Financial Performance Analysis Report: Vodafone PLC (2012-2014)

VerifiedAdded on 2019/12/03

|22

|4184

|320

Report

AI Summary

This report provides a comprehensive financial performance analysis of Vodafone PLC, examining its financial statements and key ratios over a three-year period (2012-2014). The report begins with an introduction to the importance of financial information and the purpose of financial statements, including the balance sheet, cash flow statement, and income statement. It defines essential accounting terminology such as debit, credit, books of prime entry, accounts, ledgers, and trial balance. The report then compares Vodafone, a public limited company, with other business structures, such as sole traders and partnerships, highlighting their key differences. The core of the report involves a detailed ratio analysis, calculating and interpreting profitability (gross profit margin, operating profit margin, ROCE), liquidity (current ratio, quick ratio), efficiency (receivable days, payable days, inventory days), gearing, and investor ratios (dividend yield, earnings per share, price earnings ratio). The analysis includes calculations and interpretations, drawing conclusions about Vodafone's financial health, competitive position, and shareholder value. The report concludes with an assessment of Vodafone's financial performance, comparing it to a competitor (Deutsche Telekom) and providing insights for potential investors.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................1

Task 1...............................................................................................................................................1

Task 2...............................................................................................................................................2

Task 3...............................................................................................................................................3

Task 4 calculation in appendix........................................................................................................5

.........................................................................................................................................................5

Task 5...............................................................................................................................................5

Task 6 ..............................................................................................................................................6

References........................................................................................................................................1

Appendix..........................................................................................................................................1

Introduction......................................................................................................................................1

Task 1...............................................................................................................................................1

Task 2...............................................................................................................................................2

Task 3...............................................................................................................................................3

Task 4 calculation in appendix........................................................................................................5

.........................................................................................................................................................5

Task 5...............................................................................................................................................5

Task 6 ..............................................................................................................................................6

References........................................................................................................................................1

Appendix..........................................................................................................................................1

Introduction

Financial information produced from the financial statements is of great importance for

the company. It helps in taking many crucial monetary decision related to the business. The

purpose of this report is to analyse the financial performance of Vodafone PLC on the basis of

ratio calculation and annual statements.

Task 1

The financial statements reflects the information about the results of operations, financial

position and cash flows within the business. Companies makes decisions related to allocation of

resources by using that information (Abraham, Deo and Irvine 2008). Every statement has its

own objective. These can be defined as follows:

Balance Sheet – This statement is a snapshot of the company’s business at the end of the

financial year. It includes all the assets and liabilities within the business. The purpose of

the balance sheet is to state the current financial position of the company in terms of

liquidity, funding, efficiency, debt etc.

Cash flow statement – This document shows the inflows and outflows of the cash during

the reporting financial period (Statement of Cash Flows, 2000). The purpose of the cash

flow statement is to reflect the nature of cash receipts and disbursements in various

categories.

Income statement – This document shows all the items related to income and expenses

within the business. The purpose is to show the ability of the company to generate profits.

It discloses the volume of sales and the nature of various types of expenses. It is also

capable of analysing the trends related to the company’s operations.

Terminology

Debit and credit – Under the double entry bookkeeping system, debits and credits are the

entries made in the account ledgers. It records the changes in the values which generates

from business transactions (Ball, Jayaraman and Shivakumar, 2012). It is to be noted that

source destination for the event is credited and destination account for the event is

debited.

1

Financial information produced from the financial statements is of great importance for

the company. It helps in taking many crucial monetary decision related to the business. The

purpose of this report is to analyse the financial performance of Vodafone PLC on the basis of

ratio calculation and annual statements.

Task 1

The financial statements reflects the information about the results of operations, financial

position and cash flows within the business. Companies makes decisions related to allocation of

resources by using that information (Abraham, Deo and Irvine 2008). Every statement has its

own objective. These can be defined as follows:

Balance Sheet – This statement is a snapshot of the company’s business at the end of the

financial year. It includes all the assets and liabilities within the business. The purpose of

the balance sheet is to state the current financial position of the company in terms of

liquidity, funding, efficiency, debt etc.

Cash flow statement – This document shows the inflows and outflows of the cash during

the reporting financial period (Statement of Cash Flows, 2000). The purpose of the cash

flow statement is to reflect the nature of cash receipts and disbursements in various

categories.

Income statement – This document shows all the items related to income and expenses

within the business. The purpose is to show the ability of the company to generate profits.

It discloses the volume of sales and the nature of various types of expenses. It is also

capable of analysing the trends related to the company’s operations.

Terminology

Debit and credit – Under the double entry bookkeeping system, debits and credits are the

entries made in the account ledgers. It records the changes in the values which generates

from business transactions (Ball, Jayaraman and Shivakumar, 2012). It is to be noted that

source destination for the event is credited and destination account for the event is

debited.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Books of prime entry – These are the books where initially all the transactions within

business are recorded. Later on these books are used to generate entries in a double entry

bookkeeping system (Ittelson, 2009).

Accounts and ledgers – Ledger is a book of final entry which records all the financial

events in form of individual accounts. Accounts can be of different types such as real,

nominal, personal etc. The transactions recorded in the journal follows three basic

principles:

Real account ‘Debit’ what comes in & ‘credit’ what goes out

Nominal account ‘Debit’ all losses & expenses, ‘credit’ all incomes and gains

Personal account ‘Debit’ the receiver & ‘credit’ the giver (Siano, Kitchen and

Confetto, 2010)

Trial balance - It is a measure adopted to check the accuracy of the ledge accounts. It is

required that the debit side should match with the credit side.

Financial accounts – These accounts are the summary and reporting of the financial

transactions which are made by the company. Every organization prepares final accounts

at end of the business period.

Task 2

Limited Company

In such kind of business the liabilities of the members of the organization is limited to the

extent they have invested into the business. It is being operated on a very large scale involving

many complex reporting requirements (Vickerstaff and Johal, 2014). The control remains with

the major owners and shareholders of the company.

These may be limited by share or buy guarantee. It can be public or private limited

companies. The main difference is that member limit of private ltd is restricted by law and the

company’s rules. On the other hand any individual can buy share in the public ltd. For instance

2

business are recorded. Later on these books are used to generate entries in a double entry

bookkeeping system (Ittelson, 2009).

Accounts and ledgers – Ledger is a book of final entry which records all the financial

events in form of individual accounts. Accounts can be of different types such as real,

nominal, personal etc. The transactions recorded in the journal follows three basic

principles:

Real account ‘Debit’ what comes in & ‘credit’ what goes out

Nominal account ‘Debit’ all losses & expenses, ‘credit’ all incomes and gains

Personal account ‘Debit’ the receiver & ‘credit’ the giver (Siano, Kitchen and

Confetto, 2010)

Trial balance - It is a measure adopted to check the accuracy of the ledge accounts. It is

required that the debit side should match with the credit side.

Financial accounts – These accounts are the summary and reporting of the financial

transactions which are made by the company. Every organization prepares final accounts

at end of the business period.

Task 2

Limited Company

In such kind of business the liabilities of the members of the organization is limited to the

extent they have invested into the business. It is being operated on a very large scale involving

many complex reporting requirements (Vickerstaff and Johal, 2014). The control remains with

the major owners and shareholders of the company.

These may be limited by share or buy guarantee. It can be public or private limited

companies. The main difference is that member limit of private ltd is restricted by law and the

company’s rules. On the other hand any individual can buy share in the public ltd. For instance

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Vodafone is a public ltd organization headquartered in London, UK. The brand is listed on the

London Stock Exchange and is a member of the FTSE 100 index (Vodafone. 2015). The control

and management remains with the Board of Directors and major shareholder of the organization.

It is mandatory for Vodafone to produce all the three financial statements according to the

guidelines of IFRS and GAPE

Sole Trader

It is a very simplest form of business structure and it relatively involves very low cost for

set up. As a sole trader the owner of the business holds the responsibility for all the legal aspects.

He retains complete control on the assets and relevant financial decisions. There are very few

reporting requirements (Zoan, 2014). Very high amount of flexibility is there in adopting any

kind of change or innovation. The size of the business is low however there are unlimited

liabilities which means all the personal assets are at risk in case if things go wrong. The

preparation of the financial statements depends upon the willingness of the owner

Partnership

It is a kind of arrangement were parties known as the partners agrees to come together to

do a particular business. These partners could be individuals, companies, entities, schools etc. the

partners are liable for the debts and obligations of the company. The ratio for sharing of profits

and losses is decided in an agreed ratio. For that purpose a partnership deed has been established

between the parties (Ball, Jayaraman and Shivakumar, 2012). Under such business along with

the three financial statements, individual partner’s capital accounts are also prepared.

Task 3

Ratio Analysis

Current Ratio – This ratio shows the short term obligations of the business. It can be

interpreted that company has able to maintain a current ratio around less than 1. This

reflects that company has maintained a conservative approach to the working capital

management.

Quick ratio – It shows the extent of cash and other current assets that are readily

convertible into cash as compared to short term obligations of the business (Maynard,

2013). The ratio is lower than the industry average and this suggests that Vodafone is

taking too much risk by not maintaining a suitable safeguard of liquid resources.

3

London Stock Exchange and is a member of the FTSE 100 index (Vodafone. 2015). The control

and management remains with the Board of Directors and major shareholder of the organization.

It is mandatory for Vodafone to produce all the three financial statements according to the

guidelines of IFRS and GAPE

Sole Trader

It is a very simplest form of business structure and it relatively involves very low cost for

set up. As a sole trader the owner of the business holds the responsibility for all the legal aspects.

He retains complete control on the assets and relevant financial decisions. There are very few

reporting requirements (Zoan, 2014). Very high amount of flexibility is there in adopting any

kind of change or innovation. The size of the business is low however there are unlimited

liabilities which means all the personal assets are at risk in case if things go wrong. The

preparation of the financial statements depends upon the willingness of the owner

Partnership

It is a kind of arrangement were parties known as the partners agrees to come together to

do a particular business. These partners could be individuals, companies, entities, schools etc. the

partners are liable for the debts and obligations of the company. The ratio for sharing of profits

and losses is decided in an agreed ratio. For that purpose a partnership deed has been established

between the parties (Ball, Jayaraman and Shivakumar, 2012). Under such business along with

the three financial statements, individual partner’s capital accounts are also prepared.

Task 3

Ratio Analysis

Current Ratio – This ratio shows the short term obligations of the business. It can be

interpreted that company has able to maintain a current ratio around less than 1. This

reflects that company has maintained a conservative approach to the working capital

management.

Quick ratio – It shows the extent of cash and other current assets that are readily

convertible into cash as compared to short term obligations of the business (Maynard,

2013). The ratio is lower than the industry average and this suggests that Vodafone is

taking too much risk by not maintaining a suitable safeguard of liquid resources.

3

Gross Profit Margin – It shows the underlying profitability of the core activities of the

organization. Gross profit for the three years is showing a decreasing trend. It is probably

due to the increasing competition within the industry.

Operating Profit Margin – It measures the profit generating efficiency of the company.

Vodafone has failed to maintain an appropriate operating profit margin. This decrease in

the ratio is due to increase in the proportion of selling, general and administration

expenses

ROCE (Return on Capital Employed) – Very high amount of fluctuations can be noticed

in the ROCE of the company. This thing can reduce the earning available to the

shareholders (Zoan, 2014). Company is facing issues in maintaining the efficiency of

capital usage.

Receivable Days – It is the number of days that a customer invoice is outstanding before

it is collected. The receivable rate for the business has deceased and this shows that there

is high effectiveness in the credit and collection efforts for the business.

Payable Days - It tells how long a company takes to pay its invoices from the trade

creditors. The payable day’s period is stagnant and it is good for the business. It shows

that company is capable of paying its invoices in timely manner.

Inventory Days – There are no too many fluctuations in the ratio (Vodafone. 2015). The

ratio is considerable and company holds its inventory in effective manner before selling

it.

Gearing – The debt to equity ratio is not too much high. It is considerable from industry

point of view because Vodafone operates on a very large scale.

Dividend Yield – Decrease in the dividend yield ratio can be noticed. However the

shareholders might be satisfied from this rate of dividend.

Earnings Per Share – It reflects the earning per share for the shareholders. In the current

year the earing per share is very good because it reflects adequate amount of dividend for

the investors.

Price Earnings Ratio – The price earnings ratio was very favourable for two years 2012-

13 but it decreased in 2014 (Vickerstaff and Johal, 2014). It will decrease the market

value per share also for the company

4

organization. Gross profit for the three years is showing a decreasing trend. It is probably

due to the increasing competition within the industry.

Operating Profit Margin – It measures the profit generating efficiency of the company.

Vodafone has failed to maintain an appropriate operating profit margin. This decrease in

the ratio is due to increase in the proportion of selling, general and administration

expenses

ROCE (Return on Capital Employed) – Very high amount of fluctuations can be noticed

in the ROCE of the company. This thing can reduce the earning available to the

shareholders (Zoan, 2014). Company is facing issues in maintaining the efficiency of

capital usage.

Receivable Days – It is the number of days that a customer invoice is outstanding before

it is collected. The receivable rate for the business has deceased and this shows that there

is high effectiveness in the credit and collection efforts for the business.

Payable Days - It tells how long a company takes to pay its invoices from the trade

creditors. The payable day’s period is stagnant and it is good for the business. It shows

that company is capable of paying its invoices in timely manner.

Inventory Days – There are no too many fluctuations in the ratio (Vodafone. 2015). The

ratio is considerable and company holds its inventory in effective manner before selling

it.

Gearing – The debt to equity ratio is not too much high. It is considerable from industry

point of view because Vodafone operates on a very large scale.

Dividend Yield – Decrease in the dividend yield ratio can be noticed. However the

shareholders might be satisfied from this rate of dividend.

Earnings Per Share – It reflects the earning per share for the shareholders. In the current

year the earing per share is very good because it reflects adequate amount of dividend for

the investors.

Price Earnings Ratio – The price earnings ratio was very favourable for two years 2012-

13 but it decreased in 2014 (Vickerstaff and Johal, 2014). It will decrease the market

value per share also for the company

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 4 calculation in appendix

Task 5

Vodafone

The financial performance of Vodafone reflects the combination of good performance in

the emerging markets and challenging conditions in Europe. Company has succeeded in

offsetting competitive, regulatory and macroeconomic pressures in Europe. However the price

earning ratio of Vodafone is not showing impressive results. It shows what the market is willing

to pay for a stock based on its current earnings. This low performance can restrict the investors

from investing in the stocks of Vodafone.

5

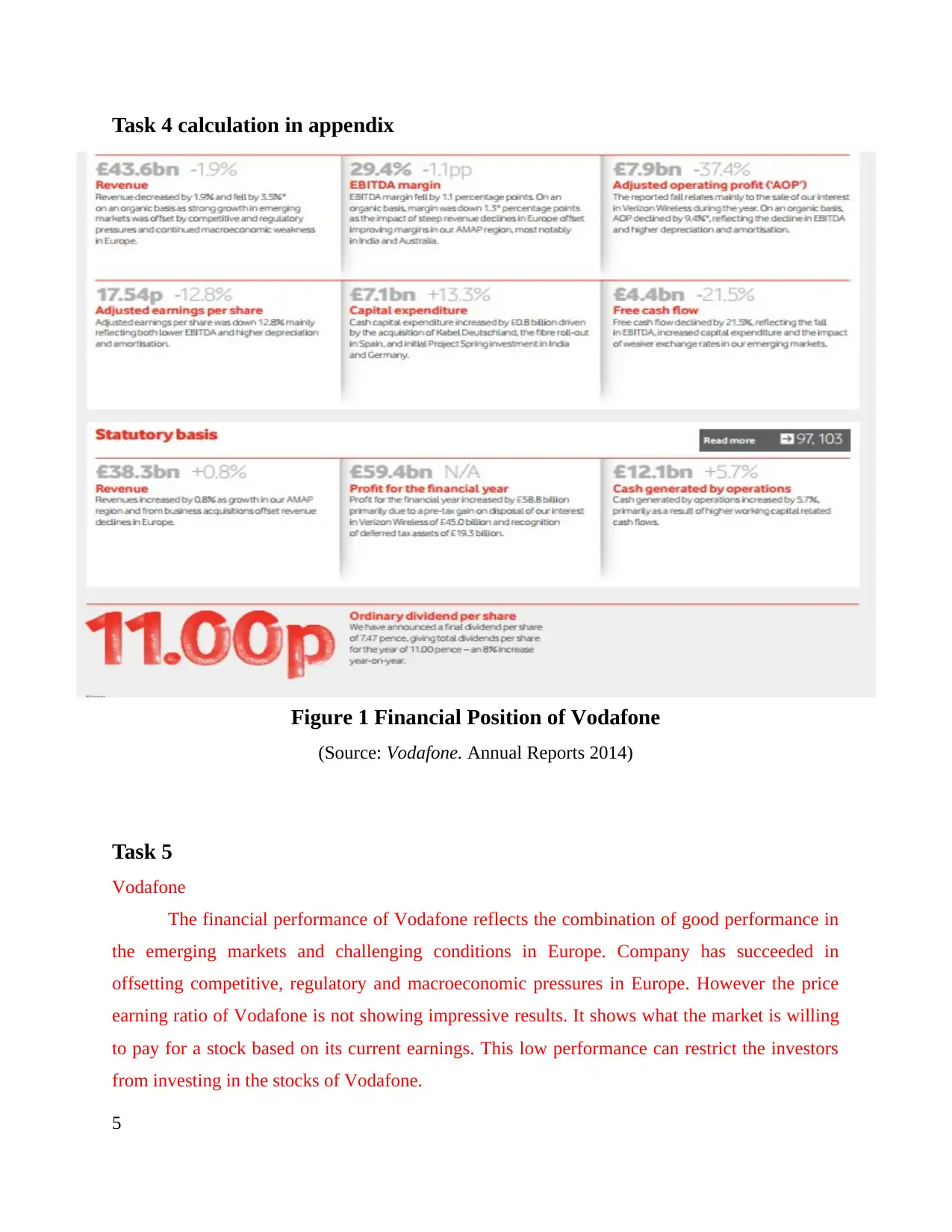

Figure 1 Financial Position of Vodafone

(Source: Vodafone. Annual Reports 2014)

Task 5

Vodafone

The financial performance of Vodafone reflects the combination of good performance in

the emerging markets and challenging conditions in Europe. Company has succeeded in

offsetting competitive, regulatory and macroeconomic pressures in Europe. However the price

earning ratio of Vodafone is not showing impressive results. It shows what the market is willing

to pay for a stock based on its current earnings. This low performance can restrict the investors

from investing in the stocks of Vodafone.

5

Figure 1 Financial Position of Vodafone

(Source: Vodafone. Annual Reports 2014)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The financial position of Vodafone can be reflected from the above figure. The revenue

was recorded at £43.6 bn. According to the annual reports the revenue has decreased by 1.9%.

The EBITDA margin was fell by 1.1pp percentage points. Further the capital expenditure for the

company has increased by 13.3% due to acquisition of Kabel Deutschland and some investments

in Spain. The profit for the financial year has increased by £58.8 billion because of pre-tax gain

on the disposal of interest in Verizon Wireles of recognition of deferred tax assets. Increase of

5.7% was also noticed in the cash generated from operations due to higher working capital

related cash flows. For the benefits of shareholders company offered a 8% increase in the

dividend per share.

Deutsche Telekom

On the other hand Deutsche Telekom is one of the strong competitor for Vodafone in UK

market. The net revenue for the business has not shown effective results as it has increased to

62658 million in the current year from 60132 million. The profit from the operations has

increased very significantly from 4930 to 7247 million. It is a strong sign of positive financial

growth. The earning per share for the shareholder has been very low as compared to Vodafone.

The company is doing good but the financial results are not up to the standard of Vodafone.

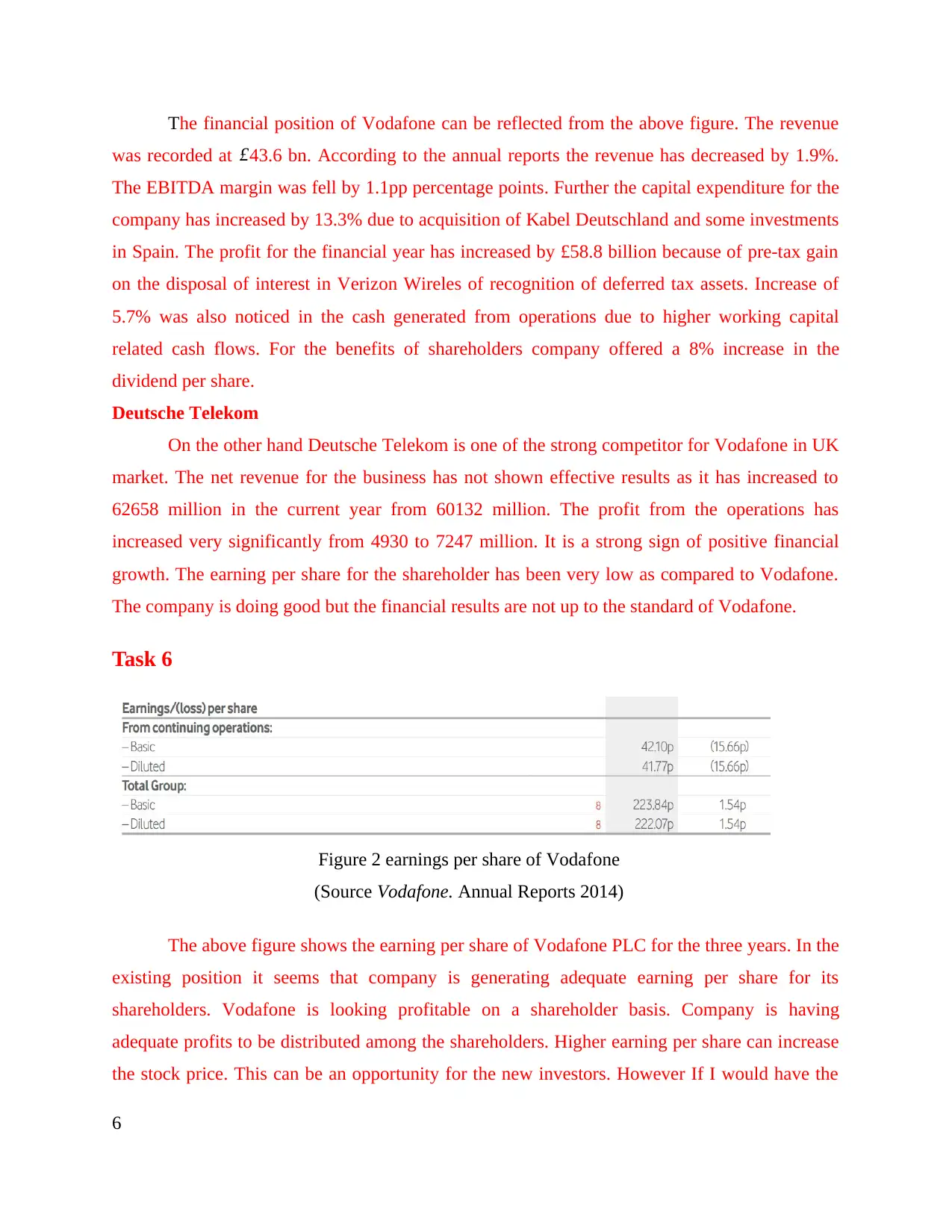

Task 6

The above figure shows the earning per share of Vodafone PLC for the three years. In the

existing position it seems that company is generating adequate earning per share for its

shareholders. Vodafone is looking profitable on a shareholder basis. Company is having

adequate profits to be distributed among the shareholders. Higher earning per share can increase

the stock price. This can be an opportunity for the new investors. However If I would have the

6

Figure 2 earnings per share of Vodafone

(Source Vodafone. Annual Reports 2014)

was recorded at £43.6 bn. According to the annual reports the revenue has decreased by 1.9%.

The EBITDA margin was fell by 1.1pp percentage points. Further the capital expenditure for the

company has increased by 13.3% due to acquisition of Kabel Deutschland and some investments

in Spain. The profit for the financial year has increased by £58.8 billion because of pre-tax gain

on the disposal of interest in Verizon Wireles of recognition of deferred tax assets. Increase of

5.7% was also noticed in the cash generated from operations due to higher working capital

related cash flows. For the benefits of shareholders company offered a 8% increase in the

dividend per share.

Deutsche Telekom

On the other hand Deutsche Telekom is one of the strong competitor for Vodafone in UK

market. The net revenue for the business has not shown effective results as it has increased to

62658 million in the current year from 60132 million. The profit from the operations has

increased very significantly from 4930 to 7247 million. It is a strong sign of positive financial

growth. The earning per share for the shareholder has been very low as compared to Vodafone.

The company is doing good but the financial results are not up to the standard of Vodafone.

Task 6

The above figure shows the earning per share of Vodafone PLC for the three years. In the

existing position it seems that company is generating adequate earning per share for its

shareholders. Vodafone is looking profitable on a shareholder basis. Company is having

adequate profits to be distributed among the shareholders. Higher earning per share can increase

the stock price. This can be an opportunity for the new investors. However If I would have the

6

Figure 2 earnings per share of Vodafone

(Source Vodafone. Annual Reports 2014)

money to invest I would like to invest in the shares of Vodafone because at present organization

is showing strong continued growth. Their business is constantly evolving to adapt to changes in

the customer behaviour, technology, regulation and the competitive landscape. Taking that into

consideration I would prefer to invest in the shares of the company.

From the above study it can be concluded that Vodafone has maintained a considerable

financial position in the industry. The rate of competition for the company is also high. .

Company’s makes decisions related to allocation of resources by using the financial information.

7

is showing strong continued growth. Their business is constantly evolving to adapt to changes in

the customer behaviour, technology, regulation and the competitive landscape. Taking that into

consideration I would prefer to invest in the shares of the company.

From the above study it can be concluded that Vodafone has maintained a considerable

financial position in the industry. The rate of competition for the company is also high. .

Company’s makes decisions related to allocation of resources by using the financial information.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Abraham, A., Deo, H. and Irvine, H., 2008. What lies beneath? Financial reporting and corporate

governance in Australian banks. Asian Review of Accounting. 16(1). pp. 4 – 20.

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary

disclosure as complements: A test of the confirmation hypothesis. Journal of Accounting

and Economics. 53(1). pp. 136-166

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary

disclosure as complements: A test of the confirmation hypothesis. Journal of Accounting

and Economics. 53(1). pp. 136-166.

Ittelson, R. T., 2009. Financial Statements: A Step-by-Step Guide to Understanding and

Creating Financial Reports. Career Press.

Maynard, J., 2013. Financial Accounting, Reporting, and Analysis. Oxford University Press

Siano, A., Kitchen, J. P. and Confetto, G. M., 2010. Financial resources and corporate reputation:

Toward common management principles for managing corporate reputation. Corporate

Communications: An International Journal. 15(1). pp.68 – 82.

Statement of Cash Flows, 2000. [Online]. Available through:<

http://www.bluelayouts.org/template/768.html>. [Accessed on 12th December 2015].

Vickerstaff, B. and Johal, P., 2014. Financial Accounting. Routledge.

Vodafone. 2015. [Online] Available through: < https://www.vodafone.co.uk/>. [Accessed on 12th

December 2015].

Zoan, N. G., 2014. Finance - Professional Essays and Assignments. Zoan NG.

1

Abraham, A., Deo, H. and Irvine, H., 2008. What lies beneath? Financial reporting and corporate

governance in Australian banks. Asian Review of Accounting. 16(1). pp. 4 – 20.

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary

disclosure as complements: A test of the confirmation hypothesis. Journal of Accounting

and Economics. 53(1). pp. 136-166

Ball, R., Jayaraman, S. and Shivakumar, L., 2012. Audited financial reporting and voluntary

disclosure as complements: A test of the confirmation hypothesis. Journal of Accounting

and Economics. 53(1). pp. 136-166.

Ittelson, R. T., 2009. Financial Statements: A Step-by-Step Guide to Understanding and

Creating Financial Reports. Career Press.

Maynard, J., 2013. Financial Accounting, Reporting, and Analysis. Oxford University Press

Siano, A., Kitchen, J. P. and Confetto, G. M., 2010. Financial resources and corporate reputation:

Toward common management principles for managing corporate reputation. Corporate

Communications: An International Journal. 15(1). pp.68 – 82.

Statement of Cash Flows, 2000. [Online]. Available through:<

http://www.bluelayouts.org/template/768.html>. [Accessed on 12th December 2015].

Vickerstaff, B. and Johal, P., 2014. Financial Accounting. Routledge.

Vodafone. 2015. [Online] Available through: < https://www.vodafone.co.uk/>. [Accessed on 12th

December 2015].

Zoan, N. G., 2014. Finance - Professional Essays and Assignments. Zoan NG.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix

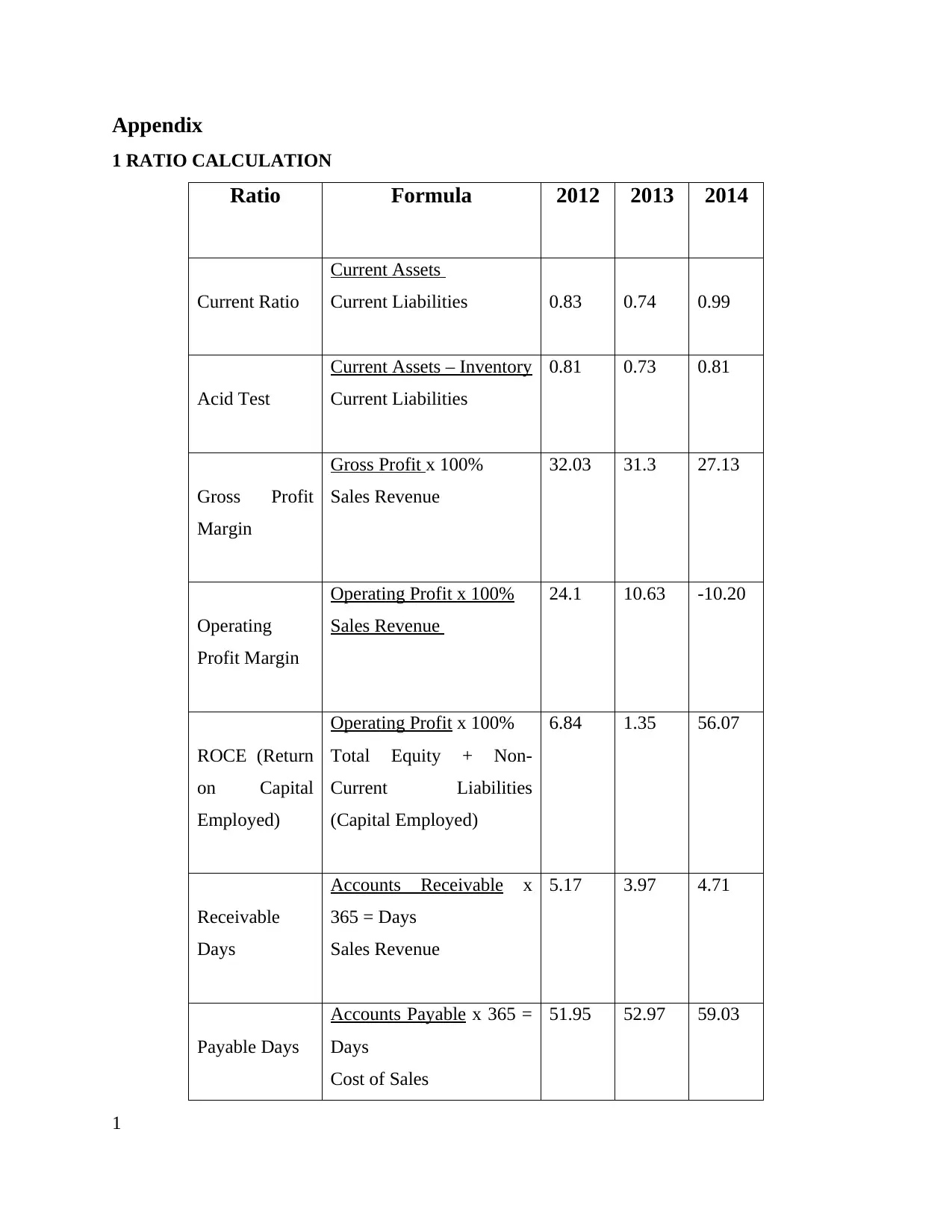

1 RATIO CALCULATION

Ratio Formula 2012 2013 2014

Current Ratio

Current Assets

Current Liabilities 0.83 0.74 0.99

Acid Test

Current Assets – Inventory

Current Liabilities

0.81 0.73 0.81

Gross Profit

Margin

Gross Profit x 100%

Sales Revenue

32.03 31.3 27.13

Operating

Profit Margin

Operating Profit x 100%

Sales Revenue

24.1 10.63 -10.20

ROCE (Return

on Capital

Employed)

Operating Profit x 100%

Total Equity + Non-

Current Liabilities

(Capital Employed)

6.84 1.35 56.07

Receivable

Days

Accounts Receivable x

365 = Days

Sales Revenue

5.17 3.97 4.71

Payable Days

Accounts Payable x 365 =

Days

Cost of Sales

51.95 52.97 59.03

1

1 RATIO CALCULATION

Ratio Formula 2012 2013 2014

Current Ratio

Current Assets

Current Liabilities 0.83 0.74 0.99

Acid Test

Current Assets – Inventory

Current Liabilities

0.81 0.73 0.81

Gross Profit

Margin

Gross Profit x 100%

Sales Revenue

32.03 31.3 27.13

Operating

Profit Margin

Operating Profit x 100%

Sales Revenue

24.1 10.63 -10.20

ROCE (Return

on Capital

Employed)

Operating Profit x 100%

Total Equity + Non-

Current Liabilities

(Capital Employed)

6.84 1.35 56.07

Receivable

Days

Accounts Receivable x

365 = Days

Sales Revenue

5.17 3.97 4.71

Payable Days

Accounts Payable x 365 =

Days

Cost of Sales

51.95 52.97 59.03

1

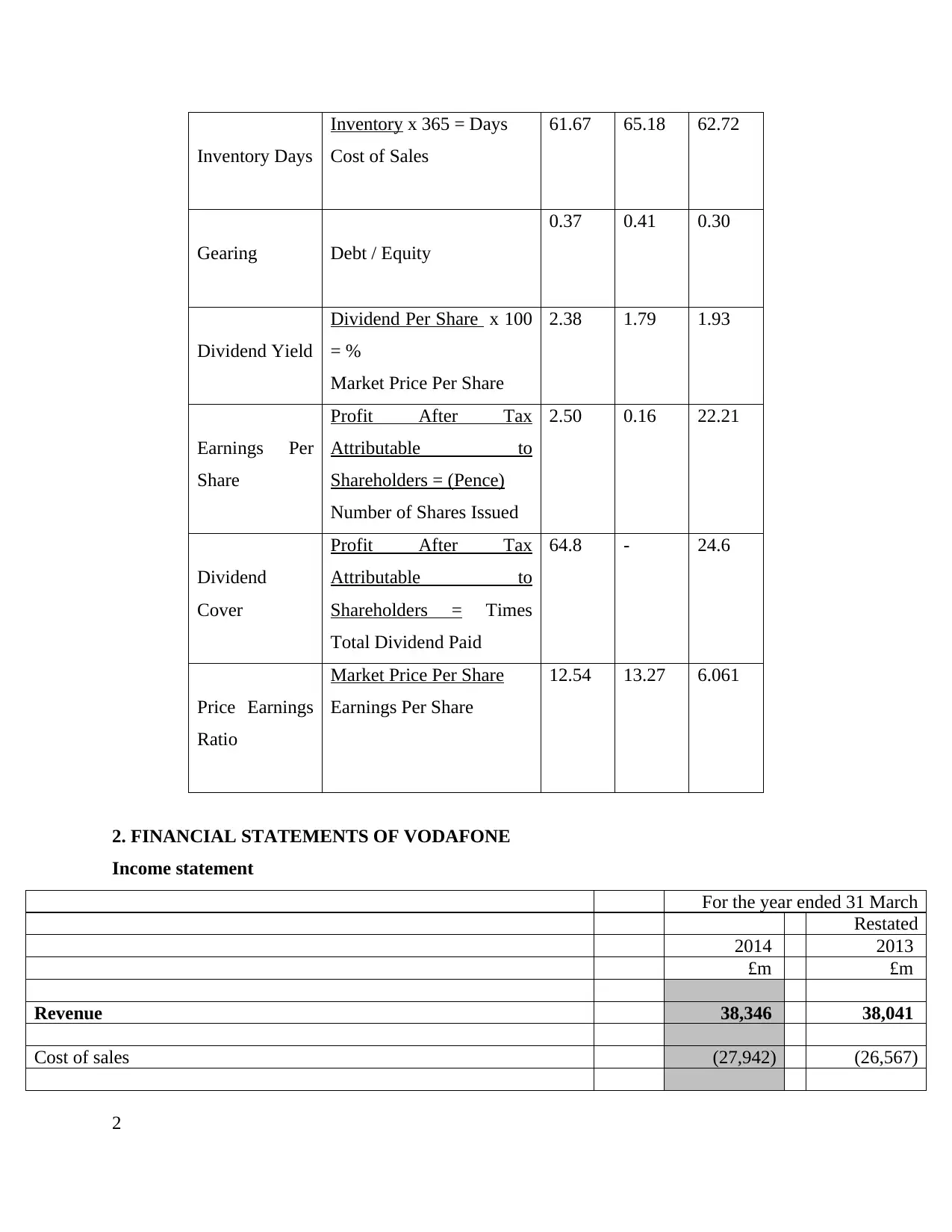

Inventory Days

Inventory x 365 = Days

Cost of Sales

61.67 65.18 62.72

Gearing Debt / Equity

0.37 0.41 0.30

Dividend Yield

Dividend Per Share x 100

= %

Market Price Per Share

2.38 1.79 1.93

Earnings Per

Share

Profit After Tax

Attributable to

Shareholders = (Pence)

Number of Shares Issued

2.50 0.16 22.21

Dividend

Cover

Profit After Tax

Attributable to

Shareholders = Times

Total Dividend Paid

64.8 - 24.6

Price Earnings

Ratio

Market Price Per Share

Earnings Per Share

12.54 13.27 6.061

2. FINANCIAL STATEMENTS OF VODAFONE

Income statement

For the year ended 31 March

Restated

2014 2013

£m £m

Revenue 38,346 38,041

Cost of sales (27,942) (26,567)

2

Inventory x 365 = Days

Cost of Sales

61.67 65.18 62.72

Gearing Debt / Equity

0.37 0.41 0.30

Dividend Yield

Dividend Per Share x 100

= %

Market Price Per Share

2.38 1.79 1.93

Earnings Per

Share

Profit After Tax

Attributable to

Shareholders = (Pence)

Number of Shares Issued

2.50 0.16 22.21

Dividend

Cover

Profit After Tax

Attributable to

Shareholders = Times

Total Dividend Paid

64.8 - 24.6

Price Earnings

Ratio

Market Price Per Share

Earnings Per Share

12.54 13.27 6.061

2. FINANCIAL STATEMENTS OF VODAFONE

Income statement

For the year ended 31 March

Restated

2014 2013

£m £m

Revenue 38,346 38,041

Cost of sales (27,942) (26,567)

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.