Visa Inc. Credit Card Fraud: A Business Analysis Case Study

VerifiedAdded on 2020/05/04

|19

|3678

|412

Case Study

AI Summary

This case study examines credit card fraud at Visa Inc., a global financial services firm. The study investigates the occurrence of fraud across genders and age groups, differentiating between online and offline fraud. Data was collected from 420 customers using questionnaires, and ANOVA was used for hypothesis testing at a 95% significance level. Key findings reveal that fraud affects both males and females across different age groups. Customer satisfaction is influenced by the advice given by the resolution team. The study highlights the importance of educating customers on fraud prevention and the need for future research to address the methods of fraud occurrence. The analysis explores the impact of response time, communication, and advice on customer satisfaction with fraud resolution. The study concludes that while the average time taken for resolution is more than the set 12 hours, the occurrence of fraud is not limited to a specific gender or age group, emphasizing the need for comprehensive fraud prevention strategies.

FOUNDATIONS OF BUSINESS ANALYSIS

CASE STUDY – VISA INC

Course Name…………………………………………………..

School ……………………………………………………

Department…………………………………………….

Lecturer name…………………………………………………..

Task Name……………………………………………………

Date………………………………………………………………

CASE STUDY – VISA INC

Course Name…………………………………………………..

School ……………………………………………………

Department…………………………………………….

Lecturer name…………………………………………………..

Task Name……………………………………………………

Date………………………………………………………………

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Visa Inc. is one of the world’s largest retail electronic payments chains of network and it is one

of the most reputable global financial services firm. It enables world commerce via the transfer

of value and information among businesses, clients, lending institutions and government

departments.

Most of customers using the credit cards have been experiencing fraud on their cards. The called

for research on how the frauds occur? Is it online or offline? The study involved if this occurs to

both males and females? Is this credit card fraud across the age-groups? The satisfaction these

cards offer to customers and if the resolution team is effective?

The analysis of variance was used to test the hypothesis. The study was carried out at 95% level

of significance with alpha 0.05. Most of the factors being tested were important in the cub the

credit card fraud. Gender case fraud occurred in both males and females. The age-group was also

influenced across the youths to old. The customer satisfaction rating was most influenced by type

of advice given by the resolution team.

Credit card customer should be really advised on the loopholes through which the frauds occur.

Public awareness of different types of credit card frauds should be done. These will improve

them and lower their chances of being fraud.

The study didn’t address ways in which the fraud they occurred. Future studies should address

ways in which the fraud occurs if online how did they do it. Was it thus suspicious emails

addresses? Billing address or shipping address?

Visa Inc. is one of the world’s largest retail electronic payments chains of network and it is one

of the most reputable global financial services firm. It enables world commerce via the transfer

of value and information among businesses, clients, lending institutions and government

departments.

Most of customers using the credit cards have been experiencing fraud on their cards. The called

for research on how the frauds occur? Is it online or offline? The study involved if this occurs to

both males and females? Is this credit card fraud across the age-groups? The satisfaction these

cards offer to customers and if the resolution team is effective?

The analysis of variance was used to test the hypothesis. The study was carried out at 95% level

of significance with alpha 0.05. Most of the factors being tested were important in the cub the

credit card fraud. Gender case fraud occurred in both males and females. The age-group was also

influenced across the youths to old. The customer satisfaction rating was most influenced by type

of advice given by the resolution team.

Credit card customer should be really advised on the loopholes through which the frauds occur.

Public awareness of different types of credit card frauds should be done. These will improve

them and lower their chances of being fraud.

The study didn’t address ways in which the fraud they occurred. Future studies should address

ways in which the fraud occurs if online how did they do it. Was it thus suspicious emails

addresses? Billing address or shipping address?

Introduction

Visa Inc. is one of the most popular firms that allow transaction of small business. This gives

them a platform to transact for businesses, customers and other financial institutions. It allows

them to do transaction for enterprises, in doing so they face challenges such as credit card fraud.

The online fraud is an issue of concern that requires to be addressed. Visa Inc seeks knowledge

on its security measures and customers concern to credit card fraud. In order to improve

customers’ loyalty and trust the company needs to understand the source of online fraud and how

to counter it.

Objectives of the study

1. To determine number of fraud experienced in different genders.

2. To determine if age affects credit card’s fraud

3. To determine average time to resolve a credit’s card fraud.

4. To determine number of occurrence of a card fraud.

5. To determine occurrence of online and offline fraud.

Research design

Data on customer experience on personal fraud was collected. The sampling technique used to

sample from the population was simple random sampling. A total of 2000 customers were

selected. In the selected sample which consisted of 2000 customers, 420 responded. The

questionnaires were sent via email and mobile phone. The respondents’ ethic was upheld since

the personal information was not detailed. The research made use of survey method to obtain

descriptive and analytical data, (Perry & Perry, 2014).

Hypothesis

In the study the following hypothesis were tested

1. Do the number of credit card fraud experienced across gender

H0: Credit card fraud is affected by gender

H1: Credit card fraud is not affected by gender

2. Customers fraud resolution team experience is satisfying

Hypothesis;

H0: Customers fraud resolution team is satisfying

Visa Inc. is one of the most popular firms that allow transaction of small business. This gives

them a platform to transact for businesses, customers and other financial institutions. It allows

them to do transaction for enterprises, in doing so they face challenges such as credit card fraud.

The online fraud is an issue of concern that requires to be addressed. Visa Inc seeks knowledge

on its security measures and customers concern to credit card fraud. In order to improve

customers’ loyalty and trust the company needs to understand the source of online fraud and how

to counter it.

Objectives of the study

1. To determine number of fraud experienced in different genders.

2. To determine if age affects credit card’s fraud

3. To determine average time to resolve a credit’s card fraud.

4. To determine number of occurrence of a card fraud.

5. To determine occurrence of online and offline fraud.

Research design

Data on customer experience on personal fraud was collected. The sampling technique used to

sample from the population was simple random sampling. A total of 2000 customers were

selected. In the selected sample which consisted of 2000 customers, 420 responded. The

questionnaires were sent via email and mobile phone. The respondents’ ethic was upheld since

the personal information was not detailed. The research made use of survey method to obtain

descriptive and analytical data, (Perry & Perry, 2014).

Hypothesis

In the study the following hypothesis were tested

1. Do the number of credit card fraud experienced across gender

H0: Credit card fraud is affected by gender

H1: Credit card fraud is not affected by gender

2. Customers fraud resolution team experience is satisfying

Hypothesis;

H0: Customers fraud resolution team is satisfying

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

H1: Customer fraud resolution team is not satisfying

3. Do credit card fraud differ across age groups

Hypothesis;

H0: Card fraud differs across age groups.

H1: Card fraud does not differ across age groups.

4. Is the average time used in resolving a credit card fraud equal to 12 hours

Hypothesis;

H0: The mean time used in resolving a card fraud is 12 hours

H1: The mean time used in resolving a card fraud is not 12 hours

5. How likely is an online or offline fraud to occur

Hypothesis;

H0: an online or offline card fraud occur in 12hours

H1: an online or offline card fraud doesn’t occur in 12 hours

6. Do response time, level of communication and level of advice affects customer

satisfaction on fraud resolution

Hypothesis;

H0: Response time, level of communication and advice affects customer satisfaction

H1: Response time, level of communication and advice does not affect customer

satisfaction

Statistical analysis

The study used analysis of variance (ANOVA) and test of hypothesis in data analysis. The p-

value in the analysis of variance and comparing it with the level of significance helped in

3. Do credit card fraud differ across age groups

Hypothesis;

H0: Card fraud differs across age groups.

H1: Card fraud does not differ across age groups.

4. Is the average time used in resolving a credit card fraud equal to 12 hours

Hypothesis;

H0: The mean time used in resolving a card fraud is 12 hours

H1: The mean time used in resolving a card fraud is not 12 hours

5. How likely is an online or offline fraud to occur

Hypothesis;

H0: an online or offline card fraud occur in 12hours

H1: an online or offline card fraud doesn’t occur in 12 hours

6. Do response time, level of communication and level of advice affects customer

satisfaction on fraud resolution

Hypothesis;

H0: Response time, level of communication and advice affects customer satisfaction

H1: Response time, level of communication and advice does not affect customer

satisfaction

Statistical analysis

The study used analysis of variance (ANOVA) and test of hypothesis in data analysis. The p-

value in the analysis of variance and comparing it with the level of significance helped in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

rejecting the null hypothesis or failing to reject the null hypothesis. If the p-value calculated was

less than the level of significance we reject null hypothesis and p-value calculated is greater than

the level of significance we thus fail to reject the null hypothesis, (Neuman, 2004).

Results, and Statistical and non-statistical Interpretation

Descriptive statistics

Data analysis was done using inferential statistics and descriptive statistics, (Kothari, 2004).

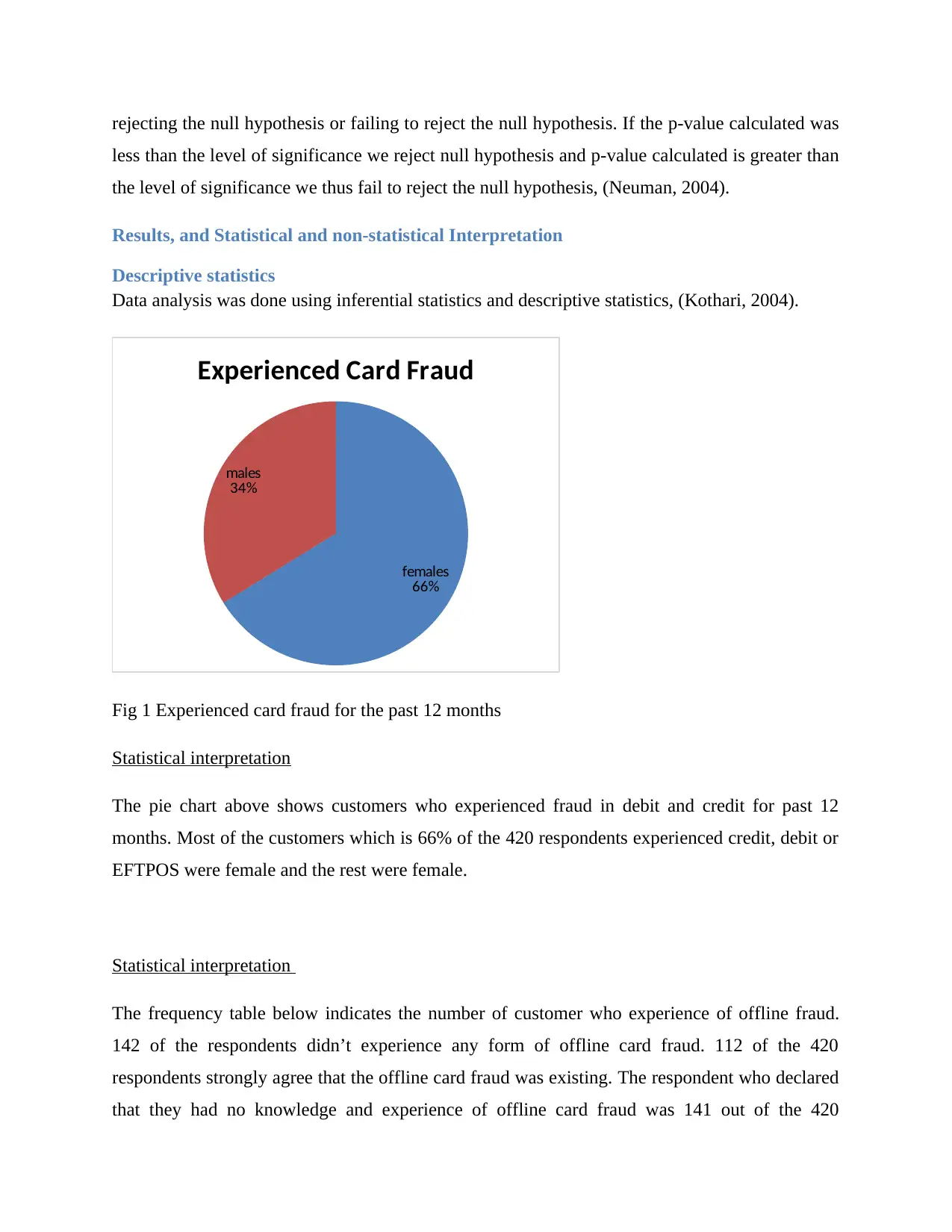

females

66%

males

34%

Experienced Card Fraud

Fig 1 Experienced card fraud for the past 12 months

Statistical interpretation

The pie chart above shows customers who experienced fraud in debit and credit for past 12

months. Most of the customers which is 66% of the 420 respondents experienced credit, debit or

EFTPOS were female and the rest were female.

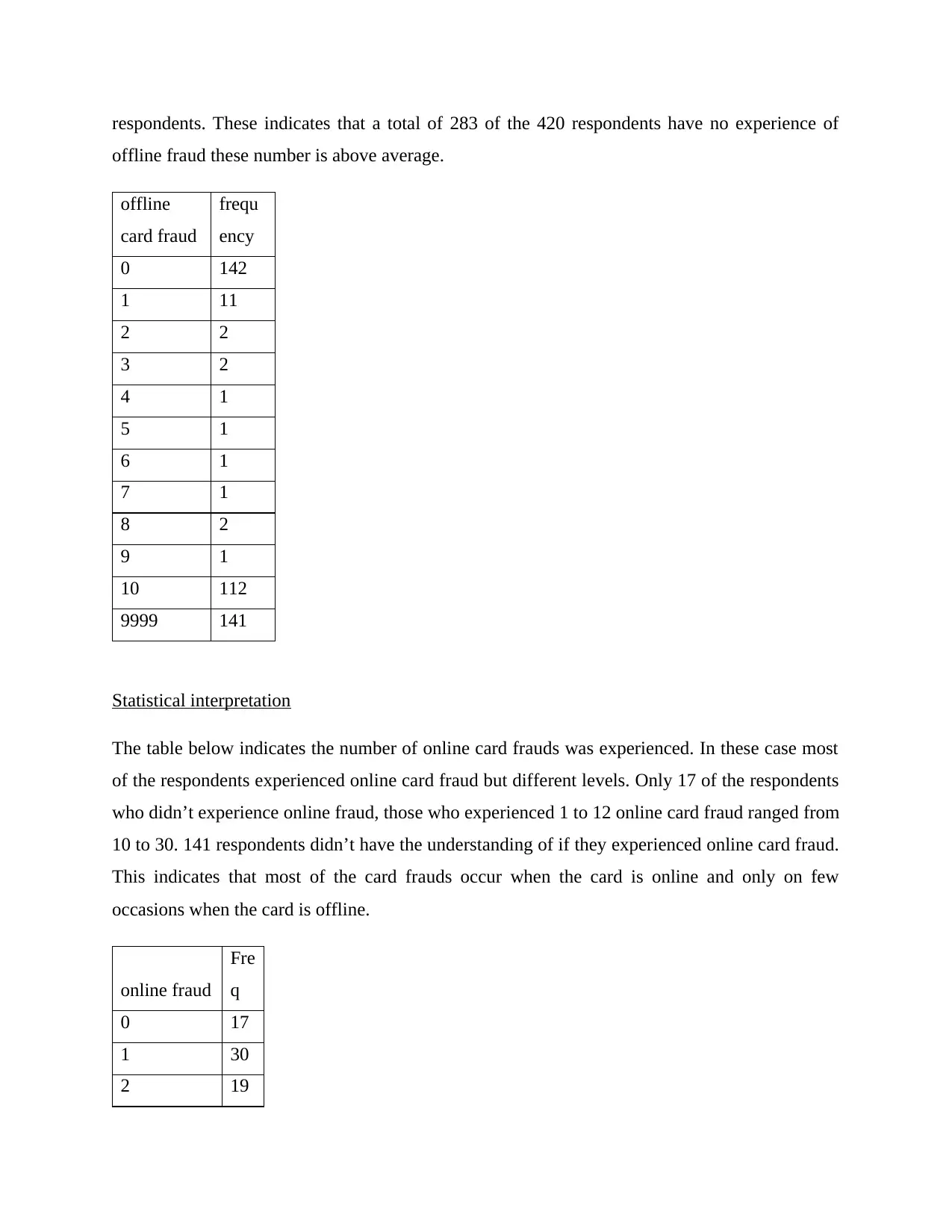

Statistical interpretation

The frequency table below indicates the number of customer who experience of offline fraud.

142 of the respondents didn’t experience any form of offline card fraud. 112 of the 420

respondents strongly agree that the offline card fraud was existing. The respondent who declared

that they had no knowledge and experience of offline card fraud was 141 out of the 420

less than the level of significance we reject null hypothesis and p-value calculated is greater than

the level of significance we thus fail to reject the null hypothesis, (Neuman, 2004).

Results, and Statistical and non-statistical Interpretation

Descriptive statistics

Data analysis was done using inferential statistics and descriptive statistics, (Kothari, 2004).

females

66%

males

34%

Experienced Card Fraud

Fig 1 Experienced card fraud for the past 12 months

Statistical interpretation

The pie chart above shows customers who experienced fraud in debit and credit for past 12

months. Most of the customers which is 66% of the 420 respondents experienced credit, debit or

EFTPOS were female and the rest were female.

Statistical interpretation

The frequency table below indicates the number of customer who experience of offline fraud.

142 of the respondents didn’t experience any form of offline card fraud. 112 of the 420

respondents strongly agree that the offline card fraud was existing. The respondent who declared

that they had no knowledge and experience of offline card fraud was 141 out of the 420

respondents. These indicates that a total of 283 of the 420 respondents have no experience of

offline fraud these number is above average.

offline

card fraud

frequ

ency

0 142

1 11

2 2

3 2

4 1

5 1

6 1

7 1

8 2

9 1

10 112

9999 141

Statistical interpretation

The table below indicates the number of online card frauds was experienced. In these case most

of the respondents experienced online card fraud but different levels. Only 17 of the respondents

who didn’t experience online fraud, those who experienced 1 to 12 online card fraud ranged from

10 to 30. 141 respondents didn’t have the understanding of if they experienced online card fraud.

This indicates that most of the card frauds occur when the card is online and only on few

occasions when the card is offline.

online fraud

Fre

q

0 17

1 30

2 19

offline fraud these number is above average.

offline

card fraud

frequ

ency

0 142

1 11

2 2

3 2

4 1

5 1

6 1

7 1

8 2

9 1

10 112

9999 141

Statistical interpretation

The table below indicates the number of online card frauds was experienced. In these case most

of the respondents experienced online card fraud but different levels. Only 17 of the respondents

who didn’t experience online fraud, those who experienced 1 to 12 online card fraud ranged from

10 to 30. 141 respondents didn’t have the understanding of if they experienced online card fraud.

This indicates that most of the card frauds occur when the card is online and only on few

occasions when the card is offline.

online fraud

Fre

q

0 17

1 30

2 19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

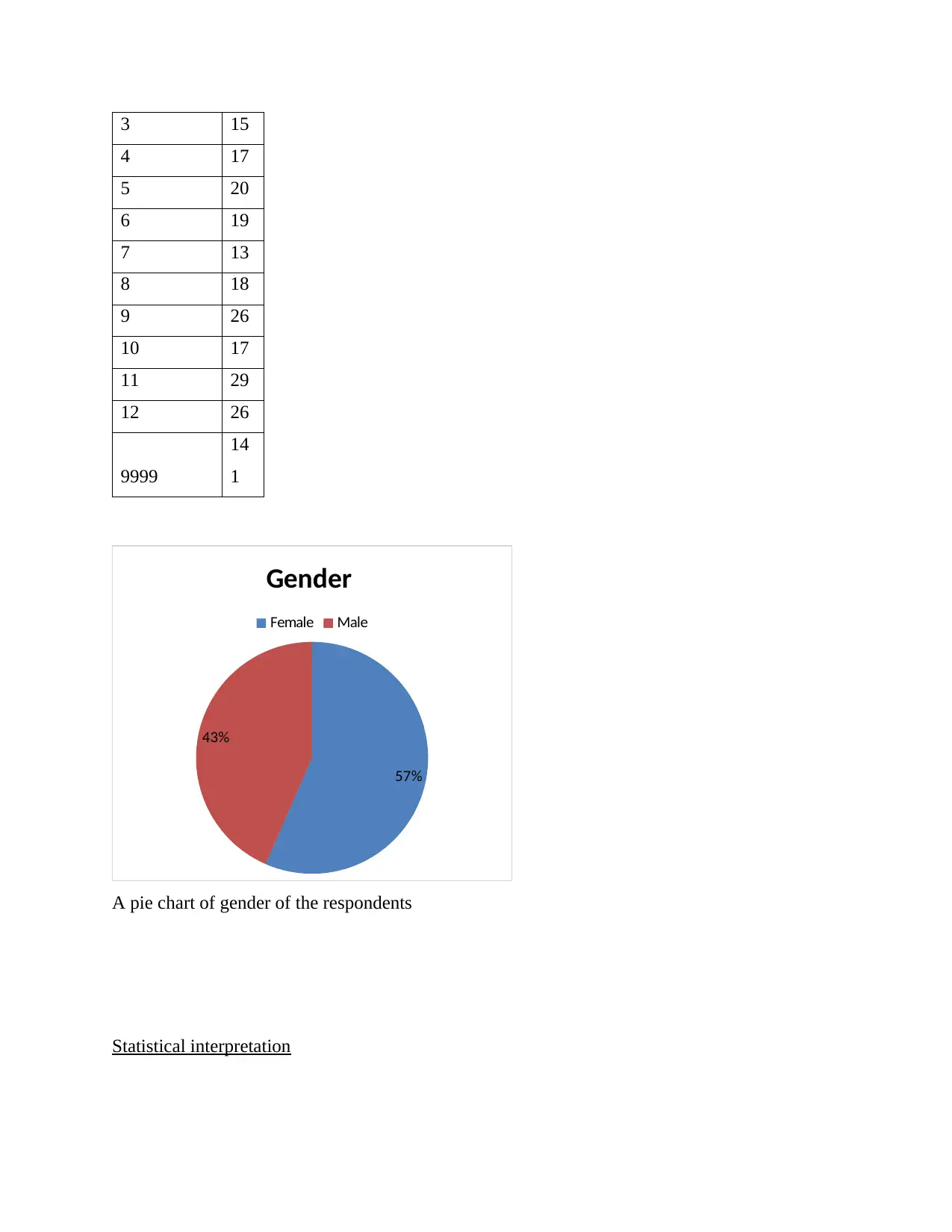

3 15

4 17

5 20

6 19

7 13

8 18

9 26

10 17

11 29

12 26

9999

14

1

A pie chart of gender of the respondents

Statistical interpretation

57%

43%

Gender

Female Male

4 17

5 20

6 19

7 13

8 18

9 26

10 17

11 29

12 26

9999

14

1

A pie chart of gender of the respondents

Statistical interpretation

57%

43%

Gender

Female Male

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

57% of the respondents were females while 43% of the respondents were males. Out of the 420

respondents 237 of them were females while 182 of them were males. These indicate the

majority of the respondents were female.

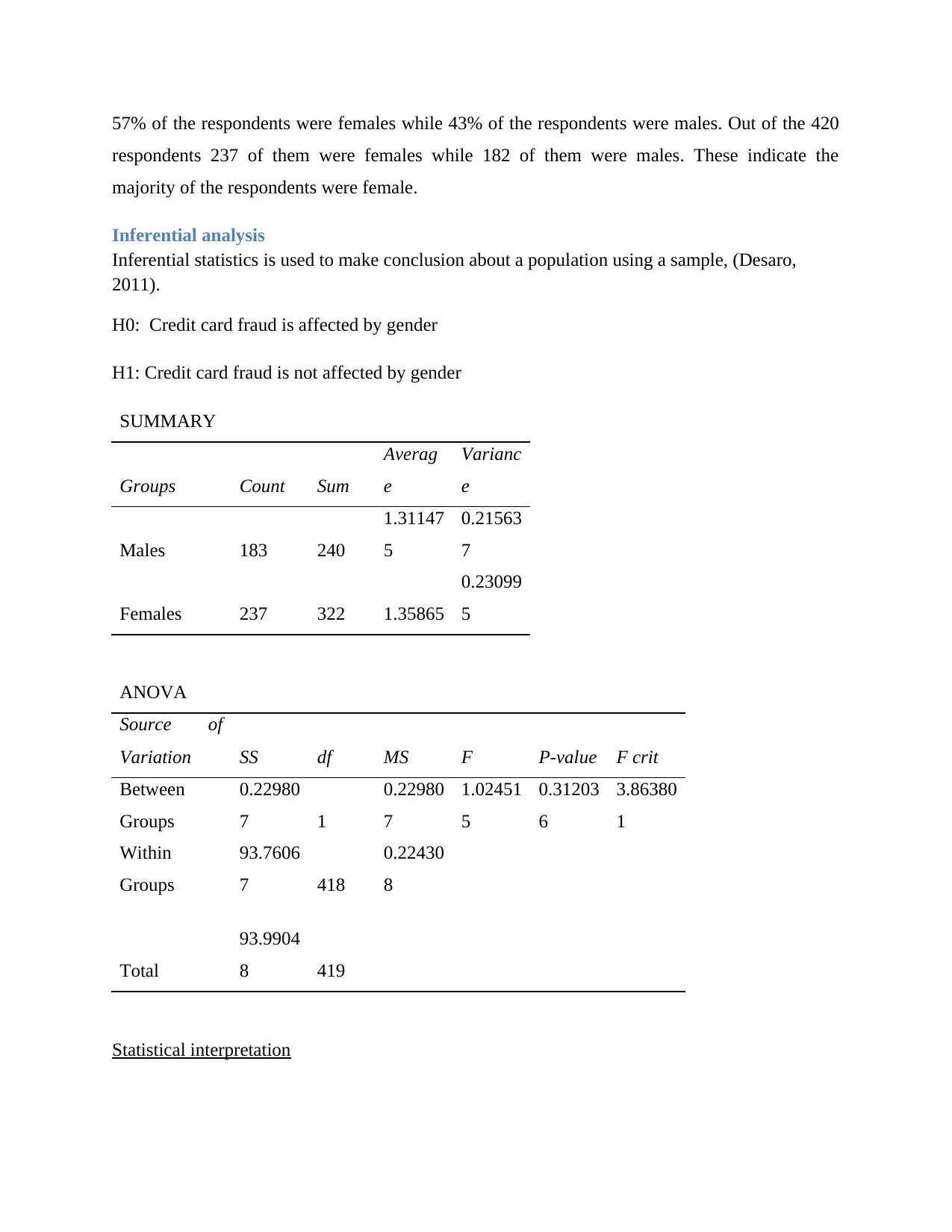

Inferential analysis

Inferential statistics is used to make conclusion about a population using a sample, (Desaro,

2011).

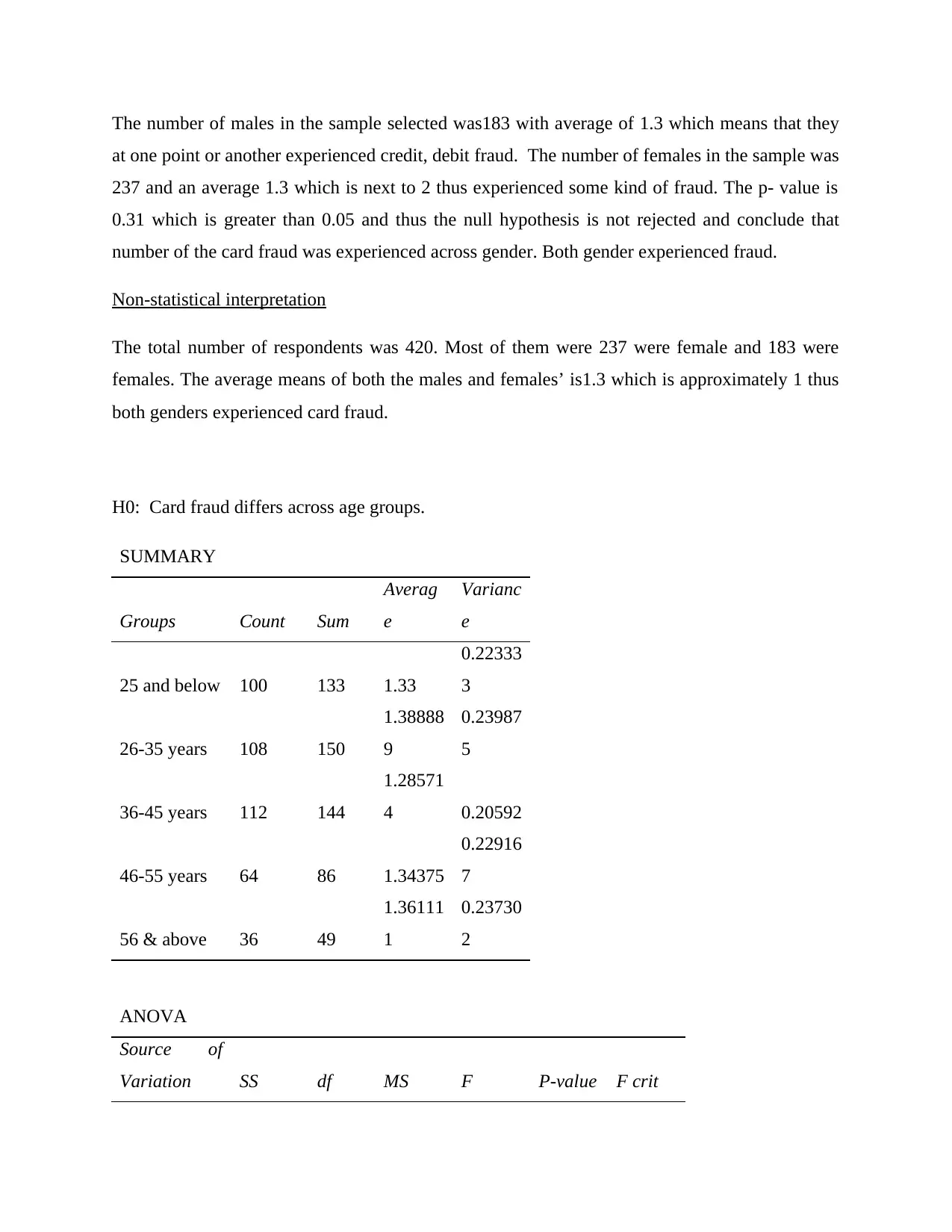

H0: Credit card fraud is affected by gender

H1: Credit card fraud is not affected by gender

SUMMARY

Groups Count Sum

Averag

e

Varianc

e

Males 183 240

1.31147

5

0.21563

7

Females 237 322 1.35865

0.23099

5

ANOVA

Source of

Variation SS df MS F P-value F crit

Between

Groups

0.22980

7 1

0.22980

7

1.02451

5

0.31203

6

3.86380

1

Within

Groups

93.7606

7 418

0.22430

8

Total

93.9904

8 419

Statistical interpretation

respondents 237 of them were females while 182 of them were males. These indicate the

majority of the respondents were female.

Inferential analysis

Inferential statistics is used to make conclusion about a population using a sample, (Desaro,

2011).

H0: Credit card fraud is affected by gender

H1: Credit card fraud is not affected by gender

SUMMARY

Groups Count Sum

Averag

e

Varianc

e

Males 183 240

1.31147

5

0.21563

7

Females 237 322 1.35865

0.23099

5

ANOVA

Source of

Variation SS df MS F P-value F crit

Between

Groups

0.22980

7 1

0.22980

7

1.02451

5

0.31203

6

3.86380

1

Within

Groups

93.7606

7 418

0.22430

8

Total

93.9904

8 419

Statistical interpretation

The number of males in the sample selected was183 with average of 1.3 which means that they

at one point or another experienced credit, debit fraud. The number of females in the sample was

237 and an average 1.3 which is next to 2 thus experienced some kind of fraud. The p- value is

0.31 which is greater than 0.05 and thus the null hypothesis is not rejected and conclude that

number of the card fraud was experienced across gender. Both gender experienced fraud.

Non-statistical interpretation

The total number of respondents was 420. Most of them were 237 were female and 183 were

females. The average means of both the males and females’ is1.3 which is approximately 1 thus

both genders experienced card fraud.

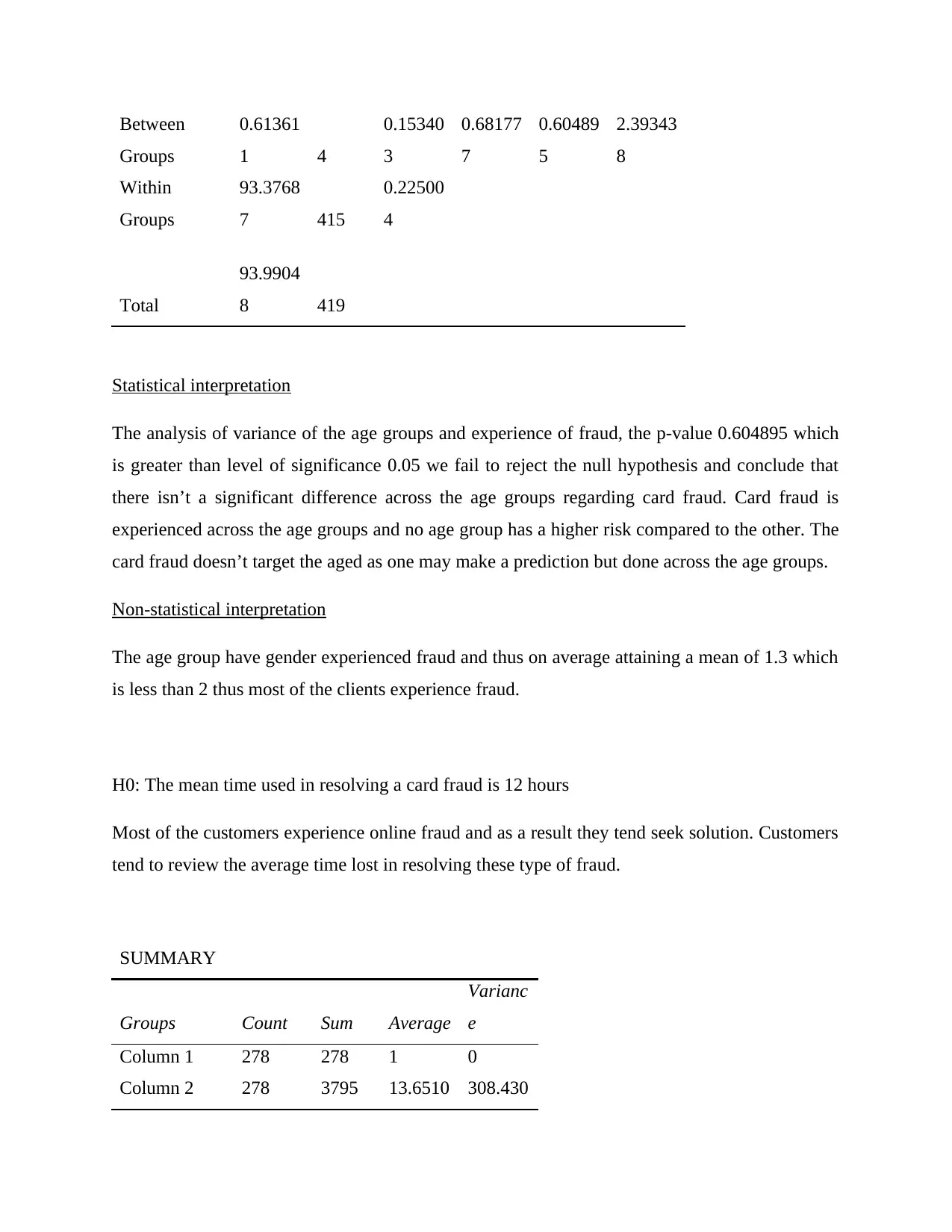

H0: Card fraud differs across age groups.

SUMMARY

Groups Count Sum

Averag

e

Varianc

e

25 and below 100 133 1.33

0.22333

3

26-35 years 108 150

1.38888

9

0.23987

5

36-45 years 112 144

1.28571

4 0.20592

46-55 years 64 86 1.34375

0.22916

7

56 & above 36 49

1.36111

1

0.23730

2

ANOVA

Source of

Variation SS df MS F P-value F crit

at one point or another experienced credit, debit fraud. The number of females in the sample was

237 and an average 1.3 which is next to 2 thus experienced some kind of fraud. The p- value is

0.31 which is greater than 0.05 and thus the null hypothesis is not rejected and conclude that

number of the card fraud was experienced across gender. Both gender experienced fraud.

Non-statistical interpretation

The total number of respondents was 420. Most of them were 237 were female and 183 were

females. The average means of both the males and females’ is1.3 which is approximately 1 thus

both genders experienced card fraud.

H0: Card fraud differs across age groups.

SUMMARY

Groups Count Sum

Averag

e

Varianc

e

25 and below 100 133 1.33

0.22333

3

26-35 years 108 150

1.38888

9

0.23987

5

36-45 years 112 144

1.28571

4 0.20592

46-55 years 64 86 1.34375

0.22916

7

56 & above 36 49

1.36111

1

0.23730

2

ANOVA

Source of

Variation SS df MS F P-value F crit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Between

Groups

0.61361

1 4

0.15340

3

0.68177

7

0.60489

5

2.39343

8

Within

Groups

93.3768

7 415

0.22500

4

Total

93.9904

8 419

Statistical interpretation

The analysis of variance of the age groups and experience of fraud, the p-value 0.604895 which

is greater than level of significance 0.05 we fail to reject the null hypothesis and conclude that

there isn’t a significant difference across the age groups regarding card fraud. Card fraud is

experienced across the age groups and no age group has a higher risk compared to the other. The

card fraud doesn’t target the aged as one may make a prediction but done across the age groups.

Non-statistical interpretation

The age group have gender experienced fraud and thus on average attaining a mean of 1.3 which

is less than 2 thus most of the clients experience fraud.

H0: The mean time used in resolving a card fraud is 12 hours

Most of the customers experience online fraud and as a result they tend seek solution. Customers

tend to review the average time lost in resolving these type of fraud.

SUMMARY

Groups Count Sum Average

Varianc

e

Column 1 278 278 1 0

Column 2 278 3795 13.6510 308.430

Groups

0.61361

1 4

0.15340

3

0.68177

7

0.60489

5

2.39343

8

Within

Groups

93.3768

7 415

0.22500

4

Total

93.9904

8 419

Statistical interpretation

The analysis of variance of the age groups and experience of fraud, the p-value 0.604895 which

is greater than level of significance 0.05 we fail to reject the null hypothesis and conclude that

there isn’t a significant difference across the age groups regarding card fraud. Card fraud is

experienced across the age groups and no age group has a higher risk compared to the other. The

card fraud doesn’t target the aged as one may make a prediction but done across the age groups.

Non-statistical interpretation

The age group have gender experienced fraud and thus on average attaining a mean of 1.3 which

is less than 2 thus most of the clients experience fraud.

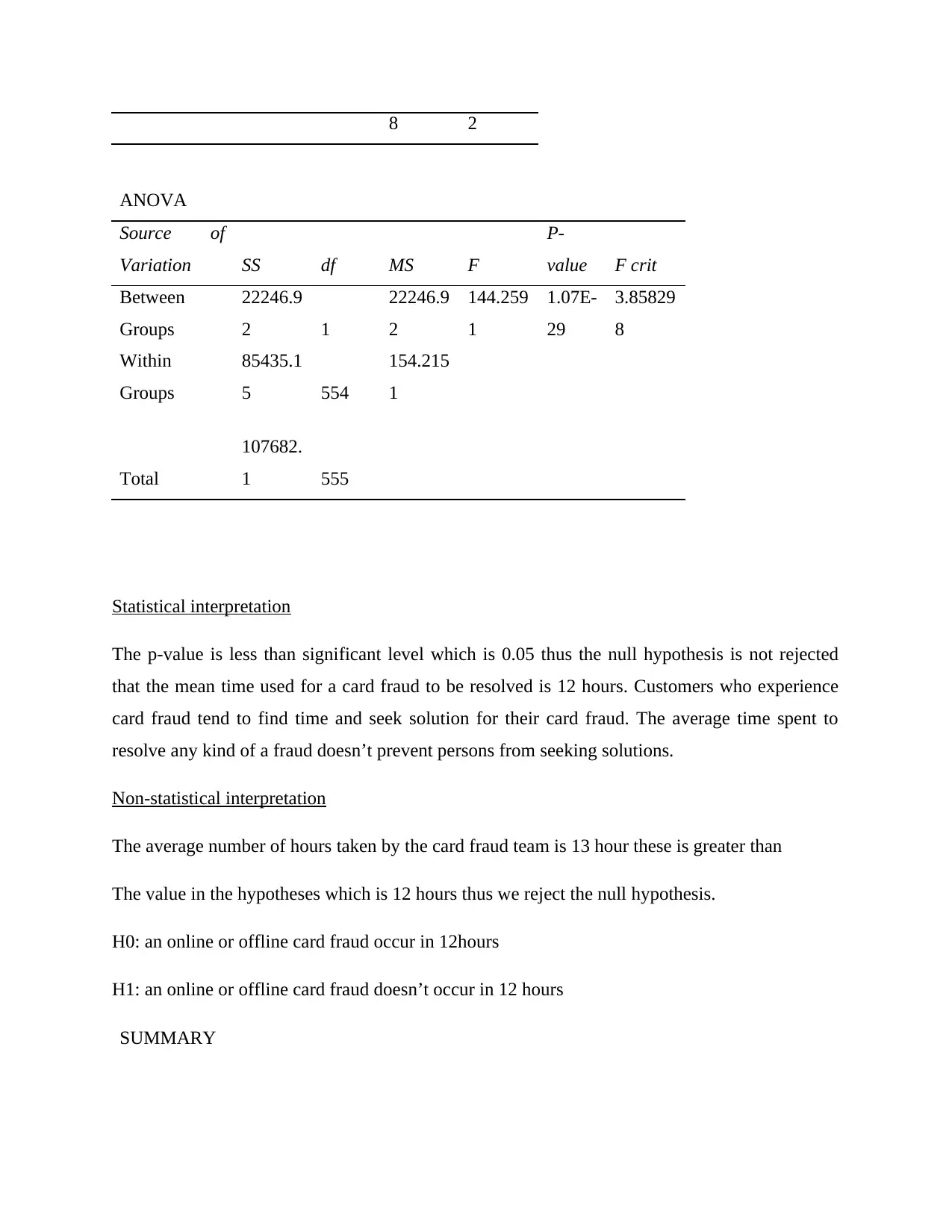

H0: The mean time used in resolving a card fraud is 12 hours

Most of the customers experience online fraud and as a result they tend seek solution. Customers

tend to review the average time lost in resolving these type of fraud.

SUMMARY

Groups Count Sum Average

Varianc

e

Column 1 278 278 1 0

Column 2 278 3795 13.6510 308.430

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 2

ANOVA

Source of

Variation SS df MS F

P-

value F crit

Between

Groups

22246.9

2 1

22246.9

2

144.259

1

1.07E-

29

3.85829

8

Within

Groups

85435.1

5 554

154.215

1

Total

107682.

1 555

Statistical interpretation

The p-value is less than significant level which is 0.05 thus the null hypothesis is not rejected

that the mean time used for a card fraud to be resolved is 12 hours. Customers who experience

card fraud tend to find time and seek solution for their card fraud. The average time spent to

resolve any kind of a fraud doesn’t prevent persons from seeking solutions.

Non-statistical interpretation

The average number of hours taken by the card fraud team is 13 hour these is greater than

The value in the hypotheses which is 12 hours thus we reject the null hypothesis.

H0: an online or offline card fraud occur in 12hours

H1: an online or offline card fraud doesn’t occur in 12 hours

SUMMARY

ANOVA

Source of

Variation SS df MS F

P-

value F crit

Between

Groups

22246.9

2 1

22246.9

2

144.259

1

1.07E-

29

3.85829

8

Within

Groups

85435.1

5 554

154.215

1

Total

107682.

1 555

Statistical interpretation

The p-value is less than significant level which is 0.05 thus the null hypothesis is not rejected

that the mean time used for a card fraud to be resolved is 12 hours. Customers who experience

card fraud tend to find time and seek solution for their card fraud. The average time spent to

resolve any kind of a fraud doesn’t prevent persons from seeking solutions.

Non-statistical interpretation

The average number of hours taken by the card fraud team is 13 hour these is greater than

The value in the hypotheses which is 12 hours thus we reject the null hypothesis.

H0: an online or offline card fraud occur in 12hours

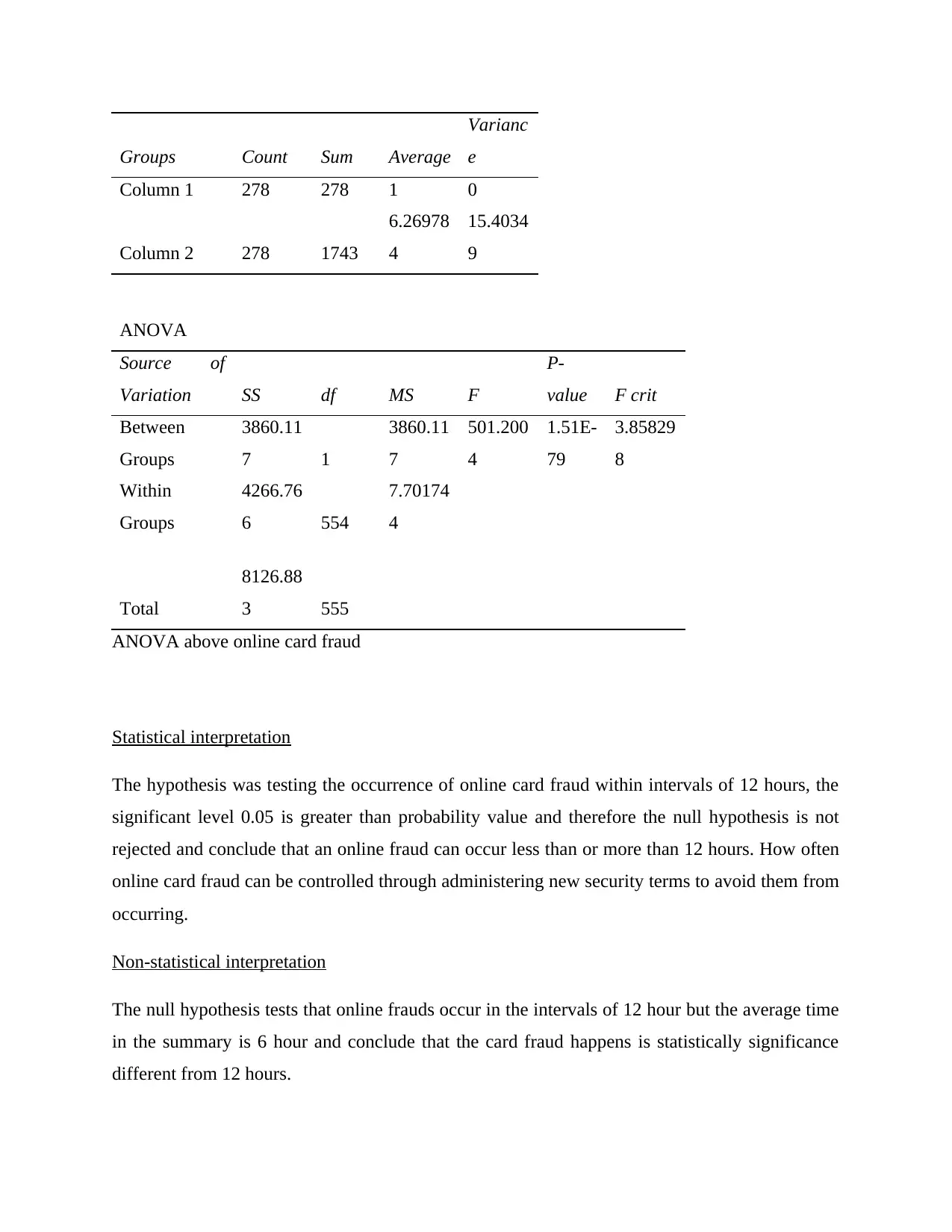

H1: an online or offline card fraud doesn’t occur in 12 hours

SUMMARY

Groups Count Sum Average

Varianc

e

Column 1 278 278 1 0

Column 2 278 1743

6.26978

4

15.4034

9

ANOVA

Source of

Variation SS df MS F

P-

value F crit

Between

Groups

3860.11

7 1

3860.11

7

501.200

4

1.51E-

79

3.85829

8

Within

Groups

4266.76

6 554

7.70174

4

Total

8126.88

3 555

ANOVA above online card fraud

Statistical interpretation

The hypothesis was testing the occurrence of online card fraud within intervals of 12 hours, the

significant level 0.05 is greater than probability value and therefore the null hypothesis is not

rejected and conclude that an online fraud can occur less than or more than 12 hours. How often

online card fraud can be controlled through administering new security terms to avoid them from

occurring.

Non-statistical interpretation

The null hypothesis tests that online frauds occur in the intervals of 12 hour but the average time

in the summary is 6 hour and conclude that the card fraud happens is statistically significance

different from 12 hours.

Varianc

e

Column 1 278 278 1 0

Column 2 278 1743

6.26978

4

15.4034

9

ANOVA

Source of

Variation SS df MS F

P-

value F crit

Between

Groups

3860.11

7 1

3860.11

7

501.200

4

1.51E-

79

3.85829

8

Within

Groups

4266.76

6 554

7.70174

4

Total

8126.88

3 555

ANOVA above online card fraud

Statistical interpretation

The hypothesis was testing the occurrence of online card fraud within intervals of 12 hours, the

significant level 0.05 is greater than probability value and therefore the null hypothesis is not

rejected and conclude that an online fraud can occur less than or more than 12 hours. How often

online card fraud can be controlled through administering new security terms to avoid them from

occurring.

Non-statistical interpretation

The null hypothesis tests that online frauds occur in the intervals of 12 hour but the average time

in the summary is 6 hour and conclude that the card fraud happens is statistically significance

different from 12 hours.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.