Managerial Accounting Report: Virgin Australia Executive Pay Analysis

VerifiedAdded on 2021/06/18

|19

|4465

|356

Report

AI Summary

This managerial accounting report provides an in-depth analysis of Virgin Australia's remuneration practices. It examines financial and non-financial indicators, goal congruence, and the application of a balanced scorecard to assess executive pay. The report reviews the remuneration committee's details, allocation of executive compensation, and the mix of performance measures used, including STI and LTI. It evaluates the company's performance against executive pay, revealing a concerning trend of increasing executive remuneration despite declining company performance. The analysis also covers the company's adherence to ethical practices. The study concludes with recommendations for improvement based on the evaluation of financial and non-financial indicators, goal congruence, and the balanced scorecard, highlighting areas for potential enhancement in Virgin Australia's remuneration strategies.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of Student:

Name of University:

Author’s Note:

Managerial Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

1.0 Executive Summary

The depictions of the report aim to address the various areas of the study which are seen to be

associated to the financial and the non-financial indicators, goal congruence and use of balanced

scorecard. The company review has been considered with the discussion on the different types of

the important aspects of the raptor which are seen to be related to the details of the remuneration

committee members, allocation of the executive remuneration and the analysis of the

performance measures of the STI and LTI. The section of the study has also evaluated the

performance of the company in terms of the executive pay. This section is seen to be followed by

the summary of the finds. Some of the latter part of the discussions has focused on the analysis

of the remuneration method are considered as per the previously reviewed topic of financial and

non-financial indicators, goal congruence and preparation of a balanced scorecard. The different

finds of the study have been able to suggest that the company discloses the main form of the

remuneration a per the fixed remuneration, LTI and STI. In addition to this, the company has

been seen to be following unethical approach for the remunerating the executives. This has been

seen to be evident with increasing nature of the executive remuneration despite of the decreasing

performance of the company.

1.0 Executive Summary

The depictions of the report aim to address the various areas of the study which are seen to be

associated to the financial and the non-financial indicators, goal congruence and use of balanced

scorecard. The company review has been considered with the discussion on the different types of

the important aspects of the raptor which are seen to be related to the details of the remuneration

committee members, allocation of the executive remuneration and the analysis of the

performance measures of the STI and LTI. The section of the study has also evaluated the

performance of the company in terms of the executive pay. This section is seen to be followed by

the summary of the finds. Some of the latter part of the discussions has focused on the analysis

of the remuneration method are considered as per the previously reviewed topic of financial and

non-financial indicators, goal congruence and preparation of a balanced scorecard. The different

finds of the study have been able to suggest that the company discloses the main form of the

remuneration a per the fixed remuneration, LTI and STI. In addition to this, the company has

been seen to be following unethical approach for the remunerating the executives. This has been

seen to be evident with increasing nature of the executive remuneration despite of the decreasing

performance of the company.

2MANAGERIAL ACCOUNTING

Table of Contents

2. Introduction..................................................................................................................................4

3. Topic and Literature Review.......................................................................................................4

3.1 Financial and Non-Financial Indicator..................................................................................5

3.2 Goal Congruence...................................................................................................................7

3.3 Balanced Score Card..............................................................................................................8

4. Company Review.........................................................................................................................9

4.1 Details of remuneration committee and its membership:..........................................................9

4.2 Allocation of executive remuneration:................................................................................10

4.3 Mix of performance measures used:....................................................................................11

4.4 Company performance versus executive pay:.....................................................................12

6.0 Analysis of the remuneration Methods....................................................................................13

6.1 Financial and Non-Financial Indicator................................................................................13

6.2 Goal Congruence.................................................................................................................16

6.3 Balanced Score Card............................................................................................................16

7.0 Recommendation.....................................................................................................................16

8.0 Conclusion...............................................................................................................................17

9.0 Reference List..........................................................................................................................18

Table of Contents

2. Introduction..................................................................................................................................4

3. Topic and Literature Review.......................................................................................................4

3.1 Financial and Non-Financial Indicator..................................................................................5

3.2 Goal Congruence...................................................................................................................7

3.3 Balanced Score Card..............................................................................................................8

4. Company Review.........................................................................................................................9

4.1 Details of remuneration committee and its membership:..........................................................9

4.2 Allocation of executive remuneration:................................................................................10

4.3 Mix of performance measures used:....................................................................................11

4.4 Company performance versus executive pay:.....................................................................12

6.0 Analysis of the remuneration Methods....................................................................................13

6.1 Financial and Non-Financial Indicator................................................................................13

6.2 Goal Congruence.................................................................................................................16

6.3 Balanced Score Card............................................................................................................16

7.0 Recommendation.....................................................................................................................16

8.0 Conclusion...............................................................................................................................17

9.0 Reference List..........................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

2. Introduction

The term remuneration is identified as the payment received for the services or the

compensation for the employment. These are seen to be based on the different types of the

present market indicators which are seen to be associated to the present market standings. The

primary objective of the study has been considered with developing the literature review for

addressing the main elements of the research topics related to the remuneration report of Virgin

Australia. The main discourse of the literature of the study has been able to depict the various

areas of the study which are seen to be associated to the financial and the non-financial

indicators, goal congruence and use of balanced scorecard. The company review has been

considered with the discussion on the different types of the important aspects of the raptor which

are seen to be related to the details of the remuneration committee members, allocation of the

executive remuneration and the analysis of the performance measures of the STI and LTI. The

section of the study has also evaluated the performance of the company in terms of the executive

pay. This section is seen to be followed by the summary of the finds. Some of the latter part of

the discussions has focused on the analysis of the remuneration method are considered as per the

previously reviewed topic of financial and non-financial indicators, goal congruence and

preparation of a balanced scorecard. The final part of the discussions has suggested the

improvement which can be made by the company based on the evaluation in the various topics

(Bussin and Lee 2016).

3. Topic and Literature Review

This section of the study has been considered with the various types of the evaluations

which has been taken into account with the number of the factors determining the financial and

non-financial measures as per the annual report of the company. It needs to be discerned that the

various type the depictions of the information on the financial interpretations has been revealed

with the declaration on the “Market price per share, Earnings per shares, Net Income/Loss,

Shareholder's Equity and Net Operating Expenditure”. The declaration of these financial

information has bee used to depict the “Price Earnings ratio, return on equity and return on

2. Introduction

The term remuneration is identified as the payment received for the services or the

compensation for the employment. These are seen to be based on the different types of the

present market indicators which are seen to be associated to the present market standings. The

primary objective of the study has been considered with developing the literature review for

addressing the main elements of the research topics related to the remuneration report of Virgin

Australia. The main discourse of the literature of the study has been able to depict the various

areas of the study which are seen to be associated to the financial and the non-financial

indicators, goal congruence and use of balanced scorecard. The company review has been

considered with the discussion on the different types of the important aspects of the raptor which

are seen to be related to the details of the remuneration committee members, allocation of the

executive remuneration and the analysis of the performance measures of the STI and LTI. The

section of the study has also evaluated the performance of the company in terms of the executive

pay. This section is seen to be followed by the summary of the finds. Some of the latter part of

the discussions has focused on the analysis of the remuneration method are considered as per the

previously reviewed topic of financial and non-financial indicators, goal congruence and

preparation of a balanced scorecard. The final part of the discussions has suggested the

improvement which can be made by the company based on the evaluation in the various topics

(Bussin and Lee 2016).

3. Topic and Literature Review

This section of the study has been considered with the various types of the evaluations

which has been taken into account with the number of the factors determining the financial and

non-financial measures as per the annual report of the company. It needs to be discerned that the

various type the depictions of the information on the financial interpretations has been revealed

with the declaration on the “Market price per share, Earnings per shares, Net Income/Loss,

Shareholder's Equity and Net Operating Expenditure”. The declaration of these financial

information has bee used to depict the “Price Earnings ratio, return on equity and return on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

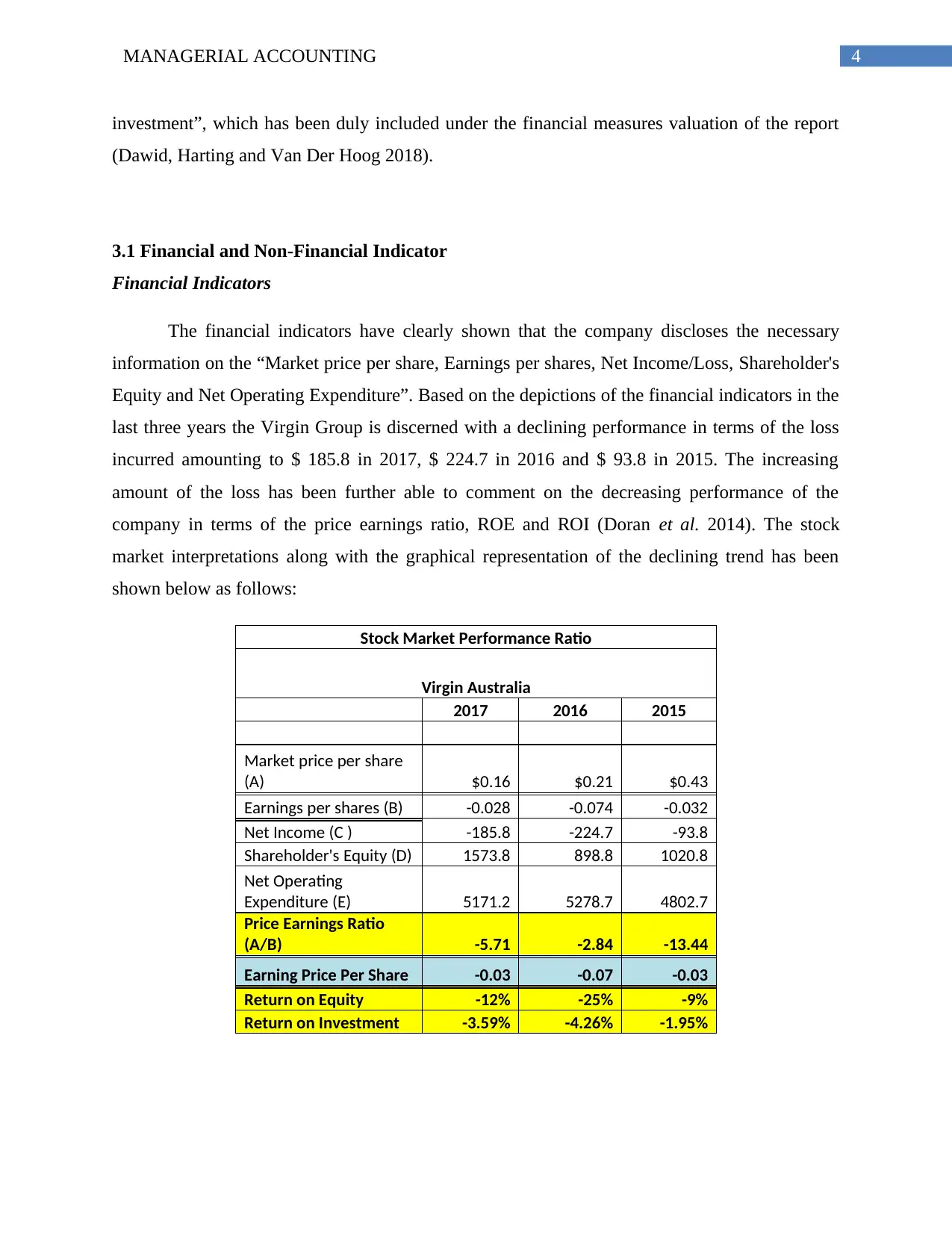

investment”, which has been duly included under the financial measures valuation of the report

(Dawid, Harting and Van Der Hoog 2018).

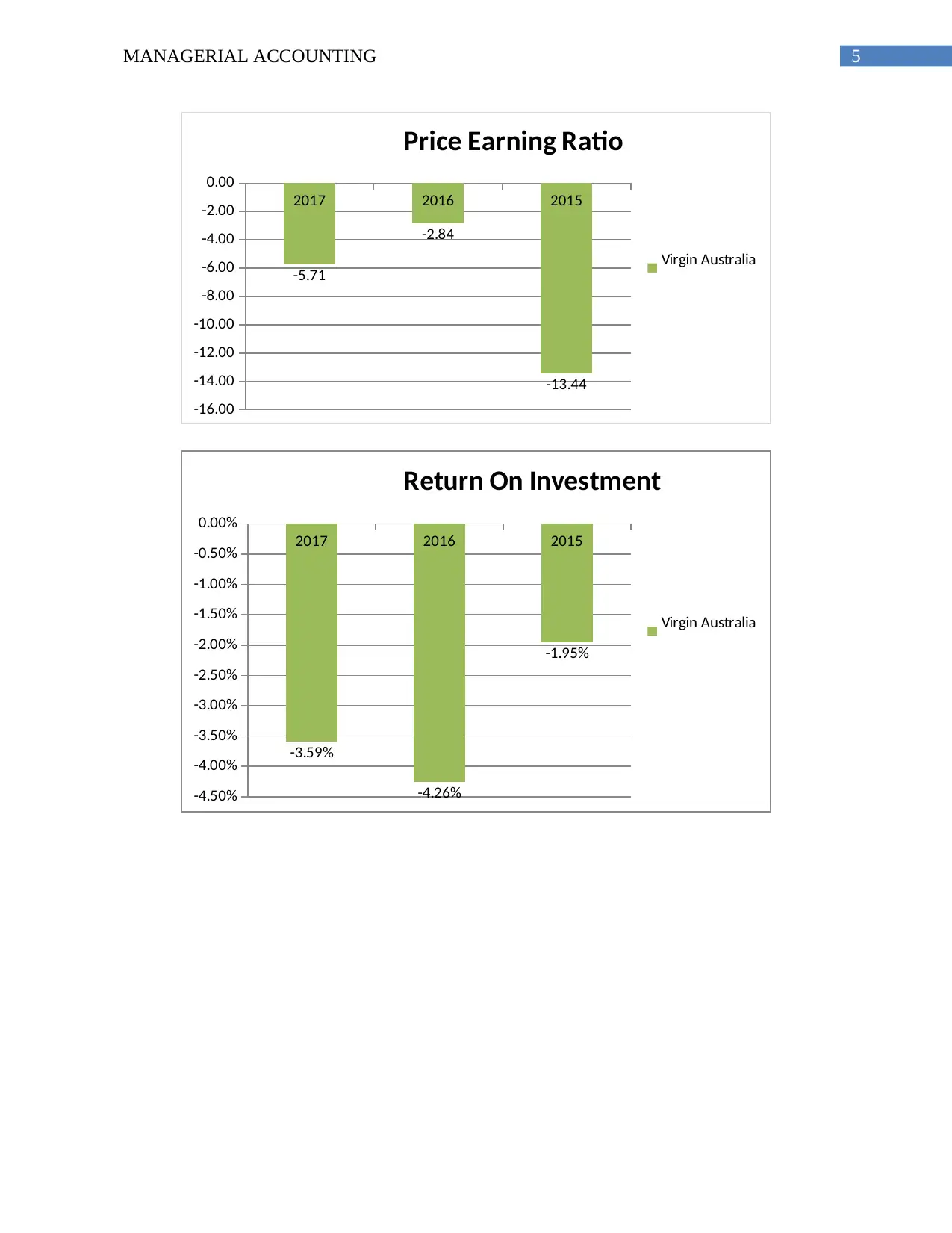

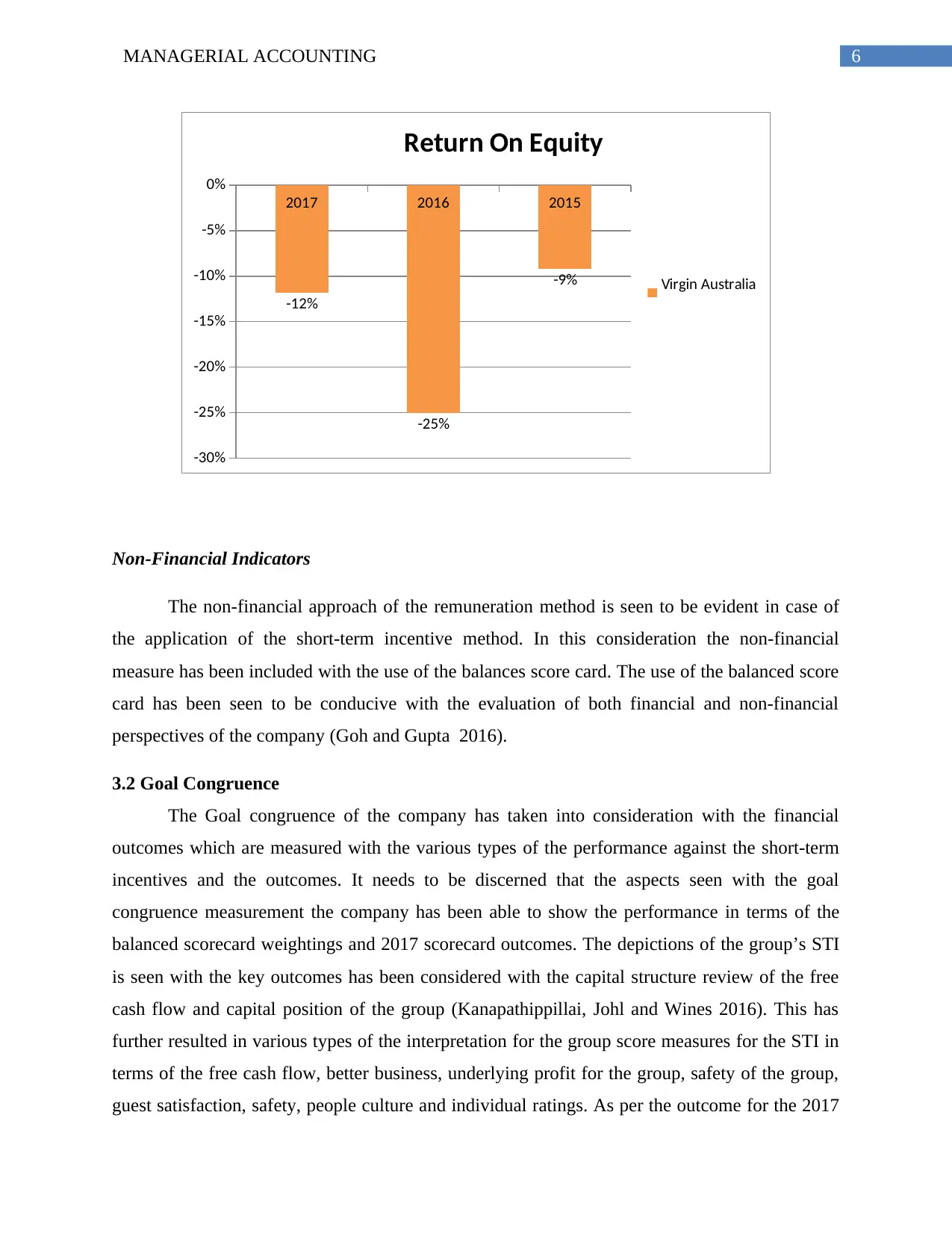

3.1 Financial and Non-Financial Indicator

Financial Indicators

The financial indicators have clearly shown that the company discloses the necessary

information on the “Market price per share, Earnings per shares, Net Income/Loss, Shareholder's

Equity and Net Operating Expenditure”. Based on the depictions of the financial indicators in the

last three years the Virgin Group is discerned with a declining performance in terms of the loss

incurred amounting to $ 185.8 in 2017, $ 224.7 in 2016 and $ 93.8 in 2015. The increasing

amount of the loss has been further able to comment on the decreasing performance of the

company in terms of the price earnings ratio, ROE and ROI (Doran et al. 2014). The stock

market interpretations along with the graphical representation of the declining trend has been

shown below as follows:

Stock Market Performance Ratio

Virgin Australia

2017 2016 2015

Market price per share

(A) $0.16 $0.21 $0.43

Earnings per shares (B) -0.028 -0.074 -0.032

Net Income (C ) -185.8 -224.7 -93.8

Shareholder's Equity (D) 1573.8 898.8 1020.8

Net Operating

Expenditure (E) 5171.2 5278.7 4802.7

Price Earnings Ratio

(A/B) -5.71 -2.84 -13.44

Earning Price Per Share -0.03 -0.07 -0.03

Return on Equity -12% -25% -9%

Return on Investment -3.59% -4.26% -1.95%

investment”, which has been duly included under the financial measures valuation of the report

(Dawid, Harting and Van Der Hoog 2018).

3.1 Financial and Non-Financial Indicator

Financial Indicators

The financial indicators have clearly shown that the company discloses the necessary

information on the “Market price per share, Earnings per shares, Net Income/Loss, Shareholder's

Equity and Net Operating Expenditure”. Based on the depictions of the financial indicators in the

last three years the Virgin Group is discerned with a declining performance in terms of the loss

incurred amounting to $ 185.8 in 2017, $ 224.7 in 2016 and $ 93.8 in 2015. The increasing

amount of the loss has been further able to comment on the decreasing performance of the

company in terms of the price earnings ratio, ROE and ROI (Doran et al. 2014). The stock

market interpretations along with the graphical representation of the declining trend has been

shown below as follows:

Stock Market Performance Ratio

Virgin Australia

2017 2016 2015

Market price per share

(A) $0.16 $0.21 $0.43

Earnings per shares (B) -0.028 -0.074 -0.032

Net Income (C ) -185.8 -224.7 -93.8

Shareholder's Equity (D) 1573.8 898.8 1020.8

Net Operating

Expenditure (E) 5171.2 5278.7 4802.7

Price Earnings Ratio

(A/B) -5.71 -2.84 -13.44

Earning Price Per Share -0.03 -0.07 -0.03

Return on Equity -12% -25% -9%

Return on Investment -3.59% -4.26% -1.95%

5MANAGERIAL ACCOUNTING

2017 2016 2015

-16.00

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

-5.71

-2.84

-13.44

Price Earning Ratio

Virgin Australia

2017 2016 2015

-4.50%

-4.00%

-3.50%

-3.00%

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

-3.59%

-4.26%

-1.95%

Return On Investment

Virgin Australia

2017 2016 2015

-16.00

-14.00

-12.00

-10.00

-8.00

-6.00

-4.00

-2.00

0.00

-5.71

-2.84

-13.44

Price Earning Ratio

Virgin Australia

2017 2016 2015

-4.50%

-4.00%

-3.50%

-3.00%

-2.50%

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

-3.59%

-4.26%

-1.95%

Return On Investment

Virgin Australia

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

2017 2016 2015

-30%

-25%

-20%

-15%

-10%

-5%

0%

-12%

-25%

-9%

Return On Equity

Virgin Australia

Non-Financial Indicators

The non-financial approach of the remuneration method is seen to be evident in case of

the application of the short-term incentive method. In this consideration the non-financial

measure has been included with the use of the balances score card. The use of the balanced score

card has been seen to be conducive with the evaluation of both financial and non-financial

perspectives of the company (Goh and Gupta 2016).

3.2 Goal Congruence

The Goal congruence of the company has taken into consideration with the financial

outcomes which are measured with the various types of the performance against the short-term

incentives and the outcomes. It needs to be discerned that the aspects seen with the goal

congruence measurement the company has been able to show the performance in terms of the

balanced scorecard weightings and 2017 scorecard outcomes. The depictions of the group’s STI

is seen with the key outcomes has been considered with the capital structure review of the free

cash flow and capital position of the group (Kanapathippillai, Johl and Wines 2016). This has

further resulted in various types of the interpretation for the group score measures for the STI in

terms of the free cash flow, better business, underlying profit for the group, safety of the group,

guest satisfaction, safety, people culture and individual ratings. As per the outcome for the 2017

2017 2016 2015

-30%

-25%

-20%

-15%

-10%

-5%

0%

-12%

-25%

-9%

Return On Equity

Virgin Australia

Non-Financial Indicators

The non-financial approach of the remuneration method is seen to be evident in case of

the application of the short-term incentive method. In this consideration the non-financial

measure has been included with the use of the balances score card. The use of the balanced score

card has been seen to be conducive with the evaluation of both financial and non-financial

perspectives of the company (Goh and Gupta 2016).

3.2 Goal Congruence

The Goal congruence of the company has taken into consideration with the financial

outcomes which are measured with the various types of the performance against the short-term

incentives and the outcomes. It needs to be discerned that the aspects seen with the goal

congruence measurement the company has been able to show the performance in terms of the

balanced scorecard weightings and 2017 scorecard outcomes. The depictions of the group’s STI

is seen with the key outcomes has been considered with the capital structure review of the free

cash flow and capital position of the group (Kanapathippillai, Johl and Wines 2016). This has

further resulted in various types of the interpretation for the group score measures for the STI in

terms of the free cash flow, better business, underlying profit for the group, safety of the group,

guest satisfaction, safety, people culture and individual ratings. As per the outcome for the 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

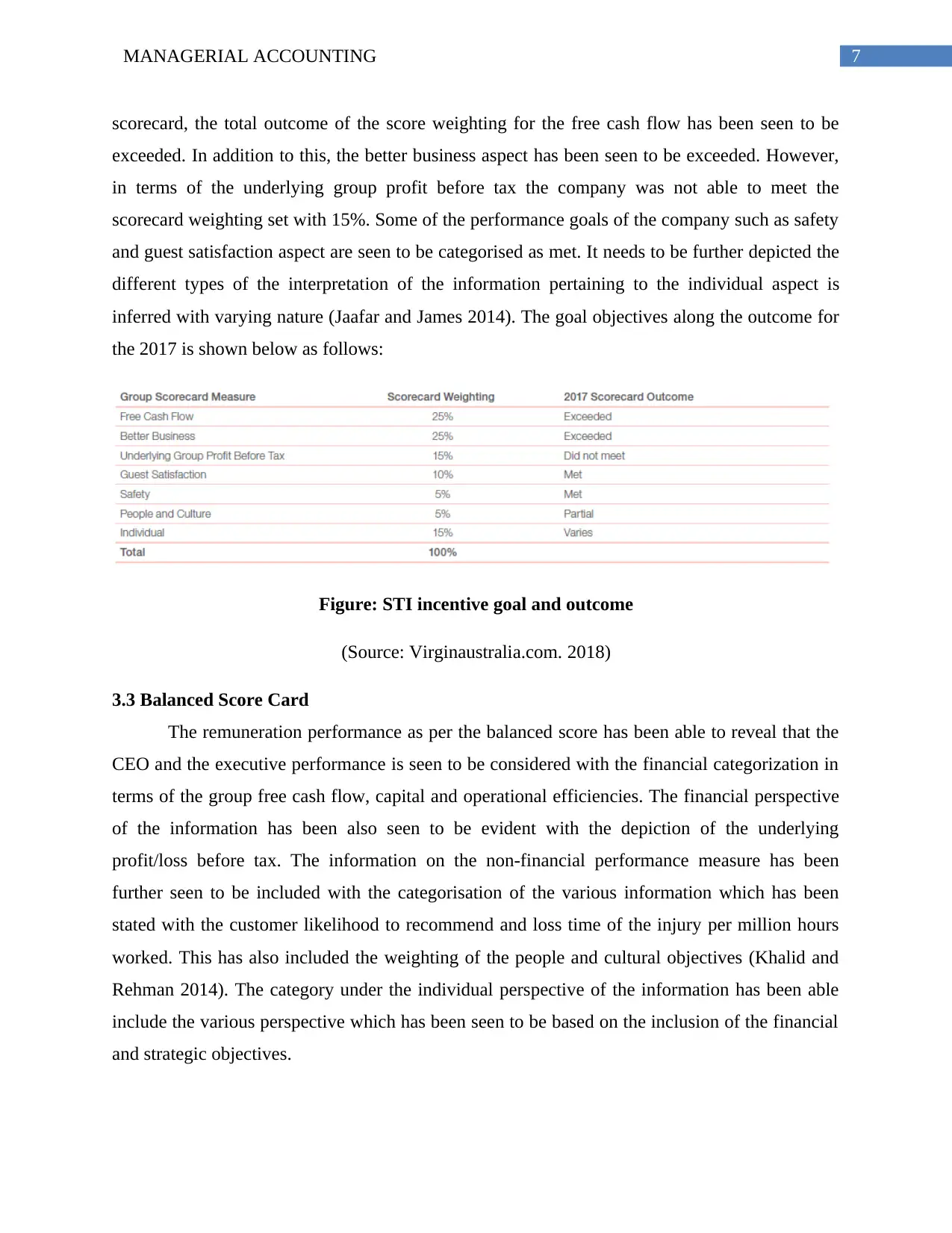

scorecard, the total outcome of the score weighting for the free cash flow has been seen to be

exceeded. In addition to this, the better business aspect has been seen to be exceeded. However,

in terms of the underlying group profit before tax the company was not able to meet the

scorecard weighting set with 15%. Some of the performance goals of the company such as safety

and guest satisfaction aspect are seen to be categorised as met. It needs to be further depicted the

different types of the interpretation of the information pertaining to the individual aspect is

inferred with varying nature (Jaafar and James 2014). The goal objectives along the outcome for

the 2017 is shown below as follows:

Figure: STI incentive goal and outcome

(Source: Virginaustralia.com. 2018)

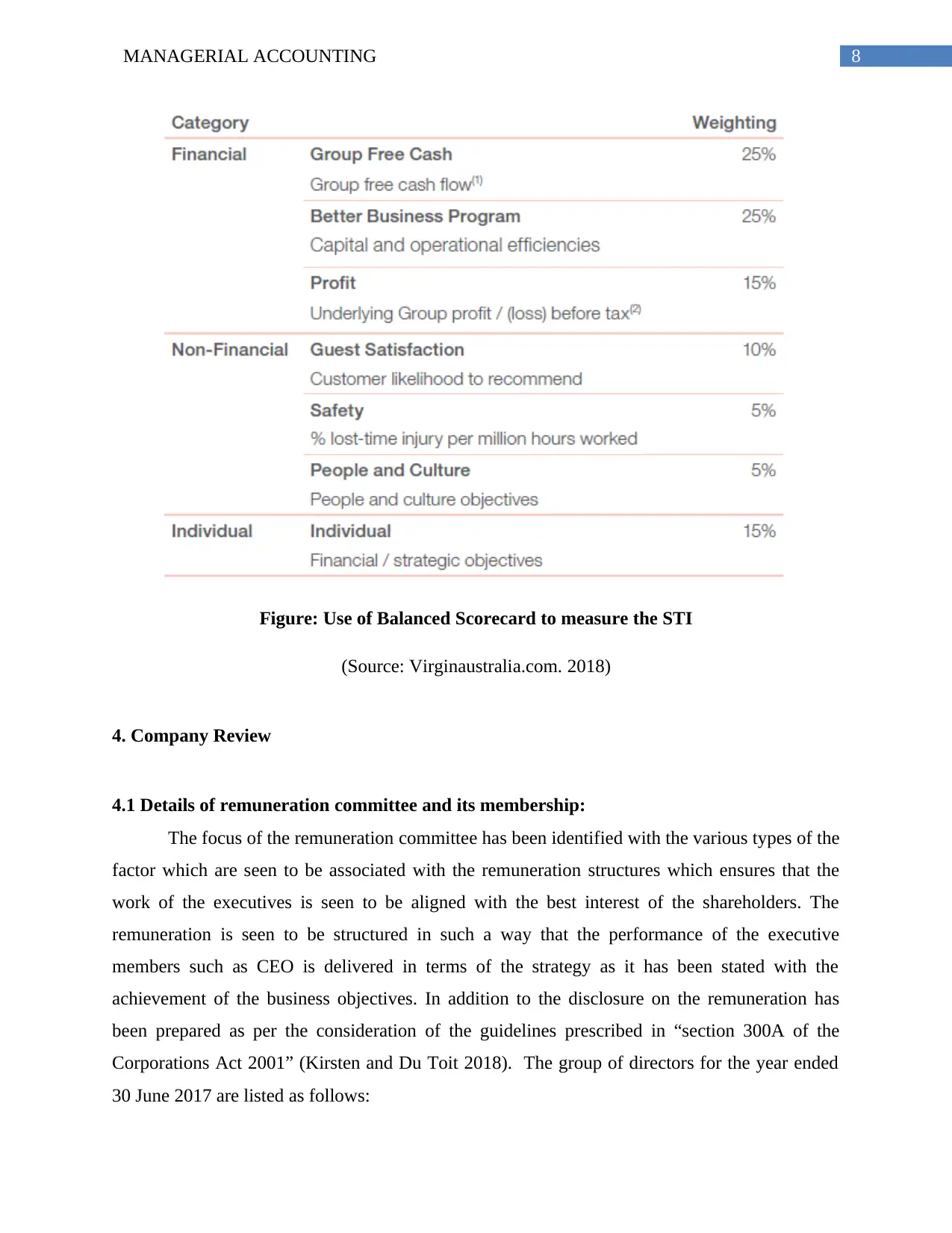

3.3 Balanced Score Card

The remuneration performance as per the balanced score has been able to reveal that the

CEO and the executive performance is seen to be considered with the financial categorization in

terms of the group free cash flow, capital and operational efficiencies. The financial perspective

of the information has been also seen to be evident with the depiction of the underlying

profit/loss before tax. The information on the non-financial performance measure has been

further seen to be included with the categorisation of the various information which has been

stated with the customer likelihood to recommend and loss time of the injury per million hours

worked. This has also included the weighting of the people and cultural objectives (Khalid and

Rehman 2014). The category under the individual perspective of the information has been able

include the various perspective which has been seen to be based on the inclusion of the financial

and strategic objectives.

scorecard, the total outcome of the score weighting for the free cash flow has been seen to be

exceeded. In addition to this, the better business aspect has been seen to be exceeded. However,

in terms of the underlying group profit before tax the company was not able to meet the

scorecard weighting set with 15%. Some of the performance goals of the company such as safety

and guest satisfaction aspect are seen to be categorised as met. It needs to be further depicted the

different types of the interpretation of the information pertaining to the individual aspect is

inferred with varying nature (Jaafar and James 2014). The goal objectives along the outcome for

the 2017 is shown below as follows:

Figure: STI incentive goal and outcome

(Source: Virginaustralia.com. 2018)

3.3 Balanced Score Card

The remuneration performance as per the balanced score has been able to reveal that the

CEO and the executive performance is seen to be considered with the financial categorization in

terms of the group free cash flow, capital and operational efficiencies. The financial perspective

of the information has been also seen to be evident with the depiction of the underlying

profit/loss before tax. The information on the non-financial performance measure has been

further seen to be included with the categorisation of the various information which has been

stated with the customer likelihood to recommend and loss time of the injury per million hours

worked. This has also included the weighting of the people and cultural objectives (Khalid and

Rehman 2014). The category under the individual perspective of the information has been able

include the various perspective which has been seen to be based on the inclusion of the financial

and strategic objectives.

8MANAGERIAL ACCOUNTING

Figure: Use of Balanced Scorecard to measure the STI

(Source: Virginaustralia.com. 2018)

4. Company Review

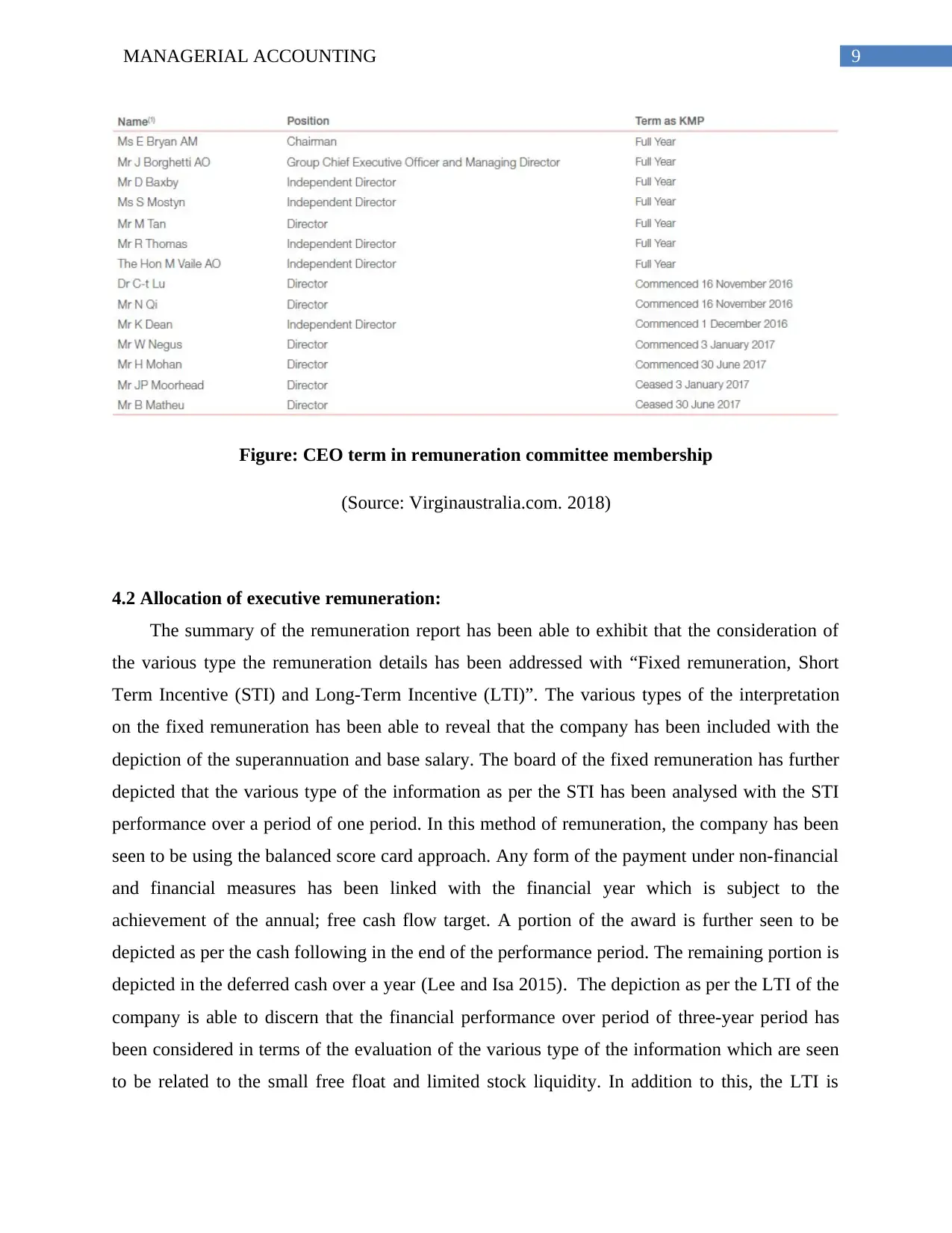

4.1 Details of remuneration committee and its membership:

The focus of the remuneration committee has been identified with the various types of the

factor which are seen to be associated with the remuneration structures which ensures that the

work of the executives is seen to be aligned with the best interest of the shareholders. The

remuneration is seen to be structured in such a way that the performance of the executive

members such as CEO is delivered in terms of the strategy as it has been stated with the

achievement of the business objectives. In addition to the disclosure on the remuneration has

been prepared as per the consideration of the guidelines prescribed in “section 300A of the

Corporations Act 2001” (Kirsten and Du Toit 2018). The group of directors for the year ended

30 June 2017 are listed as follows:

Figure: Use of Balanced Scorecard to measure the STI

(Source: Virginaustralia.com. 2018)

4. Company Review

4.1 Details of remuneration committee and its membership:

The focus of the remuneration committee has been identified with the various types of the

factor which are seen to be associated with the remuneration structures which ensures that the

work of the executives is seen to be aligned with the best interest of the shareholders. The

remuneration is seen to be structured in such a way that the performance of the executive

members such as CEO is delivered in terms of the strategy as it has been stated with the

achievement of the business objectives. In addition to the disclosure on the remuneration has

been prepared as per the consideration of the guidelines prescribed in “section 300A of the

Corporations Act 2001” (Kirsten and Du Toit 2018). The group of directors for the year ended

30 June 2017 are listed as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

Figure: CEO term in remuneration committee membership

(Source: Virginaustralia.com. 2018)

4.2 Allocation of executive remuneration:

The summary of the remuneration report has been able to exhibit that the consideration of

the various type the remuneration details has been addressed with “Fixed remuneration, Short

Term Incentive (STI) and Long-Term Incentive (LTI)”. The various types of the interpretation

on the fixed remuneration has been able to reveal that the company has been included with the

depiction of the superannuation and base salary. The board of the fixed remuneration has further

depicted that the various type of the information as per the STI has been analysed with the STI

performance over a period of one period. In this method of remuneration, the company has been

seen to be using the balanced score card approach. Any form of the payment under non-financial

and financial measures has been linked with the financial year which is subject to the

achievement of the annual; free cash flow target. A portion of the award is further seen to be

depicted as per the cash following in the end of the performance period. The remaining portion is

depicted in the deferred cash over a year (Lee and Isa 2015). The depiction as per the LTI of the

company is able to discern that the financial performance over period of three-year period has

been considered in terms of the evaluation of the various type of the information which are seen

to be related to the small free float and limited stock liquidity. In addition to this, the LTI is

Figure: CEO term in remuneration committee membership

(Source: Virginaustralia.com. 2018)

4.2 Allocation of executive remuneration:

The summary of the remuneration report has been able to exhibit that the consideration of

the various type the remuneration details has been addressed with “Fixed remuneration, Short

Term Incentive (STI) and Long-Term Incentive (LTI)”. The various types of the interpretation

on the fixed remuneration has been able to reveal that the company has been included with the

depiction of the superannuation and base salary. The board of the fixed remuneration has further

depicted that the various type of the information as per the STI has been analysed with the STI

performance over a period of one period. In this method of remuneration, the company has been

seen to be using the balanced score card approach. Any form of the payment under non-financial

and financial measures has been linked with the financial year which is subject to the

achievement of the annual; free cash flow target. A portion of the award is further seen to be

depicted as per the cash following in the end of the performance period. The remaining portion is

depicted in the deferred cash over a year (Lee and Isa 2015). The depiction as per the LTI of the

company is able to discern that the financial performance over period of three-year period has

been considered in terms of the evaluation of the various type of the information which are seen

to be related to the small free float and limited stock liquidity. In addition to this, the LTI is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

considered as the cash-based plan upon the significant delivery of financial performance such as

ROIC.

4.3 Mix of performance measures used:

The three important performance measures for the executive remuneration of the

company have been seen to be depicted with the valuation of the fixed remuneration, short term

incentives, long-term incentives and non-executive directors remunerating.

Fixed Remuneration

The fixed remuneration is seen to comprise of the base salary and the superannuation. The takes

the initiative to set the fixed remuneration to ensure the CEO and executives who are fairly

remunerated in terms of the ASX listed companies.

Short Term Incentive (STI)

The different types of the depiction of the short-term incentives of eh company has been

depicted with the various type of measure of linking the STI performance over a period of one

year. The balanced score card interpretation related to the measurement of the incentives as per

the one-year period are depicted with the adoption of the financial and non-financial measures

such as balanced scorecard. Henceforth, any payment under the STI in 2017 financial year is

subject to the achieving of free cash flow target. A portion of the award of the STI is allocated to

the ward which paid in cash following at the end of the performance period (Leong et al. 2015).

Long Term Incentive (LTI)

The LTI of the company has been depicted to be linked with the financial performance

over period of three months. The LTI structure of the company takes into consideration the

nature of the capital structure of the group which is linked with the free float and limited to the

stock liquidity. The LTI issues by the company is further considered to be paid on the delivery of

the significant improvement which is seen to be depicted in terms of the invested capital. The

ROIC is seen to be selected with the various types of the factors which has been seen to be based

on the different types of the discourse which has been seen to be considered as per the

sustainability and profitability of the airline. These are further considered with the several

financial metrices such as invested capital and earnings (Lepper and Greene 2015).

considered as the cash-based plan upon the significant delivery of financial performance such as

ROIC.

4.3 Mix of performance measures used:

The three important performance measures for the executive remuneration of the

company have been seen to be depicted with the valuation of the fixed remuneration, short term

incentives, long-term incentives and non-executive directors remunerating.

Fixed Remuneration

The fixed remuneration is seen to comprise of the base salary and the superannuation. The takes

the initiative to set the fixed remuneration to ensure the CEO and executives who are fairly

remunerated in terms of the ASX listed companies.

Short Term Incentive (STI)

The different types of the depiction of the short-term incentives of eh company has been

depicted with the various type of measure of linking the STI performance over a period of one

year. The balanced score card interpretation related to the measurement of the incentives as per

the one-year period are depicted with the adoption of the financial and non-financial measures

such as balanced scorecard. Henceforth, any payment under the STI in 2017 financial year is

subject to the achieving of free cash flow target. A portion of the award of the STI is allocated to

the ward which paid in cash following at the end of the performance period (Leong et al. 2015).

Long Term Incentive (LTI)

The LTI of the company has been depicted to be linked with the financial performance

over period of three months. The LTI structure of the company takes into consideration the

nature of the capital structure of the group which is linked with the free float and limited to the

stock liquidity. The LTI issues by the company is further considered to be paid on the delivery of

the significant improvement which is seen to be depicted in terms of the invested capital. The

ROIC is seen to be selected with the various types of the factors which has been seen to be based

on the different types of the discourse which has been seen to be considered as per the

sustainability and profitability of the airline. These are further considered with the several

financial metrices such as invested capital and earnings (Lepper and Greene 2015).

11MANAGERIAL ACCOUNTING

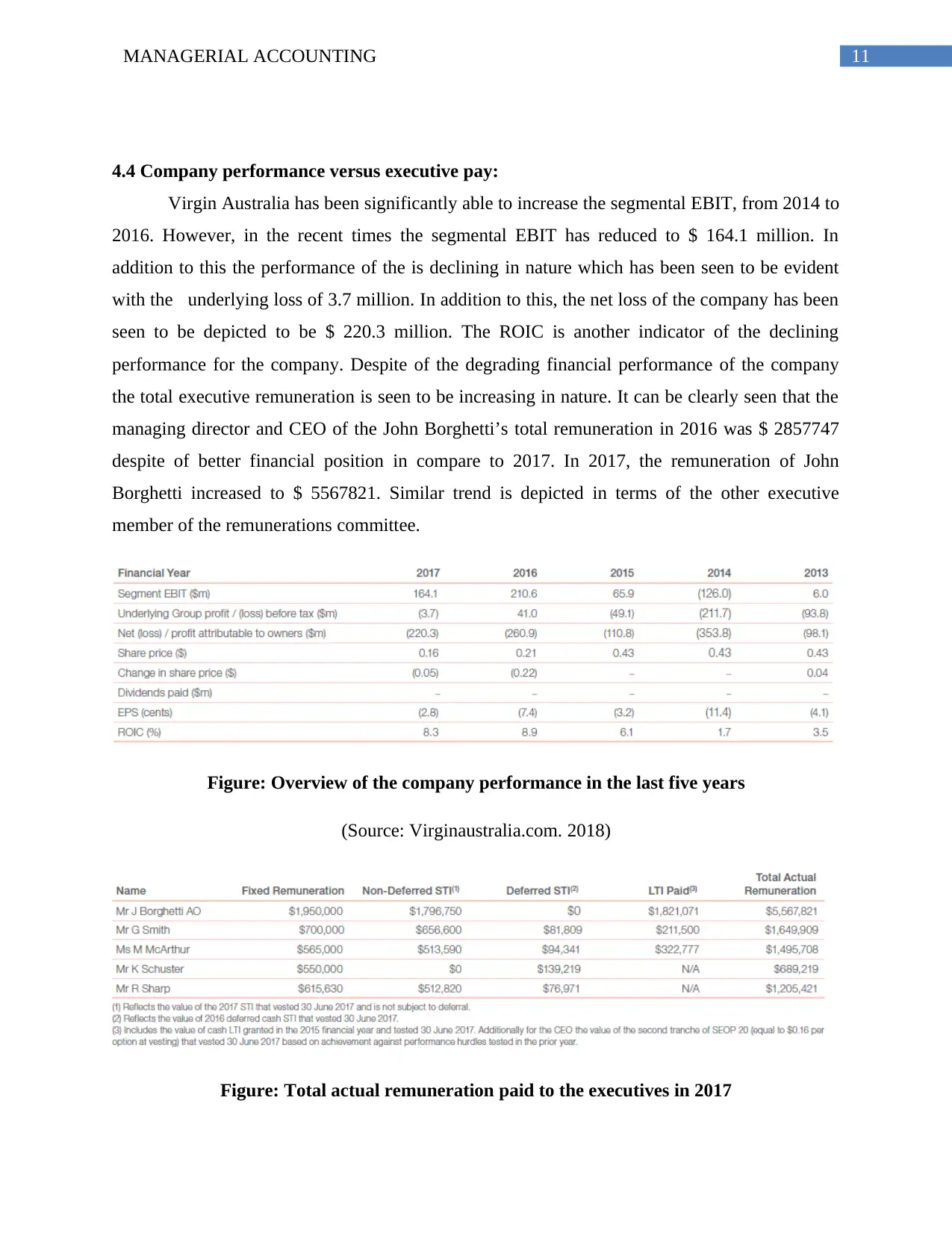

4.4 Company performance versus executive pay:

Virgin Australia has been significantly able to increase the segmental EBIT, from 2014 to

2016. However, in the recent times the segmental EBIT has reduced to $ 164.1 million. In

addition to this the performance of the is declining in nature which has been seen to be evident

with the underlying loss of 3.7 million. In addition to this, the net loss of the company has been

seen to be depicted to be $ 220.3 million. The ROIC is another indicator of the declining

performance for the company. Despite of the degrading financial performance of the company

the total executive remuneration is seen to be increasing in nature. It can be clearly seen that the

managing director and CEO of the John Borghetti’s total remuneration in 2016 was $ 2857747

despite of better financial position in compare to 2017. In 2017, the remuneration of John

Borghetti increased to $ 5567821. Similar trend is depicted in terms of the other executive

member of the remunerations committee.

Figure: Overview of the company performance in the last five years

(Source: Virginaustralia.com. 2018)

Figure: Total actual remuneration paid to the executives in 2017

4.4 Company performance versus executive pay:

Virgin Australia has been significantly able to increase the segmental EBIT, from 2014 to

2016. However, in the recent times the segmental EBIT has reduced to $ 164.1 million. In

addition to this the performance of the is declining in nature which has been seen to be evident

with the underlying loss of 3.7 million. In addition to this, the net loss of the company has been

seen to be depicted to be $ 220.3 million. The ROIC is another indicator of the declining

performance for the company. Despite of the degrading financial performance of the company

the total executive remuneration is seen to be increasing in nature. It can be clearly seen that the

managing director and CEO of the John Borghetti’s total remuneration in 2016 was $ 2857747

despite of better financial position in compare to 2017. In 2017, the remuneration of John

Borghetti increased to $ 5567821. Similar trend is depicted in terms of the other executive

member of the remunerations committee.

Figure: Overview of the company performance in the last five years

(Source: Virginaustralia.com. 2018)

Figure: Total actual remuneration paid to the executives in 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.