HI5020 Corporate Accounting: A Financial Analysis of Virgin Group

VerifiedAdded on 2023/06/12

|13

|2966

|222

Report

AI Summary

This report provides a detailed corporate accounting analysis of Virgin Group, a public limited company listed on the Australian Securities Exchange (ASX). It examines the company's cash flow statement, dissecting operating, investing, and financing activities, and analyzes changes over a three-year period (2015-2017). The report also explores the comprehensive income statement, focusing on items like foreign currency translation reserve and income tax implications. Furthermore, it delves into the company's tax treatment, including deferred tax assets and liabilities, and payable income tax. The analysis draws upon information from Virgin Australia's annual reports, offering insights into the company's financial performance and accounting practices.

Running head: CORPORATE ACCOUNTING IN VIRGIN GROUP

Corporate Accounting in Virgin Group

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting in Virgin Group

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTINGIN VIRGIN GROUP

Table of Contents

Statement of Cash Flow:..................................................................................................................2

Answer to Question (i):...............................................................................................................2

Answer to Question(ii):...............................................................................................................4

Analysis of comprehensive income statement:................................................................................5

Answer to Question(iii):..............................................................................................................5

Answer to Question(iv):..............................................................................................................5

Answer to Question(v):................................................................................................................5

Accounting in consideration to corporate income tax:....................................................................6

Answer to Question(vi):..............................................................................................................6

Answer to Question (vii):............................................................................................................6

Answer to Question (viii):...........................................................................................................6

Answer to Question (ix):.............................................................................................................7

Answer to Question(x):................................................................................................................8

Answer to Question (xi):.............................................................................................................8

References:....................................................................................................................................10

Table of Contents

Statement of Cash Flow:..................................................................................................................2

Answer to Question (i):...............................................................................................................2

Answer to Question(ii):...............................................................................................................4

Analysis of comprehensive income statement:................................................................................5

Answer to Question(iii):..............................................................................................................5

Answer to Question(iv):..............................................................................................................5

Answer to Question(v):................................................................................................................5

Accounting in consideration to corporate income tax:....................................................................6

Answer to Question(vi):..............................................................................................................6

Answer to Question (vii):............................................................................................................6

Answer to Question (viii):...........................................................................................................6

Answer to Question (ix):.............................................................................................................7

Answer to Question(x):................................................................................................................8

Answer to Question (xi):.............................................................................................................8

References:....................................................................................................................................10

2CORPORATE ACCOUNTINGIN VIRGIN GROUP

Statement of Cash Flow:

Answer to Question (i):

In the current report, Virgin Australia is chosen as a company that is positioned as mong

the renowned airline organization within Australia and is listed within the Australian Securities

Exchange (ASX) having a code of VAH. The cash flow statement of the company is segmented

within investing, financing and operating activities (Bennedsen and Zeume 2017). Moreover, an

identical amount has been is reported in the part of reconciliation of the net loss to the net cash

from the business operations within the yearly report of the company. The items that are

explained within the companies each activity head is elaborated under:

Operating activities of cash flows:

The major items explained within the head includes the receipts from the consumers, payments

meant for the suppliers and employees, received finance income, paid finance costs and a few

more. The consumer recepts are considered as the amounts attained from credit sales. For Virgin

Australia, increase is gathered within the item fom$5,567.40 million in 2016 to $5,657.10

million in 2017, for the reason that it has strong credit policy (Burrell and Morgan 2017). The

staffs along with the payment of suppliers are the amounts which are acquired by Virgin Group

on credit along with salaries of the employees. In Virgin Group situation, increasing trend might

be observed in the year 2017 because of additional purchases from the suppliers along with

observing increase in the number of employees. Finance income is the attained sum for attained

to use money for repayment on demand at a particular point of time. Increase in this item might

be observed in 2017 as this is written off as a credit portion and the sales are deemed to be

Statement of Cash Flow:

Answer to Question (i):

In the current report, Virgin Australia is chosen as a company that is positioned as mong

the renowned airline organization within Australia and is listed within the Australian Securities

Exchange (ASX) having a code of VAH. The cash flow statement of the company is segmented

within investing, financing and operating activities (Bennedsen and Zeume 2017). Moreover, an

identical amount has been is reported in the part of reconciliation of the net loss to the net cash

from the business operations within the yearly report of the company. The items that are

explained within the companies each activity head is elaborated under:

Operating activities of cash flows:

The major items explained within the head includes the receipts from the consumers, payments

meant for the suppliers and employees, received finance income, paid finance costs and a few

more. The consumer recepts are considered as the amounts attained from credit sales. For Virgin

Australia, increase is gathered within the item fom$5,567.40 million in 2016 to $5,657.10

million in 2017, for the reason that it has strong credit policy (Burrell and Morgan 2017). The

staffs along with the payment of suppliers are the amounts which are acquired by Virgin Group

on credit along with salaries of the employees. In Virgin Group situation, increasing trend might

be observed in the year 2017 because of additional purchases from the suppliers along with

observing increase in the number of employees. Finance income is the attained sum for attained

to use money for repayment on demand at a particular point of time. Increase in this item might

be observed in 2017 as this is written off as a credit portion and the sales are deemed to be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTINGIN VIRGIN GROUP

uncontrollable. Finance cost indicates the obligations and this has dropped in the company in the

year 2017 because of decreased interest payments on the loans undertaken.

Investing activities cash flow:

The major aspects those are listed within this section include plant, promptly and

equipment proceeds from along with advances to the deposits along with others (DeZoort,

Wilkins and Justice 2017). The payments associated with plant, proper and equipment is the

incurred amounts that are deemed to be necessary to carry out business conducts. In addition, for

the reason that these assets offer economic advantages to the company that is deemed as

proceeds. It might also be gathered that Virgin Australia has decreased its investment in this

aspects. Due to the same, this has not developed enough cash flows from these items as it has

sold as an aspect of plant, equipment and property. The proceeds along with the payments

associated with deposits serves as a financial instrument that is a contraindicating the repayment

time and for receiving the interest payable. Virgin Australia has made several payments in

comparison to the amounts than it has attained from deposits in the year 2017 because of

increased interest payable rate.

Financing activities cash flows:

The major items which are encompassed within this aspect include repayment of and

proceed from the borrowings, equity distribution along with various items. The borrowings

indicate the disbursed net amount to a borrower on the behalf of the lender within the loan

agreement terms. It might also be gathered from the annual report of Virgin Australia that the

proceeds firm borrowings have dropped in the year 2017. An increase has also been observed in

borrowings repayment that was also observed in the same year. Equity distribution indicates the

uncontrollable. Finance cost indicates the obligations and this has dropped in the company in the

year 2017 because of decreased interest payments on the loans undertaken.

Investing activities cash flow:

The major aspects those are listed within this section include plant, promptly and

equipment proceeds from along with advances to the deposits along with others (DeZoort,

Wilkins and Justice 2017). The payments associated with plant, proper and equipment is the

incurred amounts that are deemed to be necessary to carry out business conducts. In addition, for

the reason that these assets offer economic advantages to the company that is deemed as

proceeds. It might also be gathered that Virgin Australia has decreased its investment in this

aspects. Due to the same, this has not developed enough cash flows from these items as it has

sold as an aspect of plant, equipment and property. The proceeds along with the payments

associated with deposits serves as a financial instrument that is a contraindicating the repayment

time and for receiving the interest payable. Virgin Australia has made several payments in

comparison to the amounts than it has attained from deposits in the year 2017 because of

increased interest payable rate.

Financing activities cash flows:

The major items which are encompassed within this aspect include repayment of and

proceed from the borrowings, equity distribution along with various items. The borrowings

indicate the disbursed net amount to a borrower on the behalf of the lender within the loan

agreement terms. It might also be gathered from the annual report of Virgin Australia that the

proceeds firm borrowings have dropped in the year 2017. An increase has also been observed in

borrowings repayment that was also observed in the same year. Equity distribution indicates the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTINGIN VIRGIN GROUP

yearly cash flow that is offered to all its shareholders in the same year. In case of Virgin Group,

the amount has decreased in 2017 as more focus has been put on retained earnings maximization.

Answer to Question(ii):

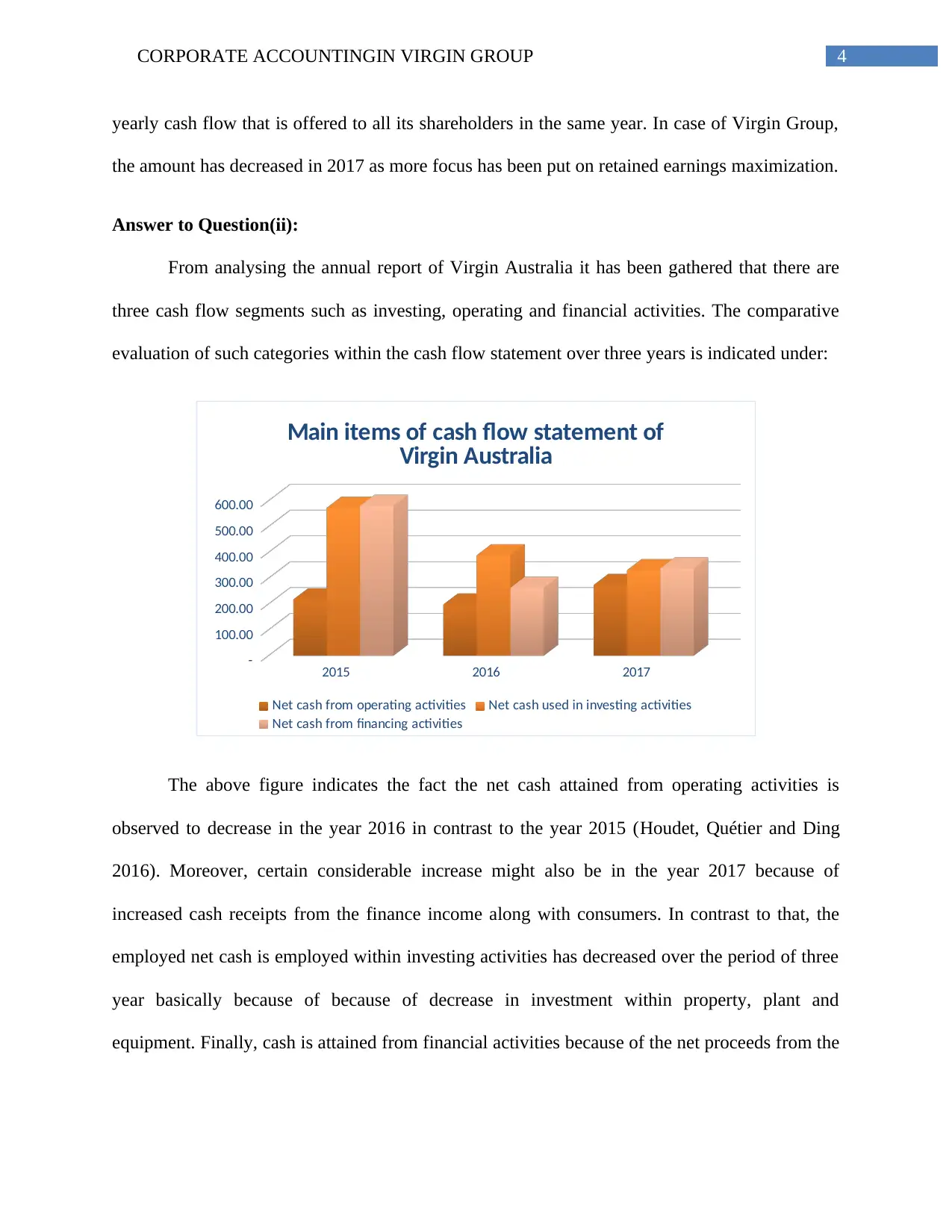

From analysing the annual report of Virgin Australia it has been gathered that there are

three cash flow segments such as investing, operating and financial activities. The comparative

evaluation of such categories within the cash flow statement over three years is indicated under:

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Main items of cash flow statement of

Virgin Australia

Net cash from operating activities Net cash used in investing activities

Net cash from financing activities

The above figure indicates the fact the net cash attained from operating activities is

observed to decrease in the year 2016 in contrast to the year 2015 (Houdet, Quétier and Ding

2016). Moreover, certain considerable increase might also be in the year 2017 because of

increased cash receipts from the finance income along with consumers. In contrast to that, the

employed net cash is employed within investing activities has decreased over the period of three

year basically because of because of decrease in investment within property, plant and

equipment. Finally, cash is attained from financial activities because of the net proceeds from the

yearly cash flow that is offered to all its shareholders in the same year. In case of Virgin Group,

the amount has decreased in 2017 as more focus has been put on retained earnings maximization.

Answer to Question(ii):

From analysing the annual report of Virgin Australia it has been gathered that there are

three cash flow segments such as investing, operating and financial activities. The comparative

evaluation of such categories within the cash flow statement over three years is indicated under:

2015 2016 2017

-

100.00

200.00

300.00

400.00

500.00

600.00

Main items of cash flow statement of

Virgin Australia

Net cash from operating activities Net cash used in investing activities

Net cash from financing activities

The above figure indicates the fact the net cash attained from operating activities is

observed to decrease in the year 2016 in contrast to the year 2015 (Houdet, Quétier and Ding

2016). Moreover, certain considerable increase might also be in the year 2017 because of

increased cash receipts from the finance income along with consumers. In contrast to that, the

employed net cash is employed within investing activities has decreased over the period of three

year basically because of because of decrease in investment within property, plant and

equipment. Finally, cash is attained from financial activities because of the net proceeds from the

5CORPORATE ACCOUNTINGIN VIRGIN GROUP

shares issuance in the year 2017. For this reason, increase might be observed within cash along

with cash equivalents of Virgin Australia in the year 2017 (Miao, Teoh And Zhu 2016).

Analysis of comprehensive income statement:

Answer to Question(iii):

As per the annual report of Virgin Asia Group in the year 2017, the major items listed in

the comprehensive income statement includes foreign currency translation reserve, cash flow

hedge reserve along with income tax advantage or expense (Leary and Roberts 2014).

Answer to Question(iv):

It has been gathered that, the implementation of foreign currency translation reserve is

conducted for interaction regarding the outcomes of foreign subsidiaries of the parent company

to the reporting currency (Ferri and Göx 2018). The utilization of cash for hedging is conducted

at the time a company intends to decrease the exposure taking place because of variations in cash

flow of a liability or asset as certain changes in particular risk like rate of interest on debt

instrument is associated with the floating rate. In addition, the income tax expense sources at the

incurred amount on profit before tax of the company (Virginaustralia.com. 2018).

Answer to Question(v):

It has been gathered that, the elaborated net income view is deemed to be other

comprehensive income. Virgin Group employs such statement for offering vital details in values

related ith above mentioned items. The major cause that such items are explained within other

comprehensive income statement is that they offer holistic and comprehensive overview of the

drivers associated with business operations and for this reason, these are not disclosed within the

income statement.

shares issuance in the year 2017. For this reason, increase might be observed within cash along

with cash equivalents of Virgin Australia in the year 2017 (Miao, Teoh And Zhu 2016).

Analysis of comprehensive income statement:

Answer to Question(iii):

As per the annual report of Virgin Asia Group in the year 2017, the major items listed in

the comprehensive income statement includes foreign currency translation reserve, cash flow

hedge reserve along with income tax advantage or expense (Leary and Roberts 2014).

Answer to Question(iv):

It has been gathered that, the implementation of foreign currency translation reserve is

conducted for interaction regarding the outcomes of foreign subsidiaries of the parent company

to the reporting currency (Ferri and Göx 2018). The utilization of cash for hedging is conducted

at the time a company intends to decrease the exposure taking place because of variations in cash

flow of a liability or asset as certain changes in particular risk like rate of interest on debt

instrument is associated with the floating rate. In addition, the income tax expense sources at the

incurred amount on profit before tax of the company (Virginaustralia.com. 2018).

Answer to Question(v):

It has been gathered that, the elaborated net income view is deemed to be other

comprehensive income. Virgin Group employs such statement for offering vital details in values

related ith above mentioned items. The major cause that such items are explained within other

comprehensive income statement is that they offer holistic and comprehensive overview of the

drivers associated with business operations and for this reason, these are not disclosed within the

income statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTINGIN VIRGIN GROUP

Accounting in consideration to corporate income tax:

Answer to Question(vi):

Tax expense is taken into consideration as a vital obligation of the company because of

municipal, federal as well as state government of the country. In situation of Virgin Australia, it

has not attained tax expense and this has attained income tax advantage in both the years 2016

and 2017. In the next year, it has attained income tax advantage of $103.8 million in comparison

to $201.9 million in 2016 (Lian, Rupley, Wang and Zheng 2017).

Answer to Question (vii):

Focussed on the annual report of Virgin Australia for the year 2017, it has been gathered

that that company has dealt with loss before income tax in the years 2016 and 2017. It is clearly

gathered from the annual report that this airline organization charges tax rate of 30% on its profit

before tax income for attaining suitable net income (Ebrahim and Fattah 2015). Conversely, for

the reason that the airline has experienced loss before income tax, it is not deemed likely to make

income tax expense responsible. Moreover, it is also not likely to make sure whether the tax

expense related with the airline requires to be explained within the company’s statement of

income. This is also considered to be computed with tax rate of 30% on the profit before tax

expense.

Answer to Question (viii):

Deferred tax assets are observed to take place in such situations in which the companies

experience additional taxes or consider making tax repayments on the financial assets. In contrast

to that, deferred tax liabilities indicate the conditions in which the changes can be recognised in

tax carrying amount along with profit related with corporate organizations. For Virgin Australia,

Accounting in consideration to corporate income tax:

Answer to Question(vi):

Tax expense is taken into consideration as a vital obligation of the company because of

municipal, federal as well as state government of the country. In situation of Virgin Australia, it

has not attained tax expense and this has attained income tax advantage in both the years 2016

and 2017. In the next year, it has attained income tax advantage of $103.8 million in comparison

to $201.9 million in 2016 (Lian, Rupley, Wang and Zheng 2017).

Answer to Question (vii):

Focussed on the annual report of Virgin Australia for the year 2017, it has been gathered

that that company has dealt with loss before income tax in the years 2016 and 2017. It is clearly

gathered from the annual report that this airline organization charges tax rate of 30% on its profit

before tax income for attaining suitable net income (Ebrahim and Fattah 2015). Conversely, for

the reason that the airline has experienced loss before income tax, it is not deemed likely to make

income tax expense responsible. Moreover, it is also not likely to make sure whether the tax

expense related with the airline requires to be explained within the company’s statement of

income. This is also considered to be computed with tax rate of 30% on the profit before tax

expense.

Answer to Question (viii):

Deferred tax assets are observed to take place in such situations in which the companies

experience additional taxes or consider making tax repayments on the financial assets. In contrast

to that, deferred tax liabilities indicate the conditions in which the changes can be recognised in

tax carrying amount along with profit related with corporate organizations. For Virgin Australia,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTINGIN VIRGIN GROUP

the deferred tax assets are accountable for $1,017.6 million in the year 2017 that was observed to

be $857.9 million in the year 2016 (Dechow and Tan 2017). In addition to that, the company’s

deferred tax liabilities are accounted to be $463.4 million for the year 2017 in contrast to $434.4

million observed in the year 2016. Recognition focused on conducted deferred tax is carried out

for the reason that high amount of depreciation is experienced because of variations in taxable

depreciation rate along with depreciation amount. Deferred tax liabilities recognition is carried

out because of temporary changes in the profits. This is because of which Virgin Australia

Company is evidenced to attain tax exemptions in the year 2016 as well as 2017 (Mintz 2016).

Answer to Question (ix):

Payable income tax or the current tax asset is deemed as a vital factor for the Australian

business firms. Considering the information provided in the annual report of Virgin Australia, it

is gathered that the current tax assets include the anticipated tax payable. This also includes

certain receivables on taxable loss or income for a particular period. These are measured with the

support of tax rates along with tax laws enacted at the financial year. However, considering the

situation of Virgin Australia it has been observed that the company has attained income tax

advantages of $201.9 million 2016 and $103.8 million in 2017 (Collins, Hribar And Tian 2014).

Moreover, an identical amount has been is reported in the part of reconciliation of the net loss to

the net cash from the business operations within the yearly report of the company. The vital

cause that is indicated by these two items is the same values for the reason that there are no

excess expenses experienced on the behalf of the company in these two years (Parsa et al. 2018).

The utilization of cash flow hedging is conducted at the time a company intends to decrease the

exposure taking place because of variations in cash flow of a liability or asset as certain changes

the deferred tax assets are accountable for $1,017.6 million in the year 2017 that was observed to

be $857.9 million in the year 2016 (Dechow and Tan 2017). In addition to that, the company’s

deferred tax liabilities are accounted to be $463.4 million for the year 2017 in contrast to $434.4

million observed in the year 2016. Recognition focused on conducted deferred tax is carried out

for the reason that high amount of depreciation is experienced because of variations in taxable

depreciation rate along with depreciation amount. Deferred tax liabilities recognition is carried

out because of temporary changes in the profits. This is because of which Virgin Australia

Company is evidenced to attain tax exemptions in the year 2016 as well as 2017 (Mintz 2016).

Answer to Question (ix):

Payable income tax or the current tax asset is deemed as a vital factor for the Australian

business firms. Considering the information provided in the annual report of Virgin Australia, it

is gathered that the current tax assets include the anticipated tax payable. This also includes

certain receivables on taxable loss or income for a particular period. These are measured with the

support of tax rates along with tax laws enacted at the financial year. However, considering the

situation of Virgin Australia it has been observed that the company has attained income tax

advantages of $201.9 million 2016 and $103.8 million in 2017 (Collins, Hribar And Tian 2014).

Moreover, an identical amount has been is reported in the part of reconciliation of the net loss to

the net cash from the business operations within the yearly report of the company. The vital

cause that is indicated by these two items is the same values for the reason that there are no

excess expenses experienced on the behalf of the company in these two years (Parsa et al. 2018).

The utilization of cash flow hedging is conducted at the time a company intends to decrease the

exposure taking place because of variations in cash flow of a liability or asset as certain changes

8CORPORATE ACCOUNTINGIN VIRGIN GROUP

in particular risk like rate of interest on debt instrument is associated with the floating rate. In

addition, the income tax expense serves the incurred amount on profit before tax of the company.

Answer to Question(x):

In accordance with the yearly report of the Virgin Australia in the year 2017, it might

also be gathered that the company has not experienced any expense related with the income tax

for the years over 2016 and 2017. Rather than that, it has also attained income tax advantage in

the mentioned years (Christensen 2015). In addition, this is the major cause for which the paid

income tax is not considered to be an item within the Virgin Australia company’s statement of

cash flow. Virgin Australia is chosen as a company that is positioned as mong the renowned

airline organization within Australia and is listed within the Australian Securities Exchange

(ASX) having a code of VAH. The cash flow statement of the company is segmented within

investing, financing and operating activities.

Answer to Question (xi):

After accomplishing critical evacuation of the Virgin Australia’s tax treatment, the most

influential item of the financial statement is recognised to be the fact that the company has

experienced loss before incurrent income tax expense over the years from 2016 and 2017. This is

the major reason for which it has attained income tax advantages. For this reason, it has turned

out to be quite complex to associate the real tax income that is paid along with consideration to

existing rate of tax in the country (Cañibano 2017). In addition, as no income tax income

expense has been experienced. There is no mentioning of the income tax paid within the country.

Along with that, considering the fact that no income tax expense has been implemented there is

no mentioning of incurred income tax within Virgin Australia Company’s cash flow statement.

in particular risk like rate of interest on debt instrument is associated with the floating rate. In

addition, the income tax expense serves the incurred amount on profit before tax of the company.

Answer to Question(x):

In accordance with the yearly report of the Virgin Australia in the year 2017, it might

also be gathered that the company has not experienced any expense related with the income tax

for the years over 2016 and 2017. Rather than that, it has also attained income tax advantage in

the mentioned years (Christensen 2015). In addition, this is the major cause for which the paid

income tax is not considered to be an item within the Virgin Australia company’s statement of

cash flow. Virgin Australia is chosen as a company that is positioned as mong the renowned

airline organization within Australia and is listed within the Australian Securities Exchange

(ASX) having a code of VAH. The cash flow statement of the company is segmented within

investing, financing and operating activities.

Answer to Question (xi):

After accomplishing critical evacuation of the Virgin Australia’s tax treatment, the most

influential item of the financial statement is recognised to be the fact that the company has

experienced loss before incurrent income tax expense over the years from 2016 and 2017. This is

the major reason for which it has attained income tax advantages. For this reason, it has turned

out to be quite complex to associate the real tax income that is paid along with consideration to

existing rate of tax in the country (Cañibano 2017). In addition, as no income tax income

expense has been experienced. There is no mentioning of the income tax paid within the country.

Along with that, considering the fact that no income tax expense has been implemented there is

no mentioning of incurred income tax within Virgin Australia Company’s cash flow statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTINGIN VIRGIN GROUP

Conversely, it has also been made for important disclosures regarding the benefits of income tax

gathered. This has also facilitated in attaining knowledge regarding the treatment of tax.

Conversely, it has also been made for important disclosures regarding the benefits of income tax

gathered. This has also facilitated in attaining knowledge regarding the treatment of tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTINGIN VIRGIN GROUP

References:

Bennedsen, M., and Zeume, S., 2017. Corporate tax havens and transparency. The Review of

Financial Studies, 31(4), 1221-1264.

Burrell, G. and Morgan, G., 2017. Sociological paradigms and organisational analysis:

Elements of the sociology of corporate life. Routledge.

Cañibano, L., 2017. Accounting and intangibles.

Christensen, D.M., 2015. Corporate accountability reporting and high-profile misconduct. The

Accounting Review, 91(2), pp.377-399.

Collins, D. W., Hribar, P. And Tian, X. S., 2014. Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics, 58(2-3), 173-200.

Dechow, P.M. and Tan, S.T., 2017. How Do Accounting Practices Spread? An Examination of

Law Firm Networks and Stock Option Backdating.

DeZoort, F.T., Wilkins, A. and Justice, S.E., 2017. Call for papers: The limits of accounting

regulation. Journal of Accounting and Public Policy, 45, p.30Z.

Ebrahim, A. and Fattah, T.A., 2015. Journal of International Accounting, Auditing and

Taxation. Journal of International Accounting, Auditing and Taxation, 24, pp.46-60.

Ferri, F. and Göx, R.F., 2018. Executive Compensation, Corporate Governance, and Say on

Pay. Foundations and Trends® in Accounting, 12(1), pp.1-103.

References:

Bennedsen, M., and Zeume, S., 2017. Corporate tax havens and transparency. The Review of

Financial Studies, 31(4), 1221-1264.

Burrell, G. and Morgan, G., 2017. Sociological paradigms and organisational analysis:

Elements of the sociology of corporate life. Routledge.

Cañibano, L., 2017. Accounting and intangibles.

Christensen, D.M., 2015. Corporate accountability reporting and high-profile misconduct. The

Accounting Review, 91(2), pp.377-399.

Collins, D. W., Hribar, P. And Tian, X. S., 2014. Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics, 58(2-3), 173-200.

Dechow, P.M. and Tan, S.T., 2017. How Do Accounting Practices Spread? An Examination of

Law Firm Networks and Stock Option Backdating.

DeZoort, F.T., Wilkins, A. and Justice, S.E., 2017. Call for papers: The limits of accounting

regulation. Journal of Accounting and Public Policy, 45, p.30Z.

Ebrahim, A. and Fattah, T.A., 2015. Journal of International Accounting, Auditing and

Taxation. Journal of International Accounting, Auditing and Taxation, 24, pp.46-60.

Ferri, F. and Göx, R.F., 2018. Executive Compensation, Corporate Governance, and Say on

Pay. Foundations and Trends® in Accounting, 12(1), pp.1-103.

11CORPORATE ACCOUNTINGIN VIRGIN GROUP

Houdet, J., Quétier, F. and Ding, H., 2016. Net impact accounting for renewable natural capital.

Possible pathways for corporate level disclosure. Working paper 2016-01—Synergiz, African

Centre for Technology Studies, University of Pretoria—Albert Luthuli Centre for Responsible

Leadership, & Integrated Sustainability Services.

Leary, M.T. and Roberts, M.R., 2014. Do peer firms affect corporate financial policy?. The

Journal of Finance, 69(1), pp.139-178.

Lian, Q., Rupley, K., Wang, Q. and Zheng, L., 2017. Corporate social responsibility and

accounting restatements.

Miao, B., Teoh, S. H. And Zhu, Z., 2016. Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), 473-515.

Mintz, S., 2016. Accounting for the public interest. Springer,.

Parsa, S., Roper, I., Muller-Camen, M. and Szigetvari, E., 2018, January. Have labour practices

and human rights disclosures enhanced corporate accountability? The case of the GRI

framework. In Accounting Forum. Elsevier.

Virginaustralia.com., 2018. Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/

2017-annual-report.pdf

Houdet, J., Quétier, F. and Ding, H., 2016. Net impact accounting for renewable natural capital.

Possible pathways for corporate level disclosure. Working paper 2016-01—Synergiz, African

Centre for Technology Studies, University of Pretoria—Albert Luthuli Centre for Responsible

Leadership, & Integrated Sustainability Services.

Leary, M.T. and Roberts, M.R., 2014. Do peer firms affect corporate financial policy?. The

Journal of Finance, 69(1), pp.139-178.

Lian, Q., Rupley, K., Wang, Q. and Zheng, L., 2017. Corporate social responsibility and

accounting restatements.

Miao, B., Teoh, S. H. And Zhu, Z., 2016. Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), 473-515.

Mintz, S., 2016. Accounting for the public interest. Springer,.

Parsa, S., Roper, I., Muller-Camen, M. and Szigetvari, E., 2018, January. Have labour practices

and human rights disclosures enhanced corporate accountability? The case of the GRI

framework. In Accounting Forum. Elsevier.

Virginaustralia.com., 2018. Retrieved from

https://www.virginaustralia.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/

2017-annual-report.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.