Vodafone PLC: Financial Performance, Ratio Analysis, and Comparison

VerifiedAdded on 2022/11/26

|11

|2538

|416

Report

AI Summary

This report presents a comprehensive financial analysis of Vodafone PLC, examining its performance from 2014 to 2016 using various financial ratios. The analysis covers profitability, liquidity, solvency, and efficiency ratios, highlighting trends and key insights into Vodafone's financial health. The report includes a detailed breakdown of Vodafone's financial statements, calculating and interpreting ratios such as ROCE, ROS, current ratio, gearing ratio, and inventory days. A comparative analysis of Vodafone's performance against Deutsche Telekom AG and the broader telecom industry is also conducted, discussing the causes of any deviations and differences in the ratios. The report concludes with an assessment of Vodafone's overall financial performance, identifying areas of strength and weakness and offering insights into potential market opportunities.

Running head: MBA ASSIGNMENT

MBA Assignment

Name of the University

Name of Student

Authors’ Note

MBA Assignment

Name of the University

Name of Student

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2MBA ASSIGNMENT

Introduction:

Vodafone Plc is a British telecommunication that has it’s headquartered in London

and provides wide range of services for meeting the satisfaction of customers. Over the last

five years, Vodafone has been undergoing a substantial transformation.

Business of organization was developed that exclusively focuses on text services and

mobile and mobile voices. It offers high speed broad band services and reaches 72 million

homes in Europe market. Across the footprint of twenty six countries, a broad portfolio of

integrated fixed, market leading and mobile leading services are offered by group. Significant

investment and organic acquisition has been the factors responsible for the progress of

organization.1 There will be enhancement in the performance of organization through

customer experience excellence program that was launched last year. Regulatory

environment is aimed at Vodafone group that enables return for investment made,

maintenance of adequate level of competitions and innovation that helps in proving value for

money and customer choices. Advantage of growth opportunities are taken by the group by

providing a broad mix of communication services such as fixed broadband, mobile, internet

of things offerings, cloud and content . There are two geographic region in which the

business of group is organized that involves Africa, Europe, Asia pacific and Middle East.

Great opportunities exist for this organization resulting from increasing customer demand for

reliable, secure, high network speed data connections.

The present report discusses about the financial performance of Vodafone plc over the

period of last three years using the tool of ratio analysis. Various ratios for analyzing

financial position of group involve calculation of efficiency ratio, liquidity ratio, leverage

ratio, investor’s ratio and profitability ratio. Furthermore, comparison of financial

1 Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice. Cengage Learning,

2013.

Introduction:

Vodafone Plc is a British telecommunication that has it’s headquartered in London

and provides wide range of services for meeting the satisfaction of customers. Over the last

five years, Vodafone has been undergoing a substantial transformation.

Business of organization was developed that exclusively focuses on text services and

mobile and mobile voices. It offers high speed broad band services and reaches 72 million

homes in Europe market. Across the footprint of twenty six countries, a broad portfolio of

integrated fixed, market leading and mobile leading services are offered by group. Significant

investment and organic acquisition has been the factors responsible for the progress of

organization.1 There will be enhancement in the performance of organization through

customer experience excellence program that was launched last year. Regulatory

environment is aimed at Vodafone group that enables return for investment made,

maintenance of adequate level of competitions and innovation that helps in proving value for

money and customer choices. Advantage of growth opportunities are taken by the group by

providing a broad mix of communication services such as fixed broadband, mobile, internet

of things offerings, cloud and content . There are two geographic region in which the

business of group is organized that involves Africa, Europe, Asia pacific and Middle East.

Great opportunities exist for this organization resulting from increasing customer demand for

reliable, secure, high network speed data connections.

The present report discusses about the financial performance of Vodafone plc over the

period of last three years using the tool of ratio analysis. Various ratios for analyzing

financial position of group involve calculation of efficiency ratio, liquidity ratio, leverage

ratio, investor’s ratio and profitability ratio. Furthermore, comparison of financial

1 Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice. Cengage Learning,

2013.

3MBA ASSIGNMENT

performance of Vodafone Plc with Deutsche telecom AG and telecom industry have been

demonstrated in the report. The possible causes for deviation and differences in the ratio have

been discussed.

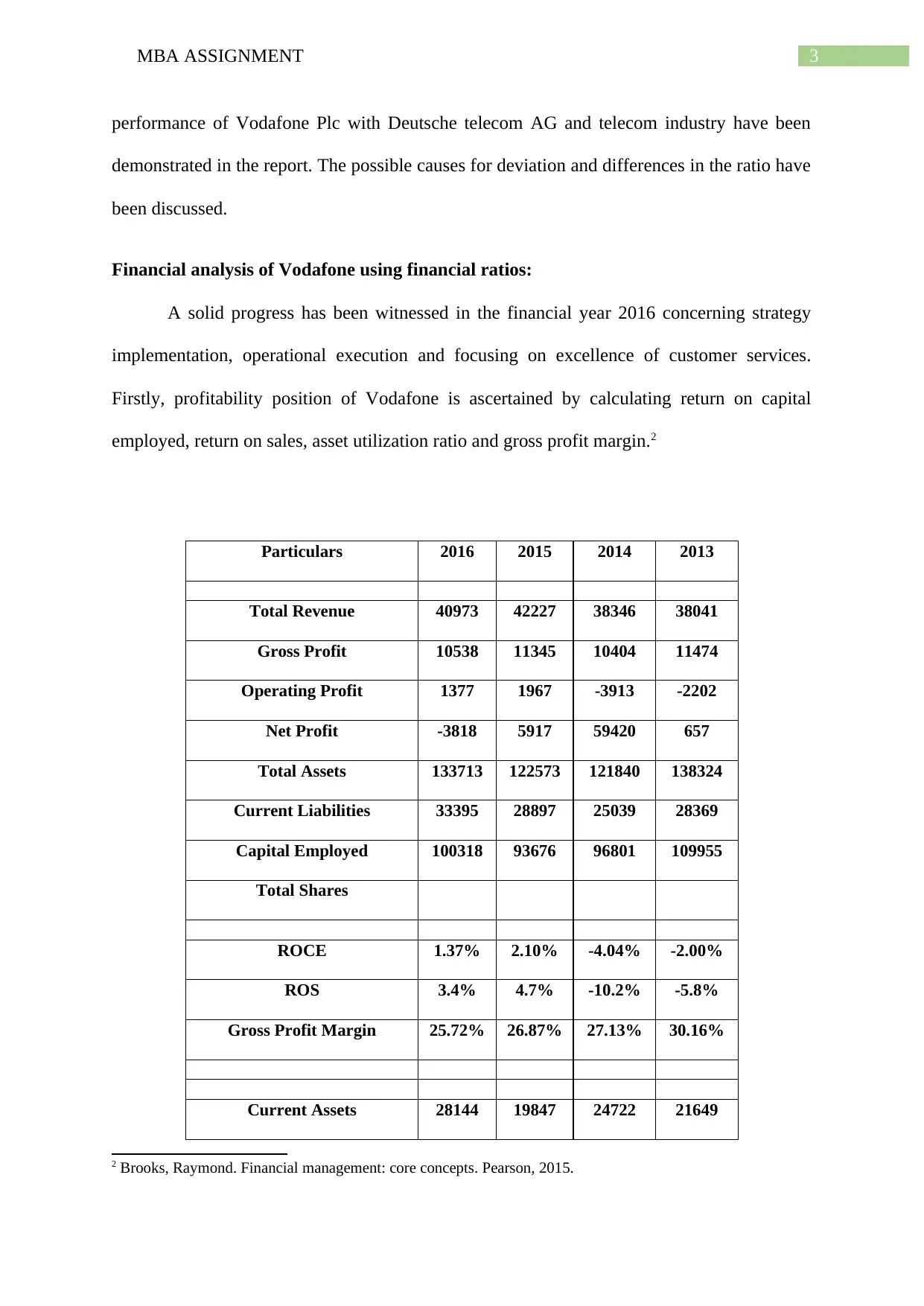

Financial analysis of Vodafone using financial ratios:

A solid progress has been witnessed in the financial year 2016 concerning strategy

implementation, operational execution and focusing on excellence of customer services.

Firstly, profitability position of Vodafone is ascertained by calculating return on capital

employed, return on sales, asset utilization ratio and gross profit margin.2

Particulars 2016 2015 2014 2013

Total Revenue 40973 42227 38346 38041

Gross Profit 10538 11345 10404 11474

Operating Profit 1377 1967 -3913 -2202

Net Profit -3818 5917 59420 657

Total Assets 133713 122573 121840 138324

Current Liabilities 33395 28897 25039 28369

Capital Employed 100318 93676 96801 109955

Total Shares

ROCE 1.37% 2.10% -4.04% -2.00%

ROS 3.4% 4.7% -10.2% -5.8%

Gross Profit Margin 25.72% 26.87% 27.13% 30.16%

Current Assets 28144 19847 24722 21649

2 Brooks, Raymond. Financial management: core concepts. Pearson, 2015.

performance of Vodafone Plc with Deutsche telecom AG and telecom industry have been

demonstrated in the report. The possible causes for deviation and differences in the ratio have

been discussed.

Financial analysis of Vodafone using financial ratios:

A solid progress has been witnessed in the financial year 2016 concerning strategy

implementation, operational execution and focusing on excellence of customer services.

Firstly, profitability position of Vodafone is ascertained by calculating return on capital

employed, return on sales, asset utilization ratio and gross profit margin.2

Particulars 2016 2015 2014 2013

Total Revenue 40973 42227 38346 38041

Gross Profit 10538 11345 10404 11474

Operating Profit 1377 1967 -3913 -2202

Net Profit -3818 5917 59420 657

Total Assets 133713 122573 121840 138324

Current Liabilities 33395 28897 25039 28369

Capital Employed 100318 93676 96801 109955

Total Shares

ROCE 1.37% 2.10% -4.04% -2.00%

ROS 3.4% 4.7% -10.2% -5.8%

Gross Profit Margin 25.72% 26.87% 27.13% 30.16%

Current Assets 28144 19847 24722 21649

2 Brooks, Raymond. Financial management: core concepts. Pearson, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4MBA ASSIGNMENT

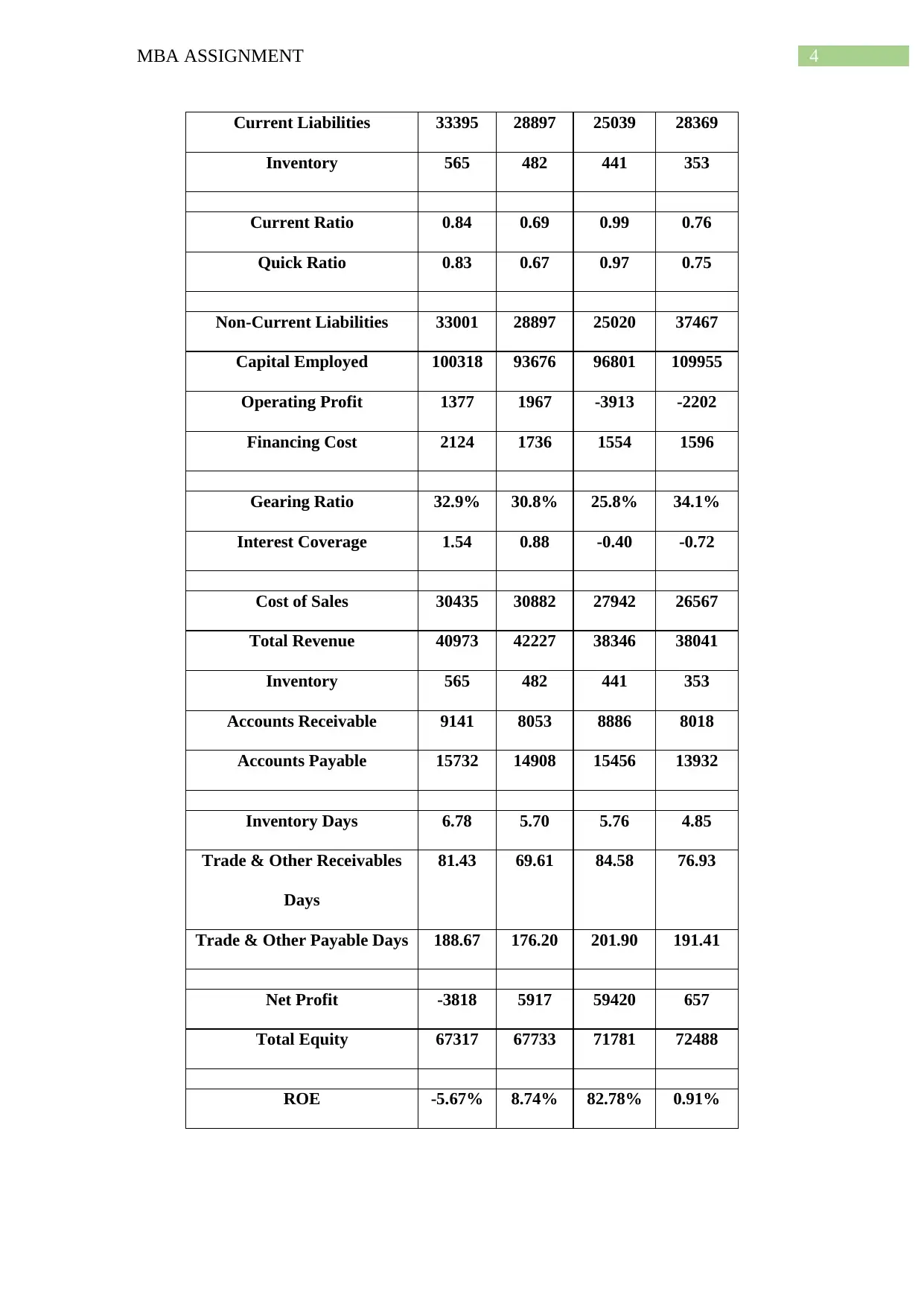

Current Liabilities 33395 28897 25039 28369

Inventory 565 482 441 353

Current Ratio 0.84 0.69 0.99 0.76

Quick Ratio 0.83 0.67 0.97 0.75

Non-Current Liabilities 33001 28897 25020 37467

Capital Employed 100318 93676 96801 109955

Operating Profit 1377 1967 -3913 -2202

Financing Cost 2124 1736 1554 1596

Gearing Ratio 32.9% 30.8% 25.8% 34.1%

Interest Coverage 1.54 0.88 -0.40 -0.72

Cost of Sales 30435 30882 27942 26567

Total Revenue 40973 42227 38346 38041

Inventory 565 482 441 353

Accounts Receivable 9141 8053 8886 8018

Accounts Payable 15732 14908 15456 13932

Inventory Days 6.78 5.70 5.76 4.85

Trade & Other Receivables

Days

81.43 69.61 84.58 76.93

Trade & Other Payable Days 188.67 176.20 201.90 191.41

Net Profit -3818 5917 59420 657

Total Equity 67317 67733 71781 72488

ROE -5.67% 8.74% 82.78% 0.91%

Current Liabilities 33395 28897 25039 28369

Inventory 565 482 441 353

Current Ratio 0.84 0.69 0.99 0.76

Quick Ratio 0.83 0.67 0.97 0.75

Non-Current Liabilities 33001 28897 25020 37467

Capital Employed 100318 93676 96801 109955

Operating Profit 1377 1967 -3913 -2202

Financing Cost 2124 1736 1554 1596

Gearing Ratio 32.9% 30.8% 25.8% 34.1%

Interest Coverage 1.54 0.88 -0.40 -0.72

Cost of Sales 30435 30882 27942 26567

Total Revenue 40973 42227 38346 38041

Inventory 565 482 441 353

Accounts Receivable 9141 8053 8886 8018

Accounts Payable 15732 14908 15456 13932

Inventory Days 6.78 5.70 5.76 4.85

Trade & Other Receivables

Days

81.43 69.61 84.58 76.93

Trade & Other Payable Days 188.67 176.20 201.90 191.41

Net Profit -3818 5917 59420 657

Total Equity 67317 67733 71781 72488

ROE -5.67% 8.74% 82.78% 0.91%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5MBA ASSIGNMENT

Table 1:

Ratios of Vodafone plc:

Profitability position depicts the return that is generated by organization to their

investors and bottom line along with efficiency and overall performance. There has been

wide fluctuation in the profitability ratio over the period. The return on capital employed has

increased from since year 2014 from -10.2% to 4.35 in year 2015; however ratio fell again to

-2.56% in year 2016. This is indicative of the fact that efficient of organization in generating

profit to organization has increased and it reduced subsequently. There has been substantial,

decline in return on sales generated from 154.52 in year 2014 to 13.64% in year 2015 and

further it stood at negative value at -98.2% in year 2016. This fall in value of sales depicts

that revenue generated from sales has declined. Now looking at the value of asset utilization

ratio, figure suggest that there has been fall in such ratio as the value stood at 0.78 in year

2015 to 0.77% in year 2016. This fall in ratio depicts that assets have not been efficiently

utilised for generating profits. Gross profit margin has reduced from 27% in year 2014 to

26.30% in year 2016 respectively. However, there has been increase in value from 2014 to

2015 but ration declined subsequently in year 2016. This fall in figures of profitability ratio

suggest that organization have not been efficient in generating return to its investors. 3

Liquidity position of Vodafone plc has been analyzed by calculating liquidity ration

such as quick ratio and current ratio. Current ratio indicates the liquidity position and ability

of organization meet their current obligations. The value of current ratio has initially

decreased to 0.69% in year 2015 as against 0.99% in year 2014. Figure subsequently

increased to 0.84% in year 2016. This shows that the capability of Vodafone plc to meet its

short-term obligations has increased. Furthermore, value of quick ratio has increased to

3 Arnold, Glen. Corporate financial management. Pearson Higher Ed, 2013.

Table 1:

Ratios of Vodafone plc:

Profitability position depicts the return that is generated by organization to their

investors and bottom line along with efficiency and overall performance. There has been

wide fluctuation in the profitability ratio over the period. The return on capital employed has

increased from since year 2014 from -10.2% to 4.35 in year 2015; however ratio fell again to

-2.56% in year 2016. This is indicative of the fact that efficient of organization in generating

profit to organization has increased and it reduced subsequently. There has been substantial,

decline in return on sales generated from 154.52 in year 2014 to 13.64% in year 2015 and

further it stood at negative value at -98.2% in year 2016. This fall in value of sales depicts

that revenue generated from sales has declined. Now looking at the value of asset utilization

ratio, figure suggest that there has been fall in such ratio as the value stood at 0.78 in year

2015 to 0.77% in year 2016. This fall in ratio depicts that assets have not been efficiently

utilised for generating profits. Gross profit margin has reduced from 27% in year 2014 to

26.30% in year 2016 respectively. However, there has been increase in value from 2014 to

2015 but ration declined subsequently in year 2016. This fall in figures of profitability ratio

suggest that organization have not been efficient in generating return to its investors. 3

Liquidity position of Vodafone plc has been analyzed by calculating liquidity ration

such as quick ratio and current ratio. Current ratio indicates the liquidity position and ability

of organization meet their current obligations. The value of current ratio has initially

decreased to 0.69% in year 2015 as against 0.99% in year 2014. Figure subsequently

increased to 0.84% in year 2016. This shows that the capability of Vodafone plc to meet its

short-term obligations has increased. Furthermore, value of quick ratio has increased to

3 Arnold, Glen. Corporate financial management. Pearson Higher Ed, 2013.

6MBA ASSIGNMENT

0.84% in 2016 as against 0.56% in year 2015. It depicts that ability of Vodafone to meet their

short-term obligations has reduced considerably.4

Solvency position of organization has been analyzed by calculating gearing ratio and

interest coverage ratio. It can be figured out from the values given that there has been

significant reduction on gearing ratio from 34% in year 2015 to 2.03% in year 2016.

Considerable reduction has been noticed in interest cover ratio. Fall in gearing ratio indicates

that Vodafone Plc has adopted conservative financial management in recent year that has

been mainly due to downturn and reduction in value of sales generated. The ability of

organization to make its interest payment is exhibited by interest cover ratio. Fall in interest

cover is not favourable for company as they are not making enough money to make payment.

Vodafone is not generating enough money to meet its obligation of paying interest. 5

Efficiency position of Vodafone plc is analyzed by calculating efficiency ratios such

as inventory days, trade and other receivable days and trade and other payable days. It

exhibits efficiency of organization in managing their liabilities and efficient use of assets for

generating revenue. Inventory days have initially decreased by fewer points in year 2015 to

5v16 as against 5.76 in year 2014. It has increased subsequently to 6.50 in year 2016. It is

indicative of the fact that efficient of organization in converting its inventories into cash has

reduced. Trade and other receivable days have significantly increased to 38.55 as compared

to 30.92 in year 2015 respectively. Increase in the number of day’s exhibit that inventories

are converted into cash at longer date that would hamper its efficiency position. Now looking

at figure of trade and other payable days, the value has considerably increased to 67.86 in

year 2016 as compared to 54.5 in year 2015 respectively. This increase in number of days for

4 Brown, Matthew T. Financial management in the industry. 2016.

5 Petty, J. William, et al. Financial management: Principles and applications. Pearson Higher Education AU,

2015.

0.84% in 2016 as against 0.56% in year 2015. It depicts that ability of Vodafone to meet their

short-term obligations has reduced considerably.4

Solvency position of organization has been analyzed by calculating gearing ratio and

interest coverage ratio. It can be figured out from the values given that there has been

significant reduction on gearing ratio from 34% in year 2015 to 2.03% in year 2016.

Considerable reduction has been noticed in interest cover ratio. Fall in gearing ratio indicates

that Vodafone Plc has adopted conservative financial management in recent year that has

been mainly due to downturn and reduction in value of sales generated. The ability of

organization to make its interest payment is exhibited by interest cover ratio. Fall in interest

cover is not favourable for company as they are not making enough money to make payment.

Vodafone is not generating enough money to meet its obligation of paying interest. 5

Efficiency position of Vodafone plc is analyzed by calculating efficiency ratios such

as inventory days, trade and other receivable days and trade and other payable days. It

exhibits efficiency of organization in managing their liabilities and efficient use of assets for

generating revenue. Inventory days have initially decreased by fewer points in year 2015 to

5v16 as against 5.76 in year 2014. It has increased subsequently to 6.50 in year 2016. It is

indicative of the fact that efficient of organization in converting its inventories into cash has

reduced. Trade and other receivable days have significantly increased to 38.55 as compared

to 30.92 in year 2015 respectively. Increase in the number of day’s exhibit that inventories

are converted into cash at longer date that would hamper its efficiency position. Now looking

at figure of trade and other payable days, the value has considerably increased to 67.86 in

year 2016 as compared to 54.5 in year 2015 respectively. This increase in number of days for

4 Brown, Matthew T. Financial management in the industry. 2016.

5 Petty, J. William, et al. Financial management: Principles and applications. Pearson Higher Education AU,

2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7MBA ASSIGNMENT

trade payable Vodafone plc is not generating enough cash for meeting their daily operations.6

7Therefore, from the above analysis, it can be said that overall, efficiency of organization has

declined considerably.

Efficiency of organization towards generating return to its investors or shareholders

are analyzed by computing return on equity for the consolidated data. There has been drastic

decline in return on equity since year 2014 as the value fell from 84.15% to 8.95% in year

2015 and further to -5.87% in year 2016 respectively. Negative value depicts that total value

of equity has fallen in present year. There has been fall in total value of dividend paid to

shareholders of organization. Working capital and liquidity of Vodafone plc is affected in

considerable decline in cash flow.8

Therefore, the overall financial performance of Vodafone Plc is not favourable as

there is adverse change in liquidity, profitability and efficiency position of company.

Comparing performance of Vodafone against Deutsche Telecom AG and telecom

industry:

Deutsche Telecom AG is a telecommunication company of Germany that is

headquartered in Bonn and has number of subsidiaries. In this part, comparison of Vodafone

plc is done with AG is a telecommunication company of Germany that is headquartered in

Bonn and telecom industry as a whole.

Looking at the financial ratios of Deutsche Telecom, it can be clearly observed that

there are negative figures and they are much more profitable as compared to Vodafone group.

6 Lasher, William R. Practical financial management. Nelson Education, 2013.

7 Ogiela, Lidia. "Intelligent techniques for secure financial management in cloud computing." Electronic

commerce research and applications 14.6 (2015): 456-464.

8 Nalwaya, Nidhi, and Rahul Vyas. "Merger and Acquisition in the Telecom Industry: An Analysis of Financial

Performance of Vodafone Plc and Hutchison Essar." Journal of Marketing & Communication 9.3 (2014): 67-73.

trade payable Vodafone plc is not generating enough cash for meeting their daily operations.6

7Therefore, from the above analysis, it can be said that overall, efficiency of organization has

declined considerably.

Efficiency of organization towards generating return to its investors or shareholders

are analyzed by computing return on equity for the consolidated data. There has been drastic

decline in return on equity since year 2014 as the value fell from 84.15% to 8.95% in year

2015 and further to -5.87% in year 2016 respectively. Negative value depicts that total value

of equity has fallen in present year. There has been fall in total value of dividend paid to

shareholders of organization. Working capital and liquidity of Vodafone plc is affected in

considerable decline in cash flow.8

Therefore, the overall financial performance of Vodafone Plc is not favourable as

there is adverse change in liquidity, profitability and efficiency position of company.

Comparing performance of Vodafone against Deutsche Telecom AG and telecom

industry:

Deutsche Telecom AG is a telecommunication company of Germany that is

headquartered in Bonn and has number of subsidiaries. In this part, comparison of Vodafone

plc is done with AG is a telecommunication company of Germany that is headquartered in

Bonn and telecom industry as a whole.

Looking at the financial ratios of Deutsche Telecom, it can be clearly observed that

there are negative figures and they are much more profitable as compared to Vodafone group.

6 Lasher, William R. Practical financial management. Nelson Education, 2013.

7 Ogiela, Lidia. "Intelligent techniques for secure financial management in cloud computing." Electronic

commerce research and applications 14.6 (2015): 456-464.

8 Nalwaya, Nidhi, and Rahul Vyas. "Merger and Acquisition in the Telecom Industry: An Analysis of Financial

Performance of Vodafone Plc and Hutchison Essar." Journal of Marketing & Communication 9.3 (2014): 67-73.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8MBA ASSIGNMENT

Although, the return on capital employed has declined for Deutsche, the value of this ratio is

considerably higher than Vodafone Plc.

ROCE for Deutsche has decreased from 9.2% to 8.16% in year 2015 and return on

sales is considerably lower than Vodafone plc. However, the Vodafone performance in term

of this ratio is beyond the performance of overall telecom industry.

For financial year 2015, ROS for Vodafone is at 13.64% as against 10.15% for

Deutsche group. AUR remained constant for two consecutive years at 0.8% compared to

0.77% in year 2015 for Vodafone plc. Assets of Deutsche are more efficiently utilized for

generating revenue compared to that of Vodafone. Relating to industry performance,

performance of Deutsche is better than Vodafone performance.9

Now, looking at solvency position of both the organization, it can be seen from figure

that ratio is lower as compared to industry standard. Solvency ratio for industry is at 70.% for

year 2015 and the ratio for both organization is significant less. It exhibits the fact that both

organizations are dependent on debt for financing their capital requirement. However,

Vodafone Plc is in much worse position as against Deutsche.10

For interest cover, Vodafone is performing below the industry standard as compared

to Deutsche that is more or less in par with industry. The industry standard for return of

equity is at 5.6% for financial year 2016.

It can be observed from figure that both organizations have been generating return on

equity beyond the performance of industry. Performance of Deutsche is much better when it

comes to generating return on equity as value stood at 9.18% in year 2015 as against 8.85%

9 Madura, Jeff. International financial management. Nelson Education, 2014.

10 Kovalev, V. V. "Financial management course." Moscow, Prospekt (2015).

Although, the return on capital employed has declined for Deutsche, the value of this ratio is

considerably higher than Vodafone Plc.

ROCE for Deutsche has decreased from 9.2% to 8.16% in year 2015 and return on

sales is considerably lower than Vodafone plc. However, the Vodafone performance in term

of this ratio is beyond the performance of overall telecom industry.

For financial year 2015, ROS for Vodafone is at 13.64% as against 10.15% for

Deutsche group. AUR remained constant for two consecutive years at 0.8% compared to

0.77% in year 2015 for Vodafone plc. Assets of Deutsche are more efficiently utilized for

generating revenue compared to that of Vodafone. Relating to industry performance,

performance of Deutsche is better than Vodafone performance.9

Now, looking at solvency position of both the organization, it can be seen from figure

that ratio is lower as compared to industry standard. Solvency ratio for industry is at 70.% for

year 2015 and the ratio for both organization is significant less. It exhibits the fact that both

organizations are dependent on debt for financing their capital requirement. However,

Vodafone Plc is in much worse position as against Deutsche.10

For interest cover, Vodafone is performing below the industry standard as compared

to Deutsche that is more or less in par with industry. The industry standard for return of

equity is at 5.6% for financial year 2016.

It can be observed from figure that both organizations have been generating return on

equity beyond the performance of industry. Performance of Deutsche is much better when it

comes to generating return on equity as value stood at 9.18% in year 2015 as against 8.85%

9 Madura, Jeff. International financial management. Nelson Education, 2014.

10 Kovalev, V. V. "Financial management course." Moscow, Prospekt (2015).

9MBA ASSIGNMENT

for Vodafone plc.11 Therefore, both organizations have been outreaching the industrial

performance.

When looking at efficient position of telecom industry, it can be exhibited from figure

that inventory days for financial year 2015 stood at 6.5. Value for Vodafone plc stood at 5.16

as compared to 16.06 for Deutsche. In this aspect, Deutsche is less efficient as compared to

Vodafone plc as they are taking long time to convert their inventories into sales Deutsche.

The industry standard of trade receivable and other days is much higher that the number of

days required converting inventories into sales for both the organizations.12

Conclusion:

It can be concluded from above analysis that the overall financial performance of

Vodafone plc is not favourable as they have been witnessing declining sales that is hampering

their profitability position. However, in some aspect the performance of Vodafone plc is

better than industry standard and Deutsche group. Vodafone plc is outperforming industrial

standard in terms of efficiency position and generating return on equity. Therefore, in terms

of efficiency and generating return on equity, Vodafone is outperforming industry while in

terms of liquidity and solvency position they are underperforming. Performance of

organization can further increase if Vodafone would grasp the market opportunities.

11 Harlow, Harold Dennis, and Harold Dennis Harlow. "Vodafone Egypt (B), managing corporate cultural

change and organizational performance." Emerald Emerging Markets Case Studies 6.4 (2016): 1-17.

12 Karadag, Hande. "Financial management challenges in small and medium-sized enterprises: A strategic

management approach." Emerging Markets Journal 5.1 (2015): 26.

for Vodafone plc.11 Therefore, both organizations have been outreaching the industrial

performance.

When looking at efficient position of telecom industry, it can be exhibited from figure

that inventory days for financial year 2015 stood at 6.5. Value for Vodafone plc stood at 5.16

as compared to 16.06 for Deutsche. In this aspect, Deutsche is less efficient as compared to

Vodafone plc as they are taking long time to convert their inventories into sales Deutsche.

The industry standard of trade receivable and other days is much higher that the number of

days required converting inventories into sales for both the organizations.12

Conclusion:

It can be concluded from above analysis that the overall financial performance of

Vodafone plc is not favourable as they have been witnessing declining sales that is hampering

their profitability position. However, in some aspect the performance of Vodafone plc is

better than industry standard and Deutsche group. Vodafone plc is outperforming industrial

standard in terms of efficiency position and generating return on equity. Therefore, in terms

of efficiency and generating return on equity, Vodafone is outperforming industry while in

terms of liquidity and solvency position they are underperforming. Performance of

organization can further increase if Vodafone would grasp the market opportunities.

11 Harlow, Harold Dennis, and Harold Dennis Harlow. "Vodafone Egypt (B), managing corporate cultural

change and organizational performance." Emerald Emerging Markets Case Studies 6.4 (2016): 1-17.

12 Karadag, Hande. "Financial management challenges in small and medium-sized enterprises: A strategic

management approach." Emerging Markets Journal 5.1 (2015): 26.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10MBA ASSIGNMENT

References list:

Arnold, Glen. Corporate financial management. Pearson Higher Ed, 2013.

Blondy, Guilhem, et al. "The role of fiscal reporting in public financial management." Public

financial management and its emerging architecture (2013): 259-281.

Boyle, Geraldine. "‘She's usually quicker than the calculator’: financial management and

decision‐making in couples living with dementia." Health & social care in the community

21.5 (2013): 554-562.

Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice.

Cengage Learning, 2013.

Brooks, Raymond. Financial management: core concepts. Pearson, 2015.

Brown, Matthew T. Financial management in the industry. 2016.

Cheema, Marvi K., Glenda M. MacQueen, and Stefanie Hassel. "Assessing personal financial

management in patients with bipolar disorder and its relation to impulsivity and response

inhibition." Cognitive neuropsychiatry 20.5 (2015): 424-437.

Harlow, Harold Dennis, and Harold Dennis Harlow. "Vodafone Egypt (B), managing

corporate cultural change and organizational performance." Emerald Emerging Markets Case

Studies 6.4 (2016): 1-17.

Karadag, Hande. "Financial management challenges in small and medium-sized enterprises:

A strategic management approach." Emerging Markets Journal 5.1 (2015): 26.

Koh, Annie, et al. Financial Management: Theory and Practice. Cengage Learning, 2014.

Kovalev, V. V. "Financial management course." Moscow, Prospekt (2015).

Lasher, William R. Practical financial management. Nelson Education, 2013.

References list:

Arnold, Glen. Corporate financial management. Pearson Higher Ed, 2013.

Blondy, Guilhem, et al. "The role of fiscal reporting in public financial management." Public

financial management and its emerging architecture (2013): 259-281.

Boyle, Geraldine. "‘She's usually quicker than the calculator’: financial management and

decision‐making in couples living with dementia." Health & social care in the community

21.5 (2013): 554-562.

Brigham, Eugene F., and Michael C. Ehrhardt. Financial management: Theory & practice.

Cengage Learning, 2013.

Brooks, Raymond. Financial management: core concepts. Pearson, 2015.

Brown, Matthew T. Financial management in the industry. 2016.

Cheema, Marvi K., Glenda M. MacQueen, and Stefanie Hassel. "Assessing personal financial

management in patients with bipolar disorder and its relation to impulsivity and response

inhibition." Cognitive neuropsychiatry 20.5 (2015): 424-437.

Harlow, Harold Dennis, and Harold Dennis Harlow. "Vodafone Egypt (B), managing

corporate cultural change and organizational performance." Emerald Emerging Markets Case

Studies 6.4 (2016): 1-17.

Karadag, Hande. "Financial management challenges in small and medium-sized enterprises:

A strategic management approach." Emerging Markets Journal 5.1 (2015): 26.

Koh, Annie, et al. Financial Management: Theory and Practice. Cengage Learning, 2014.

Kovalev, V. V. "Financial management course." Moscow, Prospekt (2015).

Lasher, William R. Practical financial management. Nelson Education, 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11MBA ASSIGNMENT

Madura, Jeff. International Financial Management, Abridged. Cengage Learning, 2015.

Madura, Jeff. International financial management. Nelson Education, 2014.

Nalwaya, Nidhi, and Rahul Vyas. "Merger and Acquisition in the Telecom Industry: An

Analysis of Financial Performance of Vodafone Plc and Hutchison Essar." Journal of

Marketing & Communication 9.3 (2014): 67-73.

Ogiela, Lidia. "Intelligent techniques for secure financial management in cloud computing."

Electronic commerce research and applications 14.6 (2015): 456-464.

Petty, J. William, et al. Financial management: Principles and applications. Pearson Higher

Education AU, 2015.

Madura, Jeff. International Financial Management, Abridged. Cengage Learning, 2015.

Madura, Jeff. International financial management. Nelson Education, 2014.

Nalwaya, Nidhi, and Rahul Vyas. "Merger and Acquisition in the Telecom Industry: An

Analysis of Financial Performance of Vodafone Plc and Hutchison Essar." Journal of

Marketing & Communication 9.3 (2014): 67-73.

Ogiela, Lidia. "Intelligent techniques for secure financial management in cloud computing."

Electronic commerce research and applications 14.6 (2015): 456-464.

Petty, J. William, et al. Financial management: Principles and applications. Pearson Higher

Education AU, 2015.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.