Comprehensive Analysis of Credit Card Fraud at Visa Inc. (2017)

VerifiedAdded on 2020/04/21

|18

|3826

|267

Report

AI Summary

This report analyzes credit card fraud at Visa Inc., based on a study of 420 participants. The research employed various statistical techniques to examine fraud patterns, customer experiences, and the effectiveness of Visa's security systems. Key findings reveal an average resolution time exceeding the acceptable 12 hours, a higher incidence of online fraud compared to offline, and the impact of response time and advice on customer satisfaction. The study found no significant difference in fraud experiences between male and female customers. The report recommends improving response times, focusing on reducing online fraud, and continuing to enhance customer service, offering data-driven insights and actionable recommendations to improve Visa's services and security measures. The report includes statistical interpretations, non-statistical interpretations, and detailed analysis of the findings, supporting the recommendations provided for the management of Visa Inc.

Business Data Analysis

Student Name:

Student Number:

Lecturer Name:

9th November 2017

1

Student Name:

Student Number:

Lecturer Name:

9th November 2017

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

Research Design..............................................................................................................................6

Hypothesis Development.................................................................................................................6

Statistical Technique and Justification............................................................................................8

Results, and Statistical and non-statistical Interpretation................................................................9

Analysis and Summary of the Statistical Results..........................................................................14

Recommendations..........................................................................................................................15

References......................................................................................................................................16

2

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

Research Design..............................................................................................................................6

Hypothesis Development.................................................................................................................6

Statistical Technique and Justification............................................................................................8

Results, and Statistical and non-statistical Interpretation................................................................9

Analysis and Summary of the Statistical Results..........................................................................14

Recommendations..........................................................................................................................15

References......................................................................................................................................16

2

Executive Summary

This aim of this study was to analyze the credit fraud and identify areas in which the Visa Inc.

can improve in their services. A sample of 420 participants was used. Various statistical analysis

approaches were employed to analyze the data. Results showed that the average time lost in

resolving a card fraud was found to be 13.65 hours (this is higher than the acceptable time of 12

hours). We also found that the number of online credit fraud were significantly more as

compared to the number of offline credit fraud. Lastly, two independent variables were found to

significantly predict the overall satisfaction of the customers. The two are the response time and

the level of advice. We then suggested the following recommendations to the management of

Visa Inc.

Improve on response time; currently the response time is more than the acceptable time

of 12 hours. The management should see on how this time comes down to at most 12

hours.

Focus more on h0w to decrease the number of online card fraud since it was established

that the online transactions are more vulnerable to fraud compared to offline transactions.

Continue working on response time and the level of advice given to the customers as they

have an impact on the overall customers’ satisfaction levels.

However, based on the results obtained, both the female and the male clients need to be accorded

equal protection in regard to credit fraud. Results showed that there is no significant difference in

the number of frauds experienced by the males and the females.

3

This aim of this study was to analyze the credit fraud and identify areas in which the Visa Inc.

can improve in their services. A sample of 420 participants was used. Various statistical analysis

approaches were employed to analyze the data. Results showed that the average time lost in

resolving a card fraud was found to be 13.65 hours (this is higher than the acceptable time of 12

hours). We also found that the number of online credit fraud were significantly more as

compared to the number of offline credit fraud. Lastly, two independent variables were found to

significantly predict the overall satisfaction of the customers. The two are the response time and

the level of advice. We then suggested the following recommendations to the management of

Visa Inc.

Improve on response time; currently the response time is more than the acceptable time

of 12 hours. The management should see on how this time comes down to at most 12

hours.

Focus more on h0w to decrease the number of online card fraud since it was established

that the online transactions are more vulnerable to fraud compared to offline transactions.

Continue working on response time and the level of advice given to the customers as they

have an impact on the overall customers’ satisfaction levels.

However, based on the results obtained, both the female and the male clients need to be accorded

equal protection in regard to credit fraud. Results showed that there is no significant difference in

the number of frauds experienced by the males and the females.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Frauds committed on credit cards proves to be one of the greatest dangers to business

foundations today. Notwithstanding, to battle the credit card fraud, it is essential to first

comprehend the systems of executing the credit fraud. The fraudsters employ a number of

methodologies to in executing their plans. Credit card fraud can be defined in simple terms as:

"A situation where an individual uses someone else’s card for his or her personal reasons at a

time when the card owner or the card issuer is not privy that the card is being used. Further, the

individual utilizing the card has no association with the cardholder or the issuer of the card, and

has no aim of either reaching the proprietor of the card or making reimbursements for the buys

made".

Frauds are committed in a number of ways;

A criminal act of deception (deceive with purpose) by utilization of unapproved account

or potentially individual data

Illegal and or unapproved account utilization for selfish gain.

Wrongly presenting account information so as to acquire merchandise as well as services.

In spite of mainstream thinking, merchants are much more in danger from frauds committed by

use of cards than the cardholders.

While shoppers may confront inconvenience attempting to get a deceitful charge turned around,

traders lose the cost of the item sold, pay chargeback expenses, and dread from the danger of

having closure of their merchant account.

4

Frauds committed on credit cards proves to be one of the greatest dangers to business

foundations today. Notwithstanding, to battle the credit card fraud, it is essential to first

comprehend the systems of executing the credit fraud. The fraudsters employ a number of

methodologies to in executing their plans. Credit card fraud can be defined in simple terms as:

"A situation where an individual uses someone else’s card for his or her personal reasons at a

time when the card owner or the card issuer is not privy that the card is being used. Further, the

individual utilizing the card has no association with the cardholder or the issuer of the card, and

has no aim of either reaching the proprietor of the card or making reimbursements for the buys

made".

Frauds are committed in a number of ways;

A criminal act of deception (deceive with purpose) by utilization of unapproved account

or potentially individual data

Illegal and or unapproved account utilization for selfish gain.

Wrongly presenting account information so as to acquire merchandise as well as services.

In spite of mainstream thinking, merchants are much more in danger from frauds committed by

use of cards than the cardholders.

While shoppers may confront inconvenience attempting to get a deceitful charge turned around,

traders lose the cost of the item sold, pay chargeback expenses, and dread from the danger of

having closure of their merchant account.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Visa Inc. operates the world's largest retail electronic payments network and is one of the most

recognized global financial services brands. It facilitates global commerce through the transfer of

value and information among financial institutions, merchants, consumers, businesses and

government entities. To address online fraud, Visa requires information on the effectiveness of

its online security system via customer experiences with fraudulent behaviors to maintain and/or

improve Visa’s market share.

The study sought to answer the following research questions:

1. Does the number of credit card frauds differ between the male and the female customers?

2. Does credit card fraud vary across the different age groups of the customers?

3. What is the average time lost in resolving a card fraud? If Visa Inc. has set a time-period

which is acceptable at 12 hours, will this be a significant improvement to the response

time compared to what customers have experienced before?

4. How often does an online or offline card fraud occur? Visa Inc. is willing to invest in an

updated online security which will decrease the number of online card fraud only if

online transactions are more vulnerable to fraud compared to offline transactions. What is

your recommendation?

5. Do any of the customers’ satisfaction scores of ‘response time’, ‘the level of advice’, and

‘the level of communication’ influence the overall satisfaction with the credit card fraud

resolution team?

5

recognized global financial services brands. It facilitates global commerce through the transfer of

value and information among financial institutions, merchants, consumers, businesses and

government entities. To address online fraud, Visa requires information on the effectiveness of

its online security system via customer experiences with fraudulent behaviors to maintain and/or

improve Visa’s market share.

The study sought to answer the following research questions:

1. Does the number of credit card frauds differ between the male and the female customers?

2. Does credit card fraud vary across the different age groups of the customers?

3. What is the average time lost in resolving a card fraud? If Visa Inc. has set a time-period

which is acceptable at 12 hours, will this be a significant improvement to the response

time compared to what customers have experienced before?

4. How often does an online or offline card fraud occur? Visa Inc. is willing to invest in an

updated online security which will decrease the number of online card fraud only if

online transactions are more vulnerable to fraud compared to offline transactions. What is

your recommendation?

5. Do any of the customers’ satisfaction scores of ‘response time’, ‘the level of advice’, and

‘the level of communication’ influence the overall satisfaction with the credit card fraud

resolution team?

5

Research Design

The design used for this study was both descriptive and analytical in nature (Shields &

Rangarajan, 2013). Data on assessing the effectiveness of Visa Inc. online security system as

well as assessing customer experience regarding personal fraud was collected. A simple random

sample of 2000 customers was selected. Surveys were sent to the respondents and only 420

responded.

The questionnaire comprised of a number of questions that attempted to know the opinions of the

respondents regarding their personal experience in relation to fraud as well as the effectiveness

of Visa Inc. online security system. The survey used to collect data is provided below and the

survey responses were collated in excel.

Hypothesis Development

In this section we present the hypothesis used for the study. The hypothesis were developed from

the research questions that the study sought to answer to answer.

1. Question 1: How many card frauds have been experienced by the male and the female

respondents?

Null hypothesis (H0): The average number of card frauds experienced by the males is equal to

that experienced by the females.

Alternate hypothesis (HA): The average number of card frauds experienced by the males is not

equal to that experienced by the females.

2. Question 2: Are there differences across the age groups regarding card fraud?

6

The design used for this study was both descriptive and analytical in nature (Shields &

Rangarajan, 2013). Data on assessing the effectiveness of Visa Inc. online security system as

well as assessing customer experience regarding personal fraud was collected. A simple random

sample of 2000 customers was selected. Surveys were sent to the respondents and only 420

responded.

The questionnaire comprised of a number of questions that attempted to know the opinions of the

respondents regarding their personal experience in relation to fraud as well as the effectiveness

of Visa Inc. online security system. The survey used to collect data is provided below and the

survey responses were collated in excel.

Hypothesis Development

In this section we present the hypothesis used for the study. The hypothesis were developed from

the research questions that the study sought to answer to answer.

1. Question 1: How many card frauds have been experienced by the male and the female

respondents?

Null hypothesis (H0): The average number of card frauds experienced by the males is equal to

that experienced by the females.

Alternate hypothesis (HA): The average number of card frauds experienced by the males is not

equal to that experienced by the females.

2. Question 2: Are there differences across the age groups regarding card fraud?

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Null hypothesis (H0): There is no association between the age group of the respondent and

whether they have experienced card fraud.

Alternate hypothesis (HA): There is association between the age group of the respondent and

whether they have experienced card fraud.

3. Question 3: What is the average time lost in resolving a card fraud? If Visa Inc. has set a

time-period which is acceptable at 12 hours, will this be a significant improvement to the

response time compared to what customers have experienced before?

Null hypothesis (H0): The average time lost in resolving a card fraud is equal to 12 hours.

Alternate hypothesis (HA): The average time lost in resolving a card fraud is not equal to 12

hours.

4. Question 4: How often does an online or offline card fraud occur? Visa Inc. is willing to

invest in an updated online security which will decrease the number of online card fraud only

if online transactions are more vulnerable to fraud compared to offline transactions. What is

your recommendation?

Null hypothesis (H0): The average number of online and offline credit frauds is equal.

Alternate hypothesis (HA): The average number of online and offline credit frauds is not

equal.

5. Question 5: Do any of the customers’ satisfaction scores of ‘response time’, ‘the level of

advice’, and ‘the level of communication’ influence the overall satisfaction with the credit

card fraud resolution team?

Null hypothesis (H0): There is no relationship between the independent variables

(satisfaction scores of ‘response time’, ‘the level of advice’, and ‘the level of

7

whether they have experienced card fraud.

Alternate hypothesis (HA): There is association between the age group of the respondent and

whether they have experienced card fraud.

3. Question 3: What is the average time lost in resolving a card fraud? If Visa Inc. has set a

time-period which is acceptable at 12 hours, will this be a significant improvement to the

response time compared to what customers have experienced before?

Null hypothesis (H0): The average time lost in resolving a card fraud is equal to 12 hours.

Alternate hypothesis (HA): The average time lost in resolving a card fraud is not equal to 12

hours.

4. Question 4: How often does an online or offline card fraud occur? Visa Inc. is willing to

invest in an updated online security which will decrease the number of online card fraud only

if online transactions are more vulnerable to fraud compared to offline transactions. What is

your recommendation?

Null hypothesis (H0): The average number of online and offline credit frauds is equal.

Alternate hypothesis (HA): The average number of online and offline credit frauds is not

equal.

5. Question 5: Do any of the customers’ satisfaction scores of ‘response time’, ‘the level of

advice’, and ‘the level of communication’ influence the overall satisfaction with the credit

card fraud resolution team?

Null hypothesis (H0): There is no relationship between the independent variables

(satisfaction scores of ‘response time’, ‘the level of advice’, and ‘the level of

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

communication’) and the dependent variable (Overall satisfaction with the credit card

fraud resolution team).

Alternate hypothesis (HA): There is relationship between the independent variables

(satisfaction scores of ‘response time’, ‘the level of advice’, and ‘the level of

communication’) and the dependent variable (Overall satisfaction with the credit card

fraud resolution team).

Statistical Technique and Justification

Hypothesis 1:

To test hypothesis one, an independent samples t-test was used as this is the most appropriate test

to compare the difference between mean two factors that are unrelated (Derrick, Toher, & White,

2017).

Hypothesis 2:

To test hypothesis two, a Chi-square test of association was used as this is the most appropriate

test to check for association between two groups of categorical variables (Plackett, 2003).

Hypothesis 3:

To test hypothesis three, one-sample t-test was used as this is the appropriate test to compare the

difference between mean of one variable and a pre-determined mean (Zikmund, Babin, Carr, &

Griffin, 2013).

Hypothesis 4:

8

fraud resolution team).

Alternate hypothesis (HA): There is relationship between the independent variables

(satisfaction scores of ‘response time’, ‘the level of advice’, and ‘the level of

communication’) and the dependent variable (Overall satisfaction with the credit card

fraud resolution team).

Statistical Technique and Justification

Hypothesis 1:

To test hypothesis one, an independent samples t-test was used as this is the most appropriate test

to compare the difference between mean two factors that are unrelated (Derrick, Toher, & White,

2017).

Hypothesis 2:

To test hypothesis two, a Chi-square test of association was used as this is the most appropriate

test to check for association between two groups of categorical variables (Plackett, 2003).

Hypothesis 3:

To test hypothesis three, one-sample t-test was used as this is the appropriate test to compare the

difference between mean of one variable and a pre-determined mean (Zikmund, Babin, Carr, &

Griffin, 2013).

Hypothesis 4:

8

To test hypothesis four, a two samples t-test was used as this is the appropriate test to compare

the difference between mean of two groups of variables (Zikmund, Babin, Carr, & Griffin,

2013).

Hypothesis 5:

To test hypothesis four, a multiple regression model was used as this is the appropriate test to

analyze the relationship between two or more independent variables with a dependent variable

(Armstrong, 2012).

Results, and Statistical and non-statistical Interpretation

In this section, we present the empirical results as well as the statistical and non-statistical

interpretation of the results.

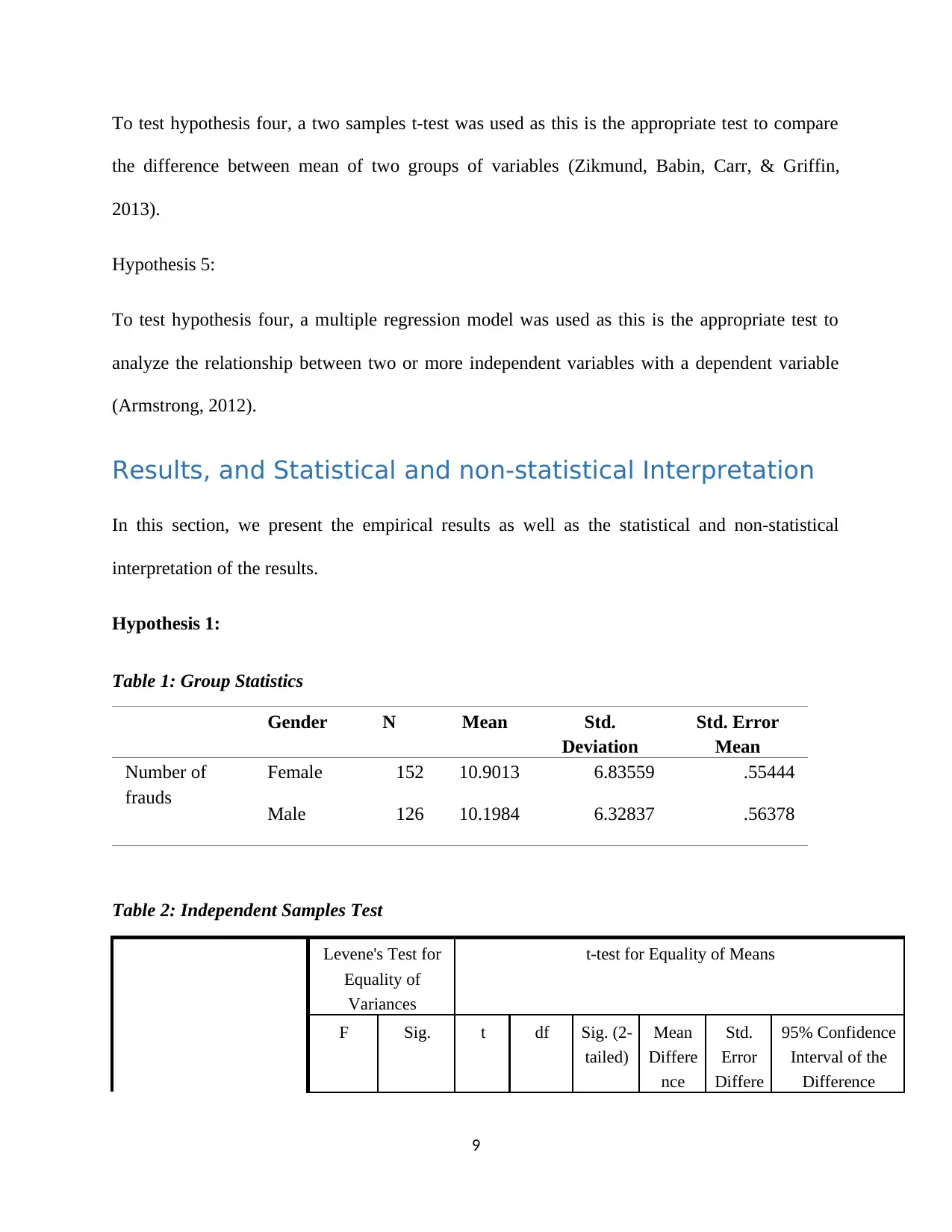

Hypothesis 1:

Table 1: Group Statistics

Gender N Mean Std.

Deviation

Std. Error

Mean

Number of

frauds

Female 152 10.9013 6.83559 .55444

Male 126 10.1984 6.32837 .56378

Table 2: Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differe

nce

Std.

Error

Differe

95% Confidence

Interval of the

Difference

9

the difference between mean of two groups of variables (Zikmund, Babin, Carr, & Griffin,

2013).

Hypothesis 5:

To test hypothesis four, a multiple regression model was used as this is the appropriate test to

analyze the relationship between two or more independent variables with a dependent variable

(Armstrong, 2012).

Results, and Statistical and non-statistical Interpretation

In this section, we present the empirical results as well as the statistical and non-statistical

interpretation of the results.

Hypothesis 1:

Table 1: Group Statistics

Gender N Mean Std.

Deviation

Std. Error

Mean

Number of

frauds

Female 152 10.9013 6.83559 .55444

Male 126 10.1984 6.32837 .56378

Table 2: Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differe

nce

Std.

Error

Differe

95% Confidence

Interval of the

Difference

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

nce Lower Upper

Number

of frauds

Equal

variances

assumed

1.855 .174 .883 276 .378 .703 .797 -.865 2.271

Equal

variances not

assumed

.889 272.6 .375 .703 .791 -.854 2.260

Statistical interpretation:

An independent samples t-test was done to compare the mean average number of card frauds

experienced by the males and the females. Results showed that the females (M = 10.91, SD =

6.84, N = 152) had no significant difference in terms of the number of card frauds experienced

when compared to the males (M = 10.20, SD = 6.32, N = 126), t (276) = 0.883, p > .05, two-

tailed. The difference of 0.703 showed an insignificant difference.

Non-statistical interpretation:

Essentially results showed that female and male respondents who took part in the study had no

significant differences in average number of card frauds they experienced.

Hypothesis 2:

Table 3: Age * whether experienced credit, debit or EFTPOS card fraud in last 12 months Cross tabulation

Whether experienced credit, debit or EFTPOS card fraud in last 12 months Total

Experienced credit, debit or EFTPOS

card fraud in last 12 months

Did not experience credit, debit or

EFTPOS card fraud in last 12 months

Age 25 years and below 67 33 100

26-35 years 66 42 108

36-45 years 80 32 112

10

Number

of frauds

Equal

variances

assumed

1.855 .174 .883 276 .378 .703 .797 -.865 2.271

Equal

variances not

assumed

.889 272.6 .375 .703 .791 -.854 2.260

Statistical interpretation:

An independent samples t-test was done to compare the mean average number of card frauds

experienced by the males and the females. Results showed that the females (M = 10.91, SD =

6.84, N = 152) had no significant difference in terms of the number of card frauds experienced

when compared to the males (M = 10.20, SD = 6.32, N = 126), t (276) = 0.883, p > .05, two-

tailed. The difference of 0.703 showed an insignificant difference.

Non-statistical interpretation:

Essentially results showed that female and male respondents who took part in the study had no

significant differences in average number of card frauds they experienced.

Hypothesis 2:

Table 3: Age * whether experienced credit, debit or EFTPOS card fraud in last 12 months Cross tabulation

Whether experienced credit, debit or EFTPOS card fraud in last 12 months Total

Experienced credit, debit or EFTPOS

card fraud in last 12 months

Did not experience credit, debit or

EFTPOS card fraud in last 12 months

Age 25 years and below 67 33 100

26-35 years 66 42 108

36-45 years 80 32 112

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

46-55 years 42 22 64

56 and over 23 13 36

Total 278 142 420

Table 4: Chi-Square Tests

Value df Asymp. Sig. (2-

sided)

Pearson Chi-Square 2.742a 4 .602

Likelihood Ratio 2.753 4 .600

Linear-by-Linear Association .024 1 .878

N of Valid Cases 420

a. 0 cells (0.0%) have expected count less than 5. The minimum expected count is 12.17.

Statistical interpretation:

A chi-square test was performed and no relationship was found between gender and whether

participants experienced credit, debit or EFTPOS card fraud in last 12 months,

χ2 ( 4 , 420 ) =2.742 , p=0.602.

Non-statistical interpretation:

Gender does not influence on whether the participant will experience credit card fraud or not.

Hypothesis 3:

Table 5: One sample t-test for difference in time lost in resolving a card fraud

Question 4 Test

Mean 13.65108 12

Variance 308.4302 0

Observations 278 204

Pooled Variance 177.9899

Hypothesized Mean Difference 0

df 480

11

56 and over 23 13 36

Total 278 142 420

Table 4: Chi-Square Tests

Value df Asymp. Sig. (2-

sided)

Pearson Chi-Square 2.742a 4 .602

Likelihood Ratio 2.753 4 .600

Linear-by-Linear Association .024 1 .878

N of Valid Cases 420

a. 0 cells (0.0%) have expected count less than 5. The minimum expected count is 12.17.

Statistical interpretation:

A chi-square test was performed and no relationship was found between gender and whether

participants experienced credit, debit or EFTPOS card fraud in last 12 months,

χ2 ( 4 , 420 ) =2.742 , p=0.602.

Non-statistical interpretation:

Gender does not influence on whether the participant will experience credit card fraud or not.

Hypothesis 3:

Table 5: One sample t-test for difference in time lost in resolving a card fraud

Question 4 Test

Mean 13.65108 12

Variance 308.4302 0

Observations 278 204

Pooled Variance 177.9899

Hypothesized Mean Difference 0

df 480

11

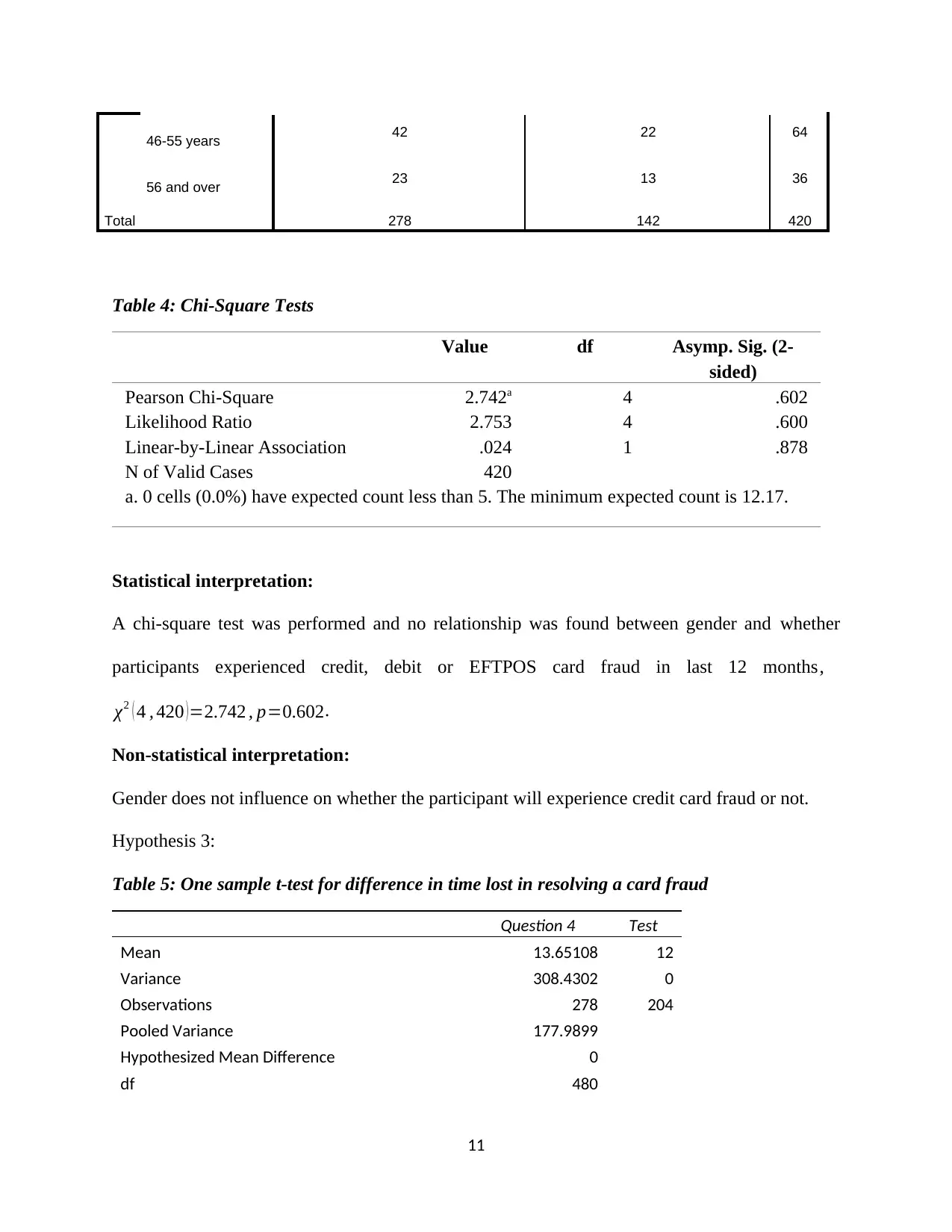

t Stat 1.342407

P(T<=t) one-tail 0.090049

t Critical one-tail 1.648034

P(T<=t) two-tail 0.180099

t Critical two-tail 1.964918

Statistical interpretation:

From Table 5, it is evident that t-calculated (1.34) is less than t-critical (1.965) and p-value is

greater than the significance level (5% level of significance), thus, we fail to reject that null

hypothesis that the average time lost in resolving a card fraud is equal to 12 hours (p-value

0.180) at 5% level of significance.

Non-statistical interpretation:

The time lost in resolving a card fraud is equal to 12 hours. Therefore, the resolving time which

is 12 hours set time-period is within the acceptable time of 12 hours.

Hypothesis 4:

Table 6: two samples t-test to compare the offline and online credit frauds

Offline Online

Mean 4.31295 6.269784

Variance 23.47211 15.40349

Observations 278 278

Pooled Variance 19.4378

Hypothesized Mean Difference 0

df 554

t Stat -5.23285

P(T<=t) one-tail 1.19E-07

t Critical one-tail 1.647609

P(T<=t) two-tail 2.37E-07

t Critical two-tail 1.964255

Statistical interpretation:

12

P(T<=t) one-tail 0.090049

t Critical one-tail 1.648034

P(T<=t) two-tail 0.180099

t Critical two-tail 1.964918

Statistical interpretation:

From Table 5, it is evident that t-calculated (1.34) is less than t-critical (1.965) and p-value is

greater than the significance level (5% level of significance), thus, we fail to reject that null

hypothesis that the average time lost in resolving a card fraud is equal to 12 hours (p-value

0.180) at 5% level of significance.

Non-statistical interpretation:

The time lost in resolving a card fraud is equal to 12 hours. Therefore, the resolving time which

is 12 hours set time-period is within the acceptable time of 12 hours.

Hypothesis 4:

Table 6: two samples t-test to compare the offline and online credit frauds

Offline Online

Mean 4.31295 6.269784

Variance 23.47211 15.40349

Observations 278 278

Pooled Variance 19.4378

Hypothesized Mean Difference 0

df 554

t Stat -5.23285

P(T<=t) one-tail 1.19E-07

t Critical one-tail 1.647609

P(T<=t) two-tail 2.37E-07

t Critical two-tail 1.964255

Statistical interpretation:

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.