Auditing Vmoto Ltd: Financial Analysis, Risks, and Performance Review

VerifiedAdded on 2023/06/04

|21

|3773

|320

Report

AI Summary

This report provides an in-depth audit of Vmoto Ltd, an Australian scooter manufacturer and distributor, focusing on its nature, key business risks, and financial performance. It includes an analysis of the company's financial position using performance analytical procedures, relevant financial report assertions, and a sampling plan. The report assesses the impact of technological obsolescence and other risks on the company's sustainability, using the risk model AR = f (IR x CR X DR) to determine the level of risk. Analytical procedures, including gross profit ratio, net profit ratio, current ratio, and debt-equity ratio, are applied to analyze the company's financial position over three years, highlighting trends and offering recommendations for improvement. The report also discusses materiality for planning purposes and associated assertions, emphasizing the importance of accurate and complete accounts for auditing purposes. This detailed analysis aims to provide auditors with a comprehensive understanding of Vmoto Ltd's financial standing and potential risks.

Auditing 1

Auditing

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 2

Table of Contents

Introduction:...............................................................................................................................3

Content:......................................................................................................................................4

Understanding of the nature of the entity and its industry and then identify key business

risks along with the risk metrics:...........................................................................................4

Conclusion:..............................................................................................................................19

References:...............................................................................................................................20

Table of Contents

Introduction:...............................................................................................................................3

Content:......................................................................................................................................4

Understanding of the nature of the entity and its industry and then identify key business

risks along with the risk metrics:...........................................................................................4

Conclusion:..............................................................................................................................19

References:...............................................................................................................................20

Auditing 3

Introduction:

The report will be providing learning over the diverse concepts of auditing. The organization

selected for the process is Vmoto Ltd. Which is an Australian company dealing with scooter

manufacturing and distribution. The report will be providing the nature of the entity and key

risks that are faced by the company in the particular market segment. The performance

analytical procedures for developing the statement of financial position will be taken into

consideration in the report. Relevant financial report assertions and the reasons for their

selections will also be done in the task. The sampling plan will also be provided in the report

and audit evidence will be provided for Vmoto Ltd. The report will include the overall

findings and analysis about the company in respect of the auditors and recommendations will

be made after a critical evaluation have been made of the financialposition of company. The

overall report will help in gaining a briefunderstanding about the various aspects and

performance measures of company.

Introduction:

The report will be providing learning over the diverse concepts of auditing. The organization

selected for the process is Vmoto Ltd. Which is an Australian company dealing with scooter

manufacturing and distribution. The report will be providing the nature of the entity and key

risks that are faced by the company in the particular market segment. The performance

analytical procedures for developing the statement of financial position will be taken into

consideration in the report. Relevant financial report assertions and the reasons for their

selections will also be done in the task. The sampling plan will also be provided in the report

and audit evidence will be provided for Vmoto Ltd. The report will include the overall

findings and analysis about the company in respect of the auditors and recommendations will

be made after a critical evaluation have been made of the financialposition of company. The

overall report will help in gaining a briefunderstanding about the various aspects and

performance measures of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 4

Content:

Understanding of the nature of the entity and its industry and then identify key business

risks along with the risk metrics:

The organization Vmoto Ltd. is occupied with the matter of assembling and offering bikes.

The significant business of the organization is to take part in assembling, creating and

marketing universally the electric controlled two-wheel vehicles, off-road vehicles and oil

vehicles. The business to which the organization has a place relates to the vehicle business

and there is mind-boggling rivalry winning in the car business of China and Australia. The

organization has been offering its items based on a unique producer hardware premise. The

geological fragment where the organization is working its business incorporates Australia and

China. The organization from the ongoing past years have been putting forth green electric

controlled bikes and has been occupied with assembling the western designed electrical bike

to cover an extensive variety of items. There are two kinds of brands through which

organization is working in the market one is Vmoto which is gone for making and creating an

incentive in Asia and the other one is Emax which is worried about focusing on western

markets (Kim, 2016).

There are roughly 40 units from where the organization is working its business which

comprises the blend of different retail outlets and the outsider merchants among China. The

organization has a limit of assembling and creating no less than 450000 of units for each

annum. The material hazard related to the business which is looked at by the organization and

that can affect the future prospects of the organization incorporates the hazard related to

innovative technological obsolescence (Lee, 2014). The tending of these issues has been

made through an interest in promoting and research, patent and enrolling the equipped and

productive experts in the workforce of an organization.

Content:

Understanding of the nature of the entity and its industry and then identify key business

risks along with the risk metrics:

The organization Vmoto Ltd. is occupied with the matter of assembling and offering bikes.

The significant business of the organization is to take part in assembling, creating and

marketing universally the electric controlled two-wheel vehicles, off-road vehicles and oil

vehicles. The business to which the organization has a place relates to the vehicle business

and there is mind-boggling rivalry winning in the car business of China and Australia. The

organization has been offering its items based on a unique producer hardware premise. The

geological fragment where the organization is working its business incorporates Australia and

China. The organization from the ongoing past years have been putting forth green electric

controlled bikes and has been occupied with assembling the western designed electrical bike

to cover an extensive variety of items. There are two kinds of brands through which

organization is working in the market one is Vmoto which is gone for making and creating an

incentive in Asia and the other one is Emax which is worried about focusing on western

markets (Kim, 2016).

There are roughly 40 units from where the organization is working its business which

comprises the blend of different retail outlets and the outsider merchants among China. The

organization has a limit of assembling and creating no less than 450000 of units for each

annum. The material hazard related to the business which is looked at by the organization and

that can affect the future prospects of the organization incorporates the hazard related to

innovative technological obsolescence (Lee, 2014). The tending of these issues has been

made through an interest in promoting and research, patent and enrolling the equipped and

productive experts in the workforce of an organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 5

The hazard can affect the long-haul maintainability of the organization in the vehicle segment

as the out-dated items won't be favoured by the clients in this industry. It tends to be seen that

the organization has been working in the business comprising of green and electric vehicle

innovation and any sort of mechanical out of date quality will significantly affect the

budgetary aftereffects of the organization in future. The danger of material misquote can be

available in the valuation of the benefits where the valuation systems as embraced by the

organization requires different suspicion to be made whose precision and adequacy can be

influenced by the objectivities and judgment of the administration making the fitting

presumptions. Anyway, the organization has been tending to this as a negligible hazard as the

organization is always checking available and building up the innovations and capacities

which are in concurrence with the most recent innovation(Vmoto Limited, 2017).

The different kinds of hazard influencing the business will incorporate natural hazard that

speaks to the defencelessness of the declaration to susceptibility accepting that there are no

inside controls working inside the endeavour. The control hazard will be related with the

actuality that the material errors won't be controlled and forestalled on an auspicious premise.

The discovery hazard, on the other hand, is related to the hazard that material error won't be

recognized by the inspectors. The different components influencing intrinsic and control

hazard includes:

Nature of the business: This will incorporate the elements, for example, nature and many-

sided quality of exchanges related to maintaining a business.

Cultural rehearses: The components influencing the related party exchanges and the

deceitful budgetary detailing will likewise shape some portion of the elements.

Experience of inspectors: The underlying review commitment and the earlier review results

will shape a premise of distinguishing and evaluating the danger of material error in the

organization and setting controls for the same (Petty, et. al., 2015).

The hazard can affect the long-haul maintainability of the organization in the vehicle segment

as the out-dated items won't be favoured by the clients in this industry. It tends to be seen that

the organization has been working in the business comprising of green and electric vehicle

innovation and any sort of mechanical out of date quality will significantly affect the

budgetary aftereffects of the organization in future. The danger of material misquote can be

available in the valuation of the benefits where the valuation systems as embraced by the

organization requires different suspicion to be made whose precision and adequacy can be

influenced by the objectivities and judgment of the administration making the fitting

presumptions. Anyway, the organization has been tending to this as a negligible hazard as the

organization is always checking available and building up the innovations and capacities

which are in concurrence with the most recent innovation(Vmoto Limited, 2017).

The different kinds of hazard influencing the business will incorporate natural hazard that

speaks to the defencelessness of the declaration to susceptibility accepting that there are no

inside controls working inside the endeavour. The control hazard will be related with the

actuality that the material errors won't be controlled and forestalled on an auspicious premise.

The discovery hazard, on the other hand, is related to the hazard that material error won't be

recognized by the inspectors. The different components influencing intrinsic and control

hazard includes:

Nature of the business: This will incorporate the elements, for example, nature and many-

sided quality of exchanges related to maintaining a business.

Cultural rehearses: The components influencing the related party exchanges and the

deceitful budgetary detailing will likewise shape some portion of the elements.

Experience of inspectors: The underlying review commitment and the earlier review results

will shape a premise of distinguishing and evaluating the danger of material error in the

organization and setting controls for the same (Petty, et. al., 2015).

Auditing 6

In connection to Vmoto Constrained the risk model [AR = f (IR x CR X DR)] has been

connected and the outcomes are drawn as under:

AR = f (IR x CR X DR)

AR = .05 (.80 x .60 X .25)

AR = .006

The risk rating in which the organization is working as a place with the medium level of

hazard as the intrinsic and control chance is making a moderate effect on the material error

occurring. The location hazard should be tried all the more oftentimes for this situation as the

controls are not executed adequately in the organization and along these lines, the recognition

of hazard winds up essential for this reality.

Analytical procedures for analysing the financial Position and financial Performance

over the last three years using appropriate ratios and metrics.

The ratio metrics will be a useful tool in analysing and assessing the company’s financial

position and performance in comparison to the industry averages and past performers. The

various ratios presented in the report will help in assessing the position concerned with

profitability, liquidity and capital position of thecompany(Vmoto Limited, 2017). The ratios

will be calculated after considering the latest annual reports and financialstatements as

presented by the company and the result will be drawn accordingly. The calculation ofvarious

in respect of Vmoto Limited for the period ending 2017, 2016 and 2015 are presented below:

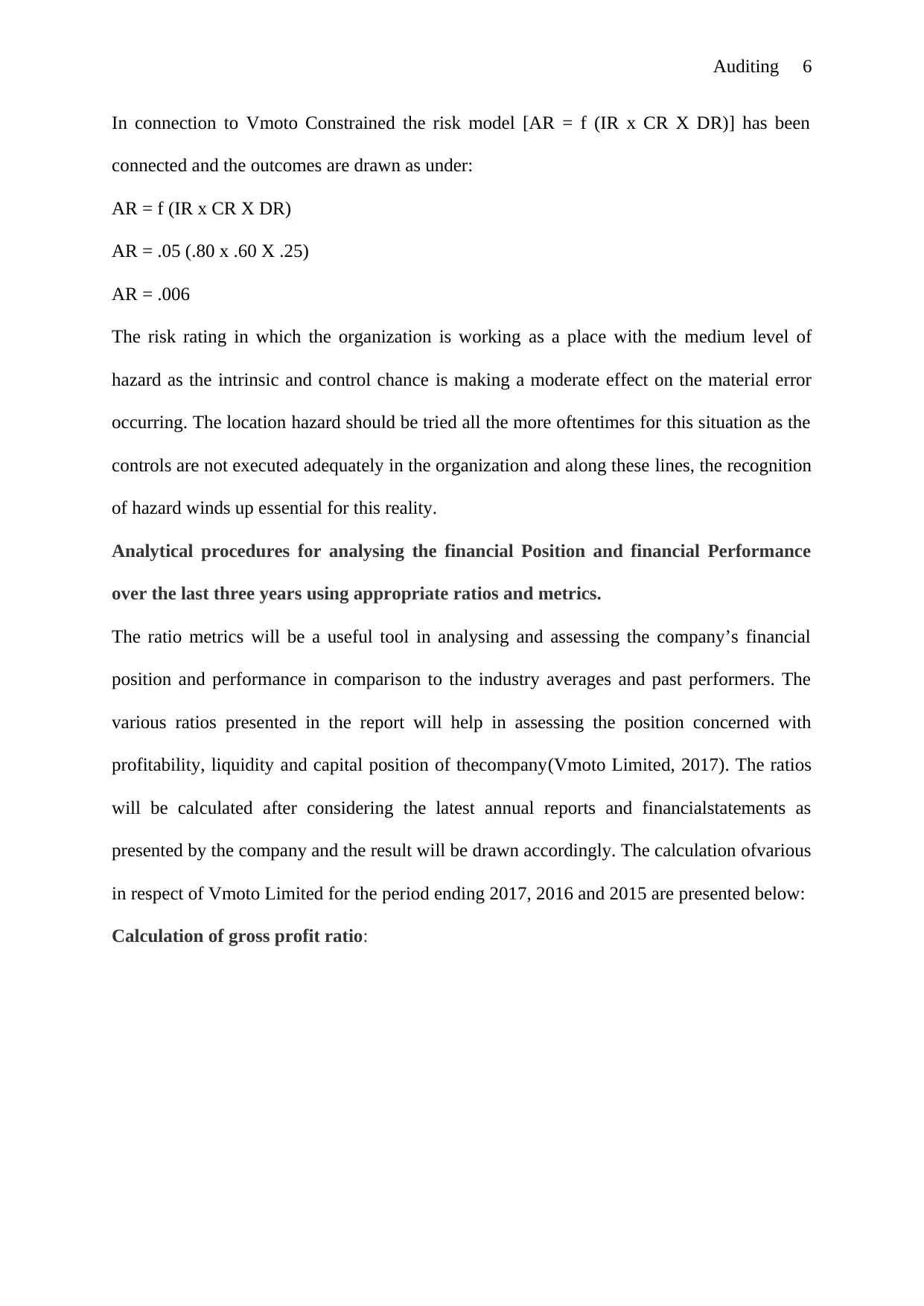

Calculation of gross profit ratio:

In connection to Vmoto Constrained the risk model [AR = f (IR x CR X DR)] has been

connected and the outcomes are drawn as under:

AR = f (IR x CR X DR)

AR = .05 (.80 x .60 X .25)

AR = .006

The risk rating in which the organization is working as a place with the medium level of

hazard as the intrinsic and control chance is making a moderate effect on the material error

occurring. The location hazard should be tried all the more oftentimes for this situation as the

controls are not executed adequately in the organization and along these lines, the recognition

of hazard winds up essential for this reality.

Analytical procedures for analysing the financial Position and financial Performance

over the last three years using appropriate ratios and metrics.

The ratio metrics will be a useful tool in analysing and assessing the company’s financial

position and performance in comparison to the industry averages and past performers. The

various ratios presented in the report will help in assessing the position concerned with

profitability, liquidity and capital position of thecompany(Vmoto Limited, 2017). The ratios

will be calculated after considering the latest annual reports and financialstatements as

presented by the company and the result will be drawn accordingly. The calculation ofvarious

in respect of Vmoto Limited for the period ending 2017, 2016 and 2015 are presented below:

Calculation of gross profit ratio:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 7

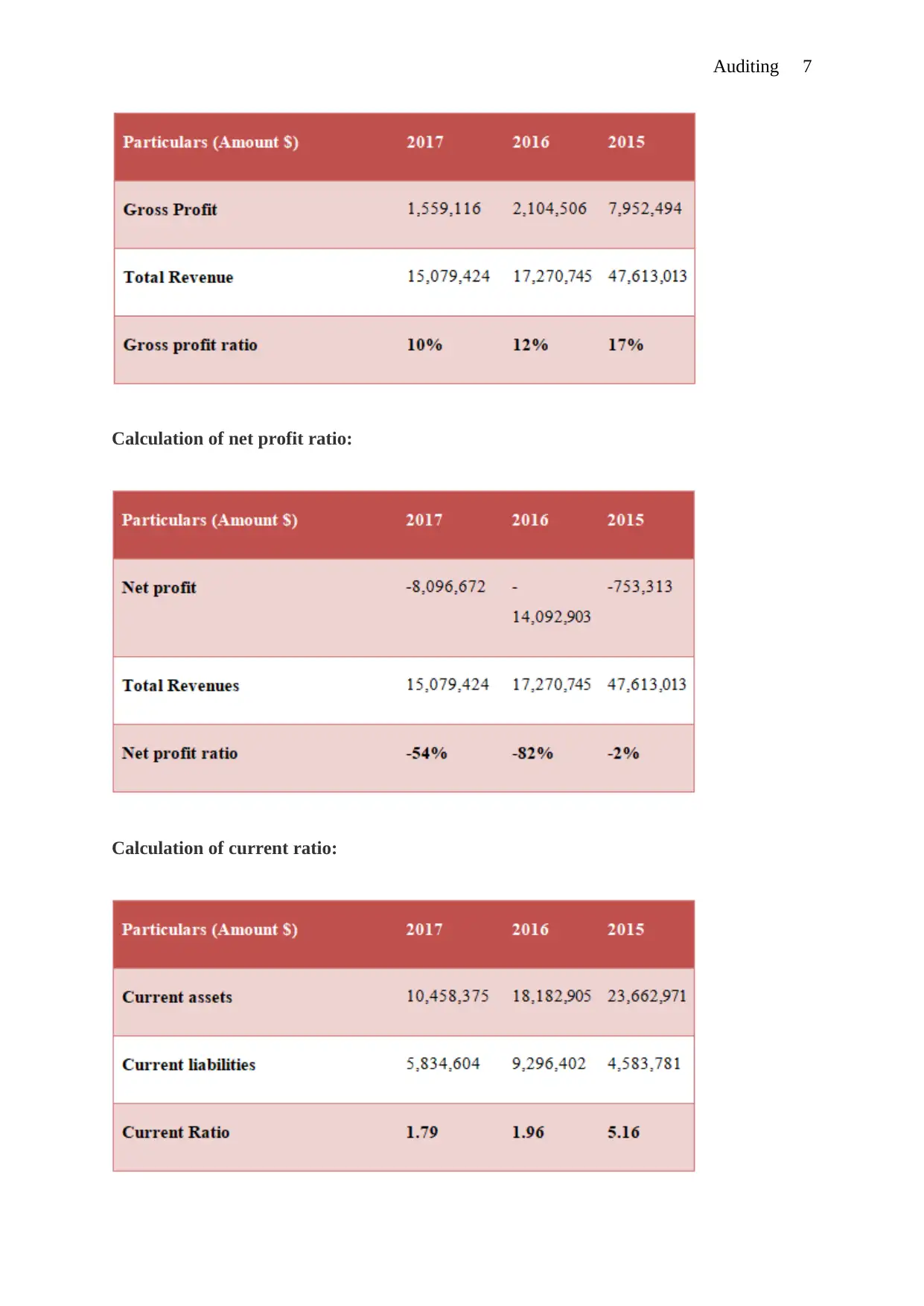

Calculation of net profit ratio:

Calculation of current ratio:

Calculation of net profit ratio:

Calculation of current ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 8

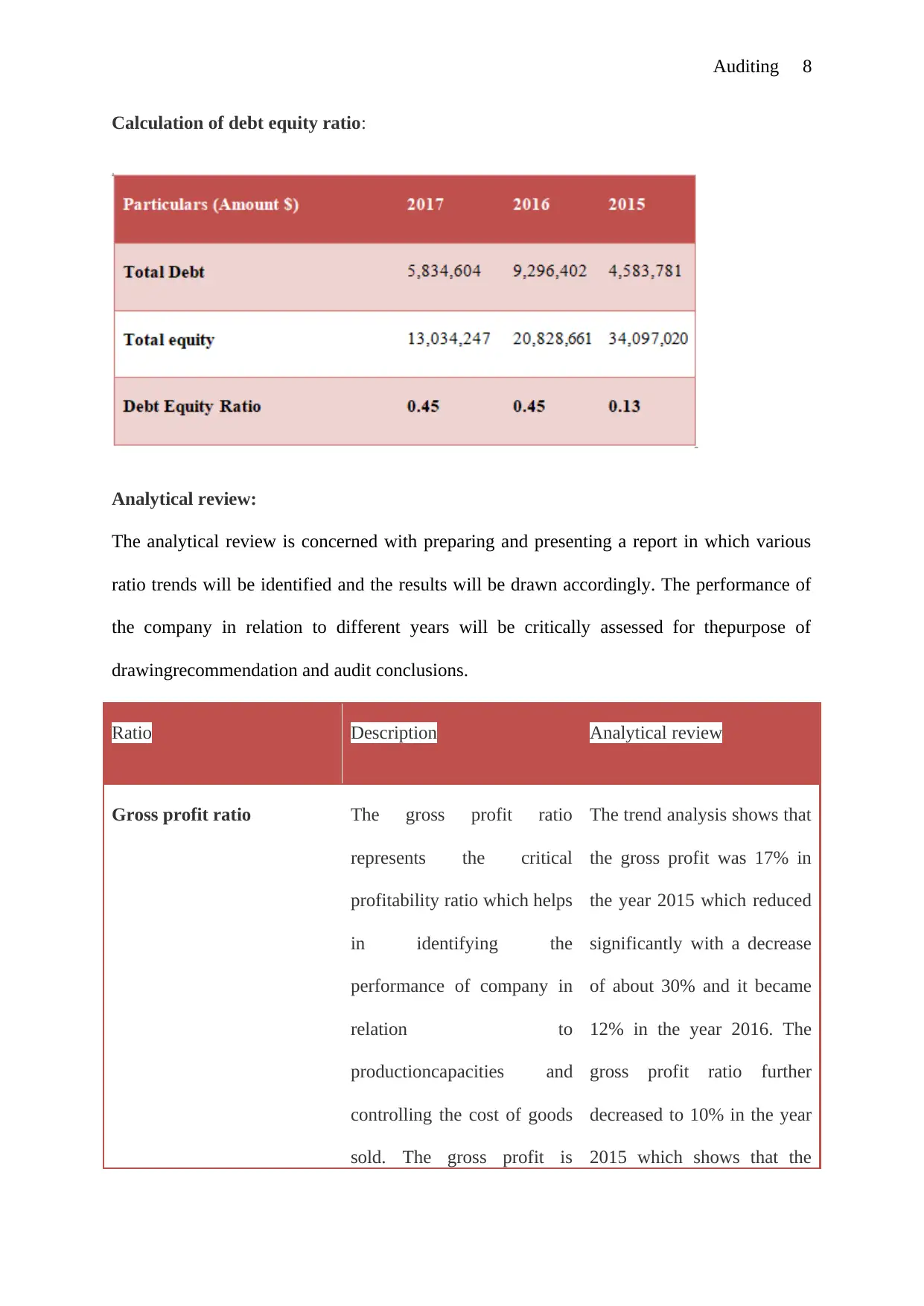

Calculation of debt equity ratio:

Analytical review:

The analytical review is concerned with preparing and presenting a report in which various

ratio trends will be identified and the results will be drawn accordingly. The performance of

the company in relation to different years will be critically assessed for thepurpose of

drawingrecommendation and audit conclusions.

Ratio Description Analytical review

Gross profit ratio The gross profit ratio

represents the critical

profitability ratio which helps

in identifying the

performance of company in

relation to

productioncapacities and

controlling the cost of goods

sold. The gross profit is

The trend analysis shows that

the gross profit was 17% in

the year 2015 which reduced

significantly with a decrease

of about 30% and it became

12% in the year 2016. The

gross profit ratio further

decreased to 10% in the year

2015 which shows that the

Calculation of debt equity ratio:

Analytical review:

The analytical review is concerned with preparing and presenting a report in which various

ratio trends will be identified and the results will be drawn accordingly. The performance of

the company in relation to different years will be critically assessed for thepurpose of

drawingrecommendation and audit conclusions.

Ratio Description Analytical review

Gross profit ratio The gross profit ratio

represents the critical

profitability ratio which helps

in identifying the

performance of company in

relation to

productioncapacities and

controlling the cost of goods

sold. The gross profit is

The trend analysis shows that

the gross profit was 17% in

the year 2015 which reduced

significantly with a decrease

of about 30% and it became

12% in the year 2016. The

gross profit ratio further

decreased to 10% in the year

2015 which shows that the

Auditing 9

worked out after considering

the cost of goods sold and it

is deducted from the

revenues obtained by

thecompanyduring the period

of reporting. The ratio is

calculated by dividing the

gross profit with revenues

obtained by the

company(Pavlova, 2017).

company was not achieving

the efficient level of cost of

goods sold in relate to

revenues achieved by

thecompany. The same can

be improved with identifying

and implementing the cost

reduction and cost control

strategies in the company.

The application of these

strategies will help in

achieving an appropriate

level of cost of goods sold

under which the gross profit

ratio will be maximum for

the company Vmoto Limited.

Net profit ratio The net profit ratio is another

way of identifying and

assessing the operational

efficiency of thecompany in

relation to industry averages

and other market factors. The

net profit ratedescribes the

operationalperformance of

The net profitability of

thecompany shows the trend

analysis associated with

operational efficiency of

thecompany. The net profit

ratio in the year 2015 was

only -2% which increased to

the loss of 82% in the year

worked out after considering

the cost of goods sold and it

is deducted from the

revenues obtained by

thecompanyduring the period

of reporting. The ratio is

calculated by dividing the

gross profit with revenues

obtained by the

company(Pavlova, 2017).

company was not achieving

the efficient level of cost of

goods sold in relate to

revenues achieved by

thecompany. The same can

be improved with identifying

and implementing the cost

reduction and cost control

strategies in the company.

The application of these

strategies will help in

achieving an appropriate

level of cost of goods sold

under which the gross profit

ratio will be maximum for

the company Vmoto Limited.

Net profit ratio The net profit ratio is another

way of identifying and

assessing the operational

efficiency of thecompany in

relation to industry averages

and other market factors. The

net profit ratedescribes the

operationalperformance of

The net profitability of

thecompany shows the trend

analysis associated with

operational efficiency of

thecompany. The net profit

ratio in the year 2015 was

only -2% which increased to

the loss of 82% in the year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 10

the company during the

reporting period. It is worked

out in the same manner as of

gross profit ratio of the

company that is by dividing

the net profitwith the

revenues achieved by the

company during the

year(Vmoto Limited, 2017).

2016. The loss further

remained at a significant

level of 54% in the year

2017. Therefore it can be

established that the company

is facing financial crunch due

to increased losses in the

current years and therefore it

is required to establish and

implement the appropriate

controlling policies to ache

higher margins of net profit.

The approach to increased

net profit can beefficient

achieved with controlling the

operating expenses and

achieving higher grossprofits.

Current ratio The liquidity position and

aspect of the company

Vmoto limited can be

analysed with the help of this

ratio. The current ratio is

determined by dividing the

current assets with the

The current ratio of the

company Vmoto limited is

1.79 in the current year 2017

which shows an adequate

position of liquidity. The

same ratio is 1.96 in the year

2016 which was significantly

the company during the

reporting period. It is worked

out in the same manner as of

gross profit ratio of the

company that is by dividing

the net profitwith the

revenues achieved by the

company during the

year(Vmoto Limited, 2017).

2016. The loss further

remained at a significant

level of 54% in the year

2017. Therefore it can be

established that the company

is facing financial crunch due

to increased losses in the

current years and therefore it

is required to establish and

implement the appropriate

controlling policies to ache

higher margins of net profit.

The approach to increased

net profit can beefficient

achieved with controlling the

operating expenses and

achieving higher grossprofits.

Current ratio The liquidity position and

aspect of the company

Vmoto limited can be

analysed with the help of this

ratio. The current ratio is

determined by dividing the

current assets with the

The current ratio of the

company Vmoto limited is

1.79 in the current year 2017

which shows an adequate

position of liquidity. The

same ratio is 1.96 in the year

2016 which was significantly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 11

current liabilities of the

company. The ratio helps in

establishing the working

capital position of company.

higher in the year 2015 that

is 5.16. The ratio above 1

represents that there are

enough and adequate assets

covering the current debt

liabilities of thecompany

Vmoto limited.

Thusthecompany is operating

sufficiently in this

aspect(Pavlova, 2017).

Debt to equity ratio The capital structuring ratio

helps in determining the

capital base with which the

company is operating I the

financial market. The debt

equity ratio helps in

assessing the efficiency with

which the capital employed

has been utilized in

thecompany associated. The

debt equity ratio of 2:1 is

considered optimum for the

companyoperating in

automobile sector(Petty,

The ratio of debt equity

remained constant in the year

2017 and 2016 in respect of

the company Vmoto limited.

The ratio was .45

whichrepresents that the debt

is employed at only half of

the amount of equity

employed in thecompany.

This has been resulting in

excessive pressure on the

operational capability as the

shareholders are expecting

higher returns. The debt

current liabilities of the

company. The ratio helps in

establishing the working

capital position of company.

higher in the year 2015 that

is 5.16. The ratio above 1

represents that there are

enough and adequate assets

covering the current debt

liabilities of thecompany

Vmoto limited.

Thusthecompany is operating

sufficiently in this

aspect(Pavlova, 2017).

Debt to equity ratio The capital structuring ratio

helps in determining the

capital base with which the

company is operating I the

financial market. The debt

equity ratio helps in

assessing the efficiency with

which the capital employed

has been utilized in

thecompany associated. The

debt equity ratio of 2:1 is

considered optimum for the

companyoperating in

automobile sector(Petty,

The ratio of debt equity

remained constant in the year

2017 and 2016 in respect of

the company Vmoto limited.

The ratio was .45

whichrepresents that the debt

is employed at only half of

the amount of equity

employed in thecompany.

This has been resulting in

excessive pressure on the

operational capability as the

shareholders are expecting

higher returns. The debt

Auditing 12

et .al., 2015). equity ratio should be

optimised at the level of 2:1

and thus more of long term

debt should be employed in

thecompany in order to

achieveminimum cost of

capital as required by

thecompany. This will also

help in maximising the

returns and increasing the

profitability of thecompany.

Materiality for planning purposes and the associated assertions in relation to Vmoto

limited:

The materiality in planning the audit work of company will be recognized as a crucial aspect

in which material accounts balances are determined with the appropriate amount of

materiality that should be examined to identify and consider the material misstatement in the

financial records of company. It can be established that there are different categories of

accounts balances as depicted in the accounts of the company and there are significant

amount of material balances which when exceeded can affect the performance and position of

the company in the industry and market concerned. The judgments about materiality will be

made in the light of the surrounding circumstances and will also be affected by the types and

nature of business transactions entered into by the company Vmoto limited. The auditors

while determining the level of materiality has to take into consideration the nature and

amount of the transaction which are happening during the reporting period. The materiality in

et .al., 2015). equity ratio should be

optimised at the level of 2:1

and thus more of long term

debt should be employed in

thecompany in order to

achieveminimum cost of

capital as required by

thecompany. This will also

help in maximising the

returns and increasing the

profitability of thecompany.

Materiality for planning purposes and the associated assertions in relation to Vmoto

limited:

The materiality in planning the audit work of company will be recognized as a crucial aspect

in which material accounts balances are determined with the appropriate amount of

materiality that should be examined to identify and consider the material misstatement in the

financial records of company. It can be established that there are different categories of

accounts balances as depicted in the accounts of the company and there are significant

amount of material balances which when exceeded can affect the performance and position of

the company in the industry and market concerned. The judgments about materiality will be

made in the light of the surrounding circumstances and will also be affected by the types and

nature of business transactions entered into by the company Vmoto limited. The auditors

while determining the level of materiality has to take into consideration the nature and

amount of the transaction which are happening during the reporting period. The materiality in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.