Financial Accounting Report: Vodafone Group PLC and Lease Accounting

VerifiedAdded on 2022/10/18

|13

|3300

|177

Report

AI Summary

This report provides a detailed analysis of Vodafone Group PLC's financial accounting practices. It begins with an overview of the company and its business operations. The report then delves into the various accounting concepts employed by Vodafone, including conservatism, accrual, entity, consistency, and going concern principles, illustrating how these concepts are applied in the company's financial reporting. Furthermore, the report examines AASB 16 (and its equivalent IFRS 16) related to lease accounting, explaining the standard's impact on Vodafone's financial statements. The report highlights how Vodafone recognizes right-of-use assets and lease liabilities, and discusses the disclosures made in its notes on accounts. The analysis also considers the materiality concept and the auditor's role in ensuring the accuracy and completeness of the financial information. Overall, the report provides a comprehensive understanding of Vodafone's financial accounting framework and its adherence to relevant accounting standards.

Running head: ADVANCE FINANCIAL ACCOUNTING

ADVANCE FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

ADVANCE FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ADVANCE FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Overview of the Company.........................................................................................................2

Accounting Concept in Business...............................................................................................2

AASB 16 – Accounting Related to Lease..................................................................................6

AASB 16/IFRS 16 in Company Financial Report.....................................................................8

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

ADVANCE FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Overview of the Company.........................................................................................................2

Accounting Concept in Business...............................................................................................2

AASB 16 – Accounting Related to Lease..................................................................................6

AASB 16/IFRS 16 in Company Financial Report.....................................................................8

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

2

ADVANCE FINANCIAL ACCOUNTING

Introduction

Accounting helps the entity to carry their accounting transaction properly in their

books of accounts as it shows all the guidelines which an entity should followed while

preparing their financial books of accounts (Beams et al., 2016). Each entity should follow all

the accounting standard in the preparation of its financial books as the accounting standard

shows about the different framework which is to be used by the entity while carrying their

business activities. Accounting standard helps the entity to present the financial statement

properly in-front of the user and help them to take proper decision in regards of the entity

information.

The report state about the entity Vodafone Group PLC and show the accounting

concept used by the entity in the preparation of its annual report. Accounting concepts helps

the entity to carry their business operation easily and also able to produce a proper amount of

information in their business statements (Gaffikin and Aitken 2014). It also shows about the

adoption of AASB 16 which is related to accounting related to lease and how the same is

been accounted by the entity in the preparation of its notes on account. It also discusses about

the disclosure which is been laid by the entity in its notes on account about the lease

accounting method used by the organization while carrying its business activities.

Overview of the Company

The assignment deals with the entity name Vodafone Group PLC which is a London

based company. The company was founded in 16 September 1991 and it having it

headquarter in London, Newbury, Berkshire, England (Annualreports.com 2019). It carries

its business operation in more than 25 countries and able to deal in Telecommunication

Business.

ADVANCE FINANCIAL ACCOUNTING

Introduction

Accounting helps the entity to carry their accounting transaction properly in their

books of accounts as it shows all the guidelines which an entity should followed while

preparing their financial books of accounts (Beams et al., 2016). Each entity should follow all

the accounting standard in the preparation of its financial books as the accounting standard

shows about the different framework which is to be used by the entity while carrying their

business activities. Accounting standard helps the entity to present the financial statement

properly in-front of the user and help them to take proper decision in regards of the entity

information.

The report state about the entity Vodafone Group PLC and show the accounting

concept used by the entity in the preparation of its annual report. Accounting concepts helps

the entity to carry their business operation easily and also able to produce a proper amount of

information in their business statements (Gaffikin and Aitken 2014). It also shows about the

adoption of AASB 16 which is related to accounting related to lease and how the same is

been accounted by the entity in the preparation of its notes on account. It also discusses about

the disclosure which is been laid by the entity in its notes on account about the lease

accounting method used by the organization while carrying its business activities.

Overview of the Company

The assignment deals with the entity name Vodafone Group PLC which is a London

based company. The company was founded in 16 September 1991 and it having it

headquarter in London, Newbury, Berkshire, England (Annualreports.com 2019). It carries

its business operation in more than 25 countries and able to deal in Telecommunication

Business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ADVANCE FINANCIAL ACCOUNTING

Accounting Concept in Business

Accounting Concept is the assumption which the entity management has taken in the

preparation of its annual report (Granof et al., 2016). This concept helps the entity to prepare

a proper financial report and help them to present a better financial information in-front of its

shareholders. Accounting concepts should be properly shown in entity financial report so that

the user will able to know what are the concepts used by the entity in regards of the

preparation of its books of accounts. Accounting concepts used by the entity has been shown

below:

Conservatism Concept - As per this concept an entity should only record the revenue in

their business when there is certainty that the entity will able to get revenue from the

transaction. In case of the expenses it should record when there is a possibility of happening

of certain event in the business (Hoyle, Schaefer and Doupnik 2015). This concept helps the

entity to have a proper amount of record in their financial information and also let them to

carry their operation easily in the industry.

The annual report of Vodafone Group PLC state that the entity has followed this

concepts properly in the preparation of its financial reports and also it able to record their

revenue when there is certainty of the happening of the income in their business activities and

it has recorded the expenses on the basis of the possibility of an event (Annualreports.com

2019). This help the users to get a proper amount of information in regards of the entity

different operations.

Accrual Concept – This concepts state that the entity should record the income only when

they able to earn the same in their business activities (Kieso, Weygandt and Warfield 2019).

In regards of the expenses the entity should record the same when there is some consumption

of asset in the accounting year. This concept state that when the company is able to receive

ADVANCE FINANCIAL ACCOUNTING

Accounting Concept in Business

Accounting Concept is the assumption which the entity management has taken in the

preparation of its annual report (Granof et al., 2016). This concept helps the entity to prepare

a proper financial report and help them to present a better financial information in-front of its

shareholders. Accounting concepts should be properly shown in entity financial report so that

the user will able to know what are the concepts used by the entity in regards of the

preparation of its books of accounts. Accounting concepts used by the entity has been shown

below:

Conservatism Concept - As per this concept an entity should only record the revenue in

their business when there is certainty that the entity will able to get revenue from the

transaction. In case of the expenses it should record when there is a possibility of happening

of certain event in the business (Hoyle, Schaefer and Doupnik 2015). This concept helps the

entity to have a proper amount of record in their financial information and also let them to

carry their operation easily in the industry.

The annual report of Vodafone Group PLC state that the entity has followed this

concepts properly in the preparation of its financial reports and also it able to record their

revenue when there is certainty of the happening of the income in their business activities and

it has recorded the expenses on the basis of the possibility of an event (Annualreports.com

2019). This help the users to get a proper amount of information in regards of the entity

different operations.

Accrual Concept – This concepts state that the entity should record the income only when

they able to earn the same in their business activities (Kieso, Weygandt and Warfield 2019).

In regards of the expenses the entity should record the same when there is some consumption

of asset in the accounting year. This concept state that when the company is able to receive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ADVANCE FINANCIAL ACCOUNTING

the cash from its customers or it able to pay to its suppliers than only the entity should record

the same in their books of account. This helps the entity to record the inflow and outflow of

cash in the business.

Vodafone Group PLC financial report shows that the entity has followed this concept

while preparing their financial statement as it has recorded many transactions on the basis of

accrual in their books of accounts (Annualreports.com 2019). These help the entity to provide

proper amount of information related to there business activities and also assists the user to

gain proper understanding of the business activities.

Entity Concept – This concept state the entity should had carry their operation separately

from the owners (Maynard 2017). As the entity should carry their operation keeping this

concept into their business activities. This help them to show the separate legal entity of both

the owner and the entity.

The company financial statement shows that they have followed these concepts in the

preparation of financial statement as the business income and the shareholder profit is shown

separately in the entity business activities (Annualreports.com 2019). As the shareholder

income is shown separately which signify that this concept is properly followed by the entity.

Consistency Concept – Entity should follow same accounting policy in each year as this

help them to give a proper understanding to the financial user about the different aspects of

entity activities (Meyer and Meyer 2014). This also help the user to compare the financial

report properly as all the report are been based upon same accounting policy which let the

user to easily compare the same in their business activities. It also helps the management to

minimize the amount of risk in the business activities.

Company annual report shows that there is no change in the accounting policy in

current year which signify that the entity is able to corporate this concept easily in their

ADVANCE FINANCIAL ACCOUNTING

the cash from its customers or it able to pay to its suppliers than only the entity should record

the same in their books of account. This helps the entity to record the inflow and outflow of

cash in the business.

Vodafone Group PLC financial report shows that the entity has followed this concept

while preparing their financial statement as it has recorded many transactions on the basis of

accrual in their books of accounts (Annualreports.com 2019). These help the entity to provide

proper amount of information related to there business activities and also assists the user to

gain proper understanding of the business activities.

Entity Concept – This concept state the entity should had carry their operation separately

from the owners (Maynard 2017). As the entity should carry their operation keeping this

concept into their business activities. This help them to show the separate legal entity of both

the owner and the entity.

The company financial statement shows that they have followed these concepts in the

preparation of financial statement as the business income and the shareholder profit is shown

separately in the entity business activities (Annualreports.com 2019). As the shareholder

income is shown separately which signify that this concept is properly followed by the entity.

Consistency Concept – Entity should follow same accounting policy in each year as this

help them to give a proper understanding to the financial user about the different aspects of

entity activities (Meyer and Meyer 2014). This also help the user to compare the financial

report properly as all the report are been based upon same accounting policy which let the

user to easily compare the same in their business activities. It also helps the management to

minimize the amount of risk in the business activities.

Company annual report shows that there is no change in the accounting policy in

current year which signify that the entity is able to corporate this concept easily in their

5

ADVANCE FINANCIAL ACCOUNTING

business activities (Annualreports.com 2019). This also state the financial user will able to

gain a proper understanding of the business and other aspects with the analysis of its annual

report.

Going Concern Concept – An entity prepares their financial statement on the basis of that

the company will carry their business activities for a longer period of time (Momblanch et al.,

2014). As on the basis of which the accounting transaction are carried by the entity. Investors

invest their money upon the company and able to earn proper amount of return from the

company so if the entity is not able to carry their business activities for a longer period than it

will the overall investors of the company.

As per the financial statement of the entity it can be seen that the entity is able to

apply this concept in their financial statement (Annualreports.com 2019). It is the duty of the

auditor to check the going concern principle among the entity and how the company has

disclosed the same in their books of accounts. As per the disclosure given by the auditor in

regards of entity financial information as it shows the factor which can affect the going

concern concept in the entity business. These are the factor which can directly affect the

going concern factor in the entity and may result in in closure of the business activities. This

also help the user to get a proper understanding of the entity business and help them to take

decision in regards of the same.

ADVANCE FINANCIAL ACCOUNTING

business activities (Annualreports.com 2019). This also state the financial user will able to

gain a proper understanding of the business and other aspects with the analysis of its annual

report.

Going Concern Concept – An entity prepares their financial statement on the basis of that

the company will carry their business activities for a longer period of time (Momblanch et al.,

2014). As on the basis of which the accounting transaction are carried by the entity. Investors

invest their money upon the company and able to earn proper amount of return from the

company so if the entity is not able to carry their business activities for a longer period than it

will the overall investors of the company.

As per the financial statement of the entity it can be seen that the entity is able to

apply this concept in their financial statement (Annualreports.com 2019). It is the duty of the

auditor to check the going concern principle among the entity and how the company has

disclosed the same in their books of accounts. As per the disclosure given by the auditor in

regards of entity financial information as it shows the factor which can affect the going

concern concept in the entity business. These are the factor which can directly affect the

going concern factor in the entity and may result in in closure of the business activities. This

also help the user to get a proper understanding of the entity business and help them to take

decision in regards of the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ADVANCE FINANCIAL ACCOUNTING

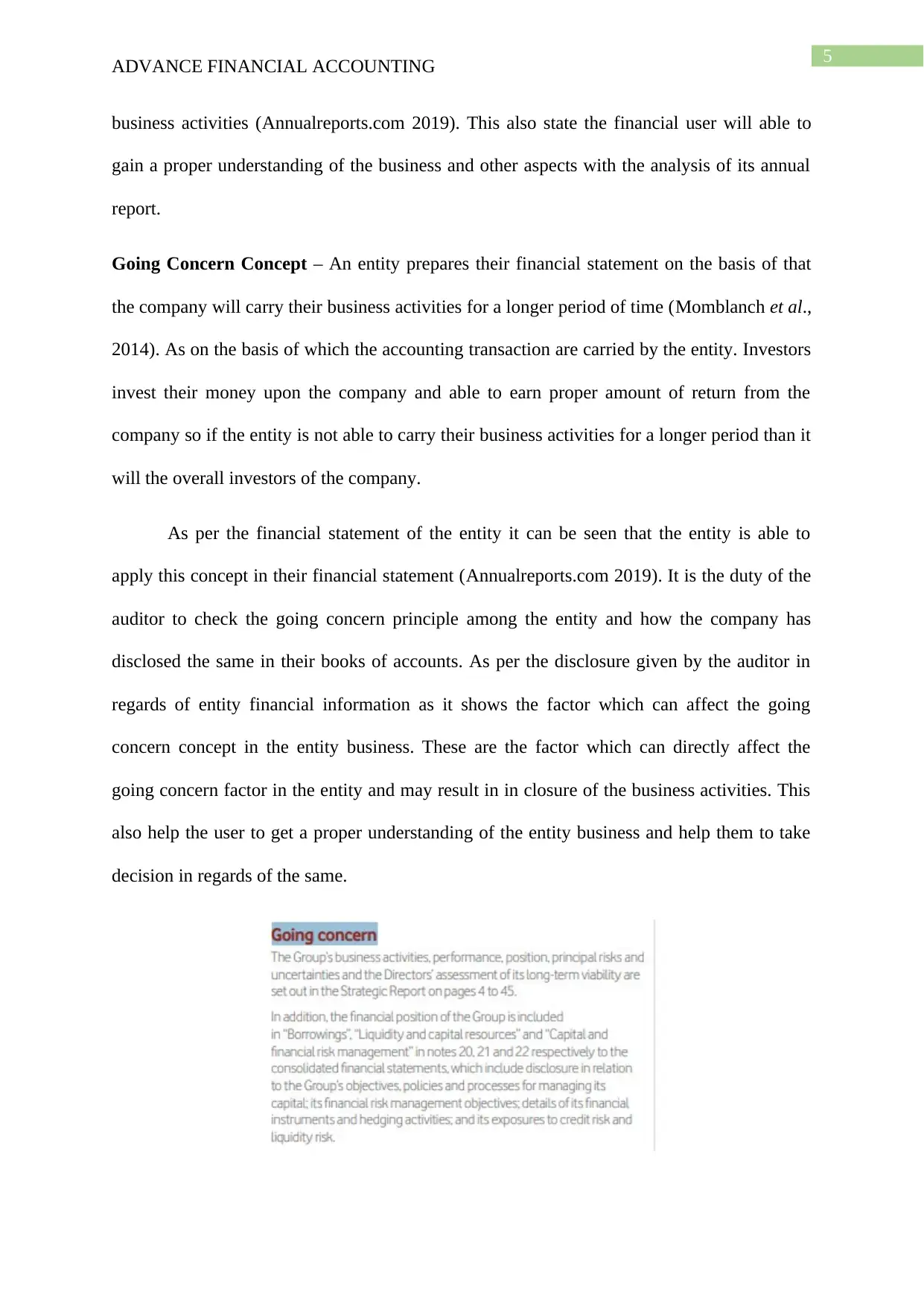

Figure: 1

(Source: Annualreports.com 2019)

Materiality Concept – All the information should be given by the entity in their financial

statement which shows a proper picture of the organization to the investors and other users.

As if the entity has omitted some information than it can have a materiality impact upon the

financial report (Parker and Northcott 2016). Auditor has to ascertain that the company books

of account are free from any kind of materiality and all the important information are

properly shown by the entity in their financial statement.

As per the auditor report the company accounts are free from material misstatement

and the entity is able to show all the required amount of information in their financial

statement (Annualreports.com 2019). This helps them to give a proper amount of information

to the investors and help them to get a proper view of the financial health of the entity.

AASB 16 – Accounting Related to Lease

This accounting standard is able to remove the AASB 117 as it does not able to have

proper amount of information inn regards of the valuation of the lease. In this standard the

framework came up with the issue of single lease accounting model as this make the

accounting for lease easy for the entity (Ramirez 2015). All the lease which are issued by the

lessee and the duration is more than 12 months than proper recording of asset and liabilities

should be done the lessee in their books of accounts. It can escape from this rule if the

underlying value of the asset is very low than it can skip the accounting of asset and liability

in their business activities.

The entity should treat the right-of-use asset similar to the valuation of other non-

financial asset and same goes with the right of use liability in the business activities

(Schaltegger and Burritt 2017). The lessee should recognize the interest on lease liability as

ADVANCE FINANCIAL ACCOUNTING

Figure: 1

(Source: Annualreports.com 2019)

Materiality Concept – All the information should be given by the entity in their financial

statement which shows a proper picture of the organization to the investors and other users.

As if the entity has omitted some information than it can have a materiality impact upon the

financial report (Parker and Northcott 2016). Auditor has to ascertain that the company books

of account are free from any kind of materiality and all the important information are

properly shown by the entity in their financial statement.

As per the auditor report the company accounts are free from material misstatement

and the entity is able to show all the required amount of information in their financial

statement (Annualreports.com 2019). This helps them to give a proper amount of information

to the investors and help them to get a proper view of the financial health of the entity.

AASB 16 – Accounting Related to Lease

This accounting standard is able to remove the AASB 117 as it does not able to have

proper amount of information inn regards of the valuation of the lease. In this standard the

framework came up with the issue of single lease accounting model as this make the

accounting for lease easy for the entity (Ramirez 2015). All the lease which are issued by the

lessee and the duration is more than 12 months than proper recording of asset and liabilities

should be done the lessee in their books of accounts. It can escape from this rule if the

underlying value of the asset is very low than it can skip the accounting of asset and liability

in their business activities.

The entity should treat the right-of-use asset similar to the valuation of other non-

financial asset and same goes with the right of use liability in the business activities

(Schaltegger and Burritt 2017). The lessee should recognize the interest on lease liability as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ADVANCE FINANCIAL ACCOUNTING

well as the amount of depreciation charged upon the right of use asset and should record the

same in their business activities. It should apply AASB 107 while preparing the cash flow

statement of the entity.

Initially the asset and liability related to the lease are recorded on present value basis

(Aasb.gov.au 2019). The measurement will include many activities such as payment made for

the extension of the lease as well as non-cancellable lease payment.

The amount of disclosure in regards of the lessee has been incorporated in AASB 16

which was not there in AASB 117 (Aasb.gov.au 2019). The information which should be

given by the lessee is solely depend upon the human judgement as the amount which the

lessee finds out to be sufficient should be given in its financial statement. It should state the

effect which the lease will make upon the financial performance, financial position and also

the cash flow statement.

It also carries the lessor requirement which was there in AASB 117. It defines the

lessor that it should differentiate the lease as operating and finance lease (Sedki, Smith and

Strickland 2014). Entity should give proper amount of disclosure about the lease it has

selected and why it has termed it as operating or finance lease.

This standard has also focus upon the amount of disclosure which should be given by

the lessor which can improve the overall understandability of the lease accounting treatment

in the business and help the user to get proper knowledge of the same. It also helps the user to

know the amount of risk which is associated in entity business and how it able to deal with

the same (Aasb.gov.au 2019). The residual value which the lessor will get should also be

presented properly in the disclosure as it give a proper amount of information to each user of

the business financial report.

ADVANCE FINANCIAL ACCOUNTING

well as the amount of depreciation charged upon the right of use asset and should record the

same in their business activities. It should apply AASB 107 while preparing the cash flow

statement of the entity.

Initially the asset and liability related to the lease are recorded on present value basis

(Aasb.gov.au 2019). The measurement will include many activities such as payment made for

the extension of the lease as well as non-cancellable lease payment.

The amount of disclosure in regards of the lessee has been incorporated in AASB 16

which was not there in AASB 117 (Aasb.gov.au 2019). The information which should be

given by the lessee is solely depend upon the human judgement as the amount which the

lessee finds out to be sufficient should be given in its financial statement. It should state the

effect which the lease will make upon the financial performance, financial position and also

the cash flow statement.

It also carries the lessor requirement which was there in AASB 117. It defines the

lessor that it should differentiate the lease as operating and finance lease (Sedki, Smith and

Strickland 2014). Entity should give proper amount of disclosure about the lease it has

selected and why it has termed it as operating or finance lease.

This standard has also focus upon the amount of disclosure which should be given by

the lessor which can improve the overall understandability of the lease accounting treatment

in the business and help the user to get proper knowledge of the same. It also helps the user to

know the amount of risk which is associated in entity business and how it able to deal with

the same (Aasb.gov.au 2019). The residual value which the lessor will get should also be

presented properly in the disclosure as it give a proper amount of information to each user of

the business financial report.

8

ADVANCE FINANCIAL ACCOUNTING

AASB 16/IFRS 16 in Company Financial Report

The annual report of Vodafone Group PLC shows that the entity does not follow

AASB 16 as it is not Australian based company but it follows the rules and norms mentioned

in IFRS 16 which is also related to the accounting for lease.

As per the notes of account given regards of the lease it shows that the entity has

followed all the accounting treatment in regards of the lease (Simkin, Norman and Rose

2014). It gives an change in regards of the lease account as it should recognise the right of

use of asset as it records the non-financial asset.

The financial information state that right of use of asset is recorded for the lease asset

in its Group (Aasb.gov.au 2019). Company is not having any lease asset currently in the

group in regards of the operating lease.

Liabilities has been recorded for future lease payment in their Group Consolidated

Statement, it also includes the reason certain period in regards of the lease in their books of

account (Sledgianowski, Gomaa and Tan 2017). Currently no liability is been recorded in

regards of future lease payment that are been disclosed as commitments, the amount of lease

liability will not be same as the it is been reported on 31st March 2019.

Lease expense denote the amount of depreciation done in the lease asset and also the

amount of the interest will be higher in early stage of the lease and it will decrease in

upcoming time (Annualreports.com 2019). The operating lease rentals are accounted with the

help of straight-line basis which is carried over the lease term as operating expenses.

The cash flow related to operating lease is been included in the operating cash flow

statement in their consolidated cash flow statement (Warren Jr, Moffitt and Byrnes 2015).

The financing activities also show about the repayment of lease liability carried by the entity.

ADVANCE FINANCIAL ACCOUNTING

AASB 16/IFRS 16 in Company Financial Report

The annual report of Vodafone Group PLC shows that the entity does not follow

AASB 16 as it is not Australian based company but it follows the rules and norms mentioned

in IFRS 16 which is also related to the accounting for lease.

As per the notes of account given regards of the lease it shows that the entity has

followed all the accounting treatment in regards of the lease (Simkin, Norman and Rose

2014). It gives an change in regards of the lease account as it should recognise the right of

use of asset as it records the non-financial asset.

The financial information state that right of use of asset is recorded for the lease asset

in its Group (Aasb.gov.au 2019). Company is not having any lease asset currently in the

group in regards of the operating lease.

Liabilities has been recorded for future lease payment in their Group Consolidated

Statement, it also includes the reason certain period in regards of the lease in their books of

account (Sledgianowski, Gomaa and Tan 2017). Currently no liability is been recorded in

regards of future lease payment that are been disclosed as commitments, the amount of lease

liability will not be same as the it is been reported on 31st March 2019.

Lease expense denote the amount of depreciation done in the lease asset and also the

amount of the interest will be higher in early stage of the lease and it will decrease in

upcoming time (Annualreports.com 2019). The operating lease rentals are accounted with the

help of straight-line basis which is carried over the lease term as operating expenses.

The cash flow related to operating lease is been included in the operating cash flow

statement in their consolidated cash flow statement (Warren Jr, Moffitt and Byrnes 2015).

The financing activities also show about the repayment of lease liability carried by the entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ADVANCE FINANCIAL ACCOUNTING

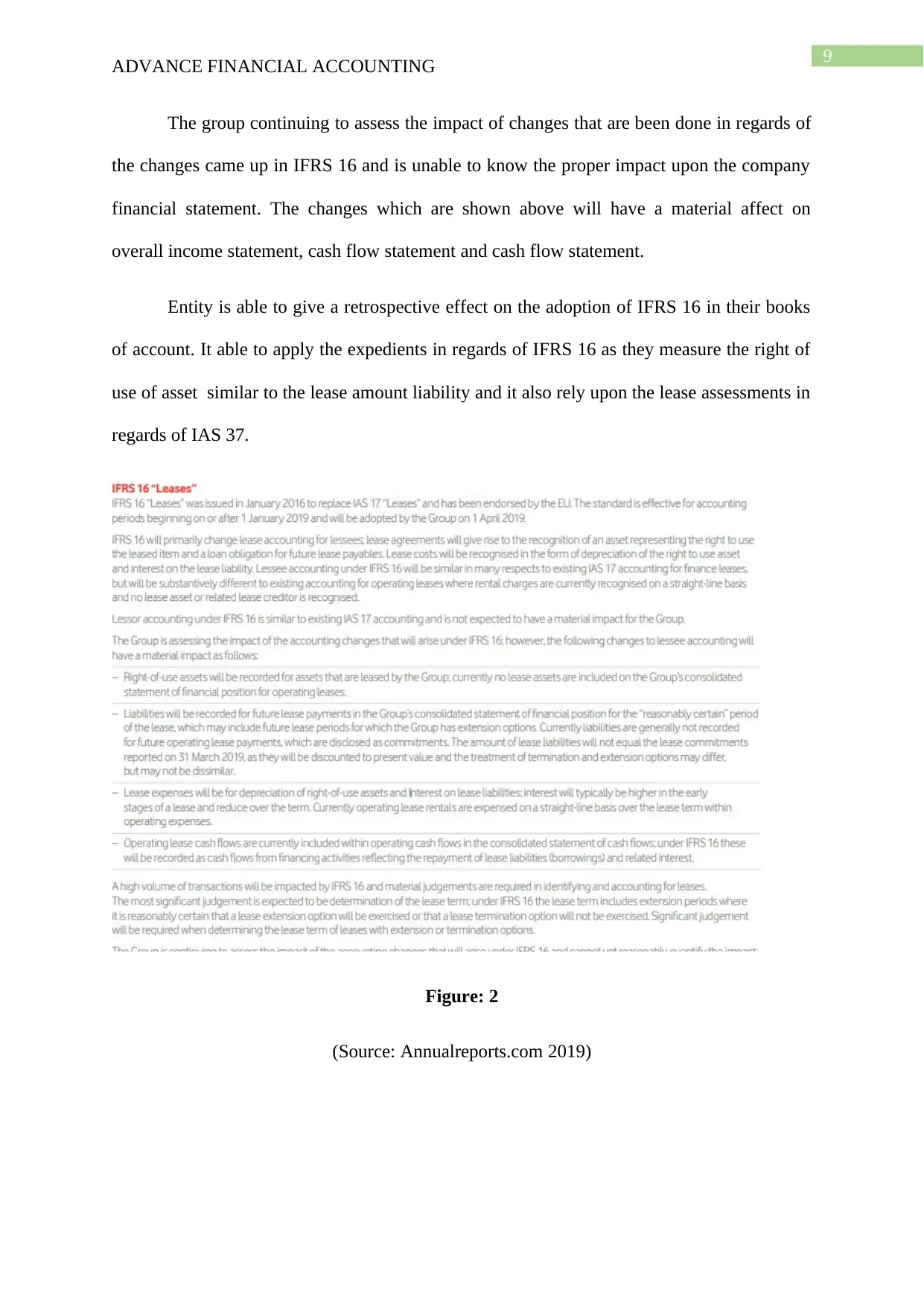

The group continuing to assess the impact of changes that are been done in regards of

the changes came up in IFRS 16 and is unable to know the proper impact upon the company

financial statement. The changes which are shown above will have a material affect on

overall income statement, cash flow statement and cash flow statement.

Entity is able to give a retrospective effect on the adoption of IFRS 16 in their books

of account. It able to apply the expedients in regards of IFRS 16 as they measure the right of

use of asset similar to the lease amount liability and it also rely upon the lease assessments in

regards of IAS 37.

Figure: 2

(Source: Annualreports.com 2019)

ADVANCE FINANCIAL ACCOUNTING

The group continuing to assess the impact of changes that are been done in regards of

the changes came up in IFRS 16 and is unable to know the proper impact upon the company

financial statement. The changes which are shown above will have a material affect on

overall income statement, cash flow statement and cash flow statement.

Entity is able to give a retrospective effect on the adoption of IFRS 16 in their books

of account. It able to apply the expedients in regards of IFRS 16 as they measure the right of

use of asset similar to the lease amount liability and it also rely upon the lease assessments in

regards of IAS 37.

Figure: 2

(Source: Annualreports.com 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ADVANCE FINANCIAL ACCOUNTING

Conclusion

On a conclusive note, it states about the important of financial accounting respect of

an entity. As financial accounting helps the entity to prepare a proper financial statement and

able to follow all the rule and norms which are been listed in different accounting standard. It

shows about Vodafone Group Plc which is a technology based company and carry its

business operation worldwide. The report discusses about the different accounting concepts

used by the entity and how the entity is able to carry its business activities properly with the

help of different accounting concepts. Some concepts which are shown are materiality

concept as this concept states that the entity should record all the information properly in

their business activities and also entity should give proper disclosure about their business

activities.

The assessment also shows the changes that are incorporated in AASB 16 Accounting

for Lease. As this standard show all the factor which the company should consider will

carrying the accounting treatment in regards of the lease as well as the reason for the adoption

of new standard in company conceptual framework. It also states about the IFRS 16 as the

company is not able to adopt with the AASB but they are following with IFRS 16 which also

state the accounting treatment in regards of the lease. As it shows the disclosure which are

given by the entity in regards of lease and how the company is able to carry its business

activities by following this accounting standard.

ADVANCE FINANCIAL ACCOUNTING

Conclusion

On a conclusive note, it states about the important of financial accounting respect of

an entity. As financial accounting helps the entity to prepare a proper financial statement and

able to follow all the rule and norms which are been listed in different accounting standard. It

shows about Vodafone Group Plc which is a technology based company and carry its

business operation worldwide. The report discusses about the different accounting concepts

used by the entity and how the entity is able to carry its business activities properly with the

help of different accounting concepts. Some concepts which are shown are materiality

concept as this concept states that the entity should record all the information properly in

their business activities and also entity should give proper disclosure about their business

activities.

The assessment also shows the changes that are incorporated in AASB 16 Accounting

for Lease. As this standard show all the factor which the company should consider will

carrying the accounting treatment in regards of the lease as well as the reason for the adoption

of new standard in company conceptual framework. It also states about the IFRS 16 as the

company is not able to adopt with the AASB but they are following with IFRS 16 which also

state the accounting treatment in regards of the lease. As it shows the disclosure which are

given by the entity in regards of lease and how the company is able to carry its business

activities by following this accounting standard.

11

ADVANCE FINANCIAL ACCOUNTING

Reference

Aasb.gov.au 2019. [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 27 Sep.

2019].

Annualreports.com 2019. [online] Annualreports.com. Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_VOD_2018.pdf

[Accessed 27 Sep. 2019].

Beams, F.A., Anthony, J.H., Bettinghaus, B. and Smith, K.A., 2016. Advanced accounting.

Pearson Education Limited 2018.

Gaffikin, M. and Aitken, M. eds., 2014. The Development of Accounting Theory (RLE

Accounting): Significant Contributors to Accounting Thought in the 20th Century. Routledge.

Granof, M.H., Khumawala, S.B., Calabrese, T.D. and Smith, D.L., 2016. Government and

Not-for-Profit Accounting, Binder Ready Version: Concepts and Practices. John Wiley &

Sons.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2019. Intermediate accounting. John Wiley

& Sons.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Meyer, M.J. and Meyer, T.S., 2014. Accounting case search: A web-based search tool for

finding published accounting cases. Journal of Accounting Education, 32(4), pp.16-23.

ADVANCE FINANCIAL ACCOUNTING

Reference

Aasb.gov.au 2019. [online] Aasb.gov.au. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 27 Sep.

2019].

Annualreports.com 2019. [online] Annualreports.com. Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/LSE_VOD_2018.pdf

[Accessed 27 Sep. 2019].

Beams, F.A., Anthony, J.H., Bettinghaus, B. and Smith, K.A., 2016. Advanced accounting.

Pearson Education Limited 2018.

Gaffikin, M. and Aitken, M. eds., 2014. The Development of Accounting Theory (RLE

Accounting): Significant Contributors to Accounting Thought in the 20th Century. Routledge.

Granof, M.H., Khumawala, S.B., Calabrese, T.D. and Smith, D.L., 2016. Government and

Not-for-Profit Accounting, Binder Ready Version: Concepts and Practices. John Wiley &

Sons.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2019. Intermediate accounting. John Wiley

& Sons.

Maynard, J., 2017. Financial accounting, reporting, and analysis. Oxford University Press.

Meyer, M.J. and Meyer, T.S., 2014. Accounting case search: A web-based search tool for

finding published accounting cases. Journal of Accounting Education, 32(4), pp.16-23.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.