MBA901 T3 2018: Financial Analysis of Virgin Australia and SME

VerifiedAdded on 2023/06/04

|18

|4943

|331

Report

AI Summary

This report provides a comprehensive financial analysis of two companies: Virgin Australia Holdings Ltd (VAH), a listed airline company, and SME Prosperous Pty Ltd, an unlisted small to medium enterprise. The report begins with an executive summary outlining the objectives and methodology, which involves in-depth study and analysis using various sources, including the ASX and company websites. Part A focuses on VAH, presenting a detailed financial comparison using comparative income statements and balance sheets over four years (2015-2018). It includes an analysis of revenue, operating expenditure, finance costs, and losses, along with a trend analysis. The report also provides ratio analysis, assessing liquidity, debt management, and asset management. Part B presents a financial summary of SME Prosperous Pty Ltd, offering a similar level of financial analysis. The report concludes with a summary of the accounting position and key findings for both companies, drawing conclusions based on the financial data and ratio analysis. The assignment also references the provided assignment brief which outlines the task and the required scope of work.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

A professional management report has been prepared on the two companies with the objective

of financial analysis and which will serve as the basis for taking investment decisions and other

decisions by stakeholders. For the purpose of the report, in-depth study and analysis of the two

companies has been done using ASX website and the respective company websites as well. The

historic records, primary, secondary and tertiary sources of information has also been used to

prepare the report. The first case study deals with one of the listed Australian companies

named Virgin Australia Holdings Ltd. The financial analysis with respect to all the financial

statements, the trend analysis and the ratio analysis has been done for past years. The

explanatory notes given by the auditor in the Auditor’s report has also been shown. Finally, the

conclusion and recommendation has been given as to what the company might face in the near

future. Part B of the Assignment also deals with the financial summary of one of the small

unlisted companies SME Prosperous Pty Ltd for which too the financial analysis has been done.-

2 | P a g e

Executive Summary

A professional management report has been prepared on the two companies with the objective

of financial analysis and which will serve as the basis for taking investment decisions and other

decisions by stakeholders. For the purpose of the report, in-depth study and analysis of the two

companies has been done using ASX website and the respective company websites as well. The

historic records, primary, secondary and tertiary sources of information has also been used to

prepare the report. The first case study deals with one of the listed Australian companies

named Virgin Australia Holdings Ltd. The financial analysis with respect to all the financial

statements, the trend analysis and the ratio analysis has been done for past years. The

explanatory notes given by the auditor in the Auditor’s report has also been shown. Finally, the

conclusion and recommendation has been given as to what the company might face in the near

future. Part B of the Assignment also deals with the financial summary of one of the small

unlisted companies SME Prosperous Pty Ltd for which too the financial analysis has been done.-

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Part A – Virgin Australia Holdings Ltd (VAH)................................................................................................4

Introduction.............................................................................................................................................4

Financial Comparison for the entity - Internal.........................................................................................4

Purpose of financial audit and audit comments....................................................................................12

Conclusion and Accounting Position of company..................................................................................13

Part B - Prosperous Pty Ltd........................................................................................................................13

Introduction...........................................................................................................................................13

Financial Analysis...................................................................................................................................13

Conclusion and Accounting Position of company..................................................................................16

References.................................................................................................................................................17

3 | P a g e

Contents

Part A – Virgin Australia Holdings Ltd (VAH)................................................................................................4

Introduction.............................................................................................................................................4

Financial Comparison for the entity - Internal.........................................................................................4

Purpose of financial audit and audit comments....................................................................................12

Conclusion and Accounting Position of company..................................................................................13

Part B - Prosperous Pty Ltd........................................................................................................................13

Introduction...........................................................................................................................................13

Financial Analysis...................................................................................................................................13

Conclusion and Accounting Position of company..................................................................................16

References.................................................................................................................................................17

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Part A – Virgin Australia Holdings Ltd (VAH)

Introduction

In this section of the report, the financial analysis of one of the companies Virgin Australia

Holdings Ltd has been done. It is listed on the Australian Stock Exchange and represented as

VAH. It is an airline company and operates in Australian as Virgin Australia, Virgin Australia

Regional Airlines, Virgin Australia International Airlines and Tigerair Australia. It was previously

being operated by Pacific Blue Airlines and was absorbed into Virgin Group in the year 2011

(Bromwich & Scapens, 2016). The company’s headquarters are based out of Brisbane and

employs nearly 10000 people. It is one of the largest Airline services company in Australia after

Qantas Group and Airline Group.

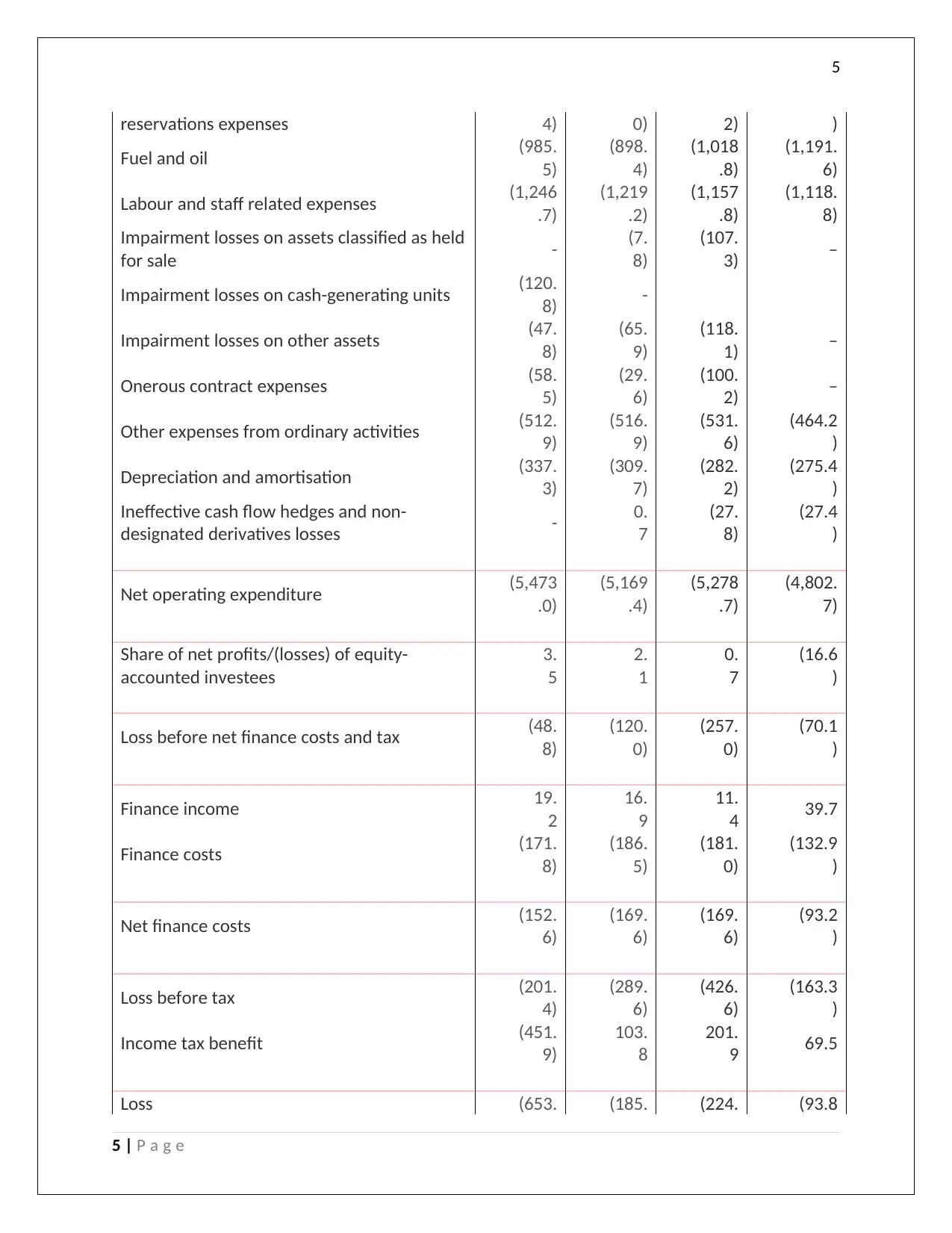

Financial Comparison for the entity - Internal

The comparative income statement for the last four years 2018, 2017, 2016 and 2015 has been

shown below:

Virgin Australia Group

Consolidated statement of profit or loss

Particulars 2018 2017 2016 2015

$m $m $m $m

Revenue and income

Airline passenger revenue 4,623.

4

4,275.

3

4,194.

8 3,999.0

Other ancillary revenue 793.

8

765.

3

790.

9 707.0

Other income 3.

5

3.

8

18.

2 17.4

Net foreign exchange gains - 2.

9

17.

1 25.8

Revenue and income 5,420.

7

5,047.

3

5,021.

0 4,749.2

Operating expenditure

Aircraft operating lease expenses (389.

0)

(426.

2)

(360.

6)

(290.0

)

Airport charges, navigation and station

operations

(1,060

.7)

(1,023

.8)

(984.

1)

(917.0

)

Contract and other maintenance expenses (246.

4)

(242.

6)

(182.

0)

(155.2

)

Commissions and other marketing and (467. (430. (408. (363.1

4 | P a g e

Part A – Virgin Australia Holdings Ltd (VAH)

Introduction

In this section of the report, the financial analysis of one of the companies Virgin Australia

Holdings Ltd has been done. It is listed on the Australian Stock Exchange and represented as

VAH. It is an airline company and operates in Australian as Virgin Australia, Virgin Australia

Regional Airlines, Virgin Australia International Airlines and Tigerair Australia. It was previously

being operated by Pacific Blue Airlines and was absorbed into Virgin Group in the year 2011

(Bromwich & Scapens, 2016). The company’s headquarters are based out of Brisbane and

employs nearly 10000 people. It is one of the largest Airline services company in Australia after

Qantas Group and Airline Group.

Financial Comparison for the entity - Internal

The comparative income statement for the last four years 2018, 2017, 2016 and 2015 has been

shown below:

Virgin Australia Group

Consolidated statement of profit or loss

Particulars 2018 2017 2016 2015

$m $m $m $m

Revenue and income

Airline passenger revenue 4,623.

4

4,275.

3

4,194.

8 3,999.0

Other ancillary revenue 793.

8

765.

3

790.

9 707.0

Other income 3.

5

3.

8

18.

2 17.4

Net foreign exchange gains - 2.

9

17.

1 25.8

Revenue and income 5,420.

7

5,047.

3

5,021.

0 4,749.2

Operating expenditure

Aircraft operating lease expenses (389.

0)

(426.

2)

(360.

6)

(290.0

)

Airport charges, navigation and station

operations

(1,060

.7)

(1,023

.8)

(984.

1)

(917.0

)

Contract and other maintenance expenses (246.

4)

(242.

6)

(182.

0)

(155.2

)

Commissions and other marketing and (467. (430. (408. (363.1

4 | P a g e

5

reservations expenses 4) 0) 2) )

Fuel and oil (985.

5)

(898.

4)

(1,018

.8)

(1,191.

6)

Labour and staff related expenses (1,246

.7)

(1,219

.2)

(1,157

.8)

(1,118.

8)

Impairment losses on assets classified as held

for sale - (7.

8)

(107.

3) –

Impairment losses on cash-generating units (120.

8) -

Impairment losses on other assets (47.

8)

(65.

9)

(118.

1) –

Onerous contract expenses (58.

5)

(29.

6)

(100.

2) –

Other expenses from ordinary activities (512.

9)

(516.

9)

(531.

6)

(464.2

)

Depreciation and amortisation (337.

3)

(309.

7)

(282.

2)

(275.4

)

Ineffective cash flow hedges and non-

designated derivatives losses - 0.

7

(27.

8)

(27.4

)

Net operating expenditure (5,473

.0)

(5,169

.4)

(5,278

.7)

(4,802.

7)

Share of net profits/(losses) of equity-

accounted investees

3.

5

2.

1

0.

7

(16.6

)

Loss before net finance costs and tax (48.

8)

(120.

0)

(257.

0)

(70.1

)

Finance income 19.

2

16.

9

11.

4 39.7

Finance costs (171.

8)

(186.

5)

(181.

0)

(132.9

)

Net finance costs (152.

6)

(169.

6)

(169.

6)

(93.2

)

Loss before tax (201.

4)

(289.

6)

(426.

6)

(163.3

)

Income tax benefit (451.

9)

103.

8

201.

9 69.5

Loss (653. (185. (224. (93.8

5 | P a g e

reservations expenses 4) 0) 2) )

Fuel and oil (985.

5)

(898.

4)

(1,018

.8)

(1,191.

6)

Labour and staff related expenses (1,246

.7)

(1,219

.2)

(1,157

.8)

(1,118.

8)

Impairment losses on assets classified as held

for sale - (7.

8)

(107.

3) –

Impairment losses on cash-generating units (120.

8) -

Impairment losses on other assets (47.

8)

(65.

9)

(118.

1) –

Onerous contract expenses (58.

5)

(29.

6)

(100.

2) –

Other expenses from ordinary activities (512.

9)

(516.

9)

(531.

6)

(464.2

)

Depreciation and amortisation (337.

3)

(309.

7)

(282.

2)

(275.4

)

Ineffective cash flow hedges and non-

designated derivatives losses - 0.

7

(27.

8)

(27.4

)

Net operating expenditure (5,473

.0)

(5,169

.4)

(5,278

.7)

(4,802.

7)

Share of net profits/(losses) of equity-

accounted investees

3.

5

2.

1

0.

7

(16.6

)

Loss before net finance costs and tax (48.

8)

(120.

0)

(257.

0)

(70.1

)

Finance income 19.

2

16.

9

11.

4 39.7

Finance costs (171.

8)

(186.

5)

(181.

0)

(132.9

)

Net finance costs (152.

6)

(169.

6)

(169.

6)

(93.2

)

Loss before tax (201.

4)

(289.

6)

(426.

6)

(163.3

)

Income tax benefit (451.

9)

103.

8

201.

9 69.5

Loss (653. (185. (224. (93.8

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

3) 8) 7) )

Attributable to:

Owners of the Company (681.

0)

(220.

3)

(260.

9)

(110.8

)

Non-controlling interests 27.

7

34.

5

36.

2 17.0

(653.

3)

(185.

8)

(224.

7)

(93.8

)

Earnings per share Cents Cents Cents Cents

Basic earnings per share (8.

1)

(2.

8)

(7.

4)

(3.2

)

Diluted earnings per share (8.

1)

(2.

8)

(7.

4)

(3.2

)

From the above financial data on income statement and trend analysis over the past 4 years,

we can see that the company has grown in terms of the revenue and the same can be seen

from the record sales in airline passenger division and other auxiliary revenue (Bumgarner &

Vasarhelyi, 2018). Besides revenue, the costs have also multiplied but the increase in operating

costs has not been in proportion of sales and thus, the cost as percentage of sales has dropped.

The major cost heads being the fuel, oil and power charges, the labour and staff related

expenses, commission to the marketing agents and companies, contract maintenance

expenses, airport lease charges and the Airport charges, station and navigations operation

expenses (Kok, Ribando, & Sloan, 2017). The major loss for the company has been the major

impairment expenses on the cash generating units as well as the assets, which were incurred

during the year. Furthermore, it can be seen that the depreciation expenses has been

increasing for the company every year on year. The finance income as well as the finance costs

have been more or less constant during the last 3 years without much change. However, the

loss for the company has been ever increasing which was $ 163.3 Mn in 2015, $ 426.6 Mn in

2016, and $ 289.6 Mn in 2017 and $ 201.4 Mn in 2018. Such has been the extent of loss that

the company never had positive EPS in the last 4 years.

The comparative balance sheet of the company for the last 4 years has been shown below:

6 | P a g e

3) 8) 7) )

Attributable to:

Owners of the Company (681.

0)

(220.

3)

(260.

9)

(110.8

)

Non-controlling interests 27.

7

34.

5

36.

2 17.0

(653.

3)

(185.

8)

(224.

7)

(93.8

)

Earnings per share Cents Cents Cents Cents

Basic earnings per share (8.

1)

(2.

8)

(7.

4)

(3.2

)

Diluted earnings per share (8.

1)

(2.

8)

(7.

4)

(3.2

)

From the above financial data on income statement and trend analysis over the past 4 years,

we can see that the company has grown in terms of the revenue and the same can be seen

from the record sales in airline passenger division and other auxiliary revenue (Bumgarner &

Vasarhelyi, 2018). Besides revenue, the costs have also multiplied but the increase in operating

costs has not been in proportion of sales and thus, the cost as percentage of sales has dropped.

The major cost heads being the fuel, oil and power charges, the labour and staff related

expenses, commission to the marketing agents and companies, contract maintenance

expenses, airport lease charges and the Airport charges, station and navigations operation

expenses (Kok, Ribando, & Sloan, 2017). The major loss for the company has been the major

impairment expenses on the cash generating units as well as the assets, which were incurred

during the year. Furthermore, it can be seen that the depreciation expenses has been

increasing for the company every year on year. The finance income as well as the finance costs

have been more or less constant during the last 3 years without much change. However, the

loss for the company has been ever increasing which was $ 163.3 Mn in 2015, $ 426.6 Mn in

2016, and $ 289.6 Mn in 2017 and $ 201.4 Mn in 2018. Such has been the extent of loss that

the company never had positive EPS in the last 4 years.

The comparative balance sheet of the company for the last 4 years has been shown below:

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

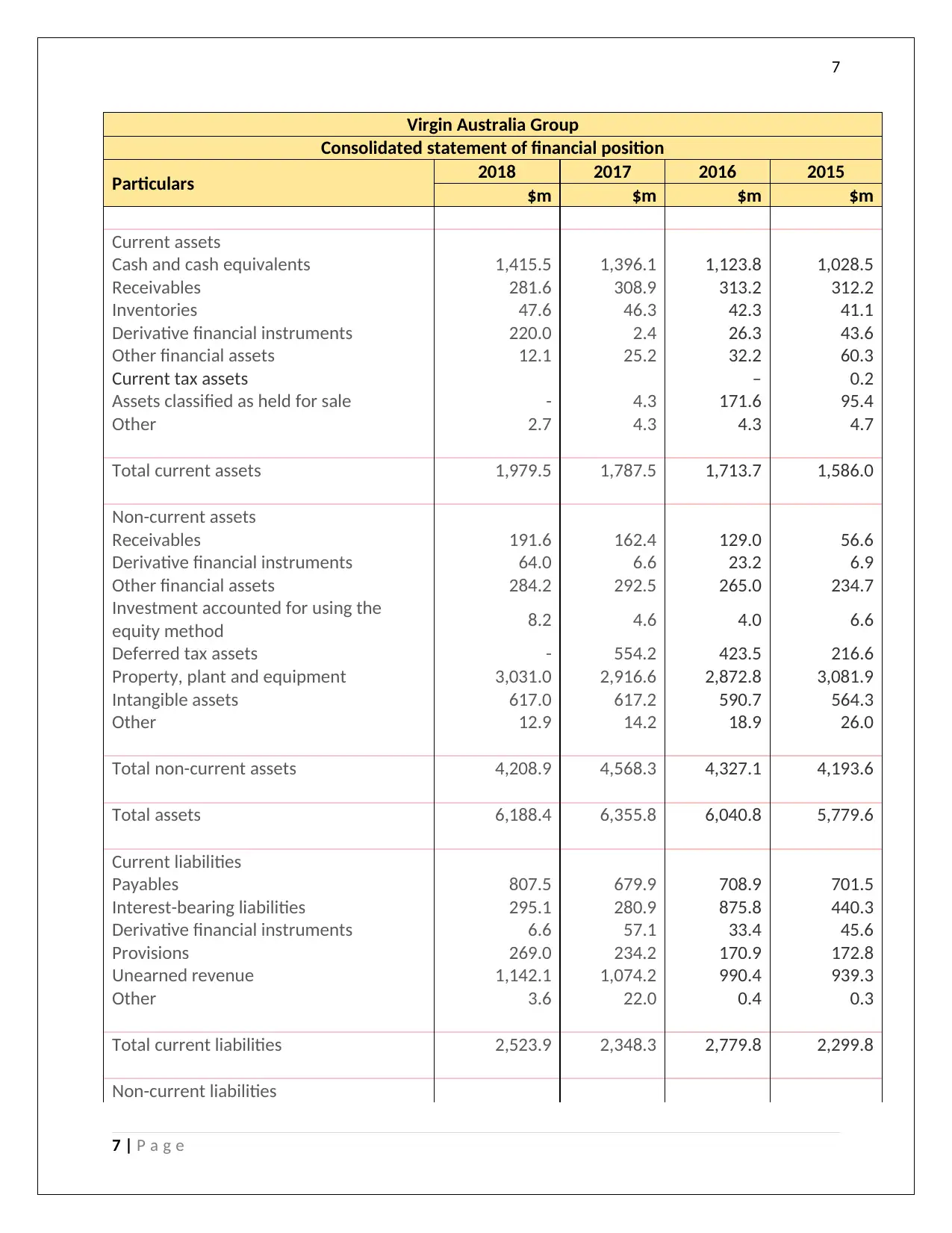

Virgin Australia Group

Consolidated statement of financial position

Particulars 2018 2017 2016 2015

$m $m $m $m

Current assets

Cash and cash equivalents 1,415.5 1,396.1 1,123.8 1,028.5

Receivables 281.6 308.9 313.2 312.2

Inventories 47.6 46.3 42.3 41.1

Derivative financial instruments 220.0 2.4 26.3 43.6

Other financial assets 12.1 25.2 32.2 60.3

Current tax assets – 0.2

Assets classified as held for sale - 4.3 171.6 95.4

Other 2.7 4.3 4.3 4.7

Total current assets 1,979.5 1,787.5 1,713.7 1,586.0

Non-current assets

Receivables 191.6 162.4 129.0 56.6

Derivative financial instruments 64.0 6.6 23.2 6.9

Other financial assets 284.2 292.5 265.0 234.7

Investment accounted for using the

equity method 8.2 4.6 4.0 6.6

Deferred tax assets - 554.2 423.5 216.6

Property, plant and equipment 3,031.0 2,916.6 2,872.8 3,081.9

Intangible assets 617.0 617.2 590.7 564.3

Other 12.9 14.2 18.9 26.0

Total non-current assets 4,208.9 4,568.3 4,327.1 4,193.6

Total assets 6,188.4 6,355.8 6,040.8 5,779.6

Current liabilities

Payables 807.5 679.9 708.9 701.5

Interest-bearing liabilities 295.1 280.9 875.8 440.3

Derivative financial instruments 6.6 57.1 33.4 45.6

Provisions 269.0 234.2 170.9 172.8

Unearned revenue 1,142.1 1,074.2 990.4 939.3

Other 3.6 22.0 0.4 0.3

Total current liabilities 2,523.9 2,348.3 2,779.8 2,299.8

Non-current liabilities

7 | P a g e

Virgin Australia Group

Consolidated statement of financial position

Particulars 2018 2017 2016 2015

$m $m $m $m

Current assets

Cash and cash equivalents 1,415.5 1,396.1 1,123.8 1,028.5

Receivables 281.6 308.9 313.2 312.2

Inventories 47.6 46.3 42.3 41.1

Derivative financial instruments 220.0 2.4 26.3 43.6

Other financial assets 12.1 25.2 32.2 60.3

Current tax assets – 0.2

Assets classified as held for sale - 4.3 171.6 95.4

Other 2.7 4.3 4.3 4.7

Total current assets 1,979.5 1,787.5 1,713.7 1,586.0

Non-current assets

Receivables 191.6 162.4 129.0 56.6

Derivative financial instruments 64.0 6.6 23.2 6.9

Other financial assets 284.2 292.5 265.0 234.7

Investment accounted for using the

equity method 8.2 4.6 4.0 6.6

Deferred tax assets - 554.2 423.5 216.6

Property, plant and equipment 3,031.0 2,916.6 2,872.8 3,081.9

Intangible assets 617.0 617.2 590.7 564.3

Other 12.9 14.2 18.9 26.0

Total non-current assets 4,208.9 4,568.3 4,327.1 4,193.6

Total assets 6,188.4 6,355.8 6,040.8 5,779.6

Current liabilities

Payables 807.5 679.9 708.9 701.5

Interest-bearing liabilities 295.1 280.9 875.8 440.3

Derivative financial instruments 6.6 57.1 33.4 45.6

Provisions 269.0 234.2 170.9 172.8

Unearned revenue 1,142.1 1,074.2 990.4 939.3

Other 3.6 22.0 0.4 0.3

Total current liabilities 2,523.9 2,348.3 2,779.8 2,299.8

Non-current liabilities

7 | P a g e

8

Payables 5.6 6.3 9.3 6.3

Interest-bearing liabilities 2,273.0 2,152.4 2,124.2 2,321.9

Derivative financial instruments 0.2 6.4 8.0 –

Provisions 277.6 263.5 214.6 122.4

Unearned revenue – 2.0

Other 13.1 5.1 6.1 6.4

Total non-current liabilities 2,569.5 2,433.7 2,362.2 2,459.0

Total liabilities 5,093.4 4,782.0 5,142.0 4,758.8

Net assets 1,095.0 1,573.8 898.8 1,020.8

Equity

Share capital 2,238.9 2,243.7 1,309.0 1,152.9

Reserves 268.3 58.8 117.2 177.3

Retained earnings (1,415.8) (734.8) (514.5) (253.6)

Equity attributable to the owners of the

Company 1,091.4 1,567.7 911.7 1,076.6

Non-controlling interests 3.6 6.1 (12.9) (55.8)

Total equity 1,095.0 1,573.8 898.8 1,020.8

From the comparative balance sheet of the company for the last 4 year, it can be seen that the

current assets have been on the increasing trend, especially the balance of cash and cash

equivalents. This is done to have more liquid cash considering the requirements of growing

business (Choy, 2018). The receivables balance has declined which indicates good collection

measures and the stock or inventory balance has been more or less constant throughout the

years. The company does not hold assets for sale anymore in 2018 and have sold it all. Amongst

the non-current assets, the balance of receivables has increased indicating that the old debtors

are not paying off the dues. The financial assets have remained more or less constant through

these years and the same has been the case with property, plant and equipment and the

intangible assets.

Amongst the current liabilities, the balance of payable has increased (which is due to increase in

business volume). However, the balances of the unearned revenue and the provision has

increased marginally. The non-current liabilities of interest bearing liabilities like debt and the

long term provisions has increased which shows that the company has not being paying off on

time (Jefferson, 2017).

8 | P a g e

Payables 5.6 6.3 9.3 6.3

Interest-bearing liabilities 2,273.0 2,152.4 2,124.2 2,321.9

Derivative financial instruments 0.2 6.4 8.0 –

Provisions 277.6 263.5 214.6 122.4

Unearned revenue – 2.0

Other 13.1 5.1 6.1 6.4

Total non-current liabilities 2,569.5 2,433.7 2,362.2 2,459.0

Total liabilities 5,093.4 4,782.0 5,142.0 4,758.8

Net assets 1,095.0 1,573.8 898.8 1,020.8

Equity

Share capital 2,238.9 2,243.7 1,309.0 1,152.9

Reserves 268.3 58.8 117.2 177.3

Retained earnings (1,415.8) (734.8) (514.5) (253.6)

Equity attributable to the owners of the

Company 1,091.4 1,567.7 911.7 1,076.6

Non-controlling interests 3.6 6.1 (12.9) (55.8)

Total equity 1,095.0 1,573.8 898.8 1,020.8

From the comparative balance sheet of the company for the last 4 year, it can be seen that the

current assets have been on the increasing trend, especially the balance of cash and cash

equivalents. This is done to have more liquid cash considering the requirements of growing

business (Choy, 2018). The receivables balance has declined which indicates good collection

measures and the stock or inventory balance has been more or less constant throughout the

years. The company does not hold assets for sale anymore in 2018 and have sold it all. Amongst

the non-current assets, the balance of receivables has increased indicating that the old debtors

are not paying off the dues. The financial assets have remained more or less constant through

these years and the same has been the case with property, plant and equipment and the

intangible assets.

Amongst the current liabilities, the balance of payable has increased (which is due to increase in

business volume). However, the balances of the unearned revenue and the provision has

increased marginally. The non-current liabilities of interest bearing liabilities like debt and the

long term provisions has increased which shows that the company has not being paying off on

time (Jefferson, 2017).

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

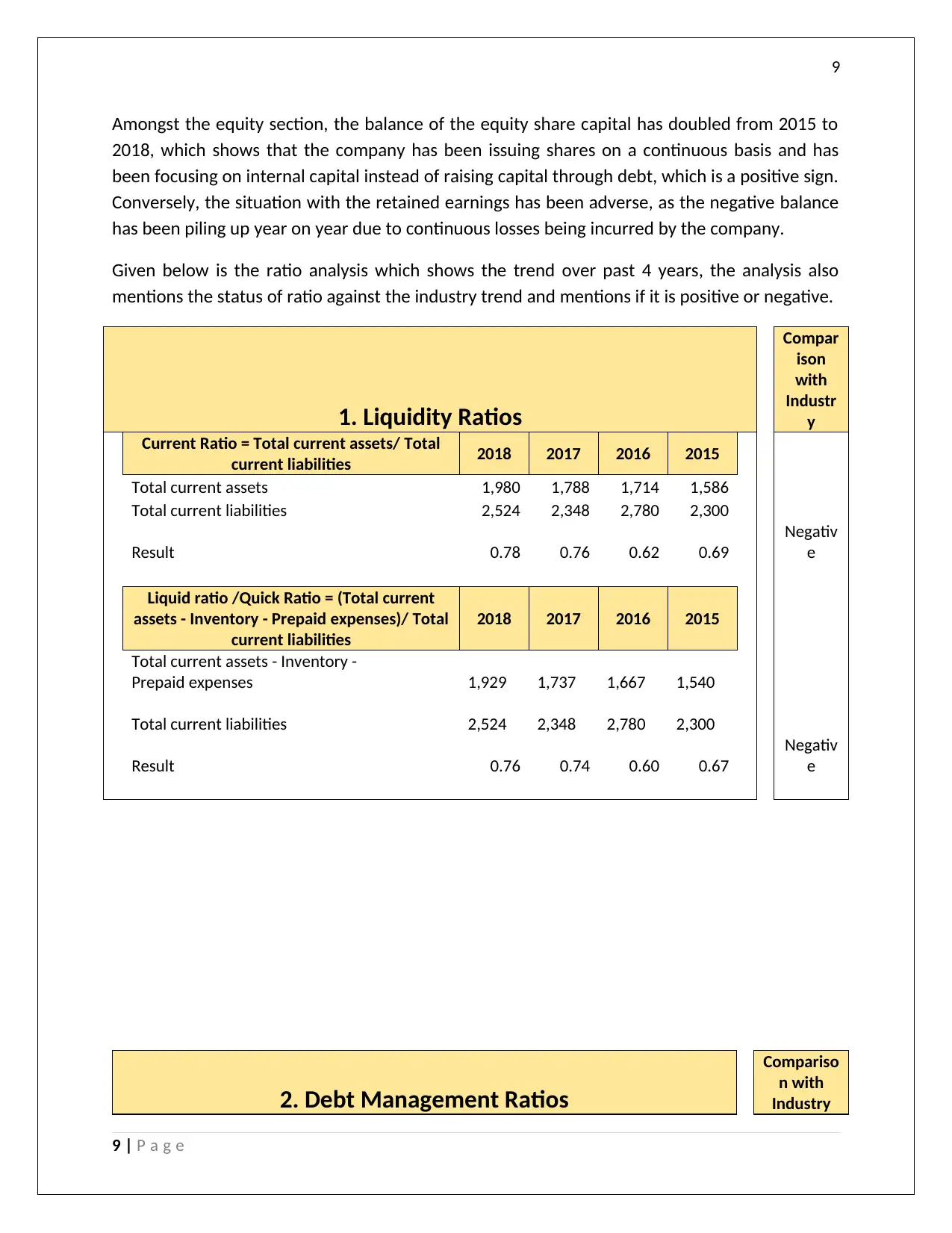

Amongst the equity section, the balance of the equity share capital has doubled from 2015 to

2018, which shows that the company has been issuing shares on a continuous basis and has

been focusing on internal capital instead of raising capital through debt, which is a positive sign.

Conversely, the situation with the retained earnings has been adverse, as the negative balance

has been piling up year on year due to continuous losses being incurred by the company.

Given below is the ratio analysis which shows the trend over past 4 years, the analysis also

mentions the status of ratio against the industry trend and mentions if it is positive or negative.

1. Liquidity Ratios

Compar

ison

with

Industr

y

Current Ratio = Total current assets/ Total

current liabilities 2018 2017 2016 2015

Total current assets 1,980 1,788 1,714 1,586

Total current liabilities 2,524 2,348 2,780 2,300

Result 0.78 0.76 0.62 0.69

Negativ

e

Liquid ratio /Quick Ratio = (Total current

assets - Inventory - Prepaid expenses)/ Total

current liabilities

2018 2017 2016 2015

Total current assets - Inventory -

Prepaid expenses 1,929 1,737 1,667 1,540

Total current liabilities 2,524 2,348 2,780 2,300

Result 0.76 0.74 0.60 0.67

Negativ

e

2. Debt Management Ratios

Compariso

n with

Industry

9 | P a g e

Amongst the equity section, the balance of the equity share capital has doubled from 2015 to

2018, which shows that the company has been issuing shares on a continuous basis and has

been focusing on internal capital instead of raising capital through debt, which is a positive sign.

Conversely, the situation with the retained earnings has been adverse, as the negative balance

has been piling up year on year due to continuous losses being incurred by the company.

Given below is the ratio analysis which shows the trend over past 4 years, the analysis also

mentions the status of ratio against the industry trend and mentions if it is positive or negative.

1. Liquidity Ratios

Compar

ison

with

Industr

y

Current Ratio = Total current assets/ Total

current liabilities 2018 2017 2016 2015

Total current assets 1,980 1,788 1,714 1,586

Total current liabilities 2,524 2,348 2,780 2,300

Result 0.78 0.76 0.62 0.69

Negativ

e

Liquid ratio /Quick Ratio = (Total current

assets - Inventory - Prepaid expenses)/ Total

current liabilities

2018 2017 2016 2015

Total current assets - Inventory -

Prepaid expenses 1,929 1,737 1,667 1,540

Total current liabilities 2,524 2,348 2,780 2,300

Result 0.76 0.74 0.60 0.67

Negativ

e

2. Debt Management Ratios

Compariso

n with

Industry

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

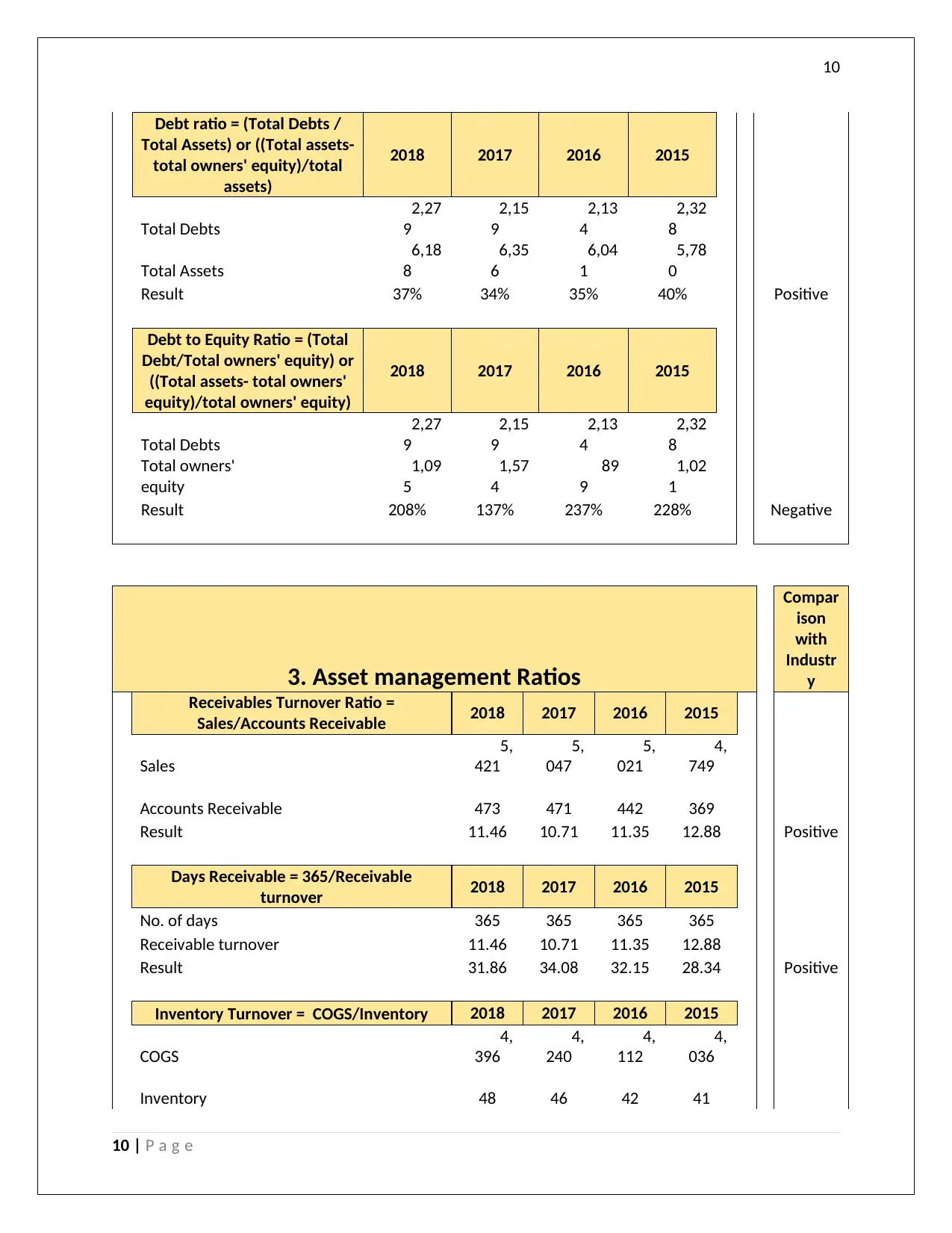

Debt ratio = (Total Debts /

Total Assets) or ((Total assets-

total owners' equity)/total

assets)

2018 2017 2016 2015

Total Debts

2,27

9

2,15

9

2,13

4

2,32

8

Total Assets

6,18

8

6,35

6

6,04

1

5,78

0

Result 37% 34% 35% 40% Positive

Debt to Equity Ratio = (Total

Debt/Total owners' equity) or

((Total assets- total owners'

equity)/total owners' equity)

2018 2017 2016 2015

Total Debts

2,27

9

2,15

9

2,13

4

2,32

8

Total owners'

equity

1,09

5

1,57

4

89

9

1,02

1

Result 208% 137% 237% 228% Negative

3. Asset management Ratios

Compar

ison

with

Industr

y

Receivables Turnover Ratio =

Sales/Accounts Receivable 2018 2017 2016 2015

Sales

5,

421

5,

047

5,

021

4,

749

Accounts Receivable 473 471 442 369

Result 11.46 10.71 11.35 12.88 Positive

Days Receivable = 365/Receivable

turnover 2018 2017 2016 2015

No. of days 365 365 365 365

Receivable turnover 11.46 10.71 11.35 12.88

Result 31.86 34.08 32.15 28.34 Positive

Inventory Turnover = COGS/Inventory 2018 2017 2016 2015

COGS

4,

396

4,

240

4,

112

4,

036

Inventory 48 46 42 41

10 | P a g e

Debt ratio = (Total Debts /

Total Assets) or ((Total assets-

total owners' equity)/total

assets)

2018 2017 2016 2015

Total Debts

2,27

9

2,15

9

2,13

4

2,32

8

Total Assets

6,18

8

6,35

6

6,04

1

5,78

0

Result 37% 34% 35% 40% Positive

Debt to Equity Ratio = (Total

Debt/Total owners' equity) or

((Total assets- total owners'

equity)/total owners' equity)

2018 2017 2016 2015

Total Debts

2,27

9

2,15

9

2,13

4

2,32

8

Total owners'

equity

1,09

5

1,57

4

89

9

1,02

1

Result 208% 137% 237% 228% Negative

3. Asset management Ratios

Compar

ison

with

Industr

y

Receivables Turnover Ratio =

Sales/Accounts Receivable 2018 2017 2016 2015

Sales

5,

421

5,

047

5,

021

4,

749

Accounts Receivable 473 471 442 369

Result 11.46 10.71 11.35 12.88 Positive

Days Receivable = 365/Receivable

turnover 2018 2017 2016 2015

No. of days 365 365 365 365

Receivable turnover 11.46 10.71 11.35 12.88

Result 31.86 34.08 32.15 28.34 Positive

Inventory Turnover = COGS/Inventory 2018 2017 2016 2015

COGS

4,

396

4,

240

4,

112

4,

036

Inventory 48 46 42 41

10 | P a g e

11

Result 92.35 91.58 97.20 98.19

Negativ

e

Days' Inventory = 365/Inventory Turnover 2018 2017 2016 2015

No. of days 365 365 365 365

Inventory turnover 92.35 91.58 97.20 98.19

Result 3.95 3.99 3.76 3.72

Negativ

e

4. Profitability ratios

Compari

son

with

Industry

Profit Margin / Net Profit ratio = Net

income / Sales 2018 2017 2016 2015

Net income

(2

01)

(

290)

(4

27)

(1

63)

Sales

5,

421

5,

047

5,

021

4,

749

Result -3.72% -5.74% -8.50% -3.44%

Negativ

e

Operating Margin ratio = Operating

Profit/Sales 2018 2017 2016 2015

Operating Profit (49)

(

120)

(2

57) (70)

Sales

5,

421

5,

047

5,

021

4,

749

Result -0.90% -2.38% -5.12% -1.48%

Negativ

e

Return on Equity = Net income/total

owners' equity 2018 2017 2016 2015

Net income

(2

01)

(

290)

(4

27)

(1

63)

Total owners' equity

1,

095

1,

574 899

1,

021

Result -18.39%

-

18.40% -47.46% -16.00%

Negativ

e

From the above trend of ratios, we can see that though the current ratio has improved a bit,

but the same is still is way below the industry trend of 2:1 times, similarly the liquid ratio or the

11 | P a g e

Result 92.35 91.58 97.20 98.19

Negativ

e

Days' Inventory = 365/Inventory Turnover 2018 2017 2016 2015

No. of days 365 365 365 365

Inventory turnover 92.35 91.58 97.20 98.19

Result 3.95 3.99 3.76 3.72

Negativ

e

4. Profitability ratios

Compari

son

with

Industry

Profit Margin / Net Profit ratio = Net

income / Sales 2018 2017 2016 2015

Net income

(2

01)

(

290)

(4

27)

(1

63)

Sales

5,

421

5,

047

5,

021

4,

749

Result -3.72% -5.74% -8.50% -3.44%

Negativ

e

Operating Margin ratio = Operating

Profit/Sales 2018 2017 2016 2015

Operating Profit (49)

(

120)

(2

57) (70)

Sales

5,

421

5,

047

5,

021

4,

749

Result -0.90% -2.38% -5.12% -1.48%

Negativ

e

Return on Equity = Net income/total

owners' equity 2018 2017 2016 2015

Net income

(2

01)

(

290)

(4

27)

(1

63)

Total owners' equity

1,

095

1,

574 899

1,

021

Result -18.39%

-

18.40% -47.46% -16.00%

Negativ

e

From the above trend of ratios, we can see that though the current ratio has improved a bit,

but the same is still is way below the industry trend of 2:1 times, similarly the liquid ratio or the

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.