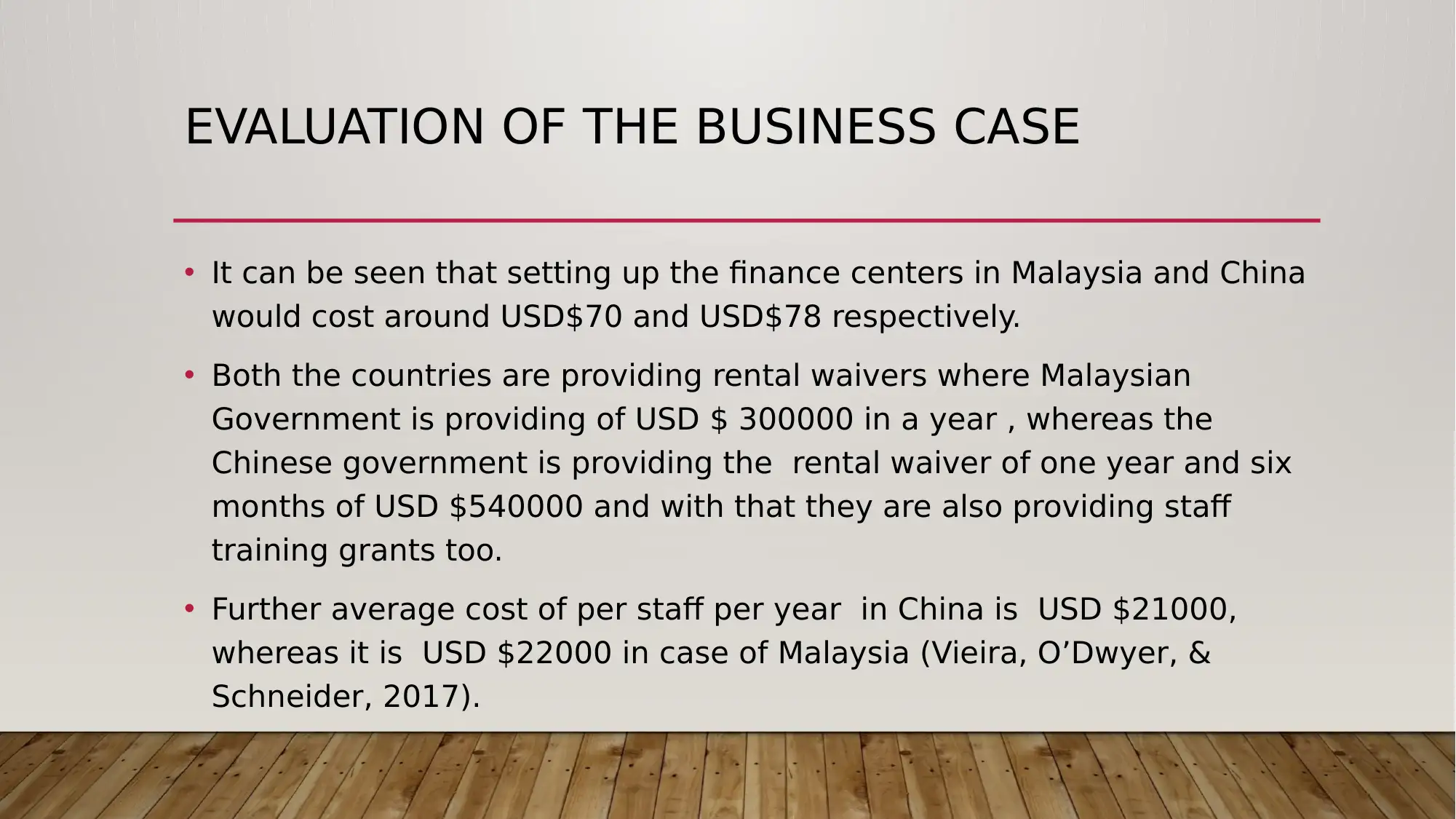

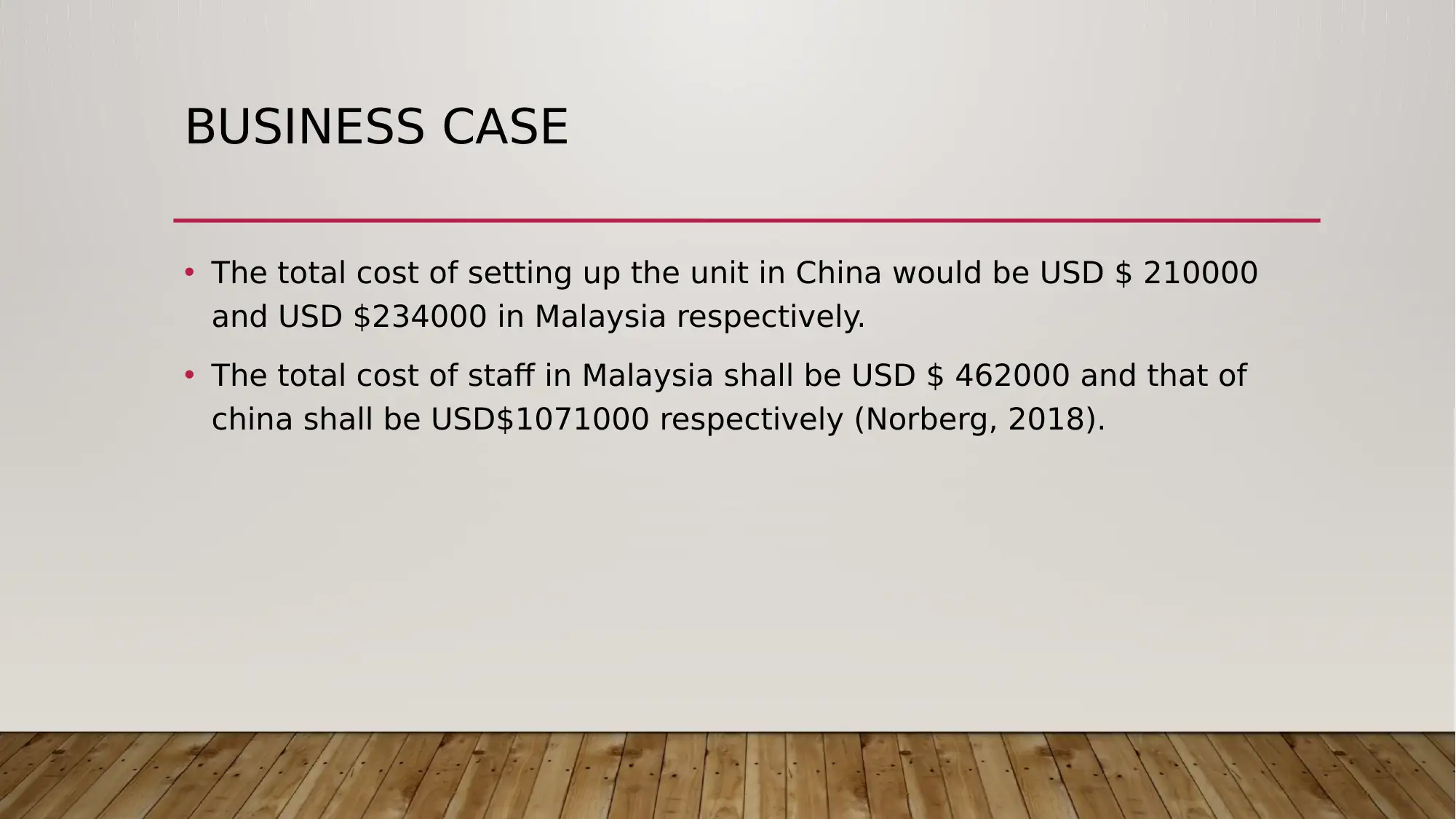

This case study examines Vino Pte Ltd, a wine distributor in the Asia Pacific region, facing rising finance costs. The assignment involves reviewing the Accounts Payable (AP) process and designing a process flow to identify improvement opportunities. It analyzes the potential of consolidating finance functions into a Shared Service Center (SSC), comparing the costs and benefits of establishing the SSC in Malaysia versus China. The study includes a qualitative and quantitative analysis of factors like staff availability, government incentives, and staff costs. The proposed solution recommends setting up the SSC in Malaysia based on a better balance of qualitative and quantitative factors, along with suggestions for training programs to reduce associated costs. The analysis uses references from various academic sources to support the findings and recommendations.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.