Virgin Australia's Financial Statement Analysis - HI5020 Assignment

VerifiedAdded on 2023/06/11

|9

|2304

|271

Report

AI Summary

This report provides a comprehensive analysis of Virgin Australia's financial statements, focusing on the cash flow statement, other comprehensive income statement, and accounting for corporate income tax. It examines the various items reported in the cash flow statement, including operating, investing, and financing activities, and discusses changes over the past three years (2015-2017). The analysis includes receipts from customers, finance income, payments to suppliers and staff, borrowings, and investments in property, plant, and equipment. The report also discusses the components of the other comprehensive income statement, such as foreign currency translation reserve and cash flow hedge reserve. Furthermore, it explores the accounting for corporate income tax, including deferred tax assets and liabilities, and analyzes the company's tax treatment, noting the income tax benefits received due to losses incurred before income tax. The report references Virgin Australia's annual reports and relevant accounting literature to support its findings.

Running head: CORPORATE ASSIGNMENT

Corporate assignment

Name of the student

Name of the university

Author Note

Corporate assignment

Name of the student

Name of the university

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ASSIGNMENT

Table of Contents

Cash flow statement:..................................................................................................................2

(i)............................................................................................................................................2

ii)............................................................................................................................................3

Other comprehensive income statement:...................................................................................4

(iii)..........................................................................................................................................4

(iv)..........................................................................................................................................5

(v)...........................................................................................................................................5

Accounting for corporate income tax:........................................................................................5

(vi)..........................................................................................................................................5

(vii).........................................................................................................................................5

(viii)........................................................................................................................................6

(ix)..........................................................................................................................................6

(x)...........................................................................................................................................7

(xi)..........................................................................................................................................7

References:.................................................................................................................................8

Table of Contents

Cash flow statement:..................................................................................................................2

(i)............................................................................................................................................2

ii)............................................................................................................................................3

Other comprehensive income statement:...................................................................................4

(iii)..........................................................................................................................................4

(iv)..........................................................................................................................................5

(v)...........................................................................................................................................5

Accounting for corporate income tax:........................................................................................5

(vi)..........................................................................................................................................5

(vii).........................................................................................................................................5

(viii)........................................................................................................................................6

(ix)..........................................................................................................................................6

(x)...........................................................................................................................................7

(xi)..........................................................................................................................................7

References:.................................................................................................................................8

2CORPORATE ASSIGNMENT

Cash flow statement:

(i)

The chosen organisation for this assignment is Virgin Australia. The selected

organisation is one of leading Airlines Company of Australia and it is a public listed

company with its code in the Australian Securities Exchange (ASX) as VAH. The cash flow

statement of this airline company is divided into three segments, which are, operating

activities, financial activities and investing activities. The following discussion is going to

focus on the items, which the chosen organisation has categorized under each heading.

Cash flows from operating activities:

The chief components under this heading are receipts from customers, finance income

received, payments of staffs and suppliers, financial costs paid and so on. The amount of

customer receipts can be obtained through credit sales (Hui, Nelson and Yeung 2016).

According to the annual report of Virgin Australia, this customer receipts has increased from

$ 5567.40 million in 2016 to $ 5657.10 million in 2017, based on its rigid credit policy.

Finance income, on the other side, represents the sum received for utilising money regarding

payment on demand during a specific point of time. In 2017, increment of this item can be

observed, as it has written off a section of the credit sales as uncollectible. The payments

related to suppliers and staffs are the amount, which the company has bought on credit and

remunerations to the employees. For Virgin Australia, this increasing trend of payments can

be seen in 2017 due to excess purchase from suppliers and increasing number of staffs.

Financial cost, on the other side, represents the obligations and for this selected company, it

has fallen in 2017 because of less interest payments for the undertaking loans.

Cash flows from financial activities:

The chief components, which are included under this heading are repayment of and

proceed from borrowings, distributions of equity and other items. The borrowings identify the

Cash flow statement:

(i)

The chosen organisation for this assignment is Virgin Australia. The selected

organisation is one of leading Airlines Company of Australia and it is a public listed

company with its code in the Australian Securities Exchange (ASX) as VAH. The cash flow

statement of this airline company is divided into three segments, which are, operating

activities, financial activities and investing activities. The following discussion is going to

focus on the items, which the chosen organisation has categorized under each heading.

Cash flows from operating activities:

The chief components under this heading are receipts from customers, finance income

received, payments of staffs and suppliers, financial costs paid and so on. The amount of

customer receipts can be obtained through credit sales (Hui, Nelson and Yeung 2016).

According to the annual report of Virgin Australia, this customer receipts has increased from

$ 5567.40 million in 2016 to $ 5657.10 million in 2017, based on its rigid credit policy.

Finance income, on the other side, represents the sum received for utilising money regarding

payment on demand during a specific point of time. In 2017, increment of this item can be

observed, as it has written off a section of the credit sales as uncollectible. The payments

related to suppliers and staffs are the amount, which the company has bought on credit and

remunerations to the employees. For Virgin Australia, this increasing trend of payments can

be seen in 2017 due to excess purchase from suppliers and increasing number of staffs.

Financial cost, on the other side, represents the obligations and for this selected company, it

has fallen in 2017 because of less interest payments for the undertaking loans.

Cash flows from financial activities:

The chief components, which are included under this heading are repayment of and

proceed from borrowings, distributions of equity and other items. The borrowings identify the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ASSIGNMENT

net amount, which is disbursed to a borrower on behalf of the lender under the terms relate to

loan agreement (Qiu, Shaukat and Tharyan 2016). From the annual report of Virgin Australia,

it can be seen that the proceeds from borrowings have decreased in 2017 while at the same

year; increase in repayment of borrowing can be seen. On the other side, equality distribution

implies the annual cash flow that is provided to the shareholders of a particular organisation.

This amount for Virgin Australia has decreased in 2017 since importance has been placed to

maximise retained earnings.

Cash flows from investing activities:

Under this heading, the chief components are payments for and proceedings from

property, proceeds from and advances to deposits, plant and equipments and others. Property

related payments along with plant and equipment are the amount, which are incurred to

obtain necessary for conducting the business operations (Lewellen and Lewellen 2016). On

the contrary, these assts give economic benefits to the concerned organisation and for this,

they are considered as proceeds. Based on annual report of Virgin Australia, it can be

observed that the company has minimised its investment on the payments related to property,

plant and equipment. As a result, the company has not created adequate cash flows from

those items as it has as the company has sold a part o their property, plant and equipment.

Deposits relating payments and proceeds are a financial instrument that is specifying a

contract during the time of repayment and to be received along with payable interest. Virgin

Australia has generated more payments in 2017 compare to the amount it has earned from

deposits in the same year due to higher rate of interest payable.

ii)

Based on the annual report of Virgin Australia, three types of cash flows can be seen

over there, which include operating activities, financial activities and investing activities

net amount, which is disbursed to a borrower on behalf of the lender under the terms relate to

loan agreement (Qiu, Shaukat and Tharyan 2016). From the annual report of Virgin Australia,

it can be seen that the proceeds from borrowings have decreased in 2017 while at the same

year; increase in repayment of borrowing can be seen. On the other side, equality distribution

implies the annual cash flow that is provided to the shareholders of a particular organisation.

This amount for Virgin Australia has decreased in 2017 since importance has been placed to

maximise retained earnings.

Cash flows from investing activities:

Under this heading, the chief components are payments for and proceedings from

property, proceeds from and advances to deposits, plant and equipments and others. Property

related payments along with plant and equipment are the amount, which are incurred to

obtain necessary for conducting the business operations (Lewellen and Lewellen 2016). On

the contrary, these assts give economic benefits to the concerned organisation and for this,

they are considered as proceeds. Based on annual report of Virgin Australia, it can be

observed that the company has minimised its investment on the payments related to property,

plant and equipment. As a result, the company has not created adequate cash flows from

those items as it has as the company has sold a part o their property, plant and equipment.

Deposits relating payments and proceeds are a financial instrument that is specifying a

contract during the time of repayment and to be received along with payable interest. Virgin

Australia has generated more payments in 2017 compare to the amount it has earned from

deposits in the same year due to higher rate of interest payable.

ii)

Based on the annual report of Virgin Australia, three types of cash flows can be seen

over there, which include operating activities, financial activities and investing activities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ASSIGNMENT

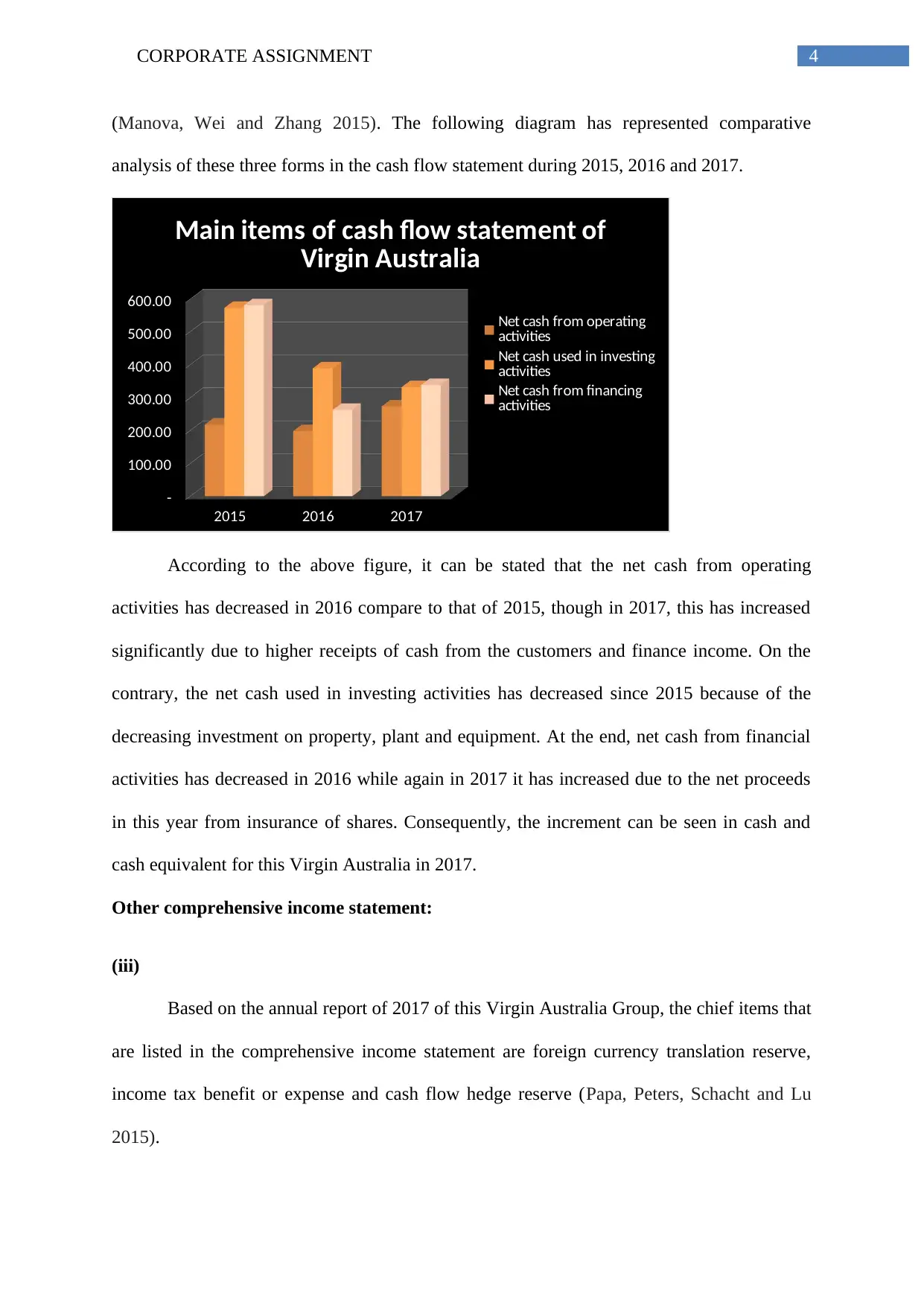

(Manova, Wei and Zhang 2015). The following diagram has represented comparative

analysis of these three forms in the cash flow statement during 2015, 2016 and 2017.

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Main items of cash flow statement of

Virgin Australia

Net cash from operating

activities

Net cash used in investing

activities

Net cash from financing

activities

According to the above figure, it can be stated that the net cash from operating

activities has decreased in 2016 compare to that of 2015, though in 2017, this has increased

significantly due to higher receipts of cash from the customers and finance income. On the

contrary, the net cash used in investing activities has decreased since 2015 because of the

decreasing investment on property, plant and equipment. At the end, net cash from financial

activities has decreased in 2016 while again in 2017 it has increased due to the net proceeds

in this year from insurance of shares. Consequently, the increment can be seen in cash and

cash equivalent for this Virgin Australia in 2017.

Other comprehensive income statement:

(iii)

Based on the annual report of 2017 of this Virgin Australia Group, the chief items that

are listed in the comprehensive income statement are foreign currency translation reserve,

income tax benefit or expense and cash flow hedge reserve (Papa, Peters, Schacht and Lu

2015).

(Manova, Wei and Zhang 2015). The following diagram has represented comparative

analysis of these three forms in the cash flow statement during 2015, 2016 and 2017.

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Main items of cash flow statement of

Virgin Australia

Net cash from operating

activities

Net cash used in investing

activities

Net cash from financing

activities

According to the above figure, it can be stated that the net cash from operating

activities has decreased in 2016 compare to that of 2015, though in 2017, this has increased

significantly due to higher receipts of cash from the customers and finance income. On the

contrary, the net cash used in investing activities has decreased since 2015 because of the

decreasing investment on property, plant and equipment. At the end, net cash from financial

activities has decreased in 2016 while again in 2017 it has increased due to the net proceeds

in this year from insurance of shares. Consequently, the increment can be seen in cash and

cash equivalent for this Virgin Australia in 2017.

Other comprehensive income statement:

(iii)

Based on the annual report of 2017 of this Virgin Australia Group, the chief items that

are listed in the comprehensive income statement are foreign currency translation reserve,

income tax benefit or expense and cash flow hedge reserve (Papa, Peters, Schacht and Lu

2015).

5CORPORATE ASSIGNMENT

(iv)

According to the concept of accountancy, using foreign currency translation reserve is

formed for exchange of the outcomes related to foreign subsidiaries of the parents firm to the

reporting currency. Income tax expenditure is the amount, which the government has incurred

on profit before deduction of tax of the organisation (Papa, Peters, Schacht and Lu 2015).

Moreover, using of cash flow hedge reserve is formed when the firm tries to decrease the

exposure that occurs due variations of cash flow of a liability or asset.

(v)

` Net income is sometimes considered as other comprehensive income. Hence, Virgin

has used this concept to provide important details regarding the values of above-discussed

items (Jaarat 2017). The chief reason behind mentioning these items under other

comprehensive income statement can be stated by the fact that they have provided

comprehensive overview along with holistic one of the drivers regarding business operations.

For this, they have not revealed in the income statement.

Accounting for corporate income tax:

(vi)

Tax expense is considered as a important obligation related to an organisation because

of the municipal, federal and state governments of the country. For the case of Virgin

Australia, the company has not incurred expense on tax rather it has received income tax

benefit in 2016 and 2017. In this context, it can be mentioned that, in 2017, the company has

received income tax benefit of $103.8 million while in 2016 it has remained $ 201.9 million.

(vii)

Based on the annual report of Virgin Australia in 2017, it can be observed that the

company has incurred some amount of loss before imposition of income tax for both 2016

(iv)

According to the concept of accountancy, using foreign currency translation reserve is

formed for exchange of the outcomes related to foreign subsidiaries of the parents firm to the

reporting currency. Income tax expenditure is the amount, which the government has incurred

on profit before deduction of tax of the organisation (Papa, Peters, Schacht and Lu 2015).

Moreover, using of cash flow hedge reserve is formed when the firm tries to decrease the

exposure that occurs due variations of cash flow of a liability or asset.

(v)

` Net income is sometimes considered as other comprehensive income. Hence, Virgin

has used this concept to provide important details regarding the values of above-discussed

items (Jaarat 2017). The chief reason behind mentioning these items under other

comprehensive income statement can be stated by the fact that they have provided

comprehensive overview along with holistic one of the drivers regarding business operations.

For this, they have not revealed in the income statement.

Accounting for corporate income tax:

(vi)

Tax expense is considered as a important obligation related to an organisation because

of the municipal, federal and state governments of the country. For the case of Virgin

Australia, the company has not incurred expense on tax rather it has received income tax

benefit in 2016 and 2017. In this context, it can be mentioned that, in 2017, the company has

received income tax benefit of $103.8 million while in 2016 it has remained $ 201.9 million.

(vii)

Based on the annual report of Virgin Australia in 2017, it can be observed that the

company has incurred some amount of loss before imposition of income tax for both 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ASSIGNMENT

and 2017. Hence, with the help of this annual report, it can be stated that airline has charged

30% tax rate on its profit before imposition of income tax on net income. However, as the

specified company has incurred loss before imposition on tax, it has become impossible for

this company to account income tax expense (Armstrong et al. 2015). Thus, it is difficult to

determine that whether this expense on tax of this airline company, which requires to be

maintained within the income statement, is measured through using 30% tax rate on profit

before expense of income tax.

(viii)

The concept of deferred tax arises in some situations where the firms bear excess

taxes or pay taxes on financial assets. On the contrary, deferred tax liabilities indicate some

situations where the variations can be recognised in tax carrying amount along with profit of

the corporate entities (Gupta and Lynch 2015). In the context of Virgin Australia, the assets

of deferred tax account to $1017.6 million in 2017 while in 2016 this amount has remained

$434.4 million in 2016. Identification of these deferred tax assets is formed as additional

amount of depreciation is incurred due to differences in taxable depreciation rate along with

depreciation amount. Identification of deferred tax liabilities has occurred from the temporary

profit variations for which it has received tax benefits in 2016 and 2017.

(ix)

Current tax asset or income tax payable is an important concept for each business

organisations of Australia (Sikka 2017). Based on the annual report of Virgin Australia, it can

be stated that the current tax assets make the expected tax receivable or payable income or

loss for the mentioned period. For Virgin, as the entity has received income tax benefit of $

201.9 million and $ 103.8 million in 2016 and 2017 accordingly, the same amounts have been

reported in the reconciliation section of net cash or net loss from operations in its annual

and 2017. Hence, with the help of this annual report, it can be stated that airline has charged

30% tax rate on its profit before imposition of income tax on net income. However, as the

specified company has incurred loss before imposition on tax, it has become impossible for

this company to account income tax expense (Armstrong et al. 2015). Thus, it is difficult to

determine that whether this expense on tax of this airline company, which requires to be

maintained within the income statement, is measured through using 30% tax rate on profit

before expense of income tax.

(viii)

The concept of deferred tax arises in some situations where the firms bear excess

taxes or pay taxes on financial assets. On the contrary, deferred tax liabilities indicate some

situations where the variations can be recognised in tax carrying amount along with profit of

the corporate entities (Gupta and Lynch 2015). In the context of Virgin Australia, the assets

of deferred tax account to $1017.6 million in 2017 while in 2016 this amount has remained

$434.4 million in 2016. Identification of these deferred tax assets is formed as additional

amount of depreciation is incurred due to differences in taxable depreciation rate along with

depreciation amount. Identification of deferred tax liabilities has occurred from the temporary

profit variations for which it has received tax benefits in 2016 and 2017.

(ix)

Current tax asset or income tax payable is an important concept for each business

organisations of Australia (Sikka 2017). Based on the annual report of Virgin Australia, it can

be stated that the current tax assets make the expected tax receivable or payable income or

loss for the mentioned period. For Virgin, as the entity has received income tax benefit of $

201.9 million and $ 103.8 million in 2016 and 2017 accordingly, the same amounts have been

reported in the reconciliation section of net cash or net loss from operations in its annual

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ASSIGNMENT

report. The chief reason behind these two items represent the same values can be stated as no

excess tax expenses are beared on behalf of the organisation for 2016 and 2017.

(x)

With the help of annual report, it can be stated that the organisation has not incurred

any expenses on income tax for 2016 and 2017. Rather, the organisation has earned benefit

on income tax in the mentioned years and this is the chief reason that considers income tax

paid is not considered as an item in the cash flow statement of the entity.

(xi)

Through critically assessing tx treatment of Virgin Australia, it can be seen that the

company has suffered from loss before incurring expense on income tax in 2016 and

2017.Conequently, the company has received income tax benefit. Hence, it has become

difficult to relate actual tax expense that is paid with the country’s prevailing tax rate (Gupta

and Lynch 2015). Moreover, due to absent of income tax expense, the company has not

mentioned any income tax paid regarding the cash flow statement.

report. The chief reason behind these two items represent the same values can be stated as no

excess tax expenses are beared on behalf of the organisation for 2016 and 2017.

(x)

With the help of annual report, it can be stated that the organisation has not incurred

any expenses on income tax for 2016 and 2017. Rather, the organisation has earned benefit

on income tax in the mentioned years and this is the chief reason that considers income tax

paid is not considered as an item in the cash flow statement of the entity.

(xi)

Through critically assessing tx treatment of Virgin Australia, it can be seen that the

company has suffered from loss before incurring expense on income tax in 2016 and

2017.Conequently, the company has received income tax benefit. Hence, it has become

difficult to relate actual tax expense that is paid with the country’s prevailing tax rate (Gupta

and Lynch 2015). Moreover, due to absent of income tax expense, the company has not

mentioned any income tax paid regarding the cash flow statement.

8CORPORATE ASSIGNMENT

References:

Armstrong, C.S., Blouin, J.L., Jagolinzer, A.D. and Larcker, D.F., 2015. Corporate

governance, incentives, and tax avoidance. Journal of Accounting and Economics, 60(1),

pp.1-17.

Gupta, S. and Lynch, D.P., 2015. The effects of changes in state tax enforcement on

corporate income tax collections. The Journal of the American Taxation Association, 38(1),

pp.125-143.

Hui, K.W., Nelson, K.K. and Yeung, P.E., 2016. On the persistence and pricing of industry-

wide and firm-specific earnings, cash flows, and accruals. Journal of Accounting and

Economics, 61(1), pp.185-202.

Jaarat, K.J., 2017. The Impact of Other Comprehensive Income (OCI) on Financial

Performance. Journal of Business Studies Quarterly, 8(4), p.109.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal of

Financial and Quantitative Analysis, 51(4), pp.1135-1164.

Manova, K., Wei, S.J. and Zhang, Z., 2015. Firm exports and multinational activity under

credit constraints. Review of Economics and Statistics, 97(3), pp.574-588.

Papa, V.T., Peters, S.J., Schacht, K.N. and Lu, S., 2015. Analyzing Bank Performance: Role

of Comprehensive Income: The Need to Increase Investor Attention on Other Comprehensive

Income Statement Items. Codes, Standards, and Position Papers, 2015(3), pp.1-91.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review, 48(1), pp.102-116.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

References:

Armstrong, C.S., Blouin, J.L., Jagolinzer, A.D. and Larcker, D.F., 2015. Corporate

governance, incentives, and tax avoidance. Journal of Accounting and Economics, 60(1),

pp.1-17.

Gupta, S. and Lynch, D.P., 2015. The effects of changes in state tax enforcement on

corporate income tax collections. The Journal of the American Taxation Association, 38(1),

pp.125-143.

Hui, K.W., Nelson, K.K. and Yeung, P.E., 2016. On the persistence and pricing of industry-

wide and firm-specific earnings, cash flows, and accruals. Journal of Accounting and

Economics, 61(1), pp.185-202.

Jaarat, K.J., 2017. The Impact of Other Comprehensive Income (OCI) on Financial

Performance. Journal of Business Studies Quarterly, 8(4), p.109.

Lewellen, J. and Lewellen, K., 2016. Investment and cash flow: New evidence. Journal of

Financial and Quantitative Analysis, 51(4), pp.1135-1164.

Manova, K., Wei, S.J. and Zhang, Z., 2015. Firm exports and multinational activity under

credit constraints. Review of Economics and Statistics, 97(3), pp.574-588.

Papa, V.T., Peters, S.J., Schacht, K.N. and Lu, S., 2015. Analyzing Bank Performance: Role

of Comprehensive Income: The Need to Increase Investor Attention on Other Comprehensive

Income Statement Items. Codes, Standards, and Position Papers, 2015(3), pp.1-91.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review, 48(1), pp.102-116.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.