Valuation Report: Analysis of Vocus Group Limited's Financials

VerifiedAdded on 2020/03/16

|6

|1180

|73

Report

AI Summary

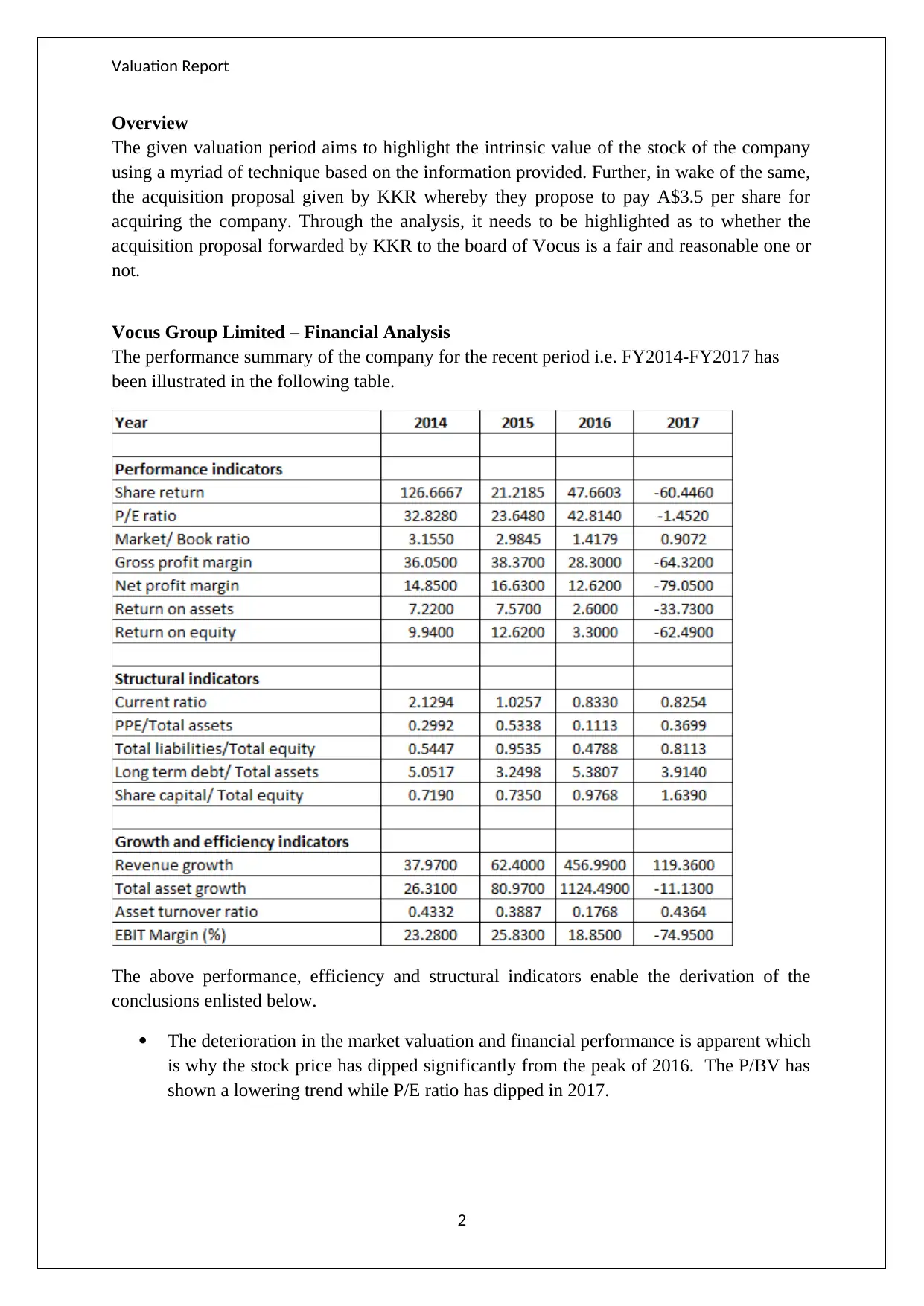

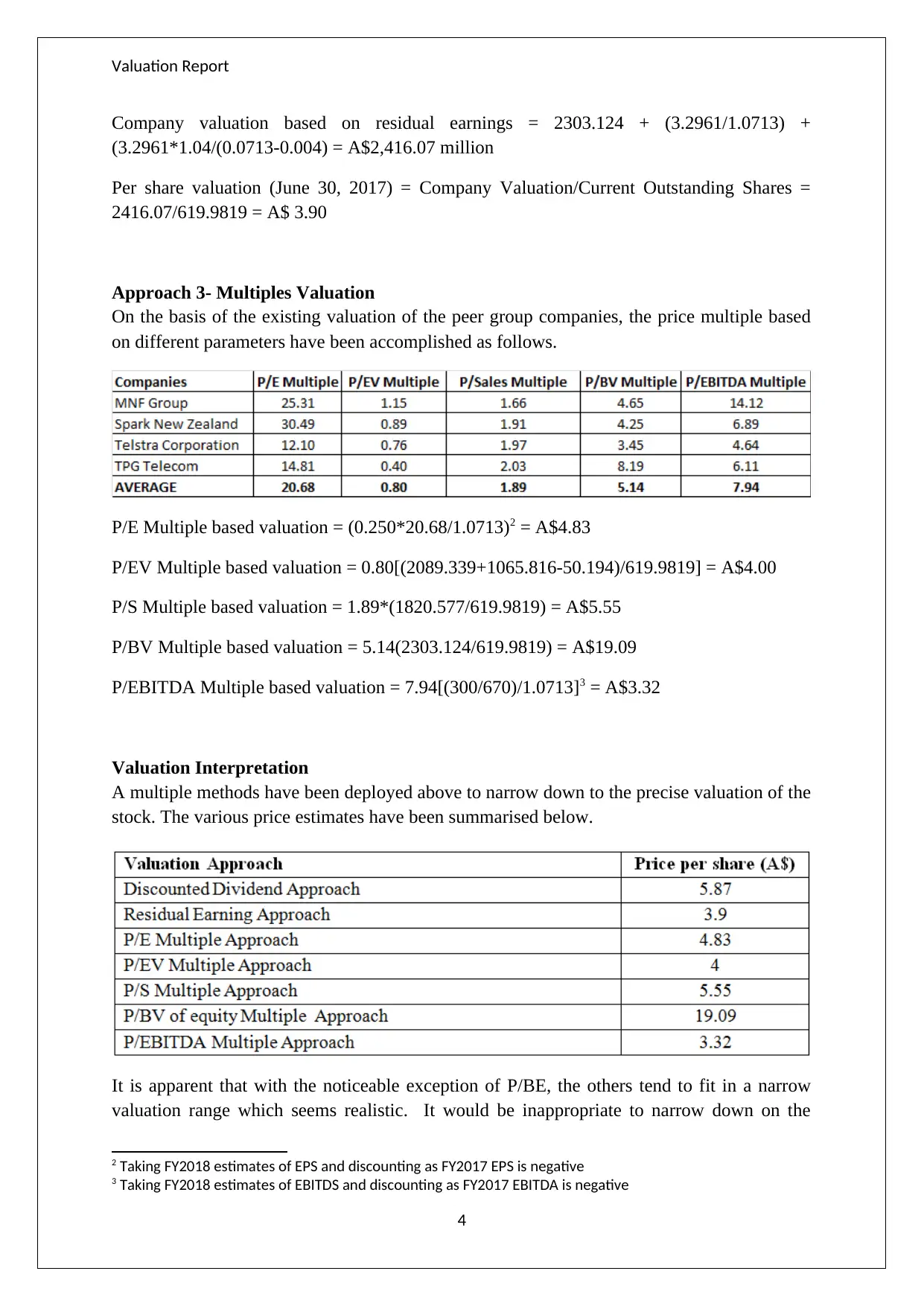

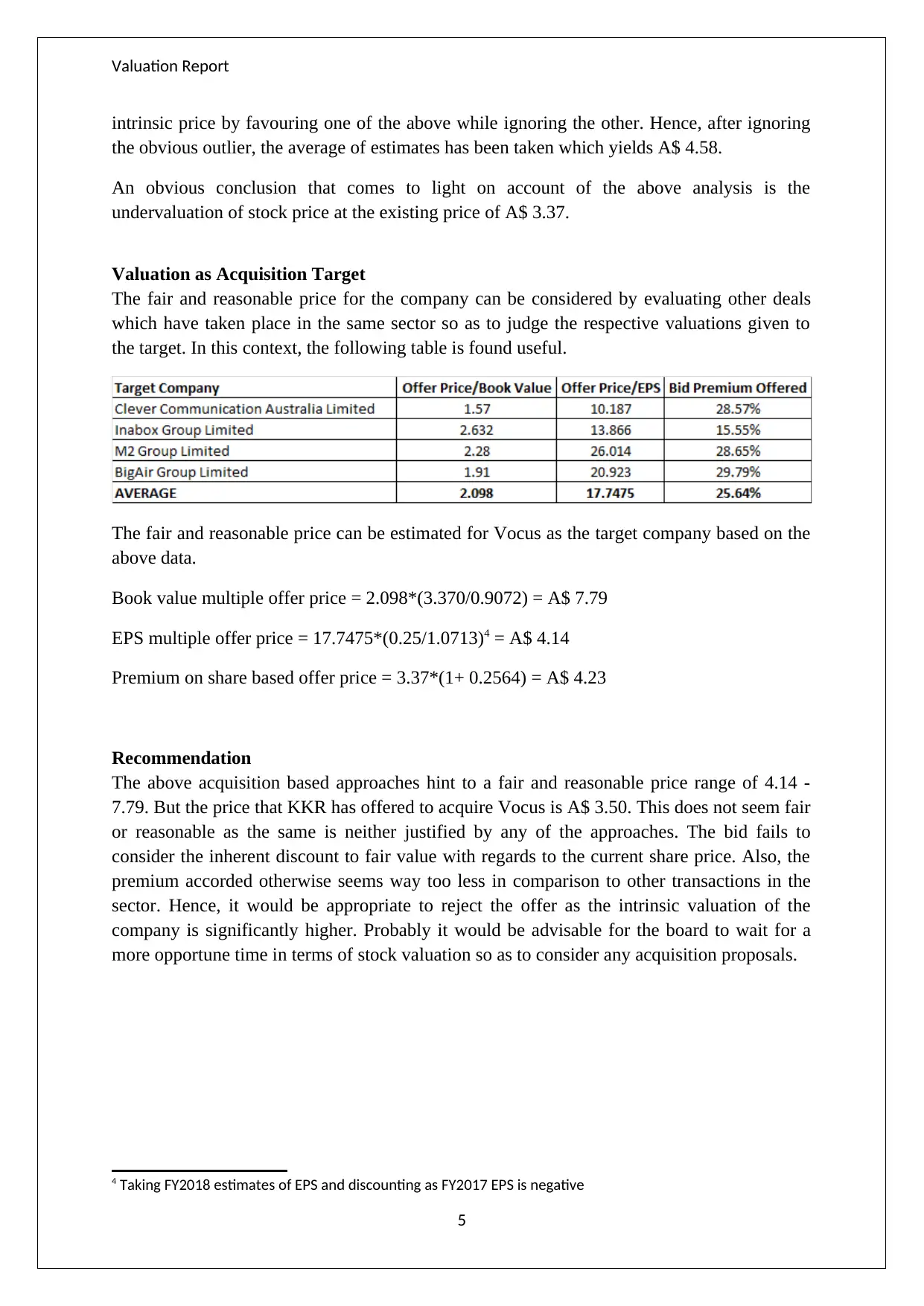

This valuation report provides a comprehensive financial analysis of Vocus Group Limited, examining its performance from FY2014 to FY2017. The report employs three primary valuation approaches: the Discounted Dividend Model, the Residual Earnings Model, and Multiples Valuation, to determine the intrinsic value of the company's stock. It calculates the estimated dividend in FY2018 using an EPS of $0.25 and a payout ratio of 50%, and also computes equity cost and residual earnings. The analysis considers factors like market valuation, revenue growth, profitability, and financial risk. Furthermore, it evaluates the acquisition proposal from KKR at A$3.5 per share, comparing it to the derived intrinsic values and similar sector deals. The report concludes that the acquisition offer is not fair and reasonable based on the valuation analysis and recommends rejecting the offer, suggesting the board wait for a more opportune time for acquisition proposals.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.