Vodafone Financial Performance Report

VerifiedAdded on 2020/01/28

|13

|4193

|40

Report

AI Summary

This report provides a comprehensive financial analysis of Vodafone, a British multinational telecommunications company, covering the years 2014 and 2015. The analysis utilizes ratio analysis to assess Vodafone's liquidity, profitability, solvency, and efficiency. Key ratios examined include current ratio, quick ratio, absolute liquid ratio, gross profit ratio, net profit ratio, operating ratio, inventory turnover ratio, debtor turnover ratio, creditor turnover ratio, debt equity ratio, and proprietary ratio. The report details the strengths and weaknesses revealed by these ratios, highlighting areas of concern such as declining profitability and liquidity issues. The analysis also discusses the implications of these findings for both short-term and long-term financial decision-making within Vodafone. The report concludes by emphasizing the importance of financial statement analysis for organizational stakeholders and strategic planning.

Introduction to Finance and

Marketing

Marketing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Main activities and markets of Vodafone.............................................................................1

1.2 Basic principles, roles and purpose of financial statements..................................................1

1.3 Analysis of financial performance of Vodafone...................................................................2

1.4 Benefits and limitations of different ratios............................................................................7

1.5 Analysis necessary for short and long term financial decisions ..........................................8

CONCLUSION................................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Main activities and markets of Vodafone.............................................................................1

1.2 Basic principles, roles and purpose of financial statements..................................................1

1.3 Analysis of financial performance of Vodafone...................................................................2

1.4 Benefits and limitations of different ratios............................................................................7

1.5 Analysis necessary for short and long term financial decisions ..........................................8

CONCLUSION................................................................................................................................9

REFERENCES .............................................................................................................................10

Index of Tables

Table 1: Ratio Analysis of Vodafone..............................................................................................3

Table 1: Ratio Analysis of Vodafone..............................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial statements helps an organisation to measure its performance in the market.

Analysis of financial statements is an efficient way to assess the position of the company in all

aspects of the business (Best, 2014). Ratio analysis is used to analyse and compare the data of

the company with its past performance. It also gives useful information about the liquidity,

solvency and efficiency of the company. These analysis form an important part in decision

making and strategies for the future (Boczko, 2016). The report includes the analysis of

Vodafone company and its performance in the last two financial years. Vodafone is a British

multinational telecom company with its networks across 50 countries (Vodafone Plc. 2015).

It is the second largest telecommunication company with its headquarters in London, UK. Along

with this, the benefits and limitations of ratios for Vodafone has also been included in the report.

TASK 1

1.1 Main activities and markets of Vodafone

Vodafone is a global company and it has variety of products in its portfolio. It is a world

famous telecommunication company has products like fixed lines, mobiles, internet services,

digital television, money transfers and mHealth services. The turnover and the customer base has

been growing at a good pace in the recent past. It has 7 billion mobile phone and 1 billion land

line customers around the world (Cheung and et.al., 2014). It also offers communication

solutions like cloud computing, unified collaborations and communications to various

companies (Vernimmen and et.al., 2014). Furthermore, mobile payment, mobile emails,

broadband, managed services and machine to machine services are provided by the company.

The profits and revenues has been constantly rising and it is a good sign for the future of the

company.

1.2 Basic principles, roles and purpose of financial statements

The purpose of financial statements is to provide information about the performance of

the company to its stakeholders and management to facilitate their decision making process

(Tugas, 2012). The stakeholders who rely on these statements are customers, suppliers, investors,

employees, management, lenders and government. All the credit decisions, investment decisions,

taxation decisions and union bargaining decisions are taken on the basis of these statements

(Hendrick and Crawford, 2014). The financial statements include Balance sheet, profit and loss

1

Financial statements helps an organisation to measure its performance in the market.

Analysis of financial statements is an efficient way to assess the position of the company in all

aspects of the business (Best, 2014). Ratio analysis is used to analyse and compare the data of

the company with its past performance. It also gives useful information about the liquidity,

solvency and efficiency of the company. These analysis form an important part in decision

making and strategies for the future (Boczko, 2016). The report includes the analysis of

Vodafone company and its performance in the last two financial years. Vodafone is a British

multinational telecom company with its networks across 50 countries (Vodafone Plc. 2015).

It is the second largest telecommunication company with its headquarters in London, UK. Along

with this, the benefits and limitations of ratios for Vodafone has also been included in the report.

TASK 1

1.1 Main activities and markets of Vodafone

Vodafone is a global company and it has variety of products in its portfolio. It is a world

famous telecommunication company has products like fixed lines, mobiles, internet services,

digital television, money transfers and mHealth services. The turnover and the customer base has

been growing at a good pace in the recent past. It has 7 billion mobile phone and 1 billion land

line customers around the world (Cheung and et.al., 2014). It also offers communication

solutions like cloud computing, unified collaborations and communications to various

companies (Vernimmen and et.al., 2014). Furthermore, mobile payment, mobile emails,

broadband, managed services and machine to machine services are provided by the company.

The profits and revenues has been constantly rising and it is a good sign for the future of the

company.

1.2 Basic principles, roles and purpose of financial statements

The purpose of financial statements is to provide information about the performance of

the company to its stakeholders and management to facilitate their decision making process

(Tugas, 2012). The stakeholders who rely on these statements are customers, suppliers, investors,

employees, management, lenders and government. All the credit decisions, investment decisions,

taxation decisions and union bargaining decisions are taken on the basis of these statements

(Hendrick and Crawford, 2014). The financial statements include Balance sheet, profit and loss

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statements and cash flow statements. So the statements not only show whether the business is

profitable or not it also helps the stakeholders to find the solvency, liquidity and efficiency of the

business (Brooks and Mukherjee, 2013). It is also mandatory for the the companies to prepare

annual statements which should depict true picture of the company.

1.3 Analysis of financial performance of Vodafone

Ratio analysis is a tool which is used by management to assess the financial statements of

a company. It gives useful details about the performance and position of the company. Ratios can

be helpful in finding out the profitability, solvency and liquidity position of the company. The

shareholders require such information to see whether their investment is profitable or not (Chen

and et.al., 2013). Similarly other stakeholders need these information for their decision making.

The major categories of ratios are:

Liquidity ratios: It calculates the short term payment capacity of the firm. So it used to

measure the short term solvency of Vodafone. Lack of liquidity is harmful for any organisation.

It could result in loss of creditor's confidence, bad image and legal actions against the company

(Minsky, 2015). High liquidity would means that the firm has idle funds which should have been

invested somewhere else. So it is important to have a proper balance between them. The ratios

which are used to calculate liquidity are current ratio, quick ratio and absolute liquid ratio (Islam

and et.al., 2013).

Profitability ratios: These ratios calculate the profitability and efficiency of the

company. The major ratio to calculate profitability are gross profit ratio, net profit ratio and

operating ratio (Krishnamurthy and Vissing-Jorgensen, 2013). This helps the management to see

the performance of the company. Profitability means capacity to generate profits which is left

after deducting all costs and expenses from it.

Turnover ratios: Turnover ratios calculates the efficiency of the company towards

managing their resources. High turnover ratio means that the organisation is using their assets in

an effective manner (Lavoori and Paramanik, 2014). The different turnover ratios are inventory

turnover ratio, debtor turnover ratio, creditor turnover ratio and assets turnover ratio (Deran and

et.al., 2014).

Solvency ratios: The liquidity ratio short term solvency of the firm while solvency

measures the long term solvency. Positive solvency ratio gives assurance to the lenders and

creditors that the firm will pay their debts on time. It is very useful in calculating the long term

2

profitable or not it also helps the stakeholders to find the solvency, liquidity and efficiency of the

business (Brooks and Mukherjee, 2013). It is also mandatory for the the companies to prepare

annual statements which should depict true picture of the company.

1.3 Analysis of financial performance of Vodafone

Ratio analysis is a tool which is used by management to assess the financial statements of

a company. It gives useful details about the performance and position of the company. Ratios can

be helpful in finding out the profitability, solvency and liquidity position of the company. The

shareholders require such information to see whether their investment is profitable or not (Chen

and et.al., 2013). Similarly other stakeholders need these information for their decision making.

The major categories of ratios are:

Liquidity ratios: It calculates the short term payment capacity of the firm. So it used to

measure the short term solvency of Vodafone. Lack of liquidity is harmful for any organisation.

It could result in loss of creditor's confidence, bad image and legal actions against the company

(Minsky, 2015). High liquidity would means that the firm has idle funds which should have been

invested somewhere else. So it is important to have a proper balance between them. The ratios

which are used to calculate liquidity are current ratio, quick ratio and absolute liquid ratio (Islam

and et.al., 2013).

Profitability ratios: These ratios calculate the profitability and efficiency of the

company. The major ratio to calculate profitability are gross profit ratio, net profit ratio and

operating ratio (Krishnamurthy and Vissing-Jorgensen, 2013). This helps the management to see

the performance of the company. Profitability means capacity to generate profits which is left

after deducting all costs and expenses from it.

Turnover ratios: Turnover ratios calculates the efficiency of the company towards

managing their resources. High turnover ratio means that the organisation is using their assets in

an effective manner (Lavoori and Paramanik, 2014). The different turnover ratios are inventory

turnover ratio, debtor turnover ratio, creditor turnover ratio and assets turnover ratio (Deran and

et.al., 2014).

Solvency ratios: The liquidity ratio short term solvency of the firm while solvency

measures the long term solvency. Positive solvency ratio gives assurance to the lenders and

creditors that the firm will pay their debts on time. It is very useful in calculating the long term

2

payment capacity of the company (Zohra and et.al., 2015). Not on payment of debts but also

instalment or interest payment capacity of the firm can also be calculated from it. The ratio

which are used to calculate it are debt equity ratio, debt to capital ratio, proprietary ratio, interest

coverage ratio and fixed asset to net worth ratio.

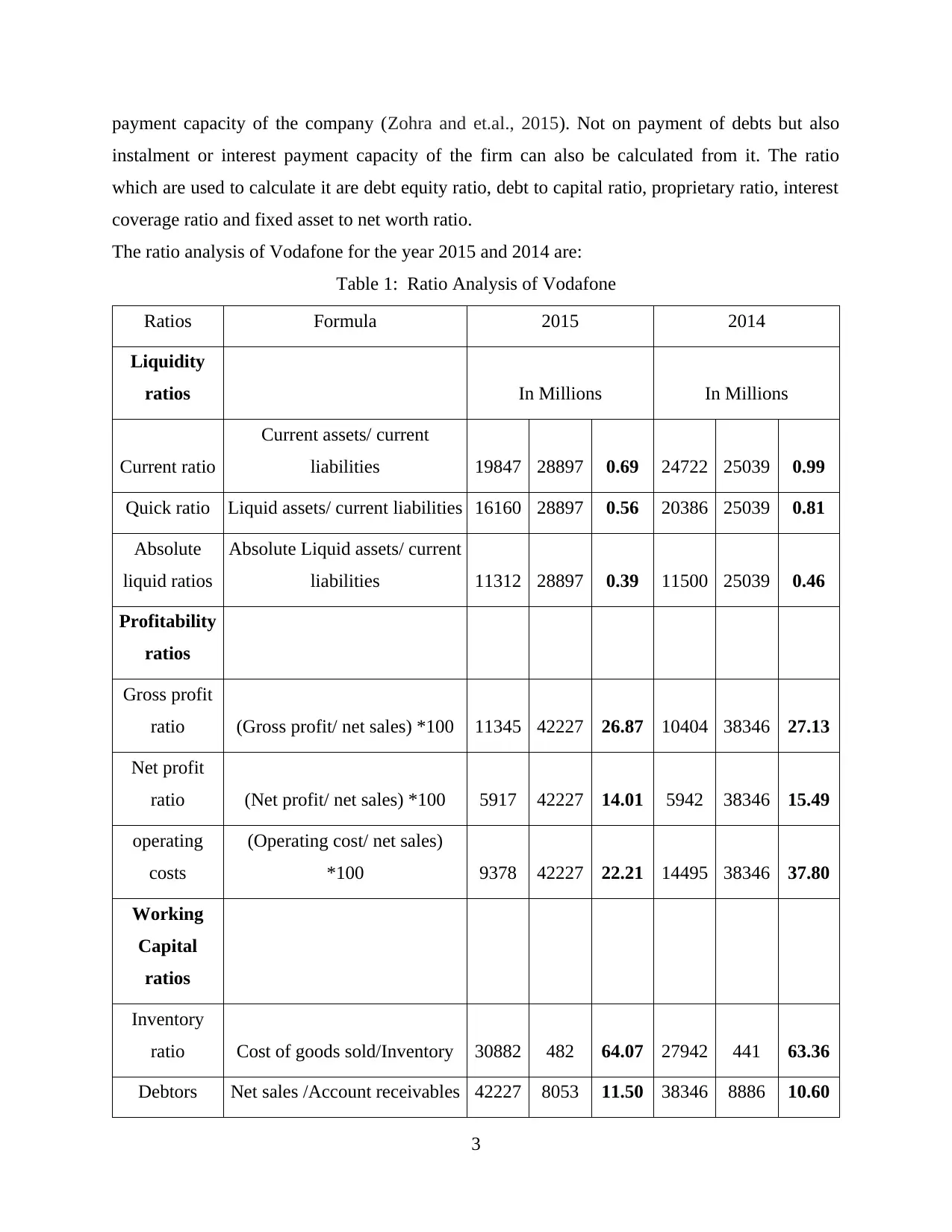

The ratio analysis of Vodafone for the year 2015 and 2014 are:

Table 1: Ratio Analysis of Vodafone

Ratios Formula 2015 2014

Liquidity

ratios In Millions In Millions

Current ratio

Current assets/ current

liabilities 19847 28897 0.69 24722 25039 0.99

Quick ratio Liquid assets/ current liabilities 16160 28897 0.56 20386 25039 0.81

Absolute

liquid ratios

Absolute Liquid assets/ current

liabilities 11312 28897 0.39 11500 25039 0.46

Profitability

ratios

Gross profit

ratio (Gross profit/ net sales) *100 11345 42227 26.87 10404 38346 27.13

Net profit

ratio (Net profit/ net sales) *100 5917 42227 14.01 5942 38346 15.49

operating

costs

(Operating cost/ net sales)

*100 9378 42227 22.21 14495 38346 37.80

Working

Capital

ratios

Inventory

ratio Cost of goods sold/Inventory 30882 482 64.07 27942 441 63.36

Debtors Net sales /Account receivables 42227 8053 11.50 38346 8886 10.60

3

instalment or interest payment capacity of the firm can also be calculated from it. The ratio

which are used to calculate it are debt equity ratio, debt to capital ratio, proprietary ratio, interest

coverage ratio and fixed asset to net worth ratio.

The ratio analysis of Vodafone for the year 2015 and 2014 are:

Table 1: Ratio Analysis of Vodafone

Ratios Formula 2015 2014

Liquidity

ratios In Millions In Millions

Current ratio

Current assets/ current

liabilities 19847 28897 0.69 24722 25039 0.99

Quick ratio Liquid assets/ current liabilities 16160 28897 0.56 20386 25039 0.81

Absolute

liquid ratios

Absolute Liquid assets/ current

liabilities 11312 28897 0.39 11500 25039 0.46

Profitability

ratios

Gross profit

ratio (Gross profit/ net sales) *100 11345 42227 26.87 10404 38346 27.13

Net profit

ratio (Net profit/ net sales) *100 5917 42227 14.01 5942 38346 15.49

operating

costs

(Operating cost/ net sales)

*100 9378 42227 22.21 14495 38346 37.80

Working

Capital

ratios

Inventory

ratio Cost of goods sold/Inventory 30882 482 64.07 27942 441 63.36

Debtors Net sales /Account receivables 42227 8053 11.50 38346 8886 10.60

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

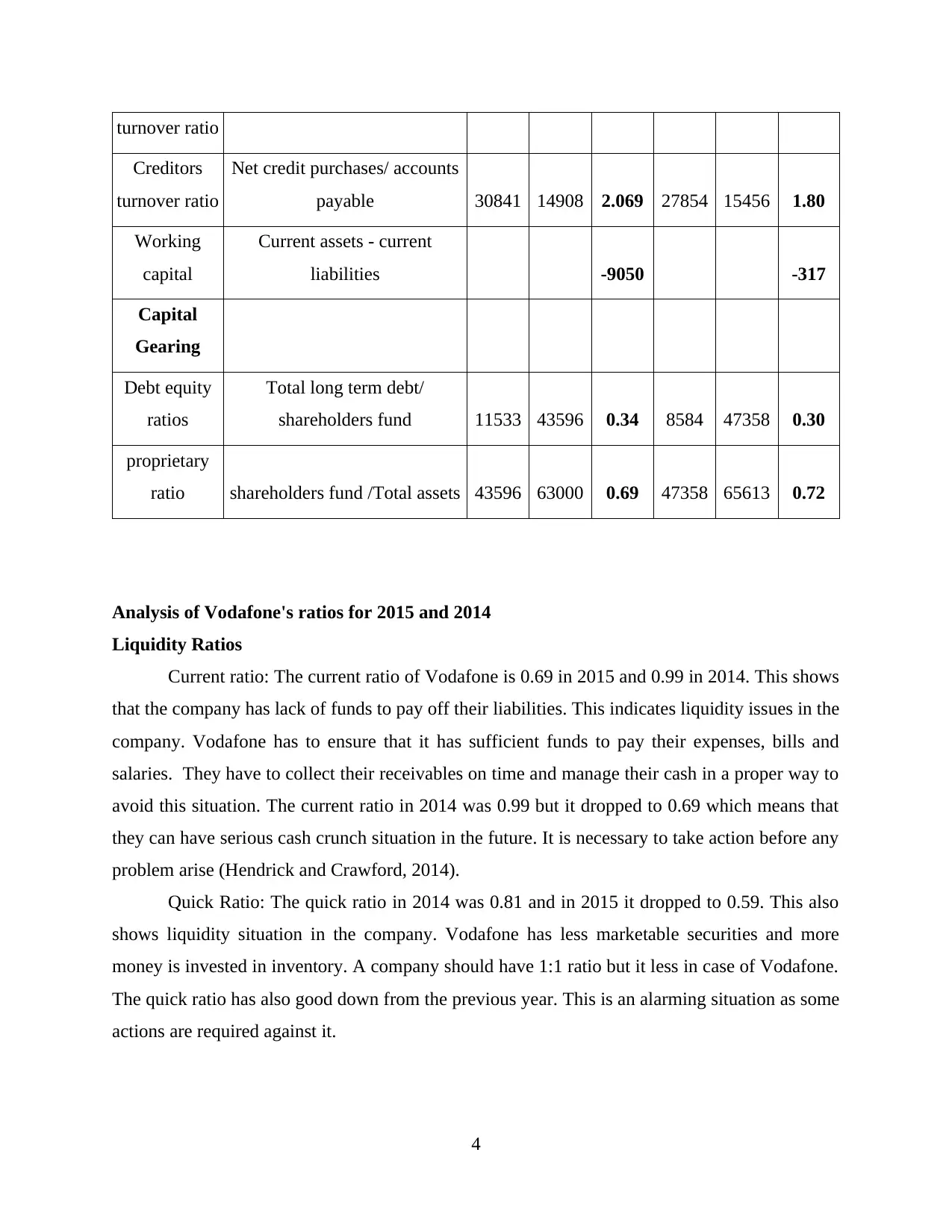

turnover ratio

Creditors

turnover ratio

Net credit purchases/ accounts

payable 30841 14908 2.069 27854 15456 1.80

Working

capital

Current assets - current

liabilities -9050 -317

Capital

Gearing

Debt equity

ratios

Total long term debt/

shareholders fund 11533 43596 0.34 8584 47358 0.30

proprietary

ratio shareholders fund /Total assets 43596 63000 0.69 47358 65613 0.72

Analysis of Vodafone's ratios for 2015 and 2014

Liquidity Ratios

Current ratio: The current ratio of Vodafone is 0.69 in 2015 and 0.99 in 2014. This shows

that the company has lack of funds to pay off their liabilities. This indicates liquidity issues in the

company. Vodafone has to ensure that it has sufficient funds to pay their expenses, bills and

salaries. They have to collect their receivables on time and manage their cash in a proper way to

avoid this situation. The current ratio in 2014 was 0.99 but it dropped to 0.69 which means that

they can have serious cash crunch situation in the future. It is necessary to take action before any

problem arise (Hendrick and Crawford, 2014).

Quick Ratio: The quick ratio in 2014 was 0.81 and in 2015 it dropped to 0.59. This also

shows liquidity situation in the company. Vodafone has less marketable securities and more

money is invested in inventory. A company should have 1:1 ratio but it less in case of Vodafone.

The quick ratio has also good down from the previous year. This is an alarming situation as some

actions are required against it.

4

Creditors

turnover ratio

Net credit purchases/ accounts

payable 30841 14908 2.069 27854 15456 1.80

Working

capital

Current assets - current

liabilities -9050 -317

Capital

Gearing

Debt equity

ratios

Total long term debt/

shareholders fund 11533 43596 0.34 8584 47358 0.30

proprietary

ratio shareholders fund /Total assets 43596 63000 0.69 47358 65613 0.72

Analysis of Vodafone's ratios for 2015 and 2014

Liquidity Ratios

Current ratio: The current ratio of Vodafone is 0.69 in 2015 and 0.99 in 2014. This shows

that the company has lack of funds to pay off their liabilities. This indicates liquidity issues in the

company. Vodafone has to ensure that it has sufficient funds to pay their expenses, bills and

salaries. They have to collect their receivables on time and manage their cash in a proper way to

avoid this situation. The current ratio in 2014 was 0.99 but it dropped to 0.69 which means that

they can have serious cash crunch situation in the future. It is necessary to take action before any

problem arise (Hendrick and Crawford, 2014).

Quick Ratio: The quick ratio in 2014 was 0.81 and in 2015 it dropped to 0.59. This also

shows liquidity situation in the company. Vodafone has less marketable securities and more

money is invested in inventory. A company should have 1:1 ratio but it less in case of Vodafone.

The quick ratio has also good down from the previous year. This is an alarming situation as some

actions are required against it.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absolute liquid ratio: The absolute liquid ratios are also very low. Vodafone has lack of

marketable securities which can be easily converted into cash. Marketable or liquid assets are

important because at the time of cash requirements these assets can be sold to pay off the debts.

The liquidity position of Vodafone is not satisfactory. It indicates that in future they will

be facing liquidity issues. It would be beneficial for them to collect their receivables on time and

invest more in liquid assets (Law and Singh, 2014).

Profitability Ratios

Gross profit: Gross profit calculates the total profit earned by the company without

including the indirect cost like selling, distribution, administration and labour costs. The gross

profit has gone down from 27.13 % to 26.87 % despite the increase in sales in 2015. The gross

profit earned by Vodafone is quite good but it should have been growing as the time progresses.

The efficiency has gone down for the company.

Net profit: Vodafone's net profits have also decreased from 15.49% to 14.01 % despite

the rise in sales in the year 2015. Net profits includes all operating and indirect costs. By

comparing the data of the two financial years it can be seen that Vodafone has not done well in

2015.

Operating ratios: It takes into consideration all operating costs of the company. It has

gone down form 37.80 to 22.21 which is a good sign. It show that Vodafone has reduced its

expenses and are using their resources efficiently.

The overall profitability ratios suggests that Vodafone has not done well in 2015. Their

gross and net profits have decreased while their operating costs have reduced. It is important for

them to reduce their indirect costs and improve the efficiency of the business. All the

unnecessary expenses have to be cut down by them.

Turnover ratios

Inventory turnover ratio: It measures the number of days to sell inventory. It was 63.36 in

2014 and it increased to 64.07 in 2015. It evaluate a firm' efficiency in managing its sales. The

rise in turnover in a good sign as it means that Vodafone is selling more than the last year.

Debtors turnover ratio: It calculate the effectiveness of the company in collecting its

debts (Hendrick and Crawford, 2014). The ratio was 10.60 in 2014 and it increased to 11.50 in

2015. It shows that the debts are collected more quickly then the last year. In 2014 it took

Vodafone 34 days to collect their debts which was reduced to 31 days in 2015. It shows that the

5

marketable securities which can be easily converted into cash. Marketable or liquid assets are

important because at the time of cash requirements these assets can be sold to pay off the debts.

The liquidity position of Vodafone is not satisfactory. It indicates that in future they will

be facing liquidity issues. It would be beneficial for them to collect their receivables on time and

invest more in liquid assets (Law and Singh, 2014).

Profitability Ratios

Gross profit: Gross profit calculates the total profit earned by the company without

including the indirect cost like selling, distribution, administration and labour costs. The gross

profit has gone down from 27.13 % to 26.87 % despite the increase in sales in 2015. The gross

profit earned by Vodafone is quite good but it should have been growing as the time progresses.

The efficiency has gone down for the company.

Net profit: Vodafone's net profits have also decreased from 15.49% to 14.01 % despite

the rise in sales in the year 2015. Net profits includes all operating and indirect costs. By

comparing the data of the two financial years it can be seen that Vodafone has not done well in

2015.

Operating ratios: It takes into consideration all operating costs of the company. It has

gone down form 37.80 to 22.21 which is a good sign. It show that Vodafone has reduced its

expenses and are using their resources efficiently.

The overall profitability ratios suggests that Vodafone has not done well in 2015. Their

gross and net profits have decreased while their operating costs have reduced. It is important for

them to reduce their indirect costs and improve the efficiency of the business. All the

unnecessary expenses have to be cut down by them.

Turnover ratios

Inventory turnover ratio: It measures the number of days to sell inventory. It was 63.36 in

2014 and it increased to 64.07 in 2015. It evaluate a firm' efficiency in managing its sales. The

rise in turnover in a good sign as it means that Vodafone is selling more than the last year.

Debtors turnover ratio: It calculate the effectiveness of the company in collecting its

debts (Hendrick and Crawford, 2014). The ratio was 10.60 in 2014 and it increased to 11.50 in

2015. It shows that the debts are collected more quickly then the last year. In 2014 it took

Vodafone 34 days to collect their debts which was reduced to 31 days in 2015. It shows that the

5

collection process of Vodafone is efficient and they have quality customers whop pay their dues

on time. The policy should not be too conservative and too tight because it will drive away the

customers.

Creditors turnover ratio: It calculates the repayment period of credit to suppliers. It has

increased from 1.8 to 2.07 in 2015. This shows that the company has been paying off its debts

quickly. Vodafone has to make sure that they use the credit period properly as they have liquidity

problem in the company.

Working capital: It is the difference between current assets and current liabilities. It

measures company's efficiency as well as the short term solvency. It should be positive but in the

case of Vodafone it is negative. It has increased to 9050 which is not a good sign because it

means that the current liabilities are more than the current assets. The short term funds are not

adequate enough to pay off the debts. The similar problem could be seen in liquidity ratios as

well.

Turnover ratios of Vodafone has shown that they have been efficient in their operations.

But the only problem with the company is that there working capital is negative. It indicates that

they have less funds to pay off their debts.

Capital Gearing ratios

Debt equity ratio: It compare the owner's funds and funds from lenders. The ratio for

Vodafone has increased from 0.30 to 0.34 in 2015. This shows that the company has more debts

than the equity. Too much leverage increases the risk and the lenders may feel vulnerable.

Lenders prefer the equity to be more than the debts. But the ratio is still below 1 which is good

for the company. It has increased by 0.04 which may not affect the business or the lenders. But it

is important for the company to ensure that it remains below the value of equity.

Proprietary ratio: The proprietary ratio for Vodafone was 0.72 which dropped to 0.69 in

2015. It is inverse of debt equity ratio as it is not very widely used. A high ratio means tat the

company has ample of funds in equity while low shows insufficient funds in equity.

The capital gearing ratio of Vodafone reveals that the company has been doing well in

maintaining its solvency. The equity is more than debts which reduces the leverage and makes

the business less risky. Though the solvency ratio has increased towards the debt side but still it

is well below the danger level. Vodafone has long term solvency and they don't have to worry

about it.

6

on time. The policy should not be too conservative and too tight because it will drive away the

customers.

Creditors turnover ratio: It calculates the repayment period of credit to suppliers. It has

increased from 1.8 to 2.07 in 2015. This shows that the company has been paying off its debts

quickly. Vodafone has to make sure that they use the credit period properly as they have liquidity

problem in the company.

Working capital: It is the difference between current assets and current liabilities. It

measures company's efficiency as well as the short term solvency. It should be positive but in the

case of Vodafone it is negative. It has increased to 9050 which is not a good sign because it

means that the current liabilities are more than the current assets. The short term funds are not

adequate enough to pay off the debts. The similar problem could be seen in liquidity ratios as

well.

Turnover ratios of Vodafone has shown that they have been efficient in their operations.

But the only problem with the company is that there working capital is negative. It indicates that

they have less funds to pay off their debts.

Capital Gearing ratios

Debt equity ratio: It compare the owner's funds and funds from lenders. The ratio for

Vodafone has increased from 0.30 to 0.34 in 2015. This shows that the company has more debts

than the equity. Too much leverage increases the risk and the lenders may feel vulnerable.

Lenders prefer the equity to be more than the debts. But the ratio is still below 1 which is good

for the company. It has increased by 0.04 which may not affect the business or the lenders. But it

is important for the company to ensure that it remains below the value of equity.

Proprietary ratio: The proprietary ratio for Vodafone was 0.72 which dropped to 0.69 in

2015. It is inverse of debt equity ratio as it is not very widely used. A high ratio means tat the

company has ample of funds in equity while low shows insufficient funds in equity.

The capital gearing ratio of Vodafone reveals that the company has been doing well in

maintaining its solvency. The equity is more than debts which reduces the leverage and makes

the business less risky. Though the solvency ratio has increased towards the debt side but still it

is well below the danger level. Vodafone has long term solvency and they don't have to worry

about it.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.4 Benefits and limitations of different ratios

Current Ratio: It is most commonly used ratios which is used by banks and financial

institutions before sanctioning a loan. The advantages of current ratio is that it is easy to

calculate and understand. It show the liquidity position and the operating cycle of the company

(Matsuoka, 2015). The efficiency of management can be seen from this ratio. But it is not

sufficient alone when deciding the liquidity position of the company. Furthermore, inclusion of

inventory leads to overestimation of liquid assets. It is because assets cannot be easily converted

into cash.

Quick ratio: It is an improved version of current ratio as it ignores inventory in its

calculation. Its advantages are that it only considers liquid assets in its calculation (Seiver,

Haddad and Do, 2014). The inventory can be seasonal and high in dying industry as such acid

test removes this limitation. But still it ignore time value and considers accounts receivables as a

liquid asset. Similar to current ratio it cannot be used alone.

Absolute liquid ratio: It only considers the marketable securities in its calculation which

is its major benefit. But it also ignores the time of cash flows and needs other ratios before

taking any decisions.

Gross profit ratio: It help in calculating the financial health of an organisation. It is very

useful tool to compare the performance of the company with the industry. A high margin means

the company is doing while low indicated loss in sales (Kamaiah, 2016). But the disadvantage of

gross profit is that it only considers direct cost in its calculation and other costs are ignored

(Financial Ratios, 2016).

Net profit ratio: It includes all the costs associated with the business which gross profit

ignores. As such it gives more relevant results. But it is difficult for the company to compare the

ratios with other companies because the costs are different.

Operating cost ratio: It helps in measuring the efficiency of the firm as well as in finding

out the operating cost of the business. But it ignores the other costs which are also important in

decision making (Obasi, 2014).

Inventory turnover ratio: It helps an organisation to study the number of days a product takes to

sell. This becomes foundation of the minimum and maximum stock that has to be maintained in

the warehouse. But it considers all the items on the average basis which may not be true.

7

Current Ratio: It is most commonly used ratios which is used by banks and financial

institutions before sanctioning a loan. The advantages of current ratio is that it is easy to

calculate and understand. It show the liquidity position and the operating cycle of the company

(Matsuoka, 2015). The efficiency of management can be seen from this ratio. But it is not

sufficient alone when deciding the liquidity position of the company. Furthermore, inclusion of

inventory leads to overestimation of liquid assets. It is because assets cannot be easily converted

into cash.

Quick ratio: It is an improved version of current ratio as it ignores inventory in its

calculation. Its advantages are that it only considers liquid assets in its calculation (Seiver,

Haddad and Do, 2014). The inventory can be seasonal and high in dying industry as such acid

test removes this limitation. But still it ignore time value and considers accounts receivables as a

liquid asset. Similar to current ratio it cannot be used alone.

Absolute liquid ratio: It only considers the marketable securities in its calculation which

is its major benefit. But it also ignores the time of cash flows and needs other ratios before

taking any decisions.

Gross profit ratio: It help in calculating the financial health of an organisation. It is very

useful tool to compare the performance of the company with the industry. A high margin means

the company is doing while low indicated loss in sales (Kamaiah, 2016). But the disadvantage of

gross profit is that it only considers direct cost in its calculation and other costs are ignored

(Financial Ratios, 2016).

Net profit ratio: It includes all the costs associated with the business which gross profit

ignores. As such it gives more relevant results. But it is difficult for the company to compare the

ratios with other companies because the costs are different.

Operating cost ratio: It helps in measuring the efficiency of the firm as well as in finding

out the operating cost of the business. But it ignores the other costs which are also important in

decision making (Obasi, 2014).

Inventory turnover ratio: It helps an organisation to study the number of days a product takes to

sell. This becomes foundation of the minimum and maximum stock that has to be maintained in

the warehouse. But it considers all the items on the average basis which may not be true.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debtor turnover ratio: The credit polices are made considering the debtor turnover ratio.

It shows whether the company is collecting its receivables on time or not. But plays an important

role deciding the liquidity position of the company.

Creditor turnover ratio: It accommodates a company to maintain its liquidity position in

the market. But gives the management information about the payment period to the creditors. But

it takes average of all the credit availed which may give wrong indication to individual creditor.

Working capital: It gives essential detail to the company regarding the working capital. Positive

indicates that company while negative indicates that Vodafone has to make changes in it (Law

and Singh, 2014).

Debt equity ratio: It helps an organisation to study the leverage position and risk that it

possess. Too much leverage can be bad for the business as such it helps in maintaining it. The

disadvantage of it is that it ignores the cost of issuing the equity and other sources of finance.

Proprietary ratio: The Proprietary ratio is similar to debt equity ratio and it also

accommodates in finding out the leverage of the company. But it also ignores the cost and

implications of other sources of finance (Hendrick and Crawford, 2014).

1.5 Analysis necessary for short and long term financial decisions

Short term financial planning involves decisions for a shorter period of time like 12

months. So all the decisions regarding working capital, buying raw materials, manufacturing,

selling and collecting cash are important in short-term financial decisions. It helps in finding out

the availability of cash to pay bills, inventory management and the policies regarding the credits

(Introduction to financial management. 2015). So it involves short term liquidity and solvency

decisions. Long term planning is much more complex than this. The management has to consider

short and long term objective of the business before making decisions. It involves projecting

revenues, sales, budgets, maintaining solvency and liquidity in the long run of the business. Lot

of changes in policies and strategies have to be done in order to ensure growth and survival of

the business. The profitability, solvency and liquidity ratio are used to make decisions regarding

the future of the company (Law and Singh, 2014).

CONCLUSION

It can be concluded from the above that financial statements and information play an

important for the organisation as well as its stakeholders. These information can be used to take

decisions about the future if the company. Vodafone has been growing at a good pace and the

8

It shows whether the company is collecting its receivables on time or not. But plays an important

role deciding the liquidity position of the company.

Creditor turnover ratio: It accommodates a company to maintain its liquidity position in

the market. But gives the management information about the payment period to the creditors. But

it takes average of all the credit availed which may give wrong indication to individual creditor.

Working capital: It gives essential detail to the company regarding the working capital. Positive

indicates that company while negative indicates that Vodafone has to make changes in it (Law

and Singh, 2014).

Debt equity ratio: It helps an organisation to study the leverage position and risk that it

possess. Too much leverage can be bad for the business as such it helps in maintaining it. The

disadvantage of it is that it ignores the cost of issuing the equity and other sources of finance.

Proprietary ratio: The Proprietary ratio is similar to debt equity ratio and it also

accommodates in finding out the leverage of the company. But it also ignores the cost and

implications of other sources of finance (Hendrick and Crawford, 2014).

1.5 Analysis necessary for short and long term financial decisions

Short term financial planning involves decisions for a shorter period of time like 12

months. So all the decisions regarding working capital, buying raw materials, manufacturing,

selling and collecting cash are important in short-term financial decisions. It helps in finding out

the availability of cash to pay bills, inventory management and the policies regarding the credits

(Introduction to financial management. 2015). So it involves short term liquidity and solvency

decisions. Long term planning is much more complex than this. The management has to consider

short and long term objective of the business before making decisions. It involves projecting

revenues, sales, budgets, maintaining solvency and liquidity in the long run of the business. Lot

of changes in policies and strategies have to be done in order to ensure growth and survival of

the business. The profitability, solvency and liquidity ratio are used to make decisions regarding

the future of the company (Law and Singh, 2014).

CONCLUSION

It can be concluded from the above that financial statements and information play an

important for the organisation as well as its stakeholders. These information can be used to take

decisions about the future if the company. Vodafone has been growing at a good pace and the

8

same is reflected in their statements. But a thorough analysis show that they have lot of problems

maintaining the liquidity position of the company. Analysis of financial statements also gives

useful details about the solvency and efficiency of various business operations. As such financial

decisions have to be taken considering all such factors. This will not only fulfil the short term

objectives of the company but they will also accomplish their long term goals.

9

maintaining the liquidity position of the company. Analysis of financial statements also gives

useful details about the solvency and efficiency of various business operations. As such financial

decisions have to be taken considering all such factors. This will not only fulfil the short term

objectives of the company but they will also accomplish their long term goals.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.