AFIN806 - VIX, Volatility Trading & Risk Management - Macquarie

VerifiedAdded on 2023/06/11

|19

|5133

|345

Report

AI Summary

This report provides a comprehensive analysis of the Chicago Board Options Exchange's Market Volatility Index (VIX) and its significance in financial markets. It explains the construction of the VIX, its importance for risk management and hedging, and examines empirical research on the performance of exchange-traded products (ETPs) linked to the VIX. Furthermore, the report delves into short volatility strategies, their applications for generating returns, and the associated risks for fund managers and financial markets, including methods for managing these risks. The report also discusses the role of VIX in managing financial market risk, the importance of risk management in determining stock scenarios, and strategies for mitigating risk through volatility risk premiums and diversified portfolios. It further evaluates the performance of VIX future contracts and volatility ETPs, analyzing market trends and investor behavior during periods of volatility, such as the BREXIT event and stock market crashes. The analysis incorporates various sources and data to provide a thorough understanding of VIX and its implications for investors and financial markets.

RISK MANGEMENT AND DERIVATIVES

2018

2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VIX AND ITS SIGNIFICANCE 1

Table of Contents

Question 1..................................................................................................................................3

Answer 1....................................................................................................................................3

Introduction............................................................................................................................3

Development of VIX..............................................................................................................4

VIX’s importance...................................................................................................................4

Question 2..................................................................................................................................5

Answer 2....................................................................................................................................5

Question 3..................................................................................................................................7

Answer 3....................................................................................................................................7

Performance of the ETP’s......................................................................................................7

Question 4................................................................................................................................10

Answer 4...............................................................................................................................10

Short Volatility Strategies....................................................................................................10

Selling Techniques...............................................................................................................10

Multi-Strategy.......................................................................................................................11

Fluctuations in stocks...........................................................................................................11

Short risk and reward strategy..............................................................................................13

Conventional Analysis..........................................................................................................13

References................................................................................................................................16

Table of Contents

Question 1..................................................................................................................................3

Answer 1....................................................................................................................................3

Introduction............................................................................................................................3

Development of VIX..............................................................................................................4

VIX’s importance...................................................................................................................4

Question 2..................................................................................................................................5

Answer 2....................................................................................................................................5

Question 3..................................................................................................................................7

Answer 3....................................................................................................................................7

Performance of the ETP’s......................................................................................................7

Question 4................................................................................................................................10

Answer 4...............................................................................................................................10

Short Volatility Strategies....................................................................................................10

Selling Techniques...............................................................................................................10

Multi-Strategy.......................................................................................................................11

Fluctuations in stocks...........................................................................................................11

Short risk and reward strategy..............................................................................................13

Conventional Analysis..........................................................................................................13

References................................................................................................................................16

VIX AND ITS SIGNIFICANCE 2

Question 1

Answer 1

Introduction

The CBOE volatility index is a common and the prolific measure of the stock market

expectation of volatility implied by S&P 500 index options. The calculation and the

publishing of the index are supervised the Chicago Board Options Exchange. It is also known

as the index of the fear gauge. This form of an index was created in the year 1993 by Robert

F. Whaley who was the professor of the Duke University. As indicated by the CBOE the

assessed instability of the S/P 500 record is estimated by VIX for an aggregate time of the

multi-day at the cash OEX alternative. These incorporate mutual funds, proficient

administrators with the heap of the cash, and the people that make ventures which looks to

benefit from the instability of the market. VIX is a suggested instability in the speech of the

business of the securities. It is similar to the securities which give the yield at the season of

the development. The VIX is frequently alluded to as the "financial specialist fear measure"

(Whaley, 2000).

For the most part when the stock costs are falling and speculators are having a dread the

unpredictability and the record climb in like manner. Like a bond, an investment opportunity

has a model for its valuation and furthermore, the quantity of parameters is locked in which

are to be assessed with abnormal state of precision (Whaley, 2000). To discover the

suggested instability the market cost of the listed alternative is likened with demonstrate

esteem. This inferred unpredictability is accordingly the best benchmark of the normal

instability of the fundamental stock over the rest of the life of the choice. Since VIX depends

Question 1

Answer 1

Introduction

The CBOE volatility index is a common and the prolific measure of the stock market

expectation of volatility implied by S&P 500 index options. The calculation and the

publishing of the index are supervised the Chicago Board Options Exchange. It is also known

as the index of the fear gauge. This form of an index was created in the year 1993 by Robert

F. Whaley who was the professor of the Duke University. As indicated by the CBOE the

assessed instability of the S/P 500 record is estimated by VIX for an aggregate time of the

multi-day at the cash OEX alternative. These incorporate mutual funds, proficient

administrators with the heap of the cash, and the people that make ventures which looks to

benefit from the instability of the market. VIX is a suggested instability in the speech of the

business of the securities. It is similar to the securities which give the yield at the season of

the development. The VIX is frequently alluded to as the "financial specialist fear measure"

(Whaley, 2000).

For the most part when the stock costs are falling and speculators are having a dread the

unpredictability and the record climb in like manner. Like a bond, an investment opportunity

has a model for its valuation and furthermore, the quantity of parameters is locked in which

are to be assessed with abnormal state of precision (Whaley, 2000). To discover the

suggested instability the market cost of the listed alternative is likened with demonstrate

esteem. This inferred unpredictability is accordingly the best benchmark of the normal

instability of the fundamental stock over the rest of the life of the choice. Since VIX depends

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VIX AND ITS SIGNIFICANCE 3

on S&P 100 record choice costs, VIX speaks to a market accord of the S&P 100 with

expected instability.

Development of VIX

At the point when the exchanges of the investment of stocks started in the year 1973, Chicago

Board Options Exchange has ensured that the market volatility index can be built by the

option price which can showcase the expectations of the future.

Since the inception of the thought, numerous techniques were proposed by various

researchers and there after Whaley proposed a straightforward approach which focuses on

dealing with the development of the market volatility. This approach is used as a measure for

the future stock price in the financial market. In the same year, the Chicago Board Option

Exchange began to figure out the construction of the CBOE index of the volatility also

known as VIX. The VIX depends on the implicit volatility of the S&P 100 index alternatives

(Cboe volatility index, 2018).

From thereafter the CBOE engaged in the calculation of the various VIX indexes, including

the VIX based on S&P 500 index, CBOE DJIA, CBOE Russell 2000, RVX, NASDAQ 100

volatility index. VIX was launched in April 2008 by national stock exchange and is depends

on Nifty 50 index option prices (Whaley, 2009).

VIX’s importance

The CBOE volatility index is helpful in estimating unpredictable risk of the S&P 500 over a

multi-day target time period for example 3 to 4 days in general. For the purpose of the

calculation the Chicago Board options Exchange works upon the observation of the price and

its behaviour of different call options and the option of the put money on the index of the

S&P 500, where different strike prices as well as the multiple expiration dates are known for

the incorporation of the trading and the weekly options. Further, the weighted average

on S&P 100 record choice costs, VIX speaks to a market accord of the S&P 100 with

expected instability.

Development of VIX

At the point when the exchanges of the investment of stocks started in the year 1973, Chicago

Board Options Exchange has ensured that the market volatility index can be built by the

option price which can showcase the expectations of the future.

Since the inception of the thought, numerous techniques were proposed by various

researchers and there after Whaley proposed a straightforward approach which focuses on

dealing with the development of the market volatility. This approach is used as a measure for

the future stock price in the financial market. In the same year, the Chicago Board Option

Exchange began to figure out the construction of the CBOE index of the volatility also

known as VIX. The VIX depends on the implicit volatility of the S&P 100 index alternatives

(Cboe volatility index, 2018).

From thereafter the CBOE engaged in the calculation of the various VIX indexes, including

the VIX based on S&P 500 index, CBOE DJIA, CBOE Russell 2000, RVX, NASDAQ 100

volatility index. VIX was launched in April 2008 by national stock exchange and is depends

on Nifty 50 index option prices (Whaley, 2009).

VIX’s importance

The CBOE volatility index is helpful in estimating unpredictable risk of the S&P 500 over a

multi-day target time period for example 3 to 4 days in general. For the purpose of the

calculation the Chicago Board options Exchange works upon the observation of the price and

its behaviour of different call options and the option of the put money on the index of the

S&P 500, where different strike prices as well as the multiple expiration dates are known for

the incorporation of the trading and the weekly options. Further, the weighted average

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VIX AND ITS SIGNIFICANCE 4

method is used to calculate the value of the index and the options by the CBOE. The actual

price is the reason for which the VIX becomes the important factor in the financial market for

each investor and individual who invest in the stock options and the index. The relationship

of the VIX with the market situations is inverse relationship in nature. Higher the VIX the

market will drop and vice versa. The investors of the market also use VIX to determine the

risky points and the level of the price of the stock (Whaley, 2013). The scenario of the VIX is

such that when the VIX escalates the prices of few of the share might have fallen already.

The importance or the significance of the VIX can be observed at the broader level altogether

with the pool of the stocks (Chang, Hsieh and McAleer, 2017). The volatility or the risk

factor of the individual stock will differ from that of the pool or group of the stocks. VIX is

also required essentially to understand the graph of the market due to which the investors and

the option traders or the ordinary traders can choose between whether to invest in the stock or

to hold for the future purposes.

Question 2

Answer 2

Another feature of the VIX is to manage the risk of the financial market and therefore, the

risk management also becomes the key essential motive in determining the scenario of the

stocks.

Most of the strategies try to reap the risk premiums options under the volatile market in the

VIX which gives the long haul edge. It has often been observed that the range of the VR may

vary and can be either positive, be negative or neutral. The direction of the VRP is a path

which depicts the performance of the stock options. This way the risk of the investor can be

mitigated by having the approach as discussed above. The volatility risk premiums are

method is used to calculate the value of the index and the options by the CBOE. The actual

price is the reason for which the VIX becomes the important factor in the financial market for

each investor and individual who invest in the stock options and the index. The relationship

of the VIX with the market situations is inverse relationship in nature. Higher the VIX the

market will drop and vice versa. The investors of the market also use VIX to determine the

risky points and the level of the price of the stock (Whaley, 2013). The scenario of the VIX is

such that when the VIX escalates the prices of few of the share might have fallen already.

The importance or the significance of the VIX can be observed at the broader level altogether

with the pool of the stocks (Chang, Hsieh and McAleer, 2017). The volatility or the risk

factor of the individual stock will differ from that of the pool or group of the stocks. VIX is

also required essentially to understand the graph of the market due to which the investors and

the option traders or the ordinary traders can choose between whether to invest in the stock or

to hold for the future purposes.

Question 2

Answer 2

Another feature of the VIX is to manage the risk of the financial market and therefore, the

risk management also becomes the key essential motive in determining the scenario of the

stocks.

Most of the strategies try to reap the risk premiums options under the volatile market in the

VIX which gives the long haul edge. It has often been observed that the range of the VR may

vary and can be either positive, be negative or neutral. The direction of the VRP is a path

which depicts the performance of the stock options. This way the risk of the investor can be

mitigated by having the approach as discussed above. The volatility risk premiums are

VIX AND ITS SIGNIFICANCE 5

favourable and keeping a record of the same can reduce the risk. There are different positions

which can also be adjusted and balanced according to the market situations through the

alignment of the relationships between the future options, Spot VIX and the volatility of the

S&P 500 (Beuhler, 2016).

Routinely a basic scaling in/out system is significantly outflanking the XIV drawdown

approach. Generally this approach cannot be followed by the investors who are seeking for

the long term. Therefore in order to avoid the risk of the escalating costs the overnight

decisions shall not be taken.

Nobody can anticipate the future, and it becomes hassle when the financial specialists are

involved in the trial and error of the options and try to understand the direction of the volatile

securities which possess the extreme level of the risk. The proactive approach is not suitable

in such a scenario and hence in order to avoid the risk of the loss the investors can turn

towards the reactive approach in which the investors react after analysing the volatility parity

of the security. To identify if the risk is eliminated or not it can be found out by the variances

in the VRP (Cui, Feng and MacKay, 2017).

The size of the security also determines the level of the risks involved. Rationally the

volatility of the risk premium is significant in the cases where the size of the volatility is high.

The exposure for the investor can be increased if the market is in favourable of the investor

and the scaling strategy fits with the future options. The risk adjusted exposure has been

provided when the chances of the profitability can be possible (Hudson, 2017).

Only one out of every odd VIX techniques is presented to the comparable dangers and each

set of risk has its own opportunities and the threats. These varied distinctions can

fundamentally navigate performance of the stock because of economic situations and the

financial markets. Hence, a diversified portfolio of the securities shall be kept in order to

favourable and keeping a record of the same can reduce the risk. There are different positions

which can also be adjusted and balanced according to the market situations through the

alignment of the relationships between the future options, Spot VIX and the volatility of the

S&P 500 (Beuhler, 2016).

Routinely a basic scaling in/out system is significantly outflanking the XIV drawdown

approach. Generally this approach cannot be followed by the investors who are seeking for

the long term. Therefore in order to avoid the risk of the escalating costs the overnight

decisions shall not be taken.

Nobody can anticipate the future, and it becomes hassle when the financial specialists are

involved in the trial and error of the options and try to understand the direction of the volatile

securities which possess the extreme level of the risk. The proactive approach is not suitable

in such a scenario and hence in order to avoid the risk of the loss the investors can turn

towards the reactive approach in which the investors react after analysing the volatility parity

of the security. To identify if the risk is eliminated or not it can be found out by the variances

in the VRP (Cui, Feng and MacKay, 2017).

The size of the security also determines the level of the risks involved. Rationally the

volatility of the risk premium is significant in the cases where the size of the volatility is high.

The exposure for the investor can be increased if the market is in favourable of the investor

and the scaling strategy fits with the future options. The risk adjusted exposure has been

provided when the chances of the profitability can be possible (Hudson, 2017).

Only one out of every odd VIX techniques is presented to the comparable dangers and each

set of risk has its own opportunities and the threats. These varied distinctions can

fundamentally navigate performance of the stock because of economic situations and the

financial markets. Hence, a diversified portfolio of the securities shall be kept in order to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VIX AND ITS SIGNIFICANCE 6

distribute the risks among the different stocks. The potential stocks can be chosen for the

investments and the stocks which are already on hold due to its non-potentiality, its risk can

be mitigated by substituting the risk with the potential ones (Pfund and Fowler, 2017).

The returns from the volatile securities can be generated timely and if a sound strategy is

designed to avail the benefits from the stock for the longer duration. In order to stay away

from the risk that can shake down or can bring a crash in the market the strategy of maintain

a future perspective can be used to decide the magnitude and ultimately the risks can be

managed efficiently (Jadhao and Chandra, 2017)

Question 3

Answer 3

Performance of the ETP’s

The exchange trade volatility products also known as ETP's VIX future contracts came into

existence in the year 2004, recorded VIX option in the year 2006 and volatile ETP's in 2009

and encourages a great deal of chances for the investors to use the class of the assets which

were earlier not allowed to (Buehler and Cusatis, 2018). The short term volatility trading by

the investors will provide the short range of the magnitude and vice versa. Amongst the lot of

examples one such example is the space created through the volatile options. The changes are

reflected however, financial emotion of the investor is also measured (Chen and Lien, 2017).

The future options are measured on the basis of the S&P 500 index and it was evolving and

was in existence since two decades. Yet the idea is not to invest in such securities.

A month ago (June 2016) demonstrated a spike in unpredictability exchanging with the most

elevated offer volume in Exchange-Traded Products (ETPs) connected to the CBOE

distribute the risks among the different stocks. The potential stocks can be chosen for the

investments and the stocks which are already on hold due to its non-potentiality, its risk can

be mitigated by substituting the risk with the potential ones (Pfund and Fowler, 2017).

The returns from the volatile securities can be generated timely and if a sound strategy is

designed to avail the benefits from the stock for the longer duration. In order to stay away

from the risk that can shake down or can bring a crash in the market the strategy of maintain

a future perspective can be used to decide the magnitude and ultimately the risks can be

managed efficiently (Jadhao and Chandra, 2017)

Question 3

Answer 3

Performance of the ETP’s

The exchange trade volatility products also known as ETP's VIX future contracts came into

existence in the year 2004, recorded VIX option in the year 2006 and volatile ETP's in 2009

and encourages a great deal of chances for the investors to use the class of the assets which

were earlier not allowed to (Buehler and Cusatis, 2018). The short term volatility trading by

the investors will provide the short range of the magnitude and vice versa. Amongst the lot of

examples one such example is the space created through the volatile options. The changes are

reflected however, financial emotion of the investor is also measured (Chen and Lien, 2017).

The future options are measured on the basis of the S&P 500 index and it was evolving and

was in existence since two decades. Yet the idea is not to invest in such securities.

A month ago (June 2016) demonstrated a spike in unpredictability exchanging with the most

elevated offer volume in Exchange-Traded Products (ETPs) connected to the CBOE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

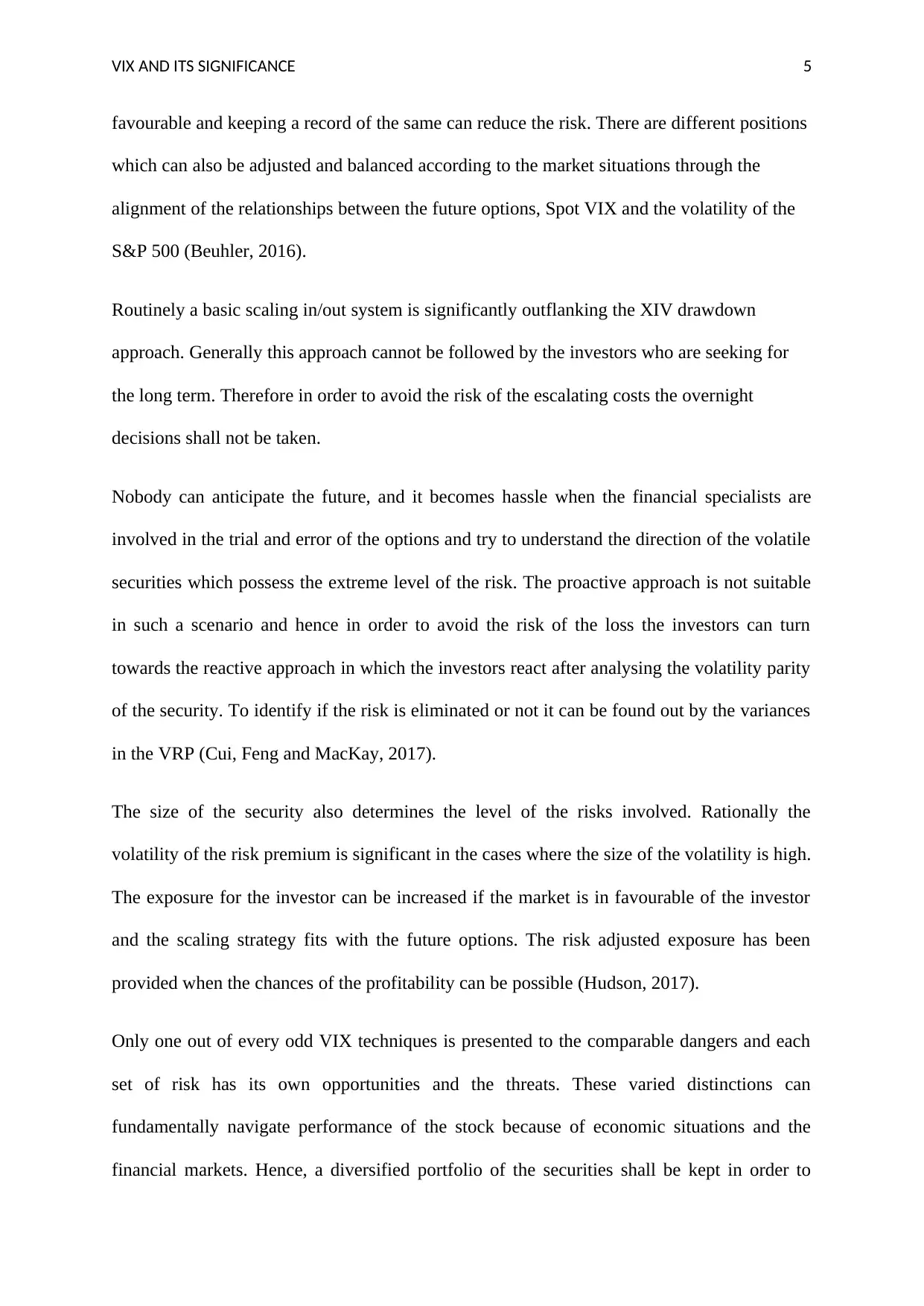

VIX AND ITS SIGNIFICANCE 7

Volatility Index or VIX Index ever. This may shock no one, surrendered the vulnerability

prompting BREXIT in any case, while famous, VIX ETPs are not without their complexities

and potential disadvantages. VIX ETPs to fail to meet expectations the VIX record and ought

to accordingly be checked nearly by financial specialists. This colossal week after week

mobilizes; in any case, the VIX tends to chill drastically. The stock was down by 6.4%, and

after a week later higher only by 25% of the time. The stellar performers in the packet of the

ETF were SPY or AGG. Under the first list the returns ranged from almost 19% to 88%

(Roy, 2018). Half the ETP’s on the list are linked to volatility including Rex VoLMAXX

which was accelerated by 98.3% (Rhoads, 2018). The CBOE volatility index reached the

summit of the stock market as the U.S stock market faced a crash by 12%. In order to hedge

their positions to mitigate the future losses, investors bid up the prices. The VIX surged by

115.6 per cent on Monday to 37.32. It rose briefly early Tuesday to over 50, the highest level

since Aug 2015 (Roy, 2018). The VIX then dropped to 22.42, rose to over 45, before fading

to roughly 35.

(Source: Kramer, 2018)

Volatility Index or VIX Index ever. This may shock no one, surrendered the vulnerability

prompting BREXIT in any case, while famous, VIX ETPs are not without their complexities

and potential disadvantages. VIX ETPs to fail to meet expectations the VIX record and ought

to accordingly be checked nearly by financial specialists. This colossal week after week

mobilizes; in any case, the VIX tends to chill drastically. The stock was down by 6.4%, and

after a week later higher only by 25% of the time. The stellar performers in the packet of the

ETF were SPY or AGG. Under the first list the returns ranged from almost 19% to 88%

(Roy, 2018). Half the ETP’s on the list are linked to volatility including Rex VoLMAXX

which was accelerated by 98.3% (Rhoads, 2018). The CBOE volatility index reached the

summit of the stock market as the U.S stock market faced a crash by 12%. In order to hedge

their positions to mitigate the future losses, investors bid up the prices. The VIX surged by

115.6 per cent on Monday to 37.32. It rose briefly early Tuesday to over 50, the highest level

since Aug 2015 (Roy, 2018). The VIX then dropped to 22.42, rose to over 45, before fading

to roughly 35.

(Source: Kramer, 2018)

VIX AND ITS SIGNIFICANCE 8

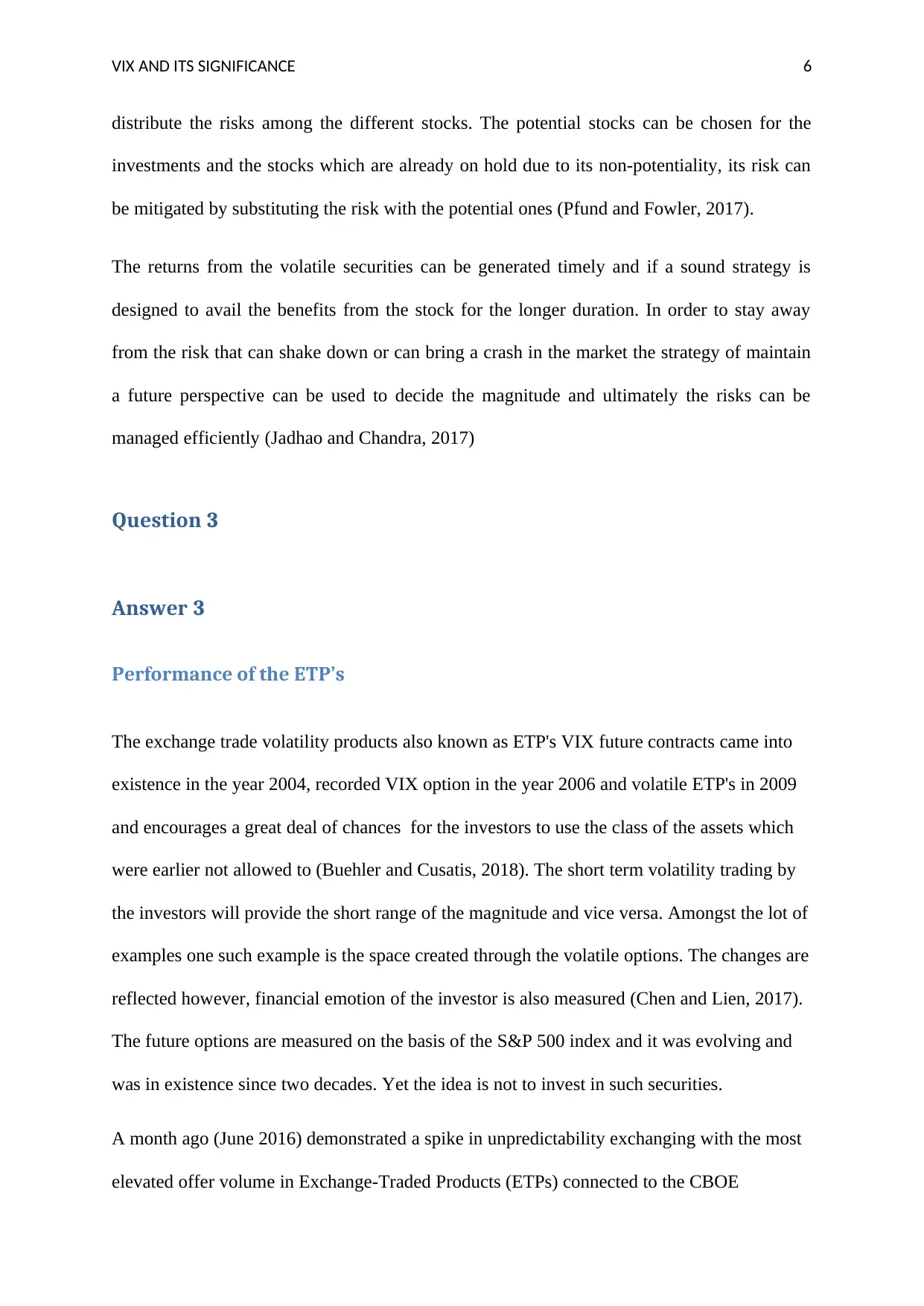

Further the top performers of the VIX in the year 2018 are as follows

(Source: Golden, 2018)

The year seems to be tough in the second half. The SPDR is down by 0.2% while the iShares

Core U.S. Aggregate bond ETF (AGG) has fallen by 1.5% in the year to the date of 10th of

April. The performance seems to be down in comparison to the previous years which

reflected a robust gain of 21.7% and 3.6 % respectively. A lot of equity analysts are givinga

view of the situation as the stock picker market. Yet some of them are also performing at a

super speed such as SPY and AGG. Aside from the VIX products therea re also some kind of

ETP’s that are related to the category of the commodities. The Ipath Bloomberg Cocoa Sub

index Total Return ETN (NIB) and the Iptah Pure Beta CocOA ETN is the commodity pack

which is leading at the next level. The profits were received at the inclining rate and touched

36% in each case. The performance of United States 3x Oil Fund and Long Crude Oil ETN

(UWT) has also been more than par. As impressive as the returns the investors are waiting to

shoot with the VIX ETF or to leverage the commodity with the triple layers.

Further the top performers of the VIX in the year 2018 are as follows

(Source: Golden, 2018)

The year seems to be tough in the second half. The SPDR is down by 0.2% while the iShares

Core U.S. Aggregate bond ETF (AGG) has fallen by 1.5% in the year to the date of 10th of

April. The performance seems to be down in comparison to the previous years which

reflected a robust gain of 21.7% and 3.6 % respectively. A lot of equity analysts are givinga

view of the situation as the stock picker market. Yet some of them are also performing at a

super speed such as SPY and AGG. Aside from the VIX products therea re also some kind of

ETP’s that are related to the category of the commodities. The Ipath Bloomberg Cocoa Sub

index Total Return ETN (NIB) and the Iptah Pure Beta CocOA ETN is the commodity pack

which is leading at the next level. The profits were received at the inclining rate and touched

36% in each case. The performance of United States 3x Oil Fund and Long Crude Oil ETN

(UWT) has also been more than par. As impressive as the returns the investors are waiting to

shoot with the VIX ETF or to leverage the commodity with the triple layers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VIX AND ITS SIGNIFICANCE 9

Question 4

Answer 4

Short Volatility Strategies

Volatility can be described as analyzing and measuring the market index returns or any

change that occur which can be negative or positive is termed as volatility. As the size of the

security changes the risk associated with it is measured accordingly. Volatility can be

measured if there is any deviation in the market index or in another word if the set of

securities that are being used, varies in any condition (Chen, Lee and Hsu, 2018). Active

volatility can be called short-term volatility; short-term volatility is the reason behind the

certain events of the uncomfortable nature that are totally beyond imagination or expectation.

The number of put options will also be affected because of the volatile market and that is the

reason why short-term volatility is called "synthetic" in nature. It can also create imbalance

and that is why strategies are designed according to market (Stanton, 2011).

How Are They Used To Create Returns For The Investors?

In order to make returns through short-term volatile strategies, there are many different ways,

for instance, hedging (Berman, 2017). Hedging comes under the modern or advanced type of

investing, or we can say Hedging is a kind of marketing strategy which is very helpful for the

investors and in which one makes an investment on the basis of the other investments. In

technical terms both the stocks that are being used are correlated negatively. Few option

strategies are explained below:

Selling Techniques

In this situation the dealer accept the costs of the securities will fall and henceforth it can be

purchased back at a reduced cost. Short offering is otherwise called "Shorting" or "going

short". The benefit is derived by the fluctuation in the costs of the buy and sale offer. The

Question 4

Answer 4

Short Volatility Strategies

Volatility can be described as analyzing and measuring the market index returns or any

change that occur which can be negative or positive is termed as volatility. As the size of the

security changes the risk associated with it is measured accordingly. Volatility can be

measured if there is any deviation in the market index or in another word if the set of

securities that are being used, varies in any condition (Chen, Lee and Hsu, 2018). Active

volatility can be called short-term volatility; short-term volatility is the reason behind the

certain events of the uncomfortable nature that are totally beyond imagination or expectation.

The number of put options will also be affected because of the volatile market and that is the

reason why short-term volatility is called "synthetic" in nature. It can also create imbalance

and that is why strategies are designed according to market (Stanton, 2011).

How Are They Used To Create Returns For The Investors?

In order to make returns through short-term volatile strategies, there are many different ways,

for instance, hedging (Berman, 2017). Hedging comes under the modern or advanced type of

investing, or we can say Hedging is a kind of marketing strategy which is very helpful for the

investors and in which one makes an investment on the basis of the other investments. In

technical terms both the stocks that are being used are correlated negatively. Few option

strategies are explained below:

Selling Techniques

In this situation the dealer accept the costs of the securities will fall and henceforth it can be

purchased back at a reduced cost. Short offering is otherwise called "Shorting" or "going

short". The benefit is derived by the fluctuation in the costs of the buy and sale offer. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VIX AND ITS SIGNIFICANCE 10

functioning of the market can be analysed by the short selling strategy. The short selling

helps a lot in observing or analysing the ways in which market functions. This strategy

restricts the impact on the investors (Engelberg, Reed and Ringgenberg, 2018). In order to

run the market smoothly and create liquidity, the short term selling is very important and also

to prevent the stocks from escalated bidding at a very high peak, the short selling kind of does

a reality check on the market. Despite all these benefits, shorting can be harmful to the long-

term path and also the upward path in the market. The short selling strategy is kind of an

alarm for the investors which are highly useful in preventing the stocks from being bid up to

the escalated heights. As the investments are bought in the short term duration it provides the

liquidity and also constraints the influence of the price on the mind of the investors.

Multi-Strategy This kind of strategy is very comfortable for the business and in this strategy,

a small amount or sum has to be paid before paying the total amount in advance before

executing the whole transaction. This complete strategy gives benefit to the high cost of

brokerage and therefore the complete expenses made during the sale are lowered and that is

why it is also very helpful while making returns (Fan, Xiao and Zhou, 2018). An investment

is made only after carefully evaluating and examining the associated losses or profits in the

investment. While purchasing the stocks on one side and selling the associate derivatives on

the other side as the call options the profits can be generated and the returns can be earned.

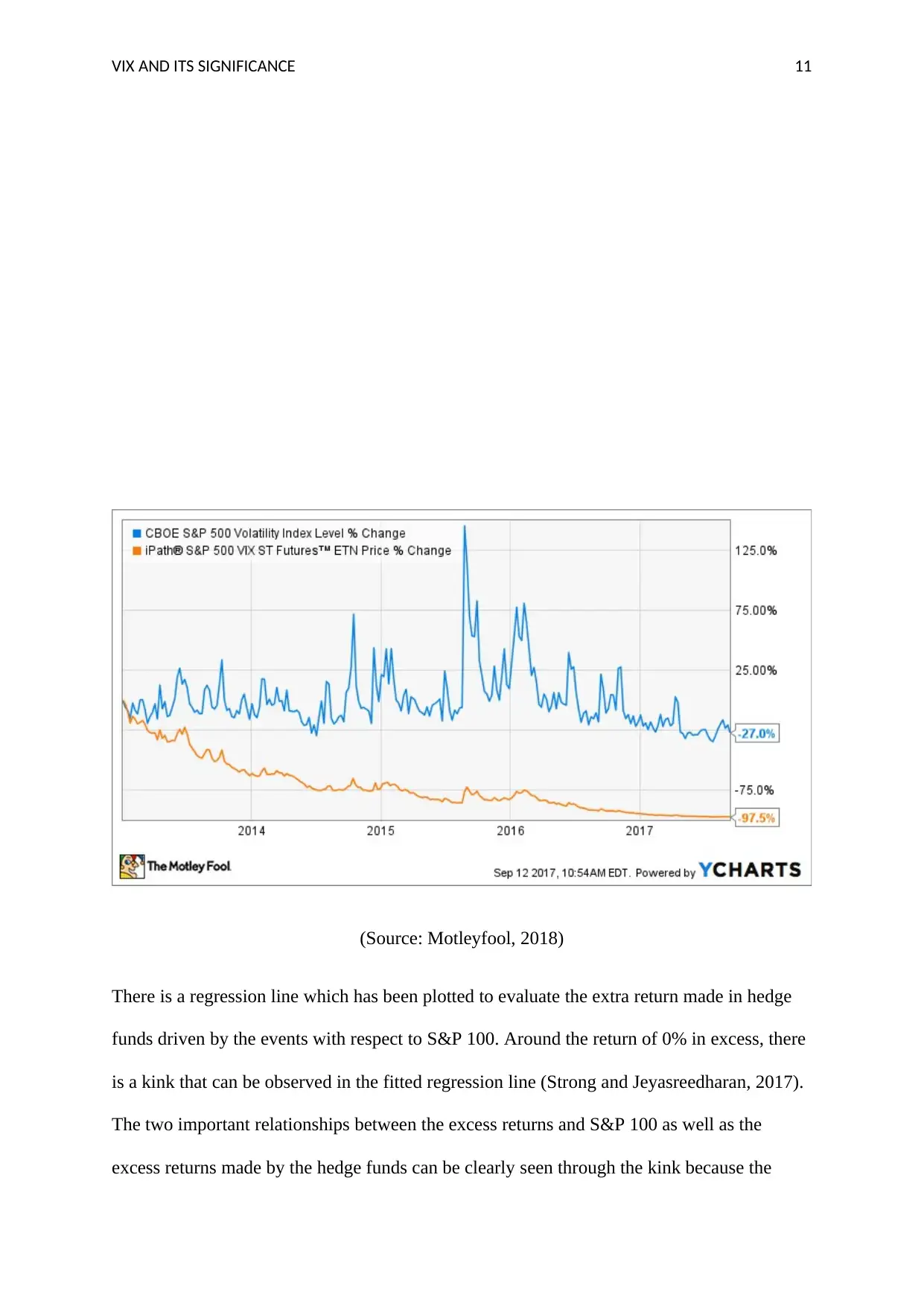

Fluctuations in stocks

The results can be of the two types positive as well as the negative.

The results of profit earned with the arbitration of merger and hedge funds driven by the

events will produce a positive change or movement in the stock. This kind of positive

movements is categorized with an exposure of small put options.

functioning of the market can be analysed by the short selling strategy. The short selling

helps a lot in observing or analysing the ways in which market functions. This strategy

restricts the impact on the investors (Engelberg, Reed and Ringgenberg, 2018). In order to

run the market smoothly and create liquidity, the short term selling is very important and also

to prevent the stocks from escalated bidding at a very high peak, the short selling kind of does

a reality check on the market. Despite all these benefits, shorting can be harmful to the long-

term path and also the upward path in the market. The short selling strategy is kind of an

alarm for the investors which are highly useful in preventing the stocks from being bid up to

the escalated heights. As the investments are bought in the short term duration it provides the

liquidity and also constraints the influence of the price on the mind of the investors.

Multi-Strategy This kind of strategy is very comfortable for the business and in this strategy,

a small amount or sum has to be paid before paying the total amount in advance before

executing the whole transaction. This complete strategy gives benefit to the high cost of

brokerage and therefore the complete expenses made during the sale are lowered and that is

why it is also very helpful while making returns (Fan, Xiao and Zhou, 2018). An investment

is made only after carefully evaluating and examining the associated losses or profits in the

investment. While purchasing the stocks on one side and selling the associate derivatives on

the other side as the call options the profits can be generated and the returns can be earned.

Fluctuations in stocks

The results can be of the two types positive as well as the negative.

The results of profit earned with the arbitration of merger and hedge funds driven by the

events will produce a positive change or movement in the stock. This kind of positive

movements is categorized with an exposure of small put options.

VIX AND ITS SIGNIFICANCE 11

(Source: Motleyfool, 2018)

There is a regression line which has been plotted to evaluate the extra return made in hedge

funds driven by the events with respect to S&P 100. Around the return of 0% in excess, there

is a kink that can be observed in the fitted regression line (Strong and Jeyasreedharan, 2017).

The two important relationships between the excess returns and S&P 100 as well as the

excess returns made by the hedge funds can be clearly seen through the kink because the

(Source: Motleyfool, 2018)

There is a regression line which has been plotted to evaluate the extra return made in hedge

funds driven by the events with respect to S&P 100. Around the return of 0% in excess, there

is a kink that can be observed in the fitted regression line (Strong and Jeyasreedharan, 2017).

The two important relationships between the excess returns and S&P 100 as well as the

excess returns made by the hedge funds can be clearly seen through the kink because the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.