Finance Case Study: Analyzing Vodafone's Hostile Bid for Mannesmann

VerifiedAdded on 2023/06/03

|12

|1750

|471

Case Study

AI Summary

This case study examines Vodafone AirTouch's hostile takeover bid for Mannesmann in 1999, focusing on the strategic rationale, financial implications, and market dynamics of the proposed merger. The analysis covers Mannesmann's initial rejection of Vodafone's friendly offer, the valuation discrepancies between the two companies, and the potential synergies that could result from a successful acquisition. It delves into the swap ratio offered to Mannesmann shareholders, the acceptability of the offer from both Vodafone and Mannesmann shareholder perspectives, and the market's expectations regarding the deal's success. The study also calculates the present value of synergies, identifies potential hurdles Vodafone faced, and discusses the reasons behind Vodafone's eagerness to complete the acquisition, ultimately assessing the valuation and strategic implications of the proposed merger in the context of the rapidly consolidating telecommunications industry.

Running head: FINANCE MERGER AND ACQUISITION

Finance Merger and Acquisition

Name of the Student:

Name of the University:

Authors Note:

Finance Merger and Acquisition

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE MERGER AND ACQUISITION

Contents

The rationale behind the acquisition of Orange by Mannesmann:..................................................2

Strategic implications to Vodafone:................................................................................................2

Description of swap:........................................................................................................................2

Acceptability of offer to shareholders of Mannesmann:.................................................................3

Acceptability of offer to shareholders of Vodafone:.......................................................................3

Market expectations of deal:............................................................................................................3

Present value of synergies:..............................................................................................................4

Hurdles in front of Vodafone:..........................................................................................................4

The reason for eagerness:................................................................................................................4

References:......................................................................................................................................6

Contents

The rationale behind the acquisition of Orange by Mannesmann:..................................................2

Strategic implications to Vodafone:................................................................................................2

Description of swap:........................................................................................................................2

Acceptability of offer to shareholders of Mannesmann:.................................................................3

Acceptability of offer to shareholders of Vodafone:.......................................................................3

Market expectations of deal:............................................................................................................3

Present value of synergies:..............................................................................................................4

Hurdles in front of Vodafone:..........................................................................................................4

The reason for eagerness:................................................................................................................4

References:......................................................................................................................................6

2FINANCE MERGER AND ACQUISITION

The rationale behind the acquisition of Orange by Mannesmann:

The objective behind the acquisition of Orange by Mannesmann was mainly to be the leader in

telecommunication industry in the European market. It was expected that the resulting synergy

subsequent to the merger of Orange and Mannesmann would help the later to not only be the

leader in the European telecommunication market but also to achieve significant amount of

operating profit in the future. The acquisition of Orange would help Mannesmann to effectively

become the leader in the European market and subsequently to be the world leader with

additional acquisitions in the future. With the opportunity to be the leader in the European

market Mannesmann paid a 22% premium over the existing stock price of Orange at the time of

acquisition. The payment of 22% premium was understandable as the expected synergies

subsequent to the acquisition of Orange was significantly huge (Jeong and Weidhaas, 2016).

Strategic implications to Vodafone:

The successful acquisition of Orange by Mannesmann helped the later to come close to be the

leader in the telecommunication market in Europe right behind Telecom Italia Mobile. With the

subsequent synergies that resulted from the acquisition of Orange PLC to the Mannesmann

helped the company to strongly compete against the Vodafone Airtouch PLC. Thus, the

acquisition of Orange PLLC by Mannesmann certainly affected the Vodafone and its hostile

takeover bid of Mannesmann.

Description of swap:

The Vodafone PLC on 17th December valued Mannesmann at €138 billion. The swap ratio on the

basis of the above valuation was 53.7 Vodafone shares for each share of Mannesmann. On that

date the takeover bid was calculated by adding 72.2% premium on the closing share price of

The rationale behind the acquisition of Orange by Mannesmann:

The objective behind the acquisition of Orange by Mannesmann was mainly to be the leader in

telecommunication industry in the European market. It was expected that the resulting synergy

subsequent to the merger of Orange and Mannesmann would help the later to not only be the

leader in the European telecommunication market but also to achieve significant amount of

operating profit in the future. The acquisition of Orange would help Mannesmann to effectively

become the leader in the European market and subsequently to be the world leader with

additional acquisitions in the future. With the opportunity to be the leader in the European

market Mannesmann paid a 22% premium over the existing stock price of Orange at the time of

acquisition. The payment of 22% premium was understandable as the expected synergies

subsequent to the acquisition of Orange was significantly huge (Jeong and Weidhaas, 2016).

Strategic implications to Vodafone:

The successful acquisition of Orange by Mannesmann helped the later to come close to be the

leader in the telecommunication market in Europe right behind Telecom Italia Mobile. With the

subsequent synergies that resulted from the acquisition of Orange PLC to the Mannesmann

helped the company to strongly compete against the Vodafone Airtouch PLC. Thus, the

acquisition of Orange PLLC by Mannesmann certainly affected the Vodafone and its hostile

takeover bid of Mannesmann.

Description of swap:

The Vodafone PLC on 17th December valued Mannesmann at €138 billion. The swap ratio on the

basis of the above valuation was 53.7 Vodafone shares for each share of Mannesmann. On that

date the takeover bid was calculated by adding 72.2% premium on the closing share price of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE MERGER AND ACQUISITION

Mannesmann as on October 18. The market value of Mannesmann’s contribution to the firm

estimated at $121 billion as on the 17th December.

On December 17, 1997

Mannesmann Vodafone

Number of outstanding shares: 517.9 million

shares

31,105 Million

Swap ratio 53.7 shares for each share of

Mannesmann

Number of shares to be issued to Mannesmann

(517.9 million x 53.7)

27811.2 million shares of

Vodafone to acquire

Mannesmann

Acceptability of offer to shareholders of Mannesmann:

Since a 72.2% premium over the closing price of shares on October 18 was offered by Vodafone

and an affordable swap rate of 53.7shares in Vodafone for each share at Mannesmann is certainly

preferable for the shareholders of Mannesmann. From the point of view of Vodafone

shareholders however, the offer made to takeover Mannesmann is not acceptable. Hence, the

shareholders of Vodafone would feel hard done by the offer of the company to take over

Mannesmann with a swap rate 53.7 shares in Vodafone for each share of Mannesmann (Kinsella,

2017).

Mannesmann as on October 18. The market value of Mannesmann’s contribution to the firm

estimated at $121 billion as on the 17th December.

On December 17, 1997

Mannesmann Vodafone

Number of outstanding shares: 517.9 million

shares

31,105 Million

Swap ratio 53.7 shares for each share of

Mannesmann

Number of shares to be issued to Mannesmann

(517.9 million x 53.7)

27811.2 million shares of

Vodafone to acquire

Mannesmann

Acceptability of offer to shareholders of Mannesmann:

Since a 72.2% premium over the closing price of shares on October 18 was offered by Vodafone

and an affordable swap rate of 53.7shares in Vodafone for each share at Mannesmann is certainly

preferable for the shareholders of Mannesmann. From the point of view of Vodafone

shareholders however, the offer made to takeover Mannesmann is not acceptable. Hence, the

shareholders of Vodafone would feel hard done by the offer of the company to take over

Mannesmann with a swap rate 53.7 shares in Vodafone for each share of Mannesmann (Kinsella,

2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE MERGER AND ACQUISITION

Acceptability of offer to shareholders of Vodafone:

The hostile takeover bid of Vodafone to acquire Mannesmann was always under the cloud due to

the continuous rejection of the offer by the management of Mannesmann. The market analysts

have always emphasised the importance of mutual consensus for any merger and acquisition to

go through and achieve desired objectives. Seldom hostile takeovers have resulted success. Thus,

the market was quite aware that the deal have significantly less chance of going through and

even slimmer chance of resulting in synergies.

The acceptability and non-acceptability of respective shareholders of Mannesmann and

Vodafone can be understood from the calculation of shareholding in merged company below:

Mannesmann shareholders' holding in Vodafone would be (%) 47.2

0

27811.20 x 100/ (31105 million + 27811.20 million)

Holding of Vodafone shareholders (100- 47.20)% 52.8

0

Market expectations of deal:

The takeover bid proposed by Vodafone to acquire Mannesmann would have helped the former

to be the undisputed world leader in the telecommunication market. Vodafone expected to be the

worldwide leader in telecommunication market and to gain huge synergy by improving the

Acceptability of offer to shareholders of Vodafone:

The hostile takeover bid of Vodafone to acquire Mannesmann was always under the cloud due to

the continuous rejection of the offer by the management of Mannesmann. The market analysts

have always emphasised the importance of mutual consensus for any merger and acquisition to

go through and achieve desired objectives. Seldom hostile takeovers have resulted success. Thus,

the market was quite aware that the deal have significantly less chance of going through and

even slimmer chance of resulting in synergies.

The acceptability and non-acceptability of respective shareholders of Mannesmann and

Vodafone can be understood from the calculation of shareholding in merged company below:

Mannesmann shareholders' holding in Vodafone would be (%) 47.2

0

27811.20 x 100/ (31105 million + 27811.20 million)

Holding of Vodafone shareholders (100- 47.20)% 52.8

0

Market expectations of deal:

The takeover bid proposed by Vodafone to acquire Mannesmann would have helped the former

to be the undisputed world leader in the telecommunication market. Vodafone expected to be the

worldwide leader in telecommunication market and to gain huge synergy by improving the

5FINANCE MERGER AND ACQUISITION

financial performance and position of the company. One of the biggest reasons behind the

strategy of Vodafone to acquire Mannesmann is to expand the business operations of Vodafone.

Mannesmann has number of different types of business including equipment in

telecommunication industry, internet services, technology in plastics handling, technology in

steel tubes, hydraulic and many more. The takeover if successful would have helped Vodafone to

expand business operations in different fields. Mannesmann has big market share in Germany

and Vodafone will be able to expand its telecommunication operations to the whole of Germany

subsequent to the acquisition of Mannesmann (Mager and Meyer-Fackler, 2017).

Present value of synergies:

The market estimated that the success of acquiring Mannesmann is around 0.6 and with the

expected market synergy 69,890.68 million in Euro. The calculation of market synergy is

provided below:

Amounts are in Euro million Mannesmann Vodafone

Share price on that date 234 4.9569

Number of outstanding shares: (million) 517.9 31105

Market value 121188.6 154184.375

Combined market value after acquisition (121189 + 154184) 275372.975

financial performance and position of the company. One of the biggest reasons behind the

strategy of Vodafone to acquire Mannesmann is to expand the business operations of Vodafone.

Mannesmann has number of different types of business including equipment in

telecommunication industry, internet services, technology in plastics handling, technology in

steel tubes, hydraulic and many more. The takeover if successful would have helped Vodafone to

expand business operations in different fields. Mannesmann has big market share in Germany

and Vodafone will be able to expand its telecommunication operations to the whole of Germany

subsequent to the acquisition of Mannesmann (Mager and Meyer-Fackler, 2017).

Present value of synergies:

The market estimated that the success of acquiring Mannesmann is around 0.6 and with the

expected market synergy 69,890.68 million in Euro. The calculation of market synergy is

provided below:

Amounts are in Euro million Mannesmann Vodafone

Share price on that date 234 4.9569

Number of outstanding shares: (million) 517.9 31105

Market value 121188.6 154184.375

Combined market value after acquisition (121189 + 154184) 275372.975

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE MERGER AND ACQUISITION

Contribution of each firms (121189 x

100/275373); (154184 x 100/275373)

44.01 55.9

9

Market value of the combined firm on October 21 (Excluding synergy)

Amounts are in Euro million Mannesmann Vodafone

Outstanding number of shares (Millions) 517.9 31105

Share price 145.35 4.186

Market value 75,276.77 130,205.5

3

Combined market value 205,482.3

0

Market value on December 17 (including

synergy)

Outstanding number of shares (Millions) 517.9 31105

Share price 234 4.9569

Market value 121,188.60 154,184.3

7

Contribution of each firms (121189 x

100/275373); (154184 x 100/275373)

44.01 55.9

9

Market value of the combined firm on October 21 (Excluding synergy)

Amounts are in Euro million Mannesmann Vodafone

Outstanding number of shares (Millions) 517.9 31105

Share price 145.35 4.186

Market value 75,276.77 130,205.5

3

Combined market value 205,482.3

0

Market value on December 17 (including

synergy)

Outstanding number of shares (Millions) 517.9 31105

Share price 234 4.9569

Market value 121,188.60 154,184.3

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE MERGER AND ACQUISITION

Combined market value 275,372.9

7

Value of synergy (275372.97 - 205482.30) 69,890.6

8

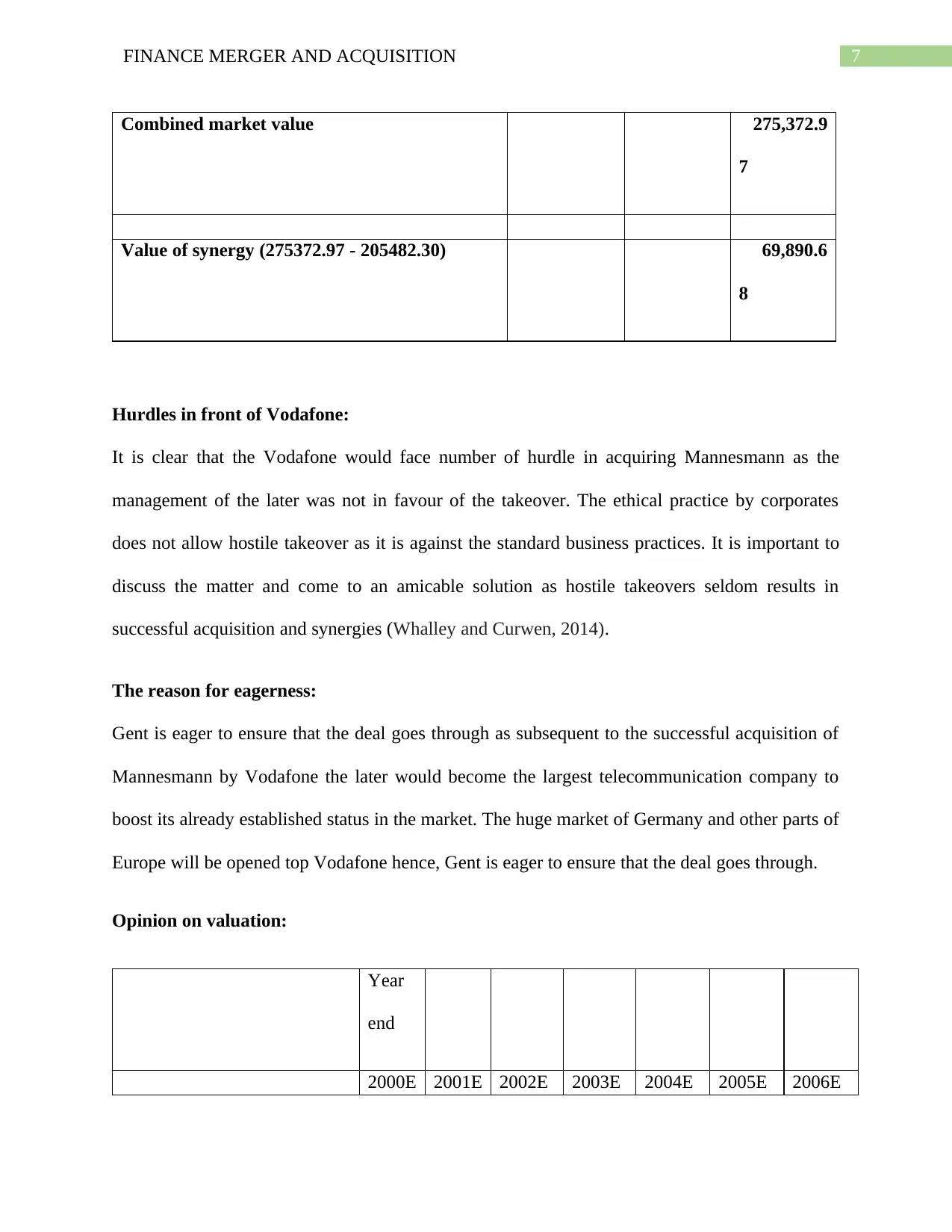

Hurdles in front of Vodafone:

It is clear that the Vodafone would face number of hurdle in acquiring Mannesmann as the

management of the later was not in favour of the takeover. The ethical practice by corporates

does not allow hostile takeover as it is against the standard business practices. It is important to

discuss the matter and come to an amicable solution as hostile takeovers seldom results in

successful acquisition and synergies (Whalley and Curwen, 2014).

The reason for eagerness:

Gent is eager to ensure that the deal goes through as subsequent to the successful acquisition of

Mannesmann by Vodafone the later would become the largest telecommunication company to

boost its already established status in the market. The huge market of Germany and other parts of

Europe will be opened top Vodafone hence, Gent is eager to ensure that the deal goes through.

Opinion on valuation:

Year

end

2000E 2001E 2002E 2003E 2004E 2005E 2006E

Combined market value 275,372.9

7

Value of synergy (275372.97 - 205482.30) 69,890.6

8

Hurdles in front of Vodafone:

It is clear that the Vodafone would face number of hurdle in acquiring Mannesmann as the

management of the later was not in favour of the takeover. The ethical practice by corporates

does not allow hostile takeover as it is against the standard business practices. It is important to

discuss the matter and come to an amicable solution as hostile takeovers seldom results in

successful acquisition and synergies (Whalley and Curwen, 2014).

The reason for eagerness:

Gent is eager to ensure that the deal goes through as subsequent to the successful acquisition of

Mannesmann by Vodafone the later would become the largest telecommunication company to

boost its already established status in the market. The huge market of Germany and other parts of

Europe will be opened top Vodafone hence, Gent is eager to ensure that the deal goes through.

Opinion on valuation:

Year

end

2000E 2001E 2002E 2003E 2004E 2005E 2006E

8FINANCE MERGER AND ACQUISITION

Synergy in revenue

- 50.00

1

53.00

46

9.00

656.

00

977.

00

1,22

1.00

Cost of revenue synergy

-

(

40.00)

(1

07.00)

(28

1.00)

(328.

00)

(488.

00)

(61

0.00)

Synergy cost

- 80.00

2

00.00

50

0.00

656.

00

732.

00

87

9.00

Impact on operating profit (in

total) - 90.00

2

46.00

68

8.00

984.

00

1,221.

00

1,48

9.00

Reductions and savings in

capital expenditures - 60.00

1

47.00

36

0.00

420.

00

469.

00

50

6.00

Profit after tax

- 58.50

1

59.90

44

7.20

639.

60

793.

65

96

7.85

After tax synergy in total

- 118.5

0

3

06.90

80

7.20

1,059.

60

1,262.

65

1,47

3.85

110.1

3

2

65.08

64

7.95

790.

48

875.

43

94

9.69

Synergy in revenue

- 50.00

1

53.00

46

9.00

656.

00

977.

00

1,22

1.00

Cost of revenue synergy

-

(

40.00)

(1

07.00)

(28

1.00)

(328.

00)

(488.

00)

(61

0.00)

Synergy cost

- 80.00

2

00.00

50

0.00

656.

00

732.

00

87

9.00

Impact on operating profit (in

total) - 90.00

2

46.00

68

8.00

984.

00

1,221.

00

1,48

9.00

Reductions and savings in

capital expenditures - 60.00

1

47.00

36

0.00

420.

00

469.

00

50

6.00

Profit after tax

- 58.50

1

59.90

44

7.20

639.

60

793.

65

96

7.85

After tax synergy in total

- 118.5

0

3

06.90

80

7.20

1,059.

60

1,262.

65

1,47

3.85

110.1

3

2

65.08

64

7.95

790.

48

875.

43

94

9.69

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE MERGER AND ACQUISITION

On the basis of following assumptions the present value of after tax synergies and Vodafone

approximation have been calculated below.

Assumptions:

Assuming Weighted average cost of capital

(WACC)

7.60%

Perpetual growth rate 4%

Tax rate 35%

Particulars Amount

(€ million)

Present value of after tax synergy by using perpetual growth model

Formula {Profit after tax of last year / (Cost of capital - growth rate)}

Present value of synergies {967.85/ (7.60% -4.00%)} 26,884.7

2

Less: Tax @35% (26884.72 x 35%) 9,409.6

5

Vodafone's approximation from synergies 17,475.0

On the basis of following assumptions the present value of after tax synergies and Vodafone

approximation have been calculated below.

Assumptions:

Assuming Weighted average cost of capital

(WACC)

7.60%

Perpetual growth rate 4%

Tax rate 35%

Particulars Amount

(€ million)

Present value of after tax synergy by using perpetual growth model

Formula {Profit after tax of last year / (Cost of capital - growth rate)}

Present value of synergies {967.85/ (7.60% -4.00%)} 26,884.7

2

Less: Tax @35% (26884.72 x 35%) 9,409.6

5

Vodafone's approximation from synergies 17,475.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE MERGER AND ACQUISITION

7

As can be seen that the premium paid is EURO 7,863 million to purchase Mannesmann shares

however the approximation of synergy is EURO 17,475 million is significantly higher thus, it is

a great proposition from the point of view of Vodafone.

7

As can be seen that the premium paid is EURO 7,863 million to purchase Mannesmann shares

however the approximation of synergy is EURO 17,475 million is significantly higher thus, it is

a great proposition from the point of view of Vodafone.

11FINANCE MERGER AND ACQUISITION

References:

Jeong, D.H. and Weidhaas, M., 2016. Executive Compensation: Mannesmann v. Disney-A Case

Study.

Kinsella, M., 2017. Hostile takeovers—An analysis through just war theory. Journal of Business

Ethics, 146(4), pp.771-786. Kinsella, M., 2017. Hostile takeovers—An analysis through just war

theory. Journal of Business Ethics, 146(4), pp.771-786.

Mager, F. and Meyer-Fackler, M., 2017. Mergers and acquisitions in Germany: 1981–

2010. Global Finance Journal, 34, pp.32-42.

Whalley, J. and Curwen, P., 2014. Managing tax by organizational means: the case of

Vodafone. Public Money & Management, 34(5), pp.371-378.

References:

Jeong, D.H. and Weidhaas, M., 2016. Executive Compensation: Mannesmann v. Disney-A Case

Study.

Kinsella, M., 2017. Hostile takeovers—An analysis through just war theory. Journal of Business

Ethics, 146(4), pp.771-786. Kinsella, M., 2017. Hostile takeovers—An analysis through just war

theory. Journal of Business Ethics, 146(4), pp.771-786.

Mager, F. and Meyer-Fackler, M., 2017. Mergers and acquisitions in Germany: 1981–

2010. Global Finance Journal, 34, pp.32-42.

Whalley, J. and Curwen, P., 2014. Managing tax by organizational means: the case of

Vodafone. Public Money & Management, 34(5), pp.371-378.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.