Financial Strategies and Analysis for Volkswagen Expansion Project

VerifiedAdded on 2020/01/23

|17

|4502

|64

Report

AI Summary

This report provides a comprehensive financial analysis of Volkswagen, focusing on the company's strategies for expansion and investment. It begins by exploring both internal and external sources of finance, such as equity issues, debt financing, and retained earnings, evaluating their implications and associated costs. The report then assesses the suitability of different financing options for Volkswagen, recommending a combination of equity finance and bank overdrafts. It delves into the importance of financial planning and the information needs of various decision-makers, including management, shareholders, and financial institutions. The report further examines the impact of finance on financial statements, including the income statement, position statement, and cash flow statement. It then analyzes budgets to make viable business decisions, including unit cost calculations and pricing strategies, with examples of markups and return on capital employed. Investment appraisal techniques, such as NPV and ARR, are used to assess project viability, and the report concludes with a comparison of financial statement formats and the interpretation of financial statements through ratio analysis, using Volkswagen's financial data as a case study.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Internal and external sources of finance......................................................................................3

Implications of different financial sources..................................................................................4

Evaluation of suitable source of finance for the business project................................................4

Analysis of cost of different sources of finance..........................................................................5

Importance of financial planning.................................................................................................5

Information requirements of different decision makers..............................................................5

Impact of finance on different financial statements.....................................................................6

Task 2...............................................................................................................................................7

Analysis of budgets in order to make viable decisions for business...........................................7

Explanation of computation of unit cost and making pricing decision using relevant

information...................................................................................................................................8

Assessment of viability of project by making use of investment appraisal techniques...............8

Comparison of suitable format of financial statements for different types of business

organization...............................................................................................................................11

Financial statement of company................................................................................................12

Interpretation of financial statement by making use of ratio analysis ......................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Internal and external sources of finance......................................................................................3

Implications of different financial sources..................................................................................4

Evaluation of suitable source of finance for the business project................................................4

Analysis of cost of different sources of finance..........................................................................5

Importance of financial planning.................................................................................................5

Information requirements of different decision makers..............................................................5

Impact of finance on different financial statements.....................................................................6

Task 2...............................................................................................................................................7

Analysis of budgets in order to make viable decisions for business...........................................7

Explanation of computation of unit cost and making pricing decision using relevant

information...................................................................................................................................8

Assessment of viability of project by making use of investment appraisal techniques...............8

Comparison of suitable format of financial statements for different types of business

organization...............................................................................................................................11

Financial statement of company................................................................................................12

Interpretation of financial statement by making use of ratio analysis ......................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

2

INDEX OF TABLES

Table 1: Cash budget (in £'000).......................................................................................................8

Table 2: Calculation of Mark up on cost price (in £'000)................................................................9

Table 3: Calculation of Price by considering return on capital employed (in £'000)......................9

Table 4: Information of available projects.....................................................................................10

Table 5: NPV of project A ............................................................................................................10

Table 6: NPV of project B.............................................................................................................10

Table 7: ARR of option 1...............................................................................................................11

Table 8: Statement showing cumulative inflow of project A........................................................12

Table 9: Statement showing cumulative inflow of Project B........................................................12

Table 10: Computation of financial ratios of Volkswagen Plc......................................................13

3

Table 1: Cash budget (in £'000).......................................................................................................8

Table 2: Calculation of Mark up on cost price (in £'000)................................................................9

Table 3: Calculation of Price by considering return on capital employed (in £'000)......................9

Table 4: Information of available projects.....................................................................................10

Table 5: NPV of project A ............................................................................................................10

Table 6: NPV of project B.............................................................................................................10

Table 7: ARR of option 1...............................................................................................................11

Table 8: Statement showing cumulative inflow of project A........................................................12

Table 9: Statement showing cumulative inflow of Project B........................................................12

Table 10: Computation of financial ratios of Volkswagen Plc......................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial sources are crucial for business entity thus organizations are required to make

optimum utilization of available resources. For this aspect, they are required make suitable

business decisions by making use of appropriable financial tools. Present project report is

focused on evaluation of financial tools that can be used by management of business in order to

make effective financial decisions (Stendardi and O’Reilly, 2006). Present study will include

description of sources of finance along with its impact and financial cost. Further description will

be provided regarding financial techniques such as unit pricing, budgeting, investment appraisal

techniques and ratio analysis in order to make better decisions. For understanding of practical

approach Volkswagen has been considered.

TASK 1

Internal and external sources of finance

Management of Volkswagen is planning for expansion for the launch of new car in the

market. For this aspect, company can generate funds from following sources:

External sources of finance Equity issue: Company can issue part of their authorized capital to generate funds for

their business project. For this financial source company will be required to pay dividend

that is part of the profit to the shareholders (Nickels, McHugh and McHugh, 2011). In

addition to this, shareholders will also have right to participate in decision making of

business. Debt finance: Management of Volkswagen can also take loan from the banking and

financial institutions. For this financial source, they will be required to pay interest

charges in regular time interval (McKinney, 2015). Further, as per their contractual deed

they will be liable for the repayment of principal amount. Bank overdraft- For the fulfilment of capital requirements company can use service of

bank overdraft. In accordance with this financial source company can make payment to

the trade payable in excess to the available balance. For this service, bank will charge

interest rate from the customer.

Internal sources of finance

4

Financial sources are crucial for business entity thus organizations are required to make

optimum utilization of available resources. For this aspect, they are required make suitable

business decisions by making use of appropriable financial tools. Present project report is

focused on evaluation of financial tools that can be used by management of business in order to

make effective financial decisions (Stendardi and O’Reilly, 2006). Present study will include

description of sources of finance along with its impact and financial cost. Further description will

be provided regarding financial techniques such as unit pricing, budgeting, investment appraisal

techniques and ratio analysis in order to make better decisions. For understanding of practical

approach Volkswagen has been considered.

TASK 1

Internal and external sources of finance

Management of Volkswagen is planning for expansion for the launch of new car in the

market. For this aspect, company can generate funds from following sources:

External sources of finance Equity issue: Company can issue part of their authorized capital to generate funds for

their business project. For this financial source company will be required to pay dividend

that is part of the profit to the shareholders (Nickels, McHugh and McHugh, 2011). In

addition to this, shareholders will also have right to participate in decision making of

business. Debt finance: Management of Volkswagen can also take loan from the banking and

financial institutions. For this financial source, they will be required to pay interest

charges in regular time interval (McKinney, 2015). Further, as per their contractual deed

they will be liable for the repayment of principal amount. Bank overdraft- For the fulfilment of capital requirements company can use service of

bank overdraft. In accordance with this financial source company can make payment to

the trade payable in excess to the available balance. For this service, bank will charge

interest rate from the customer.

Internal sources of finance

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Retained earnings- In order to generate funds for the business project, company can make

use of their previous profits. Retained earning can be defined as accumulated profits

which are not used by the company (Galloway and Deakins, 2012). However, this

financial source is available up to limited extend.

Sale of assets- Company can also sell their assets which are not providing economic

benefit to them. This financial source will also make reduction in cost of maintenance

and repairs of non-economical machines (Rao, 2003). Instead of sales, company has also

option for the lease of equipment.

Implications of different financial sources

Implication of external source of finance

External financial sources can be availed by the payment of financial cost. These sources

make reduction in profitability of business. It is because; in debt financial source company has to

pay interest which reduces net profit while in equity net profit is distributed which makes

reduction in availability of retained earnings. For debt finance, company has to provide security

of assets and in addition to this their obligations is also increased (Helfert, 2004). In equity

sources, company is not obliged for the capital payment but this sources make alteration in

controlling power of the business. It is because; equity shareholders have right to participate in

decision making of business.

Implication of internal source of finance

Internal financial sources are generally comprises of opportunity cost instead of financial

cost. Further, these source also affect liquidity position of the business as it makes increase in

current obligations. These sources are available up to limited extend thus it can only satisfy short

term requirements of business (Jury, 2012). Use of retained earnings will make reduction in

reserve and surplus due to which risk will be increased in the future contingencies. For bank

overdraft, company will be required to bank charges. It is kind of interest for short term loan

however rate of interest of this source is generally higher than other loans.

Evaluation of suitable source of finance for the business project

In accordance with the description of financial sources, it will be suitable for company to

select equity finance and facility of bank overdraft. Equity financial source is suitable for

company because it does not impose obligation of payment of principal amount. It is because;

5

use of their previous profits. Retained earning can be defined as accumulated profits

which are not used by the company (Galloway and Deakins, 2012). However, this

financial source is available up to limited extend.

Sale of assets- Company can also sell their assets which are not providing economic

benefit to them. This financial source will also make reduction in cost of maintenance

and repairs of non-economical machines (Rao, 2003). Instead of sales, company has also

option for the lease of equipment.

Implications of different financial sources

Implication of external source of finance

External financial sources can be availed by the payment of financial cost. These sources

make reduction in profitability of business. It is because; in debt financial source company has to

pay interest which reduces net profit while in equity net profit is distributed which makes

reduction in availability of retained earnings. For debt finance, company has to provide security

of assets and in addition to this their obligations is also increased (Helfert, 2004). In equity

sources, company is not obliged for the capital payment but this sources make alteration in

controlling power of the business. It is because; equity shareholders have right to participate in

decision making of business.

Implication of internal source of finance

Internal financial sources are generally comprises of opportunity cost instead of financial

cost. Further, these source also affect liquidity position of the business as it makes increase in

current obligations. These sources are available up to limited extend thus it can only satisfy short

term requirements of business (Jury, 2012). Use of retained earnings will make reduction in

reserve and surplus due to which risk will be increased in the future contingencies. For bank

overdraft, company will be required to bank charges. It is kind of interest for short term loan

however rate of interest of this source is generally higher than other loans.

Evaluation of suitable source of finance for the business project

In accordance with the description of financial sources, it will be suitable for company to

select equity finance and facility of bank overdraft. Equity financial source is suitable for

company because it does not impose obligation of payment of principal amount. It is because;

5

equity shareholders are paid at the time of wind up of company (Nofsinger and Varma, 2005).

Further, financial cost of this source is fluctuated as per the availability of profits with the

business. With the facility of bank overdraft, management of Volkswagen can satisfy their

working capital requirements in proper manner.

Analysis of cost of different sources of finance

Cost of external financial sources

For debt finance company is obliged to make payment of interest in regular time period.

Interest is charged at the fixed percentage depending on the terms and conditions of the loan.

Further, company will also be liable to make repayment of the principal amount for the discharge

of obligation. In equity source, company is required to pay dividend i.e. portion of profit to the

shareholders (Newberry and Pallot, 2005). This financial cost is not fixed in nature as it

fluctuates with the availability of profit. There is not obligation for the repayment of principal

amount. For bank overdraft company will be required to pay bank charges.

Cost of internal financial sources

Retained earnings and sales of assets do not include financial cost. However, for the

utilization of this source, company has to sacrifice the opportunity of best second alternative.

Further, profit expected from second best alternative is considered as opportunity cost of that

option.

Importance of financial planning

Financial planning can be defined as strategies developed by business organization in

order to achieve their aims and objectives in an effective manner. In the success of business,

financial planning plays vital role. By appropriable financial planning, organization can make

use of business resources in an optimum manner in order to enhance their profitability

(Broadbent and Cullen, 2012). Further, they can manage inflow and outflow of cash to maintain

proper liquidity. In addition to this, they can satisfy their working capital requirements in a

proper manner to avail business opportunities.

Information requirements of different decision makers

Information of business is required by various parties in order to make viable decisions

for the business. Description of needs of these parties is enumerated below:

6

Further, financial cost of this source is fluctuated as per the availability of profits with the

business. With the facility of bank overdraft, management of Volkswagen can satisfy their

working capital requirements in proper manner.

Analysis of cost of different sources of finance

Cost of external financial sources

For debt finance company is obliged to make payment of interest in regular time period.

Interest is charged at the fixed percentage depending on the terms and conditions of the loan.

Further, company will also be liable to make repayment of the principal amount for the discharge

of obligation. In equity source, company is required to pay dividend i.e. portion of profit to the

shareholders (Newberry and Pallot, 2005). This financial cost is not fixed in nature as it

fluctuates with the availability of profit. There is not obligation for the repayment of principal

amount. For bank overdraft company will be required to pay bank charges.

Cost of internal financial sources

Retained earnings and sales of assets do not include financial cost. However, for the

utilization of this source, company has to sacrifice the opportunity of best second alternative.

Further, profit expected from second best alternative is considered as opportunity cost of that

option.

Importance of financial planning

Financial planning can be defined as strategies developed by business organization in

order to achieve their aims and objectives in an effective manner. In the success of business,

financial planning plays vital role. By appropriable financial planning, organization can make

use of business resources in an optimum manner in order to enhance their profitability

(Broadbent and Cullen, 2012). Further, they can manage inflow and outflow of cash to maintain

proper liquidity. In addition to this, they can satisfy their working capital requirements in a

proper manner to avail business opportunities.

Information requirements of different decision makers

Information of business is required by various parties in order to make viable decisions

for the business. Description of needs of these parties is enumerated below:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management- Management requires information of business in order to make future

strategies in order to attain aims and objectives in an effective manner. Decision

regarding future operational activities are taken on the basis of past commercial activities. Shareholders- For the decision of reinvestment or divestment, shareholders require

information of business (Dyson, 2003). By considering information of business they

compare desired and actual return and make decision regarding future investment

strategies. Employees- Human resources of the business requires information to assess the potential

opportunities for growth to them. For this aspect, they consider growth, profitability and

future activities of business. Financial institutions- For the assessment of liquidity and solvency of business financial

institutions requires financial statements. By considering this information, they determine

capability of business in repayment of loan.

Government- Government requires business information in order to assure that tax

obligation is accomplished by management in proper manner (Cox and Fardon, 2003).

Further, by this information they also assess that operational activities are conducted in

an ethical manner.

Impact of finance on different financial statements

Impact of finance on different financial statements is enumerated below:

Income statement

Financial sources attracts financial cost which is recorded to the debit side of the income

statement. Due to this aspect, profitability of business is reduced as expenses side is increased.

Debt finance and bank overdraft attracts interest cost while equity finance attracts cost of

dividend.

Position statement

Both asset and liability side of the position statement is affected by the generation of

funds from the financial sources. It is because, debt increases non current obligations and equity

make increase in shareholders funds (Hopwood, Unerman and Fries, 2010). Further,

simultaneous effect is provided to the cash and cash equivalents.

Cash flow statement

7

strategies in order to attain aims and objectives in an effective manner. Decision

regarding future operational activities are taken on the basis of past commercial activities. Shareholders- For the decision of reinvestment or divestment, shareholders require

information of business (Dyson, 2003). By considering information of business they

compare desired and actual return and make decision regarding future investment

strategies. Employees- Human resources of the business requires information to assess the potential

opportunities for growth to them. For this aspect, they consider growth, profitability and

future activities of business. Financial institutions- For the assessment of liquidity and solvency of business financial

institutions requires financial statements. By considering this information, they determine

capability of business in repayment of loan.

Government- Government requires business information in order to assure that tax

obligation is accomplished by management in proper manner (Cox and Fardon, 2003).

Further, by this information they also assess that operational activities are conducted in

an ethical manner.

Impact of finance on different financial statements

Impact of finance on different financial statements is enumerated below:

Income statement

Financial sources attracts financial cost which is recorded to the debit side of the income

statement. Due to this aspect, profitability of business is reduced as expenses side is increased.

Debt finance and bank overdraft attracts interest cost while equity finance attracts cost of

dividend.

Position statement

Both asset and liability side of the position statement is affected by the generation of

funds from the financial sources. It is because, debt increases non current obligations and equity

make increase in shareholders funds (Hopwood, Unerman and Fries, 2010). Further,

simultaneous effect is provided to the cash and cash equivalents.

Cash flow statement

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

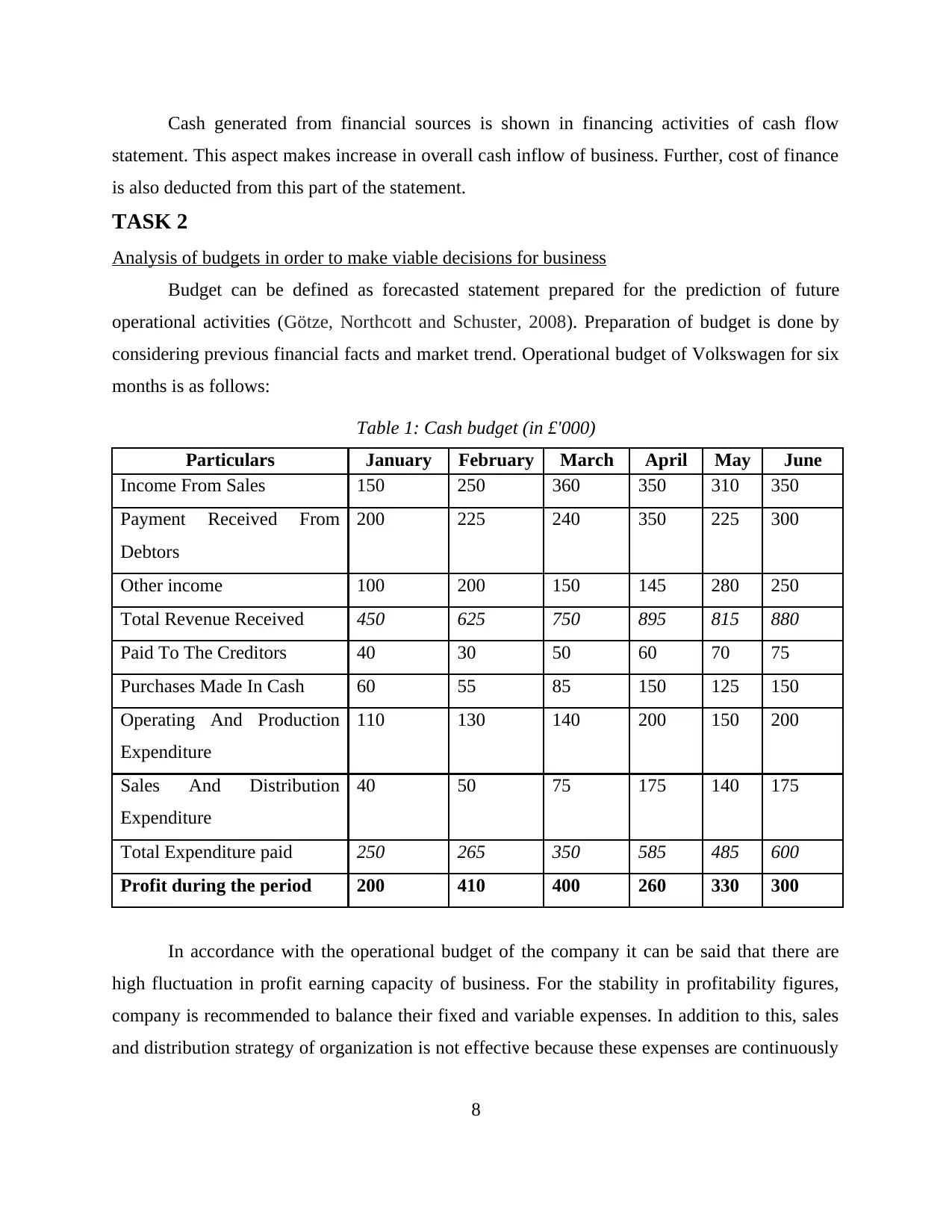

Cash generated from financial sources is shown in financing activities of cash flow

statement. This aspect makes increase in overall cash inflow of business. Further, cost of finance

is also deducted from this part of the statement.

TASK 2

Analysis of budgets in order to make viable decisions for business

Budget can be defined as forecasted statement prepared for the prediction of future

operational activities (Götze, Northcott and Schuster, 2008). Preparation of budget is done by

considering previous financial facts and market trend. Operational budget of Volkswagen for six

months is as follows:

Table 1: Cash budget (in £'000)

Particulars January February March April May June

Income From Sales 150 250 360 350 310 350

Payment Received From

Debtors

200 225 240 350 225 300

Other income 100 200 150 145 280 250

Total Revenue Received 450 625 750 895 815 880

Paid To The Creditors 40 30 50 60 70 75

Purchases Made In Cash 60 55 85 150 125 150

Operating And Production

Expenditure

110 130 140 200 150 200

Sales And Distribution

Expenditure

40 50 75 175 140 175

Total Expenditure paid 250 265 350 585 485 600

Profit during the period 200 410 400 260 330 300

In accordance with the operational budget of the company it can be said that there are

high fluctuation in profit earning capacity of business. For the stability in profitability figures,

company is recommended to balance their fixed and variable expenses. In addition to this, sales

and distribution strategy of organization is not effective because these expenses are continuously

8

statement. This aspect makes increase in overall cash inflow of business. Further, cost of finance

is also deducted from this part of the statement.

TASK 2

Analysis of budgets in order to make viable decisions for business

Budget can be defined as forecasted statement prepared for the prediction of future

operational activities (Götze, Northcott and Schuster, 2008). Preparation of budget is done by

considering previous financial facts and market trend. Operational budget of Volkswagen for six

months is as follows:

Table 1: Cash budget (in £'000)

Particulars January February March April May June

Income From Sales 150 250 360 350 310 350

Payment Received From

Debtors

200 225 240 350 225 300

Other income 100 200 150 145 280 250

Total Revenue Received 450 625 750 895 815 880

Paid To The Creditors 40 30 50 60 70 75

Purchases Made In Cash 60 55 85 150 125 150

Operating And Production

Expenditure

110 130 140 200 150 200

Sales And Distribution

Expenditure

40 50 75 175 140 175

Total Expenditure paid 250 265 350 585 485 600

Profit during the period 200 410 400 260 330 300

In accordance with the operational budget of the company it can be said that there are

high fluctuation in profit earning capacity of business. For the stability in profitability figures,

company is recommended to balance their fixed and variable expenses. In addition to this, sales

and distribution strategy of organization is not effective because these expenses are continuously

8

increasing but same effect cannot be noticed in the value of sales. Further, this strategy is

required to be modified to earn high profits.

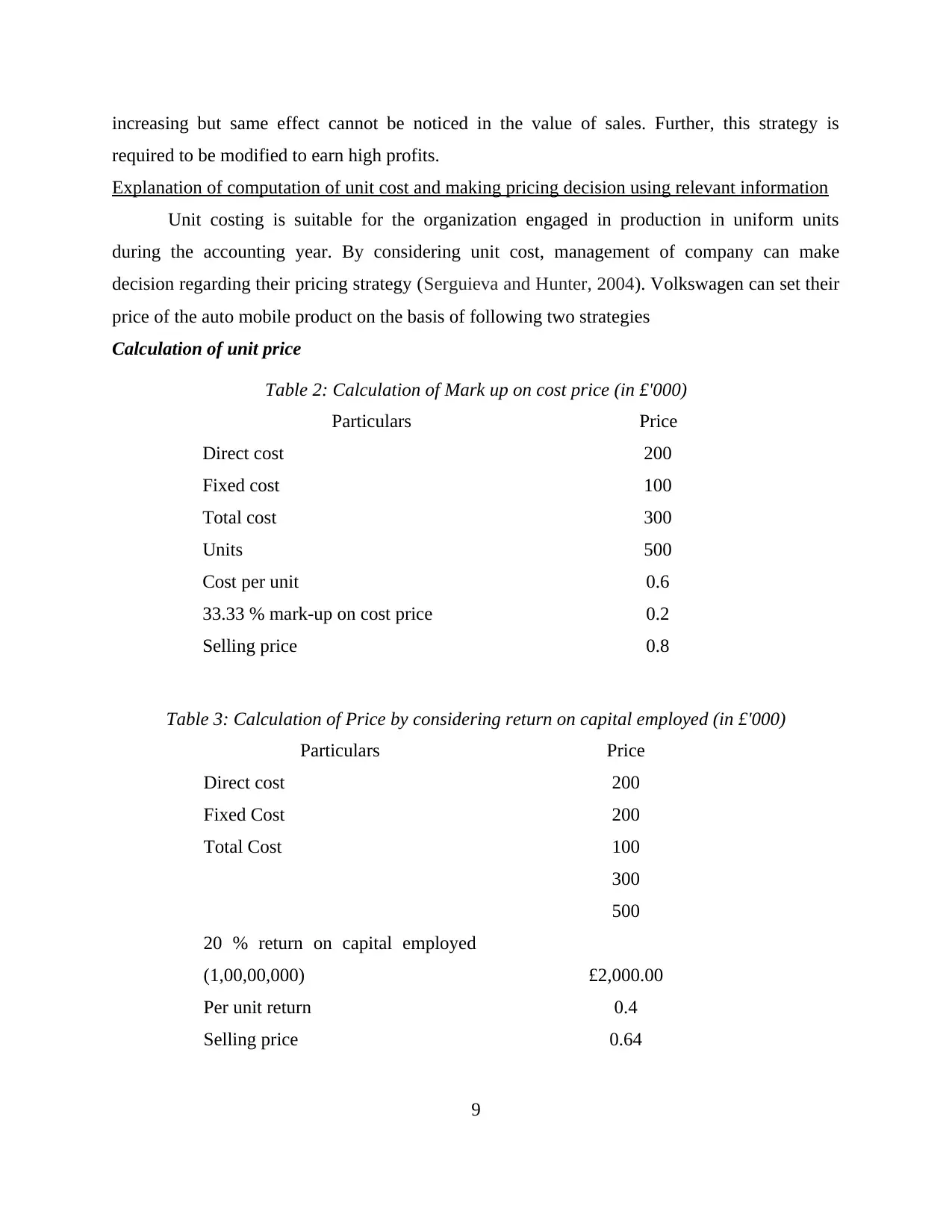

Explanation of computation of unit cost and making pricing decision using relevant information

Unit costing is suitable for the organization engaged in production in uniform units

during the accounting year. By considering unit cost, management of company can make

decision regarding their pricing strategy (Serguieva and Hunter, 2004). Volkswagen can set their

price of the auto mobile product on the basis of following two strategies

Calculation of unit price

Table 2: Calculation of Mark up on cost price (in £'000)

Particulars Price

Direct cost 200

Fixed cost 100

Total cost 300

Units 500

Cost per unit 0.6

33.33 % mark-up on cost price 0.2

Selling price 0.8

Table 3: Calculation of Price by considering return on capital employed (in £'000)

Particulars Price

Direct cost 200

Fixed Cost 200

Total Cost 100

300

500

20 % return on capital employed

(1,00,00,000) £2,000.00

Per unit return 0.4

Selling price 0.64

9

required to be modified to earn high profits.

Explanation of computation of unit cost and making pricing decision using relevant information

Unit costing is suitable for the organization engaged in production in uniform units

during the accounting year. By considering unit cost, management of company can make

decision regarding their pricing strategy (Serguieva and Hunter, 2004). Volkswagen can set their

price of the auto mobile product on the basis of following two strategies

Calculation of unit price

Table 2: Calculation of Mark up on cost price (in £'000)

Particulars Price

Direct cost 200

Fixed cost 100

Total cost 300

Units 500

Cost per unit 0.6

33.33 % mark-up on cost price 0.2

Selling price 0.8

Table 3: Calculation of Price by considering return on capital employed (in £'000)

Particulars Price

Direct cost 200

Fixed Cost 200

Total Cost 100

300

500

20 % return on capital employed

(1,00,00,000) £2,000.00

Per unit return 0.4

Selling price 0.64

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In accordance with the both techniques, it can be said that pricing from method of return

capital employed is more beneficial. It is because; it satisfies profitability requirements of

business by providing product at lower price to the customer. Due to this aspect, it is win-win

approach for both customers and the organization.

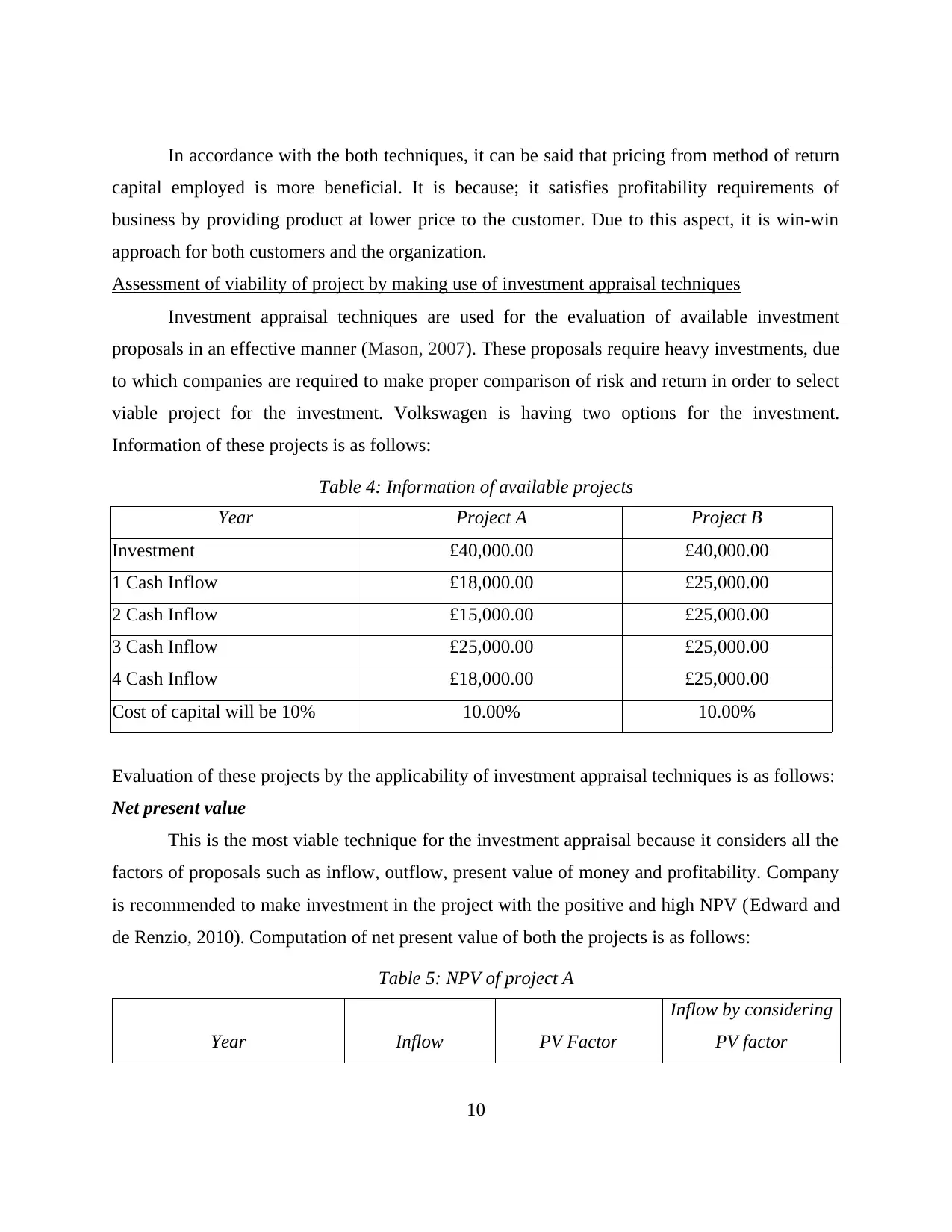

Assessment of viability of project by making use of investment appraisal techniques

Investment appraisal techniques are used for the evaluation of available investment

proposals in an effective manner (Mason, 2007). These proposals require heavy investments, due

to which companies are required to make proper comparison of risk and return in order to select

viable project for the investment. Volkswagen is having two options for the investment.

Information of these projects is as follows:

Table 4: Information of available projects

Year Project A Project B

Investment £40,000.00 £40,000.00

1 Cash Inflow £18,000.00 £25,000.00

2 Cash Inflow £15,000.00 £25,000.00

3 Cash Inflow £25,000.00 £25,000.00

4 Cash Inflow £18,000.00 £25,000.00

Cost of capital will be 10% 10.00% 10.00%

Evaluation of these projects by the applicability of investment appraisal techniques is as follows:

Net present value

This is the most viable technique for the investment appraisal because it considers all the

factors of proposals such as inflow, outflow, present value of money and profitability. Company

is recommended to make investment in the project with the positive and high NPV (Edward and

de Renzio, 2010). Computation of net present value of both the projects is as follows:

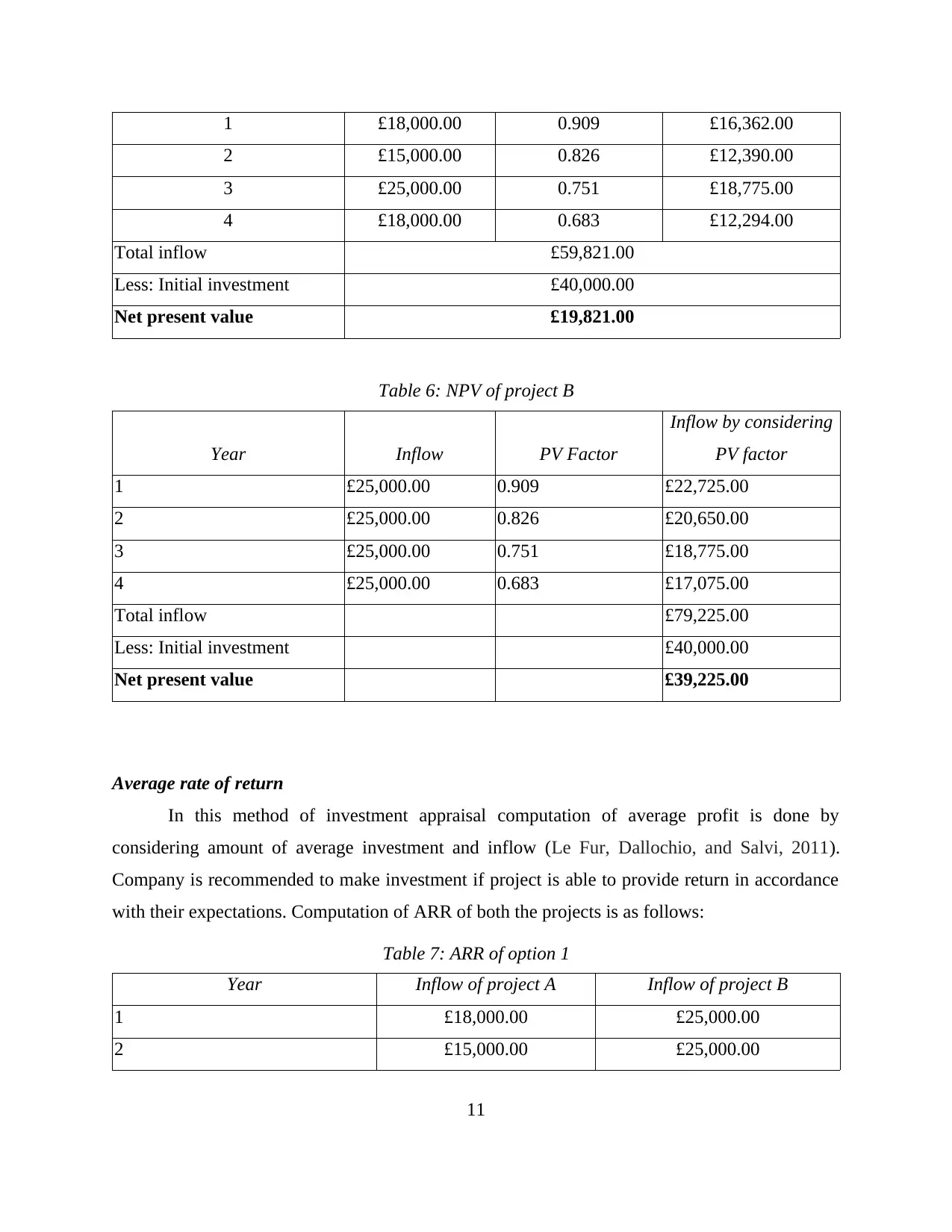

Table 5: NPV of project A

Year Inflow PV Factor

Inflow by considering

PV factor

10

capital employed is more beneficial. It is because; it satisfies profitability requirements of

business by providing product at lower price to the customer. Due to this aspect, it is win-win

approach for both customers and the organization.

Assessment of viability of project by making use of investment appraisal techniques

Investment appraisal techniques are used for the evaluation of available investment

proposals in an effective manner (Mason, 2007). These proposals require heavy investments, due

to which companies are required to make proper comparison of risk and return in order to select

viable project for the investment. Volkswagen is having two options for the investment.

Information of these projects is as follows:

Table 4: Information of available projects

Year Project A Project B

Investment £40,000.00 £40,000.00

1 Cash Inflow £18,000.00 £25,000.00

2 Cash Inflow £15,000.00 £25,000.00

3 Cash Inflow £25,000.00 £25,000.00

4 Cash Inflow £18,000.00 £25,000.00

Cost of capital will be 10% 10.00% 10.00%

Evaluation of these projects by the applicability of investment appraisal techniques is as follows:

Net present value

This is the most viable technique for the investment appraisal because it considers all the

factors of proposals such as inflow, outflow, present value of money and profitability. Company

is recommended to make investment in the project with the positive and high NPV (Edward and

de Renzio, 2010). Computation of net present value of both the projects is as follows:

Table 5: NPV of project A

Year Inflow PV Factor

Inflow by considering

PV factor

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 £18,000.00 0.909 £16,362.00

2 £15,000.00 0.826 £12,390.00

3 £25,000.00 0.751 £18,775.00

4 £18,000.00 0.683 £12,294.00

Total inflow £59,821.00

Less: Initial investment £40,000.00

Net present value £19,821.00

Table 6: NPV of project B

Year Inflow PV Factor

Inflow by considering

PV factor

1 £25,000.00 0.909 £22,725.00

2 £25,000.00 0.826 £20,650.00

3 £25,000.00 0.751 £18,775.00

4 £25,000.00 0.683 £17,075.00

Total inflow £79,225.00

Less: Initial investment £40,000.00

Net present value £39,225.00

Average rate of return

In this method of investment appraisal computation of average profit is done by

considering amount of average investment and inflow (Le Fur, Dallochio, and Salvi, 2011).

Company is recommended to make investment if project is able to provide return in accordance

with their expectations. Computation of ARR of both the projects is as follows:

Table 7: ARR of option 1

Year Inflow of project A Inflow of project B

1 £18,000.00 £25,000.00

2 £15,000.00 £25,000.00

11

2 £15,000.00 0.826 £12,390.00

3 £25,000.00 0.751 £18,775.00

4 £18,000.00 0.683 £12,294.00

Total inflow £59,821.00

Less: Initial investment £40,000.00

Net present value £19,821.00

Table 6: NPV of project B

Year Inflow PV Factor

Inflow by considering

PV factor

1 £25,000.00 0.909 £22,725.00

2 £25,000.00 0.826 £20,650.00

3 £25,000.00 0.751 £18,775.00

4 £25,000.00 0.683 £17,075.00

Total inflow £79,225.00

Less: Initial investment £40,000.00

Net present value £39,225.00

Average rate of return

In this method of investment appraisal computation of average profit is done by

considering amount of average investment and inflow (Le Fur, Dallochio, and Salvi, 2011).

Company is recommended to make investment if project is able to provide return in accordance

with their expectations. Computation of ARR of both the projects is as follows:

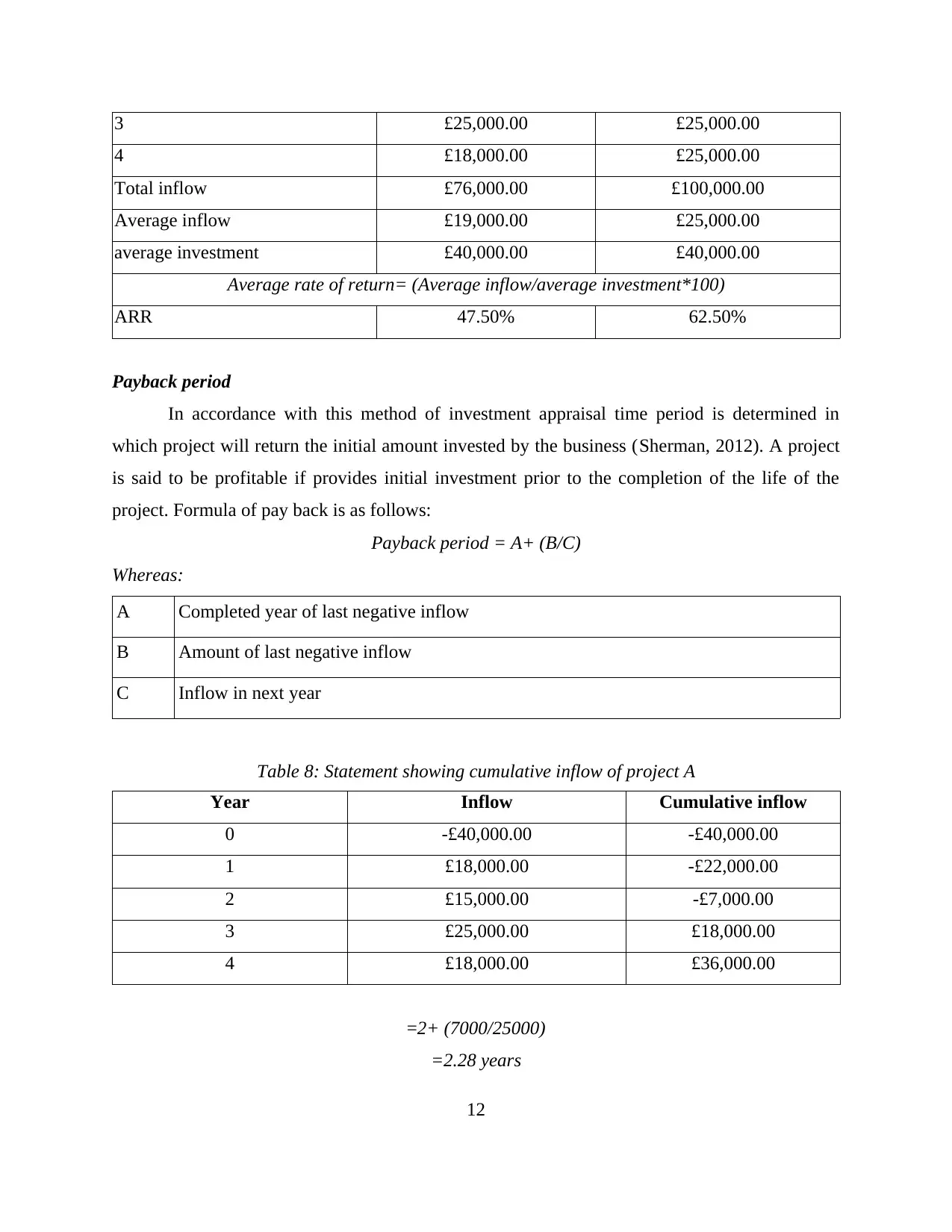

Table 7: ARR of option 1

Year Inflow of project A Inflow of project B

1 £18,000.00 £25,000.00

2 £15,000.00 £25,000.00

11

3 £25,000.00 £25,000.00

4 £18,000.00 £25,000.00

Total inflow £76,000.00 £100,000.00

Average inflow £19,000.00 £25,000.00

average investment £40,000.00 £40,000.00

Average rate of return= (Average inflow/average investment*100)

ARR 47.50% 62.50%

Payback period

In accordance with this method of investment appraisal time period is determined in

which project will return the initial amount invested by the business (Sherman, 2012). A project

is said to be profitable if provides initial investment prior to the completion of the life of the

project. Formula of pay back is as follows:

Payback period = A+ (B/C)

Whereas:

A Completed year of last negative inflow

B Amount of last negative inflow

C Inflow in next year

Table 8: Statement showing cumulative inflow of project A

Year Inflow Cumulative inflow

0 -£40,000.00 -£40,000.00

1 £18,000.00 -£22,000.00

2 £15,000.00 -£7,000.00

3 £25,000.00 £18,000.00

4 £18,000.00 £36,000.00

=2+ (7000/25000)

=2.28 years

12

4 £18,000.00 £25,000.00

Total inflow £76,000.00 £100,000.00

Average inflow £19,000.00 £25,000.00

average investment £40,000.00 £40,000.00

Average rate of return= (Average inflow/average investment*100)

ARR 47.50% 62.50%

Payback period

In accordance with this method of investment appraisal time period is determined in

which project will return the initial amount invested by the business (Sherman, 2012). A project

is said to be profitable if provides initial investment prior to the completion of the life of the

project. Formula of pay back is as follows:

Payback period = A+ (B/C)

Whereas:

A Completed year of last negative inflow

B Amount of last negative inflow

C Inflow in next year

Table 8: Statement showing cumulative inflow of project A

Year Inflow Cumulative inflow

0 -£40,000.00 -£40,000.00

1 £18,000.00 -£22,000.00

2 £15,000.00 -£7,000.00

3 £25,000.00 £18,000.00

4 £18,000.00 £36,000.00

=2+ (7000/25000)

=2.28 years

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.