Vocus Group Limited Valuation Report: Financial Analysis and Offer

VerifiedAdded on 2020/03/16

|6

|1181

|56

Report

AI Summary

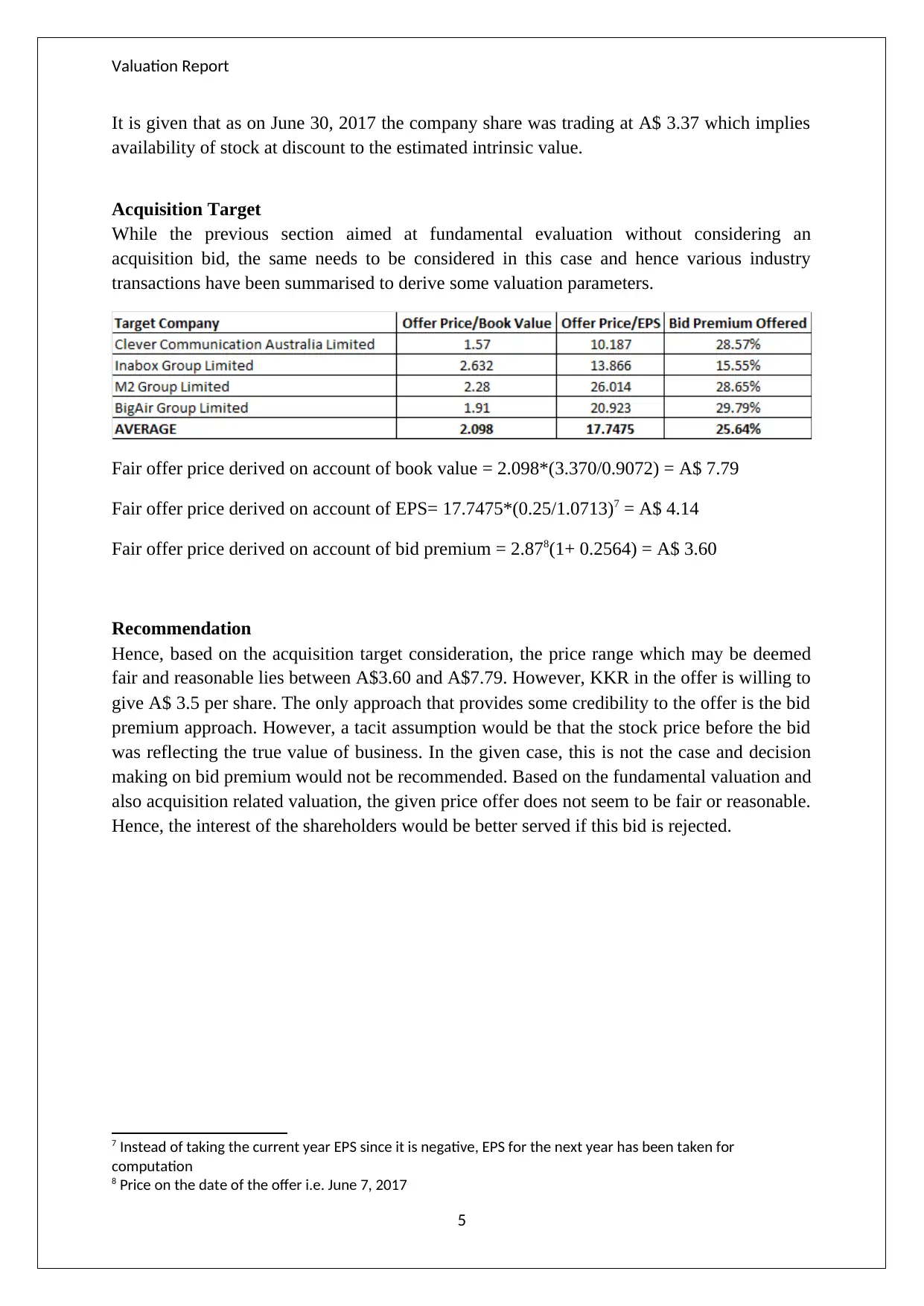

This valuation report analyzes Vocus Group Limited in response to KKR's acquisition offer of A$3.5 per share. The report begins with a performance analysis, highlighting declining profit margins and increasing debt levels. It then employs three valuation techniques: the Discounted Dividend Model, the Residual Earnings Model, and Multiples Valuation, using peer group data. The report interprets these valuations, concluding with a recommendation based on both fundamental and acquisition-related valuations. It determines the KKR offer is not fair or reasonable to shareholders and recommends its rejection. The report provides detailed calculations and assumptions for each valuation method, including the use of required returns and book value for equity. The report also considers acquisition targets and comparable transactions, including the fair offer price derived on account of book value, EPS and bid premium.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.