Financial Performance Analysis: Vodafone & Talk-Talk Telecom Plc

VerifiedAdded on 2023/06/03

|18

|4254

|135

Report

AI Summary

This report conducts a financial analysis of Vodafone Group Plc. and Talk-Talk Telecom Group Plc., two leading telecommunication companies in the UK, using ratio analysis based on their annual reports for the year ending March 31, 2016. It includes both intra-firm (comparing FY 2016 with FY 2015) and inter-firm comparisons to assess profitability, liquidity, efficiency, and solvency. The analysis reveals insights into each company's financial health, highlighting strengths and weaknesses, and identifying factors contributing to competitive advantages. Limitations of ratio analysis due to differing accounting policies and currency differences are also acknowledged.

Running Head: Financial and Auditing Studies

Financial Accounting and Auditing and Taxation

Financial Accounting and Auditing and Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Auditing Studies

Introduction

Purpose and objective of the report:

This report presents the financial analysis of two leading corporations: Vodafone Group Plc.

and Talk-Talk Telecom Group Plc. Both the companies are operating in the

telecommunication industry of United Kingdom and also are listed on the London Stock

Exchange. The financial analysis is undertaken to assess the financial health of both the

companies using the key technique of financial analysis i.e. Ratio analysis. As a part of ratio

analysis various financial ratios are determined to evaluate the company’s financial

performance in terms of profitability, liquidity, efficiency, solvency and its investment worth.

The financial information in relation to the said aspects is derived from the annual reports for

the year ending on 31st March, 2016. Both, inter-firm and intra-firm comparison of the

financial performance is carried out under this report. The intra-firm analysis of performance

of both the companies is carried by comparing the financial results of FY 2016 with that of

FY 2015 in order to determine whether the overall financial performance has improved or

deteriorated and to identify the reasons of the variation in the performance over the last two

years. The inter-firm analysis is undertaken to identify and analyse as to which company is

performing better and what are the factors that have contributed to provide competitive

advantage to one company over other.

Background of the companies

Vodafone Group Plc. had started its business in 1984 and is headquartered in Newbury,

United Kingdom. The company operates its business in Europe, Africa, Middle East and Asia

Pacific Regions. It provides a wide range of products of mobile services to its customers such

as call, text, broadband, voicemails, mobile money services, television offerings and various

other communications solutions like Vodafone Meet Anywhere and Vodafone One Net

Introduction

Purpose and objective of the report:

This report presents the financial analysis of two leading corporations: Vodafone Group Plc.

and Talk-Talk Telecom Group Plc. Both the companies are operating in the

telecommunication industry of United Kingdom and also are listed on the London Stock

Exchange. The financial analysis is undertaken to assess the financial health of both the

companies using the key technique of financial analysis i.e. Ratio analysis. As a part of ratio

analysis various financial ratios are determined to evaluate the company’s financial

performance in terms of profitability, liquidity, efficiency, solvency and its investment worth.

The financial information in relation to the said aspects is derived from the annual reports for

the year ending on 31st March, 2016. Both, inter-firm and intra-firm comparison of the

financial performance is carried out under this report. The intra-firm analysis of performance

of both the companies is carried by comparing the financial results of FY 2016 with that of

FY 2015 in order to determine whether the overall financial performance has improved or

deteriorated and to identify the reasons of the variation in the performance over the last two

years. The inter-firm analysis is undertaken to identify and analyse as to which company is

performing better and what are the factors that have contributed to provide competitive

advantage to one company over other.

Background of the companies

Vodafone Group Plc. had started its business in 1984 and is headquartered in Newbury,

United Kingdom. The company operates its business in Europe, Africa, Middle East and Asia

Pacific Regions. It provides a wide range of products of mobile services to its customers such

as call, text, broadband, voicemails, mobile money services, television offerings and various

other communications solutions like Vodafone Meet Anywhere and Vodafone One Net

Running Head: Financial and Auditing Studies

Enterprise. Moreover, Vodafone provides internet of things connection to the users of its

network so as to allow them to communicate in the secured and reliable manner over the

internet using its cloud services. Further, various carrier services are also being provided by

the company like for example international voice, IP transit and message services. Along

with the said services, Vodafone is also engaged in the provision of mobile virtual network

services. Currently, the company is serving over 536 million customers for its mobile

services and around 20 million customers for its broadband services. The company has a

customer base which comprises of domestic businesses of varied sizes, commercial units, and

various public sector units at national and international level both. Its 4G network is

successfully running across 90 countries in the world. Vodafone Group is the holding

company of various companies such as Vodafone GmbH, Vodafone Limited, Vodafone

Marketing UK, Quickcomm Pty Limited, Vodafone Espana, S.A.U., CWGNL S.A. and

Vodafone Albania Sh.A.

Talk-Talk Telecom Group Plc. is also a provider of telecommunication services across

London. The company had commenced its operations in 2003 and is headquartered in

London only. It provides its customers a wide range of services such as broadband, voice

telephony, mobile communication and telephone services. Currently, Talk-Talk Group is

serving over 4 million customers from both residential as well as commercial units through

its Talk-Talk business brands. It offers 3 customer propositions: Simply Broadband, Essential

TV and Plus TV. The company is a business to business telecom service provider that is

serving around 180000 business units and public sector units of the nation. The products and

services of the company includes connectivity & networking, hosted solutions, internet

protocol telephone systems and voice as well as data services mainly offered to small and

middle sized units of UK (Financial Times, 2018).

Limitations of comparison under ratio analysis

Enterprise. Moreover, Vodafone provides internet of things connection to the users of its

network so as to allow them to communicate in the secured and reliable manner over the

internet using its cloud services. Further, various carrier services are also being provided by

the company like for example international voice, IP transit and message services. Along

with the said services, Vodafone is also engaged in the provision of mobile virtual network

services. Currently, the company is serving over 536 million customers for its mobile

services and around 20 million customers for its broadband services. The company has a

customer base which comprises of domestic businesses of varied sizes, commercial units, and

various public sector units at national and international level both. Its 4G network is

successfully running across 90 countries in the world. Vodafone Group is the holding

company of various companies such as Vodafone GmbH, Vodafone Limited, Vodafone

Marketing UK, Quickcomm Pty Limited, Vodafone Espana, S.A.U., CWGNL S.A. and

Vodafone Albania Sh.A.

Talk-Talk Telecom Group Plc. is also a provider of telecommunication services across

London. The company had commenced its operations in 2003 and is headquartered in

London only. It provides its customers a wide range of services such as broadband, voice

telephony, mobile communication and telephone services. Currently, Talk-Talk Group is

serving over 4 million customers from both residential as well as commercial units through

its Talk-Talk business brands. It offers 3 customer propositions: Simply Broadband, Essential

TV and Plus TV. The company is a business to business telecom service provider that is

serving around 180000 business units and public sector units of the nation. The products and

services of the company includes connectivity & networking, hosted solutions, internet

protocol telephone systems and voice as well as data services mainly offered to small and

middle sized units of UK (Financial Times, 2018).

Limitations of comparison under ratio analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial and Auditing Studies

Although, ratio analysis is a useful technique of measuring and analysing the financial

performance of the company but it suffers from certain limitations which has influenced the

financial analysis. The problem with this type of financial comparison is that the accounting

policies that have been used by the companies while preparing the financial statements might

be different which does not provide a common ground to carry out the comparison. Also, the

financial statements of both the companies are presented into two different currencies as

Vodafone Group has published its financial reports in Euro Currency whereas Talk-Talk

Group has prepared and published its annual financial statements in Pound Sterling due to

which makes it difficult for the users of report to compare the performances (Foster, 2004).

Ratio Analysis

Refer Appendix for the ratio calculations:

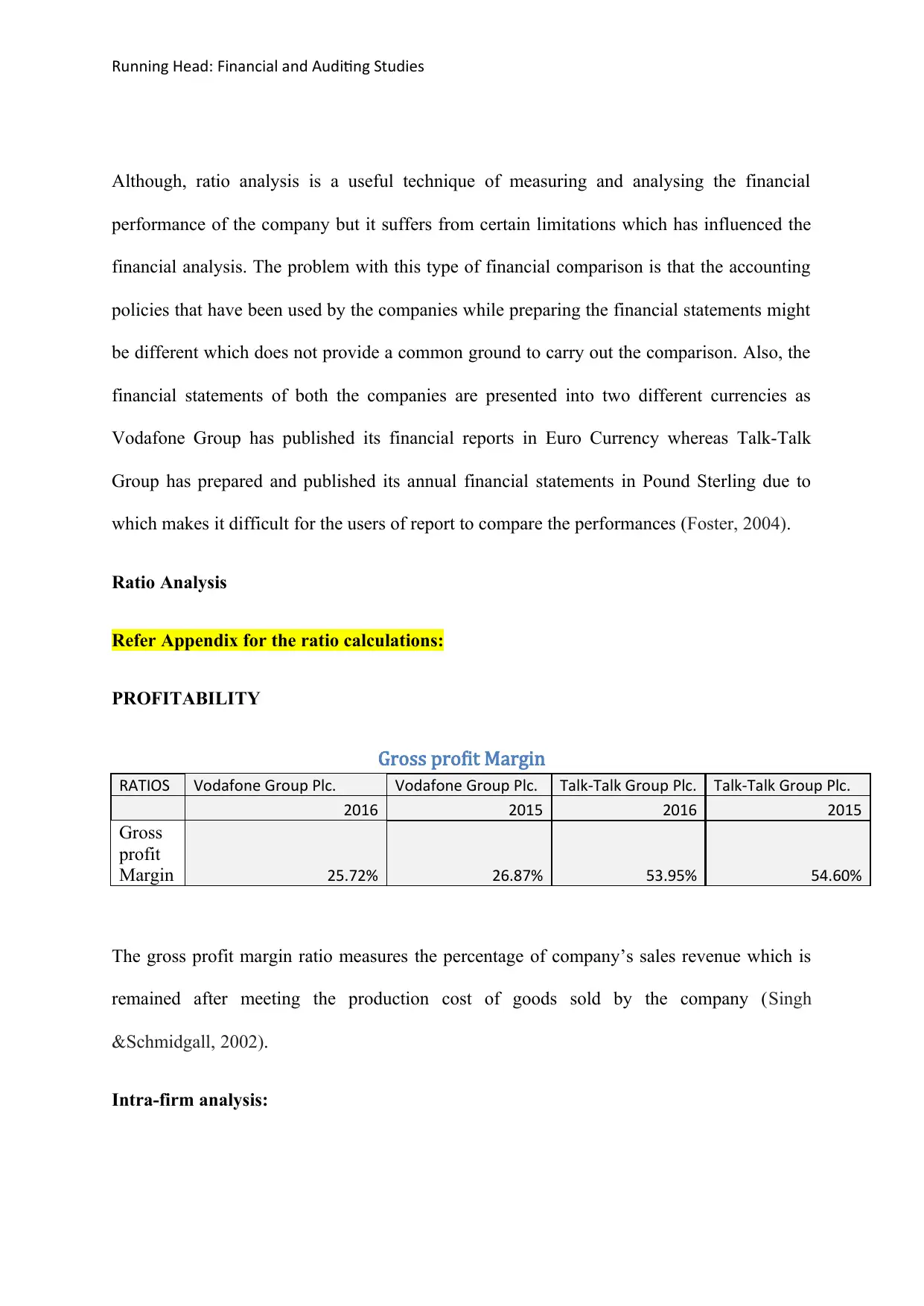

PROFITABILITY

Gross profit Margin

RATIOS Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Gross

profit

Margin 25.72% 26.87% 53.95% 54.60%

The gross profit margin ratio measures the percentage of company’s sales revenue which is

remained after meeting the production cost of goods sold by the company (Singh

&Schmidgall, 2002).

Intra-firm analysis:

Although, ratio analysis is a useful technique of measuring and analysing the financial

performance of the company but it suffers from certain limitations which has influenced the

financial analysis. The problem with this type of financial comparison is that the accounting

policies that have been used by the companies while preparing the financial statements might

be different which does not provide a common ground to carry out the comparison. Also, the

financial statements of both the companies are presented into two different currencies as

Vodafone Group has published its financial reports in Euro Currency whereas Talk-Talk

Group has prepared and published its annual financial statements in Pound Sterling due to

which makes it difficult for the users of report to compare the performances (Foster, 2004).

Ratio Analysis

Refer Appendix for the ratio calculations:

PROFITABILITY

Gross profit Margin

RATIOS Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Gross

profit

Margin 25.72% 26.87% 53.95% 54.60%

The gross profit margin ratio measures the percentage of company’s sales revenue which is

remained after meeting the production cost of goods sold by the company (Singh

&Schmidgall, 2002).

Intra-firm analysis:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Auditing Studies

Vodafone: The gross profit margin of the company has declined in 2016 as compared to 2015

due to the reason that the revenue from sales was decreased in 2016 but the cost of goods sold

did not decline with the same rate of decline in sales.

Talk-Talk Group: Even though the sales in 2016 were higher than 2015 but the GP margin of

the company declined because the rate of cost of production in relation to sales was higher in

2016.

Inter firm Analysis:

The GP margin of Talk-Talk Group is almost double the GP margin of Vodafone. This

shows that Talk-Talk is more profitable than Vodafone as it is incurred lower production cost

in relation to the sales of the companies.

Net Profit Margin

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Net

profit

Margin -9.82% 13.64% 0.11% 4.01%

The net profit margin ratio depicts the percentage of earnings left out of the total revenues

generated from the sales made during the course of business in the given period (Foster,

2004).

Intra-firm analysis:

Vodafone: There has been a significant decline in the net profit of the company in 2016 as

compared to 2015 due to incurrence of heavy financing costs and impairment losses and due

to this it had to incur losses in 2016.

Vodafone: The gross profit margin of the company has declined in 2016 as compared to 2015

due to the reason that the revenue from sales was decreased in 2016 but the cost of goods sold

did not decline with the same rate of decline in sales.

Talk-Talk Group: Even though the sales in 2016 were higher than 2015 but the GP margin of

the company declined because the rate of cost of production in relation to sales was higher in

2016.

Inter firm Analysis:

The GP margin of Talk-Talk Group is almost double the GP margin of Vodafone. This

shows that Talk-Talk is more profitable than Vodafone as it is incurred lower production cost

in relation to the sales of the companies.

Net Profit Margin

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Net

profit

Margin -9.82% 13.64% 0.11% 4.01%

The net profit margin ratio depicts the percentage of earnings left out of the total revenues

generated from the sales made during the course of business in the given period (Foster,

2004).

Intra-firm analysis:

Vodafone: There has been a significant decline in the net profit of the company in 2016 as

compared to 2015 due to incurrence of heavy financing costs and impairment losses and due

to this it had to incur losses in 2016.

Running Head: Financial and Auditing Studies

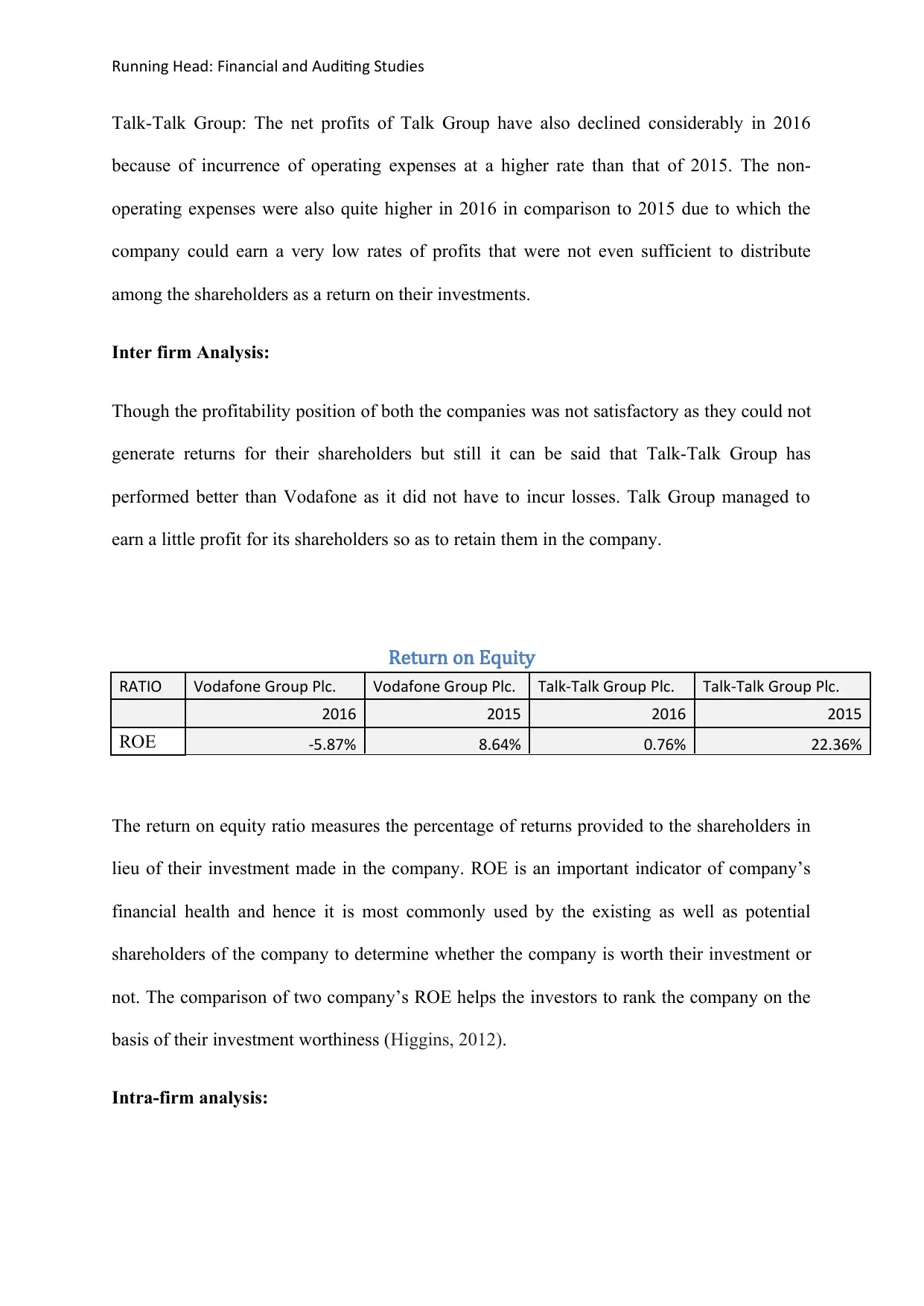

Talk-Talk Group: The net profits of Talk Group have also declined considerably in 2016

because of incurrence of operating expenses at a higher rate than that of 2015. The non-

operating expenses were also quite higher in 2016 in comparison to 2015 due to which the

company could earn a very low rates of profits that were not even sufficient to distribute

among the shareholders as a return on their investments.

Inter firm Analysis:

Though the profitability position of both the companies was not satisfactory as they could not

generate returns for their shareholders but still it can be said that Talk-Talk Group has

performed better than Vodafone as it did not have to incur losses. Talk Group managed to

earn a little profit for its shareholders so as to retain them in the company.

Return on Equity

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

ROE -5.87% 8.64% 0.76% 22.36%

The return on equity ratio measures the percentage of returns provided to the shareholders in

lieu of their investment made in the company. ROE is an important indicator of company’s

financial health and hence it is most commonly used by the existing as well as potential

shareholders of the company to determine whether the company is worth their investment or

not. The comparison of two company’s ROE helps the investors to rank the company on the

basis of their investment worthiness (Higgins, 2012).

Intra-firm analysis:

Talk-Talk Group: The net profits of Talk Group have also declined considerably in 2016

because of incurrence of operating expenses at a higher rate than that of 2015. The non-

operating expenses were also quite higher in 2016 in comparison to 2015 due to which the

company could earn a very low rates of profits that were not even sufficient to distribute

among the shareholders as a return on their investments.

Inter firm Analysis:

Though the profitability position of both the companies was not satisfactory as they could not

generate returns for their shareholders but still it can be said that Talk-Talk Group has

performed better than Vodafone as it did not have to incur losses. Talk Group managed to

earn a little profit for its shareholders so as to retain them in the company.

Return on Equity

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

ROE -5.87% 8.64% 0.76% 22.36%

The return on equity ratio measures the percentage of returns provided to the shareholders in

lieu of their investment made in the company. ROE is an important indicator of company’s

financial health and hence it is most commonly used by the existing as well as potential

shareholders of the company to determine whether the company is worth their investment or

not. The comparison of two company’s ROE helps the investors to rank the company on the

basis of their investment worthiness (Higgins, 2012).

Intra-firm analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial and Auditing Studies

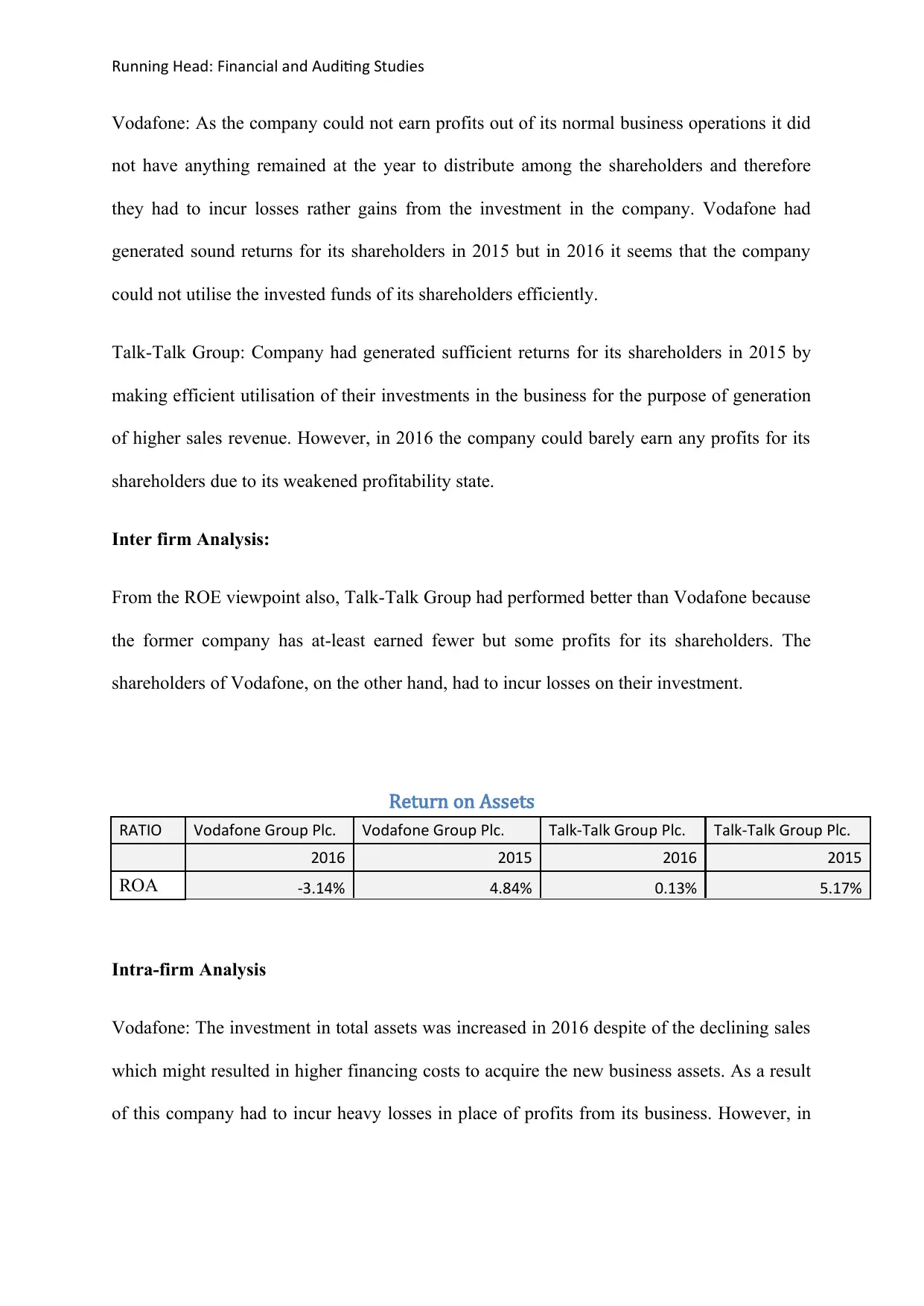

Vodafone: As the company could not earn profits out of its normal business operations it did

not have anything remained at the year to distribute among the shareholders and therefore

they had to incur losses rather gains from the investment in the company. Vodafone had

generated sound returns for its shareholders in 2015 but in 2016 it seems that the company

could not utilise the invested funds of its shareholders efficiently.

Talk-Talk Group: Company had generated sufficient returns for its shareholders in 2015 by

making efficient utilisation of their investments in the business for the purpose of generation

of higher sales revenue. However, in 2016 the company could barely earn any profits for its

shareholders due to its weakened profitability state.

Inter firm Analysis:

From the ROE viewpoint also, Talk-Talk Group had performed better than Vodafone because

the former company has at-least earned fewer but some profits for its shareholders. The

shareholders of Vodafone, on the other hand, had to incur losses on their investment.

Return on Assets

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

ROA -3.14% 4.84% 0.13% 5.17%

Intra-firm Analysis

Vodafone: The investment in total assets was increased in 2016 despite of the declining sales

which might resulted in higher financing costs to acquire the new business assets. As a result

of this company had to incur heavy losses in place of profits from its business. However, in

Vodafone: As the company could not earn profits out of its normal business operations it did

not have anything remained at the year to distribute among the shareholders and therefore

they had to incur losses rather gains from the investment in the company. Vodafone had

generated sound returns for its shareholders in 2015 but in 2016 it seems that the company

could not utilise the invested funds of its shareholders efficiently.

Talk-Talk Group: Company had generated sufficient returns for its shareholders in 2015 by

making efficient utilisation of their investments in the business for the purpose of generation

of higher sales revenue. However, in 2016 the company could barely earn any profits for its

shareholders due to its weakened profitability state.

Inter firm Analysis:

From the ROE viewpoint also, Talk-Talk Group had performed better than Vodafone because

the former company has at-least earned fewer but some profits for its shareholders. The

shareholders of Vodafone, on the other hand, had to incur losses on their investment.

Return on Assets

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

ROA -3.14% 4.84% 0.13% 5.17%

Intra-firm Analysis

Vodafone: The investment in total assets was increased in 2016 despite of the declining sales

which might resulted in higher financing costs to acquire the new business assets. As a result

of this company had to incur heavy losses in place of profits from its business. However, in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Auditing Studies

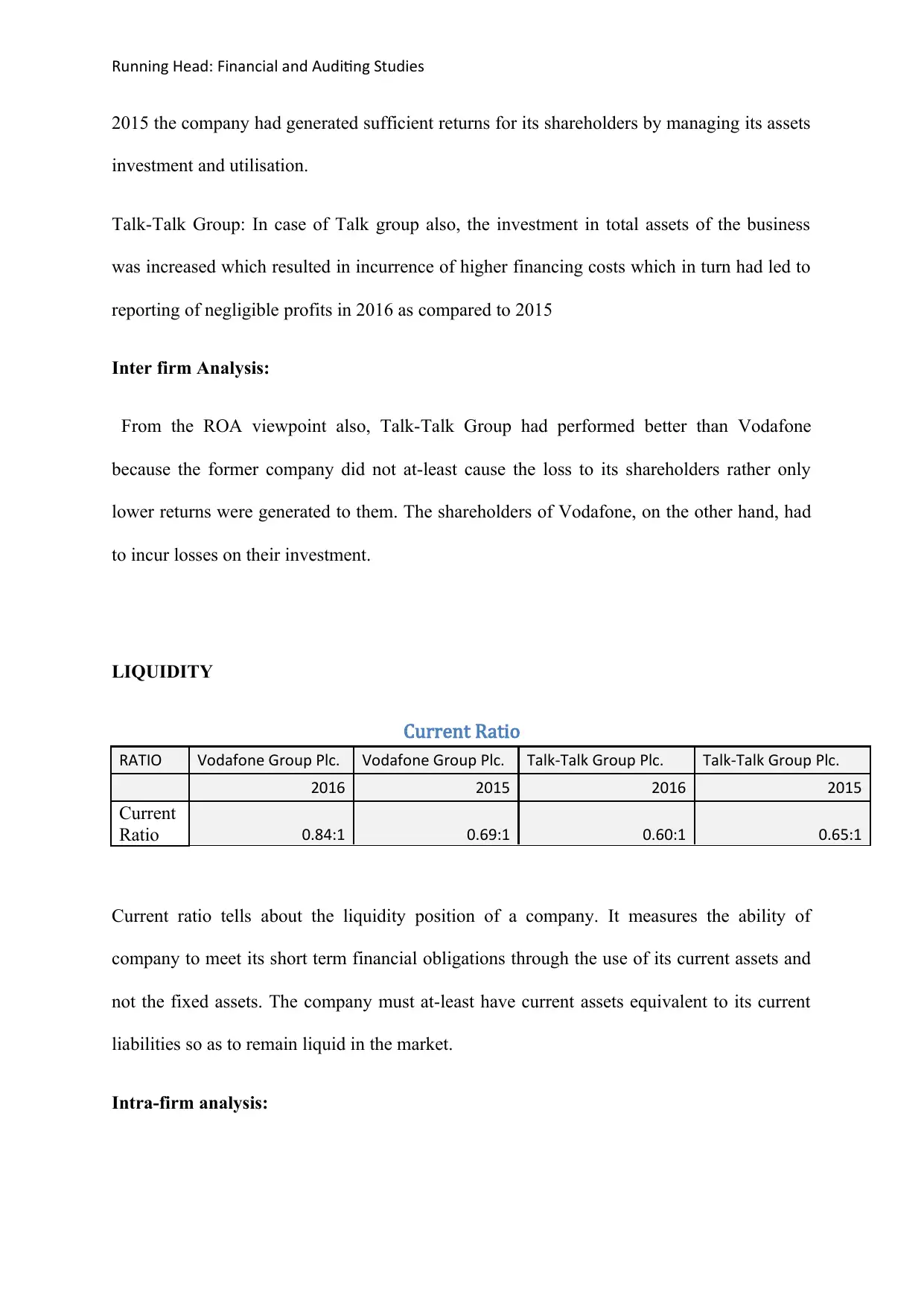

2015 the company had generated sufficient returns for its shareholders by managing its assets

investment and utilisation.

Talk-Talk Group: In case of Talk group also, the investment in total assets of the business

was increased which resulted in incurrence of higher financing costs which in turn had led to

reporting of negligible profits in 2016 as compared to 2015

Inter firm Analysis:

From the ROA viewpoint also, Talk-Talk Group had performed better than Vodafone

because the former company did not at-least cause the loss to its shareholders rather only

lower returns were generated to them. The shareholders of Vodafone, on the other hand, had

to incur losses on their investment.

LIQUIDITY

Current Ratio

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Current

Ratio 0.84:1 0.69:1 0.60:1 0.65:1

Current ratio tells about the liquidity position of a company. It measures the ability of

company to meet its short term financial obligations through the use of its current assets and

not the fixed assets. The company must at-least have current assets equivalent to its current

liabilities so as to remain liquid in the market.

Intra-firm analysis:

2015 the company had generated sufficient returns for its shareholders by managing its assets

investment and utilisation.

Talk-Talk Group: In case of Talk group also, the investment in total assets of the business

was increased which resulted in incurrence of higher financing costs which in turn had led to

reporting of negligible profits in 2016 as compared to 2015

Inter firm Analysis:

From the ROA viewpoint also, Talk-Talk Group had performed better than Vodafone

because the former company did not at-least cause the loss to its shareholders rather only

lower returns were generated to them. The shareholders of Vodafone, on the other hand, had

to incur losses on their investment.

LIQUIDITY

Current Ratio

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Current

Ratio 0.84:1 0.69:1 0.60:1 0.65:1

Current ratio tells about the liquidity position of a company. It measures the ability of

company to meet its short term financial obligations through the use of its current assets and

not the fixed assets. The company must at-least have current assets equivalent to its current

liabilities so as to remain liquid in the market.

Intra-firm analysis:

Running Head: Financial and Auditing Studies

Vodafone: The liquidity position of the company in both the years under consideration is

quite lower than the ideal current ratio of 2:1. Current ratio of Vodafone is indicating that

company could not have met its current liabilities as and when they fell due in 2016 and 2015

and due to which it had to face the liquidity crunch. However, there has been a slight

improvement in the liquidity state of Vodafone in 2016 because of increased investment in

current assets and by reducing the current obligations of business.

Talk-Talk Group: The liquidity position of Talk Group in 2016 and 2015 was below average

due to high short term financial obligations as compared to current economic resources to

meet those obligations (Talk-Talk Group, 2015). Moreover, in 2016 there had been a further

decline in the current ratio which worsened more its liquidity state.

Inter firm Analysis:

From the liquidity point of view both the companies have performed below average but still

it could be said that Vodafone had performed better than Talk-Talk as Vodafone had higher

proportion of current assets.

SOLVENCY

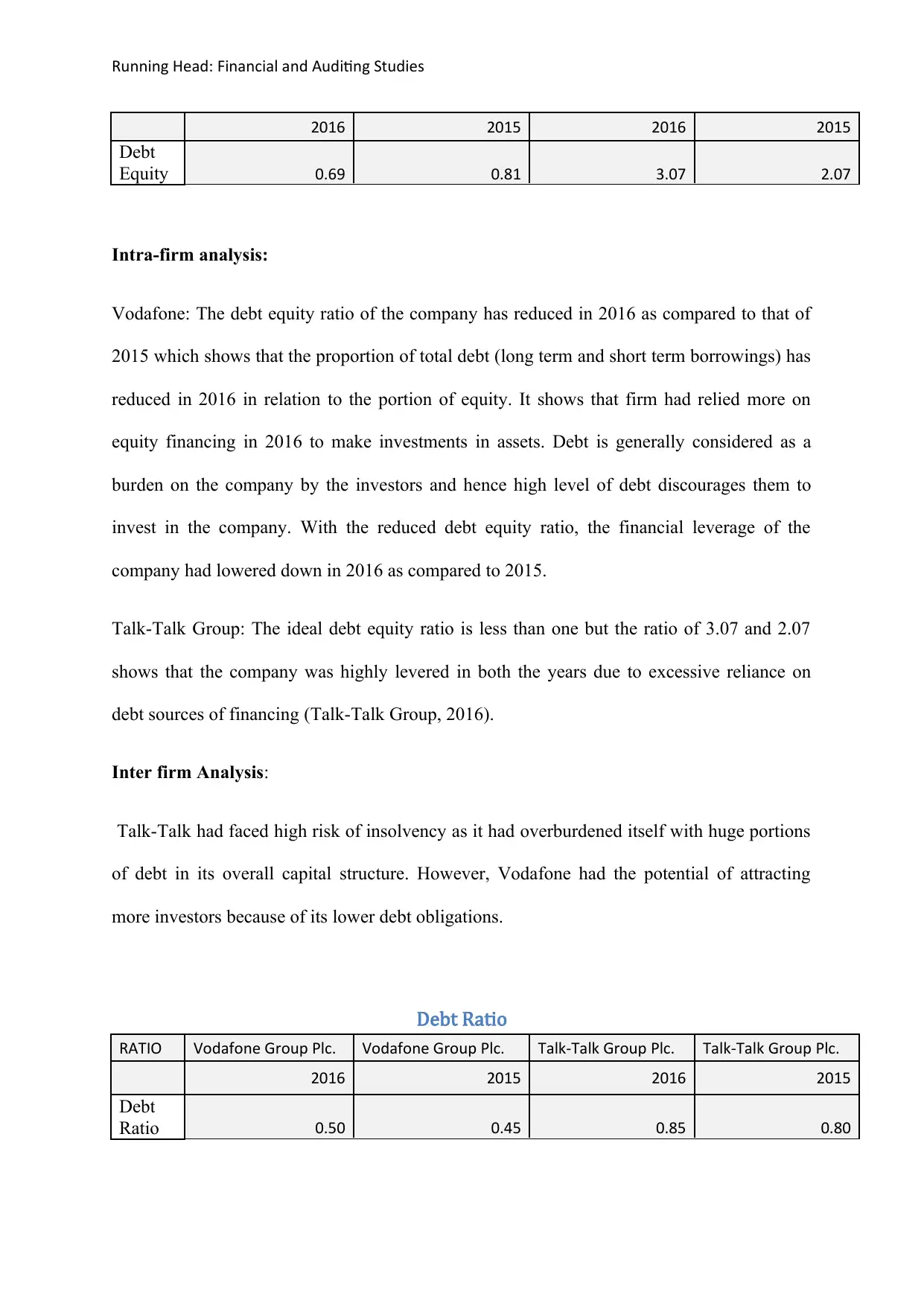

Debt equity ratio

The solvency position of the business has been determined using the key solvency ratios such

as debt equity ratio, debt ratio and the time interest ratio(Lee, Lee & Lee, 2009). Debt equity

ratio shows the relative proportion of total debt to total equity used to finance the assets of the

company.

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

Vodafone: The liquidity position of the company in both the years under consideration is

quite lower than the ideal current ratio of 2:1. Current ratio of Vodafone is indicating that

company could not have met its current liabilities as and when they fell due in 2016 and 2015

and due to which it had to face the liquidity crunch. However, there has been a slight

improvement in the liquidity state of Vodafone in 2016 because of increased investment in

current assets and by reducing the current obligations of business.

Talk-Talk Group: The liquidity position of Talk Group in 2016 and 2015 was below average

due to high short term financial obligations as compared to current economic resources to

meet those obligations (Talk-Talk Group, 2015). Moreover, in 2016 there had been a further

decline in the current ratio which worsened more its liquidity state.

Inter firm Analysis:

From the liquidity point of view both the companies have performed below average but still

it could be said that Vodafone had performed better than Talk-Talk as Vodafone had higher

proportion of current assets.

SOLVENCY

Debt equity ratio

The solvency position of the business has been determined using the key solvency ratios such

as debt equity ratio, debt ratio and the time interest ratio(Lee, Lee & Lee, 2009). Debt equity

ratio shows the relative proportion of total debt to total equity used to finance the assets of the

company.

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Financial and Auditing Studies

2016 2015 2016 2015

Debt

Equity 0.69 0.81 3.07 2.07

Intra-firm analysis:

Vodafone: The debt equity ratio of the company has reduced in 2016 as compared to that of

2015 which shows that the proportion of total debt (long term and short term borrowings) has

reduced in 2016 in relation to the portion of equity. It shows that firm had relied more on

equity financing in 2016 to make investments in assets. Debt is generally considered as a

burden on the company by the investors and hence high level of debt discourages them to

invest in the company. With the reduced debt equity ratio, the financial leverage of the

company had lowered down in 2016 as compared to 2015.

Talk-Talk Group: The ideal debt equity ratio is less than one but the ratio of 3.07 and 2.07

shows that the company was highly levered in both the years due to excessive reliance on

debt sources of financing (Talk-Talk Group, 2016).

Inter firm Analysis:

Talk-Talk had faced high risk of insolvency as it had overburdened itself with huge portions

of debt in its overall capital structure. However, Vodafone had the potential of attracting

more investors because of its lower debt obligations.

Debt Ratio

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Debt

Ratio 0.50 0.45 0.85 0.80

2016 2015 2016 2015

Debt

Equity 0.69 0.81 3.07 2.07

Intra-firm analysis:

Vodafone: The debt equity ratio of the company has reduced in 2016 as compared to that of

2015 which shows that the proportion of total debt (long term and short term borrowings) has

reduced in 2016 in relation to the portion of equity. It shows that firm had relied more on

equity financing in 2016 to make investments in assets. Debt is generally considered as a

burden on the company by the investors and hence high level of debt discourages them to

invest in the company. With the reduced debt equity ratio, the financial leverage of the

company had lowered down in 2016 as compared to 2015.

Talk-Talk Group: The ideal debt equity ratio is less than one but the ratio of 3.07 and 2.07

shows that the company was highly levered in both the years due to excessive reliance on

debt sources of financing (Talk-Talk Group, 2016).

Inter firm Analysis:

Talk-Talk had faced high risk of insolvency as it had overburdened itself with huge portions

of debt in its overall capital structure. However, Vodafone had the potential of attracting

more investors because of its lower debt obligations.

Debt Ratio

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

Debt

Ratio 0.50 0.45 0.85 0.80

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Financial and Auditing Studies

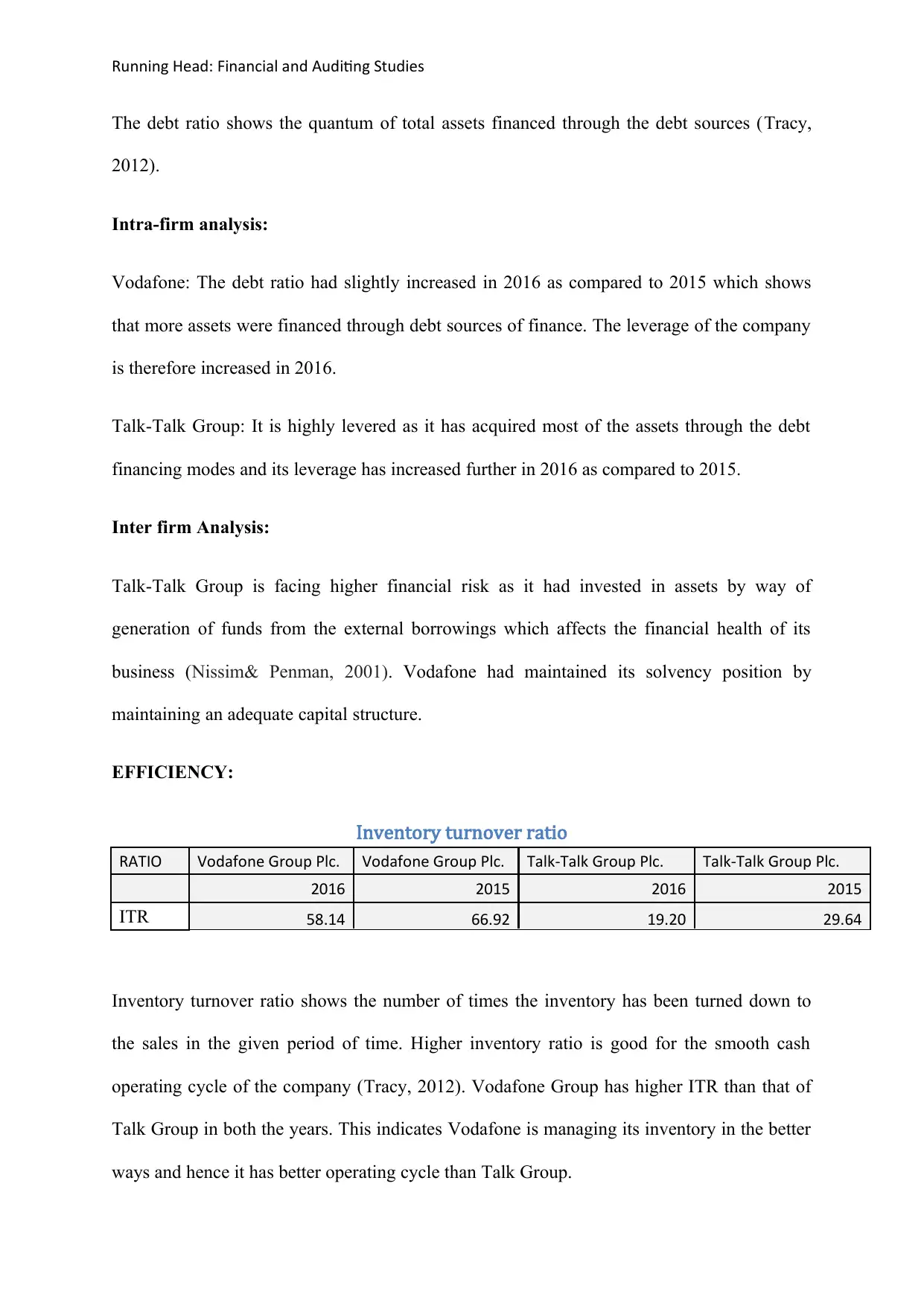

The debt ratio shows the quantum of total assets financed through the debt sources (Tracy,

2012).

Intra-firm analysis:

Vodafone: The debt ratio had slightly increased in 2016 as compared to 2015 which shows

that more assets were financed through debt sources of finance. The leverage of the company

is therefore increased in 2016.

Talk-Talk Group: It is highly levered as it has acquired most of the assets through the debt

financing modes and its leverage has increased further in 2016 as compared to 2015.

Inter firm Analysis:

Talk-Talk Group is facing higher financial risk as it had invested in assets by way of

generation of funds from the external borrowings which affects the financial health of its

business (Nissim& Penman, 2001). Vodafone had maintained its solvency position by

maintaining an adequate capital structure.

EFFICIENCY:

Inventory turnover ratio

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

ITR 58.14 66.92 19.20 29.64

Inventory turnover ratio shows the number of times the inventory has been turned down to

the sales in the given period of time. Higher inventory ratio is good for the smooth cash

operating cycle of the company (Tracy, 2012). Vodafone Group has higher ITR than that of

Talk Group in both the years. This indicates Vodafone is managing its inventory in the better

ways and hence it has better operating cycle than Talk Group.

The debt ratio shows the quantum of total assets financed through the debt sources (Tracy,

2012).

Intra-firm analysis:

Vodafone: The debt ratio had slightly increased in 2016 as compared to 2015 which shows

that more assets were financed through debt sources of finance. The leverage of the company

is therefore increased in 2016.

Talk-Talk Group: It is highly levered as it has acquired most of the assets through the debt

financing modes and its leverage has increased further in 2016 as compared to 2015.

Inter firm Analysis:

Talk-Talk Group is facing higher financial risk as it had invested in assets by way of

generation of funds from the external borrowings which affects the financial health of its

business (Nissim& Penman, 2001). Vodafone had maintained its solvency position by

maintaining an adequate capital structure.

EFFICIENCY:

Inventory turnover ratio

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

ITR 58.14 66.92 19.20 29.64

Inventory turnover ratio shows the number of times the inventory has been turned down to

the sales in the given period of time. Higher inventory ratio is good for the smooth cash

operating cycle of the company (Tracy, 2012). Vodafone Group has higher ITR than that of

Talk Group in both the years. This indicates Vodafone is managing its inventory in the better

ways and hence it has better operating cycle than Talk Group.

Running Head: Financial and Auditing Studies

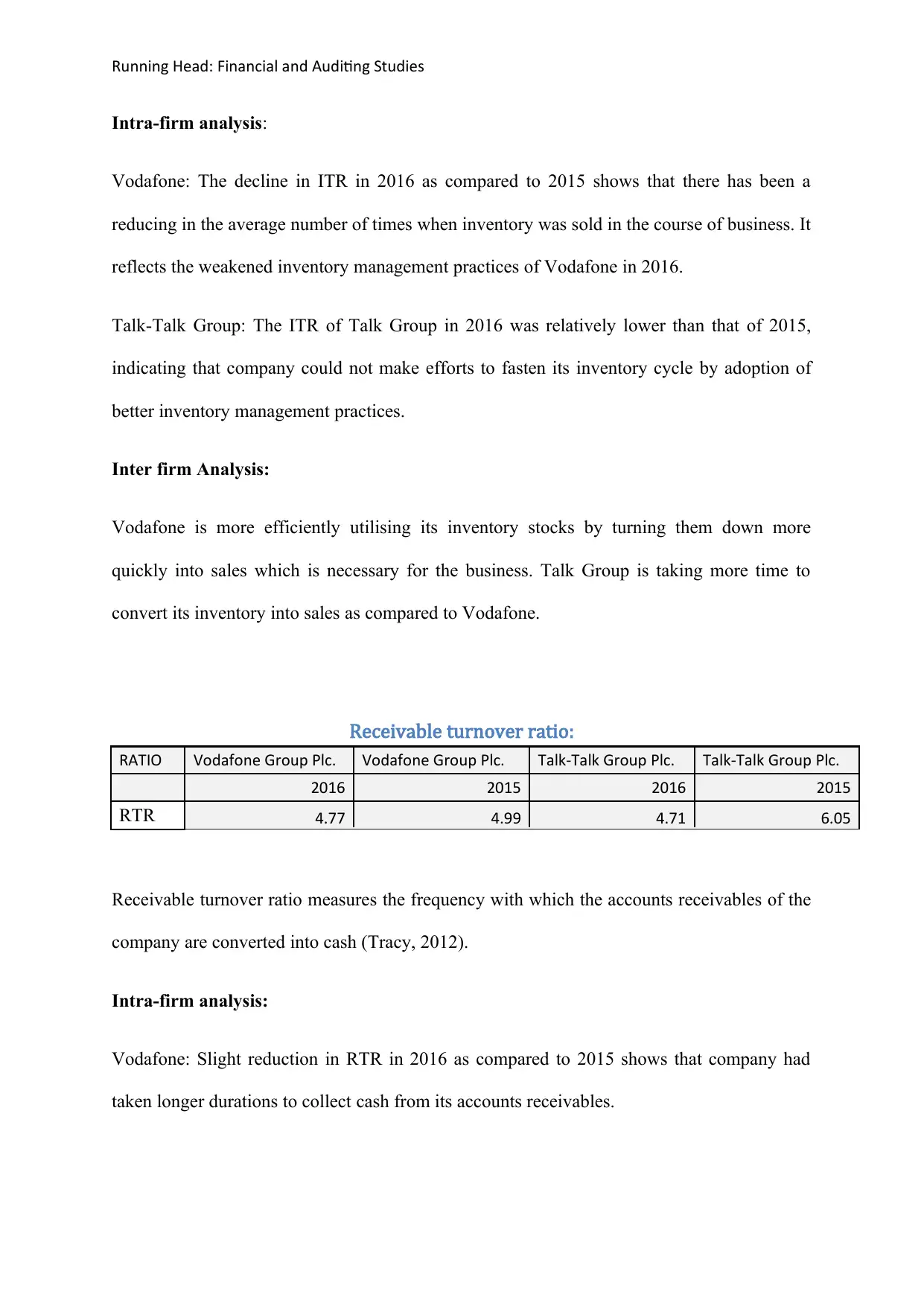

Intra-firm analysis:

Vodafone: The decline in ITR in 2016 as compared to 2015 shows that there has been a

reducing in the average number of times when inventory was sold in the course of business. It

reflects the weakened inventory management practices of Vodafone in 2016.

Talk-Talk Group: The ITR of Talk Group in 2016 was relatively lower than that of 2015,

indicating that company could not make efforts to fasten its inventory cycle by adoption of

better inventory management practices.

Inter firm Analysis:

Vodafone is more efficiently utilising its inventory stocks by turning them down more

quickly into sales which is necessary for the business. Talk Group is taking more time to

convert its inventory into sales as compared to Vodafone.

Receivable turnover ratio:

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

RTR 4.77 4.99 4.71 6.05

Receivable turnover ratio measures the frequency with which the accounts receivables of the

company are converted into cash (Tracy, 2012).

Intra-firm analysis:

Vodafone: Slight reduction in RTR in 2016 as compared to 2015 shows that company had

taken longer durations to collect cash from its accounts receivables.

Intra-firm analysis:

Vodafone: The decline in ITR in 2016 as compared to 2015 shows that there has been a

reducing in the average number of times when inventory was sold in the course of business. It

reflects the weakened inventory management practices of Vodafone in 2016.

Talk-Talk Group: The ITR of Talk Group in 2016 was relatively lower than that of 2015,

indicating that company could not make efforts to fasten its inventory cycle by adoption of

better inventory management practices.

Inter firm Analysis:

Vodafone is more efficiently utilising its inventory stocks by turning them down more

quickly into sales which is necessary for the business. Talk Group is taking more time to

convert its inventory into sales as compared to Vodafone.

Receivable turnover ratio:

RATIO Vodafone Group Plc. Vodafone Group Plc. Talk-Talk Group Plc. Talk-Talk Group Plc.

2016 2015 2016 2015

RTR 4.77 4.99 4.71 6.05

Receivable turnover ratio measures the frequency with which the accounts receivables of the

company are converted into cash (Tracy, 2012).

Intra-firm analysis:

Vodafone: Slight reduction in RTR in 2016 as compared to 2015 shows that company had

taken longer durations to collect cash from its accounts receivables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.