Financial Statement Analysis of Volkswagen Group: A Detailed Report

VerifiedAdded on 2019/12/03

|19

|4451

|375

Report

AI Summary

This report provides a comprehensive financial statement analysis of the Volkswagen Group, a leading German automobile manufacturer. The analysis employs ratio analysis, including profitability, liquidity, activity, and solvency ratios, to evaluate the company's financial performance from 2012 to 2014. The report examines key financial indicators such as gross profit ratio, net profit ratio, current ratio, debt-equity ratio, and asset turnover ratio. Furthermore, the study investigates the impact of internal and external factors on the business and includes a comparative analysis with Daimler Co. Ltd, a major competitor. The report concludes with recommendations for the company's shareholders based on the findings of the financial analysis, highlighting areas of concern and opportunities for improvement. The report aims to provide a detailed understanding of Volkswagen's financial health and strategic position within the automotive industry.

Financial statement analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

Approaches to analyze the financial statement of the company............................................1

Ratio Analysis for Volkswagen group...................................................................................3

Impact of internal and external factors on the business.........................................................7

Comparative study of Financial statement analysis of Volkswagen with Daimler Co. Ltd.. 8

Recommendation to the shareholders of the company........................................................11

REFERENCES.........................................................................................................................13

INTRODUCTION......................................................................................................................1

Approaches to analyze the financial statement of the company............................................1

Ratio Analysis for Volkswagen group...................................................................................3

Impact of internal and external factors on the business.........................................................7

Comparative study of Financial statement analysis of Volkswagen with Daimler Co. Ltd.. 8

Recommendation to the shareholders of the company........................................................11

REFERENCES.........................................................................................................................13

List of tables

Table 1: Ratio analysis – Volkswagen group.............................................................................3

Table 2: Ratio analysis - Daimler...............................................................................................9

List of figures

Figure 1: Profitability ratios – Volkswagen...............................................................................4

Figure 2: Debt- equity ratio – Volkswagen................................................................................5

Figure 3: Liquidity position – Volkswagen...............................................................................5

Figure 4: Comparison of net profit ratio for Volkswagen and Daimler...................................10

1 | P a g e

Table 1: Ratio analysis – Volkswagen group.............................................................................3

Table 2: Ratio analysis - Daimler...............................................................................................9

List of figures

Figure 1: Profitability ratios – Volkswagen...............................................................................4

Figure 2: Debt- equity ratio – Volkswagen................................................................................5

Figure 3: Liquidity position – Volkswagen...............................................................................5

Figure 4: Comparison of net profit ratio for Volkswagen and Daimler...................................10

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Volkswagen is a German automobile manufacturing company which was established in

the year 1937 and it is headquartered in Wolfsburg, Lower Saxony. Volkswagen AG is the

parent company of Volkswagen group whereas Audi, Skoda, Seat and Lamborghini are its

subsidiary companies. The activities of Volkswagen group falls in an automotive industry

and it was the second largest auto maker in the world in the year 2012. Presently, the

company aims at becoming the world's largest car maker by the year 2018 (Robinson and et.

al., 2015). Volkswagen group consists of two divisions; automotive division and financial

services division. The automotive division deals with production of passenger cars, light

commercial vehicles, trucks and buses and sale of genuine parts. On the other hand, the

financial services division emphasizes on dealer and customer financing, leasing, banking

and insurance activities, fleet division and mobility offerings. It is a large international

corporation in charge of multiple car and truck brands. The company conducts its

manufacturing and assembling activities in different part of the world. In the presented report,

we analyse the financial statements of Volkswagen group by adopting ratio analysis method.

On contrary, it's financial statements will also analyse with the competitor Daimler Co. Ltd.

Approaches to analyse the financial statement of the company

Financial statements are basically summary of operating, financing and investing

activities of the company. Financial statements analysis is the process of reviewing and

evaluating company's financial statement to make better economic decisions. Financial

statement analysis is an effectual device to review prosperity and reliability of financial

statement. The main aim of this analysis is to provide useful information to different users of

financial statement. It facilitates the investors and creditors to evaluate past performance and

financial status. Moreover, it helps in predicting future performance of the company (Wahlen,

Baginski and Bradshaw, 2014). There are two approaches to analyse financial statements:

traditional and modern approach. Traditional approach emphasizes on evaluating financial

data in financial statements and considers income statement as well as balance sheet. Under

this approach, ratio analysis, common size statement and comparative financial statement

analysis can be used. However, Modern approach is not only based on historical data

contained in income and balance sheet but also uses other financial statements such as cash

flow and fund flow. Under this approach, Modern statistical and mathematical tools are used

to analyse financial statements.

1 | P a g e

Volkswagen is a German automobile manufacturing company which was established in

the year 1937 and it is headquartered in Wolfsburg, Lower Saxony. Volkswagen AG is the

parent company of Volkswagen group whereas Audi, Skoda, Seat and Lamborghini are its

subsidiary companies. The activities of Volkswagen group falls in an automotive industry

and it was the second largest auto maker in the world in the year 2012. Presently, the

company aims at becoming the world's largest car maker by the year 2018 (Robinson and et.

al., 2015). Volkswagen group consists of two divisions; automotive division and financial

services division. The automotive division deals with production of passenger cars, light

commercial vehicles, trucks and buses and sale of genuine parts. On the other hand, the

financial services division emphasizes on dealer and customer financing, leasing, banking

and insurance activities, fleet division and mobility offerings. It is a large international

corporation in charge of multiple car and truck brands. The company conducts its

manufacturing and assembling activities in different part of the world. In the presented report,

we analyse the financial statements of Volkswagen group by adopting ratio analysis method.

On contrary, it's financial statements will also analyse with the competitor Daimler Co. Ltd.

Approaches to analyse the financial statement of the company

Financial statements are basically summary of operating, financing and investing

activities of the company. Financial statements analysis is the process of reviewing and

evaluating company's financial statement to make better economic decisions. Financial

statement analysis is an effectual device to review prosperity and reliability of financial

statement. The main aim of this analysis is to provide useful information to different users of

financial statement. It facilitates the investors and creditors to evaluate past performance and

financial status. Moreover, it helps in predicting future performance of the company (Wahlen,

Baginski and Bradshaw, 2014). There are two approaches to analyse financial statements:

traditional and modern approach. Traditional approach emphasizes on evaluating financial

data in financial statements and considers income statement as well as balance sheet. Under

this approach, ratio analysis, common size statement and comparative financial statement

analysis can be used. However, Modern approach is not only based on historical data

contained in income and balance sheet but also uses other financial statements such as cash

flow and fund flow. Under this approach, Modern statistical and mathematical tools are used

to analyse financial statements.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Comparative financial statements: Comparative financial statements refer to the

analysis of financial statement at different period of time. It includes comparative balance

sheet and comparative income statement (Fridson and Alvarez, 2011). Comparative balance

sheet is the study of trend of same item in two or more balance sheet on different dates. The

income statements provide results o business operations. Comparative income statements on

other hand present an idea of progress of business over period of time.

Common size financial statement: Common size financial statement displays various

items of the balance sheet as percentage by taking a common base figure. This statement

facilitates the analysis of financial statement for different time period of a company.

Fund flow statement: Fund flow statements are prepared to analyse reasons for change

in financial position of the company. It shows sources and application of funds for a

particular period (Sinha, 2012). This statement is prepared to explain the changes in working

capital position of the company.

Cash Flow statement: Cash flow statement measures the cash inflow and outflow

caused by core business operations. This type of statement reports the cash generated and it is

used for the time specified by business operating, financing and investing activities.

Ratio Analysis: Ratio describes the quantitative relationship that exists between two

numbers. Ratio analysis refers to analysis and interpretation of financial statement by

calculating various ratios (Epstein and Buhovac, 2014). It includes Activity ratio, liquidity

ratio, solvency ratio and profitability ratio.

Activity ratio: Activity ratio measures efficiency of the firm in generating revenues.

This type of ratio shows that how frequently assets are converted into cash or sales. Fast

conversion shows high sales and profits of the company. It includes inventory turnover ratio,

assets turnover ratio, working capital turnover ratio, receivable and payable turnover ratios.

Liquidity ratio: Liquidity ratio measures the adequacy of current and liquid assets.

This type of ratio evaluates company's ability to pay its short term debts. It also describes

short term solvency position and liquidity position of the organization (Drake and Fabozzi,

2012). It includes current ratio and Quick ratio.

Solvency ratio: Solvency ratio measures the ability of a company to survive for a

long period of time. This ratio evaluates the company’s ability to pay its long term debts.

Henceforth, it is also known as long term solvency ratio. It includes debt to equity ratio, time

interest ratio and proprietary ratio.

2 | P a g e

analysis of financial statement at different period of time. It includes comparative balance

sheet and comparative income statement (Fridson and Alvarez, 2011). Comparative balance

sheet is the study of trend of same item in two or more balance sheet on different dates. The

income statements provide results o business operations. Comparative income statements on

other hand present an idea of progress of business over period of time.

Common size financial statement: Common size financial statement displays various

items of the balance sheet as percentage by taking a common base figure. This statement

facilitates the analysis of financial statement for different time period of a company.

Fund flow statement: Fund flow statements are prepared to analyse reasons for change

in financial position of the company. It shows sources and application of funds for a

particular period (Sinha, 2012). This statement is prepared to explain the changes in working

capital position of the company.

Cash Flow statement: Cash flow statement measures the cash inflow and outflow

caused by core business operations. This type of statement reports the cash generated and it is

used for the time specified by business operating, financing and investing activities.

Ratio Analysis: Ratio describes the quantitative relationship that exists between two

numbers. Ratio analysis refers to analysis and interpretation of financial statement by

calculating various ratios (Epstein and Buhovac, 2014). It includes Activity ratio, liquidity

ratio, solvency ratio and profitability ratio.

Activity ratio: Activity ratio measures efficiency of the firm in generating revenues.

This type of ratio shows that how frequently assets are converted into cash or sales. Fast

conversion shows high sales and profits of the company. It includes inventory turnover ratio,

assets turnover ratio, working capital turnover ratio, receivable and payable turnover ratios.

Liquidity ratio: Liquidity ratio measures the adequacy of current and liquid assets.

This type of ratio evaluates company's ability to pay its short term debts. It also describes

short term solvency position and liquidity position of the organization (Drake and Fabozzi,

2012). It includes current ratio and Quick ratio.

Solvency ratio: Solvency ratio measures the ability of a company to survive for a

long period of time. This ratio evaluates the company’s ability to pay its long term debts.

Henceforth, it is also known as long term solvency ratio. It includes debt to equity ratio, time

interest ratio and proprietary ratio.

2 | P a g e

Profitability ratio: Profitability ratio analyzes the ability of a company to earn profit

for its owners. Profitability ratio measures the financial performance of a business. It includes

Gross profit ratio, net profit ratio and operating profit ratio.

Ratio Analysis for Volkswagen group

The financial position and performance of Volkswagen group is analysed by estimating

various ratios. The ratio analysis for Volkswagen group is presented underneath.

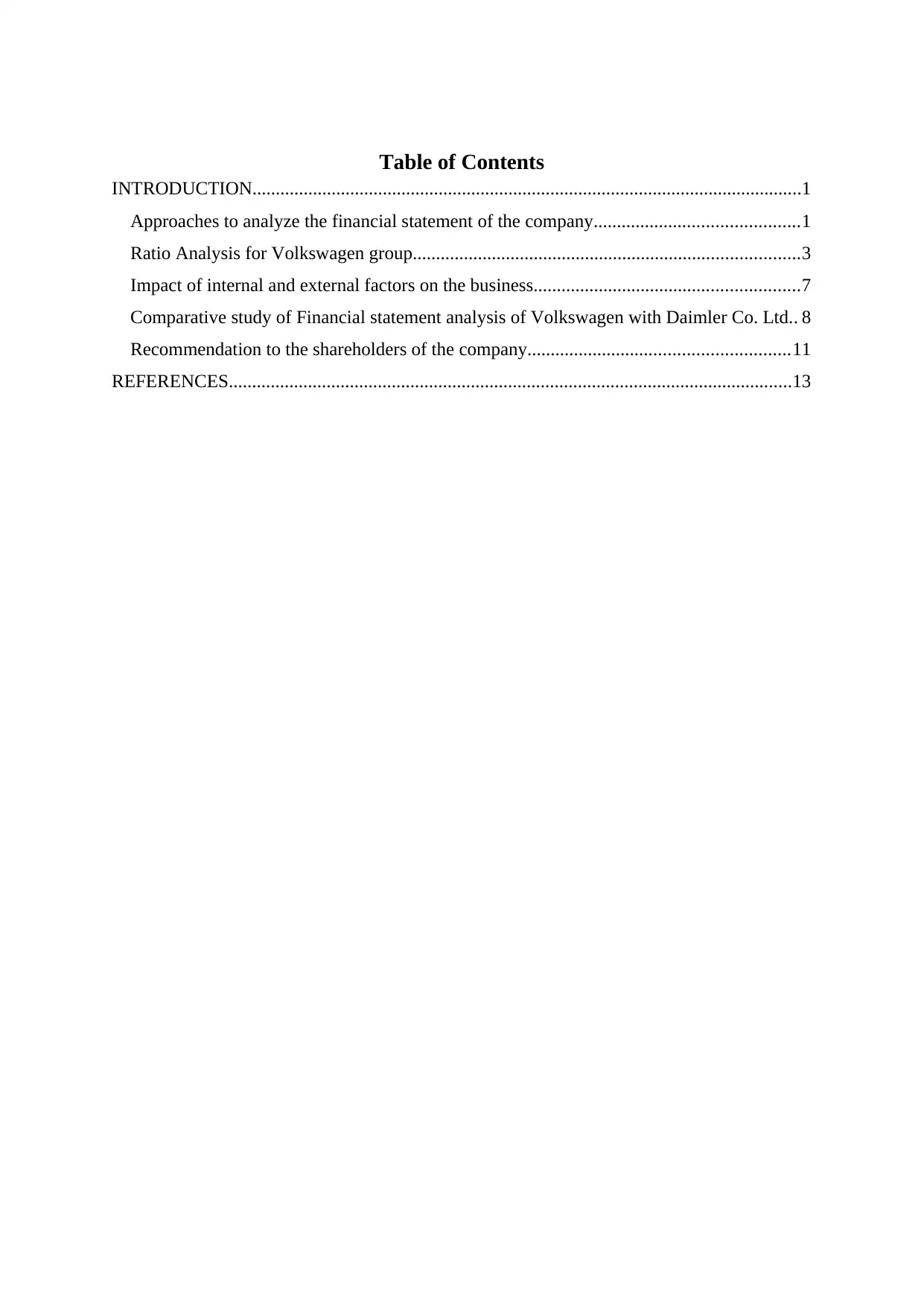

Table 1: Ratio analysis – Volkswagen group

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 36524 35600 35154

Operating profit 12697 11671 11498

Net profit 11068 9145 21881

Net Sales 202458 197007 192676

Gross Profit Ratio

(Gross Profit/ Net Sales)

*100 18.04 % 18.07 % 18.25 %

Operating Profit Ratio

(Operating Profit/ Net

Sales) *100 6.27 % 5.92 % 5.97 %

Net Profit Ratio (Net Profit/ Net Sales) *100 5.47 % 4.64 % 11.36 %

Liquidity ratios

Current Assets 131102 122192 113061

Current Liabilities 130706 118625 105526

Closing Stock 31466 28653 28674

Current Ratio

Current Assets / current

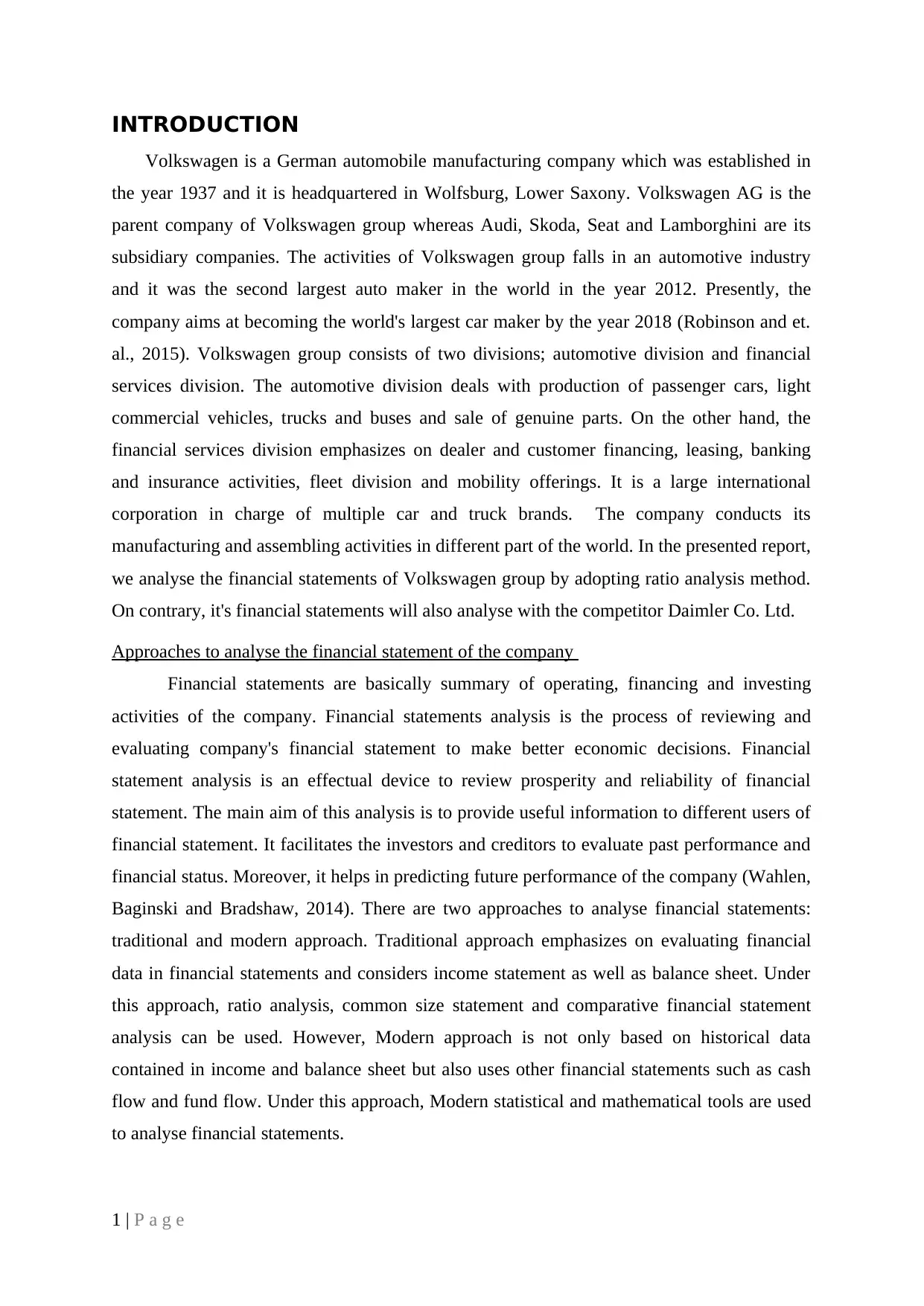

Liabilities 1.00 1.03 1.07

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.76 0.79 0.80

Activity Ratio

Net Sales 202458 197007 192676

Total Assets 351209 324333 309518

Total Assets Turnover

Ratio Net Sales/ Total Assets

0.58

times

0.61

times

0.62

times

Cost of goods sold 165934 161407 157522

3 | P a g e

for its owners. Profitability ratio measures the financial performance of a business. It includes

Gross profit ratio, net profit ratio and operating profit ratio.

Ratio Analysis for Volkswagen group

The financial position and performance of Volkswagen group is analysed by estimating

various ratios. The ratio analysis for Volkswagen group is presented underneath.

Table 1: Ratio analysis – Volkswagen group

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 36524 35600 35154

Operating profit 12697 11671 11498

Net profit 11068 9145 21881

Net Sales 202458 197007 192676

Gross Profit Ratio

(Gross Profit/ Net Sales)

*100 18.04 % 18.07 % 18.25 %

Operating Profit Ratio

(Operating Profit/ Net

Sales) *100 6.27 % 5.92 % 5.97 %

Net Profit Ratio (Net Profit/ Net Sales) *100 5.47 % 4.64 % 11.36 %

Liquidity ratios

Current Assets 131102 122192 113061

Current Liabilities 130706 118625 105526

Closing Stock 31466 28653 28674

Current Ratio

Current Assets / current

Liabilities 1.00 1.03 1.07

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.76 0.79 0.80

Activity Ratio

Net Sales 202458 197007 192676

Total Assets 351209 324333 309518

Total Assets Turnover

Ratio Net Sales/ Total Assets

0.58

times

0.61

times

0.62

times

Cost of goods sold 165934 161407 157522

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory 31466 28653 28674

Inventory Turnover ratio COGS/Inventory 5.27 5.63 5.49

Solvency Ratio

Debt 130314 115672 121996

Equity 90189 90037 81995

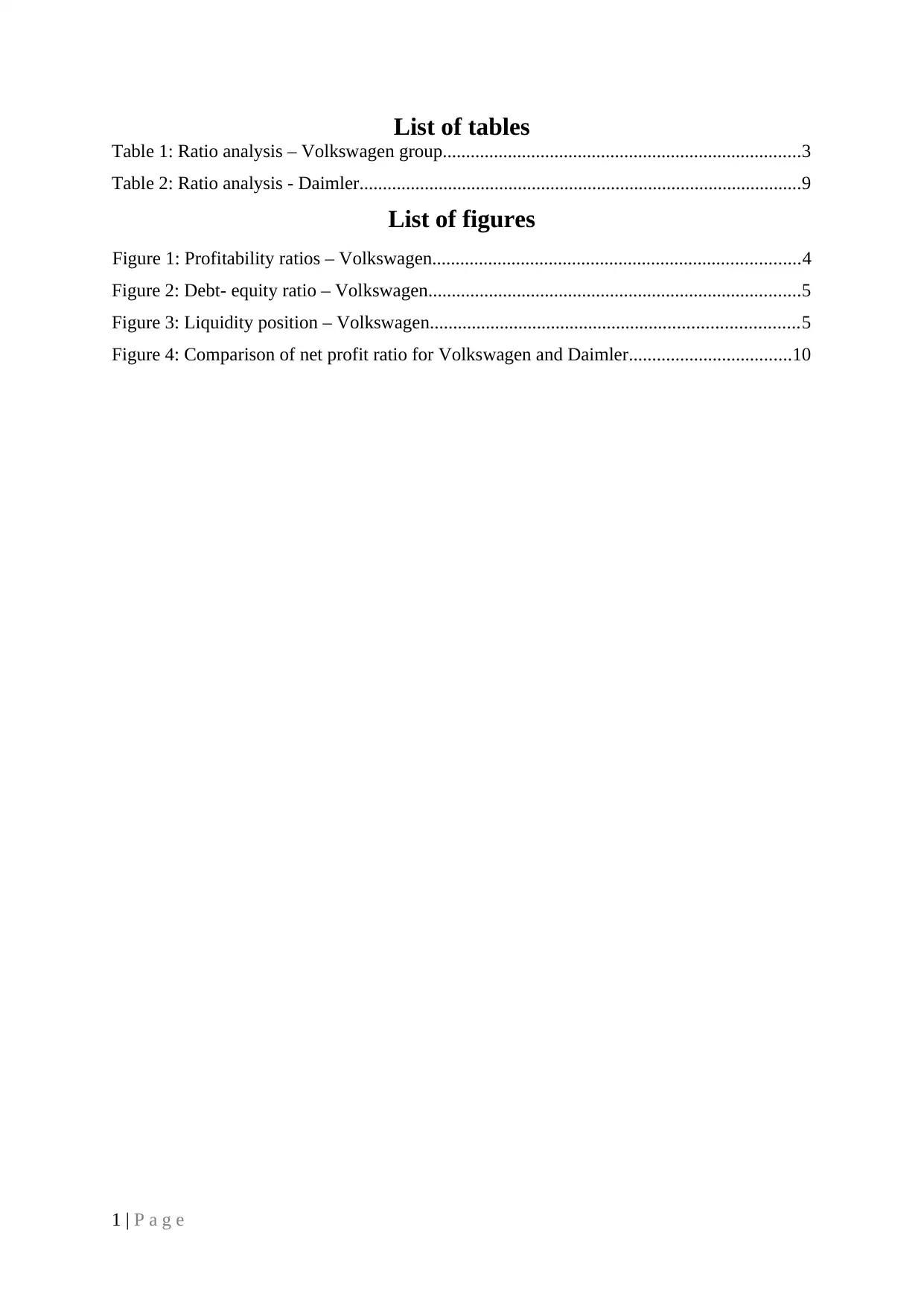

Debt Equity Ratio Debt/ Equity 1.44:1 1.28:1 1.49:1

Net income 11068 9145 21881

Annual Interest Expense 2658 2366 2546

Times Interest Ratio

Net Income/ Interest

expense

4.16

times

3.87

times

8.59

times

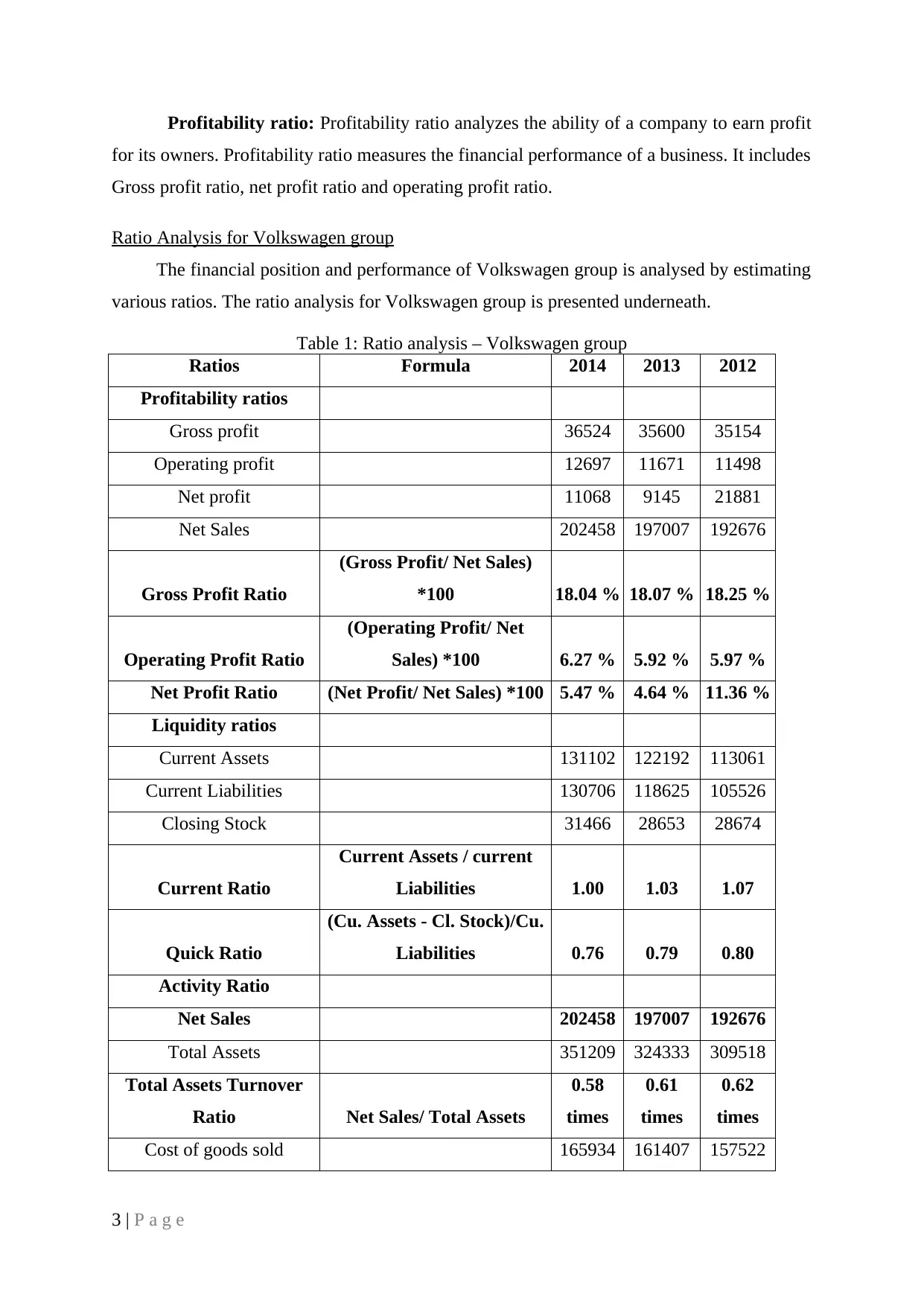

Figure 1: Profitability ratios – Volkswagen

4 | P a g e

Inventory Turnover ratio COGS/Inventory 5.27 5.63 5.49

Solvency Ratio

Debt 130314 115672 121996

Equity 90189 90037 81995

Debt Equity Ratio Debt/ Equity 1.44:1 1.28:1 1.49:1

Net income 11068 9145 21881

Annual Interest Expense 2658 2366 2546

Times Interest Ratio

Net Income/ Interest

expense

4.16

times

3.87

times

8.59

times

Figure 1: Profitability ratios – Volkswagen

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

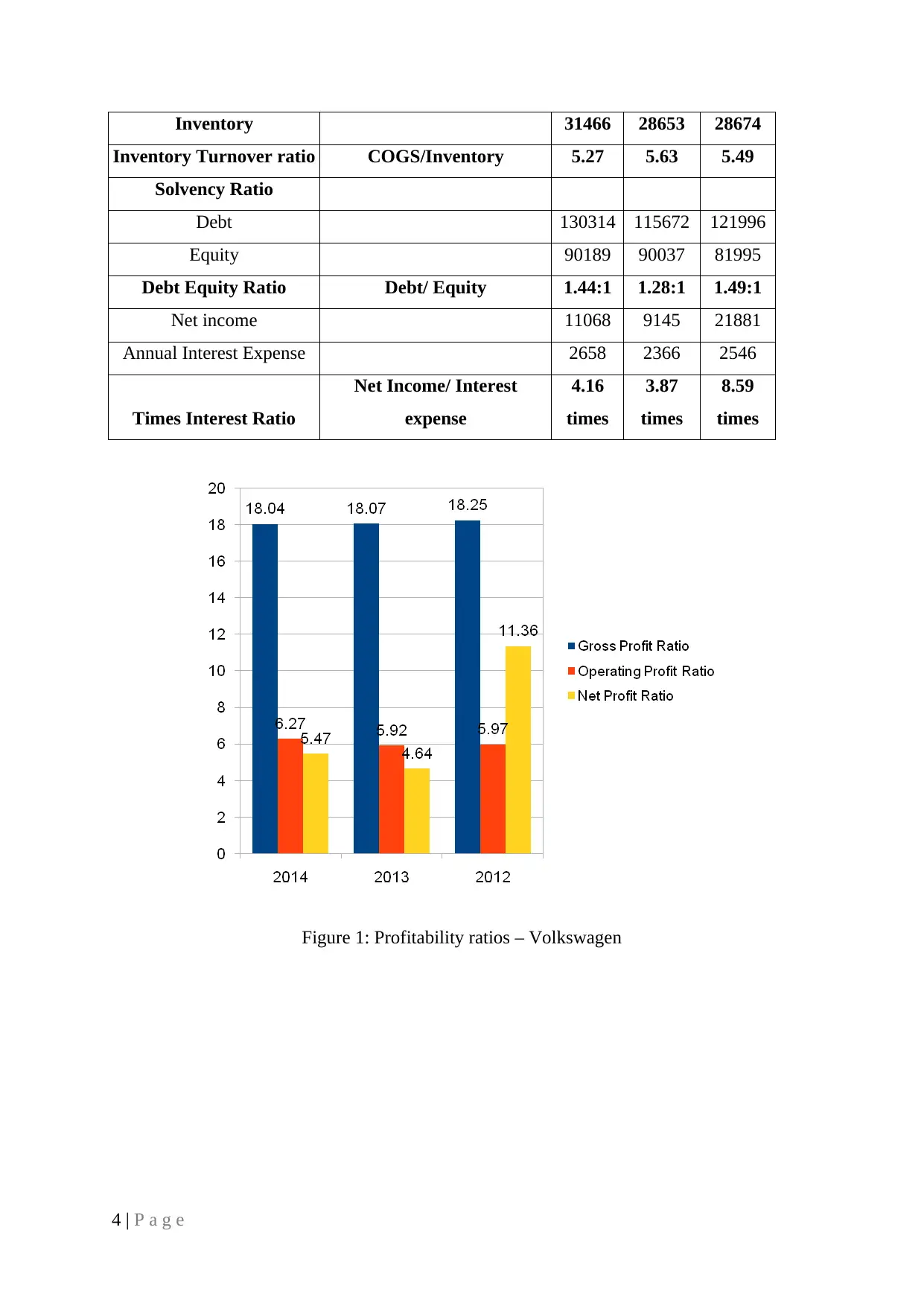

Figure 2: Debt- equity ratio – Volkswagen

5 | P a g e

5 | P a g e

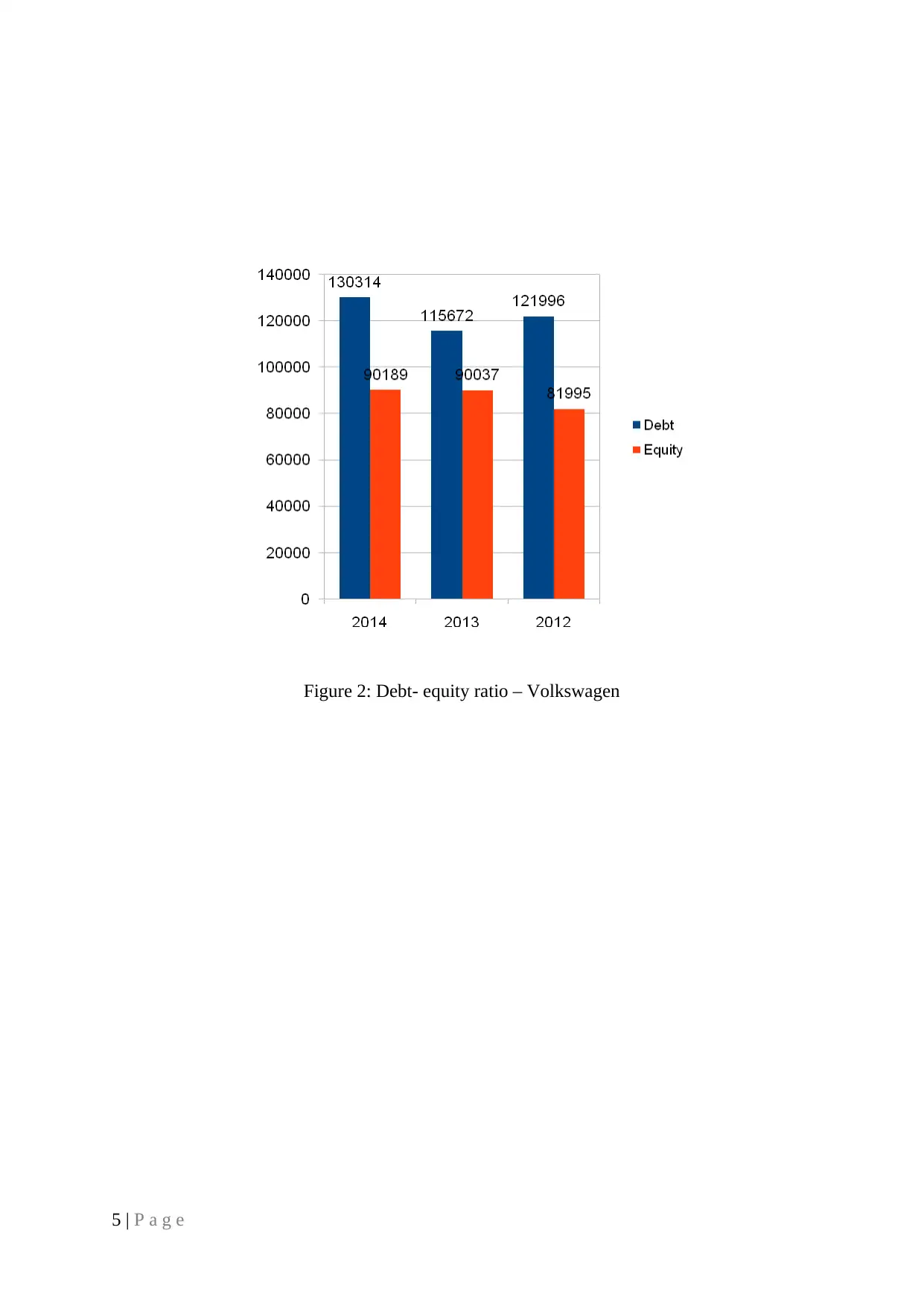

Figure 3: Liquidity position – Volkswagen

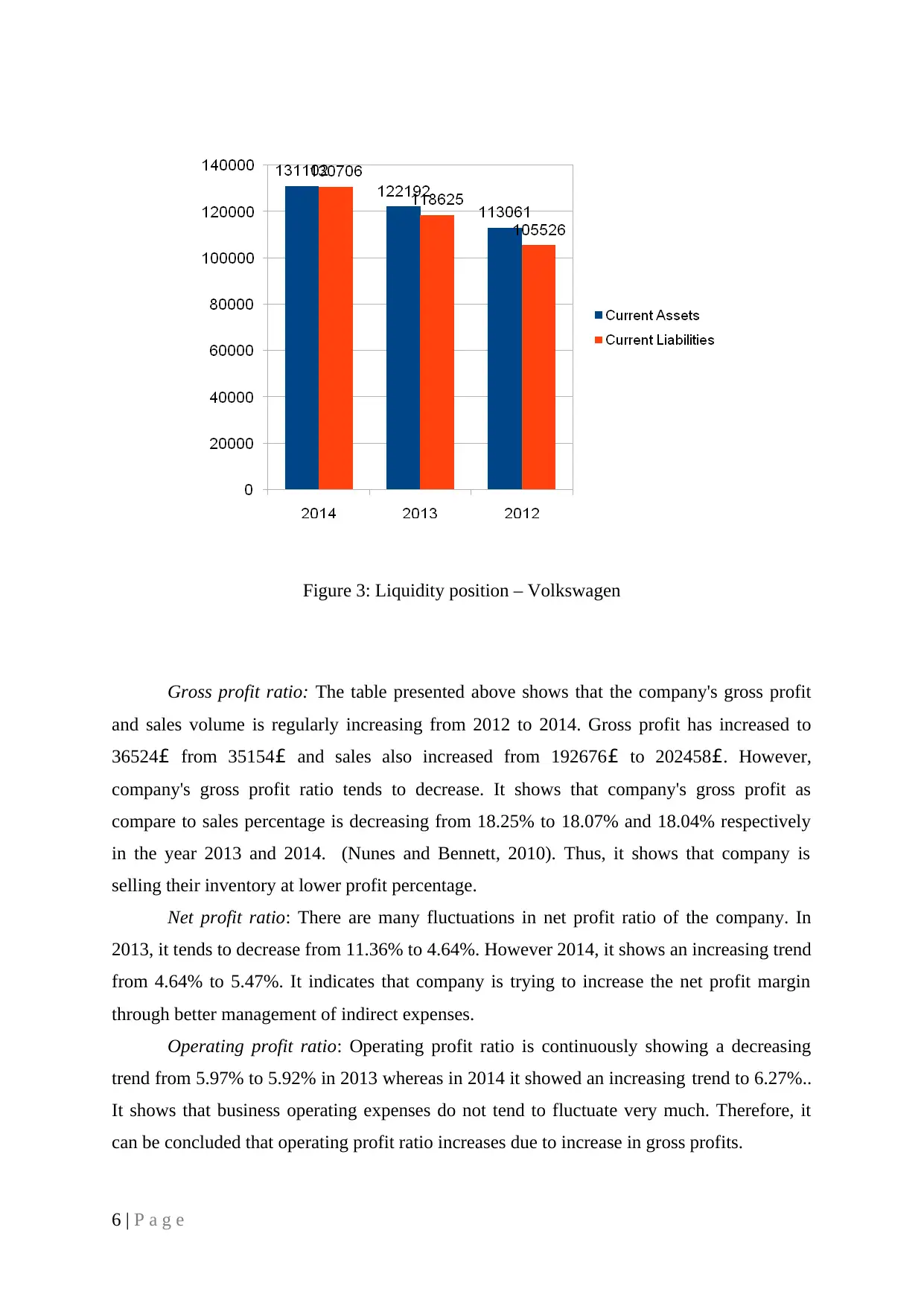

Gross profit ratio: The table presented above shows that the company's gross profit

and sales volume is regularly increasing from 2012 to 2014. Gross profit has increased to

36524£ from 35154£ and sales also increased from 192676£ to 202458£. However,

company's gross profit ratio tends to decrease. It shows that company's gross profit as

compare to sales percentage is decreasing from 18.25% to 18.07% and 18.04% respectively

in the year 2013 and 2014. (Nunes and Bennett, 2010). Thus, it shows that company is

selling their inventory at lower profit percentage.

Net profit ratio: There are many fluctuations in net profit ratio of the company. In

2013, it tends to decrease from 11.36% to 4.64%. However 2014, it shows an increasing trend

from 4.64% to 5.47%. It indicates that company is trying to increase the net profit margin

through better management of indirect expenses.

Operating profit ratio: Operating profit ratio is continuously showing a decreasing

trend from 5.97% to 5.92% in 2013 whereas in 2014 it showed an increasing trend to 6.27%..

It shows that business operating expenses do not tend to fluctuate very much. Therefore, it

can be concluded that operating profit ratio increases due to increase in gross profits.

6 | P a g e

Gross profit ratio: The table presented above shows that the company's gross profit

and sales volume is regularly increasing from 2012 to 2014. Gross profit has increased to

36524£ from 35154£ and sales also increased from 192676£ to 202458£. However,

company's gross profit ratio tends to decrease. It shows that company's gross profit as

compare to sales percentage is decreasing from 18.25% to 18.07% and 18.04% respectively

in the year 2013 and 2014. (Nunes and Bennett, 2010). Thus, it shows that company is

selling their inventory at lower profit percentage.

Net profit ratio: There are many fluctuations in net profit ratio of the company. In

2013, it tends to decrease from 11.36% to 4.64%. However 2014, it shows an increasing trend

from 4.64% to 5.47%. It indicates that company is trying to increase the net profit margin

through better management of indirect expenses.

Operating profit ratio: Operating profit ratio is continuously showing a decreasing

trend from 5.97% to 5.92% in 2013 whereas in 2014 it showed an increasing trend to 6.27%..

It shows that business operating expenses do not tend to fluctuate very much. Therefore, it

can be concluded that operating profit ratio increases due to increase in gross profits.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current ratio: Company's current ratio states the decreasing trend because the

proportional changes in current assets as compare to proportional changes in current

liabilities has decreased. In 2012, current ratio was 1.07 which decreases to 1.03 and 1.00

respectively in the year 2013 and 2014.

Quick ratio: This ratio is decreasing because of increase in company's inventory and

changes in current assets and liabilities. In 2012, the ratio was 0.80 which was decreased to

0.79 and 0.76 respectively. It shows that, proportion of liquid assets available to meet short

term liabilities are decreasing continuously.

Total Assets turnover ratio: This ratio measures that how efficiently the company is

using their assets to generate cash (Estridge and Lougee, 2007). In context to Volkswagen

group, it was 0.62 in 2012 which was decreased to 0.61 and 0.58 in 2013 and 2014

respectively. Decreasing trend indicates that company is not using its assets efficiently due to

management or production difficulties.

Inventory turnover ratio: This is an efficiency ratio which shows that how efficiently

inventory is managed by the company. In case of Volkswagen group, the company's

inventory turnover ratio increased in 2013 to 5.63 from 5.49. However in 2014, it decreased

to 5.27 from 5.63. This implies that the company is not using its inventory efficiently as

compare to 2013.

Debt equity ratio: It decreased in 2013 from 1.49 to 1.28 because of increase in equity

and decrease in debt. It shows more stable financial business. However in 2014, it increased

to 1.44 because debt is increasing and equity remained constant. It implies that company is

generating its sources through debt financing. It is considered more risky to creditors

regarding their interest payment and repayment of principal amount.

Time interest earned ratio: This ratio measures the company's ability to support its

additional debts. It decreased in 2013 because net income decreased in the company.

However in 2014, it shows an increasing trend because the company's net income increased

in this year. It shows that company's ability regarding interest payment is rising but compare

to 2012, it is very low. Therefore, the business should increase the amount of profit to

increase such ratio.

Therefore, it is concluded that profitability ratio for Volkswagen group is decreasing

which is not a good sign for the company so it has to increase its sales by contributing their

efforts. In addition to this, activity ratio also tends to decrease which is the indication of low

availability of liquid assets so the company has to ensure efficient use of inventory.

7 | P a g e

proportional changes in current assets as compare to proportional changes in current

liabilities has decreased. In 2012, current ratio was 1.07 which decreases to 1.03 and 1.00

respectively in the year 2013 and 2014.

Quick ratio: This ratio is decreasing because of increase in company's inventory and

changes in current assets and liabilities. In 2012, the ratio was 0.80 which was decreased to

0.79 and 0.76 respectively. It shows that, proportion of liquid assets available to meet short

term liabilities are decreasing continuously.

Total Assets turnover ratio: This ratio measures that how efficiently the company is

using their assets to generate cash (Estridge and Lougee, 2007). In context to Volkswagen

group, it was 0.62 in 2012 which was decreased to 0.61 and 0.58 in 2013 and 2014

respectively. Decreasing trend indicates that company is not using its assets efficiently due to

management or production difficulties.

Inventory turnover ratio: This is an efficiency ratio which shows that how efficiently

inventory is managed by the company. In case of Volkswagen group, the company's

inventory turnover ratio increased in 2013 to 5.63 from 5.49. However in 2014, it decreased

to 5.27 from 5.63. This implies that the company is not using its inventory efficiently as

compare to 2013.

Debt equity ratio: It decreased in 2013 from 1.49 to 1.28 because of increase in equity

and decrease in debt. It shows more stable financial business. However in 2014, it increased

to 1.44 because debt is increasing and equity remained constant. It implies that company is

generating its sources through debt financing. It is considered more risky to creditors

regarding their interest payment and repayment of principal amount.

Time interest earned ratio: This ratio measures the company's ability to support its

additional debts. It decreased in 2013 because net income decreased in the company.

However in 2014, it shows an increasing trend because the company's net income increased

in this year. It shows that company's ability regarding interest payment is rising but compare

to 2012, it is very low. Therefore, the business should increase the amount of profit to

increase such ratio.

Therefore, it is concluded that profitability ratio for Volkswagen group is decreasing

which is not a good sign for the company so it has to increase its sales by contributing their

efforts. In addition to this, activity ratio also tends to decrease which is the indication of low

availability of liquid assets so the company has to ensure efficient use of inventory.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Pozanski, Sadownik and Gannitsos, 2013). On contrary, the capital structure indicates the

high debt financing and low equity financing. Hence, the company has to increase its

solvency ratio and ensure adequate availability of funds for its payables. Otherwise, it will be

a burden for the company which in turn will affect the business profitability and its market

position adversely.

Impact of internal and external factors on the business

Environmental factors refer to variables and the conditions which affect the working

and performance of the company. These factors can be segregated as internal and external

factors. Internal factors are available within an organization hence; it can be controlled by the

company. It includes management change, employee morale, cultural change and financial

issues. However, external environment prevailing outside the organization and firms have no

control over such environment (Palepu and Healy, 2007). It includes political, economical,

social, technological, ecological and legal environment. PESTEL Analysis can be used to

analyse environmental factors of the Volkswagen Group.

Political factors: Volkswagen conducts its operations in distinct parts of the world.

Political situation of all countries are different and hence the firm faces many political

difficulties in its developments. Automotive industry is closely related to policies which are

made by the government (Franco and et. al., 2011). On the other hand, banking industry and

financial sector of a country plays a key role as they provide vehicle loans and interest rates

on these loans. Therefore it is the biggest challenge in front of Volkswagen to understand

different political pressure and make strategies according to the situation.

Economic Environment; Automotive industry is a key industry in development of any

country as it contributes in national income of the nation (Ross, Westerfield and Jordan,

2008). Volkswagen contributes in GDP of countries and also in the development of other

industries such as steel and glass industry. The company is highly affected by economic

conditions of the country. European debt crisis is major for the car manufacturing companies.

Countries having high fuel prices also affect the industry in order to deal with this difficulty

Volkswagen is focusing on alternatives of petrol and diesel.

Social factors: Society for Volkswagen is very large and it is different from place to

place. Volkswagen gives employment to people as it operates in many countries of the world.

The company enhances level of society and provide goods according to the customer's

preferences (Tiwari, Turner and Younis, 2014).

8 | P a g e

high debt financing and low equity financing. Hence, the company has to increase its

solvency ratio and ensure adequate availability of funds for its payables. Otherwise, it will be

a burden for the company which in turn will affect the business profitability and its market

position adversely.

Impact of internal and external factors on the business

Environmental factors refer to variables and the conditions which affect the working

and performance of the company. These factors can be segregated as internal and external

factors. Internal factors are available within an organization hence; it can be controlled by the

company. It includes management change, employee morale, cultural change and financial

issues. However, external environment prevailing outside the organization and firms have no

control over such environment (Palepu and Healy, 2007). It includes political, economical,

social, technological, ecological and legal environment. PESTEL Analysis can be used to

analyse environmental factors of the Volkswagen Group.

Political factors: Volkswagen conducts its operations in distinct parts of the world.

Political situation of all countries are different and hence the firm faces many political

difficulties in its developments. Automotive industry is closely related to policies which are

made by the government (Franco and et. al., 2011). On the other hand, banking industry and

financial sector of a country plays a key role as they provide vehicle loans and interest rates

on these loans. Therefore it is the biggest challenge in front of Volkswagen to understand

different political pressure and make strategies according to the situation.

Economic Environment; Automotive industry is a key industry in development of any

country as it contributes in national income of the nation (Ross, Westerfield and Jordan,

2008). Volkswagen contributes in GDP of countries and also in the development of other

industries such as steel and glass industry. The company is highly affected by economic

conditions of the country. European debt crisis is major for the car manufacturing companies.

Countries having high fuel prices also affect the industry in order to deal with this difficulty

Volkswagen is focusing on alternatives of petrol and diesel.

Social factors: Society for Volkswagen is very large and it is different from place to

place. Volkswagen gives employment to people as it operates in many countries of the world.

The company enhances level of society and provide goods according to the customer's

preferences (Tiwari, Turner and Younis, 2014).

8 | P a g e

Technological Factors: Volkswagen operates in both segments classical as well as

sporty. Brands such as Audi, Bentley and Skoda are highly technology upgraded well

maintained cars (Robinson and et. al., 2015). Technology helps in the production of the cars

which in turn helps in increasing sales and profitability.

Environmental factors: The car manufacturing company has vital impact on the

environment of nation. A car uses diesel and petrol as fuel which pollutes the environment.

Moreover, the raw material used, steel made from iron and smoke also pollutes the

environment. Therefore, the company needs to take care of natural environment.

Legal Factors: Automotive industry needs to follow rules and regulations as per the

legal requirement of nation (Wahlen, Baginski and Bradshaw, 2014). It is a big challenge for

Volkswagen as it is operating in many countries of the world with different legal

requirements. Therefore, the company needs to follow consumer protection law, labour law,

competition law, emission law and taxation law.

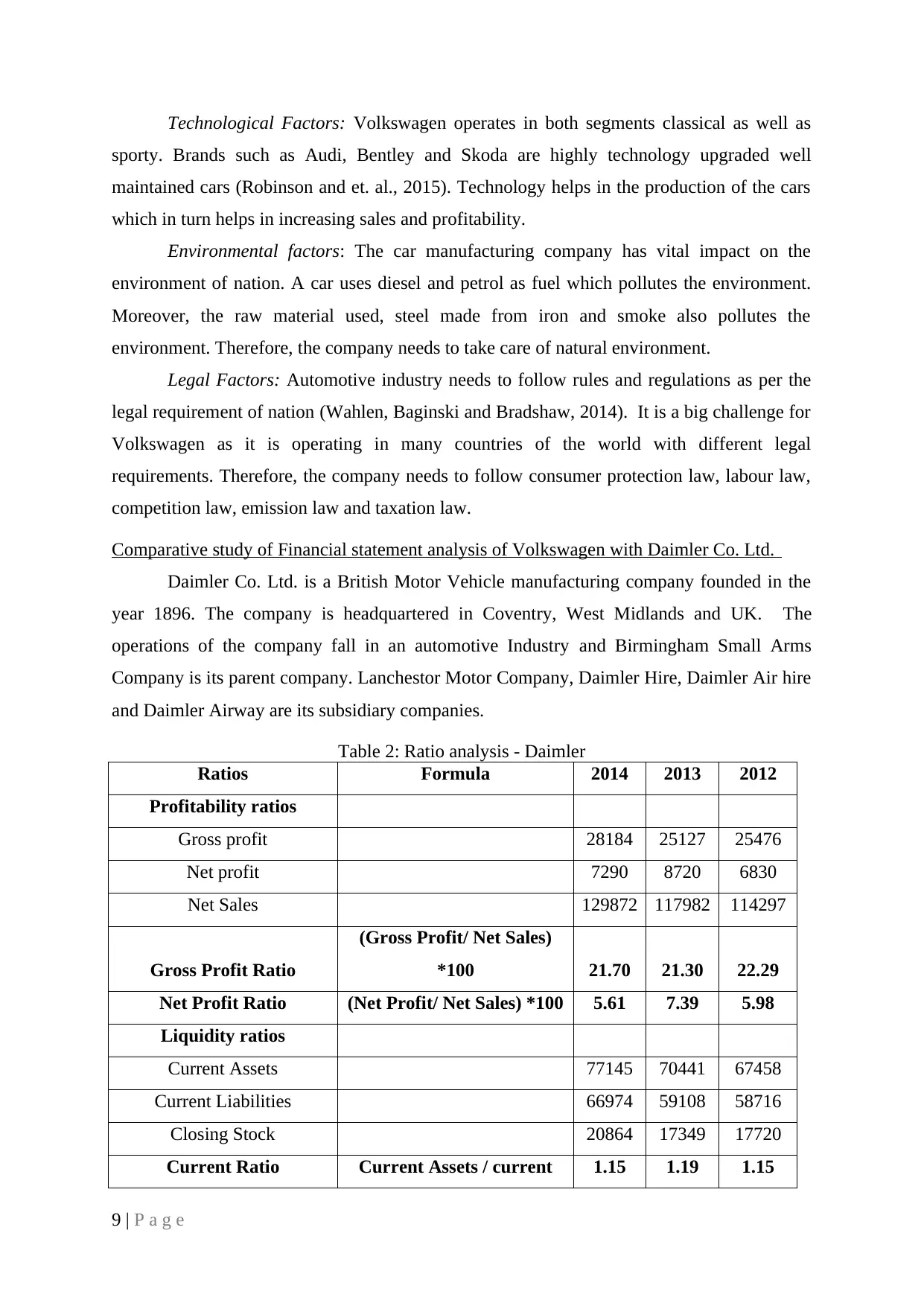

Comparative study of Financial statement analysis of Volkswagen with Daimler Co. Ltd.

Daimler Co. Ltd. is a British Motor Vehicle manufacturing company founded in the

year 1896. The company is headquartered in Coventry, West Midlands and UK. The

operations of the company fall in an automotive Industry and Birmingham Small Arms

Company is its parent company. Lanchestor Motor Company, Daimler Hire, Daimler Air hire

and Daimler Airway are its subsidiary companies.

Table 2: Ratio analysis - Daimler

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 28184 25127 25476

Net profit 7290 8720 6830

Net Sales 129872 117982 114297

Gross Profit Ratio

(Gross Profit/ Net Sales)

*100 21.70 21.30 22.29

Net Profit Ratio (Net Profit/ Net Sales) *100 5.61 7.39 5.98

Liquidity ratios

Current Assets 77145 70441 67458

Current Liabilities 66974 59108 58716

Closing Stock 20864 17349 17720

Current Ratio Current Assets / current 1.15 1.19 1.15

9 | P a g e

sporty. Brands such as Audi, Bentley and Skoda are highly technology upgraded well

maintained cars (Robinson and et. al., 2015). Technology helps in the production of the cars

which in turn helps in increasing sales and profitability.

Environmental factors: The car manufacturing company has vital impact on the

environment of nation. A car uses diesel and petrol as fuel which pollutes the environment.

Moreover, the raw material used, steel made from iron and smoke also pollutes the

environment. Therefore, the company needs to take care of natural environment.

Legal Factors: Automotive industry needs to follow rules and regulations as per the

legal requirement of nation (Wahlen, Baginski and Bradshaw, 2014). It is a big challenge for

Volkswagen as it is operating in many countries of the world with different legal

requirements. Therefore, the company needs to follow consumer protection law, labour law,

competition law, emission law and taxation law.

Comparative study of Financial statement analysis of Volkswagen with Daimler Co. Ltd.

Daimler Co. Ltd. is a British Motor Vehicle manufacturing company founded in the

year 1896. The company is headquartered in Coventry, West Midlands and UK. The

operations of the company fall in an automotive Industry and Birmingham Small Arms

Company is its parent company. Lanchestor Motor Company, Daimler Hire, Daimler Air hire

and Daimler Airway are its subsidiary companies.

Table 2: Ratio analysis - Daimler

Ratios Formula 2014 2013 2012

Profitability ratios

Gross profit 28184 25127 25476

Net profit 7290 8720 6830

Net Sales 129872 117982 114297

Gross Profit Ratio

(Gross Profit/ Net Sales)

*100 21.70 21.30 22.29

Net Profit Ratio (Net Profit/ Net Sales) *100 5.61 7.39 5.98

Liquidity ratios

Current Assets 77145 70441 67458

Current Liabilities 66974 59108 58716

Closing Stock 20864 17349 17720

Current Ratio Current Assets / current 1.15 1.19 1.15

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.